Citing more severe than expected macro headwinds, Fitch revised its sector outlook for nonprofit hospitals and health systems to “deteriorating” Aug. 16.

Nonprofit hospitals have been hamstrung by labor and broader macro inflationary pressures that “are rendering the sector even more vulnerable to future stress,” Fitch senior director Kevin Holloran said in an Aug. 16 news release. Investment losses have also contributed to a rockier 2022 than anticipated, and operating metrics are down significantly compared to last year.

“While severe volume disruption to operations appears to be waning, elevated expense pressure remains pronounced,” Mr. Holloran said. “Even if macro inflation cools, labor expenses may be reset at a permanently higher level for the rest of 2022, and likely well beyond.”

Many nonprofit hospitals and health systems are expected to violate debt service coverage covenants this year, according to the news release.

Rural communities with struggling hospitals often turn to outside investors willing to take over their health care centers. Some are willing to sell the hospitals for next to nothing to companies that promise to keep them running.

ERIN, Tenn. — Kyle Kopec gets a kick out of leading tours through the run-down hospitals his boss is buying, pointing out what he calls relics of poor management left by a revolving door of operators.

For instance, at a hospital in this town of 1,700 about a 90-minute drive northwest from Nashville, the X-ray machine is beyond repair.

“This system is so old, it’s been using a floppy disk,” said Kopec, 23, marveling at the bendy black square that hardly has enough memory to hold a single digital photo. “I’ve never actually seen a floppy disk in use. I’ve seen them in the Smithsonian.”

There’s a point to exposing these rural hospitals’ state of disrepair — the company Kopec works for, Braden Health, is buying buildings worth millions of dollars for next to nothing with a promise to keep running them as health centers serving their communities. Braden for its part, thinks it can run them more effectively than the previous owners and turn a profit.

The hospitals Braden Health is taking over sit in one of the worst spots in one of the worst states for rural hospital closures. Tennessee has experienced 16 closures since 2010 — second only to the far more populous state of Texas, which has had at least 21 closures.

The local governments that own these facilities are finding that remarkably few companies — with any level of experience — are interested in buying them. And those that are willing don’t want to pay much, if anything.

Braden Health’s Kyle Kopec holds up a sample of diagnostic images left behind at an abandoned hospital they’re taking over. They have to figure out what to do with old medical records stacked in boxes.

“When you’re on the ropes or even got your head under water, it’s really difficult to negotiate with any terms of strength,” said Michael Topchik, director of the Chartis Center for Rural Health, which tracks distressed rural hospitals closely. “And so you, oftentimes, are choosing whoever is willing to choose you.”

At this point, large health systems have already acquired or affiliated with the hospitals that have the fewest problems, Topchik said. The hospitals that are left are those that other potential buyers passed on. Turning a profit on a small rural hospital with mostly older or low-income patients can be challenging. Some operators who take over rural hospitals have gotten in trouble with insurers and even law enforcement for shady billing practices.

“You can make it profitable,” Topchik said. “But it takes an awful lot to get there.”

Dr. Beau Braden, who runs Braden Health, used his savings and some inherited wealth to get into the hospital-buying business in 2020. An emergency room doctor and addiction specialist, he previously tried to build a hospital in southwestern Florida, where he owns the large rural clinic in Ave Maria. After running into regulatory roadblocks, he saw more opportunity in reopening hospitals — which brought him to Tennessee.

“A lot of people aren’t willing to put in the time, effort, energy, and work for a small hospital with less than 25 beds. But it needs just as much time, energy, and effort as a hospital with 300 beds,” Braden said. “I just see there’s a huge need in rural hospitals and not a lot of people who can focus their time doing it.”

Braden Health’s corporate headquarters has 40 employees, according to Kopec, who is Braden’s second in command as the company’s chief compliance officer. He had limited work experience in hospitals before helping lead a hospital-buying spree at Braden Health.

Braden Health is a limited liability company and privately held, so it doesn’t have to publicly share much about its financial figures. But in filings for a certificate of need that outlines why a health care facility should be allowed to operate, Braden revealed $2 million in monthly revenue from the one hospital it ran in Lexington, Tennessee, and its balance sheet showed more than $7.5 million cash on hand.

Dr. Beau Braden (left) and Kyle Kopec talk to staffers gathered at the nurse’s station inside Houston County Community Hospital in Erin, Tennessee. Braden Health bought the facility for $20,000 ― a price that is mostly paying for the one piece of medical equipment deemed to have any value, a 2016 ambulance with 180,000 miles.

Since buying that Lexington hospital in 2020, Braden Health has signed deals for three other failing or failed hospitals and has looked at acquiring at least 10 others, mostly in Tennessee and North Carolina. Braden Health’s strategy is to build mini-networks to share staff and supplies.

At the hospital in Erin, much of the facility’s equipment is older than Kopec. And he said using outdated technology has caused Medicare to penalize the hospital with reduced payments.

The attic houses a ham radio system that seemingly never got much use, Kopec said on his way out to the roof. He wanted to show how the giant HVAC system can be controlled only from a rusty side panel accessible by a ladder. Down below, an emergency room has never been used. During a recent renovation that predated Braden Health’s ownership, its doors were built too narrow for a gurney, among other design flaws.

An old operating room is temporarily housing the ER while Braden Health starts work on new renovations. The Tennessee attorney general, who must approve any sale of a public hospital to private investors, signed off in July.

To prevent this hospital’s closure in 2013, Houston County bought it for $2.4 million and raised taxes locally to subsidize operations. “We had no business being in the hospital business,” Mayor James Bridges said. “The majority of county governments do not have the expertise and the education and knowledge that it takes to run health care facilities in 2022.”

Those with the most experience, like big corporate hospital chains based in Nashville, have been getting out of the small hospital business, too.

Communities have seen unqualified managers come and go. In Decatur County, where Braden Health is also taking over the local hospital, the previous CEO was indicted on theft charges that remain pending. And the Tennessee comptroller determined the hospital helped endanger the finances of the entire county.

“You’re looking to someone who supposedly knows what to do, who can supposedly solve the issue. And you trust them, then you’re disappointed,” said Lori Brasher, a member of Decatur County’s economic development board. “And not disappointed once, but disappointed multiple times.”

Brasher expressed much more confidence in Braden Health, which she said has concrete plans to reopen, though the timing has been delayed by an unresolved insurance claim from a burst water line that flooded a wing of the hospital.

Local residents still have trouble stomaching the sticker price: $100 for a property valued at $1.4 million by the local tax assessor. In addition to that low price, Braden Health won tax breaks for committing to invest $2 million into the building.

The Houston County hospital is valued at $4.1 million by the property assessor. But the final sale price was just $20,000 — and that wasn’t for the land or the building. Kopec said the amount was for a 2016 ambulance with 180,000 miles — deemed the only equipment with any remaining value.

An agreement with Braden Health to take over the shuttered hospital in Haywood County, Tennessee, valued at $4.6 million, was a similarly symbolic payment. All told, Braden Health is getting more than $10 million worth of real estate for less than the price of an appendectomy.

Kopec contends the value for each property is essentially negative given that the hospitals require so much investment to comply with health care standards and — according to the company’s purchase agreements — must be run as hospitals. If not, the hospitals revert to the counties.

Most of the funding for restoring these facilities comes directly from Braden, who thinks people overestimate the value of hospitals his company is taking over.

“If you look honestly at a lot of transactions that take place with rural hospitals and how many liabilities are tied up with them, there’s really not a lot of value there,” he said. Braden recently paid off a $2.3 million debt with Medicare for the Houston County hospital.

He said there’s no secret sauce, in his mind, except that small hospitals require just as much diligence as big medical centers — especially since their profit margins are so thin and patient volume so low. He wants to improve technology in ways that health plans reward hospitals, limit nurse staffing when business is slow, and watch medical supply inventories to cut waste.

It’s a tall order. Braden said he can understand any skepticism, even from the hospitals’ employees. They’ve heard turnaround promises before, and even they can be wary of the care they’d get at such run-down facilities.

Still, as Kopec bounced through the Erin hospital’s halls, he greeted nurses and clerical staff by name with a confidence that belies his age and experience. He tells anyone who will listen that rural hospitals require specialized knowledge.

“They’re not the most complicated things in the world,” Kopec said. “But if you don’t know exactly how to run them, you’re just going to run them straight into the ground.”

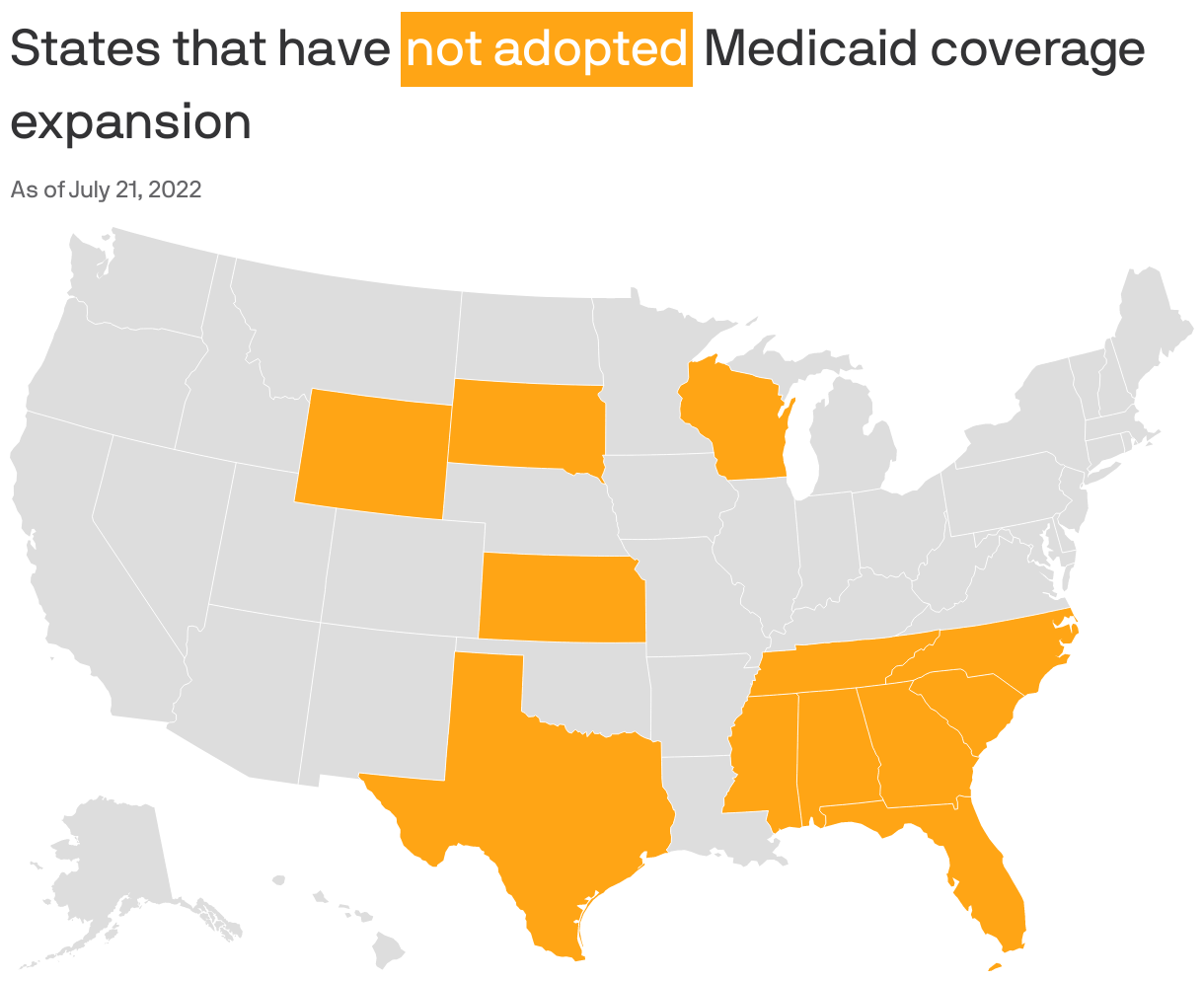

Republican-led states that have resisted expanding Medicaid for more than a decade are showing new openness to the idea.

Driving the news: In the decade-plus since the landmark Affordable Care Act was enacted, 12 states with GOP-led legislatures still have not expanded Medicaid coverage to people living below 138% of the poverty line (or nearly $19,000 annually for one person in 2022).

But there’s evidence that the political winds are changing in holdout states like North Carolina, Georgia, Wyoming, Alabama and Texas, as leaders court rural voters, assess new financial incentives and confront the bipartisan popularity of extending health care coverage.

Why it matters: Medicaid expansion, a key component of the Affordable Care Act, means increasing access to federal health insurance coverage for low-income residents, in exchange for a 10% state match of the federal spending.

Experts say it expands access to care, lowers uninsured rates and improves health outcomes for low-income populations.

More than 2 million Americans would gain coverage if the 12 states expand Medicaid, according to a 2021 estimate from the Kaiser Family Foundation.

The big picture: Some Republican states have already expanded Medicaid through executive authority or — in states where it’s legal to do so — citizen-led ballot initiatives.

Referendums on the issue passed in Nebraska, Utah and Idaho in 2018 and Missouri and Oklahoma in 2020.

Medicaid expansion is on this November’s ballot in Republican-controlled South Dakota. (Voters there in June rejected a GOP proposal to make it harder to pass.)

Be smart: In most of the remaining non-expansion states, neither ballot initiatives nor executive authority are options, leaving the legislature with the authority to make the decision.

State of play: In Georgia, as first reported by Axios Atlanta, conversations about a path forward have been taking place behind the scenes in both parties. This follows the stunning support of full expansion legislation by North Carolina’s top Republican this spring, first reported by Axios Raleigh.

“If there is a person that has spoken out more against Medicaid expansion than I have, I’d like to meet that person,” Republican Senate leader Phil Berger said at a May press conference after reversing his stance. “This is the right thing for us to do.”

Brian Robinson, former spokesman for the first Georgia governor to reject Medicaid expansion, argued in June it’s time to make the change. Politically, it would “steal an issue” from Democrats, he told Axios Atlanta.

Policy-wise, “this isn’t what we would do,” Robinson said of Medicaid’s much-criticized structure. “But Republicans can’t agree on what we would do. This is the policy and the law, and it’s not going away. It would bring home hundreds of millions from a program we’re paying into already.”

What they’re saying: “There is real momentum on Medicaid expansion in these conservative states that have been holding out,” said Melissa Burroughs of Families USA, a health care advocacy group working with partners in non-expansion states to push the policy.

Burroughs told Axios there are Republicans championing or discussing expansion in every non-expansion state, but often “political dynamics and leadership” stand in the way.

Former Alabama Gov. Robert Bentley,who had refused to expand Medicaid himself, is now urging his fellow Republicans to pass it for the benefit of rural parts of the state.

The bipartisan legislative movement on expansion this year has given advocates in Wyoming hope.

In Texas, the state with the highest percentage of uninsured residents per capita, some Republicans have co-sponsored Medicaid expansion bills. That indicates “cracks” in Republican opposition, Luis Figueroa, legislative and policy director at progressive think tank Every Texan, told Axios Austin’s Nicole Cobler and Asher Price.

Tennessee’s Republican lieutenant governorsuggested possible openness to the policy last year, though there’s been no meaningful legislative movement.

Details: The winds are shifting for several reasons, experts told Axios.

Money: The 2021 federal pandemic relief law sweetened the deal for non-expansion states, with a provision designed to offset states’ costs entirely for the first two years. Plus, Republicans’ initial fears that the federal government would pull its 90% matching funds haven’t come to pass.

COVID-19: Under the federal state of a public health emergency, Medicaid access was automatically extended. But those temporary allowances could lift next year and millions could lose coverage, putting additional pressure on leaders.

Politics: Medicaid expansion continues to be broadly popular, and the Republican campaign to “repeal and replace” the Affordable Care Act has failed in the courts and Congress — neutralizing what was once a key argument against expansion.

Health care access: As hospitals across the country close, deepening the rural health care crisis, the benefit of getting more reimbursement from additional Medicaid recipients is difficult to ignore for rural hospital revenues — though the policy is not a silver bullet to end the crisis.

The intrigue: Democrats in these states, including gubernatorial candidates like Georgia’s Stacey Abrams and Texas’ Beto O’Rourke, continue to campaign heavily on Medicaid expansion — banking on polling showing the policy to be consistently popular among the public.

“I think a lot of Republican members would like to extend Medicaid even more than they will say it,” Texas Democratic State Sen. Nathan Johnson, who has led the push for expansion there, told Axios Austin’s Cobler and Price.

He said Republicans “are handcuffed by the ideological and political constraints. They will try to do some things to help people, but they need to get over the reflexive opposition to Medicaid expansion.”

Between the lines: Even in non-expansion states, partial expansion proposals have gained traction.

Kaiser Health News found that nine of the 12 states have sought or plan to seek an extension of postpartum Medicaid coverage, including for up to one year in North Carolina, Tennessee, South Carolina and Georgia.

What we’re watching: Even in holdout states showing signs of momentum, the issue remains politically fraught.

North Carolina’s most powerful politicians say the state’s negotiations this year were torpedoed by hospitals, though Democrats and Republicans alike are optimistic about its chances next session.

The Inflation Reduction Act is law. But that doesn’t mean major health care interests are done testing their lobbying clout. Many are already lining up for year-end relief from Medicare payment cuts, regulatory changes and inflation woes.

The big picture: Year-end spending bills often contain health care “extenders” that delay cuts to hospitals that treat the poorest patients or keep money flowing to community health centers. But lawmakers may be hard-pressed to justify the price tag this time, and are seeing an unusual assortment of appeals for help.

Background: 2% Medicare sequester cuts that had been paused by the pandemic took effect last month. Another 4% cut could come at year’s end, if lawmakers don’t delay it.

These automatic reductions in spending come amid health labor force shortages, supply chain problems and other pressures that are making providers jockey for relief.

It will fall to Congress to pick winners and losers among hospitals, physicians, home health care groups, nursing homes and ambulance services. And each says the consequences of not helping are dire.

“The core question is how do they come up with the money and how do they decide to prioritize who give it to?” said Raymond James analyst Chris Meekins.

Go deeper: Hospitals arepressing hard for relief from the year-end sequester, and want Congress to extend or make permanent programs that support rural facilities and are slated to expire on Sept. 30, absent legislative action.

The American Hospital Association has estimated its members will lose at least $3 billion by year’s end.

Hospitals in the government’s discount drug program also have to be made whole after the Supreme Court unanimously overturned a huge pay cut stemming from a 2018 rule. And the industry also is seeking to reverse a planned cuts to supplementary payments for uncompensated care.

Doctors and nursing homes are among the other players lining up for relief from sequester cuts, specific Medicare payment changes that affect their businesses or new regulations.

The American Medical Association says Medicare cuts could threaten physician practices that have been racked by pandemic-induced retirements and burnout. “This is really about allowing patients and Medicare beneficiaries to continue care,” AMA President Jack Resneck told Axios.

National Association for Home Care and Hospice President Bill Dombi said over half of the home health agencies will run deficits if lawmakers don’t act. “When you have that many providers in the red, you can foresee there will be negative consequences. They’re already rejecting 20 to 30% of referrals for admissions to care, so it will be affecting patients,” said Dombi.

Ambulance services are also struggling. “Ambulance providers around the country are at a very near breaking point as we kind of walk along the ledge leading to this cliff at the end of the calendar year,” Shawn Baird, president of the American Ambulance Association and chief operating officer of Metro West Ambulance in Oregon, told Axios.

The other side: Despite Congress’ willingness to delay payment cuts, there’s not enough money to make everyone happy. And concerns about Medicare program’s solvency that emerged during the lengthy debate over the Democrats’ tax, climate and health package could dampen lawmakers’ enthusiasm for costly fixes that favor one provider group.

The continuation of the COVID-19 public health emergency and its myriad temporary payment allowances could also lessen a sense of urgency around provider relief.

The bottom line: For all the dire warnings, it’s unlikely Congress will do much until December, when it will likely pass a continuing resolution or an omnibus spending bill and could then move to delay the 4% cut.

Pharmaceutical options for both emergency contraception and abortion are available to those who can get pregnant. In this episode we take a look at the availability of these medications, how they work, and the differences between them.