Sign of the Times: On Staffing

https://www.axios.com/2023/12/14/older-american-adults-working-wages-economy

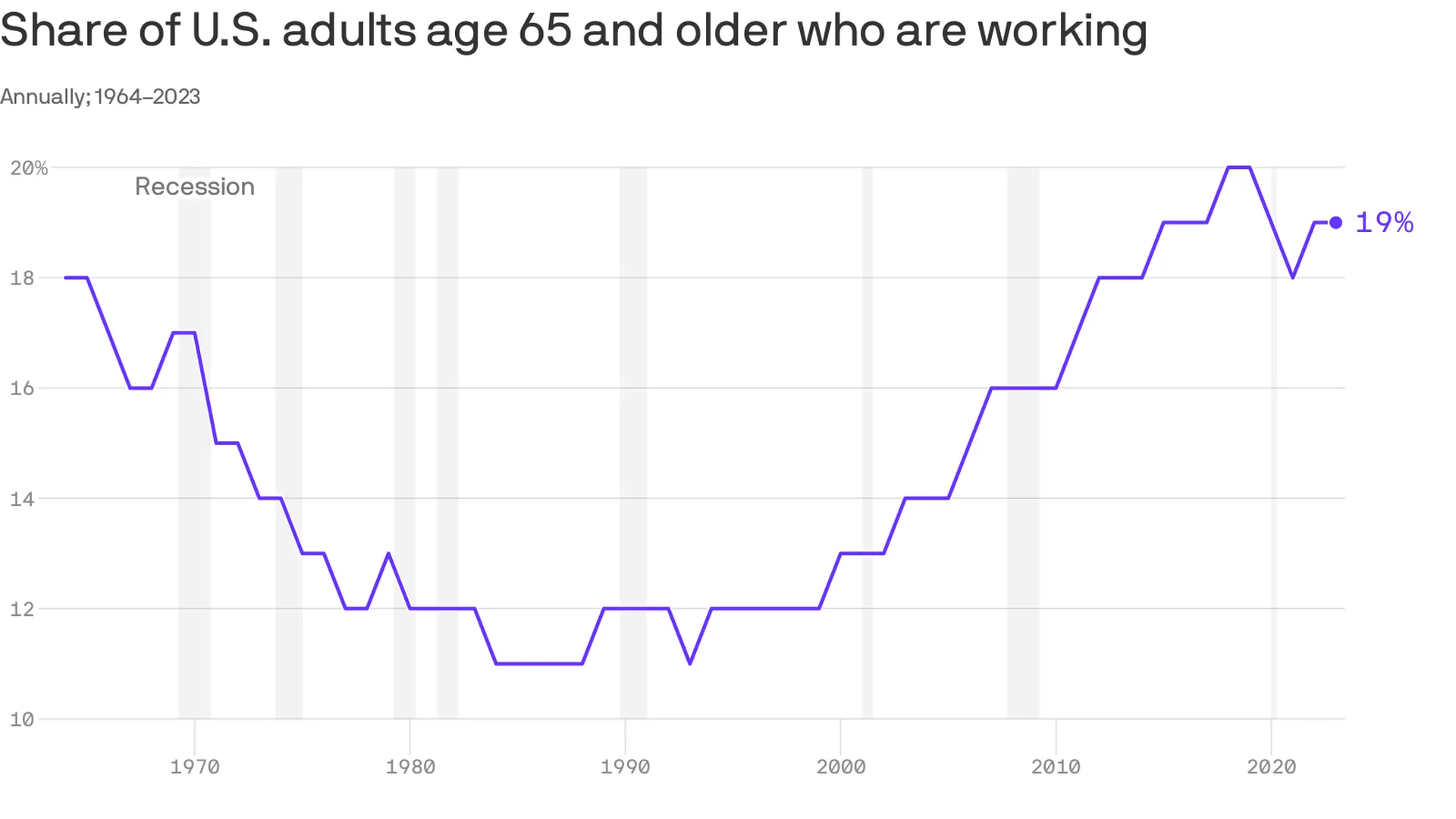

An increasing number of Americans age 65 and older are working — and earning higher wages, per a study from the Pew Research Center out Thursday.

Why it matters:

This is good for the economy, especially as the U.S. population ages — but whether or not it’s good for older Americans is a bit more subjective.

Zoom in:

The share of older adults working has been steadily increasing since the late 1980s, with a detour during the pandemic as older folks retired in greater numbers. Several forces are driving the shift:

By the numbers:

Last year, the typical 65+ worker earned $22 an hour, up from $13 (in 2022 dollars) in 1987. That’s about $3 less than the average for those age 25-64, and the number includes wages of full- and part-time workers.

Be smart:

Before Social Security existed, older people worked — a lot. In the 1880s, about three-fourths of older men were employed, said Richard Fry, senior researcher at Pew. They also didn’t live as long.

The big picture:

“If people are working longer because they find purpose in their jobs and want to stay engaged, that’s good for them individually,” said Nick Bunker, head of economic research at Indeed Hiring Lab.

What to watch:

The share of older adults working peaked before the pandemic — will it surpass those levels?

https://mailchi.mp/59f0ab20e40d/the-weekly-gist-october-27-2023?e=d1e747d2d8

Earlier this month, Governor Gavin Newsom signed a bill that puts all full- and part-time California healthcare workers, including all ancillary support staff, on a path to earning $25 per hour.

While wage increases will begin phasing in next year, the timeline for implementation depends on facility type and other factors like payer mix. Large health systems and dialysis centers have until 2026 to fully implement the new wage, while rural, independent hospitals and those with high public payer mixes, as well as other clinical facilities, have more time to comply.

The law, which replaces the $15.50 state minimum wage for all workers, is projected to impact over 469K healthcare workers in the state, potentially including 50K who already earn more than $25 per hour but are forecasted to receive wage increases to maintain their pay premiums. Strongly backed by California healthcare unions, the law ultimately received the support of the California Hospital Association on the grounds that it will “create stability and predictability for hospitals” by preempting local wage and compensation measures active in many California cities.

The Gist: On the heels of a tentatively successful labor negotiation with Kaiser Permanente—which would raise the system’s hourly minimum wage to $25—California healthcare unions have flexed their might for another win.

While this new law directly benefits healthcare workers earning less than $25 an hour, its knock-on effects will extend to those earning above that to avoid pay compression, as well as to workers in other industries that draw from the same labor pool.

The mandated higher pay may provide California healthcare employers with a recruitment edge (and lure talent away from neighboring states), but higher costs will exacerbate the margin challenges plaguing many hospitals in the state.

Nurses who work for staffing agencies are much more satisfied than their counterparts who serve hospitals, health systems, home healthcare providers and senior living facilities, according to an Oct. 18 report from MIT Sloan Management Review.

Researchers identified 200 of the largest healthcare employers in the U.S., and calculated how highly nurses rate the organization and senior leadership on Glassdoor from the beginning of COVID-19 through June 2023 (view their ranking here).

The five highest-ranked employers in the sample were staffing agencies, according to the report — and higher compensation only accounts for part of nurses’ satisfaction. Researchers analyzed the free text on Glassdoor to determine how positively nurses spoke about 200 topics, and found that nurses spoke more highly of staffing agencies on issues other than pay.

Overall, 75% of nurses’ comments about staffing agencies were positive, compared with 23% of nurses’ comments about health systems.

Staffing agencies have other healthcare employers beat in problem resolution, the researchers found. Seventy-three percent of nurses said staffing agencies resolved problems efficiently, compared to 31% of nurses employed by hospitals and health systems. The difference was even greater when it came to resolving problems effectively — 55% of nurses say staffing agencies do this, compared to 9% of nurses at hospitals and health systems.

Nurses also rated staffing agencies more highly on several measures related to honesty, according to the report. Three-quarters of nurses employed by staffing agencies spoke highly of their organizations’ speed in replying to inquiries; less than one-quarter of nurses employed by hospitals and health systems praised their organization on timely replies. Staffing agencies scored 41 percentage points higher on transparency, 36 points higher on trust and 46 points higher on honesty than their hospital and health system counterparts.

Although nurses employed by staffing agencies also ranked their compensation and work-related stress levels significantly better than nurses employed by hospitals and health systems, the latter took the lead in some metrics. Nurses prefer hospitals and health systems for health and retirement benefits, learning and development opportunities, and connection with colleagues: all “important aspects of organizational life,” according to the report.

“Healthcare systems can learn from staffing agencies, but they can also leverage their own distinctive advantages to attract and retain nurses,” the report says. “Healthcare systems should invest in their comparative advantages and emphasize them when communicating their value proposition to potential and current employees.”

Hospitals and health systems are seeing some signs of stabilization in 2023 following an extremely difficult year in 2022. Workforce-related challenges persist, however, keeping costs high and contributing to issues with patient access to care. The percentage of respondents who report that they have run at less than full capacity at some time over the past year because of staffing shortages, for example, remains at 66%, unchanged from last year’s State of Healthcare Performance Improvement report. A solid majority of respondents (63%) are struggling to meet demand within their physician enterprise, with patient concerns or complaints about access to physician clinics increasing at approximately one-third (32%) of respondent organizations.

Most organizations are pursuing multiple strategies to recruit and retain staff. They recognize, however, that this is an issue that will take years to resolve—especially with respect to nursing staff—as an older generation of talent moves toward retirement and current educational pipelines fail to generate an adequate flow of new talent. One bright spot is utilization of contract labor, which is decreasing at almost two-thirds (60%) of respondent organizations.

Many of the organizations we interviewed have recovered from a year of negative or breakeven operating margins. But most foresee a slow climb back to the 3% to 4% operating margins that help ensure long-term sustainability, with adequate resources to make needed investments for the future. Difficulties with financial performance are reflected in the relatively high percentage of respondents (24%) who report that their organization has faced challenges with respect to debt covenants over the past year, and the even higher percentage (34%) who foresee challenges over the coming year. Interviews confirmed that some of these challenges were “near misses,” not an actual breach of covenants, but hitting key metrics such as days cash on hand and debt service coverage ratios remains a concern.

As in last year’s survey, an increased rate of claims denials has had the most significant impact on revenue cycle over the past year. Interviewees confirm that this is an issue across health plans, but it seems particularly acute in markets with a higher penetration of Medicare Advantage plans. A significant percentage of respondents also report a lower percentage of commercially insured patients (52%), an increase in bad debt and uncompensated care (50%), and a higher percentage of Medicaid patients (47%).

Supply chain issues are concentrated largely in distribution delays and raw product and sourcing availability. These issues are sometimes connected when difficulties sourcing raw materials result in distribution delays. The most common measures organizations are taking to mitigate these issues are defining approved vendor product substitutes (82%) and increasing inventory levels (57%). Also, as care delivery continues to migrate to outpatient settings, organizations are working to standardize supplies across their non-acute settings and align acute and non-acute ordering to the extent possible to secure volume discounts.

| 98% of respondents are pursuing one or more recruitment and retention strategies |

| 90% have raised starting salaries or the minimum wage |

| 73% report an increased rate of claims denials |

| 71% are encountering distribution delays in their supply chain |

| 70% are boarding patients in the emergency department or post-anesthesia care unit because of a lack of staffing or bed capacity |

| 66% report that staffing shortages have required their organization to run at less than full capacity at some time over the past year |

| 63% are struggling to meet demand for patient access to their physician enterprise |

| 60% see decreasing utilization of contract labor at their organization |

| 44% report that inpatient volumes remain below pre-pandemic levels |

| 32% say that patients concerns or complaints about access to their physician enterprise are increasing |

| 24% have encountered debt covenant challenges during the past 12 months |

| None of our respondents believe that their organization has fully optimized its use of the automation technologies in which it has already invested |

The hospital workforce is critical to the care process and is most often the largest expense on a hospital or health system’s balance sheet. Even before the pandemic, labor expenses — which include costs associated with recruitment and retention, employee benefits and incentives — accounted for more than 50 percent of hospitals’ total expenses, according to the American Hospital Association.

As a result, a slight increase in labor costs can have a tremendous effect on a hospital or health system’s total expenses and operating margins. Hospitals across the country are focused on managing the premium cost of labor, while recruiting and retaining talent remains a priority, and the cost of supplies and drugs also increases due to inflation.

Here’s how 23 health systems’ labor costs are tracking based on the results of their most recent financial documents.

Note: This is not an exhaustive list. Most of the following health systems’ labor costs are for the three months ending 30, with others for the six months ending June 30 and the 12 months ending June 30 — the most recent periods for which financial data is available. The year-over-year percentage increase/decrease is also included.

1. HCA Healthcare Nashville, Tenn.)

Q2 salaries and benefits: $7.3 billion (+7.1 percent YOY)

2. Tenet Healthcare (Dallas)

Q2 salaries, wages and benefits: $2.3 billion (+7.5 percent YOY)

3. Community Health Systems (Franklin, Tenn.)

Q2 salaries and benefits: $1.3 billion (+3.2 percent YOY)

4. Universal Health Services (King of Prussia, Pa.)

Q2 salaries, wages and benefits: $1.8 billion (+4.7 percent YOY)

5. Mayo Clinic (Rochester, Minn.)Q2 salaries and benefits: $2.4 billion (+5.9 percent YOY)

6. SSM Health (St. Louis)

Q2 salaries and benefits: $1.1 billion. (+14.1 percent YOY)

7. Cleveland Clinic

Q2 salaries, wages and benefits: $2.1 billion (+8.9 percent YOY)

8. McLaren Health Care (Grand Blanc, Mich.)

Q2 salaries, wages, employee benefits and payroll taxes: $1.3 billion (+0.5 percent)

9. Sutter Health (Sacramento, Calif.)

Q2 salaries and employee benefits: $1.7 billion (6.7 percent YOY)

10. IU Health (Indianapolis)

Q2 salaries, wages and benefits: $1.1 billion (-1.6 percent YOY)

11. Mass General Brigham (Boston)

Q2 employee compensation and benefits: $2.4 billion (+4.2 percent YOY)

12. ProMedica (Toledo, Ohio)Q2 salaries, wages and employee benefits: $388.8 million (-2.5 percent YOY)

13. Orlando (Fla.) Health

Q2 salaries and benefits: $734.4 million (+17.9 percent YOY)

14. MultiCare Health (Tacoma, Wash)

Salaries, wages and employee benefits: $1.5 billion (+14.4 percent YOY)

*For the six months ended June 30

15. Banner Health (Phoenix)Salaries, benefits and contract labor: $3 billion (+4.7 percent YOY)

*For the six months ended June 30

16. UPMC (Pittsburgh)

Salaries, professional fees and benefits: $4.8 billion (+6.7 percent YOY)

*For the six months ended June 30

17. Northwell Health (New Hyde Park, N.Y.)

Salaries and employee benefits: $5.3 billion (+10.6 percent YOY)

*For the six months ended June 30

18. Providence (Renton, Wash.)

Salaries and benefits: $7.5 billion (+4.9 percent YOY)

*For the six months ended June 30

19. Sanford Health (Sioux Falls, S.D.)

Salaries and benefits: $1.8 billion (+2.6 percent YOY)

*For the six months ended June 30

20. Intermountain Health (Salt Lake City)

Employee compensation and benefits: $3.4 billion (+27.9 percent YOY)

*For the six months ended June 30

21. CommonSpirit Health (Chicago)

Salaries and benefits: $18.3 billion (+0.7 percent YOY)

*For the 12 months ended June 30

**Merged with Broomfield, Colo. -based SCL Health in April 2022

22. Ascension (St. Louis)

Salaries, wages and employee benefits: $14.3 billion (-1.3 percent YOY)

*For the 12 months ended June 30

23. Mercy Health (Chesterfield, Mo.)

Salaries and benefits: $4.6 billion (+5.3 percent)

*For the 12 months ended June 30