UnitedHealth executives made a valiant attempt yesterday to persuade investors that they have figured out how to improve customer service and keep Congress and the incoming Trump administration from passing laws that could shrink the company’s profit margins – and maybe even the company itself – but Wall Street wasn’t buying.

During their first call with investors since the murder of UnitedHealthcare CEO Brian Thompson, the company’s top brass pointed the finger of blame for rising health care costs everywhere but at themselves – primarily at hospitals and pharmaceutical companies – and made statements that simply were not true. Investors clearly did not find their comments reassuring or credible. By the end of the day shares of UnitedHealth’s stock were down more than 6% to $510.59. That marked a continuation of a slide that began after the stock price peaked at $630.73 on November 11 – a decline of almost 20%.

In a little more than two months, the company has lost an astonishing $110 billion in market capitalization, and shareholders have lost an enormous amount of the money they invested in UnitedHealth.

Earlier yesterday morning, the company released fourth-quarter and full-year 2024 earnings, which were slightly higher on a per share basis than Wall Street financial analysts had expected: $6.81 per share in the fourth quarter compared to analysts’ consensus estimate of $6.73 for the quarter. But the company posted lower revenue during the last three months of 2024 than analysts had expected. While revenue was up 7% over the same quarter in 2023, to $100.8 billion, analysts had expected revenue to grow to $101.6 billion.

And on a full-year basis, the company’s net profits fell an eye-popping 36%, from $22.4 billion in 2023 to $14.4 billion last year.

Bottom line: the company, which until last year had grown rapidly, actually shrank in some respects, especially in the division that operates the company’s health plans. UnitedHealthcare, which Thompson led, saw its revenue increase slightly but its profits fall. The other big division, Optum, which among other things owns and operates numerous physician practices and clinics and one of the country’s largest pharmacy benefit managers (PBMs), fared much better.

While Optum’s 2024 revenue was lower than UnitedHealthcare’s ($253 billion and $298 respectively), it made far more in profits on an operating basis ($16.7 billion and $15.6 respectively).

Optum’s operating profit margin was 6.6% while UnitedHealthcare’s was 5.2%.

The company’s executives blamed higher health care utilization, especially by people enrolled in its Medicare Advantage plans, for the decline in profits.

Witty and CFO John Rex pointed the finger of blame at hospitals and drug companies for rising medical prices. And they obscured the huge amounts of money the company’s PBM, Optum Rx, extracts from the pharmacy supply chain. While the company chose not to break out exactly how much of Optum’s revenues of $298 billion came from Optum Rx, it appears that more than half of it was contributed by the PBM. The company did note that Optum Rx revenues increased 15% during 2024.

Nevertheless, Witty and Rex blamed drug makers for high prices.

They also said that they would be changing the PBM’s business practices to pass through rebate discounts from drug makers to its customers, claiming that it already passes through 98% of them and will reach 100% by 2028. That clearly was a talking point aimed at Washington, where there is significant bipartisan support for legislation that would require all PBMs to do so. Despite UnitedHealth’s claim, there is no external verification to back up that they are passing 98% of rebates back to customers.

Another claim the executives made that is not true is that the Medicare Advantage program saves taxpayers money. Numerous government reports have shown the opposite, that the federal government spends considerably more on people enrolled in Medicare Advantage plans than those enrolled in the traditional Medicare program.

Reports have estimated that UnitedHealthcare, which is the largest Medicare Advantage company, and other MA plans are overpaid between $80 billion and $140 billion a year.

There is also growing bipartisan support to reform the Medicare Advantage program to reduce both the overpayments and the excessive denials of care at UnitedHealthcare and other MA insurers.

While company executives might be hoping that their fortunes will improve during the second Trump administration, Trump recently joined some Republican members of Congress, like Rep. Buddy Carter of Georgia, who are calling for significant reforms, especially to pharmacy benefit managers.

At a news conference last month, Trump promised to “knock out” those middlemen in the pharmacy supply chain.

“We are paying far too much, because we are paying far more than other countries,” he said. “We have laws that make it impossible to reduce [drug costs] and we have a thing called a ‘middleman’ … that makes more money than the drug companies, and they don’t do anything except they’re middlemen. We are going to knock out the middleman.”

An investigative piece in the Wall Street Journal, written by Mark Maremont, Danny Dougherty, and Anna Wilde Mathews, gives an eye-popping look at how UnitedHealth Group is turning diagnosis-driven billing into a high-stakes game in the conglomerate’s Medicare Advantage business.

As The Journal reported, UnitedHealth has taken a unique approach to Medicare Advantage:

directly employing thousands of doctors and arming them with software that generates diagnosis checklists before they even see patients. Former UnitedHealth physicians described how these suggested diagnoses — often obscure or irrelevant — weren’t optional. To move on to their next patient, doctors were forced to confirm, deny, or defer each proposed diagnosis.

One Oregon physician, Dr. Nicholas Jones, said UnitedHealth frequently pushed conditions so rare – like secondary hyperaldosteronism – he had to Google them. And this wasn’t limited to minor conditions.

Sickness scores for UnitedHealth’s Medicare Advantage patients jumped an average of 55% in their first year of enrollment in one of the company’s health plans compared to a mere 7% rise for patients who stayed in traditional Medicare. As the Journal noted, that’s the kind of jump you’d expect if everyone suddenly developed HIV and breast cancer.

The implications? More diagnoses mean higher “sickness scores,” which translate to billions in extra payments from Medicare. The Journal found that UnitedHealth’s practices generated an additional $4.6 billion from 2019 to 2022 compared to what it would have received if those scores had matched industry averages.

Citing fewer hospitalizations, UnitedHealth insists these practices improve patient outcomes and disease management, but the incentives to inflate diagnoses raise serious questions.

In the piece, you’ll meet Chris Henretta, a UnitedHealth Medicare Advantage “member” who lives in Florida. His doctor diagnosed him as morbidly obese, even though he’s a lifelong weightlifter and doesn’t meet the BMI threshold. “I began to suspect my doctor may have a financial incentive to portray people as higher risk,” Henretta said. The article pointed out that such a diagnosis can trigger an extra $2,400 in Medicare payments annually.

UnitedHealth’s system isn’t just about inflating diagnoses — it’s about turning them into profit centers.

The Journal reported that internal documents revealed that doctors could earn bonuses of up to $30,000 annually for engaging with the diagnosis system. Nurses tasked with “finding” new diagnoses were paid $250 per patient visit.

UnitedHealth has countered by saying these practices reflect its commitment to diagnosing and treating diseases early. But the Journal said many doctors felt pressure to play along.

Dr. Emilie Scott, a former UnitedHealth physician, called the system a money machine: “It’s not about taking care of the patient. It’s about how you get the money to flow.”

For patients and taxpayers, this system poses tough questions. Traditional Medicare patients treated by UnitedHealth doctors didn’t see the same inflation in sickness scores, which underscores how Medicare Advantage’s payment system incentivizes diagnose gaming.

What’s clear is that Medicare Advantage — and UnitedHealth’s dominant role in it — needs much closer scrutiny.

As The Journal reporters wrote, the Centers for Medicare and Medicaid Services is studying these relationships. But real change will require policymakers and the public to confront the deeper flaws in how Medicare Advantage is structured.

Be sure to dive into the original Wall Street Journal article for the full story. The fantastic graphs and photography alone are worth your time, and the detailed reporting provides invaluable insights into how one company’s profit strategies impact us all.

You have three days left, if you got suckered in by those omnipresent ads for Medicare Advantage and left regular Medicare for the siren song of cheaper coverage, “free” vision, hearing, or dental, or even “free” money to buy groceries or rides to the doc.

The open enrollment period for real Medicare closes at the end of the day Saturday, December 7th; after that, you’re locked into the Medicare Advantage plan you may have bought until next year.

If you’ve had Medicare Advantage for a year or more, however, the open enrollment period is still “open” until December 7th, but you will want to make sure you can get a “Medigap” plan that fills in the 20% that real Medicare doesn’t cover.

Companies are required to write a Medigap policy for you at a reasonable price when you turn 65, no matter how sick you are or what preexisting conditions you may have, but if you’ve been “off Medicare” by being on Medicare Advantage for more than a year, they don’t have to write you a policy, so double-check that and sign up for a Medigap policy before making the switch back to real Medicare.

So, what’s this all about and why is it so complicated?

When George W. Bush and congressional Republicans (and a handful of bought-off Democrats) created Medicare Advantage in 2003, it was the fulfillment of half of Bush’s goal of privatizing Social Security and Medicare, dating all the way back to his unsuccessful run for Congress in 1978 and a main theme of his second term in office.

Medicare Advantage is not Medicare.

These plans are private health insurance provided by private corporations, who are then reimbursed at a fixed rate by the Medicare trust fund regardless of how much their customers use their insurance. Thus, the more they can screw their customers and us taxpayers by withholding healthcare payments, the more money they make.

With real Medicare,

if your doctor says you need a test, procedure, scan, or any other medical intervention you simply get it done and real Medicare pays the bill. No muss, no fuss, no permission needed. Real Medicare always pays, and if they think something’s not kosher, they follow up after the payment’s been made so as not to slow down the delivery of your healthcare.

With Medicare Advantage,

however, you’re subject to “pre-clearance,” meaning that the insurance company inserts itself between you and your doctor: You can’t get the medical help you need until or unless the insurance company pre-clears you for payment.

These companies thus make much of their billions in profit by routinely denying claims — 1.5 million, or 18 percent of all claims, were turned down in one year alone — leaving Advantage policy holders with the horrible choice of not getting the tests or procedures they need or paying for them out-of-pocket.

Given this, you’d think that most people would stay as far away from these private Medicare Advantage plans as they could. But Congress also authorized these plans to compete unfairly with real Medicare by offering things real Medicare can’t (yet). These include free or discounted dental, hearing, eyeglasses, gym memberships, groceries, rides to the doctor, and even cash rebates.

You and I pay for those freebies, but that’s only half of the horror story.

This year, as Matthew Cunningham-Cook pointed out in Wendell Potter’s brilliant Health Care un-covered Substack newsletter, we’re ponying up an additional $64 billion to give to these private insurance companies to “reimburse” them for the freebies they relentlessly advertise on television, online, and in print.

And here’s the most obscene part of the whole thing: the companies won’t tell the government (us!) how much of that $64 billion they’ve actually spent. They just take the money and say, “Thank you very much.” And then, presumably, throw a few extra million into the pockets of each of their already obscenely-well-paid senior executives.

For example, the former CEO of the nation’s largest Medicare Advantage provider, UnitedHealth, walked away with over a billion dollars in total compensation. With a “B.” One guy. His successor made off with over a half-billion dollars in pay and stock.

Good work if you can get it: all you need do is buy off a hundred or so members of Congress, courtesy of Clarence Thomas’ billionaire-funded tie-breaking vote on Citizens United, and threaten the rest of Congress with massive advertising campaigns for their opponents if they try to stop you.

And while the companies refuse to tell us how much of the $64 billion that we’re throwing at them this year to offer “free” dental, etc. is actually used, what we do know is that most of that money is not going to pay for the freebies they advertise. As Cunningham-Cook noted, in one study only 11 percent of Advantage policyholders who’d signed up with plans offering dental care used that benefit.

Another study showed over-the-counter-drug freebies were used only a third of the time, leaving $5 billion in the insurance companies money bins just for that “reimbursable” goodie. A later study found that at least a quarter of all Advantage policyholders failed to use any of the freebies they’d been offered when they signed up.

That’s an enormous amount of what the industry calls “breakage”; benefits offered and paid for by the government but not used. Billions of dollars left over every month. And, used or not, you and I sure paid for them.

And now it looks like things are about to get a whole lot worse.

When he was president last time, Donald Trump substantially expanded Medicare Advantage, calling real Medicare “socialism.” Project 2025 and candidate Trump both promised to end real Medicare “immediately” if Trump was re-elected; at the very least, they’ll make Medicare Advantage the “default” program people are steered into when they turn 65 and sign up for Medicare.

These giant insurance companies ripped off us taxpayers last year to the tune of an estimated $140 billion over and above what it would’ve cost us if people had simply been on real Medicare, according to a report from Physicians for a National Health Program (PNHP).

If there was no Medicare Advantage scam bleeding off all that cash to pay for executives’ private jets, real Medicare could be expanded to cover dental, vision, and hearing and even end the need for Medigap plans.

But for now, the privatization gravy train continues to roll along. The insurance giants use some of that money to buy legislators, and some of it for expensive advertising to dupe seniors into joining their programs. The company (Benefytt) that hired Joe Namath to pitch Medicare Advantage, for example, was recently hit with huge fines by the Federal Trade Commission for deceptive advertising.

“Benefytt pocketed millions selling sham insurance to seniors and other consumers looking for health coverage,” said Samuel Levine, Director of the FTC’s Bureau of Consumer Protection. “The company is being ordered to pay $100 million, and we’re holding its executives accountable for this fraud.”

And what was it that the Federal Trade Commission called “sham insurance”? Medicare Advantage. Nonetheless, the Centers for Medicare Services continues to let Benefytt and Namath market these products: welcome to the power of organized money.

And it’s huge organized money. Medicare Advantage plans are massive cash cows for the companies that run them. As Cigna prepares for a merger, for example, they’re being forced to sell off their Medicare Advantage division: it’s scheduled to go for $3.7 billion. Nobody pays that kind of money unless they expect enormous returns.

And how do they make those billions?

Most Medicare Advantage companies regularly do everything they can to intimidate you into paying yourself out-of-pocket. Often, they simply refuse payment and wait for you to file a complaint against them; for people seriously ill the cumbersome “appeals” process is often more than they can handle so they just write a check, pull out a credit card, or end up deeply in debt in their golden years.

As a result, hospitals and doctor groups across the nation are beginning to refuse to take Medicare Advantage patients. And in rural areas many hospitals are simply going out of business because Medicare advantage providers refuse to pay their bills.

California-based Scripps Health, for example, cares for around 30,000 people on Medicare Advantage and recently notified all of them that Scripps will no longer offer medical services to them unless they pay out-of-pocket or revert back to real Medicare.

They made this decision because over $75 million worth of services and procedures their physicians had recommended to their patients were turned down by Medicare Advantage insurance companies. In many cases, Scripps had already provided the care and is now stuck with the bills that the Advantage companies refuse to pay.

“We are a patient care organization and not a patient denial organization and, in many ways, the model of managed care has always been about denying or delaying care – at least economically. That is why denials, [prior] authorizations and administrative processes have become a very big issue for physicians and hospitals…”

Similarly, the Mayo Clinic has warned its customers in Florida and Arizona that they won’t accept Medicare Advantage any more, either. Increasing numbers of physician groups and hospitals are simply over being ripped off by Advantage insurance companies.

Traditional Medicare has been serving Americans well since 1965: it’s one of the most efficient single-payer systems to fund healthcare that’s ever been devised. But nobody was making a buck off it, so nobody could share those profits with greedy politicians. Enter Medicare Advantage, courtesy of George W. Bush and the GOP.

While several bills have been offered in Congress to do something about this — including Mark Pocan’s and Ro Khanna’s Save Medicare Act that would end these companies’ ability to use the word “Medicare” in their policy names and advertising — the amounts of money sloshing around DC in the healthcare space now are almost unfathomable.

So far this year, according to opensecrets.org, the insurance industry has spent $117,305,895 showering gifts and persuasion on our federal lawmakers to keep their obscene profits flowing.

It’s all one more example of how five corrupt Republicans on the US Supreme Court legalizing political bribery with Citizens Unitedhave screwed average Americans and made a handful of industry executives and investors fabulously rich.

They get away with it because when people choose to sign up for Medicare Advantage at 65 (or convert to these plans in their 60s or early 70s) they’re typically not sick — and thus cost the insurance companies little.

Tragically, the people signing up for these plans have no idea all the hassles, hoops, and troubles they might have to jump through when they do get sick, have an accident, or otherwise need medical assistance.

And since the last three years of life are typically the most expensive years for healthcare, the insurance denials are more likely to happen then — long after the person’s signed up with the Advantage company and it’s too late to go back to real Medicare.

This is why it typically takes a few years for people to figure out how badly they got screwed by not going with regular Medicare but instead putting themselves in the hands of private insurance companies.

“In spite of recommendations from Mr. Pauker’s doctors, his family said, Humana has repeatedly denied authorization for inpatient rehabilitation after hospitalization, saying at times he was too healthy and at times too ill to benefit.”

“Tens of millions of denials are issued each year for both authorization and reimbursements, and audits of the private insurers show evidence of ‘widespread and persistent problems related to inappropriate denials of services and payment,’ the investigators found.”

If you have “real” Medicare with a heavily regulated Medigap policy to cover the 20% Medicare doesn’t, you never have to worry.

Your bills get paid, you can use any doctor or hospital in the country who takes Medicare, and neither Medicare nor your Medigap provider will ever try to collect from you or force you to pay for what you thought was covered.

Neither you or your doctor will ever have to do the “pre-authorization” dance with real Medicare: those terrible experiences dealing with for-profit insurance companies are part of the past.

But if you have Medicare Advantage — which is not Medicare, but private health insurance — you’re on your own.

As the Times laid out:

“About 18 percent of [Advantage] payments were denied despite meeting Medicare coverage rules, an estimated 1.5 million payments for all of 2019. In some cases, plans ignored prior authorizations or other documentation necessary to support the payment. These denials may delay or even prevent a Medicare Advantage beneficiary from getting needed care…”

Buying a Medicare Advantage policy is a leap in the dark, and the federal government is not there to catch you. And it’s all perfectly legal, thanks to Bush’s 2003 law, so your state insurance commissioner usually can’t or won’t help.

Thus, here we are, handing billions of dollars a month to insurance industry executives so they can buy new Swiss chalets, private jets, and luxury yachts. And so they can compete — unfairly — with Medicare itself, driving LBJ’s most proud achievement into debt and crisis.

Enough is enough. Let your members of Congress know it’s beyond time to fix the Court and Medicare, so scams like Medicare Advantage can no longer rip off America’s seniors while making industry executives richer than Midas.

And if you got hooked into switching out of real Medicare and now find yourself in a Medicare Advantage plan, you have three days to back out and return to real Medicare. For more information, you can also contact the nonprofit and real-Medicare-supporting Medicare Rights Center at 800-333-4114.

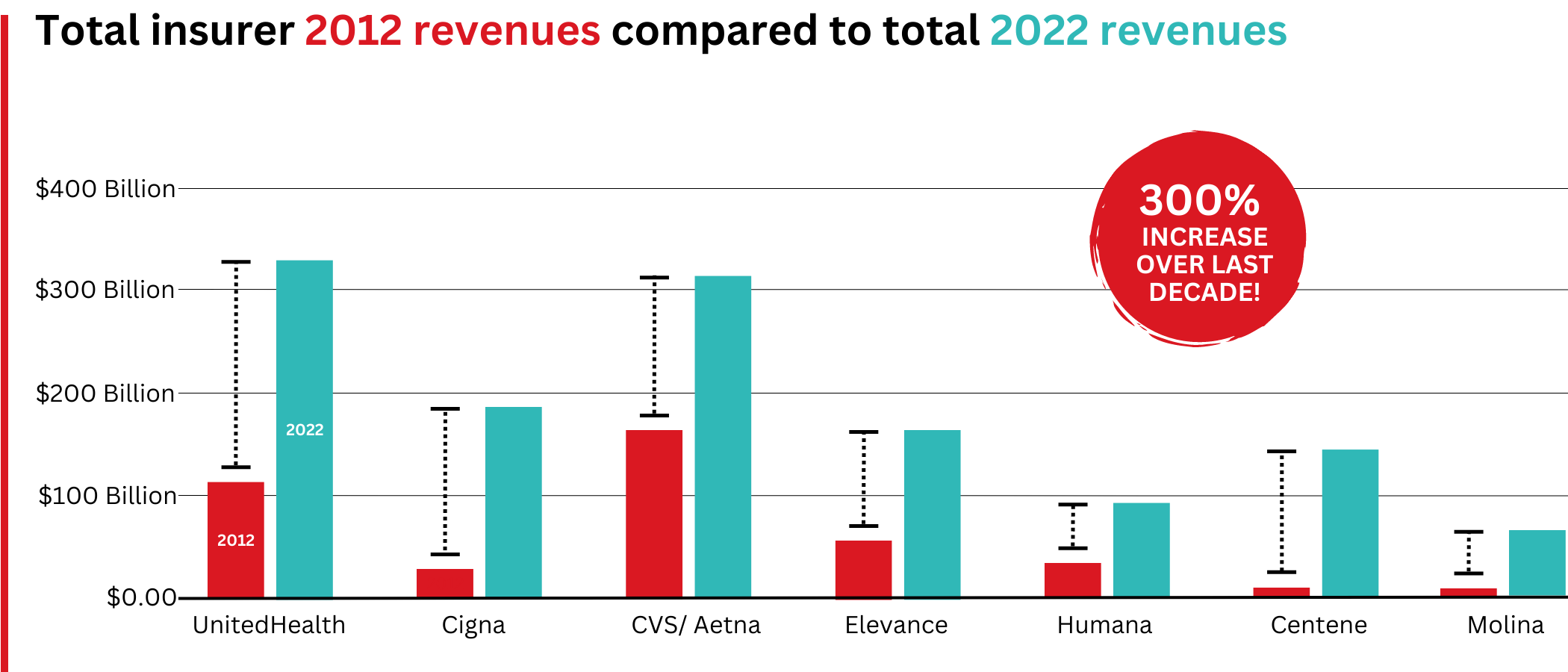

Big Insurance revenues and profits have increased by 300% and 287% respectively since 2012 due to explosive growth in the companies’ pharmacy benefit management (PBM) businesses and the Medicare replacement plans they call Medicare Advantage.

The for-profits now control more than 80% of the national PBM market and more than 70% of the Medicare Advantage market.

In 2022, Big Insurance revenues reached $1.25 trillion and profits soared to $69.3 billion.

That’s a 300% increase in revenue and a 287% increase in profits from 2012, when revenue was $412.9 billion and profits were $24 billion.

Big insurers’ revenues have grown dramatically over the past decade, the result of consolidation in the PBM business and taxpayer-supported Medicare and Medicaid programs.

Sucking billions out of the pharmacy supply chain – and taxpayers’ pockets

What has changed dramatically over the decade is that the big insurers are now getting far more of their revenues from the pharmaceutical supply chain and from taxpayers as they have moved aggressively into government programs. This is especially true of Humana, Centene, and Molina, which now get, respectively, 85%, 88%, and 94% of their health-plan revenues from government programs.

The two biggest drivers are their fast-growing pharmacy benefit managers (PBMs), the relatively new and little-known middleman between patients and pharmaceutical drug manufacturers, and the privately owned and operated Medicare replacement plans they market as Medicare Advantage.

With the exception of Humana, Centene, and Molina, most of the companies that constitute Big Insurance continue to make substantial amounts of money selling policies and services in what they refer to as their commercial businesses – to individuals, families, and employers – but the seven companies’ commercial revenue grew just 260%, or $176 billion, over 10 years (from $110.4 billion to $287.1 billion). While that’s significant, profitable growth in the commercial sector has become a major challenge for big insurers – so much so that Humana just last week announced it is exiting the employer-sponsored health-insurance marketplace entirely.

The percentage of U.S. employers providing some level of health benefits to their workers dropped from 69% to 51% between 1999 and 2022 – including a dramatic 8% decrease last year alone. Growth in this category is largely the result of insurers “stealing market share” from each other or from smaller competitors.

As a consequence of this segment’s relative stagnation, PBMs and government programs have become the new cash cows for Big Insurance.

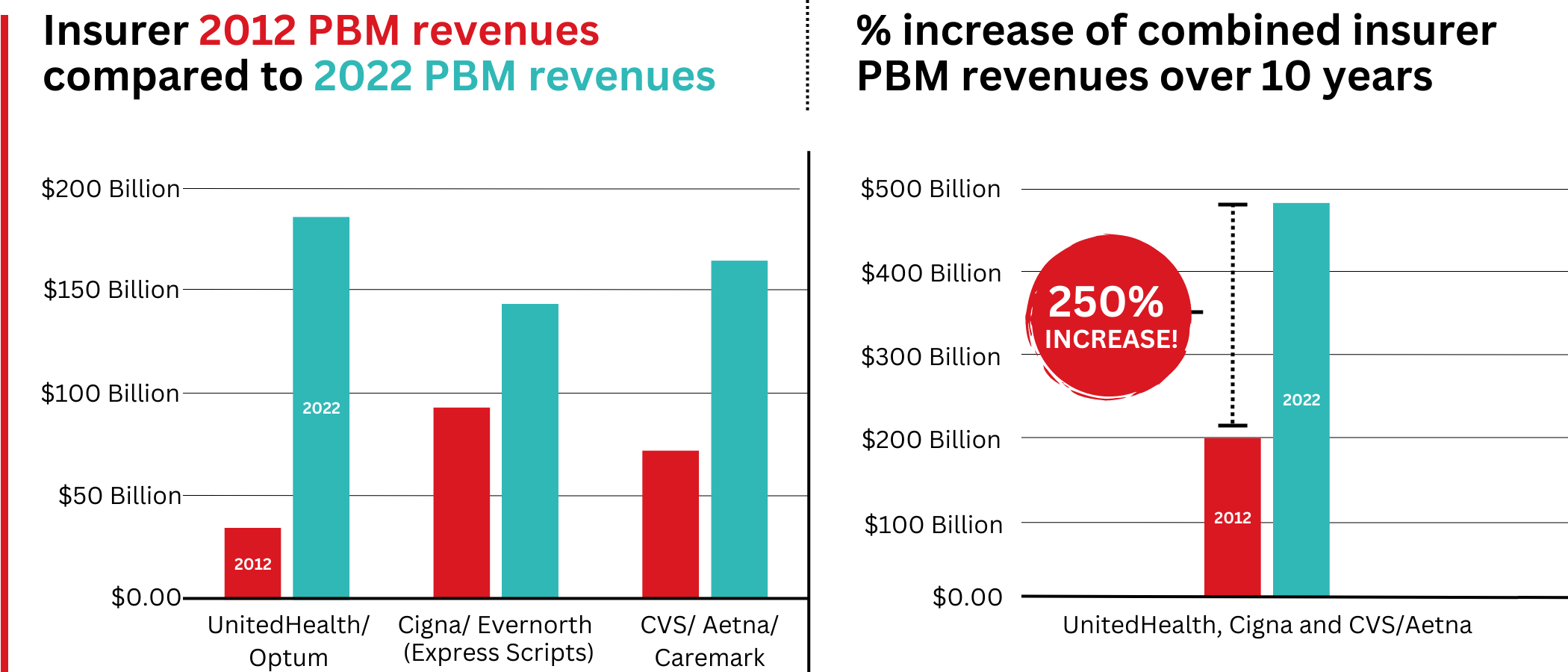

Spectacular PBM Growth

PBM HIGHLIGHTS

Cigna now gets far more revenue from its PBM than from its health plans. CVS gets more revenue from its PBM than from either Aetna’s health plans or its nearly 10,000 retail stores.

UnitedHealth has the biggest share of both the PBM and Medicare markets and, through numerous acquisitions of physician practices, is now the largest U.S. employer of doctors.

PBMs are middlemen companies that manage prescription drug benefits for health insurers, Medicare Part D drug plans, employers, and, in some cases, unions. As the Commonwealth Fund has noted:

PBMs have a significant behind-the-scenes impact in determining total drug costs for insurers, shaping patients’ access to medications, and determining how much pharmacies are paid.

The Commonwealth Fund went on to say that PBMs have faced growing scrutiny about their role in rising prescription drug costs and spending. A big reason for the scrutiny – by Congress, state lawmakers and now also by the FTC – is that the biggest PBMs are now owned by Big Insurance.

Through mergers and acquisitions in recent years, three of the seven for-profit insurers – Cigna, CVS/Aetna, and UnitedHealth – now control 80% of the U.S. pharmacy benefits market.

They determine which drugs will be listed in each of their formularies (lists of drugs they will “cover” based on secret deals they negotiate with pharmaceutical companies) and how much patients will have to pay out of their own pockets at the pharmacy counter – in many cases hundreds or thousands of dollars – before their coverage kicks in. The PBMs also “steer” health-plan enrollees to their preferred or owned pharmacies (and, increasingly, away from independent pharmacists), thereby capturing even more of what we spend on our prescription medications.

Cigna, CVS/Aetna, and UnitedHealth now control 80% of the U.S. PBM market. Correction: this graph was initially published with inaccurate numbers. The source for this information can be found here.

Ten years ago, PBMs contributed relatively little to the three companies’ revenues and profits. But since then, the rapid growth of PBMs has transformed all of the companies. The combined revenues from their PBM business units increased 250% between 2012 and 2022, from $196.7 billion to $492.4 billion.

Changes in PBM revenues between 2012 and 2022 for UnitedHealth Group, Cigna, and CVS/Aetna (Editor’s note: Cigna acquired PBM Express Scripts in 2018. To reflect revenue growth, Express Scripts’ pre-acquisition 2012 revenues are included in the Cigna total for that year.)

PBM Profit Generation

The PBM profit growth at the three companies over the past decade was even more dramatic than revenue growth. Collectively, their PBM profits increased 438%, from $6.3 billion in 2012 to $27.6 billion in 2022.

As a result of this fast growth, more than half (52%) of three companies’ profits in 2022 came from their PBM business units: Cigna’s Evernorth, CVS/Aetna’s Caremark, and UnitedHealth’s Optum. Cigna now gets far more revenue and profits from its PBM than from its health plans. And CVS gets more revenue from its PBM than from either Aetna’s health plans or its nearly 10,000 retail stores. (The companies’ business units that include their PBMs have also moved aggressively in recent years into health-care delivery through acquisitions of physician practices, clinics, dialysis centers, and other facilities. Notably, UnitedHealth Group is now the largest U.S. employer of physicians.)

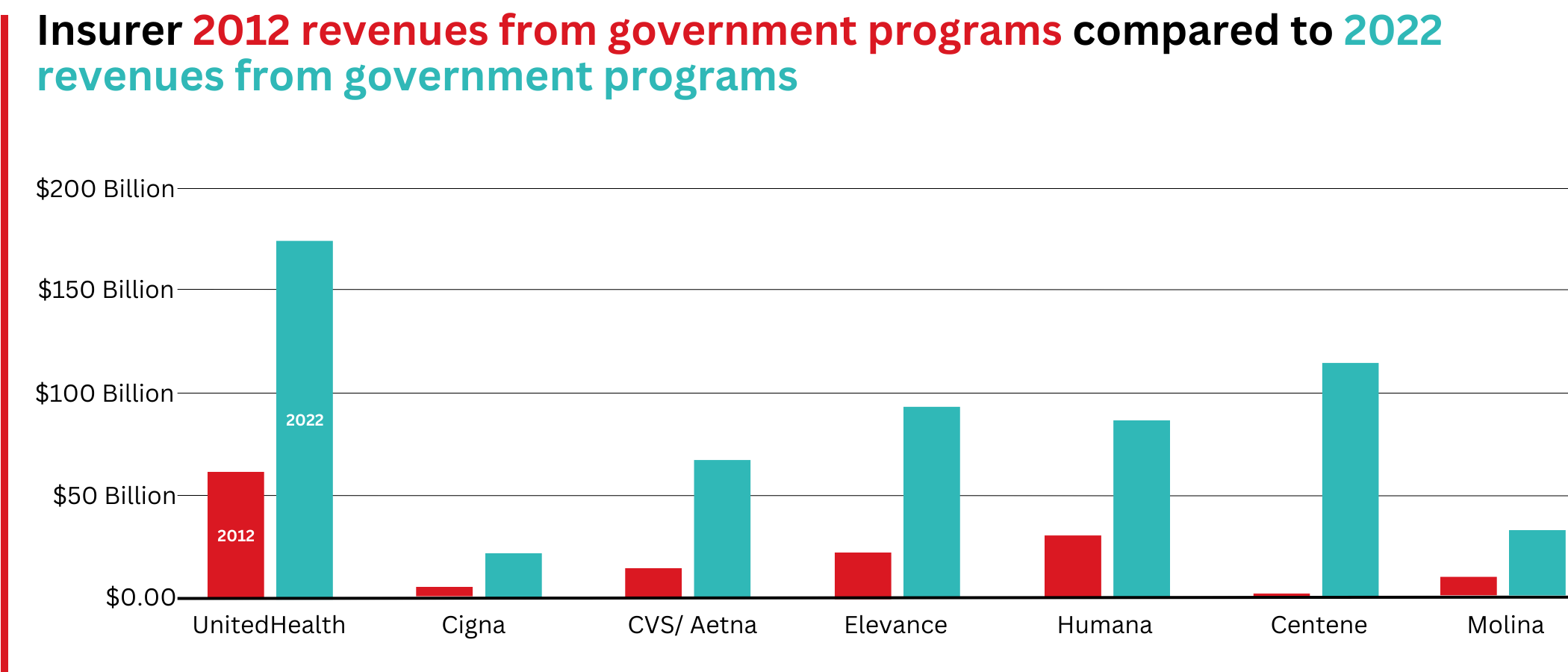

Huge strides in privatizing both Medicare and Medicaid

GOVERNMENT PROGRAMS HIGHLIGHTS

More than 90% of health-plan revenues at three of the companies come from government programs as they continue to privatize both Medicare and Medicaid, through Medicare Advantage in particular.

Enrollment in government-funded programs increased by 261% in 10 years; by contrast commercial enrollment increased by just 10% over the past decade.

Commercial enrollment actually declinedat both UnitedHealth and Humana.

85% of Humana’s health-plan members are in government-funded programs; at Centene, it is 88%, and at Molina, it is 94%.

The big insurers now manage most states’ Medicaid programs – and make billions of dollars for shareholders doing so – but most of the insurers have found that selling their privately operated Medicare replacement plans is even more financially rewarding for their shareholders.

Revenue growth from government programs has been dramatic over the past 10 years. (Note the numbers do not include revenue from the Medicare Part D program, federal subsidy payments for many ACA marketplace plan enrollees, or Medicare supplement policies.)

This is especially apparent when you see that the Big Seven’s combined revenues from taxpayer-supported programs grew 500%, from $116.3 billion in 2012 to $577 billion in 2022.

These numbers should be of interest to the Biden administration and members of Congress, many of whom are calling for much greater scrutiny of the Medicare Advantage program. Numerous media and government reports have shown that the federal government is overpaying private insurers billions of dollars a year, largely because of loopholes in laws and regulations that enable them to get more taxpayer dollars by claiming their enrollees are sicker than they really are. The companies also make aggressive use of prior authorization, largely unknown in traditional Medicare, to avoid paying for doctor-ordered care and medications.

In addition to their focus on Medicare and Medicaid, the companies also profit from the generous subsidies the government pays insurers to reduce the premiums they charge individuals and families who do not qualify for either Medicare or Medicaid or who work for an employer that does not offer subsidized coverage. But many people enrolled in those types of plans – primarily through the health insurance “marketplaces” established by the Affordable Care Act – cannot afford the deductibles and other out-of-pocket requirements they must pay before their insurers will begin paying their medical claims.

Dramatic Enrollment Shifts

Changes in health-plan enrollment over the past decade show how dramatic this shift has been. Between 2012 and 2022, enrollment in the companies’ private commercial plans increased by 10%, from 85.1 million in 2012 to 93.8 million in 2022.

By comparison, growth in enrollment in taxpayer-supported government programs increased 261%, from 27 million in 2012 to 70.4 million in 2022.

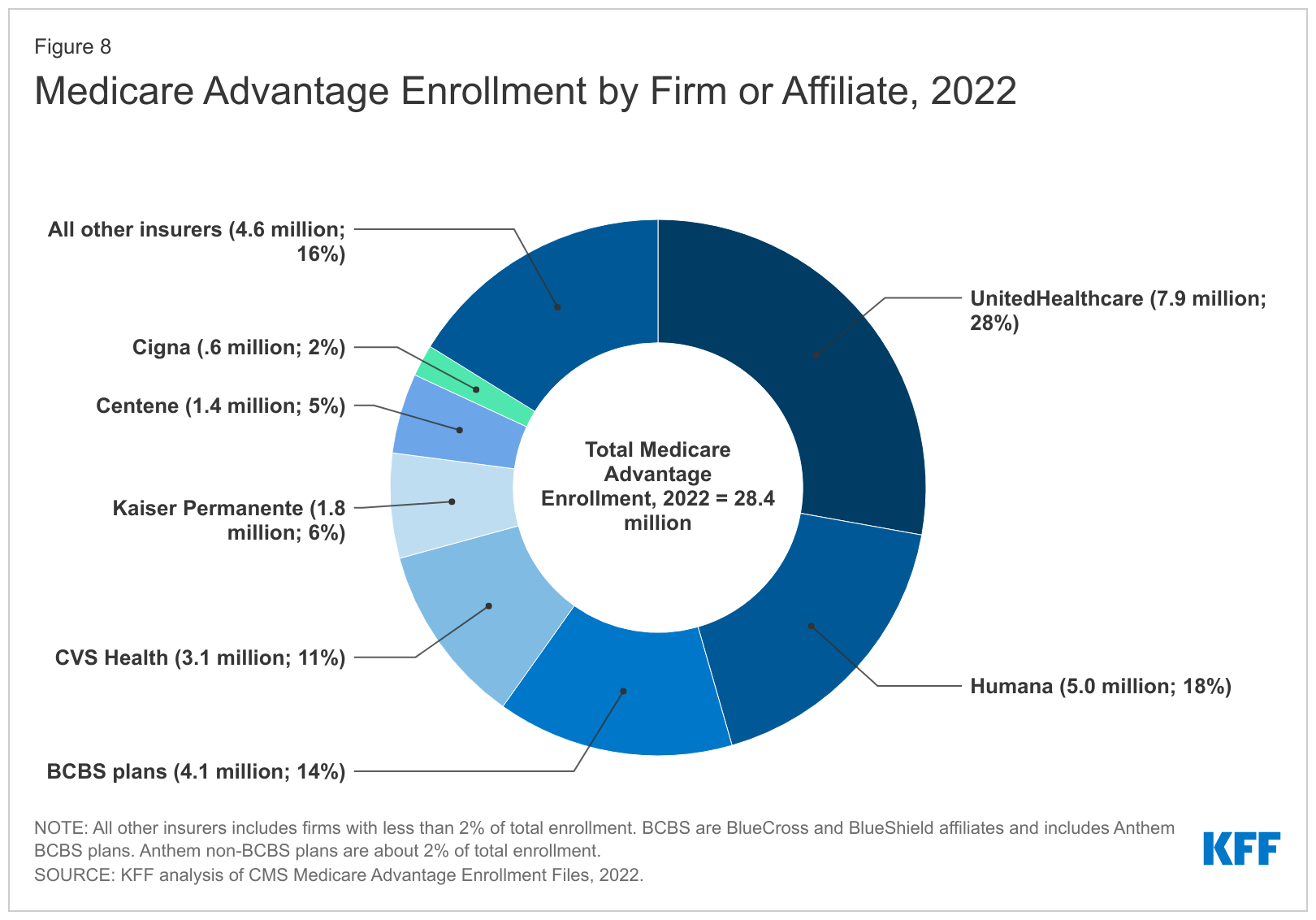

For-profit insurers dominate the Medicare Advantage market. Note that Anthem mentioned above is now known as Elevance. It owns 14 of the country’s Blue Cross Blue Shield plans.

Within that category, Medicare Advantage enrollment among the Big Seven increased 252%, from 7.8 million in 2012 to 19.7 million in 2022.

Nationwide, enrollment in Medicare Advantage plans increased to 28.4 million in 2022 (and to 30 million this year). That means that the Big Seven for-profit companies control more than 70% of the Medicare Advantage market.

UnitedHealth, Humana, Elevance, and CVS/Aetna have captured most of the Medicare Advantage market since the Affordable Care Act was passed in 2010.

The remaining growth in the government segment occurred in the Medicaid programs that a subset of the Big Seven (UnitedHealth, Elevance, Centene, and Molina in particular) manages for several states.

A few other facts and figures to keep in mind as Big Insurance thrives:

100 million of us – almost one of every three people in this country – now have medical debt.

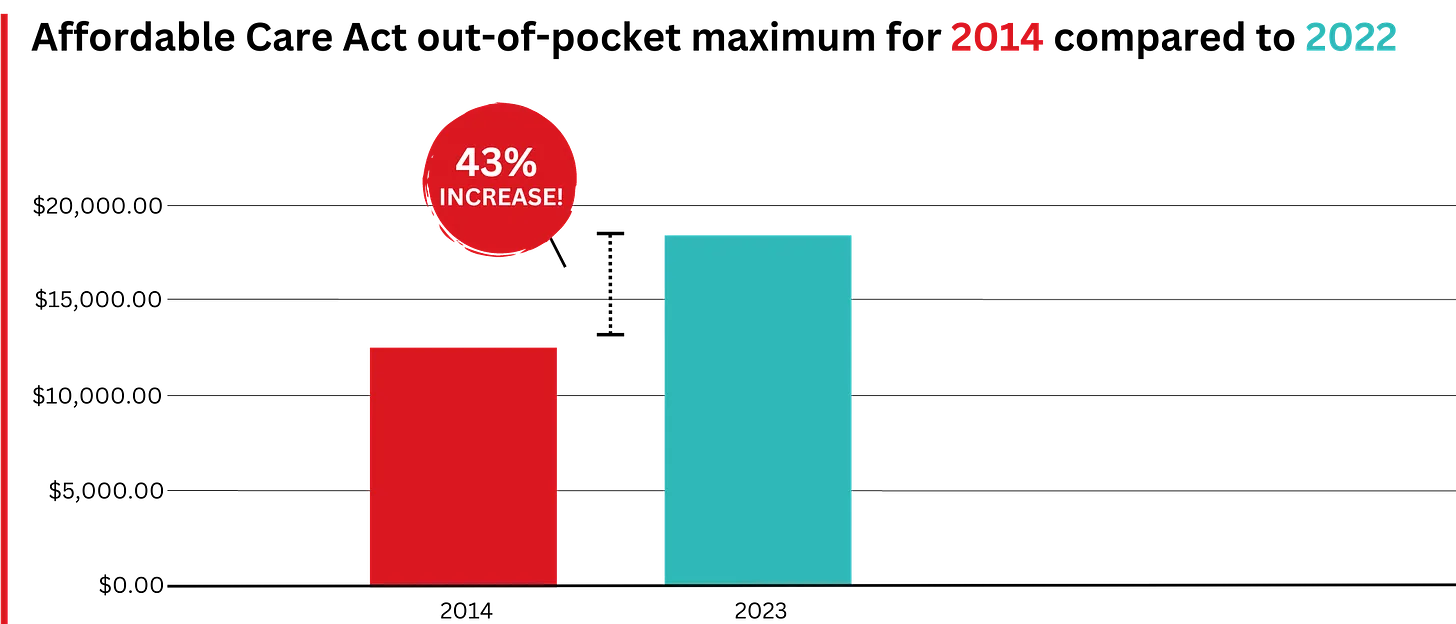

In 2023, U.S. families can be on the hook for up to $18,200 in out-of-pocket requirements before their coverage kicks in, up 43% since 2014 when it was $12,700.The Affordable Care Act allows the out-of-pocket maximum to increase annually – 43% since the maximum limit went into effect in 2014.

44% of people in the United States who purchased coverage through the individual market and (ACA) marketplaces were underinsured or functionally uninsured.

42% said they hadproblems paying medical bills or were paying off medical debt.

Half (49%) said they would be unable to pay an unexpected medical bill within 30 days, including 68% of adults with low income, 69% of Black adults, and 63% of Latino/Hispanic adults.

In 2021, about $650 million, or about one-third of all funds raised by GoFundMe, went to medical campaigns. That’s not surprising when you realize that in the United States, even people with insurance all too often feel they have no choice but to beg for money from strangers to get the care they or a loved one needs.

Even as we spend about $4.5 trillion on health care a year, Americans are now dying younger than people in other wealthy countries. Life expectancy in the United States actually decreased by 2.8 years between 2014 and 2021, erasing all gains since 1996, according to the Centers for Disease Control and Prevention.

BOTTOM LINE:

The companies that comprise Big Insurance are vastly different from what they were just 10 years ago, but policymakers, regulators, employers, and the media have so far shown scant interest in putting their business practices under the microscope.

Changes in federal law, including the Medicare Modernization Act of 2003, which created the lucrative Medicare Advantage market, and the Affordable Care Act of 2010, which gave insurers the green light to increase out-of-pocket requirements annually and restrict access to care in other ways, opened the Treasury and Medicare Trust Fund to Big Insurance. In addition, regulators have allowed almost all of their proposed acquisitions to go forward, which has created the behemoths they are today.

CVS/Health is now the 4th largest company on the Fortune 500 list of American companies. UnitedHealth Group is now No. 5 – and all the others are climbing toward the top 10.

The recent assassination of the CEO of UnitedHealthcare — the health insurance company with, reportedly, the highest rate of claims rejections(and thus dead, wounded, and furious customers and their relations) — gives us a perfect window to understand the stupidity and danger of the Musk/Trump/Ramaswamy strategy of “cutting government” to “make it more efficient, run it like a corporation.”

Consider health care, which in almost every other developed country in the world is legally part of the commons — the infrastructure of the nation, like our roads, public schools, parks, police, military, libraries, and fire departments — owned by the people collectively and run for the sole purpose of meeting a basic human need.

The entire idea of government — dating all the way back to Gilgamesh and before — is to fulfill that singular purpose of meeting citizens’ needs and keeping the nation strong and healthy. That’s a very different mandate from that of a corporation, which is solely directed (some argue by law) to generate profits.

The Veterans’ Administration healthcare system, for example, is essentially socialist rather than capitalist. The VA owns the land and buildings, pays the salaries of everybody from the surgeons to the janitors, and makes most all decisions about care. Its primary purpose — just like that of the healthcare systems of every other democracy in the world — is to keep and make veterans healthy. Its operation is nearly identical to that of Britain’s beloved socialist National Health Service.

UnitedHealthcare similarly owns its own land and buildings, and its officers and employees behave in a way that’s aligned with the company’s primary purpose, but that purpose is to make a profit. Sure, it writes checks for healthcare that’s then delivered to people, but that’s just the way UnitedHealthcare makes money; writing checks and, most importantly, refusing to write checks.

Think about it. If UnitedHealthcare’s main goal was to keep people healthy, they wouldn’t be rejecting 32 percent of claims presented to them. Like the VA, when people needed help they’d make sure they got it.

Instead, they make damn sure their executives get millions of dollars every year (and investors get billions) because making a massive profit ($23 billion last year, and nearly every penny arguably came from saying “no” to somebody’s healthcare needs) is their real business.

On the other hand, if the VA’s goal was to make or save money by “being run efficiently like a company,” they’d be refusing service to a lot more veterans (which it appears is on the horizon).

This is the essential difference between government and business, between meeting human needs (social) and reaching capitalism’s goal (profit).

It’s why its deeply idiotic to say, as Republicans have been doing since the Reagan Revolution, that “government should be run like a business.” That’s nearly as crackbrained a suggestion as saying that fire departments should make a profit (a doltish notion promoted by some Libertarians). Government should be run like a government, and companies should be run like companies.

Given how obvious this is with even a little bit of thought, where did this imbecilic idea that government should run like a business come from?

Turns out, it’s been driven for most of the past century by morbidly rich businessmen (almost entirely men) who don’t want to pay their taxes. As Jeff Tiedrich notes:

“The scariest sentence in the English language is: ‘I’m a billionaire, and I’m here to help.’”

Rightwing billionaires who don’t want to pay their fair share of the costs of society set up think tanks, policy centers, and built media operations to promote their idea that the commons are really there for them to plunder under the rubric of privatization and efficiency.

They’ve had considerable success. Slightly more than half of Medicare is now privatized, multiple Republican-controlled states are in the process of privatizing their public school systems, and the billionaire-funded Project 2025 and the incoming Trump administration have big plans for privatizing other essential government services.

The area where their success is most visible, though, is the American healthcare system. Because the desire of rightwing billionaires not to pay taxes have prevailed ever since Harry Truman first proposed single-payer healthcare like most of the rest of the world has, Americans spend significantly more on healthcare than other developed countries.

In 2022, citizens of the United States spent an estimated $12,742 per person on healthcare, the highest among wealthy nations. This is nearly twice the average of $6,850 per person for other wealthy OECD countries.

Over the next decade, it is estimated that America will spend between $55 and $60 trillion on healthcare if nothing changes and we continue to cut giant corporations in for a large slice of our healthcare money.

On the other hand, Senator Bernie Sanders’ single-payer Medicare For All plan would only cost $32 trillion over the next 10 years. And it would cover everybody in America, every man woman and child, in every medical aspect including vision, dental, psychological, and hearing.

If we keep our current system, the difference between it and the savings from a single-payer system will end up in the pockets, in large part, of massive insurance giants and their executives and investors. And as campaign contributions for bought off Republicans. This isn’t rocket science.

And you’d think that giving all those extra billions to companies like UnitedHealthcare would result in America having great health outcomes. But, no.

Despite insanely higher spending, the U.S. has a lower life expectancy at birth, higher rates of chronic diseases, higher rates of avoidable or treatable deaths, and higher maternal and infant mortality rates than any of our peer nations.

Compared to single-payer nations like Canada, the U.S. also has a higher incidence of chronic health conditions, Americans see doctors less often and have fewer hospital stays, and the U.S. has fewer hospital beds and physicians per person.

No other country in the world allows a predatory for-profit industry like this to exist as a primary way of providing healthcare. Every other advanced democracy considers healthcare a right of citizenship, rather than an opportunity for a handful of industry executives to hoard a fortune, buy Swiss chalets, and fly around on private jets.

This is one of the most widely shared graphics on social media over the past few days in posts having to do with Thompson’s murder…

Sure, there are lots of health insurance companies in other developed countries, but instead of offering basic healthcare (which is provided by the government) mostly wealthy people subscribe to them to pay for premium services like private hospital rooms, international air ambulance services, and cosmetic surgery.

Essentially, UnitedHealthcare’s CEO Brian Thompson made decisions that killed Americans for a living, in exchange for $10 million a year. He and his peers in the industry are probably paid as much as they are because there is an actual shortage of people with business training who are willing to oversee decisions that cause or allow others to die in exchange for millions in annual compensation.

That Americans are well aware of this obscenity explains the gleeful response to his murder that’s spread across social media, including the refusal of online sleuths to participate in finding his killer.

It shouldn’t need be said that vigilantism is no way to respond to toxic individuals and companies that cause Americans to die unnecessarily. Hopefully, Thompson’s murder will spark a conversation about the role of government and the commons — and the very real need to end the corrupt privatization of our healthcare system (including the Medicare Advantage scam) that has harmed so many of us and killed or injured so many of the people we love.

Last week, President-elect Donald Trump announced that Robert F. Kennedy, Jr. would be his nominee for Secretary of Health and Human Services (HHS). He followed this up on Tuesday with his selection of Dr. Mehmet Oz as his nominee for the Centers for Medicare and Medicaid Services (CMS) Administrator. If confirmed, the two men would replace Xavier Becerra and Chiquita Brooks-LaSure, respectively.

Kennedy, who ended his independent presidential campaign and endorsed Trump in August, has become known for his heterodox views on public health, including vaccine skepticism and opposition to water fluoridization.

Dr. Oz, first famous as a TV personality and more recently a Republican candidate for Pennsylvania Senator, is a strong proponent of Medicare Advantage, having co-authored an op-ed advocating for “Medicare Advantage for All” in 2020.

The Gist:

These nominees, especially Kennedy, hold a number of personal beliefs at odds with the public health consensus.

They are both likely to be confirmed, however, as the last cabinet nominee to be rejected by the Senate was John Tower in 1989. (This does not include nominees who have chosen to withdraw themselves from consideration, as former Representative Matt Gaetz has just done.)

Should they be confirmed, they will be responsible for implementing not their own but President Trump’s agenda, the specific priorities of which also remain relatively undefined.

However, possible consensus points between Trump and his nominees include public health cuts and deregulation, greater scrutiny of pharmaceutical companies, and a favoring of Medicare Advantage over traditional Medicare.

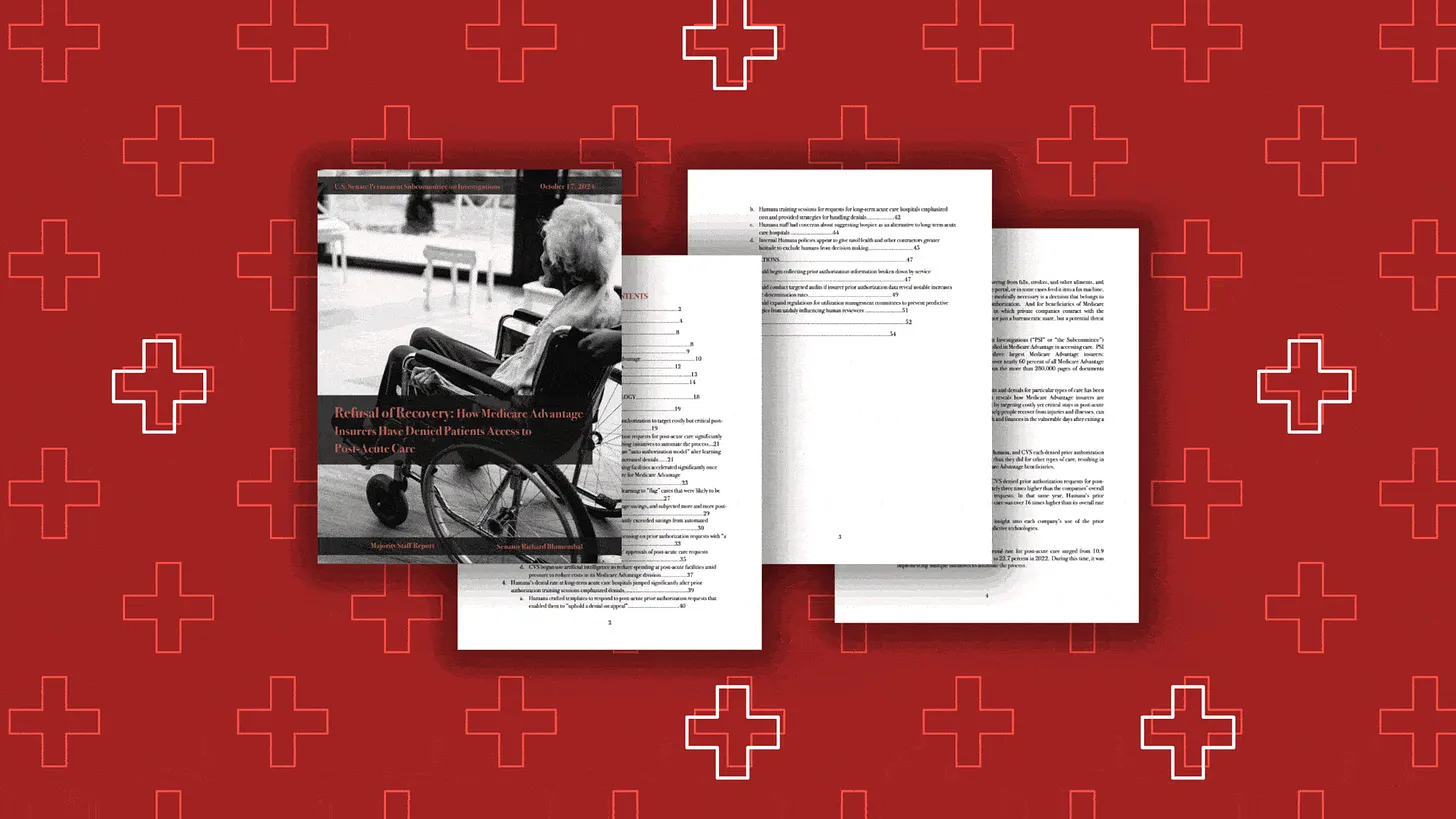

Last week, the Senate Permanent Subcommittee on Investigations, led by Sen. Richard Blumenthal (D-Connecticut), released a Majority Staff Report on rampant prior authorization (PA) abuses in Medicare Advantage (MA).

The report offers unique insight into recent trends in the use of prior authorization by Medicare Advantage plans and the strategy and motives behind insurance corporations’ use of it.

While the findings won’t surprise those who’ve been following health policy trends, it is immensely concerning that between 2019 and 2022, the prior authorization denial rate for post-acute care in UnitedHealth’s Medicare Advantage plans doubled.

The denial rate for long-term acute care hospitals in Humana’s Medicare Advantage plans increased by 54% from 2020 to 2022. During this time, UnitedHealth, CVS/Aetna, and Humana increased their use of artificial intelligence (AI) for prior authorization reviews, often resulting in increasing denial numbers and decreasing (or absent) review time by human beings.

The report recommends that the Centers for Medicare and Medicaid Services (CMS) collect additional data, conduct audits of prior authorization processes, and expand regulations on the use of technology in PA reviews. While these recommendations would be positive steps, the report’s findings call into question whether Big Insurance can ever be trusted or regulated enough to prevent abuse of patients through prior authorization and other mechanisms.

This report provides an in-depth look at insurers’ motivations. Sadly, those motivations are not to “make sure a service or prescription is a clinically appropriate option,” as UnitedHealth claims, but to decrease the amount spent on medical care to increase the corporations’ profits.

The report noted that CVS, which owns Aetna, saved $660 million in 2018 by denying Medicare Advantage patients’ claims for treatment at inpatient facilities. Around the same time, CVS found in its testing of a model to “maximize approvals,” which would be a good thing for patients, that the model jeopardized profits because it would lead to more care being covered. In 2022, CVS “deprioritized” a plan to increase auto-approvals because of the lost “savings” from denying patient care.

The report found that the motivation to increase profits, without regard for patient care, was not unique to CVS/Aetna.

UnitedHealth’s naviHealth subsidiary provided this directive to its employees: “IMPORTANT: Do NOT guide providers or give providers answers to the questions” when speaking to a patient’s doctor about a prior authorization request. Instead of working collaboratively with doctors to get patients the care they need, UnitedHealth told its workers not to bother. In a training session offered to Humana employees involved in prior authorization reviews, the company explained that reviewers should deny a request for post-acute care even if a patient needed more intensive treatment. Humana told reviewers that the lack of an in-network lower-level care facility for patients to go to was not a reason to approve post-acute care and that usually the situations can be “sorted out,” presumably by the patient with no help from the insurer.

All three companies (UnitedHealth, Humana and CVS/Aetna), which dominate the Medicare Advantage program, demonstrated a striking lack of motivation to protect and enhance patient care, instead showing a primary motivation to increase profits and margins.

The subcommittee’s report also noted that UnitedHealth, CVS/Aerna, and Humana are increasingly using AI to make care decisions and cutting humans, especially doctors, out of the process. The researchers found that in 2022, UnitedHealth looked into how using AI and machine learning could aid in predicting which denials of post-acute care requests were most likely to be overturned. One would hope this effort would be to decrease the number of wrongfully denied prior authorization requests and increase patient access to care.

However, the report includes a quote from a recap of a meeting on the project asking “what we could do in the clinical review process to change the outcome of the appeal,” meaning that UnitedHealth was interested in preventing the overturning of denials, not getting the decision right in the first place. The report also found evidence that naviHealth used artificial intelligence to help determine the coverage decisions for a patient’s post-acute care claim before any human post-acute care providers evaluated a case. The report’s authors found that denials for post-acute care facilities rose rapidly once naviHealth began managing these requests for UnitedHealth’s MA plans.

These are just some of the findings in the 54-page report on Big Insurance’s use of prior authorization to deny Medicare Advantage patient requests for post-acute care.

The report’s findings demonstrate the abuse of prior authorization by the insurers, the motivation to increase profit and decrease patient care, and the use of AI to increase denials. Further, the findings underscore that prior authorization is a tool used by Big Insurance primarily to maximize profits. The report puts forward recommendations to cut down on abusive denials, which would have some positive impact.

More importantly, I believe the report provides more evidence that it is becoming exceedingly less likely that private and for-profit insurance companies can be regulated and act in a way that promotes patient health over profits.

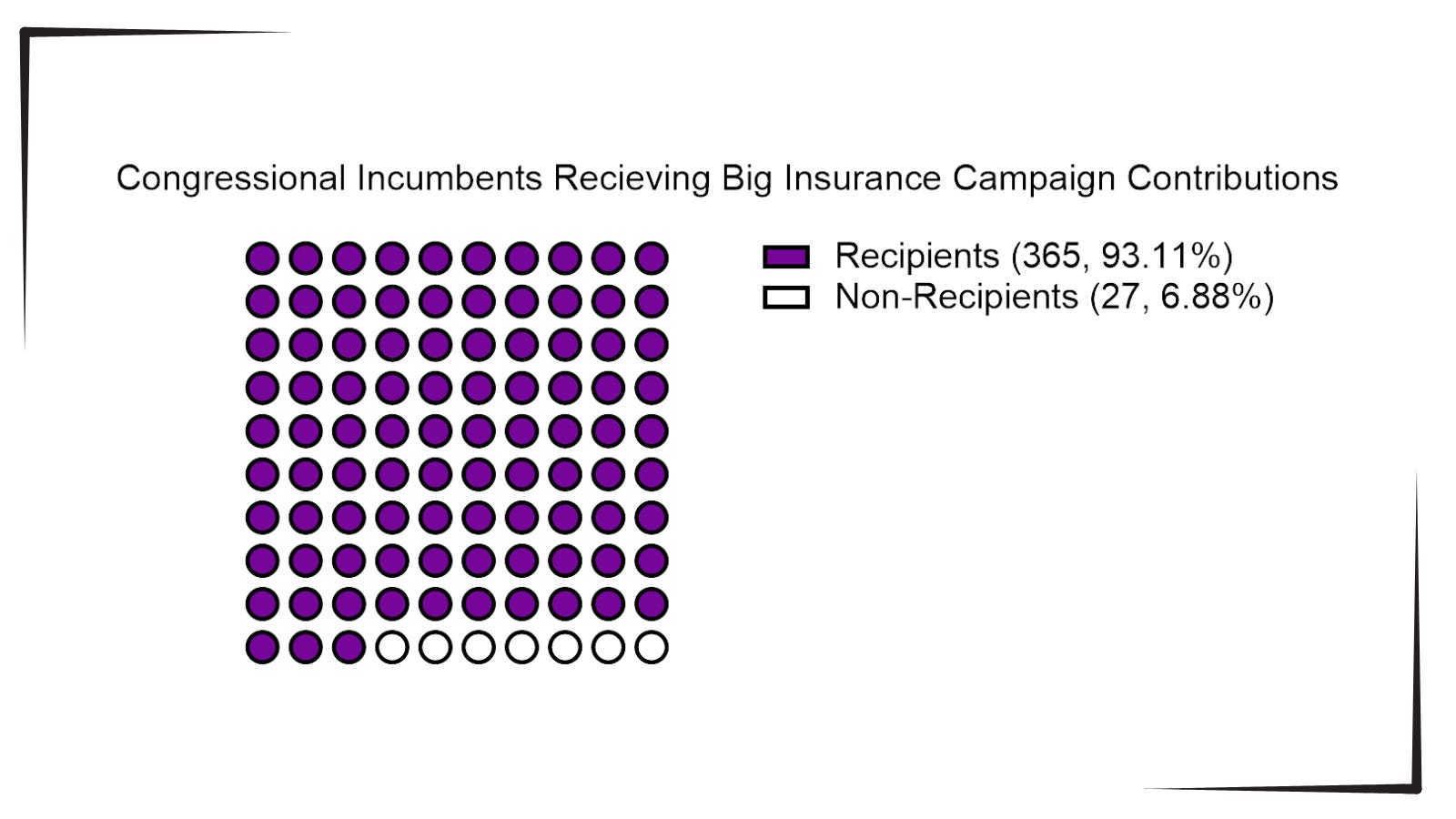

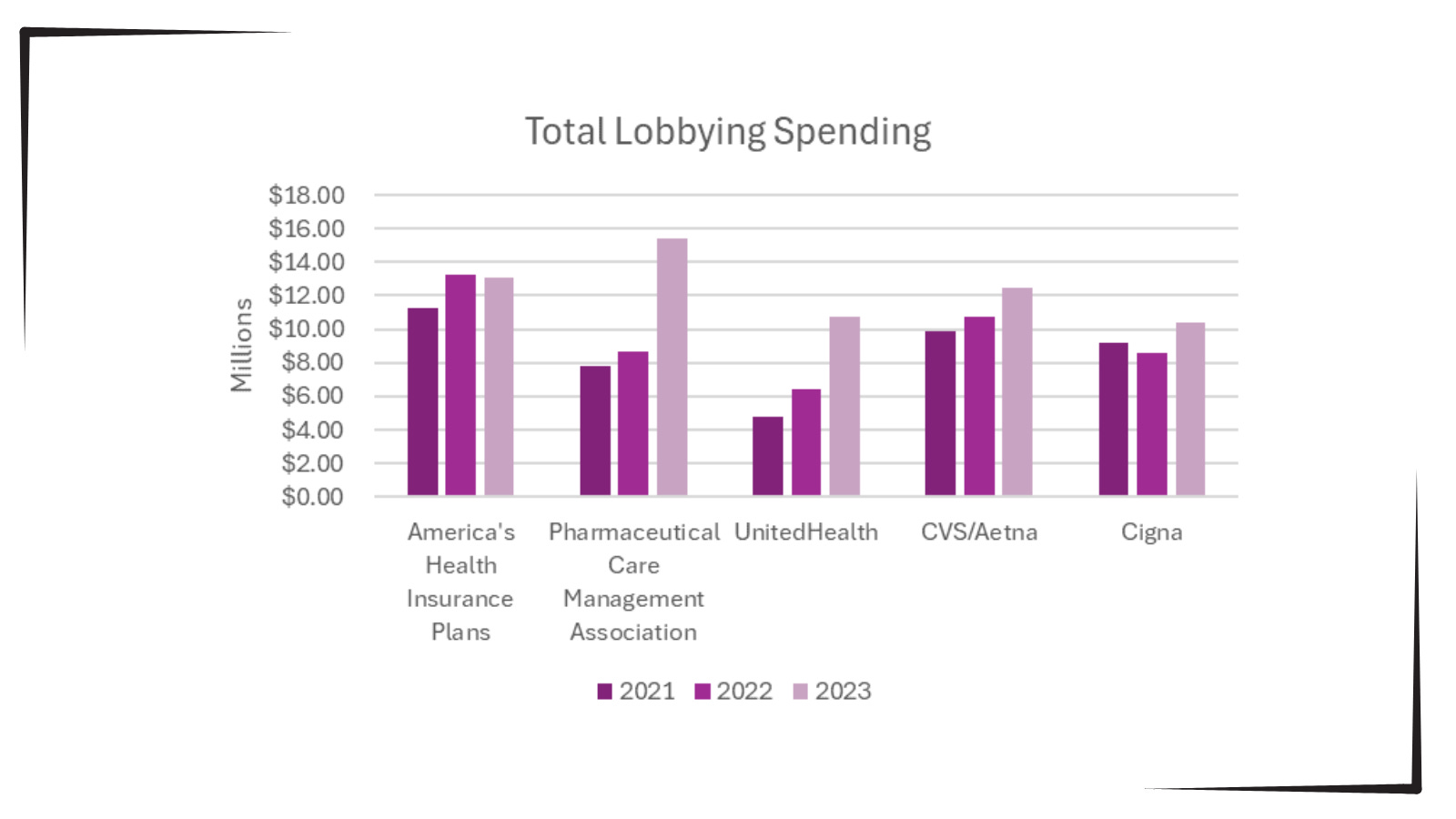

With the election looming and the beginning of annual open enrollment periods for health insurance plans, it is vital to pull back the curtain on the influx of money from Big Insurance corporations to political campaigns and lobbying.

Data available from OpenSecrets.com thus far in 2024 shows that 93% of Congressional incumbents running in 2024 received contributions from Big Insurance, including 100% of Senate incumbents. These insurance corporations run the ten largest Medicare Advantage plans in the country and are known to deny needed health care and defraud the government, but face little to no consequences.

Insurance corporations included in this analysis are UnitedHealth Group, Humana, CVS/Aetna, Kaiser Permanente, Elevance Health, Centene Corp, Cigna, Blue Cross Blue Shield Association (which represents many MA plans, including two of the largest: BCBSMichigan and Highmark), and SCAN.

Additionally, as bipartisan scrutiny of pharmacy benefit managers (PBMs) and Medicare Advantage plans has intensified, spending by Big Insurance on lobbying has increased.

Total lobbying spending by America’s Health Insurance Plans; Pharmaceutical Care Management Association; UnitedHealth; CVS/Aetna; and Cigna for the years 2021, 2022 and 2023.

This open enrollment season, people struggling to choose a health insurance plan that they can afford and that provides the care they need may ask themselves, “Why is our health care system like this?” The immense amounts of money Big Insurance spends to blanket members of Congress with contributions and lobbying hold the answer.

Additional analysis following the election will allow evaluation of just how much Big Insurance spends on politics to help protect industry profits and will give health reform advocates an idea of how to overcome this influence to pass policies for patients, not profits.

Back in February, Dr. Philip Verhoef and I wrote an op-ed for STAT News warning both patients and investors to steer clear of the health insurance industry’s private version of Medicare, which the government continues to allow insurers to market as Medicare Advantage.

As we enter the open enrollment period in which America’s seniors and disabled people are able to choose between the traditional Medicare program and a bewildering array of private plans, it’s a good time to remind you why you need to steer clear of Medicare Advantage.

Millions of people enrolled in those private plans are now getting notices from their insurers that their plans will not be available in 2025 because

three of the biggest insurance corporations (Humana, CVS/Aetna and Cigna) – and probably several smaller insurers – have decided to stop selling MA plans in hundreds of communities across the country, which means that MA enrollees in all those places are going to have to go through the agonizing chore of finding a replacement.

Why? Because Wall Street, which until this year was head-over-heels in love with Medicare Advantage, is now filing for divorce.

Investors have been running for the exits since they began seeing danger signs in for-profit insurers’ earnings reports in the last quarter of 2023. For at least two of the biggest players in MA – Humana and CVS – that exodus has in recent weeks turned into a stampede. The stock prices of those two companies have been in steep decline all year, and you can be certain the top executives of those companies are now in panic mode.

People who’ve been following my work since I blew the whistle on the health insurance racket know I’ve been trying to educate seniors – and policymakers – for at least a dozen years, going back to my time at the Center for Public Integrity, about the many shortcomings of what I’ve often called Medicare Disadvantage. I’ve also called Medicare Advantage the biggest heist of taxpayers’ dollars in American history. It’s truly epic.

The truth is that MA has been a broken system since the beginning, especially for patients. The business worked only as long as insurers were able to extract inappropriately large payments from the Medicare fund through methods like upcoding, where plans list false or exaggerated diagnoses on patient charts to get more money while providing no additional care.

In fact, the MA model relies on providing as little care as possible in general, with insurers putting care approval behind a wall of delays and denials to save money and leaving patients suffering without necessary treatment.

We wrote that op-ed just as the government began taking long-overdue steps to rein in some of those abuses and, to Wall Street’s shock, announced at the end of February that it would not be giving MA plans as much money going forward as the industry had expected. That announcement, coupled with the reins-tightening, really spooked investors.

But that wasn’t all that soured them on Medicare Advantage. The big MA insurers had to admit to Wall Street when they released quarterly earnings that despite their best efforts to delay and deny as much care as possible, seniors nevertheless were using more health care than before.

The insurers’ medical loss ratios were ticking up, meaning they were having to use more of their customers’ premiums (and Medicare fund money) paying claims than they had anticipated. And folks, Wall Street HATES it when insurers do that.

Phil and I wrote that:

Before, investors had assumed MA plans could keep the business humming along, that private insurers would always be able to keep their enrollees’ use of medical goods and services in check, and that policymakers would always look the other way as the government doled out billions in overpayments annually. They now see that these assumptions are failing, and many have sold their holdings in these companies as a result.

The selling has continued apace throughout 2024, and the biggest loser on Wall Street has been Humana, which currently has an 18% share of the MA market, second behind UnitedHealth’s 29%. CVS/Aetna’s shares have also been dropping like a rock.

Humana got another kick to the stomach from investors this week when it admitted that it likely will lose billions of dollars in payments in the future because far fewer of its MA enrollees will be in so-called four-star rated MA plans – 25% in 2025 compared to 94% in 2024. The feds give four-star rated MA plans a lot more money than lower-rated plans.

When the New York Stock Exchange closed yesterday, Humana’s share price had fallen to $241.37. That’s down more than 54% since the 52-week high of $530.54 it reached in October 2023. But get this: on Wednesday the share price reached a 52-week low of $213.31 before inching back up later in the day as some investors apparently saw a way to make money at some point down the road by buying at that low price.

And folks, that was not just a 52-week low. The last time Humana’s share price was in that territory was on April 25, 2017, when the low for the day was $214.51.

All this turmoil has led Bank of America Securities to downgrade the stock to “underperform,” another word for sell. Piper Sandler also downgraded the company yesterday. Those downgrades – and possibly more to come – could cause the stock price to sink even further.

Having worked closely with Humana’s C-suite and investor relations people when I headed corporation communications there before going to Cigna, I can assure you the company’s top brass are grasping at any levers they can get their hands on to stop the freefall. I would not want to be one of them, and I certainly would not want to be one of their customers or investors.

As I mentioned, Humana, UnitedHealth and CVS/Aetna are by far the biggest players in the MA game. Earlier this year, those three companies captured 86% of the 1.7 million new MA enrollees, thanks to spending untold millions of federal dollars on deceptive TV ads and other marketing schemes.

Humana is now dumping hundreds of thousands of its MA enrollees because they somehow managed to get the care they needed. The company is doing that for one single reason: to try to get back into Wall Street’s good graces.

Next week we’ll look at how the other two big players in Medicare Advantage, UnitedHealthcare and CVS/Aetna, are faring on Wall Street. It is a tale of two cities, as you’ll see.

On October 15, the open enrollment period for Medicare begins running through December 7 for coverage starting in January 2025. In this period, 67 million Medicare eligible seniors can review features of Medicare plans offered in their area, switch from traditional Medicare to a Medicare Advantage (MA) plan (or vice versa), change their MA selection and add/change their Medicare Part D prescription drug plans.

In 2024, Medicare Advantage plans enrolled 33 million seniors and Medicare paid private insurers $462 billion to pay for their care.

But conditions for Medicare Advantage have changed in recent years prompting many to ask ‘what is the Medicare Advantage?’

Background:

Medicare began July 30, 1965 as a key element in President Lyndon Baines Johnson’s Great Society program offering federal-government-paid insurance coverage for seniors at the age of 65. “Original Medicare” had two parts: Part A to cover hospitals and Part B to cover physicians and outpatient services. In 1972, coverage for adults with disabilities was added, and in 2003, coverage for prescription drugs (Part D) was added.

Its funding comes from payroll taxes paid by employers and their employees, and those who are self-employed PLUS income taxes paid on Social Security benefits, interest earned on the Medicare trust fund’s investments and Part A premiums from people who aren’t eligible for premium-free Part A.

Along the way, Congress authorized seniors the option of accessing Medicare through private insurers aka Part C (Balanced Budget Act of 1997), expanded its scope (Medicare Modernization Act of 2003) and supplemented its funding differential above Original Medicare (Patient Protection and Affordable Care Act 2010) to stimulate enrollment growth. The rationale for MA was straightforward: it offered federal regulators a lab to test care management for seniors with the dual aims of lowering their health costs and improving their health. Private insurers responded. By design, funding for MA was set above Original Medicare rates to encourage private insurer participation.

It worked. This year, the average MA enrollee had 43 plans from which to choose. By three measures, Medicare Part C has been successful:

Enrollment growth: Enrollment in MA plans has increased from 31% of Medicare eligible adults in 2014 to 51% in 2024 and is projected to increase in 2025. Notably, enrollment in special needs and employer-sponsored MA plans has increased faster than the individual MA market which is subject to open enrollment periods. Satisfaction appears high (69% of members do not shop for another plan during open enrollment periods) and member churn is low.

Medicare has saved money: Per the 2024 Medicare Trustees’ Report, MA has contributed to slower growth in Medicare spending than forecast. “The Social Security and Medicare programs both continue to face significant financing issues…The Hospital Insurance (HI) Trust Fund will be able to pay 100% of total scheduled benefits until 2036, 5 years later than reported last year. At that point, that fund’s reserves will become depleted and continuing program income will be sufficient to pay 89% of total scheduled benefits.”

Private insurer participation has been strong: For health insurers, Medicare Advantage is profitable: PMPM contribution margins are 50-100% higher than individual and group lines of business. And, as CMS payments to MA have tightened, the MA insurer market consolidated with 3 (UnitedHealth, Humana, CVS-Aetna) taking advantage of operating pressures on small players to increase their share to 58% of total enrollment. Advantage: Seniors, Medicare and Corporate Insurance.

But conditions going forward suggest the MA advantage might not be as strong. The market signals are clear:

Insurer belt tightening: Since 2023, seniors’ use of hospitals, specialty care and prescription drugs has returned to pre-pandemic normalcy cutting into insurer margins. In its CY 2025 Rate Announcement September 27, CMS announced “The average monthly plan premium for all MA plans, which includes MA plans that provide prescription drug coverage and MA Special Needs Plans (SNPs), is projected to decrease from $18.23 in 2024 to $17.00 in 2025. Benefit options will remain stable, including MA supplemental benefit offerings such as hearing, dental, and vision. The amount of rebate dollars, which can be used for supplemental benefits, will remain stable, with a slight increase, from 2024 to 2025. Enrollment in MA is projected to be 35.7 million in 2025, an increase from 2024, with MA enrollment representing approximately 51% of all people enrolled in Medicare.” This translates to lower margins for MA plans, fewer supplemental benefits for enrollees and lower payments to hospitals and physicians.

Increased regulatory scrutiny: The Medicare Payment Advisory Commission (MedPAC) concluded that MA plans receive payments from CMS that are 122%of spending for similar beneficiaries in traditional Medicare, on average, translating to an estimated $83 billion in overpayments in 2024. Congress is investigating. In 2023, CMS adopted tougher audit standards specific to diagnosis codes used by private MA plans to bill Medicare on behalf of their enrollees. Audits conducted by the U.S. Department of Human Services’ Office of Inspector General (OIG) applying the new standards found the majority of private MA plans guilty of upcoding and thereby overpaid by Medicare. In 2025, cut points used by CMS to award star ratings have been modified resulting in fewer plans getting 4-star ratings that enable their participation in 5% bonus payments—a major reason recent stock declines for UHG, HUM, CVS and others. Regulatory scrutiny of MA plan marketing practices, coding, denials and prior authorization procedures will intensify reflecting bipartisan intent to constrain MA profits.

Understandably, tension between MA insurers and providers has intensified as insurers seek to protect their margins. The Change Healthcare (CH) cyber-attack (February 21, 2024) that disabled insurer payments to hospitals and physicians stoked animosity since CH is a subsidiary of UnitedHealth Group–the largest sponsor of MA plans and the healthcare juggernaut. Though operating margins for half of U.S. hospitals have recovered, insurer cuts coupled with labor and prescription drug costs have decimated care delivery in almost every community. Participation in MA plan provider networks, once SOP is now a tough call for hospitals, medical groups and other providers.

My take:

What is the Medicare Advantage?

As a lab for innovation in care management for seniors, it’s promising.

As an engine to drive lower costs for senior health and extended solvency to the Medicare program, it’s unclear.

As a platform to shift incentives from fee-for-service to value across the system, it’s helpful.

But until and unless hospitals, physicians, insurers, business leaders and regulators commit to implement a transformed system of health that’s comprehensive, affordable, efficient and accountable, the Medicare Advantage will be marginalized.

In many ways, the headwinds facing MA are part of the larger narrative facing healthcare:

public sentiment against consolidation and corporatization has eroded its cherished trust and confidence. It’s true for insurance, hospitals, prescription drug companies and PBMs. The blame is shared: no one of these owns the moral high ground (though a few organizations in their ranks aspire).