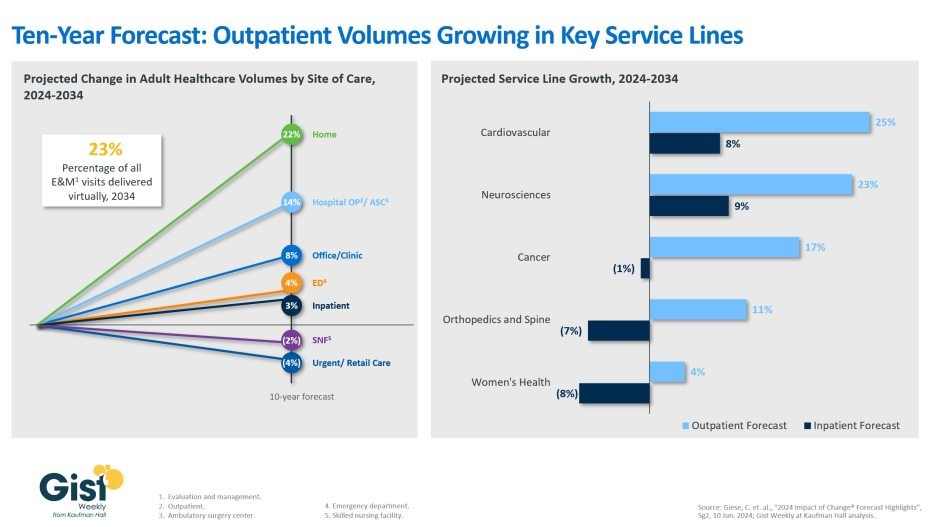

Using the latest data forecast from Sg2, a Vizient company, the graphic above illustrates how the outpatient shift will continue to accelerate through 2034.

Home-based care and outpatient services, including ambulatory surgery centers, are projected to be the fastest growing care sites over the next decade, with volumes increasing 22% and 14% respectively.

Sg2 forecasts that physician offices, emergency departments, and inpatient settings will experience more modest volumes increases, whereas skilled nursing facilities and retail care volumes are predicted to decline.

Additionally, although the initial outpatient procedural shift was largely focused on orthopedics, the next wave of outpatient volume growth will come from other service lines.

Driven by regulatory changes, as well as patient demand, outpatient cardiovascular volumes are expected to increase by 25% over the next decade, closely followed by neurosciences at 23%.

Continued health system investment into higher-acuity outpatient care remains crucial.

Economists say in an ideal world, different hospitals will specialize in different forms of care while others — particularly in rural areas — will focus on providing basic services.

Why it matters:

The hospital of the future will likely mean a significantly different patient experience, in ways both obvious (it’ll have better technology) and potentially disruptive (it could require more travel).

“My own view of what it’s going to look like in the longer run is much, much fewer hospitals that are much, much bigger,” said Yale’s Cooper.

Where it stands:

Many health systems are already cutting service lines — maternity care is a common one — or closing altogether, especially rural hospitals.

To some extent, that may be OK, some experts say. The reality created by shifting demographics is that some places just don’t have the population necessary to support certain services.

Not only do the economics not work, but a handful of specialized procedures every year probably isn’t enough to keep providers well-trained.

Between the lines:

Instead of consolidation, there should be more of a divergence between hospitals that provide basic care to local communities and those that specialize in more complex care, Cooper said.

That model, of course, would mean many patients would have to travel for certain care instead of receiving it at their local hospital.

And as technology broadlychanges the consumer experience, patients will have similar expectations for their care.

“People’s gold standard is buying stuff on Amazon at 2 in the morning, and when they compare their health care experience, they say, ‘Why can’t my health care experience be more like that?'” Kaufman said.

Emerging medical technologies will also impact the care that people receive, and hospitals are positioning themselves at the forefront of that change.

“Patients right now — and in the future — can expect more care delivery that is driven by 3D modeling; predictive analytics; advanced robotics for surgeries and treatments; and personalized therapies based on genomics,” American Hospital Association president and CEO Rick Pollack wrote in a blog post last year.

Yes, but:

Hospitals that serve higher populations of vulnerable people, who are more likely to have lower-paying government insurance, are the most financially exposed.

That means if they don’t adapt, care could become even less accessible for these patients.

Some economists’ ideal version of the future may mean lower profits for health systems.

Hospitals “should do what they do best, which is inpatient care and emergency care … and other people should do things that they do best, like the physicians working together as a multi-specialty group but not part of the hospital,” said Johns Hopkins’ Anderson.

“They wouldn’t make the substantial profits they’re making, but for the nonprofits, that’s not the goal,” he added.

The bottom line:

“Is there going to be disruption? Yes,” Cooper said. “I think there’s a romanticism about local hospitals. They’re where our kids were born and where our parents spent their final days.”

“But I firmly believe the local hospital of the future is not doing everything for everyone.”

Companies grappling with liquidity concerns are looking to cut costs and streamline operations, according to a new survey.

Dive Brief:

Over three-quarters of healthcare chief financial officers expect to see profitability increases in 2024, according to a recent survey from advisory firm BDO USA. However, to become profitable, many organizations say they will have to reduce investments in underperforming service lines, or pursue mergers and acquisitions.

More than 40% of respondents said theywill decrease investments in primary care and behavioral health services in 2024, citing disruptions from retail players. They will shift funds to home care, ambulatory services and telehealth that provide higher returns, according to the report.

Nearly three-quarters of healthcare CFOs plan to pursue some type of M&A deal in the year ahead, despite possible regulatory threats.

Dive Insight:

Though inflationary pressures have eased since the height of the COVID-19 pandemic, healthcare CFOs remain cognizant of managing costs amid liquidity concerns, according to the report.

The firmpolled 100 healthcare CFOs serving hospitals, medical groups, outpatient services, academic centers and home health providers with revenues from $250 million to $3 billion or more in October 2023.

Just over a third of organizations surveyed carried more than 60 days of cash on hand. In comparison, a recent analysis from KFF found that financially strong health systems carried at least 150 days of cash on hand in 2022.

Liquidity is a concern for CFOs given high rates of bond and loan covenant violations over the past year. More than half of organizations violated such agreements in 2023, while 41% are concerned they will in 2024, according to the report.

To remain solvent, 44% of CFOs expect to have more strategic conversations about their economic resiliency in 2024, exploring external partnerships, options for service line adjustments and investments in workforce and technology optimization.

Most organizations are interested in exploring sales, according to the report. Financially struggling organizations are among the most likely to consider deals. Nearly one in three organizations that violated their bond or loan covenants in 2023 are planning a carve-out or divestiture this year. Organizations with less than 30 days of cash on hand are also likely to consider carve-outs.

Organizations will also turn to automation to cut costs. Ninety-eight percent of organizations surveyed had pilotedgenerative AI tools in a bid to alleviate resource and cost constraints, according to the consultancy.

“Healthcare leaders believe AI will be essential to helping clinicians operate at the top of their licenses, focusing their time on patient care and interaction over administrative or repetitive tasks,” authors wrote. Nearly one in three CFOs plan to leverage automation and AI in the next 12 months.

However, CFOs are keeping an eye on the risks. As more data flows through their organizations, they are increasingly concerned about cybersecurity. More than half of executives surveyed said data breaches are a bigger risk in 2024 compared to 2023.

The upheaval of the past few years has permanently changed the healthcare landscape, and while many sectors of the industry continue to endure financial hardship, there is reason for cautious optimism in 2024 as healthcare begins to see a return on investment in technology and a resurgence in dealmaking.

This year, BDO surveyed healthcare CFOs to discover their plans, priorities, and concerns heading into 2024.

In today’s newsletter, I’ve outlined the top research findings that every healthcare leader needs to know to prepare for the year ahead.

Top 3 Workforce Investment Areas

Clinician burnout and staffing shortages remain challenging in the healthcare industry, but BDO’s survey indicated that many CFOs are bullish that the worst is behind them, with 47% stating they feel that in 2024, the talent shortage will represent less of a risk than in 2023.

Investment in the workforce is crucial to addressing staffing challenges, and in the year ahead, healthcare CFOs intend to invest in the following ways:

1. Training: 48% of CFOs plan to spend more on training, in part to buttress ongoing investment in new technologies like AI that can help with predictive staffing and financial reporting.

2. Recruitment: 48% of CFOs will spend more on recruiting, as the talent shortfall tightens an already restricted pool of candidates.

3. Compensation & Benefits: Alongside greater spending on recruiting itself, 46% of CFOs intend to increase compensation and benefits as a means of attracting talent from competitors and retaining current staff.

Transaction Plans

Dealmaking turned a corner in 2023, with activity returning to pre-pandemic levels in Q2. Despite fluctuating interest rates and the volatility of an election year, we can expect more transactions in 2024, with 72% of CFOs planning some kind of deal, relative to their organization’s financial health and liquidity. An increase in antitrust activity, however, could impact the size and type of deals that see success. Healthcare CFOs planning a large deal should be prepared for heightened scrutiny.

While we expect to see a wide range of deals taking place over the next year, two specific deal types are worth calling out:

1. Carve-outs/Divestitures: We may see an uptick in enterprise sales, carve-outs, and divestitures, particularly for institutions that have been struggling financially — 31% of institutions that violated their bond or loan covenants in 2023 are planning to pursue deals of this kind.

2. Private Equity (PE) and Venture Capital (VC): Nearly one in five (19%) CFOs, particularly those working with physician groups, plan to explore PE and VC investment as avenues toward scaling, sharing services, and safeguarding succession planning.

Service Line Investment Plans

There are still many areas where CFOs are intending to increase investment, but changed market conditions mean that some core areas of healthcare may see decreased investment as the industry realigns:

1. Specialty Services: Fifty-two percent of CFOs plan to increase their investments in specialty services like cardiology, oncology, and dermatology, while 23% of CFOs intend to partner with a capital provider or operator.

2. Service Expansion: Home care (51%), virtual/telehealth (48%), and ambulatory service centers (49%) are also priority areas for investment as institutions continue to expand and maintain access to healthcare outside of traditional hospital and clinic settings.

3. Primary Care: Although primary care remains at the heart of the healthcare industry, many CFOs (42%) have in fact signaled an intent to reduce investment in this area, reassessing their primary care strategies due to significant cash flow pressures and ongoing realignment as the retail market gains ground.

Want to know more about healthcare leaders’ plans for the year ahead? Get more insights and data in BDO’s 2024 Healthcare CFO Outlook Survey.

Where are you planning on increasing investment in your organization this year? Let me know in the comments below.

This week, a health system CFO referenced the thoughts we shared last week about many hospitals rethinking physician employment models, and looking to pull back on employing more doctors, given current financial challenges. He said, “We’ve employed more and more doctors in the hope that we’re building a group that will allow us to pivot to total cost management.

But we can’t get risk, so we’ve justified the ‘losses’ on physician practices by thinking we’re making it up with the downstream volume the medical group delivers.

But the reality now is that we’re losing money on most of that downstream business. If we just keep adding doctors that refer us services that don’t make a margin, it’s not helping us.”

While his comment has myriad implications for the physician organization, it also highlights a broader challenge we’ve heard from many health system executives: a smaller and smaller portion of the business is responsible for the overall system margin.

While the services that comprise the still-profitable book vary by organization (NICU, cardiac procedures, some cancer management, complex orthopedics, and neurosurgery are often noted), executives have been surprised how quickly some highly profitable service lines have shifted. One executive shared, “Orthopedics used to be our most profitable service line. But with rising labor costs and most of the commercial surgeries shifting outpatient, we’re losing money on at least half of it.”

These conversations highlight the flaws in the current cross-subsidy based business model. Rising costs, new competitors, and a challenging contracting environment have accelerated the need to find new and sustainable models to deliver care, plan for growth and footprint—and find a way to get paid that aligns with that future vision.