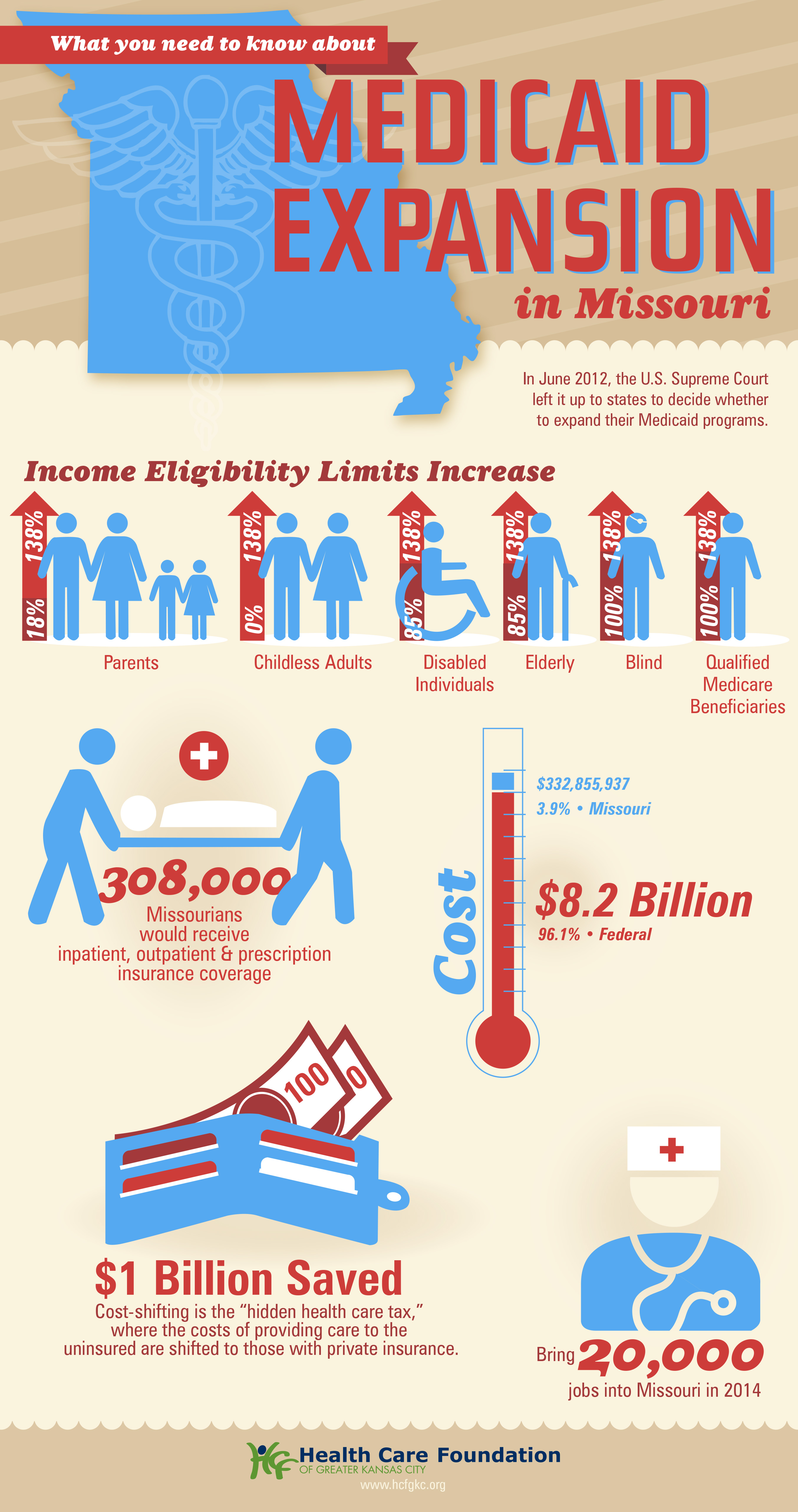

Missouri Gov. Mike Parson announced Thursday that his state would not expand Medicaid coverage to 275,000 residents who will become eligible on July 1st, despite a 2020 ballot initiative in which a majority of the state’s voters approved the expansion. Because the Missouri legislature has blocked funding for the expansion, Parson declared that the state’s Medicaid program, MO HealthNet, would run out of money if it moved forward.

The legislature’s decision to block funding was bolstered by an appeals court opinion last year, which challenged the expansion because the ballot initiative did not include a funding mechanism for widening coverage.

Under the Affordable Care Act (ACA), the federal government would have picked up 90 percent of the cost of expanding Medicaid in the state, in addition to boosting funding for existing Medicaid enrollees by 5 percent, thanks to a measure in the recent American Rescue Plan Act.

The governor’s decision leaves in place one of the strictest Medicaid eligibility standards in the nation: a family of three in Missouri must earn less than 21 percent of the federal poverty level—$5,400 per year—in order to qualify for coverage. The expansion measure would have opened the program to childless adults, and raised the eligibility limit to 138 percent of the federal poverty level.

The Missouri Hospital Association called the decision an “affront” to voters, pointing out that the state is currently running a budget surplus, and could easily allocate funds for the expansion. The status of Medicaid expansion in Missouri, which would become the 38th state to undertake expansion since the ACA’s passage, will ultimately be decided by court ruling, according to observers.

Meanwhile, like other states (mostly in the Southeast) that have resisted Medicaid expansion,Missouri will continue to see tax dollars flow out of the state to fund benefits in states that have expanded eligibility—despite the express will of voters. Given ample evidence that Medicaid expansion boosts access to care, health status, and health system sustainability,it’s nearly unfathomable that the politics of “Obamacare” continue to complicate the extension of this critical safety-net program.

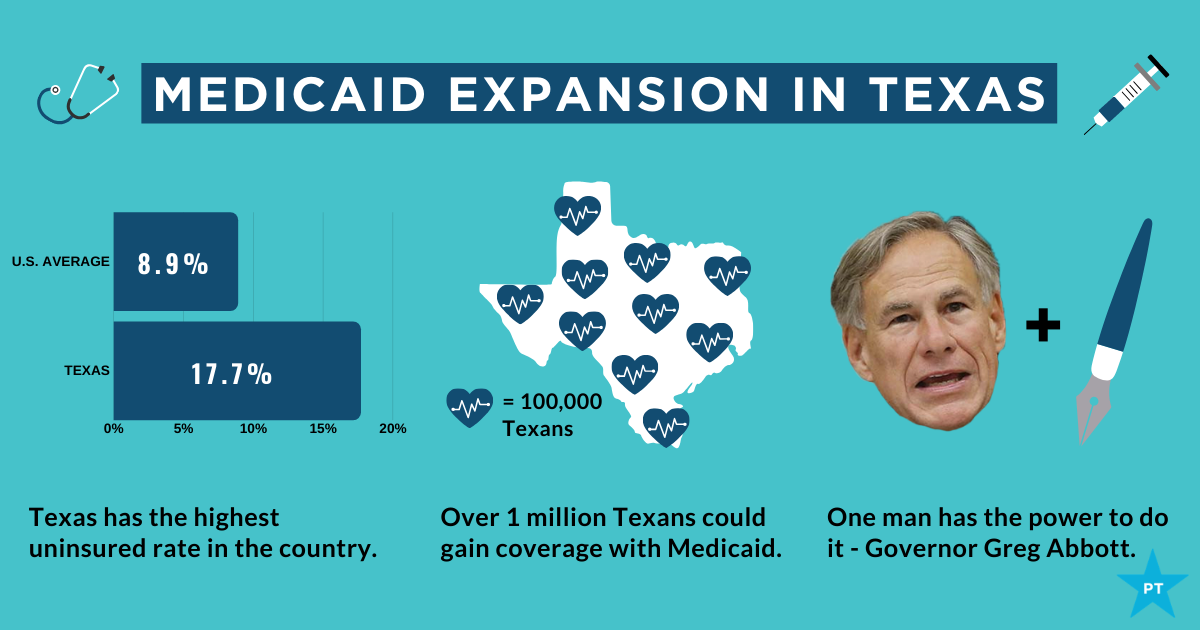

The showdown between the Biden administration and the state of Texas over Medicaid expansion continued to escalate this week. Sen. John Cornyn (R-TX) said he planned to place a hold on the confirmation of Chiquita Brooks-LaSure to become Administrator of the Centers for Medicare & Medicaid Services (CMS), until his concerns over the agency’s move last week to rescind a waiver extension previously granted by the Trump administration were addressed.

The so-called “1115 waiver”—worth more than $11B annually—would have extended by a decade Texas’ ability to use Medicaid funds to cover hospital costs for uninsured residents, rather than expanding Medicaid coverage under the Affordable Care Act (ACA). In rescinding the waiver extension, the Biden administration cited the lack of a public notice process before the waiver was granted, and said that the state’s existing waiver would instead expire next year, as previously scheduled.

Sources inside the administration told the Washington Post last week thatthe move was intended to force Texas’ hand on Medicaid expansion; the state is one of 12 that have not expanded Medicaid, leaving it with the largest share of uninsured residents of any state, with eligibility currently limited to pregnant women, children, people with disabilities, and families with monthly incomes under $300 per month, or 13.6 percent of the federal poverty level.

Enticing the dozen remaining holdout states to expand Medicaid is an important policy priority for the new administration.A key component of the recently passed American Rescue Plan Act is a package of enhanced incentives for those states to expand eligibility, offering an extended 90 percent federal match, in addition to increased funding for existing Medicaid populations.

Although none of the non-expansion states have budged yet, there has been renewed focus among state lawmakers on Medicaid expansion, including in Texas, where the idea had garnered bipartisan support. However, on Thursday, the Texas legislature voted down a proposal aimed at pushing the state toward expanding coverage for the uninsured, by an 80-68 margin. Meanwhile, the rescission of Texas’ waiver has angered the state’s Republican leadership, along with the Texas Hospital Association, whose members have benefited from the waiver’s use of funds to reimburse them for delivering uncompensated care.

While Cornyn’s hold will not ultimately stop the confirmation of the new CMS leader, the escalation on both sides over the past several days surely makes finding a compromise solution less likely. The Biden health policy team is said to be developing a new proposal, as part of an upcoming legislative package, to use the ACA marketplace to offer coverage to people in non-expansion states who might otherwise be eligible for Medicaid—yet another attempt to address one of the longest-standing points of contention stemming from the 2010 health reform law.

President Biden promised on the campaign trail to expand the Affordable Care Act to cover more of the roughly 29 million nonelderly Americans (about 11 percent of that population) who remain uninsured. He also said he’d strengthen the law by, for instance, providing an accessible and affordable public option and increasing tax credits to make it easier for people who buy insurance on their own to afford monthly premiums. Once in office, Biden immediately moved to reopen the period when people could enroll in the ACA marketplaces.

Unfortunately, the administration is paying little heed to a problem that is in many ways just as insidious as lack of insurance: underinsurance. That’s when people get too little from the insurance plans that they do have.

After passage of the ACA, the number of Americans lacking any insurance fell by 20 million, dropping to 26.7 million in 2016 — a historic low as a percentage of population. The figure began to creep up again during the Trump administration, reaching 28.9 million in 2019. That’s the problem that the current administration wants to address, and it certainly needs attention.

But according to research by the Commonwealth Fund, a foundation focused on health care, 21.3 percent of Americans have insurance so skimpy that they count as underinsured: Their out-of-pocket health-care expenses, excluding premiums, amount to at least 5 to 10 percent of household income. The limits in coverage mean their plans might provide little financial protection in a health-care crisis.

High-deductible plans offered by employers are one part of the problem. Among people covered by the companies they work for, enrollment in high-deductible health plans rose from 4 percent in 2006 to 30 percent in 2019, according to a report from the Kaiser Family Foundation. The average annual deductibles in such plans are $2,583 for an individual and $5,335 for families.

In theory, high-deductible plans, which make people spend lots of their own money before insurance kicks in, turn people into careful consumers. But research finds that people covered by such plans skip care, both unnecessary (elective cosmetic surgery, for instance) and necessary (cancer screenings and treatment, and prescriptions).Black Americans in these plans disproportionately avoid treatment, widening racial health inequities.

Health savings accountsare designed to blunt the harmful effects of high-deductible plans: Contributions by employers, and pretax contributions by individuals, help to cover costs until the deductible is reached. But not all high-deductible health plans offer such accounts, and many people in lower-wage jobs don’t have them. In the rare cases that they do, they often don’t have extra money to deposit in them.

In a November 2020 article in the journal Health Affairs, scholars affiliated with Brown University and Boston University found that enrollment in high-deductible plans had increased across all racial, ethnic and income groups from 2007 to 2018; they also found that low-income, Black and Hispanic enrollees were significantly less likely than other groups to have a health savings account — and the disparities had grown over time.

The short-term health-care plans — a.k.a. “junk” plans — that the Trump administration expanded also contribute to the problem of underinsurance. They often have low premiums but do not cover preexisting conditions or basic services like emergency health care.

Fortunately, proposals like Biden’s that make health care more accessible also tend to address the problem of underinsurance, at least in part. For example, to make individual-market insurance more affordable, Biden proposes expanding the tax credits established under the ACA. His plan calls for removing the cap on financial assistance, now set at 400 percent of the federal poverty level, in the insurance marketplaces and lowering the statutory limit on premiums to 8.5 percent of income (from nearly 10 percent).

The president also proposes to peg the size of the tax credits that subsidize premiums to the best plans on the marketplaces, the “gold” plans, rather than “silver” plans. This would increase the size of these credits, thereby making it easier for Americans to afford more-generous plans with lower deductibles.

The most ambitious Biden proposal is a public option, which would create a Medicare-like offering on marketplaces, available to anyone.Pairing this with allowing any American to opt out of their employer plan if they found a better deal on HealthCare.gov or their state marketplace — which they can’t now — would help some people escape high-deductible plans. The public option would also eliminate premiums and involve minimal to no cost-sharing for low-income enrollees — especially helpful for uninsured (and underinsured) people in states yet to expand Medicaid.

Given political realities, however, this policy may not see the light of day. So it would be best to target underinsurance directly. Most people with high-deductible plans get them through an employer. Yet unlike in the marketplace plans, the degree of cost sharing in these employer plans is the same for low-income as well as high-income employees. To deal with that problem, the government could offer incentives for employers to expand the scope of health services they cover — even in high-deductible plans. Already, many such plans exempt from the deductible some primary-care visits and generic-drug prescriptions. The list could grow to include follow-up visits and certain specialist care.

Instead of encouraging health savings accounts, the government could offer greater pretax incentives that encourage employers to absorb some of the costs that they have shifted onto their lower-income employees; that would help to prevent the insurance equity gap from widening further. The government could compensate employers that cover co-pays or other costs for their low-income employees. It could also subsidize employers that move away from high-deductible plans, at least for lower-income people.

Health insurance is complicated: More-affordable premiums are good only if they don’t bring stingy coverage. Greater investment in well-trained (and racially diverse) “navigators” — the people who help Americans enroll in plans on the federal marketplace, for example — would make it less likely that consumers would choose high-deductible plans without grasping their downsides. But it’s also important that people have options beyond risky high-deductible coverage.

The ACA expanded coverage dramatically — but the government needs to make sure that coverage amounts to more than an unused insurance card.

Small businesses are struggling to cover the high costs of healthcare for their employees after a year of COVID-19, according to a new poll sponsored by the Small Business Majority and patient advocacy group Families USA.

More than one in three small businesses owners said it’s a challenge getting coverage for themselves and their workers. That pain is particularly acute among Black, Asian American and Latino businesses, which have fewer resources than their White counterparts, SBMfound.

As a result, small businesses want policymakers to expand coverage access and lower medical costs, beyond the temporary fixes included in the sweeping $1.9 trillion American Rescue Plan passed by Congress earlier this month.

Dive Insight:

Providing health insurance can be pricey for small employers, a challenge that’s been exacerbated by the pandemic and its subsequent economic downturn.

Accessing health insurance has been a major barrier over the course of COVID-19, the national survey of 500 businesses with 100 employees or fewer in November found. The poll, conducted by Lake Research Partners for SBM and Families USA, found many such businesses have had to slash benefits during the pandemic. Among small business owners that have reduced insurance benefits, 36% have trimmed their employer contribution for medical premiums and 56% switched to a plan with a lower premium.

Additionally, one in five small business owners say they plan to change or lower coverage in the next few months, while only about a quarter have been able to maintain coverage for temporarily furloughed employees.

The situation is bleaker for minority-owned small businesses. Overall, 34% say accessing health insurance has been a top barrier during COVID-19, but that figure rises to 50%, 44% and 43% for Black, Asian American and Latino business respondents, SBM, which represents some 80,000 small businesses nationwide, said.

That’s in line with past SBM polling finding non-white entrepreneurs are more likely to face temporary or permanent closure in the next few months than their white counterparts, and are also more likely to struggle with rent, mortgage or debt repayments.

Washington did allocate a significant amount of financial aid for small businesses last year, and the ARP includes numerous provisions including increased subsidies for health insurance premiums for two years, and extended COBRA coverage for laid off employees through September.

But respondents to this latest polling urged for more long-term support.

The most popular policy proposal was bringing down the cost of prescription drugs, with 90% of businesses saying they supported the measure and 54% saying they were in strong support. Protecting coverage for people with pre-existing conditions was also popular, with 87% of small business owners in total support and 51% strongly supporting.

Three-fourths of small business owners strongly support a public health insurance option, while 73% support expanding Medicaid eligibility in all states and 66% support letting people buy into Medicare starting at age 55.

A survey of large to mid-size employers from the National Alliance of Healthcare Purchaser Coalitions published Wednesday found at least three-fourths of employers support drug price regulation, surprise billing regulation, hospital price transparency and hospital rate regulation.

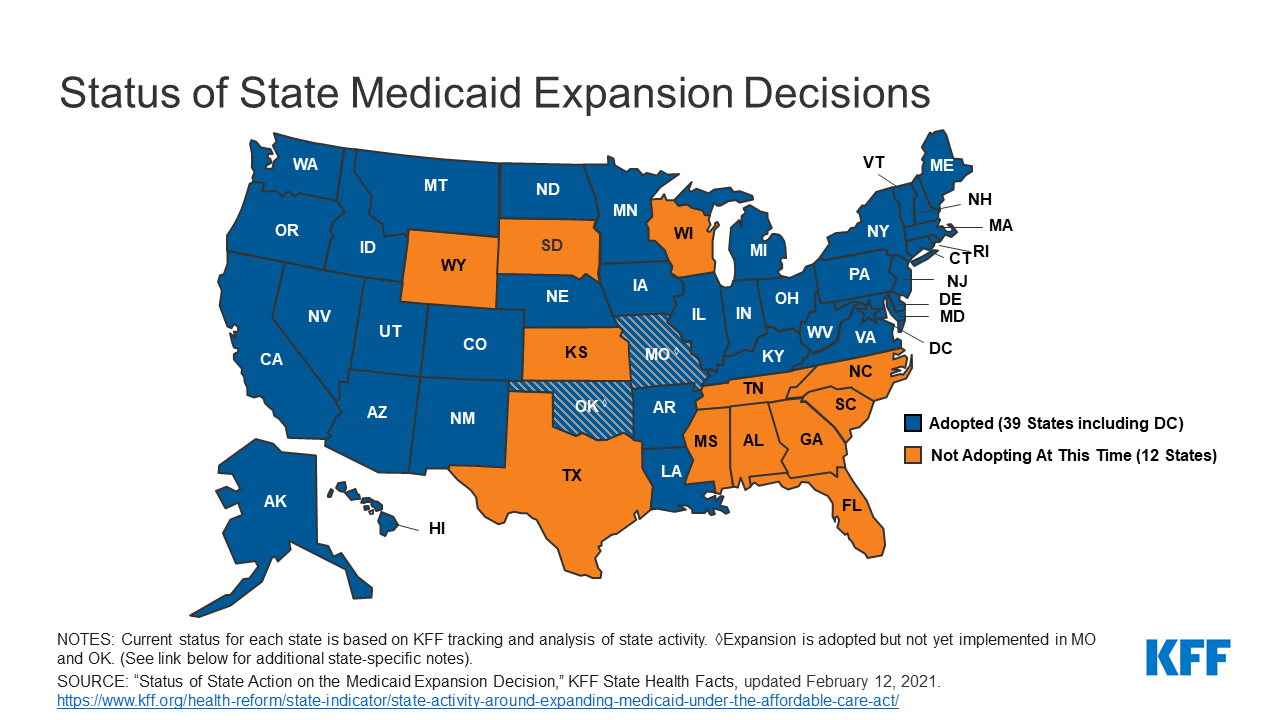

President Joe Biden has an unexpected opening to cut deals with red states to expand Medicaid, raising the prospect that the new administration could extend health protections to millions of uninsured Americans and reach a goal that has eluded Democrats for a decade.

The opportunity emerges as the covid-19 pandemic saps state budgets and strains safety nets. That may help break the Medicaid deadlock in some of the 12 states that have rejected federal funding made available by the Affordable Care Act, health officials, patient advocates and political observers say.

Any breakthrough will require a delicate political balancing act. New Medicaid compromises could leave some states with safety-net programs that, while covering more people, don’t insure as many as Democrats would like. Any expansion deals would also need to allow Republican state officials to tell their constituents they didn’t simply accept the 2010 health law, often called Obamacare.

“Getting all the remaining states to embrace the Medicaid expansion is not going to happen overnight,” said Matt Salo, executive director of the nonpartisan National Association of Medicaid Directors. “But there are significant opportunities for the Biden administration to meet many of them halfway.”

Key to these potential compromises will likely be federal signoff on conservative versions of Medicaid expansion, such as limits on who qualifies for the program or more federal funding, which congressional Democrats have proposed in the latest covid relief bill.

But any deals would bring the country closer to fulfilling the promise of the 2010 law, a pillar of Biden’s agenda, and begin to reverse Trump administration efforts to weaken public programs, which swelled the ranks of the uninsured.

“A new administration with a focus on coverage can make a difference in how these states proceed,” said Cindy Mann, who oversaw Medicaid in the Obama administration and now consults extensively with states at the law firm Manatt, Phelps & Phillips.

Medicaid, the half-century-old health insurance program for the poor and people with disabilities, and the related Children’s Health Insurance Program cover more than 70 million Americans, including nearly half the nation’s children.

Enrollment surged following enactment of the health law, which provides hundreds of billions of dollars to states to expand eligibility to low-income, working-age adults.

However, enlarging the government safety net has long been anathema to most Republicans, many of whom fear that federal programs will inevitably impose higher costs on states.

And although the GOP’s decade-long campaign to “repeal and replace” the health law has largely collapsed, hostility toward it remains high among Republican voters.

That makes it perilous for politicians to embrace any part of it, said Republican pollster Bill McInturff, a partner at Public Opinion Strategies. “A lot of Republican state legislators are sitting in core red districts, looking over their shoulders at a primary challenge,” he said.

Many conservatives have called instead for federal Medicaid block grants that cap how much federal money goes to states in exchange for giving states more leeway to decide whom they cover and what benefits their programs offer.

Many Democrats and patient advocates fear block grants will restrict access to care. But just before leaving office, the Trump administration gave Tennessee permission to experiment with such an approach.

“It’s a frustrating place to be,” said Tom Banning, the longtime head of the Texas Academy of Family Physicians, which has labored to persuade the state’s Republican leaders to drop their opposition to expanding Medicaid.“Despite covid and despite all the attention on health and disparities, we see almost no movement on this issue.”

Some 1.5 million low-income Texans are shut out of Medicaid because the state has resisted expansion, according to estimates by KFF. (KHN is an editorially independent program of KFF.)

An additional 800,000 people are locked out in Florida, which has also blocked expansion.

Two million more are caught in the 10 remaining holdouts: Alabama, Georgia, Kansas, Mississippi, North Carolina, South Carolina, South Dakota, Tennessee, Wisconsin and Wyoming.

Advocates of Medicaid expansion, which is broadly popular with voters, believe they may be able to break through in a handful of these states that allow ballot initiatives, including Mississippi and South Dakota.

Since 2018, voters in Idaho, Nebraska, Utah, Oklahoma and Missouri have backed initiatives to expand Medicaid eligibility, effectively circumventing Republican political leaders.

“The work that we’ve done around the country shows that no matter where people live — red state or blue state — there is overwhelming support for expanding access to health care,” said Kelly Hall, policy director of the Fairness Project, a nonprofit advocacy group that has helped organize the Medicaid measures.

But most of the holdout states, including Texas, don’t allow citizens to put initiatives on the ballot without legislative approval.

And although Florida has an initiative process, mounting a ballot campaign there is challenging, as political advertising is expensive. Unlike in many states, Florida’s leading hospital association hasn’t backed expansion.

Another route for expansion: compromises that could win over skeptical Republican state leaders and still get the green light from the Biden administration.

The Obama administration approved conservative Medicaid expansion in Arkansas, which funneled enrollees into the commercial insurance market, and in Indiana, which forced enrollees to pay more for their medical care.

Money is a major focus of current talks in several states, according to health officials, advocates and others involved in efforts across the country.

The health law at first fully funded Medicaid expansion with federal money, but after the first three years, states had to begin paying part of the tab. Now, states must come up with 10% of the cost of expansion.

Even that small share is a challenge for states, many of which are reeling from the economic downturn caused by the pandemic, said David Becker, a health economist at the University of Alabama-Birmingham who has assisted efforts to expand Medicaid in that state.

“The question is: Where do we get the money?” Becker said, noting that some Republicans may be open to expanding Medicaid if the federal government pays the full cost of the expansion, at least for a year or two.

Other efforts to find ways to offset state costs are underway in Kansas and North Carolina, which have Democratic governors whose expansion plans have been blocked by Republican state legislators. Kansas Gov. Laura Kelly this month proposed using money from the sale and taxation of medical marijuana.

Some Democrats in Congress are pushing to revise the health law to provide full federal funding to states that expand Medicaid now. Separately, in the stimulus bill unveiled last week, House Democrats proposed an additional boost in total Medicaid aid to states that expand.

Other Republicans have signaled interest in partly expanding Medicaid, opening the program to people making up to 100% of the federal poverty level, or about $12,900, rather than 138%, or $17,800, as the law stipulated.

The Obama administration rejected this approach, but the idea has gained traction in several states, including Georgia.

It’s unclear what kind of compromises the new administration may consider, as Biden has yet to even nominate someone to oversee the Medicaid program.

Some Democrats say it’s time to give up the search for middle ground with Republicans on Medicaid.

A better strategy, they say, is a new government insurance plan, or public option, for people in non-expansion states, a strategy Biden endorsed on the campaign trail.

“Democrats can no longer countenance millions of Americans living in poverty without insurance,” said Chris Jennings, a Democratic health care strategist who worked in the White House under Presidents Bill Clinton and Barack Obama and served on Biden’s transition team.

“This is why the Biden public option or other new ways to secure affordable, meaningful care should become the order of the day for people living in states like Florida and Texas.”

Young adults were among the most likely to be uninsured prior to the Affordable Care Act, but the law’s Medicaid expansion had a significant impact on those rates, according to a new study.

Research published by Urban Institute, this week shows the uninsured rate for people aged 19 to 25 declined from 30% to 16% between 2011 and 2018, while Medicaid enrollment for this population increased from 11% to 15% in that window.

The coverage increases were felt most keenly between 2013 and 2016, when many of the ACA’s key tenets were carried out, including Medicaid expansion and the launch of the exchanges, according to the study.

“Before the ACA, adolescents in low-income households often aged out of eligibility for public health insurance coverage through Medicaid or the Children’s Health Insurance Program as they entered adulthood,” the researchers wrote. “Further, young adults’ employment patterns made them less likely than older adults to have an offer of employer-sponsored insurance coverage.”

States that expanded Medicaid saw greater declines in the number of young people without insurance, the study found.

On average, the uninsured rates among young people declined from nearly 28% in 2011 to 11% in 2018, according to the analysis. In non-expansion states, however, the uninsured rate decreased from about 33% to nearly 21%.

In expansion states, Medicaid enrollment for people aged 19 to 25 rose from 12% in 2011 to close to 21%, according to the study, while enrollment in non-expansion states remained flat.

Urban’s researchers estimate that Medicaid expansion is linked to a 3.6 percent point decline in uninsurance among young people overall, and had the highest impact on young Hispanic people. Uninsurance decreased by 6 percentage points among Hispanic young people, the study found, and that population had the largest uninsured rate prior to the ACA.

“The effects of Medicaid expansion on young adults’ health insurance coverage and health care access provide evidence of the initial pathways through which Medicaid expansions could improve young adults’ overall health and trajectories of health throughout adulthood,” the researchers wrote.

“Beyond coverage and access to preventive care, Medicaid expansion may affect young adults’ health care use in ways not examined in our report. Thus, ensuring young adults have health insurance coverage and access to affordable care is a critical first step toward long-term health,” they wrote.

The groups said that Americans “deserve a stable healthcare market that provides access to high-quality care and affordable coverage for all.”

This week, a coalition of healthcare and employer groups called for achieving universal health coverage by expanding financial assistance to consumers, bolstering enrollment and outreach efforts, and taking additional steps to protect those who have lost or are at risk of losing employer-based coverage because of the economic downturn caused by the COVID-19 pandemic.

They have banded together to advocate for achieving universal coverage via expansion of the Affordable Care Act, which is supported by President Biden. Biden also intends to achieve universal coverage through a Medicare-like public option — a government-run health plan that would compete with private insurers.

WHAT’S THE IMPACT

Despite a lot of pre-election talk about universal healthcare coverage from elected officials and those vying for public office, achieving this has remained an elusive goal in the U.S. In a joint statement of principles, the groups said that Americans “deserve a stable healthcare market that provides access to high-quality care and affordable coverage for all.”

“Achieving universal coverage is particularly critical as we strive to contain the COVID-19 pandemic and work to address long-standing inequities in healthcare access and outcomes,” the groups wrote.

The organizations support a number of steps to make health coverage more accessible and affordable, including protecting Americans who have lost or are at risk of losing employer-provided health coverage from becoming uninsured.

They also want to make Affordable Care Act premium tax credits and cost-sharing reductions more generous, and expand eligibility for them, as well as establish an insurance affordability fund to support any unexpected high costs for caring for those with serious health conditions, or to otherwise lower premiums or cost-sharing for ACA marketplace enrollees.

Also on the group’s to-do list: Restoring federal funding for outreach and enrollment programs; automatically enrolling and renewing those eligible for Medicaid and premium-free ACA marketplace plans; and providing incentives for additional states to expand Medicaid in order to close the low-income coverage gap.

THE LARGER TREND

The concept of universal coverage is gaining traction among patients thanks in large part to the COVID-19 pandemic. In fact, A Morning Consult poll taken in the pandemic’s early days showed about 41% of Americans say they’re more likely to support universal healthcare proposals. Twenty-six percent of U.S. adults say they’re “much more likely” to support such policy initiatives, while 15% say they’re somewhat more likely.

As expected, Democrats were the most favorable to the idea, with 59% saying they were either much more likely or somewhat more likely to support a universal healthcare proposal. Just 21% of Republicans said the same. Independents were somewhere in the middle, with 34% warming up to the idea of blanket coverage.

More than 21% of Republicans said they were less likely to support universal care in the wake of the COVID-19 crisis. Seven percent of independents reported the same, while for Democrats the number was statistically insignificant.

During his campaign, President Joe Biden said he supported a public option for healthcare coverage. He also pledged to strengthen the Affordable Care Act. By executive order, Biden opened a new ACA enrollment period for those left uninsured. It begins February 15 and goes through May 15.

Under the Biden Administration, the DOJ says the ACA can stand even though there is no longer a tax penalty for not having health insurance.

The Department of Justice, under the Biden Administration, has told the Supreme Court that it has changed its stance on the Affordable Care Act.

The DOJ previously filed a brief contending that the ACA was unconstitutional because the individual mandate was inseverable from the rest of the law.

Following the change in Administration, the DOJ has reconsidered the government’s position and now takes the position that the ACA can stand, even though there is no longer a mandate for consumers to have health insurance or face a tax penalty, according to a February 10 filing.

WHY THIS MATTERS

Hospitals and health systems support the change in position.

“Without the ACA, millions of Americans will lose protections for pre-existing conditions and the health insurance coverage they have gained through the exchange marketplaces and Medicaid. We should be working to achieve universal coverage and preserve the progress we have made, not take coverage and consumer protections away,” said American Hospital Association CEO and president Rick Pollack.

The Supreme Court is expected to return a decision before the end of the term in June.

THE LARGER TREND

The Supreme Court heard oral arguments on November 10, 2020 regarding whether the elimination of the tax penalty made the remainder of the ACA invalid under the law.

The DOJ sided with the Trump Administration and Republican states that brought the legal challenge, while 20 Democratic attorneys general supported the ACA and asked the court for quick resolution.