Published in the April edition of Health Affairs Forefront, this piece unpacks why payers and other corporations have replaced health systems as the top bidders for primary care practices, driving up practice purchase prices from hundreds of dollars to tens of thousands of dollars per patient. While corporate players like UnitedHealth Group, Amazon, and Walgreens have spent an estimated $50B on primary care, it pales in comparison to the potential “$1T opportunity” in value-based care projected by McKinsey and Company.

The authors argue that this tantalizing opportunity exists because the Centers for Medicare and Medicaid Services (CMS) invited corporations to “re-insure” Medicare through capitated arrangements in Medicare Advantage (MA) and its Direct Contracting program.

While CMS intended to promote risk and value-based incentives to improve care quality and costs, the incentive structures baked into these programs have afforded payers record profits, despite neither improving patient outcomes nor reducing government healthcare spending.

The Gist: While the critiques of MA reimbursement structures in this piece are familiar, they are woven together into a convincing rebuke of the “unintended consequences” of CMS’s value-based care policy.

Through poorly designing incentives, CMS paved a runway for corporate America to capture the lion’s share of the financial returns of value-based care, paying prices for primary care that health systems can’t match.

Meanwhile, despite skyrocketing valuations for primary care practices, primary care services remain underfunded and inadequately reimbursed, pushing primary care groups closer to payers with excess profits to invest.

Running a health system recently has proven to be a very hard job. Mounting losses in the face of higher operating expenses, softer than expected volumes, deferred capex, and strained C-suite succession planning are just a few of the immediate issues with which CEOs and boards must deal.

But frankly, none of those are the biggest strategic issue facing health systems. The biggest strategic issue is the reorganization of the American healthcare landscape into an ambulatory care business that emphasizes competing for covered lives at scale in lower cost and convenient settings of care. This shift in business model has significant ramifications, if you own and operate acute care hospitals.

Village MD and Optum are two of the organizations driving the business model shift. They are owned by large publicly traded companies (Walgreens and UnitedHealth Group, respectively). Both Optum and Village MD have had a string of announced major patient care acquisitions over the past few years, none of which is in the acute care space.

The future of American healthcare will likely be dominated by large well-organized and well-run multi-specialty physician groups with a very strong primary care component. These physician service companies will be payer agnostic and focused on value-based care, though will still be prepared to operate in markets where fee-for-service dominates. They will deliver highly coordinated care in lower cost settings than hospital outpatient departments. And these companies will be armed with tools and analytics that permit them to manage the care for populations of patients, in order to deliver both better health outcomes and lower costs.

At the same time this is happening, we are experiencing steady growth in Medicare Advantage. And along with it, a stream of primary care groups who operate purpose-built clinics to take full risk on Medicare Advantage populations. These companies include ChenMed, Cano Health and Oak Street, among others. These organizations use strong culture, training, and analytics to better manage care, significantly reduce utilization, and produce better health outcomes and lower costs.

Public and private equity capital are pouring into the non-acute care sectors, fueling this growth. As of the start of 2022, nearly three quarters of all physicians in the US were employed by either corporate entities (such as private equity, insurance companies, and pharmacy companies), or employed by health systems. And this employment trend has accelerated since the start of the pandemic. The corporate entities, rather than health systems, are driving this increasing trend. Corporate purchases of physician practices increased by 86% from 2019 to 2021.

What can health systems do? To succeed in the future, you must be the nexus of care for the covered lives in your community. But that does not mean the health system must own all the healthcare assets or employ all of the physicians. The health system can be the platform to convene these assets and services in the community. In some respects, it is similar to an Apple iPhone. They are the platform that convenes the apps. Some of those apps are developed and owned by Apple. But many more apps are developed by people outside of Apple, and the iPhone is simply the platform to provide access.

Creating this platform requires a change in mindset. And it requires capital. There are many opportunities for health systems to partner with outside capital providers, such as private equity, to position for the future – from both a capital and a mindset point of view.

The change in mindset, and the access to flexible capital, is necessary as the future becomes more and more about reorganizing into an ambulatory care business that emphasizes competing for covered lives at scale in lower cost and convenient settings of care.

Cross-subsidy economics are increasingly challenged for America’s hospitals. Aging Baby Boomers are moving from commercial insurance to Medicare, decreasing the share of patients with lucrative private coverage, and insurers are increasingly reticent to provide the rate increases providers need to make up for the worsening mix.

At a recent executive retreat, one health system debated the best strategies to increase their capture of commercial volume. Most of the conversation focused on traditional market-based tactics to increase access and awareness in fast-growing, higher income areas of their service region.

For instance, the system’s chief marketing officer was pushing to increase advertising in the rapidly expanding suburbs, and advocated building ambulatory surgery centers in a wealthy area of town with a boom of new home construction.

The chief strategy officer shared a different perspective, supporting an employer-focused strategy. His logic: “In most businesses,the CEO and the janitor have the same benefit plans. If we only focus on the wealthy parts of town, we’re missing a big portion of the workers with good insurance.” He advocated for a new round of direct-to-employer contracting outreach, hoping to steer workers to high-value primary and specialty care solutions.

In reality, any system looking to move commercial share will need to do both—but even the best playbook for building commercial volume is unlikely to close the growing cross-subsidy gap. To maintain profitability in the long term, health systems must reduce costs for managing Medicare patients by delivering lower-cost care in lower-cost settings, with lower-cost staff.

While healthcare is delivered locally, the business of healthcare is regional, and the regions are only getting bigger. Hospital and health system mergers alike have continued to shift from local to regional, and the recently announced merger between Advocate Aurora Health and Atrium Health clearly highlights that the regions are only getting bigger.

Advocate Aurora, with a presence in Illinois and Wisconsin, and Atrium Health, with a presence in North Carolina, South Carolina, Georgia, and Alabama, will combine to create a $27 billion health system that will span six states and make it one of the leading healthcare delivery systems in the country. The combined organization, which will transition to a new brand, Advocate Health, will operate 67 hospitals and over 1,000 sites of care, employ nearly 150,000 teammates, and serve 5.5 million patients. Together, Advocate Health will become the 6th largest system in the country behind Kaiser Permanente, HCA Healthcare, CommonSpirit Health, Ascension, and Providence.

We have seen a number of large health systems come together recently, including Intermountain Healthcare + SCL Health to create a $15 billion revenue system, Spectrum Health + Beaumont ($14 billion), NorthShore University Health System + Edward-Elmhurst Healthcare ($5 billion), LifePoint Health + Kindred Healthcare ($14 billion), and Jefferson Health + Einstein Healthcare Network ($8 billion).

The exact reasoning for each merger differs slightly, but one of the common threads across all is scale. But not scale in the traditional M&A sense. Rather, scale in covered lives; scale in physician infrastructure and alignment; scale in clinical and operational capabilities; scale in technology, innovation, and partnerships with non-traditional players; scale for capital access; and scale for insurance risk to compete in a value-based world. It is no longer the strong acquiring the weak. Rather, strong players are coming together to gain scale to face the headwinds in a unified manner.

For Advocate Aurora and Atrium, coming together is about leveraging their combined clinical excellence, advancing data analytics capabilities and digital consumer infrastructure, improving affordability, driving health equity, creating a next-generation workforce, research, and environmental sustainability. Together, they have pledged $2 billion to disrupt the root causes of health inequities across underserved communities and create more than 20,000 new jobs.

Both Advocate Aurora and Atrium are no strangers to mergers. Advocate and Aurora came together in 2018, and prior to that Advocate was intending to merge with NorthShore before being blocked due to anti-trust. Atrium has grown over the years, merging with systems such as Navicent Health in Georgia in 2018, Wake Forest Baptist Health in North Carolina 2020, and Floyd Health System in Georgia in 2021. In the newly proposed merger, Advocate Aurora and Atrium are coming together via a joint operating arrangement where each entity will be responsible for their own liabilities and maintain ownership of their respective assets but operate together under the new parent entity and board. This may allow the combined entity more flexibility in local decision-making. The current CEOs, Jim Skogsbergh and Eugene Woods will serve as co-CEOs for the first 18 months, at which point Skogsbergh will retire, and Woods will take over as the sole CEO.

Mergers can come in various shapes and structures, but the driving forces behind consolidation are not unique. With the need to compete in value-based care, adequately manage risk, gain scale across covered lives, physicians, and points of access, successfully deliver affordable high-quality care, and the need to deal with the vertical and horizontal consolidation of the large-scale payers, the markets that health systems operate in must be large enough to be effective and relevant. We fully expect to see more of these larger scale health system mergers in the near term.

The physical delivery of healthcare is local, but, again, the business of healthcare is not; it is regional, and the regions are only getting bigger.

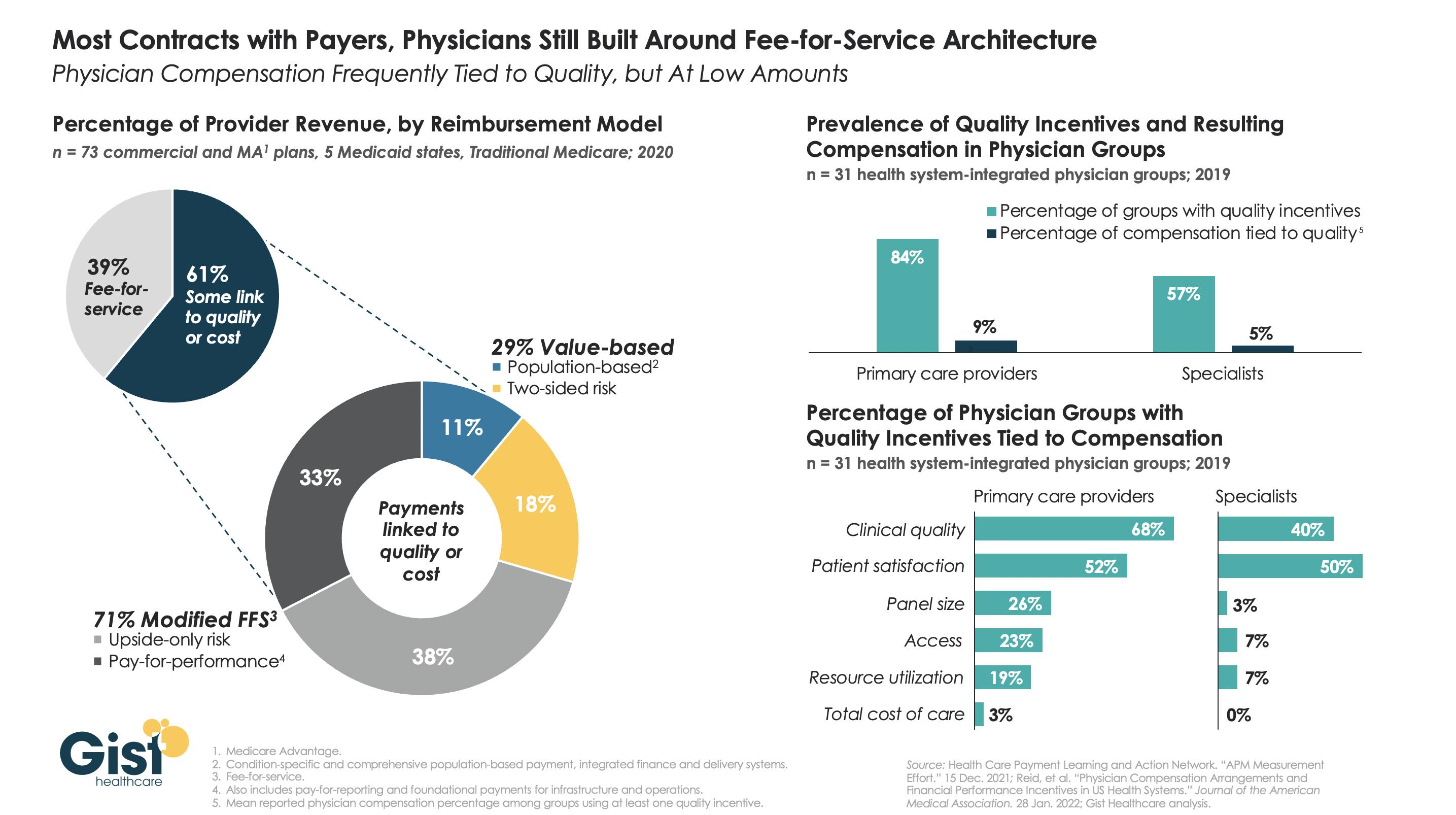

The healthcare industry has made some strides in the “journey to value” across the last decade, but in reality, most health systems and physician groups are still very much entrenched in fee-for-service incentives.

While many health plans report that significant portions of their contract dollars are tied to cost and quality performance, what plans refer to as “value” isn’t necessarily “risk-based.”

The left-hand side of the graphic below shows that, although a majority of payer contracts now include some link to quality or cost, over two-thirds of those lack any real downside risk for providers.

Data on the right show a similar parallel in physician compensation. Whilethe majority of physician groups have some quality incentives in their compensation models, less than a tenth of individual physician compensation is actually tied to quality performance.

Though myriad stakeholders, from the federal government to individual health systems and physician groups, have collectively invested billions of dollars in migrating to value-based payment over the last decade, we are still far from seeing true, performance-based incentives translate into transformation up and down the healthcare value chain.

The agency’s end goal for Medicare Advantage is to match CMS’ vision for its programs as a whole, with an emphasis on health equity.

On Wednesday, the Centers for Medicare and Medicaid Services released proposed payment policy changes for Medicare Advantage and Part D drug programs in 2023 that are meant to create more choices and provide affordable options for consumers.

The Calendar Year 2023 Advance Notice for Medicare Advantage and Part D plans is open to public comment for 30 days. This year, CMS is soliciting input through a health equity lens on the approach to some future potential changes.

The agency’s end goal for Medicare Advantage is to match CMS’ vision for its programs as a whole, which Administrator Chiquita Brooks-LaSure said is “to advance health equity; drive comprehensive, person-centered care; and promote affordability and the sustainability of the Medicare program.”

CMS is proposing an effective growth rate of 4.75% and an overall expected average change in revenue of 7.98%, following a 4.08% revenue increase planned for 2022.

WHAT’S THE IMPACT?

CMS is requesting input on a potential change to the MA and Part D Star Ratings that would take into account how well each plan advances health equity.

The agency is also requesting comment on including a quality measure in MA and Part D Star Ratings that would assess how often plans are screening for common health-related social needs, such as food insecurity, housing insecurity and transportation problems.

The Health Equity Index has been tasked with creating more transparency on how MA plans care for disadvantaged beneficiaries.

Additionally, CMS is requesting input on considerations for assessing the impact of using sub-state geographic levels of rate setting for enrollees with end-stage renal disease, particularly input regarding the impact of MA payment on care provided to rural and urban underserved populations and how such payment changes may impact health equity.

Other areas in which CMS is soliciting input include a variety of payment updates, a new measure concept to assess whether and how MA plans are transforming care by engaging in value-based models with providers’ and updates to risk-adjustment models to continue to pay appropriately for people enrolled in MA and Part D plans.

Public comments on the Advance Notice must be submitted by March 4. The Medicare Advantage and Part D payment policies for 2023 will be finalized in the 2023 Rate Announcement, which will be published no later than April 4.

REACTION

The proposed rule has already elicited reaction from various organizations, including Better Medicare Alliance.

“As we continue to review the Advance Notice in further detail, we appreciate that CMS has offered a thoughtful proposal that will help ensure stability for the millions of diverse seniors and individuals with disabilities who count on Medicare Advantage,” Mary Beth Donahue, president and CEO of the Better Medicare Alliance, said, adding that the proposal furthers the shared goal of improving health equity.

“Medicare Advantage has proven its worth for seniors and taxpayers – providing lower costs, meaningful benefits that address social determinants of health, better outcomes and greater efficiencies for the Medicare dollar,” she said. “A stable rate for 2023 ensures this work can continue. On behalf of our 170 Ally organizations and over 600,000 beneficiary advocates, we applaud CMS for putting seniors first by issuing an Advance Notice that protects coverage choices, advances health equity and preserves affordability for beneficiaries.”

AHIP also responded, with President and CEO Matt Eyles pointing out that for 2022 the average Medicare Advantage monthly premium dropped to $19, down more than 10% since 2021.

“We agree that MA plans play an essential role in improving health equity and addressing the social determinants of health that impact millions of seniors and people with disabilities,” he said. “We support CMS soliciting input on ways to advance these important goals.

“Medicare Advantage enjoys strong bipartisan support because it provides America’s seniors and people with disabilities with access to affordable, high-quality healthcare services,” said Eyles. “We will continue to review the 2023 rate notice and look forward to providing constructive feedback to CMS during the comment period.”

THE LARGER TREND

CMS’ Advance Notice follows a recent congressional letter in which 346 bipartisan members of Congress declared support for Medicare Advantage and urged the agency “to provide a stable rate and policy environment” for the program in 2023.

A December 2021 Morning Consult poll showed that 94% of Medicare Advantage beneficiaries are satisfied with their coverage, while 93% believe that protecting MA should be a priority of the Biden administration.

Google-backed One Medical is acquiring Medicare-focused primary healthcare chain Iora Health for $2.1 billion in an all-stock trade deal, the companies announced Monday.

The buy will give One Medical presence in 28 markets, covering about 40% of the U.S. population and is expected to generateannual revenue at $350 million by 2025. The deal will add about $700 billion in total addressable market, according to an investor presentation.

Under the terms of the deal, which is expected to close in the late third quarter or fourth quarter of this year, Iora stockholders will own about 27% of the combined company. One person from Iora will join One Medical’s board and Iora co-founder and CEO Rushika Fernandopulle will become One Medical’s chief innovation officer.

Dive Insight:

The acquisition aligns two key players in part of the value-based care movement that eschews traditional payer-provider arrangements in favor of a concierge membership model. Iora’s concentration in the Medicare population and related participation in CMS’ direct contracting model could be key reasons for coming under One Medical’s sights.

Jefferies analysts said they viewed the transaction as positive, particularly considering both companies’ tech and data capabilities. “Given tech orientation and emphasis on outcomes, we expect substantial derivative value from combining data and developing better treatment programs with superior outcomes across [longitudinal] care. We see this as a clear clinical and applied advantage,” they wrote.

Both companies base their business on value-based models, which some in the industry worry have suffered during the COVID-19 pandemic as cash-strapped providers avoid the risk of models not based on fee-for-service. The Biden administration’s director at the Center for Medicare and Medicaid Innovation said recently the movement is at “a critical juncture” and that more mandatory models are likely forthcoming.

One Medical has faced challenges as of late, after a first quarter that saw losses double what was expected and a controversy over COVID-19 vaccine distribution that sparked a congressional investigation. The company, however, has forged ahead in deals, including a new partnership with Baylor Scott & White.

And on the Q1 call with investors, executives highlighted a membership increase of 31% year over year.

One Medical, founded in 2007, lead the pack of recent healthcare IPOs, going public in January 2020.

The company touts its direct-to-consumer model buts also contracts directly with employers and partners with several health systems. CFO Bjorn Thaler told Healthcare Dive at the time of the IPO its pitch to investors focused on highlighting a differentiated model.

“[W]e provide the member with a very, very valuable service. They don’t have to wait 29 days to get care. They can get care oftentimes in an instant, digitally,” he said.

Boston-based Iora, which was founded in 2011, has raised nearly $350 million over seven funding rounds, according to Crunchbase. It has contracts with major payers including UnitedHealthcare, Cigna and Humana.

The deal extends One Medical into full-risk Medicare reimbursement. Iora began the direct contracting model in April across all its markets. The program ties reimbursement to spending and quality for all Medicare fee-for-service beneficiaries across a geographic region.

About 60% of Iora’s members are in the fast-growing Medicare Advantage program, which has now reached about 40% of the Medicare population.

Iora had expected revenue this year to reach nearly $300 million and as of the first quarter had 38,000 members, compared to nearly 600,000 members at One Medical, according to the investor presentation.

One Medical stock was trending slightly down in early morning trading Monday.

Many of the Center for Medicare and Medicaid Innovation’s value-based care payment models are undergoing a review, according to the Centers for Medicare & Medicaid Services (CMS).

The statement to Fierce Healthcare comes after CMS quietly updated and delayed several payment models, including pulling a controversial model that ties payments to geographic health outcomes.

“CMS remains steadfast in its commitment to transforming the healthcare system into one that rewards value and care coordination,” the agency said. “The CMS Innovation Center and its alternative payment models help execute that commitment.”

The agency added it hopes to design models that support the adoption of value-based care.

“Many of the CMS Innovation Center’s models are currently under review, and we look forward to providing updates when available,” CMS said.

CMS did not return a request for comment on how many models are under review or which ones are being scrutinized.

The statement comes after CMS has quietly updated the webpages for two payment models to note major changes. The agency made an update to the webpage for the Geographic Direct Contracting Model that said it was currently under review.

A request for applications for the model was posted Jan. 1, and the first performance period was expected to start in 2022 and run through 2024.

The model was intended to improve quality and lower costs for Medicare beneficiaries across a region, and providers in that region can enter into value-based payment arrangements.

Providers can build integrated relationships and invest in population health to better coordinate care, the agency said when the model was released last December.

But the model has gotten pushback from some provider groups. The National Association of Accountable Care Organizations has criticized the model, saying it could confuse patients who may not know whether they are participating in a direct contracting entity.

CMS also quietly pushed back the first performance period for the Kidney Care Choices model, which aims to improve the quality of dialysis care.

The model had an implementation period for 2020 that enabled participants to create the necessary infrastructure for the model, which aims to bundle care from treatment of chronic kidney disease all the way through kidney transplantation and post-transplant care.

Starting Jan. 1, 2021, providers were supposed to start taking on financial accountability including capitated payments.

But CMS posted an update on the webpage for the model, saying the start of the financial performance period will now be Jan. 1, 2022. The agency did not give a reason for the delay.

CMS’ review comes on the heels of a separate analysis conducted under the Trump administration on the value generated by the payment models. The analysis found bundled payment models that gave providers an amount of money for an entire episode of care had mixed results, while global budget models, which give providers a fixed amount for the total number of services given over a certain period of time, were given a more positive review.

It remains unclear whether that analysis is playing any role into the review undertaken by the Biden administration.