Thursday was healthcare day at the Biden White House, the latest in a series of themed days during which the President has issued executive orders on topics ranging from COVID response to climate change to racial equity.

Facing a closely divided Congress, the new administration has focused so far on actions it can take unilaterally to advance its agenda, and as President Biden described it at a signing ceremony yesterday, his healthcare agenda is centered on “restoring the Affordable Care Act and restoring Medicaid to the way it was” prior to the Trump administration.

The new executive order reopens the HealthCare.gov insurance marketplace for a “special enrollment period”, lasting from mid-February to mid-May, allowing approximately 15M uninsured Americans in 36 states (including 3M who lost employer-based insurance due to COVID) to sign up for coverage, many subsidized by the federal government.

The order also instructs agencies to review many of the regulatory changes made by the Trump administration, including loosening restrictions on short-term insurance plans, and allowing states to use waivers to implement Medicaid work requirements. (Also included in Thursday’s action was a measure to immediately rescind the ban on taxpayer funding for abortion-related counseling by international nonprofits, the so-called “Mexico City rule”.)

Actually unwinding those Trump-era changes will take months (or possibly years) of regulatory work to accomplish, but Biden’s executive order puts that work in motion. Attention now turns to Congress, which the Biden team hopes will provide funding for increased subsidies for coverage on the Obamacare exchanges, along with allocating money for the administration’s aggressive COVID response plan.

Yesterday’s executive order is best understood as the starting gun for the lengthy legislative and regulatory process that lies ahead, as the Biden administration tries to bolster the 2010 health reform law, and stamp its mark on American healthcare.

The nearest-term 2021 actions will likely center on bolstering the ACA and Medicaid, after the Trump administration took aim at both.

Even with Democrats’ surprise flipping of the Senate, enacting big healthcare policies in Congress will be a heavy lift given the razor-thin margin in that body and division within the party on strategy.

A clearer path for incoming president Joe Biden is to focus on reversing policies enacted by President Donald Trump at the executive level.Trump’s tenure has been defined in large part by a chipping away at key tenets of the Affordable Care Act, curtailing the Medicaid program and sweeping deregulations critics allege harm consumer protections.

The nearest-term actions the incoming administration is likely to take will center on bolstering the landmark health law and Medicaid, both of which has drawn more bipartisan backing in recent years. Below are what the Biden health administration is likely to roll back quickly after inauguration Wednesday.

Boosting Affordable Care Act marketplace

One of Biden’s first moves may be to open a special enrollment period to sign up for coverage during COVID-19, combined with more outreach and enrollment assistance, Cynthia Cox, director of the ACA program at the Kaiser Family Foundation, said.

Beyond COVID-19, it’s likely the Biden administration will restore federal spending on navigation, marketing and outreach for exchange plans. For example, the Trump administration reduced the minimum number of navigator programs in each state using the federal marketplace to one. Biden could return it to two, and might also bring back the requirement that navigators have a physical presence in their service area.

Biden is also likely to unilaterally shore up standards for brokers, and take steps to bolster the exchange website healthcare.gov.

The Trump administration in December proposed a rule encouraging states to privatize their health insurance marketplaces instead of using healthcare.gov, which will make it more difficult for consumers to shop between plans and could divert people to subpar coverage, Tara Straw, senior policy analyst at the Center on Budget and Policy Priorities, wrote in a December blog post.

The rule doubles down on the administration’s approval of a Georgia waiver to privatize its marketplace in November, but would allow states to follow suit and rely entirely on third-party brokers without a waiver.

That rule is not yet final, so Biden’s HHS will likely remove it from the Federal Register to avoid fragmenting marketplace functions.

Biden could also beef up consumer protections and standards for web brokers, which also sell skimpy short-term health insurance and other non-ACA-compliant coverage.

Biden is also likely to re-expand the annual enrollment period. In 2017, the Trump administration shortened the annual enrollment period to 45 days. Biden’s HHS could use rulemaking to return that period to three full months.

The incoming administration could also reverse previous CMS guidance on Section 1332 waivers that let states subvert or sidestep ACA protections on coverage and cost. The Trump administration proposed a rule in November to codify the waiver standards in regulation but — despite a recent wave of proposed and final regulations as the Trump administration hustles to preserve its health agenda — the rule has not yet been finalized, so HHS could remove it from the Federal Register as well.

By nixing the rule, Biden could also help reverse Trump administration cuts from 2018 that slashed user fees on healthcare.gov plans. The November proposed rule would further decimate the fees, which finance a large swath of marketplace operating expenses, to 2.25% in 2022, versus 3% in 2021 and 3.5% last year.

One key tenet of Biden’s health agenda is to expand ACA subsidies to more low-income Americans, something he can’t do without Congress.However, Biden could use administrative processes to reverse a Trump-era method for indexing marketplace subsidies that kicked in for the 2020 plan year, which led to a small reduction in the financial aid.

Dialing back short-term and association health plans

Biden’s HHS could also roll back the controversial expansion of short-term health plans, bare-bones coverage that isn’t required to cover the 10 essential health benefits under the ACA.

Short-term plans were created as inexpensive stop-gap insurance that could last for up to three months, giving consumers peace of mind while they shopped more comprehensive coverage. However, in 2018, the Trump administration expanded the duration of the plans to 12 months, with a three-year renewal period, and also allowed all consumers — not just those who couldn’t afford other options — to purchase them.

HHS touted the expansion as giving consumers more options, while noting they weren’t meant for everyone. A yearlong investigation by House Democrats found the plans widely discriminate against women and people with pre-existing conditions, and had major coverage limitations leaving unwitting consumers susceptible to surprise medical bills.

The Biden administration could enact stricter limits against the sale of the plans. Through additional rulemaking, HHS could limit future enrollment or make it harder to renew short-term coverage, enact stronger consumer protections or beef up standards to limit their sale.

Though actions around limiting new people coming into the plans are likely, Biden may wait to see if Congress takes up the issue, experts say.

A growing number of Americans in the individual healthcare market have subscribed the inexpensive coverage amid skyrocketing medical costs. Roughly 3 million consumers bought the plans in 2019, a 27% growth from 2018, the investigation found. The explosive growth in use makes it a bit less likely Biden’s HHS would pursue immediate, unilateral movement in the space, for fear of kicking Americans off their coverage.

Biden could also reverse Trump’s regulatory changes that have been friendly to association health plans, which allow small businesses or groups to band together to offer coverage. Though the ACA enhanced oversight of the coverage, the Trump administration in June 2018 issued a rule exempting them from rules regulating individual and small-group employer coverage.

As a result, association health plans were allowed to exclude or charge more on the basis of gender, age or other factors.

A federal court invalidated the rule later that year, and some states took legislative or regulatory actions to discourage the use of association health plans. However, the plans —which cover an estimated 3 million Americans — are still not required to cover all essential health benefits, making them a likely target for the Biden administration.

“It is something that we’re going to see some action on pretty soon, but it’s challenging. You don’t want to take those plans away from people, especially during a pandemic,” Cox said.

Expanding Medicaid coverage, eligibility

The Trump administration has given red states new avenues to constrict their Medicaid programs, which provide safety-net health insurance to some 75 million Americans.

Biden will likely first revise state demonstration waiver policies to expand coverage. Among other measures, Biden could get rid of past CMS guidance allowing states to play with Medicaid eligibility through work requirements, controversial programs tying coverage eligibility to work or volunteering hours, and to cap program funding.

Tennessee this month became the first state to receive a federal green light to convert its Medicaid funding to a block grant, following controversial CMS guidance issued early last year. Republicans tout block grants as a way to lower costs, while Democrats oppose the models as capped funding could lead to restricted benefits down the line, especially during times of emergency like a pandemic or natural disaster.

It’s more difficult to roll back a waiver if it’s already been approved, but Biden could put restrictions on it or reverse the decision before it goes into effect, experts say, though Tennessee would have an opportunity to object.

There are also actions Biden could take to reinstate certain beneficiary protections, which would require regulatory changes, KFF researchers say. Those include revising or stopping pending proposals that would change how Medicaid eligibility is determined in a way that would probably result in previously eligible people losing coverage by enacting more documentation requirements; change the government’s methodology for recouping improper payments; and reduce enhanced federal funding for eligibility workers.

Biden’s administration could also tweak regulations that have already been finalized, including the final Medicaid managed care rule for 2020 that relaxed network adequacy, beneficiary protections and quality oversight.

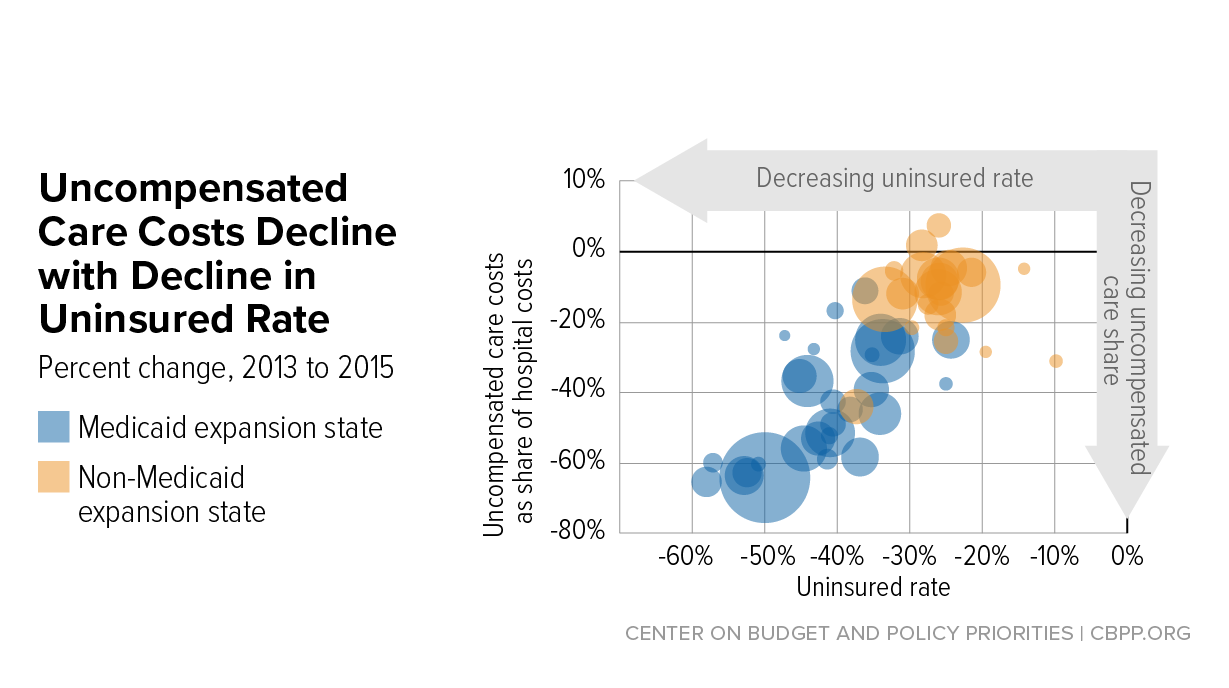

Hospital uncompensated care costs were up from $41.3B in 2018 and $38.4B in 2017, revealing an upward trend, according to AHA data.

Hospital uncompensated care costs increased right before the COVID-19 pandemic hit, according to new data from the American Hospital Association (AHA).

AHA data showed that hospitals incurred a new high of $41.61 billing in uncompensated care costs in 2019, the most recent year for which the group had complete data.

Uncompensated care costs in 2019 were up from $41.3 billion in 2018 and $38.4 billion in 2017 and were the second-highest per AHA records. Hospitals reported the most uncompensated care costs in 2013 when they incurred $46.8 billion.

Hospital uncompensated care costs decreased after the all-time high in 2013, but have recently started to tick back up after holding steady at $38.4 in 2016 and 2017.

In just the last 20 years, hospitals of all types have provided more than $660 billion in uncompensated care to patients, AHA reported. And that figure does not fully account for other ways in which provides provide financial assistance to patients of limited means, the group stated.

Each year, AHA aggregates data on uncompensated care, or care provided for which no reimbursement is received by hospitals from patients or payers. The data comes from the group’s Annual Survey of Hospitals, a comprehensive report of hospital financial data.

Uncompensated care is the sum of a hospital’s bad debt and financial assistance it provides, AHA explained.

Bad debt occurs when a hospital does not expect to obtain reimbursement for care provided, such as when patients are unable to pay their financial responsibility and do not qualify for financial assistance or are unwilling to pay their bills.

Hospitals also provide varying levels of financial assistance, AHA added. Financial assistance supports patients who cannot afford to pay and qualify for support from the hospital based on policies it has established based on the facility’s mission, financial condition, and geographic location, among other factors.

Combined, bad debt and financial assistance charges total a hospital’s uncompensated care charges, which is then multiplied by a hospital’s cost-to-charge ratio to determine total uncompensated care costs.

AHA noted that it expressed uncompensated care in costs versus charges because of significant variations in hospital payer mixes. Publishing the information as costs rather than charges enables better comparison across hospitals, the group said.

Nearly half of hospitals (48 percent) have seen bad debt and uncompensated care increase recently as a result of the ongoing COVID-19 pandemic, an analysis from consulting firm Kaufman Hall revealed.

More than 40 percent of hospitals also reported increases in percentage of uninsured or self-pay patients (44 percent) and the percentage of Medicaid patients (41 percent), which both contribute to unfunded or underfunded care at hospitals.

“The challenges brought on by the COVID-19 pandemic have affected nearly every aspect of hospital financial and clinical operations,” Lance Robinson, a managing director at Kaufman Hall, said at the time. “Organizations have responded to the challenge by adjusting their operations and strengthening important community relationships.”

Hospital uncompensated care costs – and bad debt as a result – are likely to increase in 2020 as hospitals come to terms with the impact COVID-19 has had on their financial health.

Already, hospitals have lost an estimated $323 billion in 2020 as a result of the COVID-19 pandemic, according to earlier projections from AHA.

About half of US hospitals also started the year in the red, AHA and Kaufman Hall stated in a recent report. The organizations predicted that hospital margins would sink to -7 percent in the second half of 2020 without comprehensive financial support from the government, but could decrease to a low of -11 percent if COVID-19 continued to periodically surge as it has.

President Joe Biden is expected to sign executive actions this week related to immigration, healthcare and climate, according to a memo obtained by The Hill.

The executive actions would follow 10 he signed Jan. 21 to combat COVID-19 spread.

Here are the three healthcare executive actions to expect Jan. 28, according to The Hill:

1. President Biden is set to rescind a policy banning foreign aid for abortion, known as the Mexico City policy. It prohibits the use of U.S. funds for foreign and national health organizations that perform or actively promote abortion, according to NBC News. The policy was announced by former President Ronald Reagan in 1984. According to The Hill, it has been rescinded by Democratic presidents and reinstated by Republican presidents, including former President Donald Trump, since then.

2. President Biden will also call for a review of the Title X family planning program, according to a memo obtained by The Hill. The federal program provides family planning and related preventive health services for low-income or uninsured people and others. In 2019, the Trump administration issued a final rule prohibiting providers that receive federal family planning money under the program from providing or promoting abortions. NBC News reported that the Biden administration is expected to back off this rule and “restore federal funding for Planned Parenthood,” which left the program in 2019.

3. President Biden plans to sign an executive action on Medicaid and initiate an open enrollment period under the ACA, according to a memo obtained by The Hill. The annual open enrollment period for 2021 closed in December. However, President Biden could initiate a special enrollment period.

President Biden is scheduled to take executive actions as early as Thursday to reopen federal marketplaces selling Affordable Care Act health plans and to lower recent barriers to joining Medicaid.

The orders will be Biden’s first steps since taking office to help Americans gain health insurance, a prominent campaign goal that has assumed escalating significance as the pandemic has dramatized the need for affordable health care — and deprived millions of Americans coverage as they have lost jobs in the economic fallout.

Under one order, HealthCare.gov, the online insurance marketplace for Americans who cannot get affordable coverage through their jobs, will swiftly reopen for at least a few months, according to several individuals inside and outside the administration familiar with the plans. Ordinarily, signing up for such coverage is tightly restricted outside a six-week period late each year.

Another part of Biden’s scheduled actions, the individuals said, is intended to reverse Trump-era changes to Medicaid that critics say damaged Americans’ access to the safety-net insurance. It is unclear whether Biden’s order will undo a Trump-era rule allowing states to impose work requirements, or simply direct federal health officials to review rules to make sure they expand coverage to the program that insures about 70 million low-income people in the United States.

The actions are part of a series of rapid executive orders the president is issuing in his initial days in office to demonstrate he intends to steer the machinery of government in a direction far different from that of his predecessor.

Biden has been saying for many months that helping people get insurance is a crucial federal responsibility. Yet until the actions planned for this week, he has not yet focused on this broader objective, shining a spotlight instead on trying to expand vaccinations and other federal responses to the pandemic.

The most ambitious parts of Biden’s campaign health-care platform would require Congress to provide consent and money. Those include creating a government insurance option alongside the ACA health plans sold by private insurers, and helping poor residents afford ACA coverage if they live in about a dozen states that have not expanded their Medicaid programs under the decade-old health law.

A White House spokesman declined to discuss the plans. Two HHS officials, speaking on the condition of anonymity about an event the White House has not announced, said Monday they were anticipating that the event would be held on Thursday.

According to a document obtained by The Washington Post, the president also intends to sign an order rescinding the so-called Mexico City rule, which compels nonprofits in other countries that receive federal family planning aid to promise not to perform or encourage abortions. Biden advisers last week previewed an end to this rule, which for decades has reappeared when Republicans occupied the White House and vanished under Democratic presidents.

The document also says Biden will disavow a multinational antiabortion declaration that the Trump administration signed three months ago.

The actions to expand insurance through the ACA and Medicaid come as the Supreme Court is considering two cases that could shape the outcome. One case is an effort to overturn rulings by lower federal courts, which have held that state rules, requiring some residents to work or prepare for jobs to qualify for Medicaid, are illegal. The other case involves an attempt to overturn the entire ACA.

According to the individuals inside and outside the administration, the order to reopen the federal insurance marketplaces will be framed in the context of the pandemic, essentially saying that anyone eligible for ACA coverage who has been harmed by the coronavirus will be allowed to sign up.

“This is absolutely in the covid age and the recession caused by covid,” said a health-care policy leader who has been in discussions with the administration. “There is financial displacement we need to address,” said this person, who spoke on the condition of anonymity to describe plans the White House has not announced.

The reopening of HealthCare.gov will be accompanied by an infusion of federal support to draw attention to the opportunity through advertising and other outreach efforts. This, too, reverses the Trump administration’s stance that supporting such outreach was wasteful. During its first two years, it slashed money for advertising and for community groups known as navigators that helped people enroll.

It is not clear whether restoring outreach will be part of Biden’s order or will be done more quietly within federal health-care agencies.

Federal rules already allow people to qualify for a special enrollment period to buy ACA health plans if their circumstances change in important ways, including losing a job. But such exceptions require people to seek permission individually, and many are unaware they can do so. Trump health officials also tightened the rules for qualifying for special enrollment.

In contrast, Biden is expected to open enrollment without anyone needing to seek permission, said Eliot Fishman, senior director of health policy for Families USA, a consumer health-advocacy group.

In the early days of the pandemic, the health insurance industry and congressional Democrats urged the Trump administration to reopen HealthCare.gov, the online federal ACA enrollment system on which three dozen states rely, to give more people the opportunity to sign up. At the end of March, Trump health officials decided against that.

During the most recent enrollment period, ending the middle of last month, nearly 8.3 million people signed up for health plans in the states using HealthCare.gov. The figure is about the same as the previous year, even though it includes two fewer states, which began operating their own marketplaces.

Leaders of groups helping with enrollment around the country said they were approached for help this last time by many people who had lost jobs or income because of the pandemic.

The order involving Medicaid is designed to alter course on experiments — known as “waivers” — that allow states to get federal permission to run their Medicaid programs in nontraditional ways. The work requirements, blocked so far by federal courts, are one of those experiments. Another was an announcement a year ago by Seema Verma, the Trump administration’s administrator of the Centers for Medicare and Medicaid Services, that states could apply for a fundamental change to the program, favored by conservatives, that would cap its funding, rather than operating as an entitlement program with federal money rising and falling with the number of people covered.

“You could think about it as announcing a war against the war on Medicaid,” said Katherine Hempstead, a senior policy adviser at the Robert Wood Johnson Foundation.

Dan Mendelson, founder of Avalere Health, a consulting firm, said Biden’s initial steps to broaden insurance match his campaign position that the United States does not need to switch to a system of single-payer insurance favored by more liberal Democrats.

The orders the president will sign “are going to do it through the existing programs,” Mendelson said.

As one of his first official actions upon taking office Wednesday, President Biden signed an executive order implementing a federal mask mandate, requiring masks to be worn by all federal employees and on all federal properties, as well as on all forms of interstate transportation. Yesterday Biden followed that action by officially naming his COVID response team, and issuing a detailed national plan for dealing with the pandemic. Describing the plan as a “full-scale wartime effort”, Biden highlighted the key components of the plan in an appearance with Dr. Anthony Fauci and COVID response coordinator Jeffrey Zients.

The plan instructs federal agencies to invoke the Defense Production Act to ensure adequate supplies of critical equipment, including masks, testing equipment, and vaccine-related supplies; calls for new nationalguidelines to help employers make workplaces safe for workers to return to their jobs, and to make schools safe for students to return; and promises to fully fund the states’ mobilization of the National Guard to assist in the vaccine rollout.

Also included in the plan is a new Pandemic Testing Board, charged with ramping up multiple forms of COVID testing; more investment in data gathering and reporting on the impact of the pandemic; and the establishment of a health equity task force, to ensure that vulnerable populations are an area of priority in pandemic response.

But Biden can only do so much by executive order. Funding for much of his ambitious COVID plan will require quick legislative action by Congress, meaning that the administration will either need to garner bipartisan support for its proposed “American Rescue Plan” legislation, or use the Senate’s budget reconciliation process to pass the bill with a simple majority (with Vice President Harris casting the tie-breaking vote). Even that may prove challenging, given skepticism among Republican (and some moderate Democratic) senators about the $1.9T price tag for the legislation.

We’d anticipate intense bargaining over the relief package—with broad agreement over the approximately $415B in spending on direct COVID response, but more haggling over the size of the economic stimulus component, including the promised $1,400 per person in direct financial assistance, expanded unemployment insurance, and raising the federal minimum wage to $15 per hour.

Some of the broader economic measures, along with the rest of Biden’s healthcare agenda and his larger proposals to invest in rebuilding critical infrastructure, may have to wait for future legislation, as the administration prioritizes COVID relief as its first—and most important—order of business.

Beyond the initiatives directly tied to COVID relief, President Biden’s healthcare agenda includes a broader bolstering of the protections and coverage mechanisms in the Affordable Care Act (ACA), as well as the rollback of several of the previous administration’s regulatory changes. We’ve outlined that agenda in the graphic below, as well as highlighting key members of the Biden healthcare team.

While much will depend on how the COVID pandemic continues to unfold, and how successful Biden is at striking bipartisan compromises with a closely divided Congress, we’re watching closely for the answers to several key questions:

(1) how aggressive can and will the new administration be in unwinding Trump-era reforms, particularly regarding Medicaid work requirements;

(2) what will be the thrust of Biden’s antitrust policyin the healthcare space;

(3) how hard will Biden be willing to push for expanded subsidies for individuals purchasing insurance on the ACA exchanges;

(4) how will the Biden team build on the transparency measures implemented by the Trump administration; and

(5) how will the new administration use payment reforms and other regulations to address racial and other disparities in healthcare?

All of that preceded by one burning question that has us holding our breath: who will Biden pick to run the all-important Centers for Medicare and Medicaid Services?

On January 14, 2021, Planned Parenthood Southeast and the Feminist Women’s Health Center filed a lawsuit challenging the Trump administration’s approval of Georgia’s waiver under Section 1332 of the Affordable Care Act (ACA). The lawsuit was filed in federal district court in DC. This post summarizes that legal challenge as well as parts of President Biden’s recent proposed pandemic relief package that relate to the ACA and coverage. The $1.9 trillion American Rescue Plan includes several coverage-related proposals and would follow the pandemic relief passed by Congress in December 2020.

Advocates Challenge The Approval of Georgia’s 1332 Waiver

Regular readers know that the Trump administration—through the Centers for Medicare and Medicaid Services (CMS) and the Treasury Department—approved a broad waiver request from Georgia under Section 1332 of the ACA. The approved waiver authorizes the state to establish a reinsurance program for plan year 2022 and eliminate the use of HealthCare.gov beginning with plan year 2023. CMS and Treasury approved the waiver application on November 1, 2020. The history of Georgia’s waiver application and approval is summarized in prior posts as well as in the complaint filed in the lawsuit.

The reinsurance portion of the waiver is straightforward; of the 16 states with an approved Section 1332 waiver, all but one state has established a state-based reinsurance program. But the second part of the waiver application, known as the Georgia Access Model, is far more controversial. This is the broadest waiver yet to be approved under Section 1332 and relies on interpretations of Section 1332 made in much-criticized Trump-era guidance from 2018.

Critics have long argued that Georgia’s proposal fails to satisfy Section 1332’s procedural and substantive guardrails, meaning it could not be lawfully approved by the Trump administration. Given this controversy, legal challenges to the waiver approval were expected.

The Lawsuit

Planned Parenthood Southeast and the Feminist Women’s Health Center—represented by Democracy Forward—filed a lawsuit in federal district court in DC on January 14, 2021. The lawsuit alleges that the Trump administration’s 2018 guidance and approval of Georgia’s waiver are unlawful because these actions violate Section 1332 of the ACA and the Administrative Procedure Act (APA). The lawsuit also cites many of the Trump administration’s ongoing efforts to undermine the ACA as evidence that the 2018 guidance and waiver approval are part of a pattern of ACA sabotage.

In particular, the plaintiffs argue that the 2018 guidance and waiver approval are contrary to Section 1332, exceed the scope of the agencies’ authority (by allowing states to waive non-waivable provisions of the ACA), and are arbitrary and capricious. They also argue that the waiver approval failed to satisfy procedural requirements under the ACA and APA because Georgia and the Trump administration “rushed through the process without adequate time for public comment and without adequate clarification of how the state intends to approach key issues.” Here, the lawsuit points to the fact that Georgia went through four iterations of its waiver application, that its application was incomplete, and that only eight comments (less than one half of one percent) of the 1,826 total comments submitted during the most recent federal public comment period were in support of the Georgia Access Model.

As such, the plaintiffs ask the court to vacate both the approved waiver and the 2018 guidance and declare that they are unlawful. They also ask that the federal government be enjoined from taking further action on Georgia’s waiver or considering other waivers under the 2018 guidance. The plaintiffs acknowledge that the reinsurance portion of the waiver is uncontroversial and that the focus of the lawsuit is on the Georgia Access Model; however, the plaintiffs challenge approval of the waiver as a whole and ask the court to set aside the waiver in whole or in part. The plaintiffs have not sued Georgia, although it is possible that Georgia may ask to intervene in the litigation to defend its interests.

Much of the lawsuit turns on how the Trump administration interpreted the statutory guardrails under Section 1332 and long-standing concerns about direct enrollment and enhanced direct enrollment.Federal officials can grant a Section 1332 waiver only if a state demonstrates that their proposal meets certain statutory “guardrails.”These guardrails ensure that a waiver proposal will 1) provide coverage that is at least as comprehensive as ACA coverage ( “comprehensiveness” guardrail); 2) provide coverage and cost-sharing protections that are at least as affordable as ACA requirements (“affordability” guardrail); 3) provide coverage to at least a comparable number of residents as under the ACA ( “coverage” guardrail); and 4) not increase the federal deficit. The Obama administration issued guidance in 2015 on its interpretation of these guardrails.

In 2018, the Trump administration replaced that guidance and adopted its own interpretation, which manyargued was inconsistent with Section 1332. The 2018 guidance tried to pave the way for the Trump administration to approve waivers where only some coverage under the waiver (instead of all coverage) satisfied the comprehensiveness and affordability guardrails. Under this view, waivers could be approved even if only some coverage under the waiver was as comprehensive, as affordable, and as available as coverage provided under the ACA. The 2018 guidance would also allow waivers to expand access to plans that do not have to meet the ACA’s requirements. (Separately, the Trump administration issued a final rule to codify the 2018 guidance’s interpretations into regulations.)

The lawsuit argues that the Georgia Access Model violates all four statutory guardrails because it will “drastically underperform the ACA.” The waiver proposal could lead to net enrollment losses in Georgia, which violates the coverage guardrail. The waiver could lead some consumers to enroll in non-ACA plans (such as short-term plans) with benefit gaps, which violates the comprehensiveness guardrail. And consumers will have to pay higher premiums and out-of-pocket costs through higher broker commissions, reduced competition, and adverse selection against the ACA markets, which violates the affordability guardrail and potentially the deficit neutrality guardrail (since higher ACA premiums mean higher federal outlays in the form of premium tax credits).

As health care providers in Georgia, Planned Parenthood Southeast and the Feminist Women’s Health Center allege they will be harmed for several reasons. They argue that the Georgia Access Model will make it more difficult and expensive for their patients to obtain health insurance. Fewer patients with health insurance will result in higher levels of uncompensated care. More uncompensated care will strain the plaintiffs’ resources and limit other services, such as community outreach. The loss of coverage resulting from the waiver will leave their patients in worse health and develop more complex treatment needs, making it more expensive for plaintiffs to treat those patients as a result. And approval of the waiver will make it more complicated for the plaintiffs to assist their patients with enrollment.

What Happens Next

The lawsuit was assigned to Judge James E. Boasberg of the federal district court for DC. Health policy watchers know Judge Boasberg as the judge who repeatedly invalidated the Trump administration’s approval of state Section 1115 waivers with work and community engagement requirements. He is thus no stranger to assessing the legality of waiver approvals under the APA and other federal statutes.

The lawsuit will proceed, and the Biden administration will be responsible for filing a response in court. One potential option could be for the Biden administration to ask the court for a stay while it revisits the approved waiver and perhaps holds another round of public comment on the most recent version of the waiver (which, as the lawsuit points out, was never submitted for public comment). The Biden administration could consider any new comments in reevaluating approval of the Georgia Access Model.

If the federal government newly concludes that the proposal fails to satisfy the substantive guardrails, it could have grounds to amend, suspend, or terminate Georgia’s waiver, so long as certain procedures are followed. This is because the terms and conditions of the waiver agreement between the federal government and Georgia (as well as implementing regulations) always give the federal government “the right to suspend or terminate a waiver, in whole or in part, any time before the date of expiration, if the Secretaries determine that the state materially failed to comply with the terms” of the waiver.

Georgia’s waiver agreement includes some unique terms and conditions relative to waivers in other states. Those terms seem designed to limit the federal government’s ability to suspend or terminate Georgia’s waiver. But the federal government can do so as long as it complies with relevant procedures. This includes notifying Georgia of its determination, providing an effective date, and citing reasons for the amendment or termination (i.e., why the Georgia Access Model fails to satisfy Section 1332’s substantive guardrails). Georgia would have 90 days to respond, with the possibility of providing a corrective action plan to come into compliance with the waiver conditions. Georgia must also be given an opportunity to be heard and challenge the suspension or termination.

Alternatively, the Biden administration could regularly assess and monitor the state’s compliance with the terms and conditions and its progress, or lack thereof, in implementing the Georgia Access Model. Federal officials do this with all waivers. Under the waiver approval, Georgia must, for instance, satisfy requirements related to funding, reporting and evaluation, development of an outreach and communications plan, and operational standards for eligibility determinations. If Georgia fails to comply with these terms and conditions, that too would be grounds to initiate the process to amend or terminate parts or all of Georgia’s waiver.

Coverage Provisions In Biden’s American Rescue Plan

On January 14, a few days before taking office, President Biden issued a 19-page fact sheet outlining his proposed American Rescue Plan to contain the COVID-19 virus and stabilize the economy. The announcement praised the bipartisan package adopted in December 2020 as “a step in the right direction” but notes that Congress did not go far enough to fully address the pandemic and economic fallout. Following Inauguration Day, Biden is expected to lay out an additional economic recovery plan.

Among many other initiatives, the comprehensive $1.9 trillion plan would provide funding for a national vaccination program, create a new public health jobs program, provide funding for schools to reopen safely, extend and expand emergency paid leave, extend and expand unemployment benefits, raise the minimum wage, and deliver $1,400 in support for people across the country. The Biden plan also calls for preserving and expanding health insurance, noting that 30 million people were uninsured even before the pandemic and that millions may have lost job-based coverage in 2020.

First, the American Rescue Plan calls for Congress to provide COBRA subsidies through the end of September. Presumably, these subsidies would be available from the beginning of 2021, rather than subsidizing premiums from 2020. COBRA subsidies during an economic emergency are not new. Congress subsidized COBRA premiums during the 2008 recession, with mixed results. Full COBRA subsidies were included in the original Heroes Act passed by the U.S. House of Representatives in May 2020, although not in the revised Heroes Act that was passed by the House in October 2020. But neither bill was ever taken up by the U.S. Senate. It is not clear from the fact sheet whether the Biden administration is aiming for full COBRA subsidies where the government would pay 100 percent of the premiums for COBRA coverage for laid-off workers and furloughed employees—or some other amount (e.g., 80 percent of premiums).

Second, the American Rescue Plan would accomplish one of candidate Biden’s key campaign promises by expanding and increasing the value of premium tax credits under the ACA. Democrats in Congress have repeatedly passed legislation that would accomplish what the American Rescue Plan fact sheet seems to call for. For instance, the Patient Protection and Affordable Care Enhancement Act—passed by the House in July 2020—would have expanded the availability of premium tax credits to those whose income is above 400 percent of the federal poverty level and made those credits more generous by reducing the level of income that an individual must contribute towards their health insurance premiums to 8.5 percent for those with the highest incomes. This subsidy expansion and enhancement would improve the affordability of coverage for millions of Americans who purchase coverage in the individual market.

Beyond COBRA and ACA subsidies, the American Rescue Plan calls for additional funding for veterans’ health care needs and for the Substance Abuse and Mental Health Services Administration and the Health Resources and Services Administration to expand access to behavioral health services. The proposal would also increase the federal Medicaid assistance percentage (FMAP) to 100 percent for the administration of COVID-19 vaccines to help ensure that all Medicaid enrollees will be vaccinated. The proposal does not appear to otherwise mention Medicaid, which is serving as a key safety net as incomes have dropped for millions of Americans, despite bipartisan support for an enhanced FMAP during the pandemic.

Consumers choosing insurance via the federal Affordable Care Act exchanges reached 8.25 million over the 2021 open enrollment period, about the same number as the year before, CMS said Wednesday.

Because two fewer states are participating in the federal marketplace this year, adjusted year-over-year growth in plan selections was 7%, the agency said.

Of the total, 23% of consumers were new, down by 3.6%. Renewing consumers who actively chose a new plan and those who were automatically re-enrolled both increased.

Dive Insight:

The figures are the last from the Trump administration, which has drastically reduced money toward navigators who help people use the Healthcare.gov website and find the best ACA plan for them. The administration has made no secret of its opposition to the law and after failing to overturn it in Congress has used executive actions to undermine it.

President-Elect Joe Biden and his pick for HHS chief, California Attorney General Xavier Becerra, however, are eager supporters and are likely to take a number of actions to restore and burnish it. That could be increasing tax credits and subsidies, increasing navigator funding and building on protections like essential health benefits.

The U.S. Supreme Court is expected to make its ruling on the ACA case later this spring or summer, but the Biden administration could essentially make it moot by walking back the zeroing out of the individual mandate penalty that is the linchpin of the lawsuit against it.

The relatively steady enrollment could be increased through those actions and the possibility of a special enrollment period to account for needs during the coronavirus pandemic. The COVID-19 crisis and the recession it has caused have kicked millions of people off their employer-sponsored insurance, and they could turn to the exchanges for coverage, especially with higher tax credits and subsidies.

/cdn.vox-cdn.com/uploads/chorus_asset/file/18046968/web_1863137.jpg)