A major health insurance company is backing off of a controversial plan to limit coverage of anesthesia, according to public officials.

Why it matters:

Anthem Blue Cross Blue Shield recently decided to “no longer pay for anesthesia care if the surgery or procedure goes beyond an arbitrary time limit, regardless of how long the surgical procedure takes,” according to the American Society of Anesthesiologists, which opposed the decision.

The decision was based on surgery time metrics from federal health data, NPR reported.

The policy applied to plans in Connecticut, New York and Missouri.

The latest:

“After hearing from people across the state about this concerning policy, my office reached out to Anthem, and I’m pleased to share this policy will no longer be going into effect here in Connecticut,” Connecticut Comptroller Sean Scanlon said Thursday on X.

Shortly afterward, New York Gov. Kathy Hochul issued a statement saying, “We pushed Anthem to reverse course and today they will be announcing a full reversal of this misguided policy.”

What they’re saying:

The initial coverage decision was very unusual for a major health insurer, said Marianne Udow-Phillips, who teaches insurance classes at the University of Michigan School of Public Health and formerly made coverage decisions at Blue Cross Blue Shield of Michigan.

The big picture:

Anthem’s initial decision was controversial at the time — but outrage erupted this week after the murder of UnitedHealthcare CEO Brian Thompson in New York City cast a spotlight on divisive insurance decisions.

On social media, critics of health insurers drew a direct line from controversial coverage decisions to the death of Thompson.

After UnitedHealthcare CEO Brian Thompson, left, was killed and Anthem released a controversial anesthesia policy, people shared their stories of insurance woes. (UnitedHealth Group via AP, Getty)

On Wednesday, Brian Thompson, the chief executive of UnitedHealthcare, was fatally shot in midtown Manhattan in what police are calling a “pre-meditated, preplanned, targeted attack.” Days before, Anthem Blue Cross Blue Shield said in a note to providers that it would limit anesthesia coverage in some states if a surgery or procedure exceeded a set time limit (the policy, set to go into effect in February, was swiftly reversed following an uproar).

Americans receive coverage through their employers, government programs like Medicaid or Medicare or by purchasing it themselves — often at a high cost. Even when an individual is covered by insurance, medical coverage can be expensive, with co-pays, deductibles and premiums adding up. Going to an out-of-network provider for care (which can be done unintentionally, for example if you are taken by ambulance to a hospital) can lead to exorbitant bills.

And most people don’t push back — a study found that only 0.1% of denied claims under the Affordable Care Act, a law designed to make health insurance more affordable and prevent coverage denials for pre-existing conditions, are formally appealed. This leaves many people paying out of pocket for care they thought was covered — or skipping treatment altogether.

That is to say nothing of the emotional labor of navigating the complex system. With Thompson’s killing and the Anthem policy, there’s been widespread response with a similar through line: a pervasive contempt for the state of health insurance in the United States. The most illustrative reactions, though are the personal ones, the tales of denied claims, battles with insurance agents, delayed care, filing for bankruptcy and more.

‘We sat in the hospital for three days’

Jessica Alfano, a content creator who goes by @monetizationmom, shared her story on TikTok about battling an insurance company while her one-year-old child was in the hospital with a brain tumor. When her daughter needed to have emergency surgery at a different hospital was outside their home state, UnitedHealthcare allegedly refused to approve the transfer via ambulance to New York City. She also couldn’t drive her daughter to the hospital as the insurance company told them they would not cover her at the next hospital if they left the hospital by their own will and did not arrive by ambulance. “I vividly remember being on the phone with UnitedHealthcare for days and days — nine months pregnant about to give birth alone — while my other baby was sitting in a hospital room,” she said.

While pregnant, Allie, who posts on TikTok as @theseaowl44, went to the hospital in “excruciating pain,” she said in a video. After initially being sent home by a doctor who said she was having pain from a urinary tract infection and the baby sitting on her bladder, she returned to the hospital to learn she was suffering from appendicitis. She was sent to a bigger hospital in St. Louis, where she had emergency surgery. Her son survived the surgery but died the next day after she delivered him.

About 45 minutes later, Allie suffered a pulmonary embolism and had to have an emergency dilation and curettage (D&C) to remove the placenta, nearly dying in the process. It was after all of this that she learned she had been sent to a hospital that was out of network. “We ended up with a bill from the hospital that was more than what we paid for the home that we live in, and it was going to take probably, I don’t know, 20 to 30 years to pay off this hospital bill,” Allie said. “We opted to have to file bankruptcy, but not before I exhausted every appeal with [insurance company] Cigna — I wrote letters, I spilled my heart out, I talked on the phone, I explained our situation and our story, thinking surely someone would understand this was not my fault.

On the third and final appeal, because they only allow you three, Cigna’s appeal physician told me, point blank, it was my fault that when I was dying from a ruptured appendix in the ER, that I didn’t check and make sure that the hospital I was being sent to by ambulance was in my insurance network.”

Hundreds of similar stories are being told, but the comments section on these videos paints a picture in itself. “I wear leg braces and walk with crutches as a paraplegic and they tried to deny my new leg braces and only approve me a wheelchair. They wanted to take my ability to WALK away,” commented TikToker @ChickWithSticks.

“Perfectly healthy pregnancy, until it wasn’t,” TikToker Meagan Pitts shared. “NICU stay was covered by my insurance, the neonatologist group contracted by the NICU: Denied. I’m sorry, what?”

Another wrote that her son was born with a congenital heart defect and needed open heart surgery. “My husband changed jobs & we switched to UHC,” she wrote. “They DENIED my son’s cath lab intervention!”

‘The most stressful time of my life’

One Redditor, @Sweet_Nature_7015, wrote that they struggled with UnitedHealthcare when they and their husband were in a “terrible car accident” that was the other driver’s fault. Since United Healthcare only covered two days in the hospital, the Redditor wrote that the case manager tried to find a way to “kick him out of the hospital” — but since their husband was in a coma, he was unable to be discharged safely. “The stress of being told — your health insurance isn’t covering this anymore, we have to discharge your husband — while he’s in a freaking coma and on a ventilator, etc, rediculous [sic],” they wrote. “I have to sign some papers to give up all of my husband’s benefits via his job – which included his life insurance that he had paid into, so we lost that. This allowed him to be covered by Medicaid. I can’t even put into words how much stress UHC caused on top of my husband (and my) health issues in the most stressful time of my life.”

The kicker, they wrote, was that years later the couple was awarded a court settlement from the other driver in the accident — and “UHC rolled up to the court and took the entire settlement money as their payment for those two days in the hospital they had paid for.”

‘I’m one of the lucky ones’

On the same thread, Redditor @sebastorio wrote that they went to the emergency room for an eye injury, which their doctor said could have resulted in a loss of sight. “UHC denied my claim, and I paid $1,400 out of pocket,” they said. “I’m one of the lucky ones. Can’t imagine how people would feel if that happened for critical or life-saving care.”

‘Constant stream of hostile collection calls’

Redditor @colonelcatsup opened up about their experience with insurance while having a baby, writing that they went into premature labor while insured under one company but that at midnight, their insurance switched to United Healthcare. “I gave birth in the morning. My daughter was two months early and was in the NICU for weeks so the bill was over $80,000 and United refused to pay it, saying it wasn’t their responsibility,” they wrote. “In addition to dealing with a premature baby, I had a constant stream of hostile collection calls and mail from the hospital for 18 months. My credit took a hit.”

Eventually, their employer hired an attorney to fight UHC, and the insurance company eventually paid. “I will never forgive them for the added stress hanging over me for the first year and a half of my child’s life,” they wrote.

‘Debt or death’

On Substack, on which she posted an excerpt from her Instagram, author Bess Kalb also recounted her experience with health insurance coverage when she was bleeding during her pregnancy and was asked by an EMT what insurance she had before deciding whether they would go to the nearest hospital. When her husband said to take Kalb to the hospital, despite not knowing the insurance implications, their bill was more than $10,000.https://www.instagram.com/p/DDNphXCp3Qu/embed/captioned/?cr=1&v=12

“The private insurance industry forces millions of Americans to choose between debt or death,” Kalb wrote. “Often, ghoulishly, the outcome is both. If I were worried about an ambulance out of coverage, I would have waited at home or waited in traffic for an hour to cross Los Angeles to get to my doctor’s office and sat in the waiting room bleeding out and perhaps would not be here to write this, and neither would my son.”

Health policy and politics are inextricably linked. Policy is about what the government can do to shift the financing, delivery, and quality of health care, so who controls the government has the power to shape those policies.

Elections, therefore, always have consequences for the direction of health policy – who is the president and in control of the executive branch, which party has the majority in the House and the Senate with the ability to steer legislation, and who has control in state houses. When political power in Washington is divided, legislating on health care often comes to a standstill, though the president still has significant discretion over health policy through administrative actions. And, stalemates at the federal level often spur greater action by states.

Health care issues often, but not always, play a dominant role in political campaigns. Health care is a personal issue, so it often resonates with voters. The affordability of health care, in particular, is typically a top concern for voters, along with other pocketbook issues, And, at 17% of the economy, health care has many industry stakeholders who seek influence through lobbying and campaign contributions. At the same time, individual policy issues are rarely decisive in elections.

Health “reform” – a somewhat squishy term generally understood to mean proposals that significantly transform the financing, coverage, and delivery of health care – has a long history of playing a major role in elections.

Harry Truman campaigned on universal health insurance in 1948, but his plan went nowhere in the face of opposition from the American Medical Association and other groups. While falling short of universal coverage, the creation of Medicare and Medicaid in 1965 under Lyndon Johnson dramatically reduced the number of uninsured people. President Johnson signed the Medicare and Medicaid legislation at the Truman Library in Missouri, with Truman himself looking on.

Later, Bill Clinton campaigned on health reform in 1992, and proposed the sweeping Health Security Act in the first year of his presidency. That plan went down to defeat in Congress amidst opposition from nearly all segments of the health care industry, and the controversy over it has been cited by many as a factor in Democrats losing control of both the House and the Senate in the 1994 midterm elections.

For many years after the defeat of the Clinton health plan, Democrats were hesitant to push major health reforms. Then, in the 2008 campaign, Barack Obama campaigned once again on health reform, and proposed a plan that eventually became the Affordable Care Act (ACA). The ACA ultimately passed Congress in 2010 with only Democratic votes, after many twists and turns in the legislative process. The major provisions of the ACA were not slated to take effect until 2014, and opposition quickly galvanized against the requirement to have insurance or pay a tax penalty (the “individual mandate”) and in response to criticism that the legislation contained so-called “death panels” (which it did not). Republicans took control of the House and gained a substantial number of seats in the Senate during the 2010 midterm elections, fueled partly by opposition to the ACA.

The ACA took full effect in 2014, with millions gaining coverage, but more people viewed the law unfavorably than favorably, and repeal became a rallying cry for Republicans in the 2016 campaign. Following the election of Donald Trump, there was a high profile effort to repeal the law, which was ultimately defeated following a public backlash. The ACA repeal debate was a good example of the trade-offs inherent in all health policies. Republicans sought to reduce federal spending and regulation, but the result would have been fewer people covered and weakened protections for people with pre-existing conditions. KFF polling showed that the ACA repeal effort led to increased public support for the law, which persists today.

The 2024 election presents the unusual occurrence of two candidates – current vice president Kamala Harris and former president Donald Trump – who have already served in the White House and have detailed records for comparison, as explained in this JAMA column. With President Joe Biden dropping out of the campaign, Harris inherits the record of the current administration, but has also begun to lay out an agenda of her own.

While Trump failed as president to repeal the ACA, his administration did make significant changes to it, including repealing the individual mandate penalty, reducing federal funding for consumer assistance (navigators) by 84% and outreach by 90%, and expanding short-term insurance plans that can exclude coverage of preexisting conditions.

In a strange policy twist, the Trump administration ended payments to ACA insurers to compensate them for a requirement to provide reduced cost sharing for low-income patients, with Trump saying it would cause Obamacare to be “dead” and “gone.” But, insurers responded by increasing premiums, which in turn increased federal premium subsidies and federal spending, likely strengthening the ACA.

In the 2024 campaign, Trump has vowed several times to try again to repeal and replace the ACA, though not necessarily using those words, saying instead he would create a plan with “much better health care.”

Although the Trump administration never issued a detailed plan to replace the ACA, Trump’s budget proposals as president included plans to convert the ACA into a block grant to states, cap federal funding for Medicaid, and allow states to relax the ACA’s rules protecting people with preexisting conditions. Those plans, if enacted, would have reduced federal funding for health care by about $1 trillion over a decade.

In contrast, the Biden-Harris administration has reinvigorated the ACA by restoring funding for consumer assistance and outreach and by increasing premium subsidies to make coverage more affordable, resulting in record enrollment in ACA Marketplace plans and historically low uninsured rates. The increased premium subsidies are currently slated to expire at the end of 2025, so the next president will be instrumental in determining whether they get extended. Harris has vowed to extend the subsidies, while Trump has been silent on the issue.

The health care issue most likely to figure prominently in the general election is abortion rights, with sharp contrasts between the presidential candidates and the potential to affect voter turnout. In all the states where voters have been asked to weigh in directly on abortion so far (California, Kansas, Kentucky, Michigan, Montana, Ohio, and Vermont), abortion rights have been upheld.

Trump paved the way for the US Supreme Court to overturn Roe v Wade by appointing judges and justices opposed to abortion rights. Trump recently said, “for 54 years they were trying to get Roe v Wade terminated, and I did it and I’m proud to have done it.” During the current campaign, Trump has said that abortion policy should now be left to the states.

As president, Trump had also cut off family planning funding to Planned Parenthood and other clinics that provide or refer for abortion services, but this policy was reversed by the Biden-Harris administration.

Harris supports codifying into federal the abortion access protections in Roe v Wade.

Addressing the High Price of Prescription Drugs and Health Care Services

Trump has often spotlighted the high price of prescription drugs, criticizing both the pharmaceutical industry and pharmacy benefit managers. Although he kept the issue of drug prices on the political agenda as president, in the end, his administration accomplished little to contain them.

The Trump administration created a demonstration program, capping monthly co-pays for insulin for some Medicare beneficiaries at $35. Late in his presidency, his administration issued a rule to tie Medicare reimbursement of certain physician-administered drugs to the prices paid in other countries, but it was blocked by the courts and never implemented. The Trump administration also issued regulations paving the way for states to import lower-priced drugs from Canada. The Biden-Harris administration has followed through on that idea and recently approved Florida’s plan to buy drugs from Canada, though barriers still remain to making it work in practice.

With Harris casting the tie-breaking vote in the Senate, President Biden signed the Inflation Reduction Act, far-reaching legislation that requires the federal government to negotiate the prices of certain drugs in Medicare, which was previously banned. The law also guarantees a $35 co-pay cap for insulin for all Medicare beneficiaries, and caps out-of-pocket retail drug costs for the first time in Medicare. Harris supports accelerating drug price negotiation to apply to more drugs, as well as extending the $35 cap on insulin copays and the cap on out-of-pocket drug costs to everyone outside of Medicare.

How Trump would approach drug price negotiations if elected is unclear. Trump supported federal negotiation of drug prices during his 2016 campaign, but he did not pursue the idea as president and opposed a Democratic price negotiation plan. During the current campaign, Trump said he “will tell big pharma that we will only pay the best price they offer to foreign nations,” claiming that he was the “only president in modern times who ever took on big pharma.”

Beyond drug prices, the Trump administration issued regulations requiring hospitals and health insurers to be transparent about prices, a policy that is still in place and attracts bipartisan support.

Ultimately, irrespective of the issues that get debated during the campaign, the outcome of the 2024 election – who controls the White House and Congress – will have significant implications for the future direction of health care, as is almost always the case.

However, even with changes in party control of the federal government, only incremental movement to the left or the right is the norm. Sweeping changes in health policy, such as the creation of Medicare and Medicaid or passage of the ACA, are rare in the U.S. political system. Similarly, Medicare for All, which would even more fundamentally transform the financing and coverage of health care, faces long odds, particularly in the current political environment. This is the case even though most of the public favors Medicare for All, though attitudes shift significantly after hearing messages about its potential impacts.

Importantly, it’s politically difficult to take benefits away from people once they have them. That, and the fact that seniors are a strong voting bloc, has been why Social Security and Medicare have been considered political “third rails.” The ACA and Medicaid do not have quite the same sacrosanct status, but they may be close.

The fate of billions of dollars of Affordable Care Act subsidies is riding on the election, which will also determine how much the next Congress will be consumed with relitigating the law.

Why it matters:

Enhanced ACA subsidies expire at the end of 2025 without congressional action. They’ve substantially lowered consumers’ premiums and driven more enrollment in marketplace plans, though at a hefty cost to the government.

Driving the news:

Although the fight over repealing the ACA itself has faded, the partisan battle is shifting to the fate of the enhanced subsidies, passed as part of the American Rescue Plan Act and then extended via the Inflation Reduction Act.

If Republicans win both chambers of Congress and the presidency, they’re strongly expected to let the subsidies expire.

But if Democrats win the presidency or even partial control of Congress, there’s a good chance for a prolonged debate and, possibly, a grand bargain to extend them.

Sen. Bill Cassidy, the top Republican on the HELP Committee, tied the fate of the subsidies to the election results when asked what’s ahead.

“Tell me, do Republicans have everything, do Democrats have everything, or is it divided government?” he told Axios.

By the numbers:

The enhanced subsidies have cut premium costs an average of 44%, or $705 per year, for qualified ACA enrollees, according to a KFF analysis.

“If they expire, the uninsured rate would jump and people would see huge premium increases,” said Larry Levitt, KFF’s executive vice president for health policy.

The CBO finds that extending them would raise the deficit by $335 billion over 10 years and increase the number of people with health coverage by 3.4 million.

Some Republicans are portraying the continuation of subsidies as a sop to health insurers.

“At a time when we are experiencing a record $35 trillion national debt … it is unconscionable that Democrats would continue to push for massive taxpayer-funded handouts to the wealthy and large health insurance companies,” House Budget Chair Jodey Arrington and Ways and Means Chair Jason Smith said in a joint statement responding to the CBO estimate.

What they’re saying:

“I think just not doing the enhanced subsidies, I would take that as a win for 2025,” said Brian Blase, a former Trump administration health adviser now president of Paragon Health Institute.

He pointed to the cost, also arguing that enhanced subsidies incentivize fraud, with ineligible people enrolling in zero-premium plans. “They’re associated with an unprecedented level of fraud,” he said.

“It’s entirely possible that some people are fraudulently misestimating their income,” Levitt said. But, he noted, many low-income people simply lead “volatile lives” and don’t always know what their income will be in a coming year.

What’s next:

Senate Finance Chair Ron Wyden told Axios he wants to combine an extension of the enhanced subsidies with a bill he’s sponsored that would crack down on unscrupulous insurance brokers, to help counter GOP arguments about fraud.

“I think it would be a real good package to crack down on these insurance scams and these brokers ripping off the ACA and focus on something that actually helps people, which is the premium [tax credits],” Wyden said.

The expiration of some of the 2017 Trump tax cuts next year also could provide an opening for a deal with Republicans to extend the ACA subsidies in divided government.

The bottom line:

Levitt said that although some of the repeal fervor has faded, “the future of the program, the future success of the program, very much depends on these enhanced subsidies.”

In the Congressional Budget Office’ latest report on the status of health insurance coverage from the 2023 National Health Interview Survey released last week, a cautiously optimistic picture of coverage is presented:

“In 2023, 25.0 million people of all ages (7.6%) were uninsured at the time of interview. This was lower than, but not significantly different from 2022, when 27.6 million people of all ages (8.4%) were uninsured. Among adults ages 18 64, 10.9% were uninsured at the time of interview, 23.0% had public coverage, and 68.1% had private health insurance coverage.

The percentage of adults ages 18-64 who were uninsured in 2023 (10.9%) was lower than the percentage who were uninsured in 2022 (12.2%).

Among children ages 0–17 years, 3.9% were uninsured, 44.2% had public coverage, and 54.0% had private health insurance coverage.

The percentage of people younger than age 65 with exchange-based coverage increased from 3.7% in 2019 to 4.8% in 2023.”

That represents the highest level of coverage in modern history. Later, it adds important context: The percentage of adults ages 18–64 who were uninsured decreased between 2019 and 2023 for all family income groups shown except for adults in families with incomes greater than 400% FPL. Notably, a period in which the Covid-19 pandemic prompted federal government’s emergency funding so households and businesses could maintain their coverage.

“Among adults with incomes below 100% FPL, the percentage who were uninsured in 2023 (20.2%) was lower than, but not significantly different from, the percentage who were uninsured in 2022 (22.7%).

Among adults with incomes 100% to less than 200% FPL, the percentage who were uninsured decreased from 22.3% in 2022 to 19.1% in 2023.

Among adults with incomes 200% to 400% FPL, the percentage who were uninsured decreased from 14.2% in 2022 to 11.5% in 2023.

No significant difference was observed in the percentage of adults with incomes above 400% FPL who were uninsured between 2022 (4.1%) and 2023 (4.3%).”

In 2023, among adults ages 18–64, the percentage who were uninsured was highest among health insurance coverage of any type was higher for those with higher household income but decreased coverage in 2023 correlated to ethnicity, non-expansion of state Medicaid programs: From 2019 to 2023.”

And decreases in the ranks of the uninsured were noted across all ethnic groups:

Among Hispanic adults, from 29.7% to 24.8%

Among Black non-Hispanic adults, from 14.7% to 10.4% in 2023

Among White non-Hispanic adults, decreased from 10.5% to 6.8%

Among Asian non-Hispanic adults, from 8.8% to 4.4% in 2023.

The New York Times noted “The drops cut significantly into gaps between ethnic groups.The uninsured rate among Black Americans, for example, was almost 8% higher than for white Americans in 2010, and was only 4%higher in 2022. The data points to the broad effects of the Affordable Care Act, the landmark law President Barack Obama signed in 2010 that created new state and federal insurance marketplaces and expanded Medicaid to millions of adults. National uninsured rates have continued to drop in recent years, hitting a record low in early 2023.”

But the report also flags a reversal of the trend: “The uninsured share of the population will rise over the course of the next decade, before settling at 8.9% in 2034, largely as a result of the end of COVID-19 pandemic–related Medicaid policies, the expiration of enhanced subsidies available through the Affordable Care Act health insurance Marketplaces, and a surge in immigration that began in 2022. The largest increase in the uninsured population will be among adults ages 19–44. Employment-based coverage will be the predominant source of health insurance, and as the population ages, Medicare enrollment will grow significantly. After greater-than-expected enrollment in 2023, Marketplace enrollment is projected to reach an all-time high of twenty-three million people in 2025.”

My take:

A close reading of this report suggests its forecast might be overly optimistic. it paints a best-case picture of health insurance coverage that under-estimates the realities of household economics and marketplace trends and over-estimates the value proposition promoted by health insurers to their customers. My conclusion is based on four trends that suggest coverage might slip more than the report suggests:

The affordability of healthcare insurance is increasingly problematic to lower- and middle-income households who face inflationary prices for housing, food, energy and transportation. The CBO report verifies that household income is key to coverage and working age populations are most-at risk of losing its protections. Subsidies to fund premiums for those eligible, employer plans that expose workers to high deductibles and increased non-covered services are likely to push fewer to enroll as premiums become unaffordable to working age adults and unattractive to their employers. As outlined in a sobering KFF analysis, half of the adult population is worried about the affordability of their healthcare—and that includes 48% who have health insurance. And wages in the working age population are not keeping pace with prices for food, shelter and energy, leaving healthcare expenses including their insurance premiums and out-of-pocket obligations at greater risk.

The value proposition for health insurance coverage is eroding among employers, consumers and lawmakers. To large employers that provide employee insurance, medical costs are forcing benefits reduction or cessation altogether. Insurance has not negated their medical costs. To small employers, it’s an expensive bet to recruit and keep their workforce. To government sponsors (i.e. Medicare, Medicaid, VHA, et al), insurance is a necessary but increasingly expensive obligation with growing dependence on private insurers to administer their programs. State and federal regulators are keen to limit public spending and address disparities in their public insurance programs. All recognize that private insurers play a necessary role in the system and all recognize that confidence in health insurance protections is suspect. Thus, increased regulation of private insurers is likely though unwelcome by its members.

Public funding for government payers will be increasingly limited increasing insurer dependence on private capital for sustainability and growth. Funding for Medicare, Medicaid, Veterans and Military Health, Public Health et al are dependent on appropriations and tax collections. All are structured to invite private insurer participation: all are seeing corporate insurers seize market share from their weaker competitors. The issues are complex and controversial as evidenced by the ongoing debates about fairness in Medicare Advantage and administration of Medicaid expansion among others. And polls indicate widespread dissatisfaction with the system and lack of confidence in its insurers, hospitals, physicians or the government to fix it.

Access to private capital for private health insurers is shrinking enabling corporate insurers to play bigger roles in financing and delivering services. Private investments in healthcare services (i.e. hospitals, physicians, clinics) has slowed and momentum has shifted from sellers to buyers seeking less risk and higher returns. Capital deployment by corporate insurers i.e. UHG, HUM et al has resulted in vertically-integrated systems of health inclusive of physician services, drug distribution, ASCs and more. And funding for AI-investments that lower their admin costs and increase their contracting leverage with providers is a strategic advantage for corporate insurer that operate nationally at scale. Unless the federal government bridles their growth (which is unlikely), corporate insurers will control national coverage while others fail.

Thus, no one knows for sure what coverage will be in 2034 as presented in the CBO report. Its analysis appropriately considers medical inflation, population growth and an incremental shift to value-based purchasing in healthcare, but it fails to accommodate highly relevant changes in the capital markets, corporate insurer shareholder interests and voter sentiment.

P.S. This is an important week for healthcare: Today marks the two-year anniversary of the Supreme Court’s Dobbs decision that overturned Roe v. Wade, ending the constitutional right to an abortion that pushed reproductive rights to states.

And Thursday in Atlanta, President Joe Biden and former President Donald Trump will make history in the first presidential debate between an incumbent and a former president.

Reproductive rights will be a prominent theme along with immigration and border security as wedge issues for voters.

The economy and inflation are the issues of most consequence to most voters, so unless the campaigns directly link healthcare spending and out of pocket costs to voter angst about their household finances, not much will be said.

Notably, half of the U.S. population have unpaid medical bills and medical debt is directly related to their financial insecurity. Worth watching.

One of the things I’ve always found most fascinating about news coverage and policymaker attention to health insurers is how little focus is placed on what these companies say to their investors.

It’s no secret that each quarter, all public companies update their shareholders and provide guidance for the future. When I was at Cigna, preparing the CEO to speak with reporters and investor analysts was arguably considered the most important role I had every three months.

Mining insights from those earnings reports has been a focus of mine since I became an insurance industry whistleblower. Recently, for example, we’ve highlighted how CVS/Aetna, in particular, has taken a beating on its stock price for reporting increased spending on medical care by seniors in Medicare Advantage plans.

Now, though, CEOs have become even more public and open, beyond their quarterly earnings calls, about the challenges they are having extracting further profit from the Medicaid and Medicare programs. This should be noted, particularly by the bipartisan group of lawmakers in Washington increasingly eyeing regulatory reform on insurer practices like prior authorization, as evidence that insurers are going to become even more aggressive in limiting care to preserve their 2024 profits.

Centene’s CEO saida few days ago that medical claims are increasing in the company’s managed Medicaid business. UnitedHealth and Elevance, which owns several Blue Cross Blue Shield companies that have converted to for-profit status, also recently reported they’re seeing similar results. Combined with increased medical spending on Medicare Advantage claims, one might guess this would begin to worry investors that insurers would lower their profit forecasts.

But none of these companies have so far expressed concern about not meeting their 2024 profit expectations.

So, medical claims in Medicaid and Medicare Advantage plans – now the majority of the business for many of the largest insurers – are rising, but these companies aren’t expecting to disappoint Wall Street with a drop in profits. How is that possible?

Because insurers can deploy the tools to prevent patients from accessing care. And their playbook isn’t secret, or complicated.

By further increasing prior authorization in Medicaid and Medicare Advantage plans, insurers can limit how many seniors and low-income Americans follow through with legitimate care and procedures. (Here’s a recent congressional report on increased hurdles insurers have put in place to prevent children from receiving preventive care in Medicaid plans. And insurers’ increasing use of prior authorization in Medicare Advantage is something we’ve regularly covered.)

Unlike their marketplace and employer-based plans, insurers can’t negotiate reimbursement rates for Medicaid and Medicare Advantage plans that they manage.

But beyond prior authorization, they can put other layers of bureaucracy in place that increase how long it takes a provider to be reimbursed for providing care – and to make it more complicated for doctors to ensure they’re reimbursed fully for the care they provide.

In effect, these tactics can amount to decreasing the already industry-low rate of reimbursement for doctors from the Medicaid and Medicare Advantage programs. Physicians, you should expect to see more hurdles to reimbursement in these programs throughout the balance of 2024 as insurers look to hoard as much cash as they can.

In Medicare Advantage plans, insurers can pursue the industry jargon of a “benefit buydown” to further shift costs onto plan enrollees and off insurers themselves. Because the federal government pays insurers a flat amount per Medicare Advantage enrollee, regardless of how much health care spending each patient has, it is in the insurers’ financial interest to claim that seniors and disabled people enrolled in their plans are sicker than they really are.

Rising out-of-pocket costs that seniors and disabled people in Medicare Advantage plans are facing is a consequence of insurers wanting to squeeze further profits out of the program, and is a way to maintain direct government payments per enrollee within the insurers’ coffers.

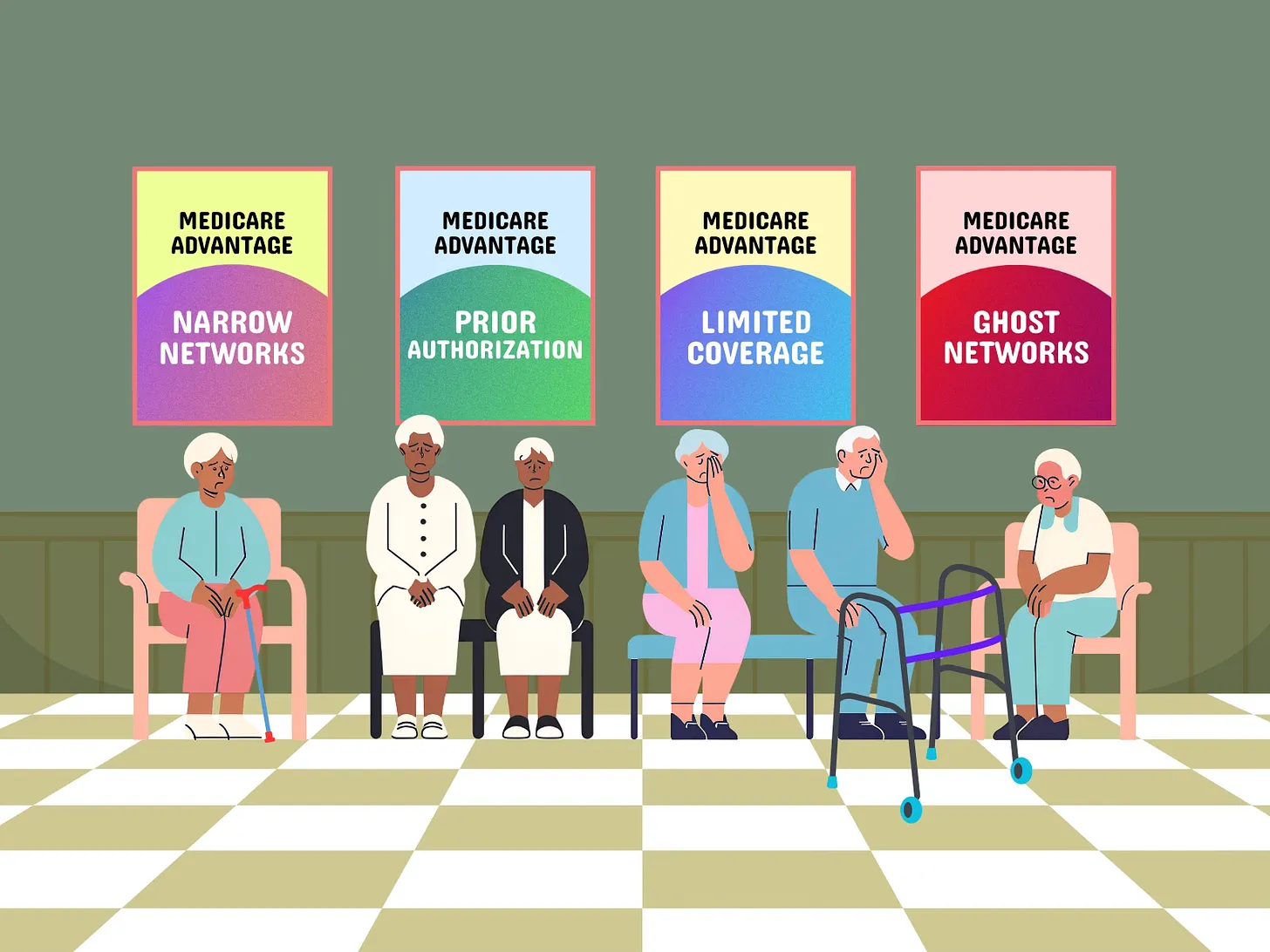

Physicians for a National Health Program estimate nearly 12 million seniors are in a Medicare Advantage plan that excludes more than 70% of doctors in their county.

Negative stories about Medicare Advantage (MA) insurers are finally making it to mainstream media after percolating below the surface for years. More and more patients, physicians, and even health care executives are speaking up about the disastrous expansion of this program. Shockingly, some of these stories have come from the insurance companies themselves.

With no hint of shame or irony, executives like CFO Thomas Cowhey of CVS Health have delivered lines such as “The goal next year is margin over membership,” making explicit that more money is their mantra. With all these reports of limited networks, care denials, delayed payments, and corporate greed, you may feel like the story of MA can’t get any worse.

Impossibly, it does. Physicians for a National Health Program (PNHP) has just recently released a bombshell report exposing the sheer breadth of harm that MA insurers have done to patients and health care workers across the country. The report combines policy analysis of dozens of academic studies, news reports, and government investigations with personal stories from people hurt by the insurance companies running these plans. We want to take some time to explore the report’s findings, and highly encourage you to read it in full as well.

Patients in MA experience difficulties from the moment they begin to seek care. By PNHP’s estimate, 11.7 million beneficiaries are in a plan that excludes more than 70% of doctors in their county. These narrow networks mean that patients often have to travel hours for an appointment, and can’t see their preferred family physician or the right specialist for their condition. This can have dire consequences.

One study found that cancer patients in MA are less likely to be treated at teaching hospitals, Commission on Cancer-accredited hospitals, or National Cancer Institute-designated centers. As a result, these patients suffer higher mortality rates following surgery for a number of kinds of cancer, with some cancer patients in MA plans being twice as likely to die as those in traditional Medicare.

Put simply, narrow networks designed to reap profits in MA are killing patients.

Even if they’re able to find the right doctor, getting care doesn’t become any easier. MA insurers almost always require prior authorization for standard, evidence-based tests, procedures, and treatments, making patients wait weeks or even months to get the life-saving care they need now.

In one story from the report, a physician recounts how damaging this practice can be:

I had a patient with several chronic diseases who was very sick and had just survived major abdominal surgery, almost miraculously. In the aftermath, she desperately needed to go to acute rehab, which is the most intensive rehab – we found a facility, she liked it, her family liked it, and then her MA plan looked at the place and said ‘No, she’s healthy enough to not go to acute rehab, we won’t authorize it.’ This was after our PM&R specialist, physical therapist, and 3 MDs on our team had told her she needed acute rehab, and that it was the only thing that would keep her out of the hospital again. And this insurer, without anyone ever looking at her, rejected that conclusion. And we knew that on traditional Medicare this never would’ve happened.

Prior authorization is also a gigantic waste of time and resources for doctors and health care workers who want to spend that time caring for patients. PNHP found that medical practices are forced to waste between 11.1 and 20.5 million hours per year filling out authorization forms and fighting with insurance companies to get necessary care approved.

Much of this is done arbitrarily, wearing patients down with bureaucracy so the insurance company doesn’t have to pay for treatment. When challenged on appeal, somewhere around 80% of denials are reversed, proving there was no good medical reason for the denial in the first place.

Assuming you can find a doctor in your narrow network, and that your doctor makes it through the red-tape nightmare to get your necessary care approved, you may then find yourself dealing with severely limited coverage and thousands of dollars in medical bills. In fact, 7.3 million beneficiaries in MA are considered underinsured based on their reporting of high health care costs. Seniors and people with disabilities are often enticed into MA by advertisements or insurance brokers who tout low premiums and supplemental benefits as big perks of their plans, only to find that once they actually become sick, coverage dries up fast.

After experiencing all of these hardships, many beneficiaries find themselves wanting to get out of MA and go to traditional Medicare, and studiesshow that those who are seriously ill or who have high health care costs indeed switch out of the program at high rates. Unfortunately, if you stay in MA too long, you may be trapped in the program for good.

For the first twelve months someone is in MA, they have a guarantee that no Medigap insurer can deny them a policy. However, once this period is up, this guarantee disappears in 46 of 50 states.

If you decide to switch back to traditional Medicare after a year, you are no longer guaranteed to receive this coverage, and you can be denied a policy on the basis of “pre-existing conditions,” a practice that most believe was fully outlawed following the passage of the Affordable Care Act.

Imagine you get sick while in MA, and rack up thousands of dollars in medical bills that you can’t pay. When you try to switch to traditional Medicare, you can be denied Medigap coverage because of the very illness that made you need to leave MA. Many people simply cannot afford Medicare without Medigap, meaning their only option is to stay in their MA plan.

If all of this seems crazy, that’s because it is. Medicare Advantage is a total rejection of the founding principles of Medicare and health care in general, and every harmful practice in this report is done in the name of profit. Restricting networks, denying care, refusing to cover costs–these are all ways that insurance companies in MA keep our taxpayer dollars while leaving patients and health care workers to deal with the consequences. We need to work together to get these greedy middlemen out of Medicare before they take it over entirely. Our hard-earned dollars should be going to traditional Medicare, the program that actually serves its constituents.

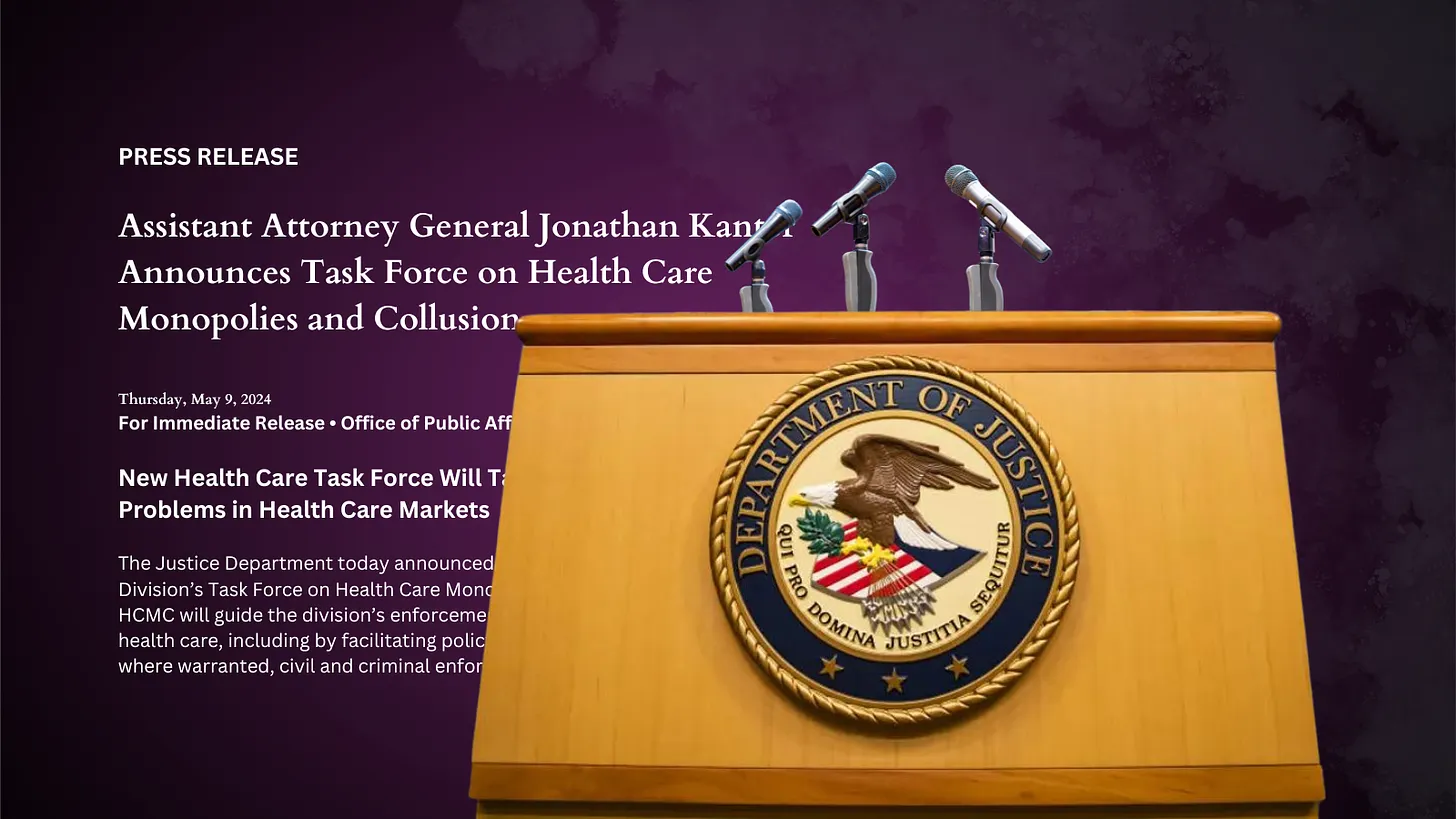

Abuses by payers are myriad, but these five areas could bear the most fruit for federal antitrust investigators.

Earlier this month, the U.S. Department of Justice announced it has haunched an investigation into “issues regarding payer-provider consolidation” along with other problems associated with mergers and acquisitions in health care. This is significant. For years Washington has trained its oversight authority on pharmaceutical manufacturers, private equity investments in health care and, more recently, pharmacy benefits managers controlled by big insurers. This has held bad actors like Martin Skhreli and Steward Healthcare accountable. But, it has also let insurers grow ever larger, under the radar.

No longer.

This task force will specifically evaluate the following, as an example: “A health insurance company buys several medical practices that compete with each other. It also prohibits its medical practices from contracting with rival health insurance companies.” The government will also dig into “anticompetitive uses of health care data,” “preventing transparency,” “price fixing,” and other areas that could drag nefarious activities of insurers into the spotlight.

I applaud the Department of Justice’s continued focus on these issues, building on the Department’s action announced in February to begin an antitrust investigation into UnitedHealth Group. (If you haven’t read the piece we published in February on UnitedHealth’s self-dealing that helped lead DOJ to open that antitrust inquiry, you can do so here.) The following are a few areas of low-hanging fruit that I hope the task force will focus on as they consider the impact insurers’ ongoing vertical integration has had on the overall health care system.

1. Insurers purchasing physician practices

Once a low-profile issue, Congress and the Biden administration alike have increasingly turned their focus to insurance companies – often referred to as payers – that now own and operate physician practices and clinics – those being paid. Even for someone without a law degree, it is easy to see the conflict this creates, particularly at scale.

There is the oft-cited statistic that UnitedHealth has said that through its Optum division, the company employs or otherwise controls about 10 percent of doctors in the U.S. – around 130,000 physicians and other practitioners in 16 states. This prompted me to take a closer look at publicly available information on the number of doctors employed by other insurers to get a better handle on how much control of physician practices payers now have.

It is difficult to put a percentage on physicians employed by each insurer, but it is clear that the others are following UnitedHealth’s lead. CVS/Aetna purchased Signify Health in 2023, adding 10,000 clinicians to its portfolio. The company says it supports “more than 40,000 physicians, pharmacists, nurses and nurse practitioners.”

Clearly taking a page out of UnitedHealth’s playbook, Elevance (formerly Anthem), which owns Blue Cross Blue Shield plans in 14 states announced last month a “strategic partnership” with 900 providers across several states. Elevance did not disclose the terms of the deal except to say it, “will primarily be through a combination of cash and our equity interest in certain care delivery and enablement assets of Carelon Health.”

As insurers have acquired physician practices, they also have created a rinse-and-repeat strategy associated with kicking physicians they don’t own out of network, and in some cases targeting those same practices for acquisition. Aetna and Humana recently told investors they will be reviewing their networks of physicians, signaling they’ll soon be further narrowing their networks. A good question for this task force: when insurers review those contracts with doctors, do they ever kick the doctors they employ out of network? (Doubtful.) This could specifically draw attention from the task force’s focus on “health care contract language and other practices that restrict competition,” such as contract provisions that require or encourage patients to seek care from doctors directly employed or closely controlled by patients’ insurers.

Additionally, UnitedHealth CEO Andrew Witty recently told analysts, “As I think you see some of the funding changes play out across the — across the next few years, I suspect that may also create new opportunities for us as different companies assess their positions.” My translation:UnitedHealth’s burdensome business practices and the way it shortchanges doctors (those “funding changes” he referenced) contribute to the financial distress that is forcing many health care providers to “assess their positions.”

As the task force continues to consider the impact of private equity in health care monopolies, transactions like this one should receive equal consideration for their lack of transparency and overall impact on market consolidation.

2. Co-mingling of middlemen

I have watched with interest for over the past year as both Democrats and Republicans in Washington increasingly trained their fire on pharmacy benefit managers. The natural next area of focus in that space, which this new task force could advance, should be around how the

three PBMs that control 80 percent of market share are all combined with health insurance companies – namely CVS/Aetna (Caremark), UnitedHealth (Optum Rx), and Cigna (Express Scripts).

An important, and politically popular, area where this consolidation has played out is in the squeeze placed on small, independent pharmacists across the country. More than 300 community pharmacies have closed in the past year alone, out of an inability to operate or push back on unfair margins pushed by these PBM-insurer monopolies. As we have written here, the fees these PBMs charge have increased more than 100,000 percent over the past decade, and are quietly contributing significantly to the profits of the largest health insurers.

We still have little insight into how these business lines interact with each other, and the ultimate impact that has on patients. Given the enormous influence just three insurance companies have over what prescriptions Americans can receive, and how much should be paid for each prescription, the task force would do well to focus on what insurers and PBMs are doing behind the scenes to maximize profits and limit patient access to prescription drugs. It’s already gaining traction on Capitol Hill, with one Congressman recently saying, “I’ll continue to bust this up … this vertical integration in health care.”

3. Prior authorization requests

CVS/Aetna shares were hammered after the company reported a significant increase in payment of Medicare Advantage claims during the first three month is of this year. Expect all insurers to notice. And as they have seen their forecasts fall short of Wall Street’s expectations – particularly because of increasing scrutiny in Washington of Medicare Advantage – these corporations will look to increase their already aggressive use of prior authorization to limit claims payments.

It is not as though insurers make seeking the care you need easy. Far from it. Prior authorization has become “medical injustice disguised as paperwork,” as the New York Times said in a recent, excellent video detailing the widespread nature of this profiteering practice.

While not a stated direct focus of this task force, the increased impact of prior authorization in care delivery is a direct outgrowth of a few large health insurers effectively controlling the marketplace. As insurers directly employ more doctors and enroll more Americans in their plans, they can use prior authorization to increasingly determine whether a patient can get care, period.

Scrutiny in this space could add momentum to increasing activity in state legislatures and Washington to rein in excessive prior authorization. As of early March, nine states and the District of Columbia had passed bills to limit how far insurers could go with prior authorization. And earlier this year, the Centers for Medicare and Medicaid released a final rule that is expected to save physicians $15 billion over the next decade by putting limits on insurer prior authorization tactics.

4. Rising out-of-pocket costs

Regular readers of this newsletter know one of my crusades is to ensure folks who pay good money for health insurance – out of their paychecks or through their tax dollars – can use it when they need it. It was a big win earlier this year for the Lower Out of Pockets Now coalition (which I lead) when President Biden called for a cap on prescription drug out-of-pocket costs of $2,000 annually for everybody, not just Medicare beneficiaries.

If there was true competition and real consumer choice in health insurance, payers wouldn’t be able to get away with increasingly shifting patients into high-deductible plans. But the fact that a few big players control the health insurance market has allowed the oligopoly of payers to do just that, with ever-rising deductibles alongside ever-rising premiums.

The task force’s focus on price fixing, collusion, and transparency in health care costs will, I hope, include some focus on how insurers use their size and clout to drive up out-of-pocket costs and premiums simultaneously – with little recourse to employers or their employees.

5. Implementing crystal clear laws and rules in health care

You know you’re a monopoly or close to it when you can pretty much do whatever you want and get away with it. Look no further than America’s health insurance companies and implementation of the No Surprises Act.

As I wrote earlier this year, Congress and CMS have been clear about how out-of-network hospital bills should be negotiated between insurers and physicians. Yet in case after case, including many that have become the basis of lawsuits, insurers are clearly flouting the Act passed by Congress and the rules promulgated by CMS. Payers are doing this, doctors have said, simply because of their size and ability to weather criticism from physicians, regulators, and the courts – while doctors struggle to pay their bills with significant payments still owed pending out-of-network negotiations with insurers.

One would hope, at a minimum, this task force, focused on rooting out the ills of monopolies, would document how insurers are well aware of how they are supposed to implement legislation like the No Surprises Act, but flout it anyway.