Economists say in an ideal world, different hospitals will specialize in different forms of care while others — particularly in rural areas — will focus on providing basic services.

Why it matters:

The hospital of the future will likely mean a significantly different patient experience, in ways both obvious (it’ll have better technology) and potentially disruptive (it could require more travel).

“My own view of what it’s going to look like in the longer run is much, much fewer hospitals that are much, much bigger,” said Yale’s Cooper.

Where it stands:

Many health systems are already cutting service lines — maternity care is a common one — or closing altogether, especially rural hospitals.

To some extent, that may be OK, some experts say. The reality created by shifting demographics is that some places just don’t have the population necessary to support certain services.

Not only do the economics not work, but a handful of specialized procedures every year probably isn’t enough to keep providers well-trained.

Between the lines:

Instead of consolidation, there should be more of a divergence between hospitals that provide basic care to local communities and those that specialize in more complex care, Cooper said.

That model, of course, would mean many patients would have to travel for certain care instead of receiving it at their local hospital.

And as technology broadlychanges the consumer experience, patients will have similar expectations for their care.

“People’s gold standard is buying stuff on Amazon at 2 in the morning, and when they compare their health care experience, they say, ‘Why can’t my health care experience be more like that?'” Kaufman said.

Emerging medical technologies will also impact the care that people receive, and hospitals are positioning themselves at the forefront of that change.

“Patients right now — and in the future — can expect more care delivery that is driven by 3D modeling; predictive analytics; advanced robotics for surgeries and treatments; and personalized therapies based on genomics,” American Hospital Association president and CEO Rick Pollack wrote in a blog post last year.

Yes, but:

Hospitals that serve higher populations of vulnerable people, who are more likely to have lower-paying government insurance, are the most financially exposed.

That means if they don’t adapt, care could become even less accessible for these patients.

Some economists’ ideal version of the future may mean lower profits for health systems.

Hospitals “should do what they do best, which is inpatient care and emergency care … and other people should do things that they do best, like the physicians working together as a multi-specialty group but not part of the hospital,” said Johns Hopkins’ Anderson.

“They wouldn’t make the substantial profits they’re making, but for the nonprofits, that’s not the goal,” he added.

The bottom line:

“Is there going to be disruption? Yes,” Cooper said. “I think there’s a romanticism about local hospitals. They’re where our kids were born and where our parents spent their final days.”

“But I firmly believe the local hospital of the future is not doing everything for everyone.”

We recently spoke with a health system COO who wanted help playing out scenarios regarding the relationship between specialist physicians and their private equity (PE) partners. The system is located in one of the markets referenced in a recent study that has some of the highest levels of private equity ownership in the country. One physician group, whose doctors provide almost all the system’s coverage for a key specialty, has worked with PE partners for five years, and the relationship is not going well. “We’re hearing that many of the younger doctors want to leave. And many of the others are close to retirement,” he shared.

“We’re really concerned about what could happen if the group implodes.” The key issue: the doctors signed very restrictive noncompete agreements when they sold their practice, which could prohibit them from working in the market.

The health system would consider bringing some of the doctors into their employed medical group, but executives are worried this might be impossible for the duration of the noncompete agreements. “If these doctors can’t stay locally, we might have to rebuild that specialty from scratch. And I can’t imagine how disruptive that would be,” he worried.

When the FTC announced a proposed rule earlier this year that would ban employers from imposing noncompete agreements, many health systems reacted with alarm, fearing the that the freedom to move would lead to frequent bidding wars, ultimately driving up the cost of physician talent in the market.

But the situation shows how perspectives would change depending on who holds the noncompete.

Mid-sized markets like this one, where coverage for several specialties may come from single groups, are particularly vulnerable. Regardless, this situation highlights the need to diversify physician relationships to guard against getting caught in a “coverage crisis”.

Academic medicine combines healthcare with higher education, the two sectors of the American economy that have exhibited outsized cost growth during the past 50 years. The result is a stunning disconnection between the business practices of academic medical centers (AMCs) and the supply-demand dynamics reshaping healthcare delivery.

Market, technological and regulatory forces are pushing the healthcare industry to deliver higher-value care that generates better outcomes at lower costs. A parallel movement is shifting resources out of specialty and acute care services into primary, preventive, behavioral health and chronic disease care services. In the process, care delivery is decentralizing and becoming more consumer-centric.

AMCs Double Down

Counter to these trends, academic medicine is doubling down on high-cost, centralized, specialty-focused care delivery. Privilege has its price. Several AMCs — including Mass General Brigham, IU Health, UCSF, Ohio State and UPMC — are undertaking multibillion-dollar expansions of their existing campuses. Collectively, AMCs expect American society to fund their continued growth and profitability irrespective of cost, effectiveness and contribution to health status.

Despite being tax-exempt and having access to a large pool of free labor (residents), AMCs charge the highest treatment prices in most markets. [1] Archaic formulas allocate residency “slots” and lucrative Graduate Medical Education payments (over $20 billion annually) disproportionately into specialty care and more-established AMCs. Given their cushy funding arrangements, it’s no wonder AMCs fight vigorously to maintain an out-of-date status quo.

Legacy practices from the early 1900s still dominate medical education, medical research and clinical care. Like tenured faculty, academic physicians manage their practices with little interference. Clinical deans rule their departments with a free hand. With few exceptions, interdisciplinary coordination is an oxymoron. The result is fragmented care delivery that tolerates duplication, medical error and poor patient service.

Irresistible consumerism confronts immovable institutional inertia. As exhibited by substantial operating losses at many AMCs, their foundations are beginning to crack. [2]

Medicine’s Rise from Poverty to Prosperity

In his 1984 Pulitzer Prize-winning work, Paul Starr chronicles the social transformation of American medicine during the 19th and 20th centuries. Prior to the 1900s, doctors had low social status. Most care took place in the home. Pay was low. The profession lacked professional standards. There were too many quacks. Most doctors lived hand-to-mouth.

As the century turned, several cultural, economic, scientific and legal developments converged to elevate the profession’s status in American society. Stricter licensing reduced the supply of physicians and closed most existing medical schools. Legislation and legal rulings restricted corporate ownership of medical practices and enshrined physicians’ operating autonomy. Scientific breakthroughs gave medicine more healing power.

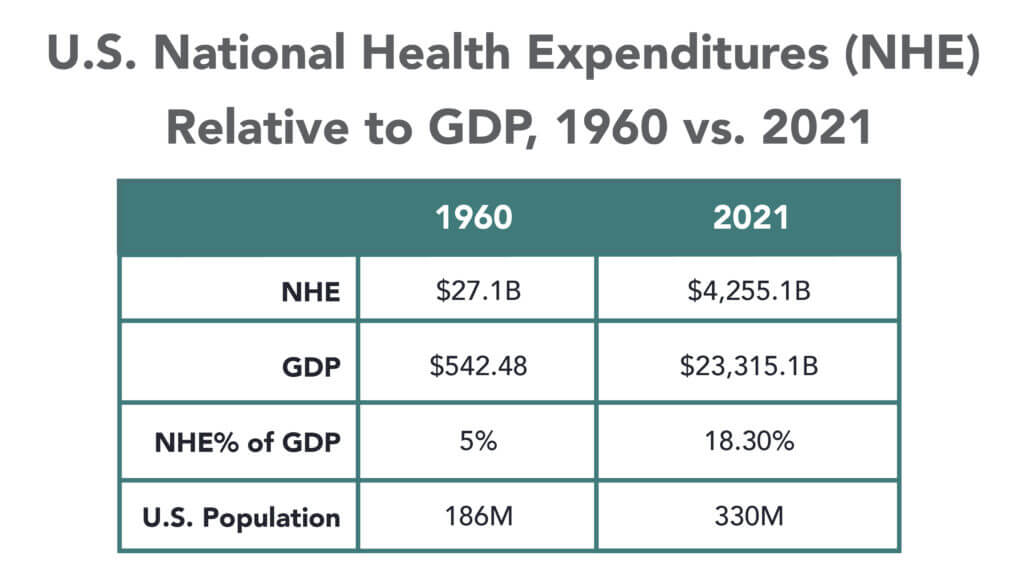

Through the decades that followed, the American Medical Association and state medical societies frustrated external attempts to control medical delivery externally and institute national health insurance. They insisted on fee-for-service payment and the absolute right of patients to choose their doctors. These are causal factors underlying healthcare’s skyrocketing cost increases, growing from 5% of the U.S. gross domestic product (GDP) in 1960 to over 18% in 2021.

Academic and community-based physicians have always had a tenuous relationship. Status and prestige accompany academic affiliations. Academic practices require referrals from community physicians but rarely consult with them on treatment protocols. For their part, community physicians marvel at the lack of market awareness exhibited by academic practices. They have tolerated one another to perpetuate collective physician control over healthcare operations.

Incomes and prestige for both community and academic physicians rose as the medical profession limited practitioner supply, established payment guidelines, encouraged specialization, controlled service delivery and socialized capital investment. One hundred years later, the business of healthcare still exhibits these characteristics. Gleaming new medical centers testify to the profession’s success in socializing capital investment and maintaining autonomy over hospital operations.

Entrenched beliefs and behaviors explain why most hospitals, despite their high construction costs, are largely deserted after 4 p.m. and on weekends. They explain the maldistribution of facilities and practitioners. They explain the overdevelopment of specialty care. They explain the underinvestment in preventive care, mental health services and public health.

Value-Focused Backlash Portends Reckoning

These beliefs and behaviors are contributing to AMC’s current economic dislocation. Dependent upon public subsidies and premium treatment payments to maintain financial sustainability, high-cost AMCs are particularly vulnerable to value-based competitors.

The marketplace is attacking inefficient clinical care with tech-savvy, consumer-friendly business models. Care delivery is decentralizing even as many AMCs invest more heavily in campus-based medicine. A market-based reckoning confronts academic medicine.

A visit up north illustrates the general unwillingness of academic physicians to accept market realities and their continued insistence on maintaining full control over the academic medical enterprise. It’s like watching a train wreck occur in slow motion.

Minnesota Madness

After experiencing severe economic distress, the University of Minnesota sold its University of Minnesota Medical Center (UMMC) to Fairview Health in 1997. Fairview currently operates UMMC in partnership with the University of Minnesota Physicians (UMP) under the banner of M Health Fairview.

In September 2022, Sanford Health and Fairview Health signed a letter of intent to merge. The new combined company would bear the Sanford name with its headquarters in Sioux Falls, South Dakota. Despite the opportunity to double its catchment area for specialty referrals, the University and UMP oppose the merger with Sanford. They fear out-of-state ownership could compromise the integrity of UMMC’s operations.

Fairview wants the Sanford merger to help it address massive operating losses resulting, in part, from its contractual arrangements with UMP. Negotiations between the parties have become acrimonious. Amid the turmoil, the University and UMP announced in January 2023 their intention to acquire UMMC from Fairview and build a new state-of-the-art medical center on the University’s Minneapolis campus.

The University has named this proposal “MPact Health Care Innovation.” It calls for the Minnesota state legislature to fund the multibillion-dollar cost of acquiring, building and operating the new medical enterprise. Typical of academic medical practices, UMP expects external sources to pony up the funding to support their high-cost centralized business model while they continue to call the shots.

The arrogance and obliviousness of the University’s proposal is staggering. Minnesota struggles with rising rates of chronic disease and inequitable healthcare access for low-income urban and rural communities. The idea that a massive governmental investment in academic medicine will “bridge the past and future for a healthier Minnesota” as the MPact tagline proclaims is ludicrous.

Out of Touch

Like the rest of the country, Minnesota is experiencing declining life expectancy. Despite spending more than double the average per-capita healthcare cost of other wealthy countries, the United States scores among the worst in health status measures. Spending more on high-end academic medicine won’t change these dismal health outcomes. Spending more on preventive care, health promotion and social determinants of health could.

The real gem in the University of Minnesota’s medical enterprise is its medical school. It has trained 70% of the state’s physicians. It ranks third and fourth nationally in primary care and family medicine. It is advancing a progressive approach to interdisciplinary and multi-professional care.

If the Minnesota state legislature really wants to advance health in Minnesota, it should expand funding for the University’s aligned health schools and community-based programs without funding the acquisition and expansion of the University’s clinical facilities.

No Privilege Without Performance

Our nation must stop enabling academic medicine’s excesses. Funding AMCs’ insatiable appetite for facilities and specialized care delivery is counterproductive. It is time for academic medicine to embrace preventive health, holistic care delivery and affordable care access.

Privilege comes with responsibility. AMCs that resist the pivot to value-based care and healthier communities deserve to lose market relevance.

America has the means to create a healthier society. It requires shifting resources out of healthcare into public health. We must have the will to make community-based health networks a reality. It starts by saying no to needless expansion of acute care facilities.

As the nation’s leading provider of retail healthcare, CVS Health partners with hospitals and health systems in many local markets.

The health systems assist providers at CVS MinuteClinic locations and accept referrals from patients needing a higher level of care. Here are CVS’ clinical affiliates, according to its website:

Walgreens’ growing U.S. healthcare segment is continuing to bolster the retail health chain’s financial performance. The business, which includes value-based provider VillageMD, recorded $1.6 billion in sales in the second quarter, an increase of $1.1 billion from last year.

VillageMD sales were up 30%, including a boost from its recent acquisition of medical group Summit Health. Specialty pharmacy Shields Health Solutions grew sales 41%, while at-home care provider CareCentrix’s sales were up 25%.

Thanks in part to a jump in revenue in its healthcare segment, Walgreens’ results beat Wall Street expectations even as profit declined more than 20% amid lower COVID-19 vaccine volumes and test sales, higher salary costs, opioid litigation charges and costs associated with its $3.5 billion investment in its Summit acquisition.

Dive Insight:

Walgreens has been working to expand its business scope beyond pharmacies to more consumer-centric healthcare, and has acquired a number of companies to build out its growing U.S. healthcare division.

In its earnings results for the second quarter ended Feb. 28, the business reported gross profit of $32 million, as income from Shields and CareCentrix was offset by VillageMD expansion costs. VillageMD added 133 clinics compared to the second quarter last year.

“With the closing of VillageMD’s acquisition of Summit Health, [Walgreens] is now one of the largest players in primary care,” CEO Roz Brewer said in the company’s earnings release on Tuesday.

VillageMD also acquired a Connecticut-based medical group in March for an undisclosed amount. That group, called Starling Physicians, operates more than 30 primary care and multi-specialty practices across the state.

Starling “will contribute heavily to revenue and EBITDA growth in the second half of 2023,” said Walgreens CFO James Kehoe on a Tuesday morning call with investors. “Overall, the primary care business and the specialty care business is doing really, really well.”

Despite the recent deals, Walgreens is moving beyond its peak investment period in healthcare, management said on the call. VillageMD, for example, plans to concentrate growth and investments in specific markets where it can be “hyper-relevant” moving forward, according to Walgreens President John Standley.

Newport Beach, Calif.-based Hoag is spending $1 billion on a project that will add two specialty hospitals and expand its Sand Canyon Medical Center in Irvine, The Orange County Register reported Nov. 14.

Once completed, the project will have added between 1,000 to 1,500 employees, many of whom have specialized jobs and training, according to the report.

The specialty hospitals — which will focus on women’s health, digestive illnesses and cancer — will have inpatient and outpatient facilities. Operating rooms will be housed in a new building, and pharmacy and labs in another. The project will feature six new buildings, including 155 inpatient beds, eight operating rooms and 120,000 square feet of outpatient facilities.

Construction is expected to be completed by 2025.

In 2025, the city is also expected to see the opening of UC Irvine’s $1.3 billion medical complex with a full-service hospital. Earlier this year, City of Hope opened an outpatient cancer center and is now building an adjacent cancer-focused hospital, which is also set to open in 2025.

Healthcare mergers reached a record-high $19.2 billion in total transacted revenue in the second quarter of this year, led by the planned tie-up of Advocate Aurora Health and Atrium Health and several other large deals, according to the latest quarterly M&A report from Kaufman Hall.

Still, the number of healthcare transactions announced during the second quarter remained below pre-pandemic levels at just 13 deals, one more than the record-low total seen in the first quarter of this year. Activity so far in 2022 underscores what could be a longer-term shift toward fewer but larger hospital deals, the industry consultants said.

Kaufman Hall also predicted continued interest in partnerships between health systems and skilled nursing facilities that can offer new services or more specialized care. Such facilities can support patients’ earlier discharge from inpatient care to a lower-cost setting and can help reduce hospital re-admissions, the report said.

Dive Insight:

Dealmaking in the first half of the year continues a sluggish pace established in 2021, when just 49 health system mergers were announced all year. Last year’s tally marked the lowest annual deal total in a decade, according to Kaufman Hall.

But deals are getting larger. The second quarter’s $19.2 billion in transacted revenue is more than double the total of $8.5 billion seen in the second quarter of 2021, when a similar number of transactions was announced.

Megamergers, in which the seller’s annual revenue tops $1 billion, remain an ongoing trend. Kaufman Hall tracked two such deals in the second quarter: the Advocate-Atrium transaction and Trinity Health’s planned acquisition of Iowa-based MercyOne.

The second quarter saw two additional transactions with smaller-party revenue above $500 million: Bellin Health System’s merger with Gundersen Health System and George Washington University Hospital’s combination with Universal Health Services.

All told, the average size of the smaller party in a deal reached a record $1.5 billion in the second quarter. This was more than double 2021’s record average size of $619 million, Kaufman Hall found.

A couple of recent transactions illustrate the trend toward partnerships with skilled nursing facilities, the report noted. Hackensack Meridian Health announced in late March that the majority of its long-term care facilities would be acquired by Complete Care, and in April, Virtua Health announced the sale of its two skilled nursing facilities to Tryko Partners. Kaufman Hall advised Virtua Health in the transaction.

As we reported recently, healthcare M&A hit record highs in the first quarter of 2021—with deal activity in the physician practice space surging 87 percent. The graphic above highlights private equity firms’ increasing investment in the sector over the last five years. Both the number and size of PE-backed healthcare deals have increased substantially from 2015 to 2020, up 39 and 45 percent respectively.

In 2020, physician practices and services comprised nearly a fifth of all transactions, with PE firms driving the majority. One in five physician transactions involvedprimary care practices—a signal that investors are banking on profits to be made in the shift to value-based care models.

Meanwhile, PE firms are still rolling up high-margin specialty practices, with ophthalmology, orthopedics, dermatology, and anesthesiology groups all receiving significant funding in 2020. PE investment in physician practices will likely continue to accelerate, as investors view healthcare as a promising place to deploy readily available capital.

But we remain convinced that private equity investors have little interest in being long-term owners of practices,and will ultimately look for an exit by selling “rolled-up” physician entities to health systems or insurers.

Virtual care company Doctor on Demand and clinical navigator Grand Rounds have announced plans to merge, creating a multibillion-dollar digital health firm.

The goal of combining the two venture-backed companies, which will continue to operate under their existing brands for the time being, is to integrate medical and behavioral healthcare with patient navigation and advocacy to try to better coordinate care in the fragmented U.S. medical system.

Financial terms of the deal, which is expected to close in the first half of this year, were not disclosed, but it is an all-stock deal with no capital from outside investors, company spokespeople told Healthcare Dive.

Dive Insight:

The digital health boom stemming from the coronavirus pandemic resulted in a flurry of high-profile deals last year, including the biggest U.S. digital health acquisition of all time: Teladoc Health’s $18.5 billion buy of chronic care management company Livongo. Such tie-ups in the virtual care space come as a slew of growing companies race to build out end-to-end offerings, making them more attractive to potential payer and employer clients and helping them snap up valuable market share.

Ten-year-old Grand Rounds peddles a clinical navigation platform and patient advocacy tools to businesses to help their workers navigate the complex and disjointed healthcare system, while nine-year-old Doctor on Demand is one of the major virtual care providers in the U.S.

Merging is meant to ameliorate the problem of uncoordinated care while accelerating telehealth utilization in previously niche areas like primary care, specialty care, behavioral health and chronic condition management, the two companies said in a Tuesday release.

Grand Rounds and Doctor on Demand first started discussing a potential deal in the early days of the coronavirus pandemic, as both companies saw surging demand for their offerings. COVID-19 completely overhauled how healthcare is delivered as consumers sought safe digital access to doctors, resulting in massive tailwinds for digital health companies and unprecedented investor interest in the sector.

Equity funding in digital health globally hit an all-time high of $26.5 billion in 2020, according to CB Insights, with mental and women’s health services seeing particularly fast growth in investor interest.

Both companies reported strong funding rounds in the middle of last year, catapulting Grand Rounds and Doctor on Demand to enterprise valuations of $1.34 billion and $821 million respectively, according to private equity marketplace SharesPost. Doctor on Demand says its current valuation is $875 million.

The combined entity will operate in an increasingly competitive space against such market giants as Teladoc, which currently sits at a market cap of $31.3 billion, and Amwell, which went public in September last year and has a market cap of $5.1 billion.

Grand Rounds CEO Owen Tripp will serve as CEO of the combined business, while Doctor on Demand’s current CEO Hill Ferguson will continue to lead the Doctor on Demand business as the two companies integrate and will join the combined company’s board.

My husband, Andy, has Parkinson’s disease. A year ago, his neurologist recommended a new pill that he was to take at bedtime. We quickly learned that the medication would cost US$1,300 for a one-month supply of 30 pills. In addition, Andy could obtain the drug from only one specialty pharmacy and would have to use mail order.

This was our introduction to specialty drugs.

These medications are becoming increasingly common, though many Americans are unfamiliar with the term. In 2018, the Food and Drug Administration approved 59 new medications, of which 39 are considered specialty drugs.

Specialty drugs are generally high-cost drugs requiring special handling such as refrigeration or injection, though Andy’s did not. They treat complex conditions such as cancer and multiple sclerosis.

Specialty drugs are often available only through specialty pharmacies. In addition to filling prescriptions, these outlets provide educational and support services to patients. For example, they provide refill reminders and help patients learn how to inject their drugs.

In a forthcoming article, professor Isaac Buck and I argue that specialty drugs raise significant legal and ethical questions. These merit attention from the public and policymakers.

Specialty drug concerns

First, the term “specialty drug” is somewhat elusive and has no clear definition. In addition, government authorities and medical experts are not the ones who decide whether a medication is designated a specialty drug. Rather, the decision is entirely up to pharmacy benefit managers, or PBMs.

PBMs administer health plans’ drug benefit programs and thereby serve insurers. PBMs have been criticized for driving up health care costs. Drugs that are specialty drugs under one insurance policy are sometimes classified differently in other policies. Furthermore, some specialty drugs are simple pills that do not involve complicated instructions, and thus, it is unclear why they are categorized as specialty drugs.

The second problem is the very high cost of specialty drugs. The average price tag of the more than 300 medications that are considered specialty drugs is approximately $79,000 per year.Almost half of the dollars that Americans pay for medications are spent on specialty drugs. In fact, Medicare spent $32.8 billion on specialty drugs in 2015.

Because of these exorbitant costs, some insurers have created what they call a “specialty tier” in their health plans. In this tier, patients’ cost-sharing responsibilities are higher than they are for medications in other tiers. If your drug is placed in a specialty tier, your coinsurance payment, or the percentage of cost that you pay, may be 25% to 33% of the drug’s price.

This leads to a situation in which you may have the least generous insurance coverage for your most expensive drugs. Under some plans you might pay $10 per month for generic drugs but hundreds of dollars per month for specialty drugs. This can translate into many thousands of dollars in annual out-of-pocket costs, even for consumers with good health insurance. There are no federal regulations in the U.S. that limit drug prices or insurers’ tiering practices.

Conflict of interest and patient choice

A third problem is conflict of interest. PBMs own or co-own the top four specialty pharmacies in the U.S., which are responsible for two-thirds of nationwide specialty drug prescription revenues.

PBMs frequently require patients to purchase their medications from the specific specialty pharmacy that they own. Thus, PBMs have much to gain from designating medications as specialty drugs. Doing so may lead to significant revenues in the form of purchases at PBM-owned specialty pharmacies.

A related problem is the limiting of patient choice. Many specialty pharmacies fill prescriptions only through mail order. Consequently, patients may be restricted to using just one pharmacy and be forced to rely on the mail for delivery.

Some patients enjoy the convenience of home delivery. Others, however, prefer the traditional approach of visiting a drugstore in person. They may worry that the mail will be late, their package will be stolen, or they will be out of town when the drugs arrive. Yet, such patients do not have the option of a brick and mortar pharmacy.

Possible corrective measures

Both political parties have stated that health care costs are a priority for them. However, they have shown a limited appetite for tackling this herculean problem.

The House recently passed a bill that would enable the federal government to negotiate prices with drug manufacturers. Such negotiations could well lower specialty drug prices. The Senate, however, is unlikely to approve the bill, and Congress is unlikely to pass sweeping legislation in a divisive election year.

There has been more success at the federal level in promoting consumer choice. Medicare rules establish that Medicare plans may not force participants to use mail-order pharmacies.

In the meantime, individual states offer useful solutions. For example, some have provided patients with relief in the form of capping out-of-pocket costs. California limits consumers’ expenditures to $250 or $500 for a 30-day supply, depending on the drug type.

At least 15 states also have pharmacy choice statutes. Several ban PBM mandates that prevent patients from freely selecting their preferred qualified pharmacy. Many ban mail-order only requirements.

Some states have recognized that PBMs should not be entirely free to designate medications as specialty drugs. Because such designations can significantly disadvantage patients and may increase patients’ costs, such states have statutory definitions for the term “specialty drug.”

They generally mandate that the drug require special administration, delivery, storage or oversight. Such requirements may justify purchase from a specialty pharmacy. However, drugs without complicated instructions should not be deemed specialty drugs.

One more option that some insurers have already adopted is allowing patients to obtain just a few pills or doses for an initial trial period. Sometimes individuals quickly learn that they cannot tolerate a medication or that it is ineffective. Such “partial fill” programs can spare patients the exorbitant cost of a full 30-day specialty drug supply.

Specialty drugs contribute significantly to the American health care cost crisis. Additional state, or better yet, federal laws should be enacted to constrain PBMs’ authority over specialty drugs. We need further regulation concerning drug classification, pricing, conflicts of interest and patient choice.