The nation’s largest for-profit hospital systems by revenue — HCA Healthcare, Community Health Systems, Tenet Healthcare and Universal Health Services —reported mixed results during the third quarter of 2023, despite announcing strong demand for patient services.

With the exception of HCA, each operator reported lower profits in the third quarter compared with the same period last year. Health systems CHS and HCA reported earnings that fell short of Wall Street expectations for revenue.

Major operators posted declining profits in the third quarter compared to the same period in 2022

Q3 net income in millions, by operator

Health System

Profit

Percent Change YOY

Community Health Systems

$−91

−117%

HCA Healthcare

$1,800

59%

Tenet Healthcare

$101

−23%

Universal Health Services

$167

−9%

Admissions rose across the board compared to the same period last year: Same facility equivalent admissions rose4.1% at HCA , 3.7% at CHS and 0.6% at Tenet,and adjusted admissions at acute hospitals rose 6.8% at UHS.

Although the for-profit operators began cost containment strategies earlier this year — recognizing that rising expenses, including costs of salary and wages, were pressuring hospital profitability post-pandemic — expenses also rose, with growth in salaries and benefit costs once again pressuring most operators’ revenue.

Hospital operators faced new challenges this quarter, executives said, including increased physician staffing fees and what hospital executives characterizedas aggressive behavior from payers.

Hospitals highlight rising physician fees

Rising physician fees were a topic of concern on earnings calls this quarter, with executives reporting fees that were 15% to 40% higher compared with the same period last year.

Third-party staffing firms charge hospitals physician fees, a percentage of physicians’ salaries, on top of the salaries themselves. Physician fees are separate but related to contract labor costs, which plagued hospitals during the COVID-19 pandemic as they attempted to stem staffing shortages.

Hospitals typically contract specialty hospitalist roles — like anesthesiologists, radiologists and emergency department physicians — and incur associated staffing costs.

Physician fees at HCA, the country’s largest hospital chain, grew 20% year over year in the third quarter, according to CFO Bill Rutherford.

Physician fees were up by as much as 40% at UHS — making up 7.6% of totaloperating expenses this quarter and surpassing the company’s initial projections for the year,CEOMarc Miller said during an earnings call. Historically, physician fees accounted for about 6% of UHS’ total expenses.

Likewise, Franklin, Tennessee-based CHS attributed some of its third-quarter losses to “increased rates for outsourced medical specialists,” according to a release on the operator’s earnings.

Tenet CEO Saum Sutaria noted that physician fee expenses were up 15% year over year, but said on an earnings call that the operator had spied rising physician fees during the pandemic, and had begun efforts to contain costs — including restructuring staffing contracts and in-sourcing critical physician services.

As a result, physician fee costs at Tenet had remained “relatively flat” from the second quarter to the third quarter this year, according to the Sutaria.

Physician fee increases may be a delayed consequence of the No Surprises Act, which went into effect in January of last year, experts say.

On an earnings call, UHS CFO Steve Filton said “the industry has largely had to reset itself” in wake of the law. Tenet and CHS executives echoed the sentiment, noting that the law had disrupted staffing firms’ business models and complicated payment processes.

The No Surprises Act prevents patients who unknowingly receive out-of-network care at an in-network facility from being stuck with unexpectedbills. However, the act has had unintended ripple effects, experts say.

Staffing firms and hospitals allege that the arbitration process created to resolve disputes between providers and insurers is unbalanced and incentivizes insurers to withhold reimbursement for care. In an August survey, over half of doctors reported insurers have either ignored decisions made by arbitrators or declined to pay claims in full.

In other cases, a backlog prevents claims from being adjudicated at all. Last year, the CMS found the federal arbitration process had only reached a payment determination in 15% of cases. Federal regulators have been forced to pause and restart the arbitration process multiple times in the wake of federal court decisions challenging arbitration methodology.

Although the act went into effect more than a year ago, many hospitals are just now feeling the strain, saidLoren Adler, associate director at the Brookings Institute’s Schaeffer Initiative on Health Policy.

That’s because most insurers, hospitals and medical groups operate on three-year contracts, according to Adler. Staffing firms, which have struggled since the No Surprises Act was enacted, have passed on costs to hospitals as contracts come up for negotiation and insurers charge firms higher rates.

In the face of rising costs, some hospitals may opt to follow Tenet and CHS and in-source physicians — either to retain contracts with physicians who worked with firms that have folded or because the passing of the No Surprises Act makes outsourcing less attractive.

CHS hired 500 physicians from staffing firm American Physician Partners after the company collapsed in July. CFO Kevin Hammons said on an earnings call that hiring the physicians had saved CHS “approximately $4 million sequentially compared to the subsidy payments previously paid” to the staffing firm.

However, in-sourcing may not be an effective cost containment strategy for all operators. HCA reported it was hemorrhaging money following its first-quarter majority stake purchase of staffing firm Valesco, which brought about 5,000 physicians onto its payroll. HCA CEO Sam Hazen said the system expects to lose $50 million per quarter on the venture through 2024, citing low payments as the primary issue.

Payer problems

Hospital executives also tied quarterly losses to aggressive behavior from insurers during third-quarter earnings calls.

UHS executives said payers were improperly denying high volumes of claims and disrupting payments to its hospitals, with UHS’ Miller characterizing insurers as “increasingly aggressive” during the third quarter. Though insurers had reduced their number of claims audits, denials and patient status changes during the early stages of the pandemic, payers were increasing denials and reviews, according to UHS’ Filton.

Tenet’s Sutaria said that claims denials were “excessive and inappropriate” during a third-quarter earnings call, adding that the hospital system was working to push back on the volume of claims denials.

Their number one strategy is to provide “excellent documentation” to refute denials quickly, Sutaria said.

Still, excessive claims denials can drive up administrative costs for hospitals, according to Matthew Bates, managing director at Kaufman Hall.

“That denial creates a lot more work, because now I have to deal with that bill two, three, four times to get through the denial process,” Bates said. “It starts to rapidly eat into the operating margins… [becoming] both a cashflow problem and an administrative costs burden.”

Executives across the four for-profit operators said they planned to negotiate with insurers to receive more favorable rates and limit the number of denials in subsequent quarters.

HCA’s Hazen said that it was important for HCA to maintain its in-network status with insurers “to avoid the surprise billing and that [independent dispute resolution] process,” but that it would work with its payers to get “reasonable rates” going forward.

A Los Angeles jury awarded $41.49 million to a former nurse who said Kaiser Permanente’s hospitals and health plan retaliated against and eventually terminated her for raising issues with patient safety and care quality, MyNewsLA reported Dec. 12.

The former nurse, Maria Gatchalian, was awarded $11.49 million in compensatory damages, including $9 million for emotional distress, and $30 million in punitive damages.

“We stand by her termination and are surprised and disappointed in the verdict,” Murtaza Sanwari, senior vice president and area manager for Kaiser Permanente Woodland Hills/West Ventura County, told Becker’s in a statement. “Kaiser Permanente plans to appeal this decision and will maintain our high standards in protecting the health and safety of all our patients.”

Before her termination in 2019, Ms. Gatchalian had worked at the Kaiser Permanente Woodland Hills Medical Center since 1989, first as a registered nurse in the neonatal intensive care unit and later as a charge nurse in that unit.

According to MyNewsLA, Ms. Gatchalian said she had repeatedly raised concerns with Kaiser management about patient safety and care quality related to alleged understaffing and was discouraged from submitting formal complaints. Oakland, Calif.-based Kaiser argued in court that Ms. Gatchalian admitted she had placed her bare feet on equipment in the NICU, and the organization made the decision to terminate her following her conduct.

“We work hard to make Kaiser Permanente a great place to work and a great place to receive care,” Mr. Sanwari said. “The allegations in this lawsuit are at odds with the facts we showed in the courtroom.”

“To be clear, this charge nurse’s job was to be a leader for other nurses, ensure the standards of care were followed and to protect the neonatal babies entrusted to our care. She was terminated in 2019 following an incident where she was found sitting in a recliner in the neonatal intensive care unit, on her personal phone and resting her bare feet on an isolette with a neonatal infant inside. Neonatal intensive care units are critical care units designed for critically ill babies most often born prematurely and very susceptible to infections.

The isolette, where this nurse placed her bare feet, is a protective environment designed to shield the infant from infection causing germs. Placing her bare feet on the isolette may have created risk to the infant which could have been life threatening. Her actions were egregious and in violation of our infection control policies and standards.”

Claim denials are increasing, especially in Medicare Advantage, and it’s affecting hospital’s revenue cycles and patient care.

“We definitely are seeing an increase in denials,” said Sherri Liebl, executive director of Revenue Cycle, CentraCare Health, a large multispecialty system in Minnesota. CareCare has two acute care hospitals, seven Critical Access Hospitals and 30 standalone clinics, many of them in rural areas.

CentraCare reported a positive margin this year, but in no way realizes the profits of insurers, especially the national insurers where Liebl is having the most difficulty with claims.

CentraCare’s goal in its cost to collect – not all-around denials – is to be at 2%. The health system is closer to 7% on its cost to collect.

“The cost for our organization is exorbitant,” Lieble said.

Much of the blame for denials is falling to artificial intelligence being used in algorithms to deny claims.

UnitedHealthcare has been sued in a class action lawsuit that alleges the insurer unlawfully used an artificial intelligence algorithm to deny rehabilitative care to sick Medicare Advantage patients.

Cigna has also been suedfor allegedly using algorithms to deny claims. The lawsuit claims the Cigna PXDX algorithm enables automatic denials for treatments that do not match preset criteria, evading the legally required individual physician review process.

A Cigna Healthcare spokesperson said the vast majority of claims reviewed through PXDX are automatically paid, and that the PXDX process does not involve algorithms, AI or machine learning, but a simple sorting technology that has been used for more than a decade to match up codes. Claims declined for payment via PXDX represent less than 1% of the total volume of claims, the spokesperson said.

Industry consultant Adam Hjerpe, who formerly worked for UnitedHealth Group, said there’s nothing new about payers using artificial intelligence. AI has been used for 20 years in robotic processes, statements in Excel and algorithms, he said.

Everybody is working with good intent, Hjerpe said. There are reasonable controls in place to avoid fraud and abuse.

Claims are being denied for missing information, or for the information being out of sequence, or for the claim giving an incomplete picture of the care.

“We don’t want care delayed,” he said.

Nobody wins in claims denials, said Susan Taylor, Pega’s vice president of Healthcare and Life Sciences.

While payers save money in the short-term, in the long-term, the best arrangement is to have payers and providers work together to prevent denials, said Taylor, who has worked in healthcare for more than 25 years, starting on the health system side before moving into IT.

“There are more claims of note being denied,” Taylor said. “If you look at the ecosystem, there are a lot of opportunities for error.”

The solution is building an agility layer to streamline workflows throughout the revenue cycle, from initial claim submission to the complex denials processing stage.

WHY THIS MATTERS

Liebl said that denials have increased over the past two years and that there’s also been an uptick in payer audits months after payment has been made.

Insurers want justification for why CentraCare should keep its payments, and this is especially true for Medicare Advantage claims, she said.

One insurer said the claim didn’t meet inpatient criteria and downgraded the claim to an observation patient.

“We have a pretty good success rate as far as being able to justify we did the right care,” Liebl said.

Asked what’s driving the higher denial rates Lieble said, “Everybody wants to keep margins and expand their business. I think it comes down to profit margins, trying to keep profit margins high; we’re just trying to stay afloat.”

To combat denials and work with payers, CentraCare founded a joint operating committee to have successful partnerships. They’ve been more successful with the local Minnesota plans than the national plans, but Liebl is optimistic, she said.

“I am hopeful we can create partnerships …” she said. “Some of the denials we receive are against their payer policy. We need to be able to hold payers accountable.”

Larger health systems have a little more clout, and CentraCare is able to partner with other health systems through the Minnesota Hospital Association.

What’s being lost in all this is the patient, Liebl said. Sometimes a patient is getting a bill up to a year after a procedure.

“Sometimes the patient focus is lost when we work through some of this,” she said.

“They keep our money longer,” Liebl said. “They hold our money hostage. We have denials sitting out there for 300 days. It’s a lot of administrative burden on our part. We’ve spent a lot of money just to get the money in the door. Finally when that claim has been resolved, it’s a year later. No one wins? I think there is some winning going on one side.”

Here are 68 health systems with strong operational metrics and solid financial positions, according to reports from credit rating agencies Fitch Ratings, Moody’s Investors Service and S&P Global in 2023.

AdventHealth has an “AA” rating and stable outlook with Fitch. The rating reflects the Altamonte Springs, Fla.-based system’s strong financial profile, characterized by still-adequate liquidity and moderate leverage, typically strong and highly predictable profitability, Fitch said.

Advocate Aurora Health has an “AA” rating and stable outlook with Fitch. The Downers Grove, Ill.- and Milwaukee-based system’s rating reflects a very strong financial profile in the context of an already sound market position and geographic reach that was enhanced after merging with Charlotte, N.C.-based Atrium Health, Fitch said.

AnMed Health has an “AA-” rating and stable outlook with Fitch. The Anderson, S.C.-based system has maintained strong performance through the COVID-19 pandemic and current labor market pressures, Fitch said.

AtlantiCare has an “AA-” rating and stable outlook with Fitch. The Atlantic City, N.J.-based system has a strong balance sheet with solid liquidity position and low debt burden, Fitch said.

Atrium Health has an “AA-” rating and stable outlook with S&P Global. The Charlotte, N.C.-based system’s rating reflects a robust financial profile, growing geographic diversity and expectations that management will continue to deploy capital with discipline.

Banner Health has an “AA-” and stable outlook with Fitch. The Phoenix-based system’s rating highlights the strength of its core hospital delivery system and growth of its insurance division, Fitch said.

BayCare Health System has an “AA” rating and stable outlook with Fitch. The Tampa, Fla.-based system’s rating reflects its excellent financial profile supported by its leading market position in a four-county area and the ability to sustain a solid operating outlook in the face of inflationary sector headwinds, Fitch said.

Bayhealth has an “AA” rating and stable outlook with Fitch. The rating reflects the strength of the Dover, Del.-based system’s market positions and the stability of its financial profile, Fitch said.

Beacon Health System has an “AA-” rating and stable outlook with Fitch. The rating reflects the strength of the South Bend, Ind.-based system’s balance sheet, the rating agency said.

Berkshire Health has an “AA-” rating and stable outlook with Fitch. The Pittsfield, Mass.-based system has a strong financial profile, solid liquidity and modest leverage, according to Fitch.

Bryan Health has an “AA-” rating and stable outlook with Fitch. The rating reflects the Lincoln, Neb., system’s leading and growing market position as a regional referral center with strong expense flexibility and cash flow, Fitch said.

Cape Cod Healthcare has an “AA-” and stable outlook with Fitch. The Hyannis, Mass.-based system’s rating reflects a dominant market position in its service area and historically solid operating results, the rating agency said.

Carle Health has an “AA-” rating and stable outlook with Fitch. The rating reflects the Urbana, Ill.-based system’s distinctly leading market position over a broad service area, Fitch said.

CaroMont Health has an “AA-” rating and stable outlook with S&P Global. The Gastonia, N.C.-based system has a healthy financial profile and robust market share in a competitive region.

CentraCare has an “AA-” rating and stable outlook with Fitch. The St. Cloud, Minn.-based system has a leading market position, and its management’s focus on addressing workforce pressures, patient access and capacity constraints will improve operating margins over the medium term, Fitch said.

Children’s Health System of Texas has an “AA” and stable outlook with Fitch. The Dallas-based system’s rating reflects its solid operating performance in 2022, resulting from inpatient, outpatient and surgical volume growth, as well as one-time support from pandemic-era stimulus funding, Fitch said.

Children’s Minnesota has an “AA” rating and stable outlook with Fitch. The Minneapolis-based system’s broad reach within the region continues to support long-term sustainability as a market leader and preferred provider for children’s health care, Fitch said.

Concord (N.H.) Hospital has an “AA-” rating and stable outlook with Fitch. The rating reflects the strength of Concord’s leverage and liquidity assessment and Fitch’s assessment that two recently acquired hospitals will be strategically and financially accretive.

Cone Health has an “AA” rating and stable outlook with Fitch. The rating reflects the expectation that the Greensboro, N.C.-based system will gradually return to stronger results in the medium term, the rating agency said.

Cottage Health has an “AA-” rating and stable outlook with Fitch. The rating reflects the Santa Barbara, Calif.-based system’s leading market position and broad reach in a service area that exhibits modest population growth but consistently high demand for acute care services, Fitch said.

Deaconess Health System has an “AA” rating and stable outlook with Fitch. The Evansville, Ind.-based system demonstrated operating cost flexibility through the pandemic and recent labor and inflationary pressure, Fitch said.

Duke University Health System has an “AA-” rating and stable outlook with Fitch. Fitch projects the Durham, N.C.-based system will benefit from the integration of the former Private Diagnostic Clinic and from North Carolina’s recently enacted Medicaid expansion and Healthcare Access and Stabilization Program.

El Camino Health has an “AA-” rating and stable outlook with Fitch. The Mountain View, Calif.-based system has a history of generating double-digit operating EBITDA margins, driven by a solid market position that features strong demographics and a very healthy payer mix, Fitch said.

Franciscan Health has an “AA” rating and stable outlook with Fitch. The rating reflects the Mishawaka, Ind.-based system’s strong and stable balance sheet, favorable payer mix, and leading or near leading market share in its service areas, Fitch said.

Froedtert Health has an “AA” rating and stable outlook with Fitch. The rating reflects the Milwaukee-based system’s maintenance of a strong, albeit compressed, operating performance and a robust liquidity position, Fitch said.

Geisinger has an “AA-” credit rating and stable outlook with S&P. The Danville, Pa.-based system enjoys strong integration and value-based care experience, the ratings agency said.

Hackensack Meridian Health has an “AA-” rating and stable outlook with Fitch. The Edison, N.J.-based system’s rating is supported by its strong presence in its large and demographically favorable market, Fitch said.

Harris Health System has an “AA” rating and stable outlook with Fitch. The Houston-based system has a “very strong” revenue defensibility, primarily based on the district’s significant taxing margin that provides support for operations and debt service, Fitch said.

Hoag Memorial Hospital Presbyterian has an “AA” rating and stable outlook with Fitch. The Newport Beach, Calif.-based system’s rating is supported by a leading market position in its immediate area and very strong financial profile, Fitch said.

Intermountain Health has an “Aa1” rating and stable outlook with Moody’s. The Salt Lake City-based system’s rating is reflected by its distinctly leading market position in Utah and strong absolute and relative cash levels, Moody’s said.

Inspira Health has an “AA-” rating and stable outlook with Fitch. The Mullica Hill, N.J.-based system’s rating reflects its leading market position in a stable service area and a large medical staff supported by a growing residency program, Fitch said.

IU Health has an “AA” rating and stable outlook with Fitch. The Indianapolis-based system has a long track record of strong operating margins and an overall credit profile that is supported by a strong balance sheet, the rating agency said.

Lucile Packard Children’s Hospital has an “AA-” rating and stable outlook with Fitch. The rating reflects the Palo Alto, Calif.-based hospital’s role as a nationally known, leading children’s hospital, Fitch said. It also benefits from resilient clinical volumes and a solid market position, as well as its relationship with Stanford University and Stanford Health Care.

Kaiser Permanente has an “AA-” and stable outlook with Fitch. The Oakland, Calif.-based system’s rating is driven by a strong financial profile, which is maintained despite a challenging operating environment in fiscal year 2022.

Mayo Clinic has an “Aa2” rating and stable outlook with Moody’s. The Rochester, Minn.-based system’s credit profile characterized by its excellent reputations for clinical services, research and education, Moody’s said.

McLaren Health Care has an “AA-” rating and stable outlook with Fitch. The Grand Blanc, Mich.-based system has a leading market position over a broad service area covering much of Michigan and a track-record of profitability despite sector-wide market challenges in recent years, Fitch said.

McLeod Regional Medical Center has an “AA-” rating and stable outlook with Fitch. The rating reflects the Florence, S.C.-based system’s very strong financial profile assessment, historically strong operating EBITDA margins and its solid market position, Fitch said.

MemorialCare has an “AA-” rating and stable outlook with Fitch. The rating reflects the Fountain Valley, Calif.-based system’s strong financial profile and excellent leverage metrics despite its weaker operating performance, Fitch said.

Memorial Sloan-Kettering Cancer Center has an “AA” rating and stable outlook with Fitch. The rating reflects Fitch’s expectation that the New York City-based system’s national and international reputation as a premier cancer hospital will continue to support growth in its leading and increasing market share for its specialty services.

Midland (Texas) Health has an “AA-” rating and stable outlook with Fitch. The rating reflects Midland’s exceptional market position and limited competition for acute-care services and growing outpatient services, Fitch said.

Monument Health has an “AA-” rating and stable outlook with Fitch. The rating reflects the Rapid City, S.D.-based system’s dominant inpatient market share and excellent market position across its geographically broad service area, Fitch said.

Munson Healthcare has an “AA” rating and stable outlook with Fitch. The rating reflects the strength of the Traverse City, Mich.-based system’s market position and its leverage and liquidity profiles.

MyMichigan Health has an “AA-” rating and stable outlook with Fitch. The Midland-based system reflects the system’s market position as the largest provider of acute care services and its leading market position in a sizable geographic area covering 25 counties in mid and northern Michigan, the rating agency said.

North Mississippi Health Services has an “AA” rating and stable outlook with Fitch. The Tupelo-based system’s rating reflects its very strong cash position and strong market position, Fitch said.

NewYork-Presbyterian Hospital has an “AA” rating and stable outlook with Fitch. The rating reflects the New York City-based system’s market position as one of New York’s major academic healthcare systems with a reputation that extends beyond the region, Fitch said.

Novant Health has an “AA-” rating and stable outlook with Fitch. The Winston-Salem, N.C.-based system has a highly competitive market share in three separate North Carolina markets, Fitch said, including a leading position in Winston-Salem (46.8 percent) and second only to Atrium Health in the Charlotte area.

NYC Health + Hospitals has an “AA-” rating with Fitch. The New York City system is the largest municipal health system in the country, serving more than 1 million New Yorkers annually in more than 70 patient locations across the city, including 11 hospitals, and employs more than 43,000 people.

OhioHealth has an “AA+” rating and stable outlook with Fitch. The Columbus-based system has an exceptionally strong credit profile, very favorable leverage metrics and reliably strong profitability, Fitch said.

Orlando (Fla.) Health has an “AA-” rating and stable outlook with Fitch. The system’s upgrade from “A+” reflects the continued strength of the health system’s operating performance, growth in unrestricted liquidity and excellent market position in a demographically favorable market, Fitch said.

Phoenix Children’s Hospital has an “AA-” and stable outlook with Fitch. The rating reflects its position as a distinct leading provider of pediatric health services in a growing primary service area, Fitch said.

The Queen’s Health System has an “AA” rating and stable outlook with Fitch. The Honolulu-based system’s rating reflects its leading state-wide market position, historically strong operating performance and diverse revenue streams, the rating agency said.

Rush System for Health has an “AA-” and stable outlook with Fitch. The Chicago-based system has a strong financial profile despite ongoing labor issues and inflationary pressures, Fitch said.

Saint Francis Healthcare System has an “AA” rating and stable outlook with Fitch. The Cape Girardeau, Mo.-based system enjoys robust operational performance and a strong local market share as well as manageable capital plans, Fitch said.

Salem (Ore.) Health has an “AA-” rating and stable outlook with Fitch. The system has a “very strong” financial profile and a leading market share position, Fitch said.

Sanford Health has an “AA-” rating and stable outlook with Fitch. The Sioux Falls, S.D.-based system rating reflects its leading inpatient market share positions in multiple markets and strong overall financial profile, the rating agency said.

Stanford Health Care has an “AA” rating and stable outlook with Fitch. The Palo Alto, Calif.-based system’s rating is supported by its extensive clinical reach in the greater San Francisco and Central Valley regions and nationwide/worldwide destination position for extremely high-acuity services, Fitch said.

SSM Health has an “AA-” rating and stable outlook with Fitch. The St. Louis-based system has a strong financial profile, multi-state presence and scale, with solid revenue diversity, Fitch said.

St. Clair Health has an “AA-” rating and stable outlook with Fitch. The rating reflects the Pittsburgh-based system’s strong financial profile assessment, solid market position and historically strong operating performance, the rating agency said.

St. Tammany Parish Hospital has an “AA-” rating and stable outlook with Fitch. The rating reflects the Covington, La.-based system’s strong operating risk assessment and very strong financial profile supported by consistently robust operating cash flows, Fitch said.

Texas Medical Center has an “AA-” rating and stable outlook with Fitch. The rating reflects the Houston-based system’s profitable service enterprise, its long and collaborative relationship with strong university, nonprofit and medical industry partners, and sizable financial reserve levels, Fitch said.

TriHealth has an “AA-” rating and stable outlook with Fitch. The Cincinnati-based system’s rating reflects its broad reach, high-acuity services and stable market position in a highly fragmented and competitive market, Fitch said.

UChicago Medicine has an “AA-” rating and stable outlook with Fitch. The rating reflects the system’s broad and growing reach for high-acuity services and the considerable benefits it receives from its high degree of integration with the University of Chicago, Fitch said.

UCHealth has an “AA” rating and stable outlook with Fitch. The Aurora, Colo.-based system’s margins are expected to remain robust, and the operating risk assessment remains strong, Fitch said.

University of Kansas Health System has an “AA-” rating and stable outlook with S&P Global. The Kansas City-based system has a solid market presence, good financial profile and solid management team, though some balance sheet figures remain relatively weak to peers, the rating agency said.

Virtua Health has an “AA-” rating and stable outlook with Fitch. The rating is supported by the Marlton, N.J.-based system’s leading market position in a stable service area and the successful integration of the Lourdes Health System, Fitch said.

VHC Health has an”AA-” rating and stable outlook with Fitch. The Arlington-based system has demonstrated strong operating cost flexibility, growth in high acuity service lines and an expanding outpatient footprint, Fitch said.

WellSpan Health has an “Aa3” rating and stable outlook with Moody’s. The York, Pa.-based system has a distinctly leading market position across several contiguous counties in central Pennsylvania, and management’s financial stewardship and savings initiatives will continue to support sound operating cash flow margins when compared to peers, Moody’s said.

Willis-Knighton Health System has an “AA-” rating and stable outlook with Fitch. The Shreveport, La.-based system has a “dominant inpatient market position” and is well positioned to manage operating pressures, Fitch said.

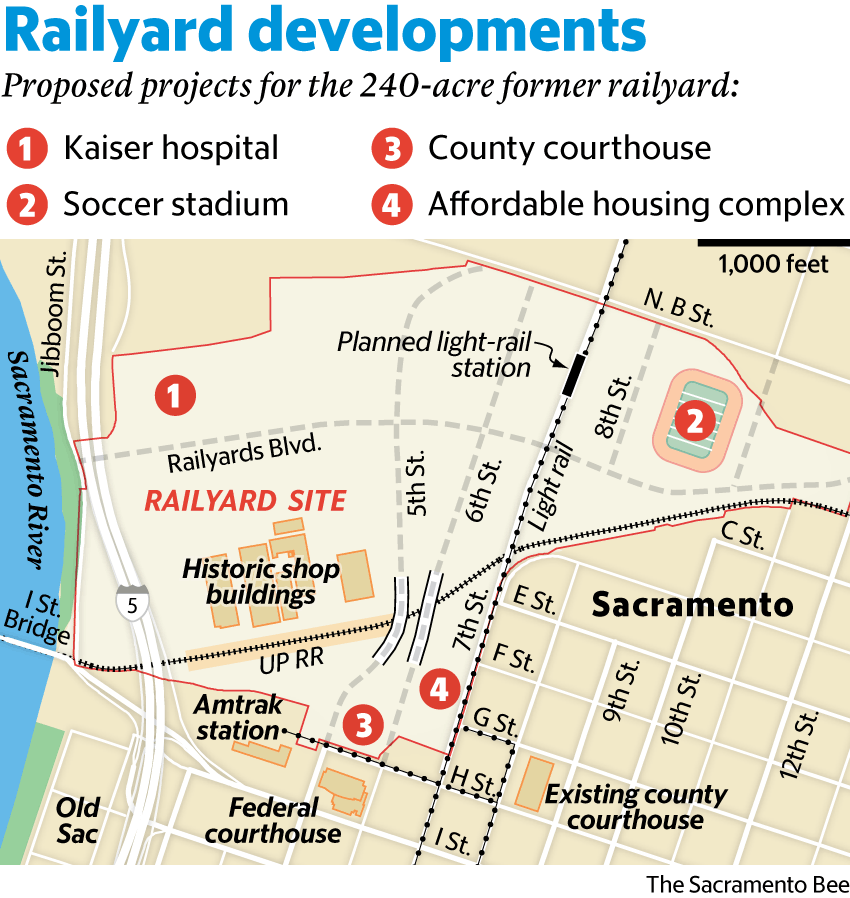

Oakland, Calif.-based Kaiser Permenante’s new hospital development in Sacramento, Calif., could cost as much as $1.48 billion, Sacramento Business Journal reported Dec. 11.

The project costs 50% more than when the health system first announced the new hospital six years ago. The 310-bed hospital building is expected to cost $924.4 million. When Kaiser assessed the building part of the project in 2018, it projected that it would cost $749.5 million.

Currently, Kaiser operates a 287-bed hospital in the area. However, it does not meet California’s earthquake compliance standards.

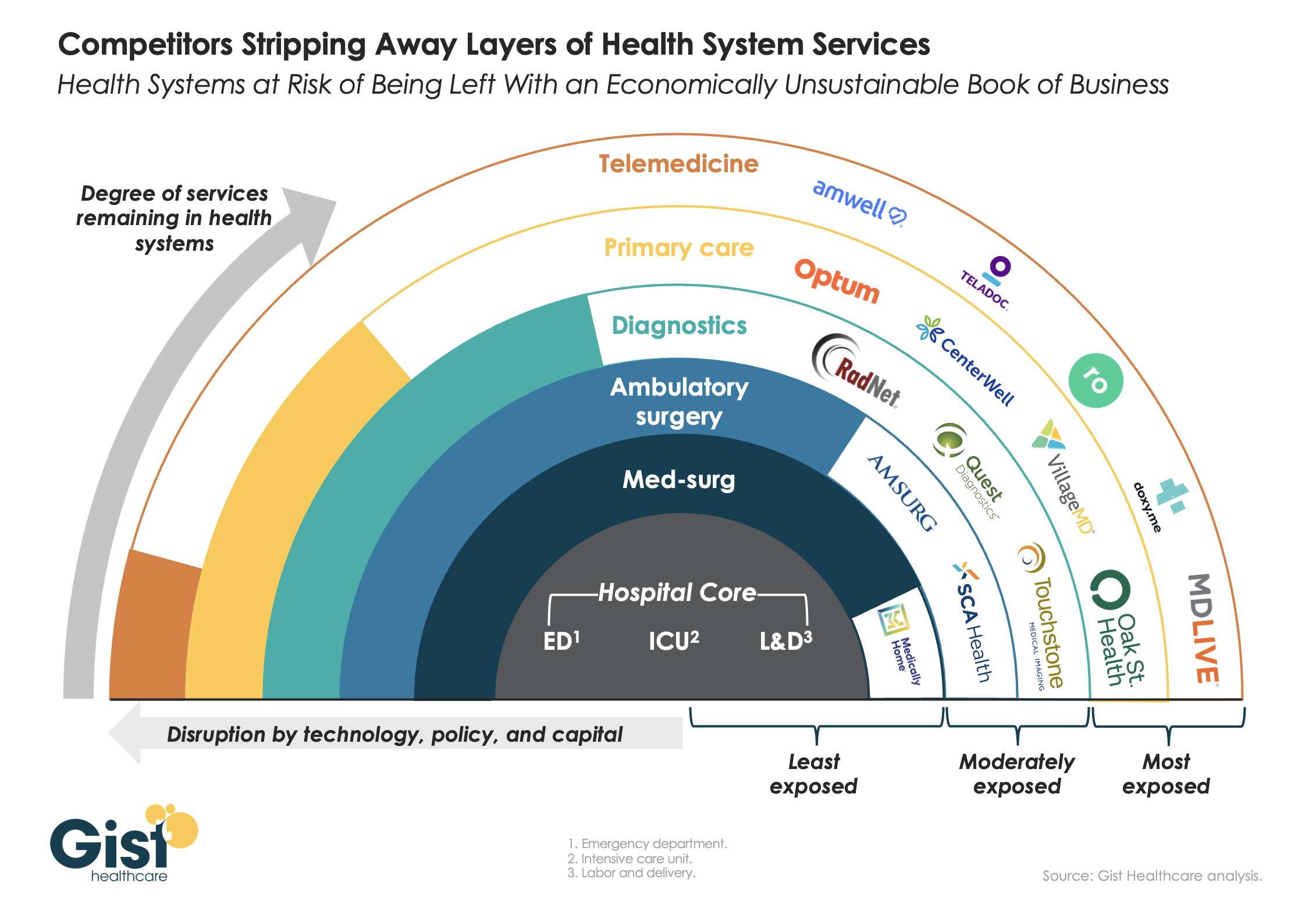

This week’s graphic features our assessment of the many emerging competitive challenges to traditional health systems.

Beyond inflation and high labor costs, health systems are struggling because competitors—ranging from vertically integrated payers to PE-backed physician groups—are effectively stripping away profitable services and moving them to lower-cost care sites. The tandem forces of technological advancement, policy changes, and capital investment have unlocked the ability of disruptors to enter market segments once considered safely within health system control.

While health systems’ most-exposed services, like telemedicine and primary care, were never key revenue sources (although they are key referral drivers), there are now more competitors than ever providing diagnostics and ambulatory surgery, which health systems have relied on to maintain their margins.

Moving forward, traditional systems run the risk of being “crammed down” into a smaller portfolio of (largely unprofitable) services: the emergency department, intensive care unit, and labor and delivery.

Health systems cannot support their operations by solely providing these core services, yet this is the future many will face if they don’temulate the strategies of disruptors by embracing the site-of-care shift, prioritizing high-margin procedures, rethinking care delivery within the hospital, and implementing lower-cost care models that enable them to compete on price.

West Reading, Pa.-based Tower Health continues to make progress on its performance improvement plan as its operating margin for the three months ended Sept. 30 rose to -4.2% from -8% during the same period in 2022. Its operating cash flow margin also increased from -0.9% to 2.3%.

During the first quarter of fiscal 2024, the three months ending Sept. 30, revenue decreased 2.9% year over year to $457.4 million. Expenses decreased 6.4% to $476.5 million.

Tower’s operating loss for the period was $19.1 million, compared with a loss of $37.6 million for the prior-year period.

As of Sept. 30, total balance sheet unrestricted cash and board-designated investment funds for capital improvements totalled $154 million — a decrease of $54 million from June 30, 2023. The main factors for the decrease were $15 million of debt service payments, physician incentive compensation payments of $9 million, capital expenditures of $6 million, negative changes in working capital of $32 million, partially offset by EBITDA of $10 million.

Total days of cash on hand for the system was 30 on Sept. 30.

After including the performance of its investment portfolio and other nonoperating items, the health system ended the three-month period with a net loss of $20.9 million, compared with a net loss of $37.6 million for the same period in 2022.

West Reading, Pa.-based Tower Health will be out of network for all Cigna Healthcare members starting Jan. 1 following a disagreement over reimbursement rates, the Reading Eagle reported Nov. 24.

The split applies to all Tower Health facilities and physicians for Cigna commercial, Medicare Advantage and behavioral health plans. Cigna said it is continuing to negotiate with Tower Health, but the health system has already begun to notify patients about the impending contract break.

“Tower Health, like other health systems, has been contending with unprecedented cost increases for personnel, supplies, equipment and medication necessary to continue providing high quality care,” a health system spokesperson told the Eagle. “Cigna has been unwilling to compensate Tower Health at reasonable payment rates.”

“We are disappointed that Tower Health is choosing to leave our network Jan. 1 unless we agree to their demands for significant rate increases that will make healthcare much more expensive for the people we serve,” a Cigna spokesperson told the Eagle. “It’s important to understand who pays the bills: any increase in cost of care is paid directly by local employers, their employees and families.”

Medicare Advantage and commercial claims denials have spiked across the country, leaving hospitals increasingly financially strapped, according to research published Nov. 17 by the American Hospital Association and Syntellis.

The report analyzed data from a national sample of 1,300 hospitals and health systems. From January 2022 to July 2023, revenue reductions related to Medicare Advantage denials increased 55.7% for the median hospital. During the same period, denial-related revenue reductions rose 20.2% for commercial plans. For denials relative to net patient service revenue for the median hospital, Medicare Advantage plans saw an increase of 63.3% and commercial plans rose 20%.

“[Hospitals] must take larger revenue reductions to account for those lost reimbursements from commercial payers and Medicare Advantage plans, which cover more than 31 million Americans and make up about half of all Medicare beneficiaries,” the report said. “The challenges will only worsen as Medicare Advantage enrollment continues to grow.”

In November 2022, an AHA survey found that half of hospitals and health systems reported having more than $100 million in unpaid claims that were more than 6 months old. As of June 2023, health systems had a median of 124 days cash on hand, down from 173 days in January 2022.

The new data coincides with recent reporting from Becker’s about hospitals across the country that have ended some or all Medicare Advantage contracts. The reasons behind contract terminations vary by system and by payer offering the plan. Some systems have cited steep losses amid excessive prior authorization denial rates and slow payments from insurers. Others have noted that most MA carriers have faced allegations of billing fraud from the federal government and are being probed by lawmakers over their high denial rates.

“It’s become a game of delay, deny and not pay,” Chris Van Gorder, president and CEO of San Diego-based Scripps Health, told Becker’s in September.

According to data shared with Becker’s by FTI Consulting, among the 64 contract disputes reported in the media this year through Sept. 30, 37 involved Medicare Advantage plans, and 10 disputes exclusively involved MA plans. In the third quarter alone, 15 disputes involved MA plans, compared to seven in the third quarter of 2022, a 115% increase year over year.