Cigna, my former employer, disclosed this morning that during the first seven months of this year, it spent $5 billion of the money it took from its health plan and pharmacy benefit customers to buy back shares of its own stock, a gimmick that rewards shareholders at the expense of those customers.

Cigna also disclosed that its revenues increased a stunning 25% – to $60.5 billion – during the second quarter of this year compared to the same period in 2023. Profits also grew, from $1.8 billion to $1.9 billion.

One of the ways Cigna made so much money was by purging health plan enrollees it decided were not profitable enough to meet Wall Street’s profit expectations.

Enrollment in its U.S. health plans fell by nearly half a million people – from 17.9 million to 17.4 million – over the past year. The company signaled to investors that it was more than OK with that decline, noting that it ran off those customers through “targeted pricing actions in certain geographies.” What that means is that Cigna increased premiums so much for those folks that they either found other insurers or joined the ranks of the uninsured.

It was an entirely different story in Cigna’s pharmacy benefit (PBM) business, which saw a 24% increase in total pharmacy customers. The vast majority of Cigna’s revenues now come from its role as one of the country’s largest middlemen in the pharmacy supply chain. Revenue from Cigna’s pharmacy operations totaled nearly $50 billion in the second quarter of this year, up from $38.2 billion last year. By contrast, revenue from its health plan business increased modestly, from $12.7 billion to $13.1 billion.

But by purging 478,000 men, women and children from its rolls, Cigna reported a profit margin of 9.2% for its health plan operations. That, folks, is exceedingly high in the health insurance business.

One way Cigna and the other industry giants can reward their shareholders so handsomely is by making their health plan and pharmacy customers pay more and more out of their own pockets before the insurers pay a dime.

The Affordable Care Act made it illegal for insurers to refuse to sell coverage to people with preexisting conditions or to set premiums based on someone’s health status.

But that law kept open a big back door that enables insurers like Cigna to make people with health problems pay huge sums of money for their care through deductibles and copayments. As a consequence, millions of Americans are walking away from the pharmacy counter without their medications, and many others who simply cannot live without their meds often wind up buried under a mountain of medical debt.

A growing number of bills have been or soon will be introduced by members of Congress to fulfill Biden’s pledge, but you can expect Cigna and other big insurers to insist that doing so will mean premiums will have to go up.

That’s bullshit.

It might mean that Cigna and the other giants might have to curtail their stock buyback programs and accept slimmer profit margins, but it does not mean premiums will have to go up.

Wall Street will howl if one of the tools insurers use to gouge their customers is taken away – just as investors are punishing Cigna today for the sin of not predicting even higher profits for the rest of the year –

but reducing out-of-pocket requirements would put a significant dent in the enormous and ongoing transfer of wealth by middlemen like Cigna from middle-class Americans, especially those struggling with health issues, to fat cat investors and corporate executives.

Today, we celebrate the 59th birthday of Medicare, a cornerstone of American health care that has provided critical services to millions of seniors since its inception in 1965.

This historic program was a watershed moment in our nation’s history, transforming the landscape of health care and ensuring that older Americans and the disabled could access necessary medical services without facing financial ruin. Medicare’s legacy is one of promise and protection, grounded in the belief that no American should go without the health care they need.

However, as we celebrate this milestone, it is crucial to reflect on the current state of Medicare and the growing threat posed by big health insurers’ Medicare Advantage plans. These plans, most of which are operated by private, for-profit insurance companies, have been aggressively marketed as a superior alternative to traditional Medicare.

But the reality is starkly different. Medicare Advantage plans are siphoning off vital resources, wasting taxpayer dollars and ultimately leading to poorer health outcomes and often untimely death of many senior enrollees.

The original intent of Medicare was to provide a straightforward, government-managed health care solution for seniors, but over the years Medicare Advantage plans have deviated from this mission.

These plans often prioritize profit over patient care, leading to higher costs and more restrictive networks. In many cases, seniors enrolled in Medicare Advantage plans face significant hurdles in accessing the care they need, such as dwindling provider choices and burdensome prior authorization requirements.

These overpayments, often justified by health insurers through dubious risk adjustment practices, divert funds away from traditional Medicare. This not only threatens the sustainability of Medicare but also undermines the quality and availability of care for all beneficiaries.

As a former insurance executive, I have seen firsthand how corporate interests can aggressively game public programs. And they’ve gotten really good at the Medicare game.

The good news: A growing number of regulators are focused on the encroaching influence of Medicare Advantage plans and health insurers’ business practices. Which is great, because reducing overpayments to private insurers and ensuring that Medicare dollars are used efficiently is the only way lawmakers and regulators can protect this vital program for future generations.

As state hospital association leaders assemble in Big Sky, Montana this week, the environment for hospital-friendly legislation is threatening at best:

The public’s trust in hospitals has eroded. Hospital financial performance is a mixed bag: some are profitable and many aren’t. Congress thinks hospitals need more regulation to increase price transparency, require ownership disclosure, verify community benefits that justify tax exemptions and impose restrictions on hospital private equity investments. And programs through which state and federal health policies are authorized—HHS, CMS, FTC, FDA, CMMI et al—are in limbo as a result of the June 28, 2024 Chevron ruling by the Supreme Court.

At a federal level, the American Hospital Association has successfully fended-off a significant portion of proposed cuts to key programs (DSH, rural), delayed Congressional action against facility fees and site neutral payments, influenced improvement from April’s proposed 2025 Medicare rate from 2.6% to 2.9%, advanced legislation to protect healthcare workers and streamline prior authorization business practices by insurers. In most cases, it has pursued a unified agenda alongside its Coalition (America’s Essential Hospitals, the Federation of American Hospitals, the Catholic Health Association and the Association of American Medical Colleges , Children’s Hospital Association et al) and it has invested heavily in its lobbying: $6.46 million in the second quarter 2024 (plus $4.1 million by HCA, AAMC, Tenet and others).

At the state level, the attention hospitals get is equally intense but more complicated: It starts with money and demand: Examples:

State resources: 9 states don’t tax any income, regardless of the source (AL, FL, NV, NH, TN, SD, TX, WA, WY); 4 states don’t tax any retirement income: (IL, IA, MS, PA); 8 states tax social security benefits (CO, MN, MT, NM, RI, UT, VT, WV)

Population health status: WalletHub used 44 measures to assess each state and the District of Columbia on healthcare cost, access, and outcomes. WalletHub weighted the three categories equally. The Top 5: MN, RI, SD, IA, NH; the bottom 5: MS, AL, WV, GA, OK

There are Blue and Red states. Some are growing and some declining. All are integrating more diverse populations and divergence between low- and high-income household financial security and spending. The health system, and its hospitals, impact all.

Healthcare spending for state employees, Medicaid and dual eligible enrollees and public health programs consume a third or more of total state spending. And actions taken in states vis a vis ballot referenda, executive orders, administrative agency rulings and legislative actions result in wide variance in the regulatory environments for hospitals. Consider:

32 states have passed legislation to lower health system costs

31 states have CON requirements (24 of these have been revised since 2021).

15 states have passed laws to reduce or eliminate facility fees including hospitals

17 have passed legislative to increase competition in healthcare

23 passed legislation to reduce surprise medical bills

9 have passed legislation to address community benefit declarations by NFP hospital and health systems.

9 have passed legislation to reduce insurer prior authorization obstacles.

13 passed legislation involving reference pricing requirements for hospitals

8 states passed legislation requiring minimal levels of primary care services

24 modified their Certificate of Need programs

3 states have all-payer payment policies.

8 states have drug price control commissions/mechanisms to limit price increases.

And all are grappling with determinations about abortion services, drug formulary design for Medicaid, state health employee health costs, Medicaid eligibility and funding, staffing requirements in hospitals and nursing homes, rural health solvency, telehealth efficacy, insurer plan design restrictions, and scope of practice expansion for nurse practitioners, pharmacists and much more.

The advocacy environment for hospitals at the state and federal levels will be dicier going forward: the near-term macro-environment is unwelcoming for hospitals presumed to have returned to profitability after the pandemic.

It’s root in four convergent issues:

Economic Uncertainty: Last week’s BLS jobs report signaled softening of the economy and alarmed some thinking it a harbinger of a possible recession.

Middle East Tension: the Israeli-Palestinian conflict appears headed toward a broader regional conflict involving Lebanon, Iran and others.

Campaign 2024: hyper-partisanship coupled with disinformation on both sides lends to voter unrest: healthcare affordability, price transparency, consolidation, executive compensation and inequity are ripe targets.

Healthcare Workforce Disenchantment (including Physicians): Hospitals directly employ half of the physician workforce and 30% of total health industry employment. Labor-management tension in hospitals is mounting.

For hospitals, effective advocacy is imperative: the reservoir of good will enjoyed for decades is evaporating. Advertising “we’re there for you” is timely as rural providers need a lifeline, and public castigation of “corporate insurers and billionaire critics” necessary to rally supporters.

But beyond these, two things are clear:

The marketplace for “hospitals” is fundamentally different than the past requiring a clearer value proposition and fresh messaging.

And in states, hospitals will encounter unique opportunities and challenges in plotting strategies for their future. No two are alike.

Big Sky is a symbolic locale for this week’s meeting of state health executives: the Big Sky over hospitals is cloudy.

Growing demand for GLP-1 drugs like Ozempic and Wegovy and hospital consolidation could help drive up the cost of Affordable Care Act coverage next year by 9% or more, according to a preliminary review by the Peterson Center on Healthcare and KFF.

Why it matters:

While most enrollees in the market get subsidies and won’t have to foot the added bill, premium increases generally result in higher federal spending on subsidies, the analysis notes.

So, too, is the explosion in demand for drugsused for diabetes treatment and weight loss.

Though few ACA plans cover drugs that are approved only for weight loss, several insurers singled out GLP-1s as a driving force behind premium increases for 2025.

The analysis notes insurers are using strategies like prior authorization, step therapy and limiting quantities to control demand of Ozempic and other GLP-1s that are approved for diabetes but have potential for off-label use to lose weight.

Specialty drugs and biologics, including pricey gene therapies, are also becoming more prevalent and driving premiums upward.

Most insurers say ongoing state Medicaid redeterminations, COVID-19 treatment and tests and the federal surprise billing ban are not having a major effect on 2025 premiums.

Context:

Last year, insurers proposed rate increases for 2024 coverage that were between 2% and 10%, with a median increase of 6%, Peterson-KFF notes.

This year’s detailed review of factors driving premium changes for 2025 found insurers have somewhat higher proposed rate increases, with a median of 9%.

The basis for the federal subsidies is the percent change in the benchmark ACA silver plan.

The bottom line:

Medical inflation has picked up and now exceeds the growth of non-medical prices — a big change from 2021 to 2023. ACA plans are adjusting to keep pace and reflect their higher costs and overhead.

Some of America’s largest hospital systems saw their financials soar in the first half of 2024. And yet, more than 700 facilities across the country still are at risk of closing.

Why it matters:

It’s a familiar tale of the rich getting richer, as big, mostly for-profit health systems see improved margins while smaller facilities in outlying areas are barely hanging on.

That could worsen access for some of the most vulnerable Americans — and hasten consolidation in an industry that’s been a magnet for M&A.

The big picture:

Health systems with big footprints, including large academic medical centers, have weathered the pandemic and economic headwinds and are seeing margins as good or better than before COVID-19.

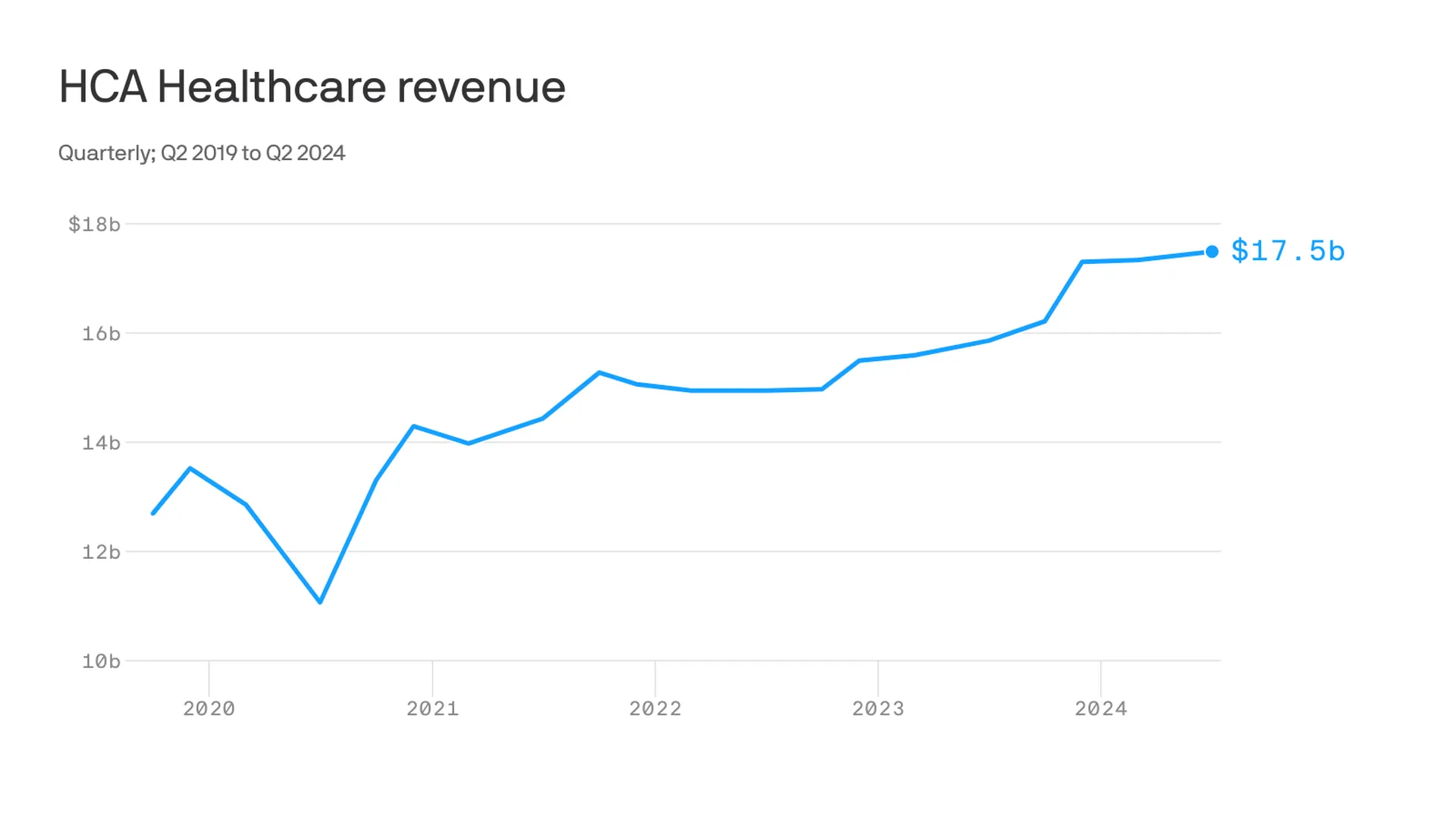

Nashville-based industry behemoth HCA Healthcare posted 23% year-over-year profit growth for the quarter, revising its forecast for the rest of the year, projecting it’ll reach as much as $6 billion. It posted a 10% year-over-year increase in revenue.

King of Prussia, Pennsylvania-based Universal Health Services similarly reported a strong quarter, posting nearly 69% growth on its bottom line over the same period last year while Dallas-based Tenet Healthcare reported a 111% jump in its net income over the same quarter last year.

Yes, but:

Smaller nonprofit hospitals, especially in rural areas, that made it through the crisis with the help of government aid are paring services like maternity wards and struggling to stay open.

“There are a lot of hospitals that survived, but their balance sheets are so weakened, their margin for error is basically zero at this point,” said Mike Eaton, senior vice president of strategy at population health company Navvis.

Hospitals that once could manage their expenses and the needs of communities are “going to really struggle to invest in what comes next,” he said.

Between the lines:

The biggest health systems have benefited from less volatility, seeing stabilizing drug prices and more predictable supply chains and labor costs, per a new report from Strata Decision Technology.

“It’s at least something you can manage to,” Steve Wasson, Strata’s chief data and intelligence officer, told Axios.

Revenues already were up thanks to renegotiated contracts health systems struck with payers last year, Wasson said.

There also have been changes on the federal side that boosted Medicare admissions and put some hospitals in line to be reimbursed for billions in underpayments from the 340B drug discount program.

Zoom in:

It’s all translated to operating margins that are up 17% year-to-date compared with the same time period in 2023, according to the latest Kaufman Hall National Hospital Flash Report.

Volumes as measured by hospital discharges per day are up 4% year-to-date.

Expenses per day are also up 6% year to date, including labor (4%), supplies (8%) and drugs (8%), but are far less volatile and thus easier to plan for, said Erik Swanson, senior vice president at Kaufman Hall.

But there’s a growing gulf between the top third of U.S. hospitals, which are seeing outsize growth, and the rest, Swanson said.

Threat level: A new report from the Center for Healthcare Quality and Payment Reform estimated 703 hospitals — or more than one-third of rural hospitals — are at risk of closure, based on Centers for Medicare and Medicaid Services financial information from July. Losses on privately insured patients are the biggest culprit.

“We’re looking at 50% of rural operating in the red. The situation is very challenging,” Michael Topchik, partner at Chartis Center for Rural Health, told Axios.

These smaller hospitals may still be there, but there will continue to be a steady erosion of the kinds of services they offer, such as obstetrics, cancer care and general surgery, he said.

What’s next:

Private equity investment in rural health care is already booming and with it, prospects for service and staffing cuts.

The South generally has the highest concentration of private equity-owned rural hospitals, often with lower patient satisfaction and fewer full-time staff compared with non-acquired hospitals, according to the Private Equity Stakeholder Project.

Congress is ramping up oversight of private equity investments in the sector, though most lawmakers are loath to take steps to actually halt deals.

Walmart’s announcement on April 30 that it was pulling the plug on Walmart Health stunned the healthcare ecosystem. [1] Few saw it coming.

Launched amid much fanfare in 2019, Walmart Health has operated 51 health centers in five states, with a robust virtual care platform. Walmart’s news release noted that “the challenging reimbursement environment and escalating operating costs create a lack of profitability that make the care business unsustainable for us at this time.” Despite its legendary supply-chain capabilities, expansive market presence and sizable consumer demand for affordable primary care services, Walmart couldn’t make its business model work in healthcare.

Just two weeks earlier with much less fanfare, and in stark contrast to Walmart, the big health insurer Elevance announced it was doubling-down on primary care. On April 15, Elevance issued a news release detailing a new strategic partnership with the private-equity firm Clayton, Dubilier & Rice (CD&R) to “accelerate innovation in primary care delivery, enhance the healthcare experience and improve health outcomes.” [2]

What gives? Why is Elevance expanding its primary care footprint when the retail behemoth Walmart believes investing in primary care is unprofitable? The answer lies at the heart of the debate over the future of U.S. healthcare. As a nation, the United States overinvests in healthcare delivery while underinvesting in preventive care and health promotion.

Enlightened healthcare companies, like Elevance, are attacking this imbalance aggressively.

Elevance isn’t alone. Other large health insurers — including UnitedHealthcare, CVS/Aetna and Humana — and some large health systems (e.g., AdventHealth, Corewell Health and Intermountain Healthcare) are investing in primary care services to support what I refer to as 3D-WPH, shorthand for “democratized and decentralized distribution of whole-person health.”

3D-WPH is the disruptive innovation that is rewiring U.S. healthcare to improve outcomes, lower costs, personalize care delivery and promote community wellbeing. It is an unstoppable force.

Transactional Versus Integrated Primary Care

Across multiple retail product and service categories — including groceries, clothing, electronics, financial services, generic drugs and vision care — Walmart applies ruthless efficiency management to increase consumer selection and lower prices. Consistent with the company’s mission of helping its customers to “save money and live better,”

Walmart Health provided routine, standalone primary care services at low, transparent prices. Despite scale and superior logistics, Walmart could not deliver these routine care services profitably.

Here’s the problem with applying Walmart’s retailing expertise to healthcare:

While exceptional primary care services are rarely profitable in their own right, they can reduce total care costs by limiting the need for subsequent acute care services. Preventive care works. Companies that invest in primary care can benefit by reducing total cost of care.

Unfortunately, few providers and payers practice this integrated approach to care delivery. Most providers rely on their primary care networks to refer patients for profitable specialty care services. Most payers use their primary care networks to deny access to these same specialty care services.

This competition between using primary care networks as referral and denial machines dramatically increases the intermediary costs of U.S. healthcare delivery. Patients get lost as these titanic payer-provider battles unfold, even as costs continue to rise, and health status continues to decline.

Whole-Person Health Works

A growing number of payers and providers, however, are recalibrating their business models to lower total care costs by integrating primary care services into a whole-person health delivery model.

In its news release, Elevance described its strategic partnership with CD&R as follows:

The strategic partnership’s advanced primary care models take a whole-health approach to address the physical, social and behavioral health of every person. The foundation of the new advanced primary care offering will be stronger patient-provider relationships supported by data-driven insights, care coordination and referral management, and integrated health coaching. It will also leverage realigned incentives through value-based care agreements that enable care providers, assist individuals in leading healthier lives, and make care more affordable.

“We know that when primary care providers are resourced and empowered, they guide consumers through some of life’s most vulnerable moments, while helping people to take control of their own health,” said Bryony Winn, president of health solutions at Elevance Health, in the news release. “By bringing a new model of advanced primary care to markets across the country, our partnership with CD&R will create a win-win for consumers and care providers alike.”

Whole health personalizes and integrates care delivery. I would suggest that transactional and fragmented primary care service provision cannot compete with 3D-WPH.

For all its strengths, Walmart Health is not positioned to advance whole-person health. Primary care service provision without connection to whole-person health is a recipe for financial disaster. Walmart Health’s demise confirms this market reality.

Countries with nationalized health systems practice whole-person health expansively. With one-third the per capita income and one-fifth the per capita healthcare expenditure, Portugal has a life expectancy that is more than five years longer than it is in the United States. [5] Portugal achieves better population health metrics than the United States by operating community health networks throughout the country that combine primary care and public health services.

The VA, Portugal and numerous other organizations and countries prove the thesis that investing in primary care lowers total care costs and improves health outcomes. The evidence supporting this thesis is both compelling and incontrovertible.

Solving Healthcare’s Primary Care Conundrum

Economists refer to a circumstance when individuals overuse scarce public goods as a tragedy of the commons.

Public grazing fields highlight the challenge posed by such a circumstance. [6] It is in the financial interest of individual ranchers to overgraze their herd on a public grazing field. Overgrazing by all, however, would obliterate the grazing field, which is against the public’s interest.

Societies address these “tragedies” by establishing and enforcing rules to govern public goods.

U.S. healthcare, however, reverses this type of economic tragedy. Advanced primary care services represent a public good. All acknowledge the benefits and societal returns, yet few providers and payers invest in advanced primary care services. Providers don’t invest because it leads to lower treatment volumes. Payers don’t invest because primary care’s higher costs trigger higher premiums, prompting their members to switch plans.

We can’t solve the primary care conundrum until we enable both providers and payers to benefit from investments in advanced primary care services. Fragmented, transactional medicine, even when delivered efficiently, is not cost-effective. Walmart Health discovered this economic reality the hard way and exited the business.

By contrast, Elevance is reorganizing itself to overcome healthcare’s reverse tragedy of the commons. They are betting that offering advanced primary care services within integrated delivery networks will both lower costs and improve health outcomes. Healthcare’s future belongs to the companies, like Elevance, that are striving to solve the industry’s primary care conundrum.