In his first address to a joint session of Congress, delivered on the eve of his 100th day in office, President Biden laid out his vision for two major legislative proposals to follow the $1.9T stimulus package he signed into law last month.

The first, described as an “infrastructure” bill, focuses largely on investing in transportation-related improvements, building projects, and “green” upgrades to the nation’s energy grid, along with a $400B investment in home-based care for the elderly and people with disabilities—which amounts to over 17 percent of the package’s $2.3T price tag.

The second, which he unveiled in Wednesday’s speech, is a $1.8T “families” bill, is largely aimed at expanding childcare subsidies, early childhood education, paid family and medical leave, and educational investments. Included in that package is $200B to extend the temporary subsidies—approved as part of last month’s stimulus law—for those seeking health insurance coverage on the individual marketplaces created by the Affordable Care Act (ACA).

Notably absent from either proposal were two categories of healthcare reform that received much focus and airtime during last year’s election campaign: reducing the cost of prescription drugs and lowering the eligibility age for Medicare to 60 or below. Given the closely divided makeup of the new Congress, and the relatively moderate position staked out by the Biden administration on healthcare issues (with a bias toward bolstering the ACA rather than pursuing sweeping changes), we’re not surprised to see the Medicare expansion go unmentioned.

But the bipartisan popularity of lowering prescription drug costs seems like a missed opportunity for Biden, who encouraged the Congress to return to it separately, later in the year. We’ll see. For now, with even some Democrats expressing concern about the $4.1T price tag of Biden’s proposals, we would be surprised if all $600B of the healthcare-related spending makes it to the final legislation. In particular, our guess is that some portion of the home-care spending will get traded away in favor of other components of the package. Expect negotiations to be intense.

Just as other industries are rolling back some consumer-friendly changes made early in the pandemic — think empty middle seats on airplanes — so, too, are health insurers.

Many voluntarily waived all deductibles, copayments and other costs for insured patients who fell ill with covid-19 and needed hospital care, doctor visits, medications or other treatment.

Setting aside those fees was a good move from a public relations standpoint. The industry got credit for helping customers during tough times. And it had political and financial benefits for insurers, too.

But nothing lasts forever.

Starting at the end of last year — and continuing into the spring — a growing number of insurers are quietly ending those fee waivers for covid treatment on some or all policies.

“When it comes to treatment, more and more consumers will find that the normal course of deductibles, copayments and coinsurance will apply,” said Sabrina Corlette, research professor and co-director of the Center on Health Insurance Reforms at Georgetown University.

Even so, “the good news is that vaccinations and most covid tests should still be free,” added Corlette.

That’s because federal law requires insurers to waive costs for covid testing and vaccination.

Guidance issued early in President Joe Biden’s term reinforced that Trump administration rule about waiving cost sharing for testing and said it applies even in situations in which an asymptomatic person wants a test before, say, visiting a relative.

But treatment is different.

Insurers voluntarily waived those costs, so they can decide when to reinstate them.

Indeed, the initial step not to charge treatment fees may have preempted any effort by the federal government to mandate it, said Cynthia Cox, a vice president at KFF and director for its program on the Affordable Care Act.

In a study released in November, researchers found about 88% of people covered by insurance plans — those bought by individuals and some group plans offered by employers — had policies that waived such payments at some point during the pandemic, said Cox, a co-author. But many of those waivers were expected to expire by the end of the year or early this year.

Some did.

Anthem, for example, stopped them at the end of January. UnitedHealth, another of the nation’s largest insurers, began rolling back waivers in the fall, finishing up by the end of March. Deductible-free inpatient treatment for covid through Aetna expired Feb. 28.

A few insurers continue to forgo patient cost sharing in some types of policies. Humana, for example, has left the cost-sharing waiver in place for Medicare Advantage members, but dropped it Jan. 1 for those in job-based group plans.

Not all are making the changes.

For example, Premera Blue Cross in Washington and Sharp Health Plan in California have extended treatment cost waivers through June. Kaiser Permanente said it is keeping its program in place for members diagnosed with covid and has not set an end date. Meanwhile, UPMC in Pittsburgh planned to continue to waive all copayments and deductibles for in-network treatment through April 20.

What It All Means

Waivers may result in little savings for people with mild cases of covid that are treated at home. But the savings for patients who fall seriously ill and wind up in the hospital could be substantial.

Emergency room visits and hospitalization are expensive, and many insured patients must pay a portion of those costs through annual deductibles before full coverage kicks in.

Deductibles have been on the rise for years. Single-coverage deductibles for people who work for large employers average $1,418, while those for employees of small firms average $2,295, according to a survey of employers by KFF. (KHN is an editorially independent program of KFF.)

Annual deductibles for Affordable Care Act plans are generally higher, depending on the plan type.

Both kinds of coverage also include copayments, which are flat-dollar amounts, and often coinsurance, which is a percentage of the cost of office visits, hospital stays and prescription drugs.

Ending the waivers for treatment “is a big deal if you get sick,” said Robert Laszewski, an insurance industry consultant in Maryland. “And then you find out you have to pay $5,000 out-of-pocket that your cousin didn’t two months ago.”

Costs and Benefits

Still, those patient fees represent only a slice of the overall cost of caring for a hospitalized patient with covid.

While it helped patients’ cash flow, insurers saw other kinds of benefits.

For one thing, insurers recognized early on that patients — facing stay-at-home orders and other restrictions — were avoiding medical care in droves, driving down what insurers had to fork out for care.

“I think they were realizing they would be reporting extraordinarily good profits because they could see utilization dropping like a rock,” said Laszewski. “Doctors, hospitals, restaurants and everyone else were in big trouble. So, it was good politics to waive copays and deductibles.”

Besides generating goodwill, insurers may benefit in another way.

Under the ACA, insurers are required to spend at least 80% of their premium revenue on direct health care, rather than on marketing and administration. (Large group plans must spend 85%.)

By waiving those fees, insurers’ own spending went up a bit, potentially helping offset some share of what are expected to be hefty rebates this summer. That’s because insurers whose spending on direct medical care falls short of the ACA’s threshold must issue rebates by Aug. 1 to the individuals or employers who purchased the plans.

A record $2.5 billion was rebated for policies in effect in 2019, with the average rebate per person coming in at about $219.

Knowing their spending was falling during the pandemic helped fuel decisions to waive patient copayments for treatment, since insurers knew “they would have to give this money back in one form or another because of the rebates,” Cox said.

It’s a mixed bag for consumers.

“If they completely offset the rebates through waiving cost sharing, then it strictly benefits only those with covid who needed significant treatment,” noted Cox. “But, if they issue rebates, there’s more broad distribution.”

Even with that, insurers can expect to send a lot back in rebates this fall.

In a report out this week, KFF estimated that insurers may owe $2.1 billion in rebates for last year’s policies, the second-highest amount issued under the ACA. Under the law, rebate amounts are based on three years of financial data and profits. Final numbers aren’t expected until later in the year.

The rebates “are likely driven in part by suppressed health care utilization during the COVID-19 pandemic,” the report says.

Still, economist Joe Antos at the American Enterprise Institute says waiving the copays and deductibles may boost goodwill in the public eye more than rebates. “It’s a community benefit they could get some credit for,” said Antos, whereas many policyholders who get a small rebate check may just cash it and “it doesn’t have an impact on how they think about anything.”

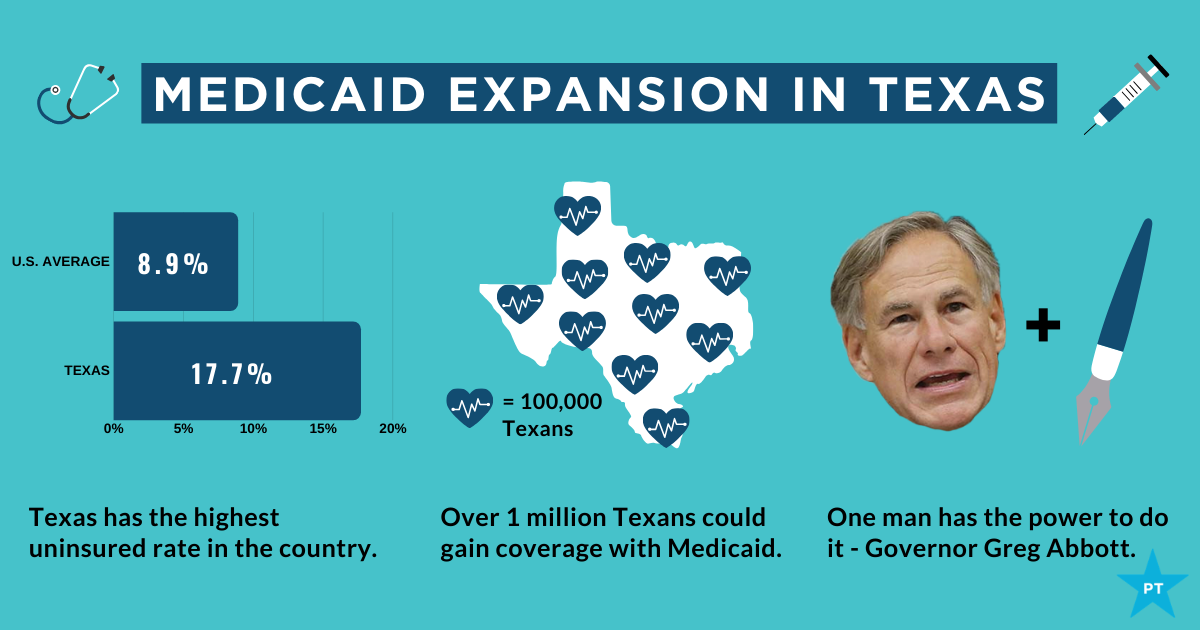

The showdown between the Biden administration and the state of Texas over Medicaid expansion continued to escalate this week. Sen. John Cornyn (R-TX) said he planned to place a hold on the confirmation of Chiquita Brooks-LaSure to become Administrator of the Centers for Medicare & Medicaid Services (CMS), until his concerns over the agency’s move last week to rescind a waiver extension previously granted by the Trump administration were addressed.

The so-called “1115 waiver”—worth more than $11B annually—would have extended by a decade Texas’ ability to use Medicaid funds to cover hospital costs for uninsured residents, rather than expanding Medicaid coverage under the Affordable Care Act (ACA). In rescinding the waiver extension, the Biden administration cited the lack of a public notice process before the waiver was granted, and said that the state’s existing waiver would instead expire next year, as previously scheduled.

Sources inside the administration told the Washington Post last week thatthe move was intended to force Texas’ hand on Medicaid expansion; the state is one of 12 that have not expanded Medicaid, leaving it with the largest share of uninsured residents of any state, with eligibility currently limited to pregnant women, children, people with disabilities, and families with monthly incomes under $300 per month, or 13.6 percent of the federal poverty level.

Enticing the dozen remaining holdout states to expand Medicaid is an important policy priority for the new administration.A key component of the recently passed American Rescue Plan Act is a package of enhanced incentives for those states to expand eligibility, offering an extended 90 percent federal match, in addition to increased funding for existing Medicaid populations.

Although none of the non-expansion states have budged yet, there has been renewed focus among state lawmakers on Medicaid expansion, including in Texas, where the idea had garnered bipartisan support. However, on Thursday, the Texas legislature voted down a proposal aimed at pushing the state toward expanding coverage for the uninsured, by an 80-68 margin. Meanwhile, the rescission of Texas’ waiver has angered the state’s Republican leadership, along with the Texas Hospital Association, whose members have benefited from the waiver’s use of funds to reimburse them for delivering uncompensated care.

While Cornyn’s hold will not ultimately stop the confirmation of the new CMS leader, the escalation on both sides over the past several days surely makes finding a compromise solution less likely. The Biden health policy team is said to be developing a new proposal, as part of an upcoming legislative package, to use the ACA marketplace to offer coverage to people in non-expansion states who might otherwise be eligible for Medicaid—yet another attempt to address one of the longest-standing points of contention stemming from the 2010 health reform law.

President Biden promised on the campaign trail to expand the Affordable Care Act to cover more of the roughly 29 million nonelderly Americans (about 11 percent of that population) who remain uninsured. He also said he’d strengthen the law by, for instance, providing an accessible and affordable public option and increasing tax credits to make it easier for people who buy insurance on their own to afford monthly premiums. Once in office, Biden immediately moved to reopen the period when people could enroll in the ACA marketplaces.

Unfortunately, the administration is paying little heed to a problem that is in many ways just as insidious as lack of insurance: underinsurance. That’s when people get too little from the insurance plans that they do have.

After passage of the ACA, the number of Americans lacking any insurance fell by 20 million, dropping to 26.7 million in 2016 — a historic low as a percentage of population. The figure began to creep up again during the Trump administration, reaching 28.9 million in 2019. That’s the problem that the current administration wants to address, and it certainly needs attention.

But according to research by the Commonwealth Fund, a foundation focused on health care, 21.3 percent of Americans have insurance so skimpy that they count as underinsured: Their out-of-pocket health-care expenses, excluding premiums, amount to at least 5 to 10 percent of household income. The limits in coverage mean their plans might provide little financial protection in a health-care crisis.

High-deductible plans offered by employers are one part of the problem. Among people covered by the companies they work for, enrollment in high-deductible health plans rose from 4 percent in 2006 to 30 percent in 2019, according to a report from the Kaiser Family Foundation. The average annual deductibles in such plans are $2,583 for an individual and $5,335 for families.

In theory, high-deductible plans, which make people spend lots of their own money before insurance kicks in, turn people into careful consumers. But research finds that people covered by such plans skip care, both unnecessary (elective cosmetic surgery, for instance) and necessary (cancer screenings and treatment, and prescriptions).Black Americans in these plans disproportionately avoid treatment, widening racial health inequities.

Health savings accountsare designed to blunt the harmful effects of high-deductible plans: Contributions by employers, and pretax contributions by individuals, help to cover costs until the deductible is reached. But not all high-deductible health plans offer such accounts, and many people in lower-wage jobs don’t have them. In the rare cases that they do, they often don’t have extra money to deposit in them.

In a November 2020 article in the journal Health Affairs, scholars affiliated with Brown University and Boston University found that enrollment in high-deductible plans had increased across all racial, ethnic and income groups from 2007 to 2018; they also found that low-income, Black and Hispanic enrollees were significantly less likely than other groups to have a health savings account — and the disparities had grown over time.

The short-term health-care plans — a.k.a. “junk” plans — that the Trump administration expanded also contribute to the problem of underinsurance. They often have low premiums but do not cover preexisting conditions or basic services like emergency health care.

Fortunately, proposals like Biden’s that make health care more accessible also tend to address the problem of underinsurance, at least in part. For example, to make individual-market insurance more affordable, Biden proposes expanding the tax credits established under the ACA. His plan calls for removing the cap on financial assistance, now set at 400 percent of the federal poverty level, in the insurance marketplaces and lowering the statutory limit on premiums to 8.5 percent of income (from nearly 10 percent).

The president also proposes to peg the size of the tax credits that subsidize premiums to the best plans on the marketplaces, the “gold” plans, rather than “silver” plans. This would increase the size of these credits, thereby making it easier for Americans to afford more-generous plans with lower deductibles.

The most ambitious Biden proposal is a public option, which would create a Medicare-like offering on marketplaces, available to anyone.Pairing this with allowing any American to opt out of their employer plan if they found a better deal on HealthCare.gov or their state marketplace — which they can’t now — would help some people escape high-deductible plans. The public option would also eliminate premiums and involve minimal to no cost-sharing for low-income enrollees — especially helpful for uninsured (and underinsured) people in states yet to expand Medicaid.

Given political realities, however, this policy may not see the light of day. So it would be best to target underinsurance directly. Most people with high-deductible plans get them through an employer. Yet unlike in the marketplace plans, the degree of cost sharing in these employer plans is the same for low-income as well as high-income employees. To deal with that problem, the government could offer incentives for employers to expand the scope of health services they cover — even in high-deductible plans. Already, many such plans exempt from the deductible some primary-care visits and generic-drug prescriptions. The list could grow to include follow-up visits and certain specialist care.

Instead of encouraging health savings accounts, the government could offer greater pretax incentives that encourage employers to absorb some of the costs that they have shifted onto their lower-income employees; that would help to prevent the insurance equity gap from widening further. The government could compensate employers that cover co-pays or other costs for their low-income employees. It could also subsidize employers that move away from high-deductible plans, at least for lower-income people.

Health insurance is complicated: More-affordable premiums are good only if they don’t bring stingy coverage. Greater investment in well-trained (and racially diverse) “navigators” — the people who help Americans enroll in plans on the federal marketplace, for example — would make it less likely that consumers would choose high-deductible plans without grasping their downsides. But it’s also important that people have options beyond risky high-deductible coverage.

The ACA expanded coverage dramatically — but the government needs to make sure that coverage amounts to more than an unused insurance card.

President Joe Biden moved to unwind Medicaid work requirements in Michigan and Wisconsin, after pulling the rules in Arkansas and New Hampshire.

CMS sent letters to health officials in Michigan and Wisconsin April 6 withdrawing their approval to implement work requirements for Medicaid beneficiaries. In both letters, CMS noted that combined with the COVID-19 pandemic, the work rules risk “significant coverage losses and harm to beneficiaries.”

In March, the Biden administration revoked approval for similar Medicaid work requirements in Arkansas and New Hampshire.

Small businesses are struggling to cover the high costs of healthcare for their employees after a year of COVID-19, according to a new poll sponsored by the Small Business Majority and patient advocacy group Families USA.

More than one in three small businesses owners said it’s a challenge getting coverage for themselves and their workers. That pain is particularly acute among Black, Asian American and Latino businesses, which have fewer resources than their White counterparts, SBMfound.

As a result, small businesses want policymakers to expand coverage access and lower medical costs, beyond the temporary fixes included in the sweeping $1.9 trillion American Rescue Plan passed by Congress earlier this month.

Dive Insight:

Providing health insurance can be pricey for small employers, a challenge that’s been exacerbated by the pandemic and its subsequent economic downturn.

Accessing health insurance has been a major barrier over the course of COVID-19, the national survey of 500 businesses with 100 employees or fewer in November found. The poll, conducted by Lake Research Partners for SBM and Families USA, found many such businesses have had to slash benefits during the pandemic. Among small business owners that have reduced insurance benefits, 36% have trimmed their employer contribution for medical premiums and 56% switched to a plan with a lower premium.

Additionally, one in five small business owners say they plan to change or lower coverage in the next few months, while only about a quarter have been able to maintain coverage for temporarily furloughed employees.

The situation is bleaker for minority-owned small businesses. Overall, 34% say accessing health insurance has been a top barrier during COVID-19, but that figure rises to 50%, 44% and 43% for Black, Asian American and Latino business respondents, SBM, which represents some 80,000 small businesses nationwide, said.

That’s in line with past SBM polling finding non-white entrepreneurs are more likely to face temporary or permanent closure in the next few months than their white counterparts, and are also more likely to struggle with rent, mortgage or debt repayments.

Washington did allocate a significant amount of financial aid for small businesses last year, and the ARP includes numerous provisions including increased subsidies for health insurance premiums for two years, and extended COBRA coverage for laid off employees through September.

But respondents to this latest polling urged for more long-term support.

The most popular policy proposal was bringing down the cost of prescription drugs, with 90% of businesses saying they supported the measure and 54% saying they were in strong support. Protecting coverage for people with pre-existing conditions was also popular, with 87% of small business owners in total support and 51% strongly supporting.

Three-fourths of small business owners strongly support a public health insurance option, while 73% support expanding Medicaid eligibility in all states and 66% support letting people buy into Medicare starting at age 55.

A survey of large to mid-size employers from the National Alliance of Healthcare Purchaser Coalitions published Wednesday found at least three-fourths of employers support drug price regulation, surprise billing regulation, hospital price transparency and hospital rate regulation.

The American Rescue Plan stimulus package just sweetened the deal for the twelve holdout states that haven’t yet expanded Medicaid.In exchange for expanding eligibility to the roughly four million adults with incomes up to 133 percent of the federal poverty level, new expansion states will also be eligible for afive percent increase in the federal matching rate for their entire traditional Medicaid population for a two-year period.

The graphic above shows the cumulative fiscal impact for holdout states, should all Medicaid-eligible individuals enroll. Since the traditional Medicaid population is so much larger than the expansion population, the temporary increase more than offsets states’ cost to cover their share of the expansion, resulting in an estimated net fiscal benefit of almost $10B. While the net benefit would vary from state to state, a Kaiser Family Foundation analysis found the two most populous non-expansion states, Texas and Florida, could net up to $1.9B and $1.8B respectively across the two-year period.

Medicaid expansion has had a significant positive financial impact on hospitals, reducing uncompensated care and increasing overall operating margin by an average of 1.7 percent.

A recent analysis by the Center on Budget and Policy Priorities founduncompensated care costs as a share of hospital expenses fell an average of 45 percent in Medicaid expansion statesbetween 2013 and 2017. So far, only two states eligible for the enhanced expansion, Alabama and Wyoming, have signaled interest in taking advantage of the new deal. Convincing the remaining ten to follow suit will require intense and coordinated advocacy efforts from the healthcare and business communities. Making the financial case for expansion should prove straightforward, compared to overcoming long-entrenched political opposition.

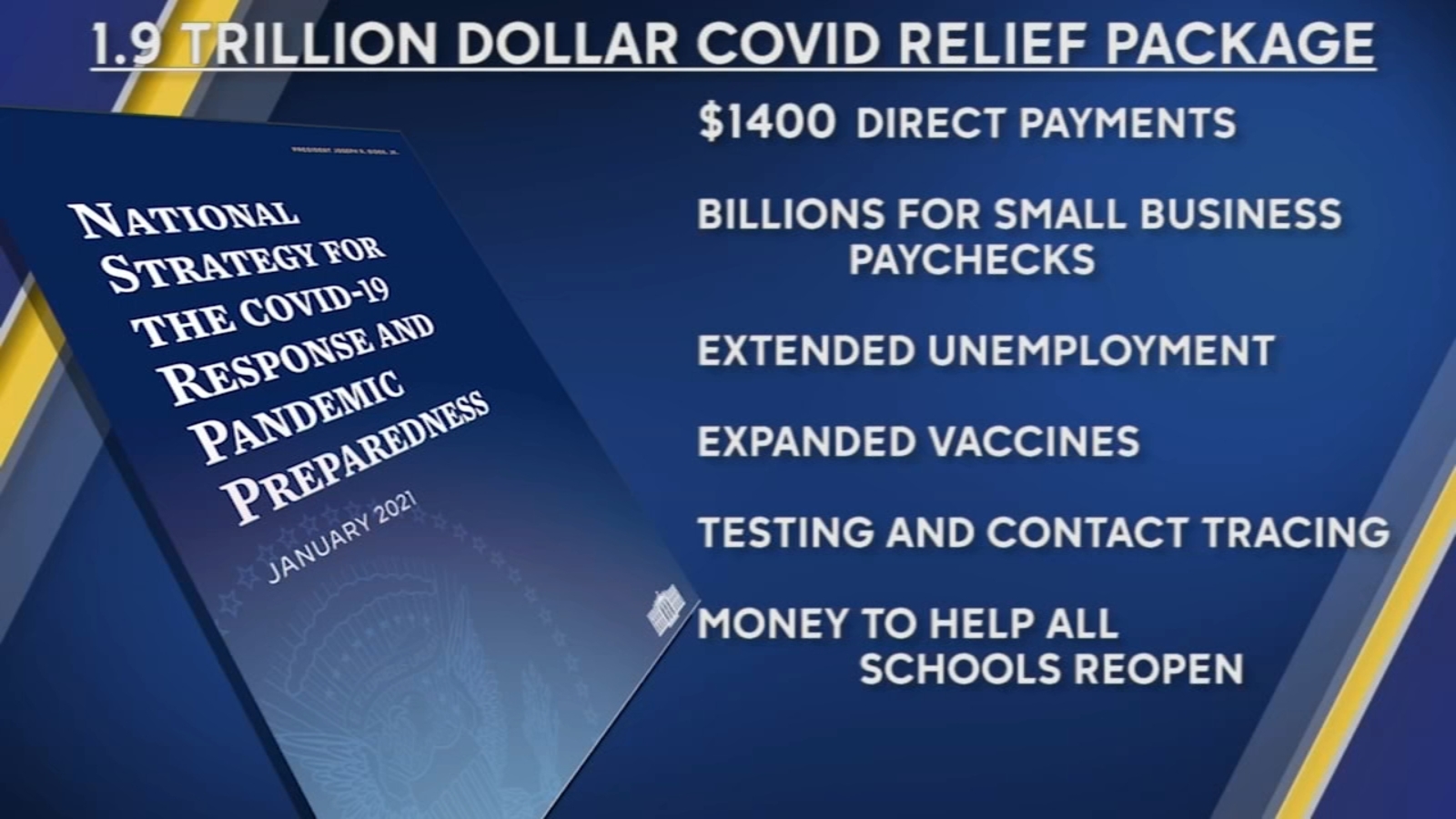

On Thursday, President Biden signed the American Rescue Plan (ARP) Act of 2021 into law, committing nearly$1.9T of federal spending to boost the nation’s recovery from the coronavirus pandemic. In addition to direct payments to American families, extension of unemployment benefits, several anti-poverty measures, and aid to state and local governments, the plan also contains several key healthcare measures.

Approved by Congress on a near party-line vote using the budget reconciliation process, the law includes thebroadest expansion of the 2010 Affordable Care Act (ACA) to date. It extends subsidies for upper-middle income individuals to purchase coverage on the Obamacare exchanges, caps premiumsfor those higher earners at a substantially lower level, and boosts subsidies for those at the lower end of the income scale.

The Congressional Budget Office (CBO) estimates that expanded ACA subsidies in the ARPwill result in 2.5M more Americans gaining coverage in the next two years. Fully subsidized COBRA coverage for workers who lost their jobs due to COVID is also extended through the end of September, which the CBO estimates will benefit an additional 2M unemployed Americans.

The ARP also puts in place new support for Medicaid, enhancing coverage for home-based care, maternity services, and COVID testing and vaccination, and providing new incentives for the 12 states which haven’t yet expanded Medicaid eligibility under the ACA to do so. In addition to the ACA’s 90 percent match for those states’ Medicaid expansion populations, the lucky dozen will also receive a 5 percent bump to federal matching for the rest of their Medicaid populations should they choose to expand.

Three policy changes of keen interest to providers were left out of the final version of the bill. First, while a special relief fund of $8.5B was created for rural providers, there was no additional allocation of relief funds for hospitals and other providers, similar to the $178B allocated by the CARES Act, despite initial proposals of up to $35B in additional funding. (Around $25B of the initial round of provider relief is still unspent.) Second, the ARPdid not extend or alter the repayment schedule for advance payments to providers made last year, in spite of industry pressure to implement more favorable repayment conditions. Finally, the new law does not extend last year’s pause on sequester-related cuts to Medicare reimbursement, although the House is expected to consider a separate measure to address that issue next week.

Notably, the coverage-related provisions of the ARP are only temporary, lasting through September of next year. That sets up the 2022 midterm elections as yet another campaign cycle dominated by promises to uphold and protect the Affordable Care Act—by then a 12-year-old law bolstered by this week’s COVID recovery legislation.

The House on Wednesday passed the mammoth $1.9 trillion COVID-19 relief package, which President Biden is expected to sign Friday.

The House approved the relief package in a starkly partisan 220-211 vote, sending the legislation to the White House and clinching Democrats’ first big legislative victory in the Biden era. No Republicans voted for the package and all but one House Democrat—Rep. Jared Golden of Maine—supported it. The Hill’s Cristina Marcos has more here.

The political split: Unlike the previous relief measures enacted last year, Democrats barely bothered to negotiate with Republicans and pushed the relief package through Congress along party lines using the budget reconciliation process. That allowed them to go as big as they wanted to go without running into a Senate GOP filibuster.

Republicans argue the use of a process dodging the filibuster shows Biden wasn’t serious about bringing unity, and House GOP lawmakers on Wednesday warned of the bill’s total cost.

But Democrats think Republicans will pay for their opposition to the popular bill and argued that they would oppose anything Biden proposed.

What’s in the $1.9T COVID-19 relief package: Along with $1,400 direct payments to households, an extension of expanded unemployment benefits, and aid for state and local governments, the package is loaded with other provisions intended to speed up the recovery from the recession and help struggling families fight the impact of COVID-19.

Tax credits: The bill increases the child tax credit for households below certain income thresholds for 2021 and makes it fully refundable, and also expands the earned income tax credit for the year.

Child care: $15 billion for grants to help low-income families afford child care and increases the child and dependent care tax credit for one year.

Pensions: $86 billion to bailout struggling union pension funds.

Transportation: $30 billion to bolster local subway and bus systems, $8 billion for airports, $1.5 billion for furloughed Amtrak workers, and $3 billion for wages at aerospace companies.

Housing: $27.4 billion in emergency rental assistance, another $10 billion to help homeowners avoid foreclosure, $5 billion in vouchers for public housing, $5 billion to tackle homelessness and $5 billion more to help households cover utility bills.

Small businesses: The American Rescue Plan broadens eligibility guidelines for the Paycheck Protection Program, allowing more nonprofit entities to be eligible, adds $15 billion in emergency grants and also sets aside more than $28 billion in funding for restaurants.

ObamaCare subsidies and Medicaid expansion: The bill increases ObamaCare subsidies through 2022 to make them more generous, a longtime goal for Democrats, and opens up more fully subsidized plans to individuals. It also would provide extra Medicaid funding to states that expand the program and have yet to do so.