The healthcare industry is facing an urgent need to reduce costs and increase revenue. Research from the Healthcare Advisory Council reveals the not-for-profit health system will need between $40 million and $44 million annually in cost avoidance over the next eight years to maintain a sustainable margin. The challenge is significant, but emerging technologies and innovative strategies are creating opportunities for greater efficiency, better patient care and decreased costs, according to executives and other leaders in healthcare.

Making a Margin on Medicare

Health systems with the best margin sustainability pursue effective cost-avoidance practices, including:

- Embedding cost discipline throughout the organization

- Escalating spending decisions

- Reducing unnecessary hires

- Matching patient acuity to the level of care

- Reducing drug formulary costs

But even with these practices, cost avoidance is challenging—particularly when it comes to Medicare-reliant seniors, who often require frequent medical treatments and hospital admissions. Turning to advanced electronic medical records (EMRs) that are designed around a health system’s risk and workflow can improve treatment decisions and continuity of care, leading to decreased admissions, better cost effectiveness and a greater profit margin.

Simultaneously, some health systems are looking to a pre-paid, value-based medicine model, as opposed to the more common fee-for-service model. Value-based medicine moves the payment upstream, incentivizing providers to focus on maintaining patient health rather than on providing medical interventions. Decreasing the amount of care needed to keep patients healthy has a direct impact on the size of an organization’s margins.

Blockchain: The Potential to Change Healthcare

One of the most common inefficiencies in healthcare is how physicians are credentialed. The months-long process for clinician credentialing commands significant time and costs. Emerging blockchain technology may be one solution to this persistent point of inefficiency.

With blockchain, rather than sending a clinician credentialing application to several organizations for verification, the physician and all credentialing locations—as members of a dedicated blockchain network—can have access to the physician’s highly encrypted log. Any changes to the physician’s log can be transmitted to the network and validated by private keys known only to each party and with algorithms agreed upon by the network. In this, trust transfers from a third-party clearinghouse to the network as a whole.

In the blockchain world, the physician could provide access codes to the hospital to review their verified credentials. This could save as much as 80 percent of the current cost and time invested in physician credentialing. Using the same technology and process, blockchain may also be a valuable tool for finding efficiencies when working with patient records.

Venture Capital: Strategic Investing 2.0

Healthcare system-based venture capital funds are growing rapidly. In 2017, more than 150 distinct corporate venture groups operated within the healthcare arena, according to Health Enterprise Partners, and these groups participated in 38 percent of all healthcare IT financing.

There are four common objectives for starting such a fund:

- Generate new income sources not subject to healthcare reimbursement pressure

- Identify promising companies that executives might not otherwise encounter

- Create a vehicle to enhance brand integrity and expand market reach

- Foster a culture of innovation

Once healthcare investors establish their fund objectives (or mix of objectives), they define their investment approach. This includes establishing a decision-making chain with operational leaders and board members that can allow decisions to be made quickly and in an established pattern. It also includes building infrastructure and could mean adopting a rigorous information environment system, like a healthcare customer relationship management (CRM) system, as well as developing stringent custody and accounting procedures for securities.

Funds should gather resources to support the interactions between the investment fund and the companies in which they invest. At the outset, they should decide the relationship they will have with their investment targets and whether return on investment is a primary or secondary goal. As a part of choosing investment targets, it is important that funds address an important problem of the parent organization and in a way that the organization supports.

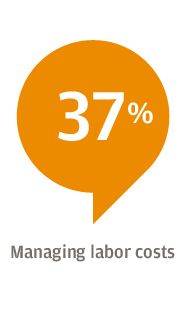

Time Is Money: Accelerating the Pace of Care

For health systems, every patient hour costs $250 in direct operating costs, more than half of which owe to labor. By this, improving efficiency and decreasing the time needed for tasks can save money and support a healthy margin. A mix of advanced analytical data and targeted interpersonal relations can help reduce the time required for common hospital and health system tasks. Predictive analytic modeling software can help yield clearer insight into operations, revealing ways to break down barriers between departments and more effectively manage census levels. This optimizes census distribution inside a complex medical center.

Another rich source of potential healthcare savings lies in the staff hiring process. Successful staff hiring for all income levels is one of the great challenges for health systems, but data analytics can help make the hiring process more efficient. With models built on the characteristics of successful hires, predictive analytics can point to applicants with the best potential for success, improving confidence in hiring decisions. Importantly, while analytics and automation can play a big part in finding the best applicants, once a candidate becomes an employee, important decisions like promotions or relocations require direct personal contact.

Data and Dollars Innovation

As health systems explore avenues for increased efficiency, lower costs and better margins, J.P. Morgan has developed digital innovations to support healthcare investment, strategy and operation. Two of the most applicable include:

- Enhanced Healthcare Lockbox: J.P. Morgan has supercharged its lockbox technology with machine learning. The auto-posting rate has increased by nearly one-fifth, allowing hospitals and health systems to redeploy assets to other revenue-generating sectors like denial management. The high-tech upgrade has also saved three to four days in clients’ working capital.

- Corporate Quick Pay: The need for hospitals and health systems to collect an increasing amount of money directly from patients has resulted in an explosion in low-dollar patient refunds. This creates a problem for the accounts payable departments of healthcare institutions, which were not designed to issue thousands of small checks to patients. J.P. Morgan’s Corporate Quick Pay solution allows health systems to send payments directly to a patient’s bank account using email or text message.

These innovations in artificial intelligence and machine learning drive efficiency across a range of areas. Consider the benefits one client enjoyed by virtue of J.P. Morgan’s digital tools:

- 70,000 paper-based claims converted to electronic

- 99.3 percent lift rate for all paper received in lockbox

- 18 percent increase in auto-posting after implementation

- Three to four days’ improvement to working capital

Going forward, emerging technologies and strategies are indispensable for healthcare systems striving to grow margins in a time when health costs and needs are increasing. Ultimately, hospitals and health systems that find pathways to greater profitability will be best positioned to achieve their primary goal: delivering better care that leads to better patient outcomes.