There is a local urgent care chain that we frequented regularly when my kids were young and cycling through rounds of ear infections and strep throat. The experience was always solid, driven by online scheduling, efficient operations, and good customer service.

A few years ago, the clinics were bought by a local health system. We recently visited one for the first time post-acquisition, when my now teenage son needed to rule out a broken bone from a sports injury. This experience at the same urgent care left a very different impression.

In contrast to the “easy in, easy out” experience I expected, we sat in an exam room for hours, even though the place was not crowded. While this could be due to the staffing challenges pervasive across the industry, other elements of the acquisition left a different impression.

Gone was the advertised cash pricing (and I’m anticipating a higher bill once we get one). The new patient self-registration system was overly complex, built for a hospital, not an immediate care setting.

The only signs of “systemness”? Multiple prompts to sign up for the health system’s MyChart patient portal (not interested, they have few facilities close by), and a printed referral to an employed orthopedic surgeon a forty-minute drive from home (with no guidance as to whether or when we should seek it, given that no bones were broken).

A few days ago, a scheduler from the system called to book the appointment. With no inquiry as to whether my son’s pain had improved, the interaction felt like a business transaction, not clinical follow-up. I declined.

Just because a care site is acquired by a health system, that doesn’t mean that patients will feel any value from its being part of a system.

Right or wrong, my impression was that health system ownership has made for a worse experience: inefficient, more complicated, and possibly more expensive.

Nothing about the visit gave me confidence that there was a benefit to following up with an affiliated provider. The health system had failed to earn our referral.

Systems buy assets like urgent care to create entry points that will generate downstream demand and hopefully build loyalty to the brand. But capturing that must start with delivering an excellent experience in every encounter, not merely changing the name on the building.

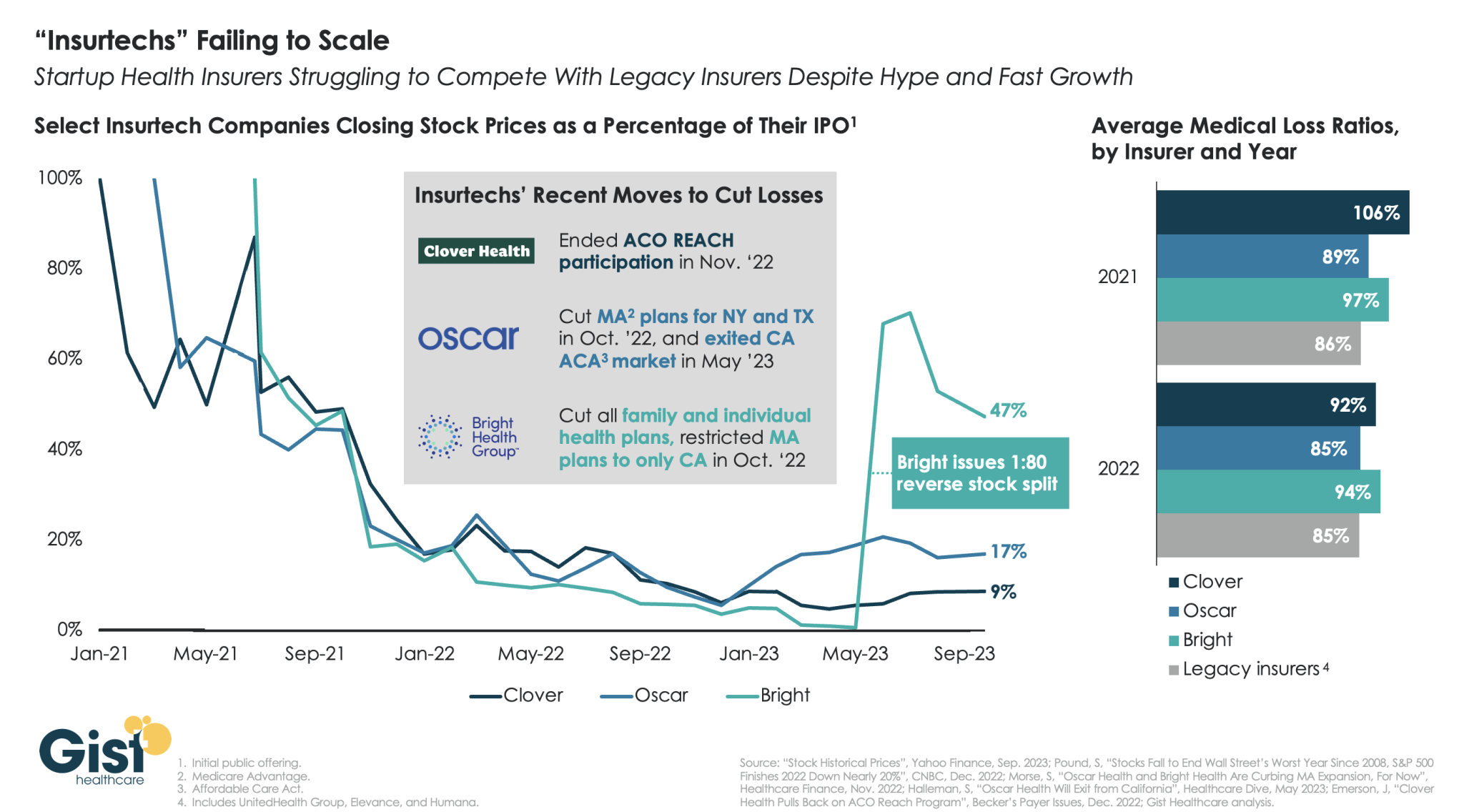

“Insurtechs” Clover Health, Oscar Health, and Bright Health all went public in the midst of the hot equity market of 2021. Investors were excited by the fast growth of these health insurer startups, and their potential to revolutionize an industry dominated by a few large players.

However, the hype has dissipated as financial performance has deteriorated. After growing at all costs during a period of low interest rates, changing market conditions directed investors to demand a pivot to profitability,which the companies have struggled to deliver—twoyears later,none of the three has turned a profit.

Oscar and Bright have cut back their market presence significantly, while Clover has mostly carried on while sustaining high losses. In the last two years, only Oscar has posted a medical loss ratio in line with other major payers, who meanwhile are reporting expectation-beating profits. While Oscar has shown signs of righting the ship since the appointment of former Aetna CEO Mark Bertolini,

the future of these small insurers remains uncertain. As their losses mount and they exit markets, they may become less desirable as acquisition targets for large payers.

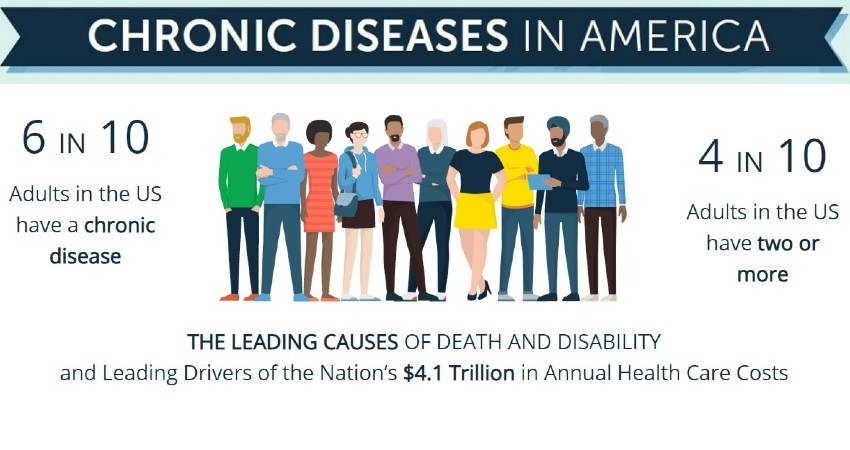

Published this week in the Washington Post, this unsparing article packages a year of investigative reporting into a thorough accounting of why US life expectancy is undergoing a rapid decline.

After peaking in 2014, US life expectancy has declined each subsequent year, trending far worse than peer countries. In a quarter of US counties, working-age Americans are dying at the highest rates in 40 years, reversing decades of progress. While deaths from firearms and opioids play a role, chronic diseases remain our nation’s greatest killer, erasing more than double the years of life as all overdoses, homicides, suicides, and car accidents combined.

The drivers of this trend are too numerous to list, but experts suggest targeting “the causes of the causes”, namely social factors, as the death rate gap between the rich and poor has grown almost 15x faster than the income gap since 1980.

The Gist: This reporting is a sobering reminder of the responsibilities—and failures—borne by our nation’s healthcare system.

The massive death toll of chronic disease in this country is not an indictment of the care Americans receive, but of the care and other resources they cannot access or afford.

While it’s not the mandate of health systems to reduce systemic issues like poverty, there is no solution to the problem without health systems playing a key role in increasing access to care, while convening community resources in service of these larger goals.

Late last week, the Congressional Budget Office (CBO) released its analysis of the Center for Medicare and Medicaid Innovation (CMMI)’s spending outlays, revealing that in its first decade of operations it produced a $5.4B net increase in federal spending instead of a projected $2.8B reduction.

Moreover, CBO revised its CMMI projection for 2021-2030 from a $77.5B net spending reduction to a $1.3B increase, predicting CMMI may only begin to generate annual savings in 2031. CBO says its updated projections largely reflect revised expectations on CMMI’s ability to identify and scale models that actually reduce Medicare spending.

CMMI was created by the Affordable Care Act (ACA) in 2010 to test new payment models and other initiatives for reducing the federal government’s healthcare costs, but of the nearly 50 models it has run, only four have become permanent programs.

The Gist: This critical report confirms what many in the healthcare world already believed: the ACA’s value-based care initiatives have largely struggled to reduce Medicare spending.

There are plenty of policy factors to blame, including the lack of mandatory participation for providers and conflicting incentives across care models, but one factor left out of the CBO report is CMMI’s disproportionate emphasis on accountable care organizations (ACOs) to produce meaningful cost savings, even as years of data proved otherwise.

ACOs are designed to reduce spending primarily through utilization management, but research has shown that prices, not utilization, are responsible for the US’s high medical spend relative to other countries.

While CMMI’s mission is still laudable and important, the center must make good on its 2021 “strategic refresh” if it hopes to continue receiving Congressional support.

On Wednesday, 75K Kaiser Permanente (KP) healthcare workers in five states and Washington, DC walked off the job as part of the largest healthcare strike in US history.

The striking workers are a diverse group, based mostly in California, that includes support staff, X-ray technicians, medical assistants, and pharmacy workers. They will continue their work stoppage until Saturday morning, though union leadership is threatening an even larger strike in November if a new contract agreement is not reached by then.

Their employment contract expired on September 30th, and while negotiations have progressed on issues like shift-payment differentials and employee training investments, union leaders and KP executives remain at odds over key wage increase demands, with the unions asking for a $25 national minimum wage, and KP proposing $21.

The company has sought to minimize disruptions to patient care during the strike, bringing in temporary labor to keep critical infrastructure open, but has told its members to expect some non-urgent procedures to be rescheduled, some clinic and pharmacy operating hours to be reduced, and call center wait times to be lengthy.

The Gist: Kaiser Permanente has enjoyed solid relations with its unions for decades, making this strike a significant break from precedent,fueled by post-pandemic burnout and staffing shortages.

While KP is keeping all essential services open, care disruptions are inevitable with around one third of its total workforce on strike.

The stakes of these labor negotiations extend far beyond just KP and its employees, as union success could inspire other unionized healthcare workers to adopt similar tactics and demands. (Case in point: Employees at eleven Tenet Healthcare facilities in California represented by SEIU-UHW, one of the unions representing striking KP workers, just voted to authorize their own strike.)

While happening alongside high-profile strikes in other industries, labor unrest is a troubling trend for health systems, whose margins remain well below historical levels amid persistently high labor and supply expenses.

Short-term, limited-duration insurance (STLDI) plans are exempt from the Affordable Care Act’s (ACA) essential benefit coverage requirements and from prohibitions on medical underwriting.

This means that consumers with preexisting conditions can be denied coverage and anyone who purchases such a plan may lack coverage for key services.

In August 2018, under the Trump administration, the U.S. Department of Health and Human Services revised the definition of short-term plans to include coverage with an initial term of less than 12 months that could be renewed for up to 36 months. While the purported goal of this change was to increase coverage and reduce uninsured rates, our analysis indicates that it did not accomplish this: coverage did not increase and the uninsured rate did not drop.

In July 2023, the Biden administration issued a notice to limit the initial duration of short-term plans to three months, with an option to renew for one additional month. This change was intended to ensure that people purchasing insurance coverage have meaningful protection and to preserve the preexisting condition protections in the ACA.

In 2019, the Congressional Budget Office (CBO), using its forecast model (data were not yet available), estimated that 1.5 million people would purchase short-term plans and that 500,000 would gain coverage (relative to being uninsured). Our analysis suggests that these forecasts substantially overstated the effects of the rule change; far fewer people enrolled in STLDI plans and the enrollment that did occur was from people moving off marketplace coverage.

There is no evidence that the number of uninsured people declined because these plans became available.

Using data from the American Community Survey and marketplace enrollment from the Centers for Medicare and Medicaid Services (CMS), we assessed whether the loosening of STLDI regulations (under the Trump administration) led to increased enrollment in off-marketplace nongroup coverage in states that permitted sales compared to those that did not. Plans sold off the marketplace include STLDI as well as ACA-compliant plans, grandfathered coverage, health care sharing ministries, and fixed indemnity plans. Next, we looked to see whether the Trump-era regulations increased nongroup insurance coverage altogether (including marketplace coverage) in these states. Finally, we looked to see whether the broader availability of STLDI was associated with lower uninsured rates. We examined coverage patterns for adults ages 26 to 64 and then focused on young men ages 26 to 35, who may be most sensitive to the presence of regulations similar to those in the ACA because they are less likely to have preexisting conditions or to seek comprehensive coverage.

In 2017, 2.6 million adults ages 26 to 64, about 1.6 percent of that population, purchased private nongroup insurance outside the marketplace. By 2020, about 270,000 more people were enrolled in off-marketplace nongroup plans, across all states, than had been in 2017. There was a larger increase in off-marketplace nongroup enrollment among all adults and among young adults (we cannot separate young men in the CMS data) in states that permitted the sale of STLDI coverage, compared to those that prohibited it. This is consistent with the evidence of growth in sales of these plans. Across all states, about 160,000 more young adults, ages 26 to 34, held off-marketplace nongroup coverage in 2020 than in 2017.

The ACS data show that off-marketplace plans largely substituted for marketplace plans in states that permitted the sale of STLDI. Patterns of enrollment in nongroup plans overall were very similar in states with and without STLDI plans available for purchase over this period. While nongroup coverage was consistently more popular in states with no restrictions, between 2017 and 2020 enrollment in nongroup plans declined slightly more in states where STLDI plans were available for purchase than in those where they were not. The same pattern of marginally greater declines held for young men (and young adults) in states where STLDI plans were available.

Nongroup coverage was slightly higher in states where STLDI plans were available for sale, but the overall uninsured rate is much higher in these states, primarily because many did not expand Medicaid eligibility.

The gap in uninsured rates between states with STLDI plans available and those in which they were not available widened through 2018, narrowed slightly in 2019, and rose again in 2020. Patterns among young men were similar.

The lack of reliable information on STLDI plans and the small size of the market make it difficult to draw strong inferences about how changes in regulations affected participation. Nonetheless, by comparing states where the 2018 regulatory changes took effect and those where they did not, we are able to rule out any notable effects. A modest number of people — no more than one-fifth of the 1.5 million the CBO projected — are likely to have enrolled in STLDI plans that became available after the Trump administration’s regulatory change. This enrollment mainly appears to have displaced marketplace coverage.

There is no evidence that the broader availability of STLDI plans had any meaningful effect on nongroup coverage in general or on uninsurance, either in the full population or among young men.

This suggests that the Biden administration’s proposed tightening of STLDI is unlikely to have substantial negative effects on nongroup coverage or uninsurance. Instead, limiting STLDI will likely strengthen the health insurance marketplaces that offer reliable, comprehensive nongroup coverage.

Misinformation. A recent and major problem facing us all, and one that is pervasive in many realms including medicine and healthcare, which are, of course, favorite realms around here. But is all this stuff recent? Is misinformation a new phenomenon in the world of medicine and health, or does it have a history?

The answer to that, thanks in part to funding from the National Institute for Healthcare Management, is the topic of this week’s Healthcare Triage.