Last week, California’s legislature passed a bill establishing the Distressed Hospital Loan Program, which will dole out $150M in interest-free emergency loans to struggling nonprofit hospitals in the state which meet specific eligibility criteria, including operating in an underserved area and serving a large share of Medicaid beneficiaries. A combination of state agencies will establish a specific methodology for selection, but hospitals that are part of a health system with more than two separately licensed hospital facilities will be ineligible.

Hospitals receiving loans must provide a plan for how they will use the loans to achieve financial sustainability, and must pay back the money within six years.

The Gist: With twenty percent of the state’s hospitals at risk of shuttering, California lawmakers are hoping to provide the most vulnerable hospitals an alternative to either closure or consolidation, an example other states may follow. But unlike the Paycheck Protection Program loans that shored up businesses through the pandemic’s initial disruption, the outlook for small, struggling, independent hospitals isn’t expected to improve in coming years, even if the economy recovers.

Whether these loans provide lifelines or merely serve as Band-Aids on an untenable situation will depend on whether recipient hospitals can use them to restructure their operating models to absorb increased labor costs amid stagnating volumes and commercial reimbursement.

If these loans aren’t used for transformation, they will only delay the inevitable: more closures, and more mergers to find shelter in scale.

The healthcare financings that came in the past couple of weeks generally did well. Maturities seemed to do better than put bonds, and it remains important to pay attention to couponing and how best to navigate a challenging yield curve. But these are episodic indicators rather than trends, given that the scale of issuance remains muted. Other capital markets—like real estate—are becoming more active and offer competitive funding and different credit considerations relative to debt market options. Credit management continues to be the main driver of low external capital formation, but those looking for outside funding should spend time up front considering the full array of channels and structures.

This Part of the Crisis

And now it’s official. After JPMorgan acquired First Republic Bank—with a whole lot of help from the Federal Deposit Insurance Corporation—CEO Jamie Dimon declared, “this part of the crisis is over.” Not sure regional bank shareholders would agree, but from Mr. Dimon’s perspective the biggest bank got bigger, which made it a good day.

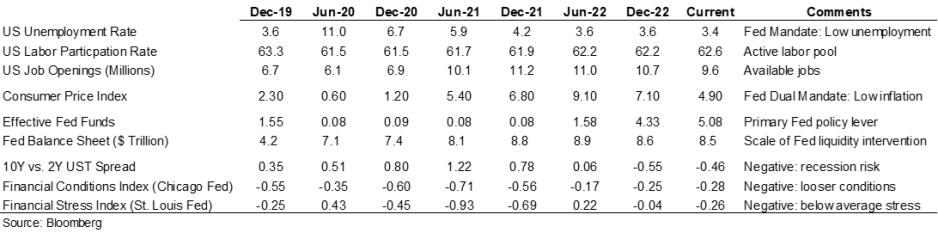

Last week the Federal Reserve raised rates another 25 basis points and the expectation (hope) seems to be that the Fed has reached the peak of its tightening cycle or will at least pause to see if constrictive forces like higher rates and regional bank balance sheet deflation slow activity enough to bring inflation back to the 2.0% Fed target. Assuming this is a pause point, it makes sense to check in on a few economic and market indicators.

Inflation is improving, although it remains well above the Fed’s 2.0% target range, and there are other indicators (like labor participation and unemployment) that have recovered some of the ground lost in 2020. But the weird part remains that this all seems quite civilized. To some, the Treasury curve spread continues to suggest a recession is looming, but in my neighborhood workers are still in short supply, restaurants are busy, and contractors are booked well into the future. Today’s ~3.36% 10-year Treasury rate is less than 100 basis points higher than the average since the start of the Fed interventionist era in 2008 and a whopping 257 basis points lower than the average since 1965. Think about how much capital has been raised in market environments much worse than now (including most of the modern-day healthcare inpatient infrastructure). Again, the main culprit in retarded capital formation is institutional credit management concerns rather than the funding environment.

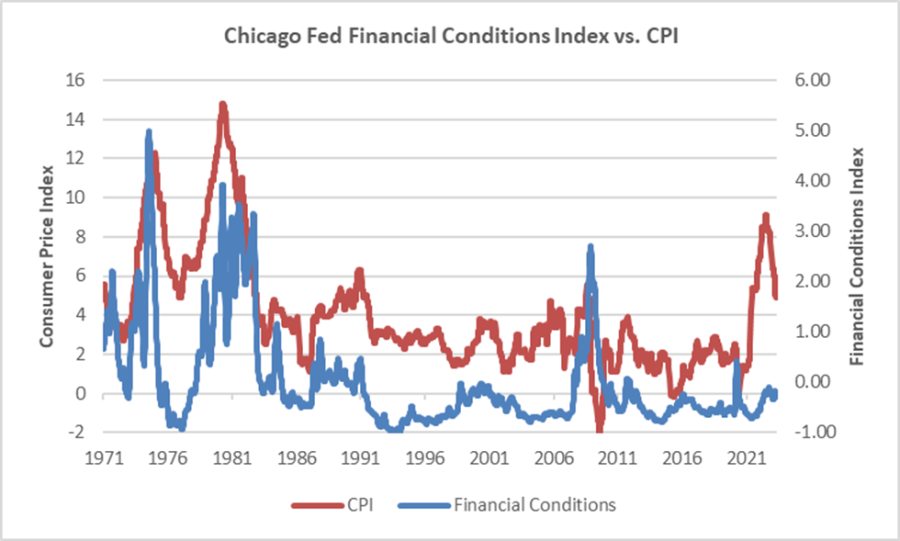

The major fallout from the Fed’s recent anti-inflation efforts seems concentrated with financial intermediaries rather than consumers (or workers), and the financial intermediary stress the Fed is relying on to help curb economic activity is grounded in their own balance sheet management decisions rather than deteriorating loan portfolios. We’ve looked at this before, but it bears repeating that in the “great inflation” of the 1970s, the Chicago Fed’s Financial Conditions Index reached its highest recorded points (higher means tighter than average conditions) and in this most recent inflationary cycle, that same index has remained consistently accommodative. Can you wring inflation out of a system while retaining relatively accommodative financial conditions? Which begs the question of whether any Fed pause is more about shifting priorities: downgrading the inflation fight in favor of moderating the financial intermediary threat? We might be living a remake of the 1970s version of stubborn inflation, which means that all the attendant issues—rolling volatility across operations, financing, and investing—might be sticking around as well.

Meanwhile, somewhere out in the Atlantic the debt ceiling storm is forming. Who knows whether it will make landfall as a storm or a hurricane, but it does remind us that the operative portion of the Jamie Dimon quote noted above is this part of the crisis is over. The next part of the long saga that is about us climbing out of a deep fiscal and monetary hole will roll in and new variations of the same central challenge will emerge for healthcare leaders.

A Healthcare Makeover

Ken Kaufman has been advancing the idea that healthcare needs a “makeover” to align with post-COVID realities. Look for a piece from him on this soon, but the thesis is that reverting to a 2019 world isn’t going to happen, which means that restructuring is the only option. The most recent National Hospital Flash Report suggests improving margins, but they remain well below historical norms and the labor part of the expense equation is structurally higher. Where we are is not sustainable and waiting for a reversion is a rapidly decaying option.

My contribution to Ken’s argument is to reemphasize that balance sheet is the essential (only) bridge between here and a restructured sector and the journey is going to require very careful planning about how to size, position, and deploy liquidity, leverage, and investments. Of course, the central focus will be on how to reposition operations. But if organic cash generation remains anemic, the gap will be filled by either weakening the balance sheet (drawing down reserves, adding leverage, or adopting more aggressive asset allocation) or by partnering with organizations that have the necessary resources.

Organizations reach the point of greatest enterprise risk when the scale of operating challenges outstrips the scale of balance sheet resources. Missteps are manageable when the imbalance is the product of rapid growth but not when it is the result of deflating resources. If the core imperative is to remake operations, the co-equal imperative is continuously repositioning the balance sheet to carry you from here to whatever defines success.

Sacramento, Calif.-based Sutter Health reported $88 million in operating income for the first quarter of 2023 on revenues of $3.8 billion.

Such figures compared with $95 million operating income on $3.6 billion of revenues in the same period last year.

The positive first-quarter operating income figure builds on a 2022 operating income of $278 million. Overall income for the first quarter totaled $220 million compared with a $166 million loss in the same period in 2022.

Sutter Health, which is undergoing some executive management changes, employs 51,000 people and operates 282 care facilities.

Here are 24 health systems with strong operational metrics and solid financial positions, according to reports from credit rating agencies Fitch Ratings, Moody’s Investors Service and S&P Global in 2023.

Note: This is not an exhaustive list. Health system names were compiled from credit rating reports.

1. Atrium Health has an ‘AA-‘ and stable outlook with S&P Global. The Charlotte, N.C.-based system’s rating reflects a robust financial profile, growing geographic diversity and expectations that management will continue to deploy capital with discipline.

2. Berkshire Health has an “AA-” rating and stable outlook with Fitch. The Pittsfield, Mass.-based system has a strong financial profile, solid liquidity and modest leverage, according to Fitch.

3. CaroMont Health has an “AA-” rating and stable outlook with S&P Global. The Gastonia, N.C.-based system has a healthy financial profile and robust market share in a competitive region.

4. CentraCare has an “AA-” rating and stable outlook with Fitch. The St. Cloud, Minn.-based system has a leading market position, and its management’s focus on addressing workforce pressures, patient access and capacity constraints will improve operating margins over the medium term, Fitch said.

5. Children’s Minnesota has an “AA” rating and stable outlook with Fitch. The Minneapolis-based system’s broad reach within the region continues to support long-term sustainability as a market leader and preferred provider for children’s health care, Fitch said.

6. Cone Health has an “AA” rating and stable outlook with Fitch. The rating reflects the expectation that the Greensboro, N.C.-based system will gradually return to stronger results in the medium term, the rating agency said.

7. El Camino Health has an “AA-” rating and stable outlook with Fitch. The Mountain View, Calif.-based system has a history of generating double-digit operating EBITDA margins, driven by a solid market position that features strong demographics and a very healthy payer mix, Fitch said.

8. Harris Health System has an “AA” rating and stable outlook with Fitch. The Houston-based system has a “very strong” revenue defensibility, primarily based on the district’s significant taxing margin that provides support for operations and debt service, Fitch said.

9. Hoag Memorial Hospital Presbyterian has an “AA” rating and stable outlook with Fitch. The Newport Beach, Calif.-based system’s rating is supported by a leading market position in its immediate area and very strong financial profile, Fitch said.

10. Inspira Health has an “AA-” rating and stable outlook with Fitch. The Mullica Hill, N.J.-based system’s rating reflects its leading market position in a stable service area and a large medical staff supported by a growing residency program, Fitch said.

11. Mayo Clinic has an “Aa2” rating and stable outlook with Moody’s. The Rochester, Minn.-based system’s credit profile characterized by its excellent reputations for clinical services, research and education, Moody’s said.

12. McLaren Health Care has an “AA-” rating and stable outlook with Fitch. The Grand Blanc, Mich.-based system has a leading market position over a broad service area covering much of Michigan and a track-record of profitability despite sector-wide market challenges in recent years, Fitch said.

13. Novant Health has an “AA-” rating and stable outlook with Fitch. The Winston-Salem, N.C.-based system has a highly competitive market share in three separate North Carolina markets, Fitch said, including a leading position in Winston-Salem (46.8 percent) and second only to Atrium Health in the Charlotte area.

14. NYC Health + Hospitals has an “AA-” rating with Fitch. The New York City system is the largest municipal health system in the country, serving more than 1 million New Yorkers annually in more than 70 patient locations across the city, including 11 hospitals, and employs more than 43,000 people.

15. Orlando (Fla.) Health has an “AA-” and stable outlook with Fitch. The system’s upgrade from “A+” reflects the continued strength of the health system’s operating performance, growth in unrestricted liquidity and excellent market position in a demographically favorable market, Fitch said.

16. Rush System for Health has an “AA-” and stable outlook with Fitch. The Chicago-based system has a strong financial profile despite ongoing labor issues and inflationary pressures, Fitch said.

17. Saint Francis Healthcare System has an “AA” rating and stable outlook with Fitch. The Cape Girardeau, Mo.-based system enjoys robust operational performance and a strong local market share as well as manageable capital plans, Fitch said.

18. Salem (Ore.) Health has an “AA-” rating and stable outlook with Fitch. The system has a “very strong” financial profile and a leading market share position, Fitch said.

19. Stanford Health Care has an “AA” rating and stable outlook with Fitch. The Palo Alto, Calif.-based system’s rating is supported by its extensive clinical reach in the greater San Francisco and Central Valley regions and nationwide/worldwide destination position for extremely high-acuity services, Fitch said.

20. SSM Health has an “AA-” rating and stable outlook with Fitch. The St. Louis-based system has a strong financial profile, multi-state presence and scale, with solid revenue diversity, Fitch said.

21. UCHealth has an “AA” rating and stable outlook with Fitch. The Aurora, Colo.-based system’s margins are expected to remain robust, and the operating risk assessment remains strong, Fitch said.

22. University of Kansas Health System has an “AA-” rating and stable outlook with S&P Global. The Kansas City-based system has a solid market presence, good financial profile and solid management team, though some balance sheet figures remain relatively weak to peers, the rating agency said.

23. WellSpan Health has an “Aa3” rating and stable outlook with Moody’s. The York, Pa.-based system has a distinctly leading market position across several contiguous counties in central Pennsylvania, and management’s financial stewardship and savings initiatives will continue to support sound operating cash flow margins when compared to peers, Moody’s said.

24. Willis-Knighton Health System has an “AA-” rating and stable outlook with Fitch. The Shreveport, La.-based system has a “dominant inpatient market position” and is well positioned to manage operating pressures, Fitch said.

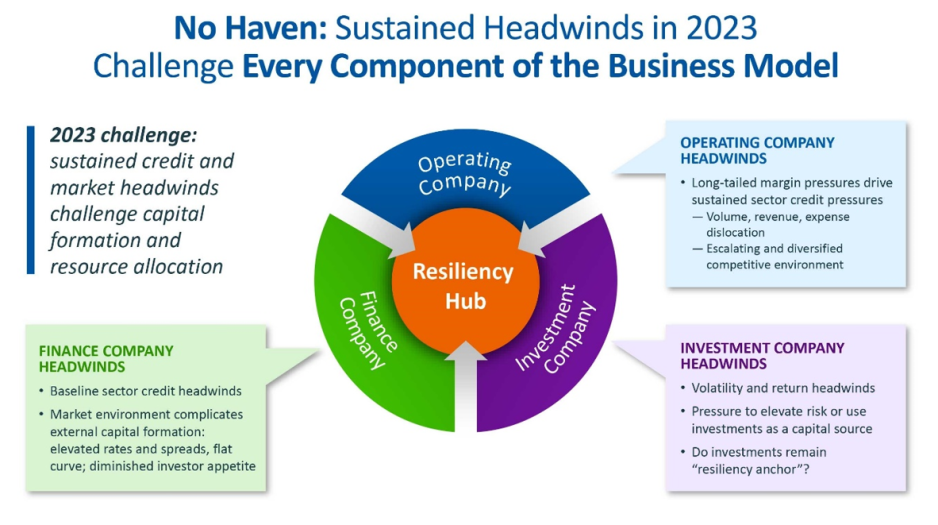

For the first time in recent history, we saw all three functions of the not-for-profit healthcare system’s financial structure suffer significant and sustained dislocation over the course of the year 2022 (Figure above).

The headwinds disrupting these functions are carrying over into 2023, and it is uncertain how long they will continue to erode the operating and financial performance of not-for-profit hospitals and health systems.

The Operating Function is challenged by elevated expenses, uncertain recovery of service volumes, and an escalating and diversified competitive environment.

The Finance Function is challenged by a more difficult credit environment (all three rating agencies

now have a negative perspective on the not-forprofit healthcare sector), rising rates for debt, and a diminished investor appetite for new healthcare debt issuance. Total healthcare debt issuance in 2022 was $28 billion, down sharply from a trailing two-year average of $46 billion.

The Investment Function is challenged by volatility and heightened risk in markets concerned with the Federal Reserve’s tightening of monetary policy and the prospect of a recession. The S&P 500—a major stock index—was down almost 20% in 2022. Investments had served as a “resiliency anchor” during the first two years of the pandemic; their ability to continue to serve that function is now in question.

A significant factor in Operating Function challenges is labor: both increases in the cost of labor and staffing shortages that are forcing many organizations to run at less than full capacity. In Kaufman Hall’s 2022 State of Healthcare Performance Improvement Survey, for example, 67% of respondents had seen year-over-year increases of more than 10% for clinical staff wages, and 66% reported that they had run their facilities at less-than-full capacity because of staffing shortages.

These are long-term challenges,

dependent in part on increasing the pipeline of new talent entering healthcare professions, and they will not be quickly resolved. Recovery of returns from the Investment Function is similarly uncertain. Ideally, not-for-profit health systems can maintain a one-way flow of funds into the Investment Function, continuing to build the basis that generates returns. Organizations must now contemplate flows in the other direction to access

funds needed to cover operating losses, which in many cases would involve selling invested assets at a loss in a down market and reducing the basis available to generate returns when markets recover.

The current situation demonstrates why financial reserves are so important:

many not-for-profit hospitals and health systems will have to rely on them to cover losses until they can reach a point where operations and markets have stabilized, or they have been able to adjust their business to a new, lower margin environment. As noted above, relief funding and the MAAP program helped bolster financial reserves after the initial shock of the pandemic. As the impact of relief funding wanes and organizations repay remaining balances under the MAAP program, Days Cash on Hand has begun to shrink, and the need to cover operating losses is hastening this decline. From its highest

point in 2021, Days Cash on Hand had decreased, as of September 2022, by:

29% at the 75th percentile, declining from 302 to 216 DCOH (a drop of 86 days)

28% at the 50th percentile, declining from 202 to 147 DCOH (a drop of 55 days)

49% at the 25th percentile, declining from 67 to 34 DCOH (a drop of 33 days)

Financial reserves are playing the role for which they were intended; the only question is whether enough not-for-profit hospitals and health systems have built sufficient reserves to carry them through what is likely to be a protracted period of recovery from the pandemic.

KEY TAKEAWAYS

All three functions of the not-for-profit healthcare system’s financial structure—operations, finance, and investments—suffered significant and sustained dislocation over the course of 2022.

These headwinds will continue to challenge not-forprofit

hospitals and health systems well into 2023.

Days Cash on Hand is showing a steady decline, as the impact of relief funding recedes and the need to cover operating losses persists.

Financial reserves are playing a critical role in covering operating losses as hospitals and health systems struggle to stabilize their operational and financial performance.

Conclusion

Not-for-profit hospitals and health systems serve many community needs. They provide patients access to healthcare when and where they need it. They invest in new technologies and treatments that offer patients and their families lifesaving advances in care. They offer career opportunities to a broad range of highly skilled professionals, supporting the economic health of the communities they serve.

These services and investments are expensive and cannot be covered solely by the revenue received from providing care to patients.

Strong financial reserves are the foundation of good financial stewardship for not-for-profit hospitals and health systems.

Financial reserves help fund needed investments in facilities and technology, improve an organization’s debt capacity, enable better access to capital at more affordable interest rates, and provide a critical resource to meet expenses when organizations need to bridge periods of operational disruption or financial distress. Many hospitals and health systems today are relying on the strength of their reserves to navigate a difficult

environment; without these reserves, they would not be able to meet their expenses and would be at risk of closure.

Financial reserves, in other words, are serving the very purpose for which they are intended—ensuring that hospitals and health systems can continue to serve their communities in the face of challenging operational and financial headwinds.

When these headwinds have subsided, rebuilding these reserves should be a top priority to ensure that our not-for-profit hospitals and health systems can remain a vital resource for the communities they serve.

Not-for-profit hospitals and health systems rely on three interdependent functions to contribute to the financial resilience of the organization: namely, the ability to withstand adverse changes to these core functions and continue to provide services to the community (Figure above).

The Operating Function:

The Operating Function manages the portfolio of clinical services and strategic initiatives that define the charitable mission of the organization. Clinical services generate patient revenue, and if that revenue creates a positive margin (i.e., exceeds expenses), that excess is invested back into the health system. Operating margins are, on average, very low in not-for-profit healthcare. For example, for the not-for-profit hospitals and health systems rated by Moody’s Investors Service, median operating margins from 2017–2021 ranged between 2.1% and 2.9%. These rated organizations represent only a few hundred of the thousands of hospitals and health systems in the country and are among the most financially healthy. A 2018 study of a wider group of more than 2,800 hospitals found an average clinical operating margin of -2.7%.

The Finance Function:

Because the positive margins generated by the Operating Function are rarely enough to support the intensive capital needs of maintaining and improving acute-care facilities, care delivery models, and technology, not-for-profit health systems rely on the Finance Function for internal and external capital formation. The Finance Function builds cash reserves and secures external financing

(e.g., bond proceeds, bank lines of credit) to support the capital spending needs of the organization. The cash reserves maintained by the Finance Function also help the organization meet daily expenses at times when expenses exceed revenues.

The Investment Function:

Not-for-profit hospitals and health systems will also endeavor to invest some of their cash reserves to generate returns that, first, act as an additional hedge against potential risks that could disrupt operations or cash flow, and second, pursue independent returns. Any independent returns generated serve as an important supplement to revenues generated through the Operating Function.

The three functions described above are common to all not-for-profit organizations. The main differences are mostly within the Operating Function. In higher education, for example, tuition revenue takes the place of clinical revenue. While higher education also maintains enterprise risk, the Operating Function for colleges and universities is less vulnerable to volume swings as enrollment is typically steady and predictable. Likewise, higher education is less labor intensive than healthcare.

Financial reserves include all liquid cash resources and unrestricted investments held in the Finance and Investment Functions. These reserves are equivalent to the emergency funds individuals are encouraged to maintain to help them meet living expenses for six to twelve months in case of a job loss or other disruption to income.

Absolute reserve levels are important, as discussed above, but they must also be viewed relative to a hospital’s daily operating expenses. A common

metric used to describe these reserves is Days Cash on Hand. If an organization has 250 Days Cash on Hand, that means that it would be able to meet its operating expenses for 250 days if revenue was suddenly shut off. The size of Days Cash on Hand will be proportionate to the size of the hospital and health system. Some of the largest not-for-profit health systems have annual operating expenses approaching $30 billion annually: meeting those expenses for 250 days would require Days Cash on Hand of more than $20 billion.

The shutdown that occurred in the early days of the pandemic (March through May 2020) is an example of a time when cash flow nearly shut off for most hospitals (except for emergency care). Reserves, measured in absolute and relative terms such as Days Cash on Hand, allowed hospitals that were nearly empty to maintain staffing and operations throughout the period. Other hospitals that were inundated with patients during the initial surge were able to fund increased staffing and personal protective equipment costs through their reserves. Other examples of how reserves provide a buffer

against unexpected events include natural disasters such as hurricanes, tornadoes, deep freezes, and wildfires, which can require the temporary shutdown of operations; cyberattacks, which can halt a hospital’s ability to provide services; a defunct payer that is unable to reimburse hospitals for care already provided; or an escalation in labor costs as experienced by many during 2022.

Without the reserves to pay for contract labor or premium pay, many hospitals would have undoubtedly had to close or limit services to their community.

KEY TAKEAWAYS

Financial reserves are created through the interdependent relationship of operating, finance, and investment functions in not-for-profit health systems.

These reserves build financial resilience: the ability to withstand adverse changes to core functions and continue to provide services to the community.

Financial reserves play an important role in supplementing any shortfalls in revenue or capital formation in one or more of these three functions.

Financial reserves are equivalent to individual emergency funds—both are intended to cover expenses if income or revenue flows are significantly disrupted.

A common metric used to describe financial reserves is Days Cash on Hand: an organization’s combined liquid, unrestricted cash resources and investments, measured by how many days these reserves could cover operating expenses if cash flows were suddenly shut off.

Financial reserves, measured in absolute and relative terms such as Days Cash on Hand, allowed hospitals that were nearly empty during the early days of the pandemic to maintain staffing and operations throughout the period. Other hospitals that were inundated with patients during the initial surge were able to fund increased staffing and personal protective equipment costs through their reserves.

A Comparison: Financial Reserves and Higher Education Not-for-Profits

Not-for-profit hospitals and health systems are not alone in their reliance on financial reserves; most not-for-profit organizations carry reserves that enable them to maintain operations and make needed investments even in times of weaker operating performance. Higher education is probably most comparable to healthcare, with significant overlaps between the two sectors. Moody’s Investors Service, one of the three major rating agencies, notes that 16% of its rated higher education institutions have affiliated academic medical centers (AMCs), and revenue from patient care at these AMCs contributes to 28% of the overall revenues for the higher education sector.

The magnitude of Days Cash on Hand levels varies by industry; financial reserves maintained by private not-for-profit higher education

institutions, for example, are significantly greater than those maintained by not-for-profit hospitals and health systems. For comprehensive private universities across all rating categories, Moody’s reports median Days Cash on Hand in 2021 of 498 days for assets that could be liquidated within a year. This compares with a median 265 Days Cash on Hand in 2021 across all freestanding hospitals, single-state, and multi-state healthcare systems rated by Moody’s.

Financial reserves are a critical measure of financial health across both healthcare and higher education. They help ensure that not-for-profit colleges, universities, hospitals, and health systems can continue to fulfill their vital societal functions when operations are disrupted, or when they are experiencing a period of sustained financial distress.

Here is a summary of recent credit downgrades and outlook revisions for hospitals and health systems going back to the most recent major roundup March 16.

The various downgrades reflect continued operating challenges many nonprofit systems are facing and will likely continue to deal with for some years to come. The most recent downgrades and revisions, which have not been included in any more recent roundups, are listed first.

Baptist Health Care (Pensacola, Fla.):

BHC had the rating downgraded on a series of its bonds as a reflection of “pressured operating performance and cash flow,” S&P Global said April 19.

As well as typical industry pressures of inflation and labor expenses, the three-hospital system may face further challenge because of a replacement project for its flagship Baptist Hospital that is due to be completed in late 2023.

Beacon Health (South Bend, Ind.):

Beacon Health System had its outlook revised to negative from stable on “AA-” rated bonds it holds, S&P Global said April 14.

The move reflects weaker operating results and an expectation of increased debt over the near term.

Kuakini Health System (Honolulu):

Kuakini Health System, which has a “CCC” long-term rating, has been placed on CreditWatch with negative implications, S&P Global said April 14.

The move reflects the system’s sustained operating challenges with no foreseeable major changes and questions about its long-term viability, the agency said, describing the system’s “precarious financial position.”

Baystate Health (Springfield, Mass.):

Baystate Health had ratings downgraded on specific bonds related to its flagship medical center, S&P Global said April 12.

While ratings were affirmed on other debt, those on others specific to the 780-bed Baystate Medical Center were downgraded to “A” from “A+” as the system’s operating challenges continue into 2023, the agency said.

Penn State Health (Hershey, Pa.):

Higher-than-expected operating losses have led to Penn State Health being downgraded on a series of bonds from “A+” to “A,” S&P Global said April 6.

Original budgets for the first part of fiscal 2023 targeted a slightly positive full-year operating margin, but data shows a $75 million lower-than-forecasted figure, S&P Global said. Operating income showed a loss of $154.5 million for the six months ending Dec. 31 compared with a $48.8 million loss in all of fiscal 2022.

Legacy Health(Portland, Ore.):

Legacy Health had its outlook revised to negative from stable amid expectations the eight-hospital system will continue to experience difficult operating conditions and concern it will continue to fail to meet debt obligations, Moody’s said April 5.

The rating on its revenue bonds was affirmed at “A1.” Total debt stands at $738 million.

Providence (Renton, Wash.):

The 51-hospital system recorded the first of three downgrades in the space of a few weeks March 17 when Fitch Ratings attached an “A” grade to both the system’s default rating and a series of bonds worth approximately $7.4 billion. The outlook for the system is negative due to its higher-than-average debt loads, Fitch said.

S&P Global then downgraded Providence to the same notch from “A+” March 21 amid higher expenses and an expectation of only a multiyear process of recovery. The outlook for the system was also negative given the steep operating losses that need to be dealt with, S&P said.

Finally, Providence was downgraded by Moody’s on a series of bonds from “A1” to “A2.

Thomas Jefferson (Philadelphia):

Thomas Jefferson University has undergone a credit downgrade with cash flow margins expected to stay low for “several years,” Moody’s said March 30.

The 18-hospital system, which also operates 10 colleges located primarily on two campuses in Philadelphia, is expected to stabilize its days of cash on hand to about 140, but debt will remain high, Moody’s said. The outlook is stable.

Oaklawn Hospital (Marshall, Mich.):

The 68-bed community hospital was downgraded to “BBB-” from “BBB” as it reported operating losses due to higher expenses and length of patient stay, Fitch Ratings said March 29.

The downgrade refers both to its default rating and on bonds worth $63.5 million. The outlook is negative.

DCH Health (Tuscaloosa, Ala.):

The three-hospital system saw its rating on a series of bonds lowered to “A-” from “A” as it continues to suffer operating losses, S&P Global said March 29.

The system’s “deeply negative underlying operations” are unlikely to lead to any substantial improvement in the near future, the agency said.

DCH Health operates a total of 510 staffed beds.

AU Health System (Augusta, Ga.):

The system, which is being pursued by Marietta, Ga.-based Wellstar Health, was downgraded March 23 amid concern over negative cash flow and that it may breach covenant agreements later this year, Moody’s said.

The downgrade to “B2” from “Ba3” applies to revenue bonds the system holds. The outlook is negative.

PeaceHealth (Vancouver, Wash.):

“Considerable operating stress” was the driver behind Fitch Ratings downgrading the 10-hospital system March 21.

The downgrade to “A+” from “AA-” applied to both the system’s default rating and on a series of bonds. The outlook is stable.

Management is targeting a return to profitability by fiscal 2026, Fitch noted.

Mercy Iowa CityHospital:

The hospital, part of Des Moines, Iowa-based MercyOne, was downgraded March 16 to “Caa1” from “B1” because of what Moody’s called “severe cash flow deterioration.” The “Caa1” categorization is seen as “substantial risk.”

According to a new report from the American Hospital Association (AHA), hospitals and health systems are facing significant financial pressures from rising expenses, including for labor, drugs, medical supplies and more. And without increased government support, the organization warns that patients’ access to care could be at risk.

Hospitals continue to see expenses grow, negative margins

In the report, AHA writes that several factors, including historic inflation and critical workforce shortages leading to a reliance on contract labor, led to “2022 being the most financially challenging year for hospitals since the pandemic began.”

According to data from Syntellis Performance Solutions, overall hospital expenses increased by 17.5% between 2019 and 2022 — more than double the increases in Medicare reimbursements during the same time. Between 2019 and 2022, Medicare reimbursement only grew by 7.5%.

With expenses significantly outpacing reimbursement, hospital margins have been consistently negative over the last year. In fact, AHA noted that “over half of hospitals ended 2022 operating at a financial loss — an unsustainable situation for any organization in any sector, let alone hospitals.”

So far, this trend has continued into 2023, with hospitals reporting negative median operating margins in both January and February.

A recent analysis also found that the first quarter of 2023 had the largest number of bond defaults among hospitals in over 10 years.

Between 2019, and 2022 hospital labor expenses increased by 20.8%, a rise that was largely driven by a growing reliance on contract labor to fill in workforce gaps during the pandemic. Even after accounting for an increase in patient acuity, labor expenses per patient increased by 24.7%.

Compared to pre-pandemic levels, hospitals saw a 56.8% increase in the rates they were charged for contract employees in 2022. Overall, hospitals’ contract labor expenses increased by a “staggering” 257.9% in 2022 compared to 2019 levels.

A sharp rise in inflation in recent months has also led to a significant increase in hospitals’ non-labor expenses, particularly for drugs and medical expenses. According to a report by Kaufman Hall, just non-labor expenses would lead to a $49 billion one-year expense increase for hospitals and health systems.

Since 2019, non-labor expenses have grown 16.6% per patient. Hospitals’ expenses for drugs and medical supplies/equipment have seen similar increases per patient at 19.7% and 18.5%, respectively. Costs of laboratory services (27.1%), emergency services (31.9%), and purchased services, including IT and food and nutrition services, (18%) have also increased significantly per patient.

Outside of labor and non-labor expenses, AHA writes that policies from health insurers have also contributed to significant burden among hospital staff and increased administrative costs. Currently, administrative costs account for up to 31% of total healthcare spending — of which, billing and insurance makes up 82%.

With the COVID-19 public health emergency ending on May 11, several important hospital waivers and flexibilities will soon end, and “[t]he downstream effects of this will be wide-ranging as hospitals will be faced with a set of additional challenges,” AHA writes.

“Rising costs for drugs, supplies, and labor coupled with sicker patients, longer hospital stays, and government reimbursement rates that do not come close to covering the costs of caring for patients have created a dire situation for hospitals and health systems,” said AHA president and CEO Rick Pollack.

“This is not just a financial problem; it is an access problem.

When healthcare providers cannot afford the tools and teams they need to care for patients, they will be forced to make hard choices and the people who will be impacted the most are patients. We can’t let that happen. Congress and others must act to preserve the care our nation needs and depend on.”

To address these financial challenges and ensure that hospitals are able to continue caring for patients, AHA has suggested several actions Congress could take to support hospitals going forward, including:

Enacting policies to support efforts to boost the healthcare workforce and ensure of future pipeline of professionals to combat longstanding labor shortages

Rejecting attempts to cut Medicare or Medicaid payments to hospitals, which could further reduce patients’ access to care

Encouraging CMS to use its “special exceptions and adjustments” to make retrospective adjustments to account for differences between what was implemented for fiscal year 2022 and what is currently projected

Creating a special statutory designation and providing additional support to hospitals that serve historically marginalized communities

“As the hospital field maintains its commitment to care in the face of significant challenges, policymakers must step up and help protect the health and well-being of our nation by ensuring America has strong hospitals and health systems,” AHA writes.

One of the great things about my job is getting the opportunity to talk with healthcare CEOs around the country on a regular basis.

Lately, every CEO I talk with tells me how hard it is to run a healthcare organization in 2023.

These are people with long experience, people who over time have pushed the right buttons and pulled the right levers to make their organizations successful and to give their communities the care they need.

Hearing these recent comments from CEOs takes us back to the concept of “wicked problems,” which we’ve referred to in the past, and suggests that the current hospital operating environment is overwhelmed by wicked problems.

As a reminder, the wicked problem concept was developed in 1973 by social scientists Horst Rittel and Melvin Webber.

Unlike math problems, wicked problems have no single, correct solution. In fact, a solution that improves one aspect of a wicked problem usually makes another aspect of the problem worse.

Poverty is a common example of a wicked problem.

According to Rittel and Webber, all wicked problems have these five characteristics:

They are hard to define.

It’s hard to know when they are solved.

Potential solutions are not right or wrong, only better or worse.

There is no end to the number of solutions or approaches to a wicked problem.

There is no way to test the solution to a wicked problem—once implemented, solutions are not easily reversable, and those solutions affect many people in profound ways.

Healthcare is one of our nation’s critical wicked problems, and the broad and persistent effects of COVID have made that problem worse.

Like all wicked problems, the wicked problem of healthcare can be defined in many different ways and from many different perspectives.

If we were to frame the wicked problem of healthcare just in the context of hospitals and health systems coming off of their worst financial year in memory, it could look something like this:

Hospitals and health systems need to make a margin in order to carry out their “duty of care”—that is, their responsibility to improve health for communities, which increasingly include public health undertakings.

However, in 2022, more than half of hospitals in America had negative margins due largely to macroeconomic factors related to labor, inflation, utilization, and insufficient revenue growth.

The actions then needed to improve financial performance likely involve reducing labor costs and eliminating unprofitable services.

But these solutions in the hospital world are seen as another wicked problem, and actions taken to improve financial and clinical operations are often cautiously approached in order to protect the organization’s duty of care.

As you can see, the very actions to solve the wicked problem of provider healthcare may likely make aspects of the strategic problem worse.

Everyone reading this blog is dedicated to solving these and other wicked problems related to health and healthcare and the provision of sufficient care to the American community.

Solutions to healthcare’s wicked problems are never clear, and those solutions are not easily tested and eventually can affect many.

And in the wicked problem lexicon, once uncertain solutions have been implemented they are very hard to undo.

And healthcare’s many and varied dissatisfied stakeholders demand rapid solutions and then complain loudly when those solutions fall short, as any one solution inevitably will when the problem is as wicked as the current healthcare environment.

This is the new role of healthcare leaders: solvers of wicked problems.

Using data from Kaufman Hall’s National Hospital Flash Report, as well as publicly available investor reports for some of the nation’s largest nonprofit health systems, the graphic above takes stock of the current state of health system margins.

The median US hospital has now maintained a negative operating margin for a full year. Some good news may be on the horizon, as the picture is slightly less gloomy than a year ago, with year-over-yearrevenues increasing seven points more than total expenses.

However, the external conditions suppressing operating margins aren’t expected to abate, and many large health systems are still struggling.

Among large national non-profits Ascension, CommonSpirit Health, Providence, and Trinity Health, operating income in FY 2022 decreased 180 percent on average, and investment returns fell by 150 percent on average, compared to the year prior.

While health systems’ drop in investment returns mirrors the overall stock market downturn, and is largely comprised of unrealized returns, systems may not be able to rely on investment income to make up for ongoing operating losses.