In the past year, cost was a bigger factor driving Americans to skip recommended healthcare than fear of contracting COVID-19, according to a report released June 1 by Patientco, a revenue cycle management company focusing on patient payment technology.

Patientco surveyed 3,116 patients and 46 healthcare providers, finding 34 percent of female patients and 30 percent of male patients have avoided care in the past year citing concerns about out-of-pocket costs.

Below are three more notable findings from the report:

Healthcare affordability is not an issue that affects only Americans with low incomes, as 85 percent of patients with household incomes greater than $175,000 are less likely to defer care when flexible payment options are offered.

Across all ages, income levels and education levels, most patients said they struggled to understand their medical bills and what they owed. Nearly two-thirds of patients said they did not understand their explanation of benefits, did not know what they should do with the information in their explanation of benefits, or waited too long to obtain their explanation of benefits.

Forty-five percent of patients said they would need financial assistance for medical bills that exceed $500, and 66 percent of patients said the same for medical bills that exceed $1,000.

Average benchmark premiums for plans on the Affordable Care Act’s exchanges have fallen for the third straight year, according to a new analysis.

Researchers at the Urban Institute, a left-leaning think tank, found that the average benchmark premium on the exchanges fell by 1.7% for 2021. That follows decreases of 1.2% in 2019 and 3.2% in 2020.

By contrast, premiums for employer-sponsored plans increased by 4% in both 2019 and 2020, according to the report. Data for 2021 on the employer market are not yet available, the researchers said.

The national average benchmark premium was $443 per month for a 40-year-old nonsmoker, according to the report, before accounting for any tax credits.

The researchers found much significant variation in premium levels between states, though the difference in growth rates was smaller. Minnesota reported the lowest average benchmark premium at $292 per month, and the highest was in Wisconsin at $782 per month.

Average benchmark premiums topped $500 in 10 states, according to the report.

One of the key trends that’s slowing premium growth is increasing competition in the exchanges, as many insurers are expanding their offerings or returning to the marketplaces to offer plans, according to the report.

“New entrants included national and regional insurers, Medicaid insurers, and small start-up insurers,” the researchers wrote.

“Medicaid insurers are those who operated exclusively in the Medicaid managed-care market before 2014; they have increased their participation in the Marketplaces over time. Medicaid insurers are experienced in establishing narrow, low-cost provider networks that allow them to offer lower premiums than other insurers.”

UnitedHealthcare, for example, participated in just four regions included in the study in 2017, but had upped its participation to 11 for 2021. Aetna participated in three regions included in the study in 2017 before fully exiting the exchanges; CVS Health CEO Karen Lynch told investors earlier this year that the insurer plans to return to the marketplaces in 2022.

Several states have also launched programs that aim to lower premiums, according to the report. These include reinsurance programs, which have been rolled out in 12 states as of this year. Some states have also expanded Medicaid in recent years, which leads to some low-income people with costly health needs switching to that program, the researchers said.

UPDATE: May 21, 2021: Late Thursday, drug manufacturing giant Eli Lilly filed a motion in an Indiana district court to halt 340B-related monetary penalties, scant days after the Biden administration set a June 1 deadline for biopharmaceutical companies to comply with new conditions in the drug discount program and allow hospital contract pharmacies access to discounted drugs.

The suit alleges a Monday letter from Diana Espinosa, acting head of the Health Resources and Services Administration, gives “no legal explanation or justification for the arbitrary June 1 deadline.”

Lilly previously filed an almost identical lawsuit January 2020. The Indianapolis-based biopharma said it expected the government to follow the briefing schedule outlined in that suit before mandating compliance with 340B and forcing it to pay “substantial and irretrievable sums of money.”

“If the Court ultimately decides Lilly was required to extend 340B pricing to contract pharmacies, Lilly will comply with that decision. Conversely, if the Court ultimately decides manufacturers are not required to extend 340B pricing to contract pharmacies, then we surely expect the government will comply with that decision. But there is no explanation or justification for the government’s attempt to make Lilly pay now, other than to evade this Court’s review and leave Lilly without recourse for such payments,” the motion reads.

In the petition, Lilly, which brought in $6.2 billion in profit last year, alleges the shifting terms of the program are due to HHS director Xavier Becerra bending to political pressure to “take action” against drug manufacturers, as pharmaceutical prices continue to climb.

Lilly asked the district court to temporarily block HHS from moving against Lilly until the drugmaker’s request for a preliminary injunction is resolved; and for an accelerated legal schedule to settle its claims before the looming June deadline.

An HRSA spokesperson declined to comment on the suit.

Dive Brief:

HHS’ Health Resources and Services Administration called out six pharmaceutical companies Tuesday for violating rules under the 340B drug discount program, ordering them to repay affected providers for previous overcharges and warning of more penalties if they don’t comply.

In July 2020 some drugmakers stopped giving the 340B ceiling price on their products sold to covered entities and dispensed through contract pharmacies, while others limited sales by requiring specific data or selling products only after a covered entity demonstrated 340B compliance, according to HRSA.

In letters from Diana Espinosa, acting administrator of HRSA, the agency requested AstraZeneca, Eli Lilly, United Therapeutics, Sanofi, Novo Nordisk and Novartis give an update on their plans to restart selling covered outpatient drugs at the 340B price to covered entities that dispense medications through contract pharmacies by June 1.

Dive Insight:

Providers and drugmakers have sparred for years over the 340B drug discount program that requires pharmaceutical companies to give discounts on outpatient drugs for providers serving low-income communities.

AHA along with five other provider groups in December filed a federal lawsuit against HHS, alleging the department failed to enforce 340B program requirements and allowed actions from drug companies that undermined the program. That lawsuit was later dismissed.

But with the change in administrations, providers now seem to have an ally in the fight.

Previously, as California’s Attorney General, newly minted HHS chief Xavier Becerra led a group of states pushing the agency to force drugmakers to comply with the law late last year.

Provider groups cheered the move after raising the alarm last year that an increasing number of drug companies were refusing to offer discounts to such eligible hospitals.

“The denial of these discounts has damaged providers and patients and must stop. It is vital that these companies immediately begin to repay the millions of dollars owed to these providers,” 340B Health CEO Maureen Testoni said in a statement.

In separate letters to drugmakers, HRSA outlines complaints against them and their actions, ultimately saying their policies violated the statute and resulted in overcharges that need to be refunded. The companies must work to ensure all impacted entities are contacted and efforts are made to pursue mutually agreed upon refund arrangements, according to the letters.

Any additional violations will be subject to a $5,000 penalty for each instance of overcharging under the program’s Ceiling Price and Civil Monetary Penalties final rule.

The American Hospital Association also praised the agency in a release for “taking the decisive action we’ve called for against drug companies that skirt the law by limiting the distribution of certain 340B drugs through community pharmacies.”

Hospitals in the 340B program provide 60% of all uncompensated care in the U.S. and 75% of all hospital care to Medicaid patients, according to 340B Health.

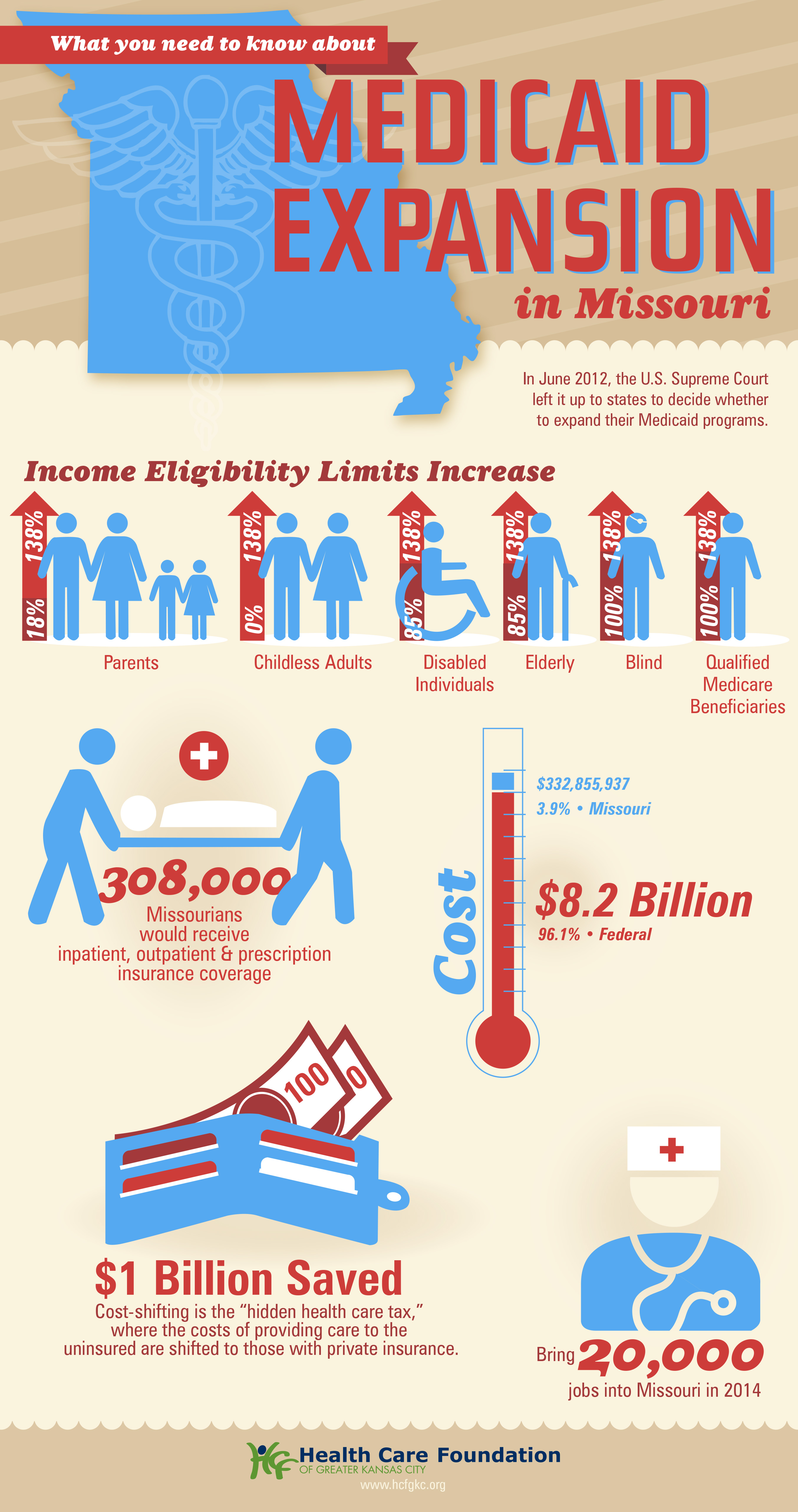

Missouri Gov. Mike Parson announced Thursday that his state would not expand Medicaid coverage to 275,000 residents who will become eligible on July 1st, despite a 2020 ballot initiative in which a majority of the state’s voters approved the expansion. Because the Missouri legislature has blocked funding for the expansion, Parson declared that the state’s Medicaid program, MO HealthNet, would run out of money if it moved forward.

The legislature’s decision to block funding was bolstered by an appeals court opinion last year, which challenged the expansion because the ballot initiative did not include a funding mechanism for widening coverage.

Under the Affordable Care Act (ACA), the federal government would have picked up 90 percent of the cost of expanding Medicaid in the state, in addition to boosting funding for existing Medicaid enrollees by 5 percent, thanks to a measure in the recent American Rescue Plan Act.

The governor’s decision leaves in place one of the strictest Medicaid eligibility standards in the nation: a family of three in Missouri must earn less than 21 percent of the federal poverty level—$5,400 per year—in order to qualify for coverage. The expansion measure would have opened the program to childless adults, and raised the eligibility limit to 138 percent of the federal poverty level.

The Missouri Hospital Association called the decision an “affront” to voters, pointing out that the state is currently running a budget surplus, and could easily allocate funds for the expansion. The status of Medicaid expansion in Missouri, which would become the 38th state to undertake expansion since the ACA’s passage, will ultimately be decided by court ruling, according to observers.

Meanwhile, like other states (mostly in the Southeast) that have resisted Medicaid expansion,Missouri will continue to see tax dollars flow out of the state to fund benefits in states that have expanded eligibility—despite the express will of voters. Given ample evidence that Medicaid expansion boosts access to care, health status, and health system sustainability,it’s nearly unfathomable that the politics of “Obamacare” continue to complicate the extension of this critical safety-net program.

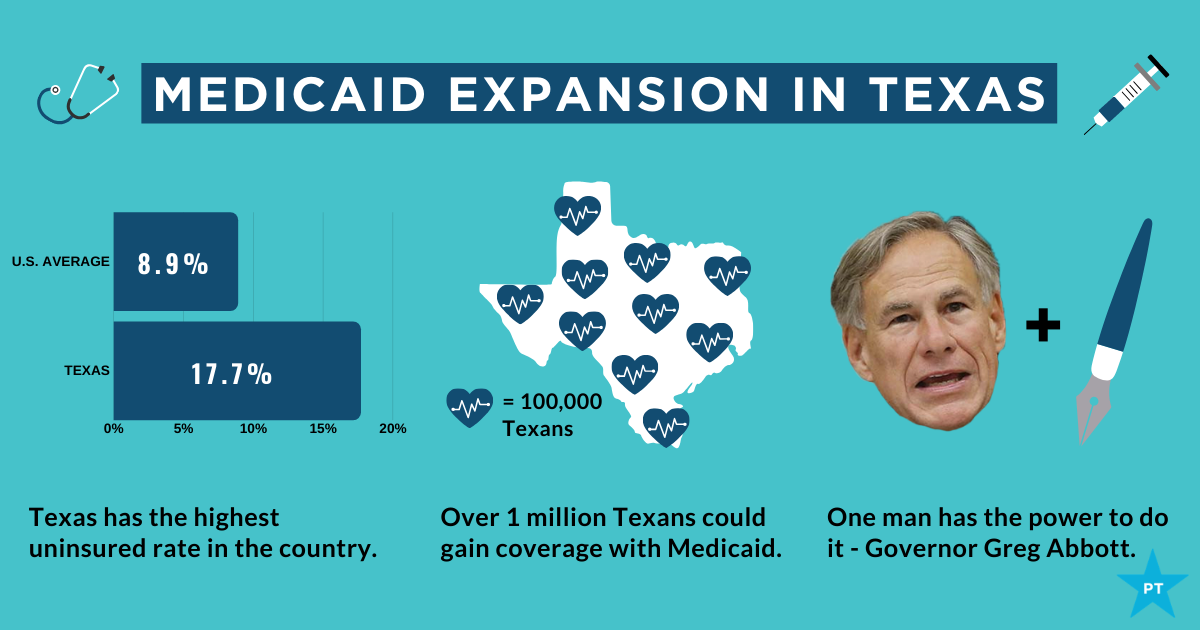

The showdown between the Biden administration and the state of Texas over Medicaid expansion continued to escalate this week. Sen. John Cornyn (R-TX) said he planned to place a hold on the confirmation of Chiquita Brooks-LaSure to become Administrator of the Centers for Medicare & Medicaid Services (CMS), until his concerns over the agency’s move last week to rescind a waiver extension previously granted by the Trump administration were addressed.

The so-called “1115 waiver”—worth more than $11B annually—would have extended by a decade Texas’ ability to use Medicaid funds to cover hospital costs for uninsured residents, rather than expanding Medicaid coverage under the Affordable Care Act (ACA). In rescinding the waiver extension, the Biden administration cited the lack of a public notice process before the waiver was granted, and said that the state’s existing waiver would instead expire next year, as previously scheduled.

Sources inside the administration told the Washington Post last week thatthe move was intended to force Texas’ hand on Medicaid expansion; the state is one of 12 that have not expanded Medicaid, leaving it with the largest share of uninsured residents of any state, with eligibility currently limited to pregnant women, children, people with disabilities, and families with monthly incomes under $300 per month, or 13.6 percent of the federal poverty level.

Enticing the dozen remaining holdout states to expand Medicaid is an important policy priority for the new administration.A key component of the recently passed American Rescue Plan Act is a package of enhanced incentives for those states to expand eligibility, offering an extended 90 percent federal match, in addition to increased funding for existing Medicaid populations.

Although none of the non-expansion states have budged yet, there has been renewed focus among state lawmakers on Medicaid expansion, including in Texas, where the idea had garnered bipartisan support. However, on Thursday, the Texas legislature voted down a proposal aimed at pushing the state toward expanding coverage for the uninsured, by an 80-68 margin. Meanwhile, the rescission of Texas’ waiver has angered the state’s Republican leadership, along with the Texas Hospital Association, whose members have benefited from the waiver’s use of funds to reimburse them for delivering uncompensated care.

While Cornyn’s hold will not ultimately stop the confirmation of the new CMS leader, the escalation on both sides over the past several days surely makes finding a compromise solution less likely. The Biden health policy team is said to be developing a new proposal, as part of an upcoming legislative package, to use the ACA marketplace to offer coverage to people in non-expansion states who might otherwise be eligible for Medicaid—yet another attempt to address one of the longest-standing points of contention stemming from the 2010 health reform law.

The American Rescue Plan stimulus package just sweetened the deal for the twelve holdout states that haven’t yet expanded Medicaid.In exchange for expanding eligibility to the roughly four million adults with incomes up to 133 percent of the federal poverty level, new expansion states will also be eligible for afive percent increase in the federal matching rate for their entire traditional Medicaid population for a two-year period.

The graphic above shows the cumulative fiscal impact for holdout states, should all Medicaid-eligible individuals enroll. Since the traditional Medicaid population is so much larger than the expansion population, the temporary increase more than offsets states’ cost to cover their share of the expansion, resulting in an estimated net fiscal benefit of almost $10B. While the net benefit would vary from state to state, a Kaiser Family Foundation analysis found the two most populous non-expansion states, Texas and Florida, could net up to $1.9B and $1.8B respectively across the two-year period.

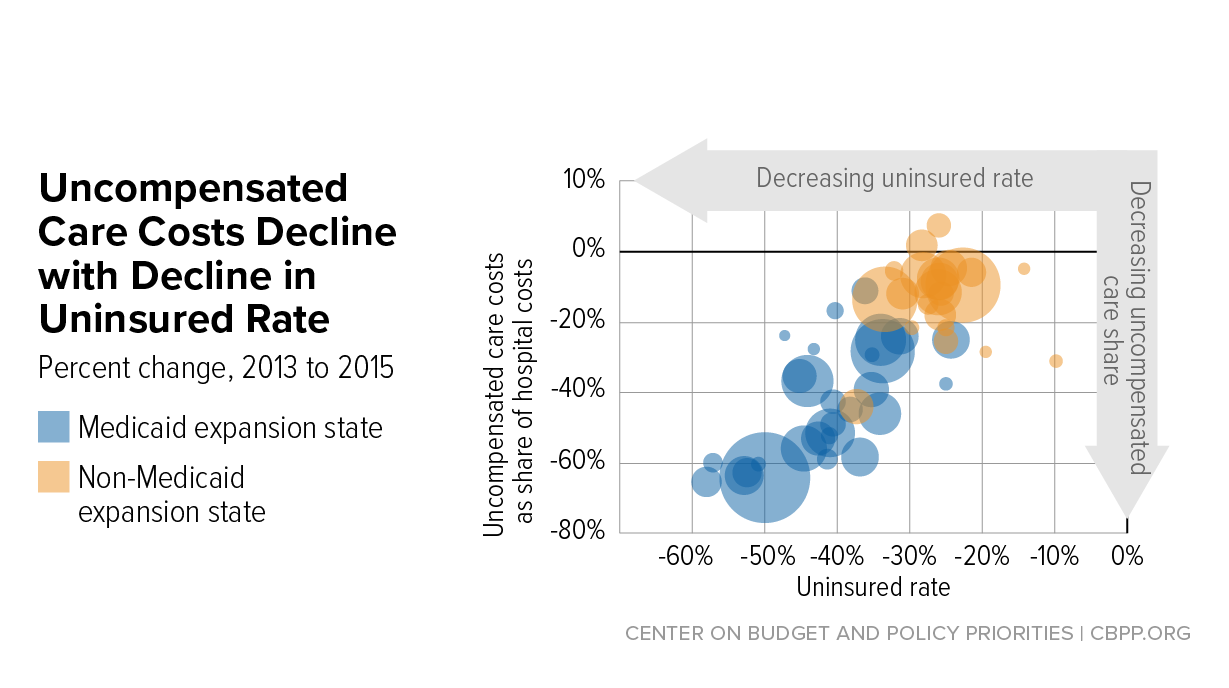

Medicaid expansion has had a significant positive financial impact on hospitals, reducing uncompensated care and increasing overall operating margin by an average of 1.7 percent.

A recent analysis by the Center on Budget and Policy Priorities founduncompensated care costs as a share of hospital expenses fell an average of 45 percent in Medicaid expansion statesbetween 2013 and 2017. So far, only two states eligible for the enhanced expansion, Alabama and Wyoming, have signaled interest in taking advantage of the new deal. Convincing the remaining ten to follow suit will require intense and coordinated advocacy efforts from the healthcare and business communities. Making the financial case for expansion should prove straightforward, compared to overcoming long-entrenched political opposition.

Under the Biden Administration, the DOJ says the ACA can stand even though there is no longer a tax penalty for not having health insurance.

The Department of Justice, under the Biden Administration, has told the Supreme Court that it has changed its stance on the Affordable Care Act.

The DOJ previously filed a brief contending that the ACA was unconstitutional because the individual mandate was inseverable from the rest of the law.

Following the change in Administration, the DOJ has reconsidered the government’s position and now takes the position that the ACA can stand, even though there is no longer a mandate for consumers to have health insurance or face a tax penalty, according to a February 10 filing.

WHY THIS MATTERS

Hospitals and health systems support the change in position.

“Without the ACA, millions of Americans will lose protections for pre-existing conditions and the health insurance coverage they have gained through the exchange marketplaces and Medicaid. We should be working to achieve universal coverage and preserve the progress we have made, not take coverage and consumer protections away,” said American Hospital Association CEO and president Rick Pollack.

The Supreme Court is expected to return a decision before the end of the term in June.

THE LARGER TREND

The Supreme Court heard oral arguments on November 10, 2020 regarding whether the elimination of the tax penalty made the remainder of the ACA invalid under the law.

The DOJ sided with the Trump Administration and Republican states that brought the legal challenge, while 20 Democratic attorneys general supported the ACA and asked the court for quick resolution.

Hospital uncompensated care costs were up from $41.3B in 2018 and $38.4B in 2017, revealing an upward trend, according to AHA data.

Hospital uncompensated care costs increased right before the COVID-19 pandemic hit, according to new data from the American Hospital Association (AHA).

AHA data showed that hospitals incurred a new high of $41.61 billing in uncompensated care costs in 2019, the most recent year for which the group had complete data.

Uncompensated care costs in 2019 were up from $41.3 billion in 2018 and $38.4 billion in 2017 and were the second-highest per AHA records. Hospitals reported the most uncompensated care costs in 2013 when they incurred $46.8 billion.

Hospital uncompensated care costs decreased after the all-time high in 2013, but have recently started to tick back up after holding steady at $38.4 in 2016 and 2017.

In just the last 20 years, hospitals of all types have provided more than $660 billion in uncompensated care to patients, AHA reported. And that figure does not fully account for other ways in which provides provide financial assistance to patients of limited means, the group stated.

Each year, AHA aggregates data on uncompensated care, or care provided for which no reimbursement is received by hospitals from patients or payers. The data comes from the group’s Annual Survey of Hospitals, a comprehensive report of hospital financial data.

Uncompensated care is the sum of a hospital’s bad debt and financial assistance it provides, AHA explained.

Bad debt occurs when a hospital does not expect to obtain reimbursement for care provided, such as when patients are unable to pay their financial responsibility and do not qualify for financial assistance or are unwilling to pay their bills.

Hospitals also provide varying levels of financial assistance, AHA added. Financial assistance supports patients who cannot afford to pay and qualify for support from the hospital based on policies it has established based on the facility’s mission, financial condition, and geographic location, among other factors.

Combined, bad debt and financial assistance charges total a hospital’s uncompensated care charges, which is then multiplied by a hospital’s cost-to-charge ratio to determine total uncompensated care costs.

AHA noted that it expressed uncompensated care in costs versus charges because of significant variations in hospital payer mixes. Publishing the information as costs rather than charges enables better comparison across hospitals, the group said.

Nearly half of hospitals (48 percent) have seen bad debt and uncompensated care increase recently as a result of the ongoing COVID-19 pandemic, an analysis from consulting firm Kaufman Hall revealed.

More than 40 percent of hospitals also reported increases in percentage of uninsured or self-pay patients (44 percent) and the percentage of Medicaid patients (41 percent), which both contribute to unfunded or underfunded care at hospitals.

“The challenges brought on by the COVID-19 pandemic have affected nearly every aspect of hospital financial and clinical operations,” Lance Robinson, a managing director at Kaufman Hall, said at the time. “Organizations have responded to the challenge by adjusting their operations and strengthening important community relationships.”

Hospital uncompensated care costs – and bad debt as a result – are likely to increase in 2020 as hospitals come to terms with the impact COVID-19 has had on their financial health.

Already, hospitals have lost an estimated $323 billion in 2020 as a result of the COVID-19 pandemic, according to earlier projections from AHA.

About half of US hospitals also started the year in the red, AHA and Kaufman Hall stated in a recent report. The organizations predicted that hospital margins would sink to -7 percent in the second half of 2020 without comprehensive financial support from the government, but could decrease to a low of -11 percent if COVID-19 continued to periodically surge as it has.

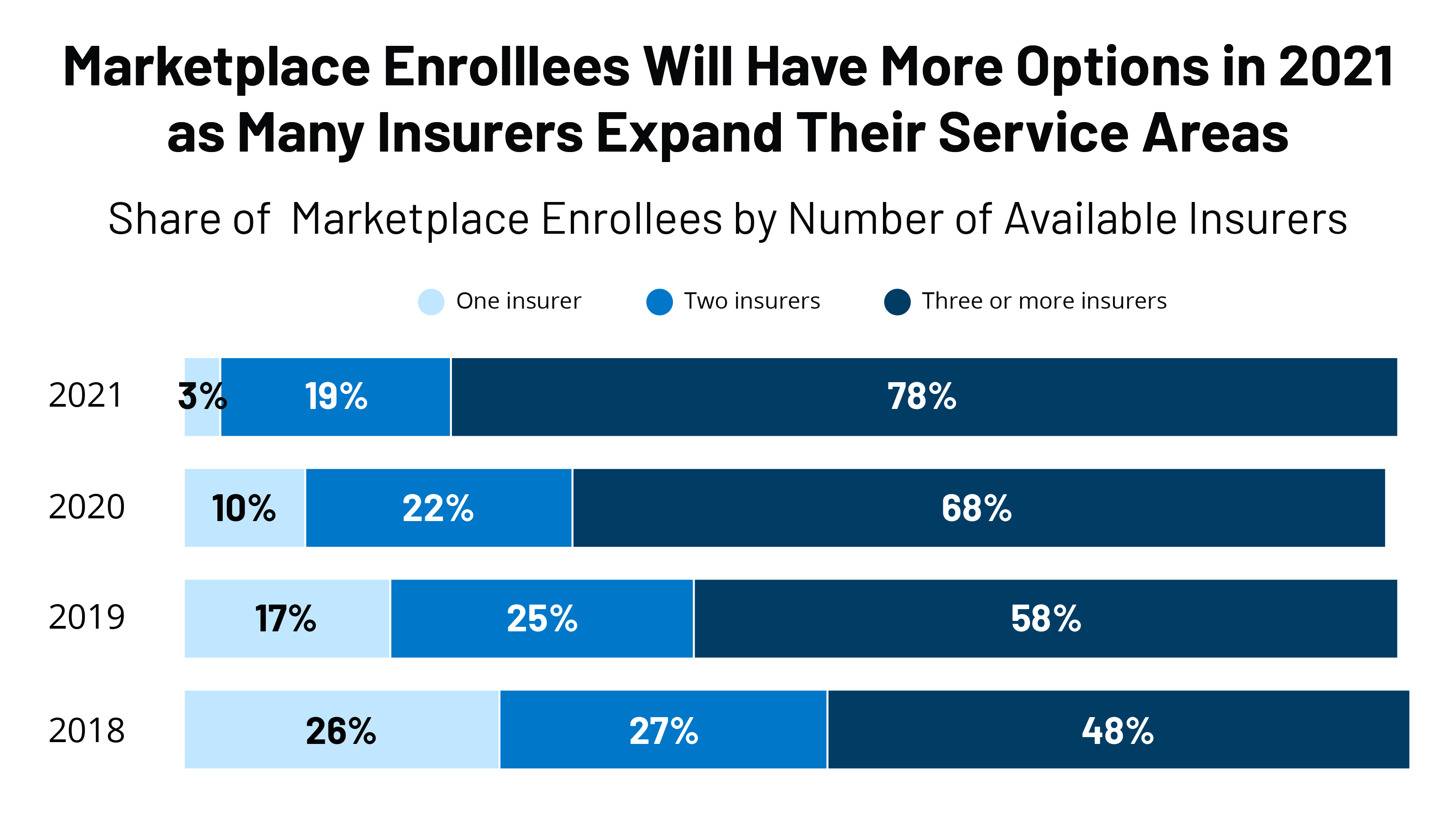

Some 30 insurers are entering the individual market, and an additional 61 are expanding their service area within states, a KFF report says.

Insurer participation in the Affordable Care Act marketplace in 2021 is seeing a third straight year of growth as several insurers are entering the market or expanding their service area, according to a recent Kaiser Family Foundationreport.

For instance, in 2020, UnitedHealthcare, the nation’s largest insurer, became a new entrant in five states, according to the report: Arizona, Maryland, North Carolina, Tennessee and Virginia. Twenty states had new entrants to the market.

For 2021, 30 insurers are entering the individual market, and an additional 61 are expanding their service area within states.

There will be an average of five insurers per state in 2021, up from a low of 3.5 in 2018, but still below the peak of six in 2015. Only 10% of counties will have a single insurer offering in 2021, down from 52% of counties in 2018, the report said. Rural areas tend to have fewer insurers in the ACA market.

Often, when there is only one insurer participating on the exchange, that company is a Blue Cross Blue Shield or Anthem plan, the report said. Before the ACA, state individual markets were often dominated by a single Blue Cross Blue Shield plan.

WHY THIS MATTERS

Despite uncertainties surrounding the ongoing pandemic, the end of the individual mandate and the question of whether the Supreme Court will rule next year to invalidate the entire ACA, the numbers show that insurers appear bullish on participation.

Insurers remained profitable during the pandemic due to decreases in healthcare utilization and claims costs. They are on track yet again to owe substantial rebates to consumers based on low medical loss ratios in 2021.

Even with the lack of a mandate, individuals continue to enroll in ACA plans, with enrollment this year more than keeping pace with last year’s figures. Premiums for 2021 are 1-4% below the average.

THE LARGER TREND

The enrollment numbers continue a trend of rising insurer participation in the ACA going into the 2020 market, and lower premiums.

Insurer participation next year equals the average participation levels at the outset of the marketplaces in 2014, according to the KFF report.

Since 2014, the number of insurers participating on the exchanges has been in flux. Going into the 2018 plan year, many insurers left the market or reduced their footprint due to losses in the market.

Millions of Americans are in danger of losing their homes when federal and local limits on evictions expire at the end of the year, a growing body of research shows.

A report issued this month from the National Low Income Housing Coalition (NLIHC) and the University of Arizona estimates that 6.7 million households could be evicted in the coming months. That amounts to 19 million people potentially losing their homes, rivaling the dislocation that foreclosures caused after the subprime housing bust.

Apart from being a humanitarian disaster, the crisis threatens to exacerbate the coronavirus pandemic, according to a forthcoming study in the Journal of Urban Health.

“Our concern is we’re going to see a huge increase in evictions after the CDC moratorium is lifted,” said Andrew Aurand, vice president of research at the NLIHC and a co-author of the report.

The number of Americans struggling to pay rent has steadily risen since this summer, according to the Census Bureau’s Household Pulse Survey. In the latest survey, from early November, 11.6 million people indicated they wouldn’t be able to pay the rent or mortgage next month.

Meanwhile, some renters who are still paying rent are relying on “unsustainable” income to make ends meet. Among those who report trouble making rent, “More than half are borrowing from family and friends to meet their spending needs, one-third are using credit cards, and one-third are spending down savings,” the NLIHC report found.

Approaching a “payment cliff”

In early September, the U.S. Centers for Disease Control and Prevention barred evictions through year-end, describing the move as a public health measure to reduce spread of the coronavirus. The CDC order protects renters earning less than $99,000 if they have lost income during the pandemic and are likely to become homeless if they’re evicted.

Many states and cities also imposed renter protections during the spring and summer, and others established rental assistance programs to help tenants make ends meet. However, both types of programs are quickly expiring.

Once the CDC moratorium expires,Aurand said, “We expect to see a jump in [eviction] filings, and we know that even now, filings are already occurring. Come January, sadly, for a number of tenants, the next step is the landlord will evict them.”

The situation could reach crisis levels in the new year. With Congress yet to pass another coronavirus relief package, about 12 million Americans are set to lose their unemployment benefits the day after Christmas, a sharp fall in income that would make it harder for many people to pay rent. An abrupt cutoff would slash income by about $19 billion per month, Nancy Vanden Houten, lead economist at Oxford Economics, said in a research note.

Although the Trump Administration has restricted evictions for most households through the end of the year, it did not relieve renters of the need to pay rent. That means many renters may face a “payment cliff” at year’s end, when they must pay several months’ worth of back rent or face eviction.

“If renters are required to quickly repay past due rent or face eviction, the hardship will fall predominantly on lower-income families who have already been disproportionately affected by the coronavirus crisis,” Vanden Houten wrote.

Said Aurand, “If you were a low-income renter before the pandemic and you were hit financially, even if your income starts to recover, you’re going to have a very hard time paying back that rental debt.”

“What we really need is rental assistance,” he noted. “The underlying problem is renters struggling to pay their rent because we’re in an economic crisis, and the moratorium doesn’t address that.”

Long-term impact

Academics have also pushed for direct aid to renters and homeowners, citing the extreme economic fallout from the coronavirus and related shutdowns. In Los Angeles, where 1 in 5 renters were late on rent at some point this summer, residents are facing “an income crisis layered atop of a housing crisis,” researchers at the University of California – Los Angeles have said.

“Delivering assistance to renters now can not just stave off looming evictions, but also prevent quieter and longer-term problems that are no less serious, such as renters struggling to pay back credit card or other debt, struggling to manage a repayment plan, or emerging from the pandemic with little savings left,” they wrote in August report. “Renter assistance can also help the smaller landlords who are disproportionately seeing tenants unable to pay.”

A groundswell of evictions would cause enormous financial hardship. Losing a home is one of the most traumatic events a family can experience, with research showing that people who have experienced eviction are more likely to lose their jobs, fall ill or suffer from mental-health consequences. Children whose families are evicted are more likely to drop out of school, while evictions also contribute to the spread of COVID-19, according to a forthcoming study from UCLA viewed by “60 Minutes.“

“We’ve got a country that’s about to witness evictions like they’ve never witnessed before,” Laura Tucker, a social worker for Florida’s Hillsborough County School District, told “60 Minutes.”

“An eviction can impact a family’s ability to re-house for more than 10 years,” she said.

For that reason, housing and public health experts have said that rental aid now

“Now is the time for action to provide emergency rental assistance. A failure to do so will result in millions of renters spiraling deeper into debt and housing poverty, while public costs and public health risks of eviction-related homelessness increase,” the NLIHC report says. “These outcomes are preventable.”