Layoffs are slowing at hospitals and health systems as margins gradually improve, but CFOs continue to focus on controlling costs — particularly on the labor and supply fronts — to secure the long-term sustainability of their organizations.

Last year was characterized by hospital and health systems big and small trimming their workforces due to financial and operational challenges.

From October 2022 through December 2023, Becker’sreported on more than 100 hospitals and health systems across the country that laid off workers, eliminated positions or reduced or closed certain facilities and services to help shore up finances.

While layoffs have been reported at some hospitals this year, workforce cuts have been occuring at a slower rate compared to last year.

Hospital revenues are up year over year as patient volumes continue to rebound. Operating margins have fluctuated in the last 12 months, from a -1.2% low in February 2023 to 5.5% highs in June and December, according to Kaufman Hall. In January, average operating and operating EBITDA margins dropped to 5.1%.

Kaufman analysts noted that too many hospitals are losing money and high-performing hospitals doing better and better, “effectively pulling away from the pack.”

Fitch Ratings has described 2024 as another “make or break” year for a significant portion of the nonprofit hospital sector, which continues to battle an ongoing “labordemic.” However, the U.S. has also avoided a recession so far, partly due to a robust healthcare job market, according to The Wall Street Journal.

Nearly a quarter of health systems are appointing new executives to lead provider compensation — a function previously headed by COOs and CFOs, according to a recent report shared with Becker’s.

That stat comes from the American Association of Provider Compensation Professionals, which recently surveyed 75 U.S. health systems and medical groups to learn more about their management methods.

Health systems have been expanding their provider networks since the late 2000s and are continuing to work toward alignment, according to the report. Previously, COOs and CFOs might have led provider compensation strategy — but the arena has grown too complex and calls for an executive presence of its own.

As such, a number of roles specific to provider compensation have emerged, from the executive director level up to the senior vice presidency. Nearly 25% of health systems surveyed have created a new executive position to develop and lead a provider compensation department; 93% of these departments have sole responsibility for their organization’s compensation design and 84% have full control of compensation strategy, from management of fair market value to contract management.

“The core function of this new resource, department, and team was to build and manage compensation models developed for physicians. For many organizations, this expanded to include advanced practice providers,” the report says. “Over the years, organizations have understood the role to be much more strategic than initially proposed, which is why organizations across the country have developed roles [specific to provider compensation].”

Below are the adjusted expenses for nonprofit, for-profit and government hospitals per inpatient day in 2022 in every U.S. state, according to the latest estimates provided by Kaiser State Health Facts.

The figures are based on information from the 2022 American Hospital Association Annual Survey. They are an estimate of the expenses incurred in a day of inpatient care and have been adjusted higher to reflect an estimate of outpatient service volumes, according to the Kaiser Family Foundation.

The foundation notes the figures are “only an estimate of expenses incurred by the hospital” for one day of inpatient care and do not substitute actual charges or reimbursement for care provided.

National average Nonprofit hospitals: $3,167 For-profit hospitals: $2,383 State/local government hospitals: $2,857

U.S. Hospital YTD Operating Margin Index November 2021-December 2023

The observations and questions from this chart are both interesting and required reading for hospital executives:

Why were hospitals profitable at the 4% plus level through the worst of the 2021 Covid period?

What exactly happened between December of 2021 and January of 2022 that resulted in a profitability decrease from a positive 4.2% to a negative 3.4%?

Despite the best efforts of hospital executives, overall operating margins were negative throughout calendar year 2022 and did not return to positive territory until March of 2023.

Hospital margins remained positive throughout 2023 and into 2024. However, overall margins have remained below those experienced in both 2021 and in the pre-Covid year of 2019.

The above questions and observations have proven interesting, and the ongoing numbers have proven quite useful in many quarters of healthcare. But recently I was talking with Erik Swanson, who is the leader of the Kaufman Hall Flash Report and our executive behind the data, numbers, and statistics. Erik and I were speculating about all of the above observations, but our key speculation was whether the 2023 operating margin results actually reflected a hospital financial turnaround or, in fact, were there “numbers behind the numbers” that told a different and much more nuanced story. So Erik and I asked different questions and took a much deeper dive into the Flash Report numbers. The results of that dive were quite telling:

Too many hospitals are still losing money. Despite the fact that the Operating Margin Index median for 2023 and into 2024 was over 2%, when you look harder at the Flash Report data, you find that 40% of American hospitals continue to lose money from operations into 2024.

There is a group of hospitals that have substantially recovered financially. Interestingly, the data shows over time that the high-performing hospitals in the country are doing better and better. They are effectively pulling away from the pack.

This leads to the key question: Why are high-performing hospitals doing better? It turns out that several key strategic and managerial moves are responsible for high-performing hospitals’ better and growing operating profitability:

Outpatient revenue. Hospitals with higher and accelerating outpatient revenue were, in general, more profitable.

Contract labor. Hospitals that have lowered their percentage of contract labor most quickly are now showing better operating profitability.

An important managerial fact.The Flash Report found that hospitals with aggressive reductions in contract labor were also correlated to rising wage rates for full-time employees. In other words, rising wage rates have appeared to attract and retain full-time staff which, in turn, has allowed those hospitals to reduce contract labor more quickly, all of which has led to higher profitability.

Average length of stay.No surprise here. A lower average length of stay is correlated to improved profitability. Those hospitals that have hyper-focused on patient throughput, which has led to appropriate and prompt patient discharge, have also proven this to be a positive financial strategy.

Lower financial performers have financially stagnated throughout the pandemic. The data shows that throughout the pandemic, hospitals with good financial results improved those results, but of more consequence, hospitals with poor financial performance saw that performance worsen. The Flash Report documents that the poorest financially performing hospitals currently show negative operating margins ranging from negative 4% to negative 19%. Continuation of this level of financial performance is not only unstainable but also makes crucial re-investment in community healthcare impossible.

The urban hospital/rural hospital myth. A popular and often quoted hospital comparison is that there is an observable financial divide between urban and rural hospitals. Erik Swanson and I found that recent data does not support this common perception. When you compare “all rurals” to “all urbans” on the basis of average operating margin, no statistically significant difference emerges. However, what does emerge—and is a very important statistical observation—is that the lowest performing 20% of rural hospitals are, in fact, generating much lower margins then their urban counterparts this year. It is at this lowest level of rural hospital performance where the real damage is being done.

Rural hospitals and obstetrics. The data does confirm one very important American healthcare issue: Obstetrics and delivery services are one of the leading money losers of all hospital service offerings. And the data further confirms that rural hospitals are closing obstetric departments with more frequency in order to protect the financial viability of the overall rural hospital enterprise. This is a health policy issue of major and growing consequence.

The point here is that data, numbers, and statistics matter both to setting long-term social health policy agendas and to the strategic management of complex provider organizations. But the other point is that the quality and depth of the analysis is an equally important part of the process. A first glance at the numbers may suggest one set of outcomes. However, a deeper, more careful and penetrating analysis may reveal critical quantitative conclusions that are much more telling and sophisticated and can accurately guide first-class organizational decision-making. Hopefully the analytics here are a good example of this very point.

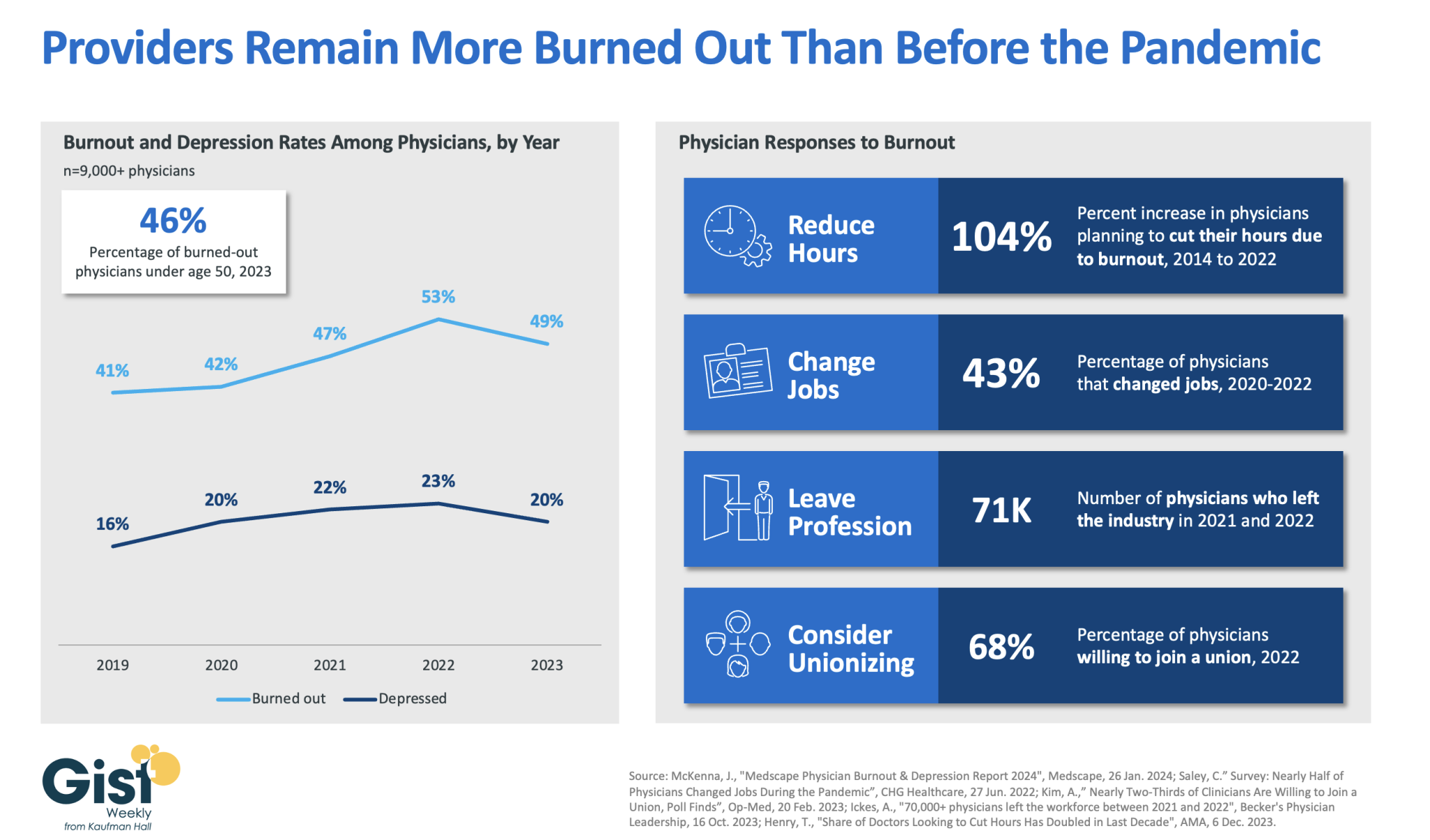

In 2023, nearly half of physicians reported feeling burned out, and a fifth reported feeling depressed. Although this does represent a drop from 2022’s peak, physicians remain more distressed than they were before the pandemic.

These numbers reveal some of the toll that the continued labor shortages, financial challenges, and payment changes of the past few years have taken on providers. In response to feeling burned out, an increased number of physicians say they are planning to cut their hours and over a third say they actually have changed jobs. Many have left the industry all together and the majority now say they are willing to join a union.

Health systems have long prioritized addressing provider burnout, but tighter operating margins have heightened both the challenge and the importance of helping to relieve it.

Continuing to find solutions to reduce administrative tasks, enhance team-based care models, and empower providers in decision-making processes are as important as ever for provider organizations today.

On Tuesday, the Centers for Medicare and Medicaid Services (CMS) published a final rule redefining how disproportionate share hospital (DSH) payments are determined.

Hospitals used to calculate their Medicaid shortfalls based on the costs and payments associated with all of their Medicaid-eligible patients, even if some of those patients used a different primary payer. Prompted by Congress to address this issue in 2021, CMS is now limiting the scope of Medicaid shortfall to only patients for whom Medicaid is their primary payer. The rule exempts safety-net hospitals providing care to the highest percentages of low-income patients, defined as those in the 97th percentile of inpatient days treating Medicare SSI (Social Security Income) recipients.

This change is expected to amount to an $8B annual reduction in DSH payments over the next four years. Congress has repeatedly delayed the implementation of these cuts, which are now set to go in effect on March 8, 2024.

The Gist: Though the formula for calculating appropriate DSH payments has always been complex, the point of the program is to provide additional support to hospitals caring for underserved, low-income populations.

This $8B cut may be targeted at hospitals with slightly better payer mixes, but it will be felt heavily by many safety-net providers reliant on the payments, especially in today’s challenging financial operating environment where over 40 percent of hospitals are still losing money on operations.

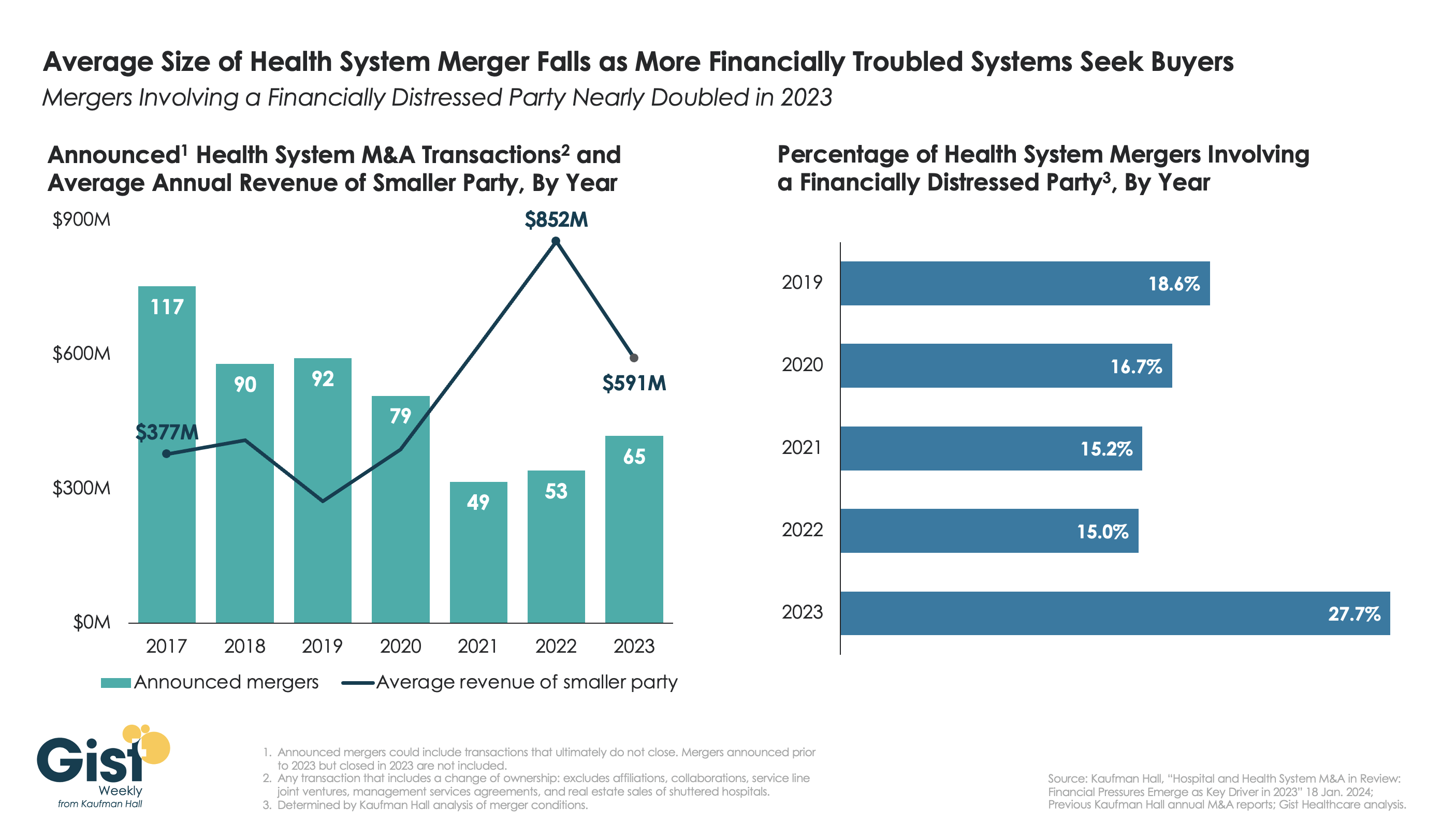

This week’s graphic highlights data from Kaufman Hall’s recently released 2023 Hospital and Health System M&A Report on the current dynamics in health system mergers and acquisitions (M&A) activity.

After a slowdown during the pandemic, 2023 saw an uptick in M&A activity with 65 announced transactions, the most since 2020. Continuing the trend of the past two years, the number of announced “mega mergers,” in which the smaller party had at least $1B in annual revenue, represented more than a tenth of total announced transactions.

However, the average size of mergers fell in 2023, as financial distress emerged as a key driver of M&A activity. The percent of mergers involving a financially distressed party spiked to nearly 28 percent in 2023, almost double the level seen in prior years.

CARES Act funding had buoyed some health systems’ balance sheets through the pandemic, but with the end of federal aid, more systems needed to seek shelter through scale.

With the median hospital operating margin still barely hitting two percent, we anticipate this heightened level M&A activity to continue in 2024 as health systems search for stronger partners that can help them stabilize financially.

If you’re a U.S. health industry watcher, it would appear the $4.5 trillion system is under fire at every corner.

Pressures to lower costs, increase accessibility and affordability to all populations, disclose prices and demonstrate value are hitting every sector. Complicating matters, state and federal legislators are challenging ‘business as usual’ seeking ways to spend tax dollars more wisely with surprisingly strong bipartisan support on many issues. No sector faces these challenges more intensely than hospitals.

In 2022 (the latest year for NHE data from CMS), hospitals accounted for 30.4% of total spending ($1.35 trillion. While total healthcare spending increased 4.1% that year, hospital spending was up 2.2%–less than physician services (+2.7%), prescription drugs (+8.4%), private insurance (+5.9%) and the overall inflation rate (+6.5%) and only slightly less than the overall economy (GDP +1.9%). Operating margins were negative (-.3%) because operating costs increased more than revenues (+7.7% vs. 6.5%) creating deficits for most. Hardest hit: the safety net, rural hospitals and those that operate in markets with challenging economic conditions.

In 2023, the hospital outlook improved. Pre-Covid utilization levels were restored. Workforce tensions eased somewhat. And many not-for-profits and investor-owned operators who had invested their cash flows in equities saw their non-operating income hit record levels as the S&P 500 gained 26.29% for the year.

In 2024, the S&P is up 5.15% YTD but most hospital operators are uncertain about the future, even some that appear to have weathered the pandemic storm better than others. A sense of frustration and despair is felt widely across the sector, especially in critical access, rural, safety net, public and small community hospitals where long-term survival is in question.

The cynicism felt by hospitals is rooted in four conflicts in which many believe hospitals are losing ground:

Hospitals vs. Insurers:

Insurers believe hospitals are inefficient and wasteful, and their business models afford them the role of deciding how much they’ll pay hospitals and when based on data they keep private. They change their rules annually to meet their financial needs. Longer-term contracts are out of the question. They have the upper hand on hospitals.

Hospitals take financial risks for facilities, technologies, workforce and therapies necessary to care. Their direct costs are driven by inflationary pressures in their wage and supply chains outside their control and indirect costs from regulatory compliance and administrative overhead, Demand is soaring. Hospital balance sheets are eroding while insurers are doubling down on hospital reimbursement cuts to offset shortfalls they anticipate from Medicare Advantage. Their finances and long-term sustainability are primarily controlled by insurers. They have minimal latitude to modify workforces, technology and clinical practices annually in response to insurer requirements.

Hospitals vs. the Drug Procurement Establishment:

Drug manufacturers enjoy patent protections and regulatory apparatus that discourage competition and enable near-total price elasticity. They operate thru a labyrinth of manufacturers, wholesalers, distributors and dispensers in which their therapies gain market access through monopolies created to fend-off competition. They protect themselves in the U.S. market through well-funded advocacy and tight relationships with middlemen (GPOs, PBMs) and it’s understandable: the global market for prescription drugs is worth $1.6 trillion, the US represents 27% but only 4% of the world population.

And ownership of the 3 major PBMs that control 80% of drug benefits by insurers assures the drug establishment will be protected.

Prescription drugs are the third biggest expense in hospitals after payroll and med/surg supplies. They’re a major source of unexpected out-of-pocket cost to patients and unanticipated costs to hospitals, especially cancer therapies. And hospitals (other than academic hospitals that do applied research) are relegated to customers though every patient uses their products.

Prescription drug cost escalation is a threat to the solvency and affordability of hospital care in every community.

Hospitals vs. the FTC, DOJ and State Officials:

Hospital consolidation has been a staple in hospital sustainability and growth strategies. It’s a major focus of regulator attention. Horizontal consolidation has enabled hospitals to share operating costs thru shared services and concentrate clinical programs for better outcomes. Vertical consolidation has enabled hospitals to diversify as a hedge against declining inpatient demand: today, 200+ sponsor health insurance plans, 60% employ physicians directly and the majority offer long-term, senior care and/or post-acute services. But regulators like the FTC think hospital consolidation has been harmful to consumers and third-party data has shown promised cost-savings to consumers are not realized.

Federal regulators are also scrutinizing the tax exemptions afforded not-for-profit hospitals, their investment strategies, the roles of private equity in hospital prices and quality and executive compensation among other concerns. And in many states, elected officials are building their statewide campaigns around reining in “out of control” hospitals and so on.

Bottom line: Hospitals are prime targets for regulators.

Hospitals vs. Congress:

Influential members in key House and Senate Committees are now investigating regulatory changes that could protect rural and safety net hospitals while cutting payments to the rest. In key Committees (Senate HELP and Finance, House Energy and Commerce, Budget), hospitals are a target. Example: The Lower Cost, More Transparency Act passed in the the House December 11, 2023. It includes price transparency requirements for hospitals and PBMs, site-neutral payments, additional funding for rural and community health among more. The American Hospital Association objected noting “The AHA supports the elimination of the Medicaid disproportionate share hospital (DSH) reductions for two years. However, hospitals and health systems strongly oppose efforts to include permanent site-neutral payment cuts in this bill. In addition, the AHA has concerns about the added regulatory burdens on hospitals and health systems from the sections to codify the Hospital Price Transparency Rule and to establish unique identifiers for off-campus hospital outpatient departments (HOPDs).” Nonetheless, hospitals appear to be fighting an uphill battle in Congress.

Hospitals have other problems:

Threats from retail health mega-companies are disruptive. The public’s trust in hospitals has been fractured. Lenders are becoming more cautious in their term sheets. And the hospital workforce—especially its doctors and nurses—is disgruntled. But the four conflicts above seem most important to the future for hospitals.

However, conflict resolution on these is problematic because opinions about hospitals inside and outside the sector are strongly held and remedy proposals vary widely across hospital tribes—not-for profits, investor-owned, public, safety nets, rural, specialty and others.

Nonetheless, conflict resolution on these issues must be pursued if hospitals are to be effective, affordable and accessible contributors and/or hubs for community health systems in the future. The risks of inaction for society, the communities served and the 5.48 million (NAICS Bureau of Labor 622) employed in the sector cannot be overstated. The likelihood they can be resolved without the addition of new voices and fresh solutions is unlikely.

PS: In the sections that follow, citations illustrate the gist of today’s major message: hospitals are under attack—some deserved, some not. It’s a tough business climate for all of them requiring fresh ideas from a broad set of stakeholders.

PS If you’ve been following the travails of Mission Hospital, Asheville NC—its sale to HCA Healthcare in 2019 under a cloud of suspicion and now its “immediate jeopardy” warning from CMS alleging safety and quality concerns—accountability falls squarely on its Board of Directors. I read the asset purchase agreement between HCA and Mission: it sets forth the principles of operating post-acquisition but does not specify measurable ways patient safety, outcomes, staffing levels and program quality will be defined. It does not appear HCA is in violation with the terms of the APA, but irreparable damage has been done and the community has lost confidence in the new Mission to operate in its best interest. Sadly, evidence shows the process was flawed, disclosures by key parties were incomplete and the hospital’s Board is sworn to secrecy preventing a full investigation.

The lessons are 2 for every hospital:

Boards must be prepared vis a vis education, objective data and independent counsel to carry out their fiduciary responsibility to their communities and key stakeholders. And the business of running hospitals is complex, easily prone to over-simplification and misinformation but highly important and visible in communities where they operate.

Business relationships, price transparency, board performance, executive compensation et al can no longer to treated as private arrangements.

“What if 10 percent, or even five percent, of the employers in our market decide to stop providing health benefits?” a Chief Strategy Officer (CSO) at a midsized health system in the Southeast recently asked.

“Their health insurance costs have been growing like crazy for 20 years. Some of these companies could easily decide to just give their employees some amount of tax-advantaged dollars and let them do their own thing.” An emerging option for employers is the relatively new individual coverage Health Reimbursement Arrangement (ICHRA), which allows employers to give tax-deductible contributions to employees to use for healthcare, including purchasing health insurance on an exchange.

According to the CSO, “What happens is this: We’ll go from getting 250 percent of Medicare for beneficiaries in a commercial group plan to getting 125 percent for beneficiaries in a market plan. I don’t know any provider with the margins to withstand that kind of shift without significant pain—certainly not us.”

The conversation shifted to a discussion about treating employers like true customers that pay generously for healthcare services, which involves increasing engagement with them and better understanding their specific problems with their employees’ healthcare. What complaints are they hearing about their employee’s difficulties with things like making timely appointments or finding after-hours care?

Provider organizations can help keep employers in the health insurance market by regularly checking in with them about their healthcare challenges, meaningfully focusing on mitigating their pain points, and exploring new kinds of mutually beneficial partnerships.

They should also carefully monitor the employer market in their region and create financial assessments of the potential impact of employers shifting employees to health insurance stipend arrangements.

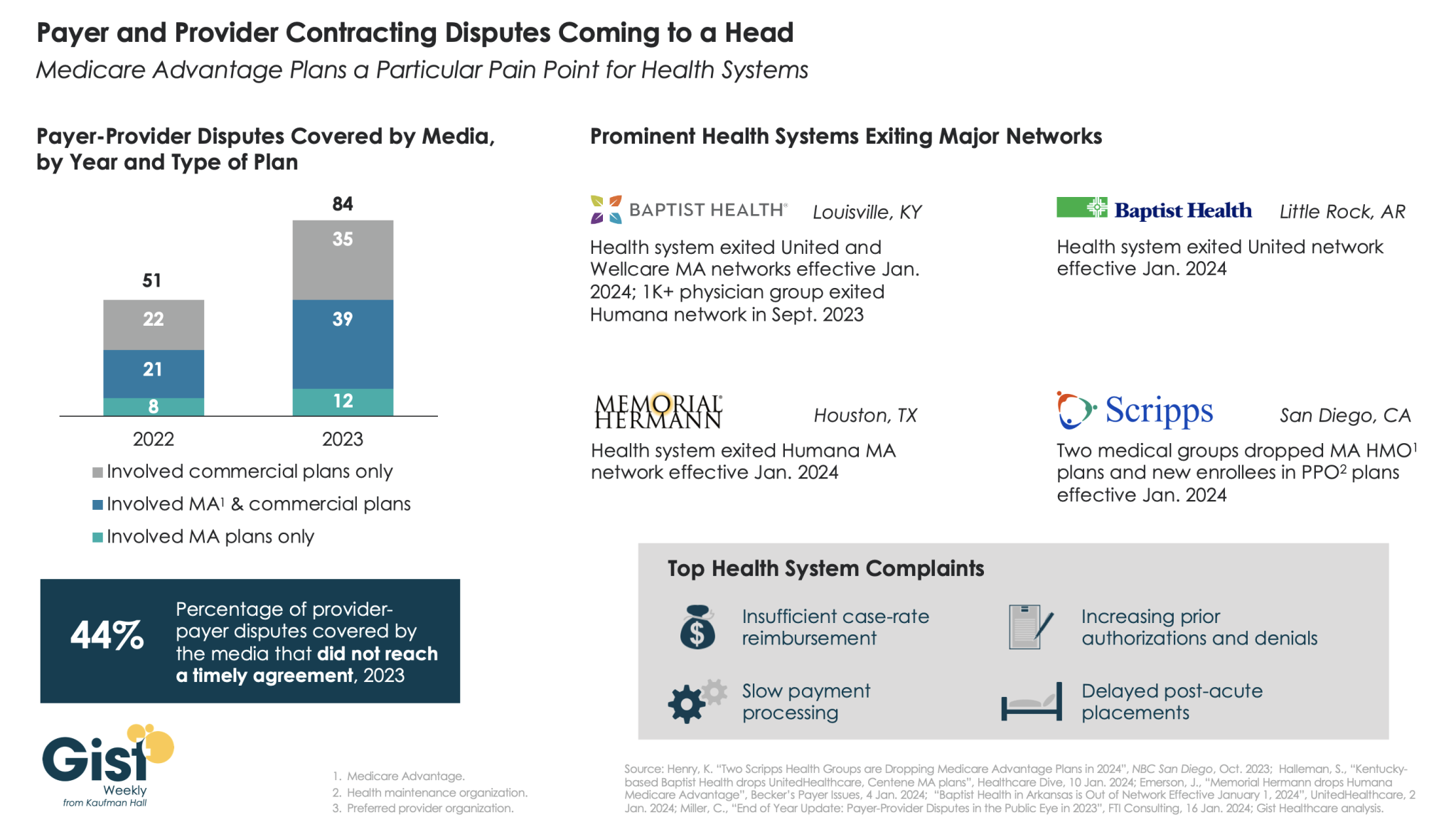

In this week’s graphic, we highlight new data on the increase in payer-provider contracting disputes covered by the media.

From 2022 to 2023, there was a 69 percent increase in the number of payer-provider contracting disputes that received media coverage. Nearly half of last year’s disputes did not reach agreement and resulted in network exits.

Large provider organizations—including Louisville, KY-based Baptist Health, Little Rock, AR-based Baptist Health, Houston, TX-based Memorial Hermann Health System, and two large medical groups affiliated with San Diego-based Scripps Health—dropped Medicare Advantage (MA) plans from at least one major payer, like United or Humana, as of Jan. 1, 2024.

Some dropped the payer’s commercial plans as well. Provider organizations leaving these networks have cited insufficient reimbursement rates and unsatisfactory business practices that drive up their cost of care delivery, especially around increased prior authorization requirements.

While contracting disputes will ultimately be influenced by the competitive strength of a given provider and payer in a particular market, it’s important for both sides to recognize thatthe patients in the middle of these disputes can be the ones most harmed when they can no longer see their trusted physicians.