Thanks to TV shows and movies, we tend to think of

private equity bidding wars as involving fast-growing

Silicon Valley companies. But when Oak Street Health,

a Chicago-based network of seven primary care clinics,

began looking for investors last year, more than a dozen

firms flew to Chicago to court the physicians and most of

them ended up bidding for the group of seven primary care clinics, according to a report in Modern Healthcare.

Oak Street is not alone — almost any independent

physician group of scale these days is likely to be an

attractive target for so-called “smart money,” investors

and their advisers.

Increased regulatory requirements and complexity has led

many independent small groups to “throw up their hands

and decide to sell to or join larger entities,” says Andrew

Kadar, a managing director in L.E.K. Consulting’s healthcare

services practice, which advises private equity groups.

While many such physicians sell to a health system and

become salaried employees, investor-backed practice management groups may have certain advantages, Kadar says. “Each private equity firm has its own approach, but in general they tend to give physicians a continued degree of independence and are willing to invest in new tools and technology.”

What is private equity up to? What attracts these

titans of capitalism to one of the most bureaucratic,

heavily regulated industries in the United States? And

what does the acquisition spree mean for physicians?

Here are five things to know about private equity and

healthcare in 2019.

1. The feeding frenzy is just ramping up

The driving force behind investors’ interest in healthcare

is the amount of “dry powder” in the industry — the term

market watchers use for funds sitting idle and ready to

invest, which McKinsey estimates at around $1.8 trillion

Investors are hungry for deals, and healthcare providers

are an attractive target for multiple reasons:

• The healthcare industry is growing faster than the

GDP. Healthcare is a relatively recession-proof industry

(demand remains constant even during downturns).

• Many providers are currently not professionally

managed, and many specialties remain fragmented.

• Investors see an opportunity to create value by

increasing efficiencies and consolidating market power.

Thus, with many independent providers still competing

on their own, there remains ample opportunity to

roll up practices into a single practice-management

organization owned by investors. “A lot of deals are

making the headlines, but when you look closely you’ll

see that most specialties aren’t highly penetrated yet by

investors,” says Bill Frack, a former managing director at

L.E.K. Consulting who is now leading a new healthcare

delivery venture. “We are still at the beginning.”

2. Investors have various strategies for creating value

Far from the leveraged-buyout days of the 1980s, which

relied primarily on financial engineering to generate

returns, almost all private equity deals today require

investors to find ways to add value to organizations over

the course of their holding period (typically around five

to seven years). By and large, in healthcare they follow

two strategies for doing so.

The most prevalent play is to buy high-volume, high margin specialist groups such as anesthesiologists,

dermatologists, and orthopedic surgeons. The PE

group then looks to maximize fee-for-service revenue

in the group by ensuring that the team is correctly

and exhaustively coding patient encounters (via ICD10) and encouraging physicians to see more patients.

Simultaneously, they work to improve revenue-cycle

management and drive efficiencies of scale into sales

and back-office administration.

Private equity firms may also look to vertically integrate

by acquiring providers of services for which their

specialists were previously referring out. For instance, oncologist groups might buy radiation treatment centers;

orthopedic surgeons might acquire rehab centers;

dermatologists might acquire pathology labs to process

biopsies, and so on.

Investors exit either through a sale to a larger PE group or,

for the largest groups, through an initial public offering.

Consolidating fee-for-service providers “is a very mature

strategy, and there’s not a single specialty you could

name where an investor wouldn’t have an incentive to

[form a roll-up],” says Brandon Hull, who serves on the

advisory council of New Mountain Capital, a private

equity firm that is investing in healthcare, and is a longtime board member at athenahealth.

Hull says investors are starting to take another approach

to creating value — which he argues “is more virtuous

and aligned with social goals.” In this strategy, investors buy up general medicine specialists — such as internal

medicine, pediatrics, or ob-gyns — and then negotiate

value-based contracts from payers.

To succeed under these contracts, investor-backed medical

groups identify the most cost-effective proceduralists

and diagnosticians in their network and instruct general

practitioners to refer only to them; and they work hard

to play a larger role in patients’ health and thus keep

healthcare utilization down. Groups that employ this

approach include Privia and Iora Health. In this strategy,

investors typically exit by selling the organization to a

larger PE group, a payer, or a health system.

Interestingly, groups that pursue the first strategy often

transition to the second – for instance, an efficiently run

orthopedic group might start with a focus on growing

revenue by maximizing fee-for-service opportunities,

but then consider pursuing bundled payments for hip

replacements. Or an investor-backed oncology group

confident in its treatment protocols and ability to keep

operational costs down might accept capitated payments

for treating patients recently diagnosed with cancer.

3. Private equity can be a great deal for physicians

How these deals are structured depends on whether a

specialty group is the first group acquired by investors —

what is known in private-equity lingo as “the platform”—

or whether it’s being added to an existing group, what is

known as a “tuck-in.”

Physicians in the platform practice are often offered

substantial equity and can benefit from the group’s

appreciation — while, of course, being exposed to the risk that

their share-value may decrease if the group fails to deliver on

its intended value proposition. Physicians in subsequent tuckin groups tend to have simpler contracts with a salary base

and added incentives tied to productivity and other measures.

L.E.K.’s Frack says both models can be attractive, but

that a more simple employment model is probably best

suited to most physicians. “I would tell docs that if they

have a strong group of doctors, they don’t have much to

lose. Even if the deal falls flat for investors, the doctors

will likely just be acquired by another investor, and they

won’t be left holding the bag.”

4. Technology underpins it all

A similar private-equity healthcare frenzy in the 1990s failed

spectacularly. One reason for the collapse was that the

technology did not exist for investors to realize back-office

efficiencies and handle the complexity of value-based contracts.

Today, cloud-based EHR and revenue-cycle management

systems harness the power of network effects to help

provider organizations handle complex and unique

payer contracts, improve back-office efficiency through

automation and machine-learning, implement best practices

for care, and quickly onboard the new practices they acquire.

Technology is particularly important for the general

medicine specialist groups looking to win under fee-for-value contracts. “The moment you start to care about

a patient’s entire episode of care, you need a massive

upgrade of your back-end systems, including full

visibility into what’s happening to your patient outside

your office. Now the technology exists to truly achieve

care coordination,” New Mountain Capital’s Hull says.

5. Public perception can be a problem

Even if physicians believe a private equity deal is their

best option, there’s a public relations risk in tying a medical practice to capitalists whose ultimate goal is to earn a return. Most coverage of private equity in mainstream media outlets questions whether investors’ profit motive is bad for patients. Physician associations and medical journals have also raised concerns in a very public way.

Such public skepticism should worry anyone who

remembers the crash of the first private-equity wave in

the 1990s, says New Mountain Capital’s Hull, who ties

that crash to the failure of managed care. “The American

consumer perceived that doctors were getting bonuses

for denying them care; this became the grim punchline

of late-night talk shows, and the whole thing fell apart.”

Frack advises investors and physicians to “monitor

quality data like a hawk, so that the group can counter

anecdotal accounts of bad care.”

Hull adds that savvy investors should take a page from

the many healthcare startups that are laser-focused on building trust with patients, particularly when it comes

to end-of-life decisions and hospice care. “They know

that success in healthcare depends on patients trusting

their doctors to help them make the best medical

decisions,” Hull says.

Positioned to accommodate uncertainty L.E.K.’s Kadar argues out that whatever direction Washington decides to take healthcare, an efficient, professionally managed group practice with advantages

of scale is well-positioned to succeed — and private

equity is one way for physician groups to reach that goal.

“These groups can adapt more quickly than smaller,

independent practices, whether progressives or

conservatives are in power,” he says. As an example,

Kadar imagines a scenario in which Medicare-for-all

comes to pass. “It turns out that most [PE-backed] groups

do very well on Medicare Advantage contracts. If your

group is focused on delivering more efficient, effective care, with strong operations, you’re in a good position no matter what happens.”

Former Representative Jim Delaney (D-Md) threw down the gauntlet to the left-leaning attendees at the California Democratic convention on June 2 by challenging Medicare-for-all.

”The problem with Medicare for all, it’s actually really simple, is that it makes private insurance illegal. And 150 million Americans have private insurance, and 70% of them like it according to polling. So if we want to actually create universal health care, we’re never going to do it by trying to get 150 million Americans to give up what they want.”

The crowd booed at first, but then gave him a respectful hearing. Pundit George Will and commentator Charlie Sykes think Delaney has a good point politically. But let’s look at Delaney’s claim through the apolitical lens of this blog.

1. Why Did Delaney make this claim?

Two reasons: He wanted to move the debate over U.S. healthcare from sound bites to substance. And Rep. Delaney wanted to distinguish himself from the rest of the pack of Democrat Presidential contenders and position himself as a moderate on this and other issues.

2. Does Medicare-for-all mean making private health insurance illegal?

Clearly for Sen. Bernie Sanders the answer is yes. But not for any of the other Democrat Presidential candidates, at least not right away. Some like Mayor Pete Buttigieg and entrepreneur Andrew Yang contemplate a gradual path, eventually leading to a single public payer. In Yang’s case, he expects that public health insurance will eventually out-compete private insurance, not that it will be outlawed. Others like Senators Cory Booker and Amy Klobuchar, Governors Hickenlooper and Inslee, and Rep. Eric Swalwell contemplate using public insurance, alongside private insurance, as the means to get to universal coverage, more like “Medicare for all who want it.” This month’s Kaiser Family Foundation poll found that 55% do not perceive that Medicare-for-all would mean abolishing private insurance.

3. How many Democratic candidates advocate Medicare-for-all?

Of the 24 Democrats who have announced their candidacy (25, if you count former Sen. Mike Gravel), 13 advocate some version of Medicare-for-all, but 10 prefer some other approach to achieve universal coverage. Former Vice-President Joe Biden has not put forward a clear position yet. (Sen. Gravel supports universal healthcare “like Medicare.”)

4. What about Republicans?

Many Republicans, including the President himself, have at times given lip service to universal healthcare coverage. Most of them also advocate “protecting” Medicare, in some cases by scaling it back and limiting it. However, the President and Senate Republicans are once again pledging to “repeal and replace Obamacare” with a new plan, touted as “phenomenal” (though no details so far). At first the new plan was promised “in a very short period of time,” then “in next 2 months,” and now most recently “after the 2020 election.” For them, opposition to Medicare-for-all is a political matter of faith, not just a strategy for preserving private health insurance for those who want it.

5. How many Americans have private health insurance?

Private employer-based insurance covered 181 million Americans in 2017. According to the Census Bureau the full 2017 breakdown is:

(Note: Some individuals had more than one type of insurance during year)

6. Are Americans satisfied with their own private employer-based healthcare insurance?

Americans currently rate the “coverage” (69%) and “quality” (80%) for their own individual health plans as “good” or “excellent,” according to a December 2018 Gallup poll.

7. How does this compare with Medicare satisfaction statistics?

For Medicare recipients the ratings for “coverage” (88%) and “quality” (88%) are even better, in the same poll.

8. Do Americans see any downside to having employer-based healthcare insurance?

Many Americans feel locked into their current jobs lest they lose health benefits. This is especially so if they have chronic pre-existing conditions. Fear of losing coverage subtly puts them at the mercy of the employer for wages and work conditions. In addition, employees are shouldering a larger share of premiums and copays with each passing year. A Rand study showed that in the first decade of the 2000s, workers gains in productivity were offset by higher healthcare costs, holding their take-home wages flat. Increasingly, employees are switching to plans with high deductibles and less doctor choice.

Americans also express dissatisfaction with the wider system, even if they are satisfied with their own plans. They rate “coverage” at 34% and “quality” at 55% nationally.

Americans polled by Gallup are especially dissatisfied with costs. Only 58% are satisfied with cost of their own plan, while a low 20% are satisfied with overall cost in the national system.

9. Who are other stakeholders in the healthcare debate besides employees with employer-based insurance?

All Americans have a stake in healthcare reform. But here are some stakeholder sub-groups with special issues:

The uninsured are special stakeholders, as well.

10. Which of these stakeholders have the most to lose with Medicare-for-all?

In the first instance, healthcare insurers would be most directly affected. On closer look, I predict that several functions would not change much at all under a single-payer. There would still be enrollments, benefits management, claims processing, chronic disease management, contract negotiation, and customer service. These functions would continue, either in the form of subcontracts with government payers or in the form of direct government employment. Meanwhile, some would say that insurance companies have abdicated their job of true risk management, and have simply become pass-throughs for local health system monopolies and oligopolies. Under Medicare-for-all administrative complexities would be simplified, and inflated profits and salaries would be constrained, with resultant cost savings for the overall system

11. Which of these stakeholders have the most to gain with Medicare-for-all?

Big business and public sector employers probably have the most to gain from Medicare-for-all or other healthcare reform. In 1991, Sam Walton famously railed to his managers, “These people are skinnin’ us alive not just here in Bentonville but everywhere else, too….They’re charging us five and six times what they ought to charge us….So we need to work on a program where we’ve got hospitals and doctors…saving our customers money and our employees money.” Walmart and others like Bezos, Buffet and Dimon’s innovative Haven healthcare management enterprise are taking matters into their own hands out of frustration with traditional insurance’s inability to control healthcare costs and deliver value.

Small businesses also stand to gain much from jettisoning healthcare costs and administrative burdens under a single payer system. Small businesses feel a disproportionate brunt of current high healthcare costs. For them, a single sick employee can jack up their experience-rating. Tracking payments and maintaining regulatory compliance saps valuable administrative time. For these reasons, just 29 percent of small businesses with fewer than 50 employees provided group health insurance in 2016. Many dropped insurance for their employees and referred them to the public exchanges instead.

12. Is Medicare-for-all the end goal for its supporters, or only the means to a further goal?

Democrat candidates base their arguments for Medicare-for-all, or for their alternative approaches, primarily on achieving universal coverage. This is a worthy goal in itself. Having healthcare insurance has been linked to quality of life, life expectancy, worker productivity, and financial security.

But this blog has argued that an even more critical goal is constraining costs. Climbing healthcare costs are consuming an ever-greater share of the GDP, diverting resources from other worthy projects, and stressing household, corporate and public budgets.

This blog, thus, sees single payer as a means to the end of leveraging cost containment.

13. If Medicare-for-all in some form would give government the ability to finally constrain costs, who would be the biggest losers?

Clearly, potentially the biggest losers would be the healthcare industry, from front-line workers to professionals to health system CEOs. However, many could shift into higher-value healthcare activities. Others could transition to equivalent jobs in other service industries. True, a few might need to accept cuts in their bloated incomes. Since healthcare currently comprises almost one-fifth of all economic activity, these transitions should be done slowly. Leaders should do some industrial policy planning to facilitate changes and mitigate disruptions. Having said that, we should keep in mind that healthcare professionals are generally well educated, motivated, adaptable and resourceful, thus able to successfully navigate change.

Conclusion

Rep. Delaney asks a good question: Whether Americans with current employer-based health insurance would trade it for Medicare-for-all. Would they recognize that Medicare gets better quality and coverage ratings than private insurance? Would they view changing to Medicare-for-all as a fair bargain to achieve universal access for all? Do they think that single-payer would give the government leverage to finally constrain costs? Do they recognize that the total cost of healthcare – whether in the form of out-of-pocket payments, paycheck deductions, or new “$30 trillion” healthcare taxes – comes out of their wallets, one way or another?

On the other hand, could a larger public insurer (Medicare-for-all-who-want-it) gain sufficient reach and clout to tame the healthcare tapeworm without a Sanders-style single payer system? This blog will tackle that question in another post.

Now, take action.

The news is full of stories about monumental surprise hospital bills, sky-high drug prices and patients going bankrupt. The government’s approach to addressing this, via an executive order that President Trump signed June 24, 2019, is to make hospitals disclose prices, including negotiated rates with insurers, so that patients supposedly can comparison shop. But this is fool’s gold – information that doesn’t address the real question about why these prices are so high in the first place.

I know from my time as an academic researcher, hospital board member, adviser to Congress and health insurance CEO that the problems in health care are far deeper than just knowledge about hospital charges that few will ever pay.

While it is easy to blame greedy pharmaceutical manufacturers, health insurers and hospital executives, the problem comes from the very nature of our confused system. Who actually benefits from these high prices and why do they persist? Is it just greed, or something endemic in the system?

Many in the health care system, including hospitals, doctors and insurers, are complicit in this confusing mess, although all can justify their individual actions.

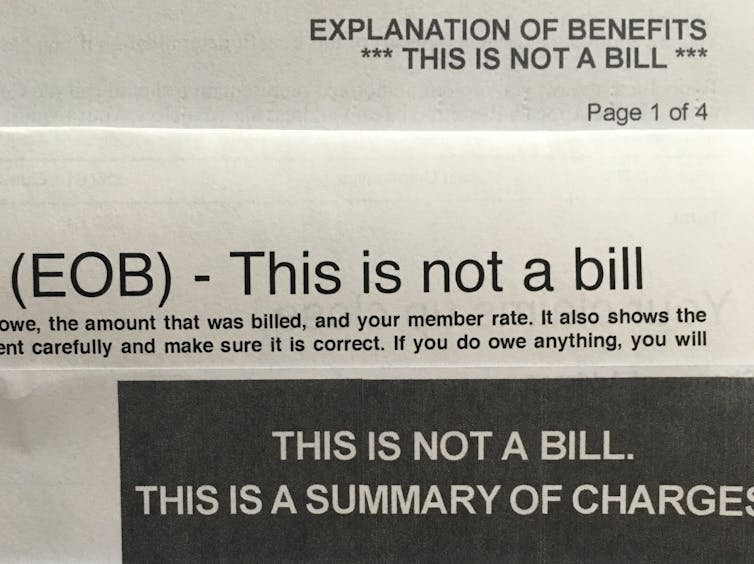

The confusion begins for the patient when he or she receives an explanation of benefit (EOB). This typically says it is “Not a Bill,” although it really looks like one. What it actually shows is incredibly high provider prices and an equally implausible discount. The bottom line lists the actual payment and the amount the patient owes. Patients are supposed to be grateful for the discounts after they recover from the sticker shock of the listed price.

When a service is provided out-of-network, or is not covered at all, or the person doesn’t have insurance, the patient is supposed to pay this full amount. Such “surprise bills” typically come to those least prepared to pay and, as a result, providers typically recover very little. So no one wins, except the collection agency and the lawyers.

I believe the standard EOB is the beginning of unnecessary complexity that leads to higher prices and an impossibly flawed market where shopping can never really work properly.

This ridiculous situation actually starts with insurance companies selling policies to ill-informed employers who don’t understand health care but effectively are the purchasers. Employers hire brokers and consultants to collect proposals from insurers; by some estimates, as many as 50 million people in the U.S. are covered by such plans.

These proposals frequently focus on the size of the discount from providers’ list prices as an indicator of how much the employer can save. The overall total cost or coverage is more important, but harder to estimate, since it depends on actual care delivered to employees. The unrecognized incentive for providers and insurers is to increase prices in order to increase the size of the discount.

I have actually seen cases where the insurer requests higher list prices from a provider to pump up the discount they can report to employers. This is crazy.

One solution to this mess would be to require uniform prices by all providers to all purchasers. Maryland has a form of this “all-payer” system where everyone pays the same under rate regulation or negotiation. France, Germany, Japan and the Netherlands also use this form of control.

Benchmark pricing against what Medicare pays would do something similar, with everyone paying a fixed percent of these nationally regulated rates. This would blunt the ability of hospitals to arbitrarily jack up list charges and negotiate contract prices with insurers based on relative market power.

Unfortunately for consumers, such rate setting may be a political “bridge too far.” While some progressives might like regulation, conservatives likely will not because it challenges their faith in the superiority of free-market negotiations around prices.

And it might dampen innovation and even competition, depending on how realistic and flexible the regulators are in responding to new technology, alternative procedures, quality differentials and consumer demands – the decisions where markets are supposed work well.

The overarching question is whether patients and employers can ever do comparison shopping effectively. Clearly for many things, there can be no head-to-head choice. Trauma, highly complex surgery and other care cannot be predicted ahead of time or standardized to fit a consumer market model.

However, some things can be compared. Insurers now routinely let consumers know if a test or image could be done for less elsewhere. Perhaps comparing just a few services as an overall cost indicator is the best we can do.

But it may also be possible to determine overall relative bargains for a typical package of care to guide choices. My Cleveland hospital, MetroHealth System, manages Medicaid patients for a total cost which is 29% less than when they wander around without a medical home. This is a meaningful difference.

A first step towards comparison shopping might be eliminating the EOB as we know it. Rather than showing meaningless list prices, it would be more revealing if hospitals and insurers had to disclose their actual payment terms.

An alternative benchmark might be to provide health care consumers with a range of contract rates or the Medicare rate for a service. Then the difference between what you and others actually pay could be useful in comparing providers and insurers.

Those who long for a total overhaul of our system through “Medicare for All” or its variants, such as many Democrats vying for the nomination,will still have to deal with the question of how to contract and pay for all these moving parts. The temptation will be toward simple solutions involving prices, discounts and rate regulation – still, I believe, effectively a pursuit of fool’s gold.

KINGSPORT, Tenn. – Molly Worley is an angry grandma.

For weeks she has stubbornly occupied a folding lawn chair on a grassy median outside Holston Valley Medical Center, sheltered from sweltering Appalachian summer sun by a thin tarp and flanked by a rotating crew staging a round-the-clock protest since May 1.

Behind them is the state-of-the-art neonatal intensive care unit where Worley’s newborn grandson spent his first weeks of life treated for opioid exposure.

In the same building is a Level I trauma center to respond to the most critical emergencies.

Both facilities will downgraded in the coming months, diverting the sickest babies and adults elsewhere.

The cuts are the latest fallout from an unusual and controversial merger between two former rival hospital systems headquartered in northeast Tennessee.

The newly formed company, Ballad Health, is now the sole hospital provider for a region the size of New Jersey. For nearly 1.2 million people people living in a largely rural stretch of 29 counties in northeast Tennessee and nearby parts of Virginia, North Carolina and Kentucky, Ballad hospitals are the only inpatient option.

Mergers involving hospitals that compete for same patients face opposition from the Federal Trade Commission, which can block mergers on the grounds the combined company can limit patient choices, cut services, raise prices and diminish quality.

Ballad officials found a way to bypass FTC rules. They turned to Tennessee state Sen. Rusty Crowe, R-Johnson City, who successfully carried legislation making the merger possible. Crowe is a longtime paid consultant with Ballad hospitals.

Only a handful of other states have exempted similar hospital mergers from FTC anti-monopoly rules. Ballad’s is the largest.

CEO Alan Levine said the merger lets the hospital system save money and keep rural hospitals afloat in a state that is already No. 2 in the nation for closures.

Eliminating overlapping staff and services, including the trauma center and NICU, will free funds to invest in other public health initiatives. Ballad pledged to keep open all of its rural hospitals for five years and to invest $308 million in public health, medical education and other initiatives.

“Every decision we make starts and ends with how can we best serve the community and what does the evidence show will lead to the best possible outcome,” Levine said.

“You don’t want a trauma center on every corner and you don’t want a NICU on every corner because it dilutes volume and hurts quality,” he said.

No rural hospitals owned by Ballad have been closed.

Some residents, doctors, nurses, EMS workers and public officials say the changes by Ballad expose the dangers of a single system imposing decisions on health care services on a captive audience that has no other options. More than 23,000 people have signed a petition opposing Ballad’s proposed changes.

“Never ever have I been this outspoken about anything,” said Worley, 60. “This NICU saved my grandson’s life. With Ballad we have no other choice. They have a monopoly at every level of health care.”

As hospital systems across the country struggle to stay afloat, particularly in rural areas, Ballad’s plan is being closely watched by other states weighing whether to allow other hospitals to take a similar approach.