Manatee Memorial Hospital in Bradenton, Fla., is revising its charity care policies due to funding shortfalls, a move the investor-owned hospital called a “difficult, yet responsible, fiscally prudent decision,” according to a June 3 report by the Sarasota Herald-Tribune.

Part of King of Prussia, Pa.-based Universal Health Services, Manatee Memorial Hospital is a 300-bed facility staffed by over 800 physicians, residents, and allied health professionals.

In May, the hospital informed stakeholders it would no longer accept patients enrolled in Manatee County’s healthcare plan or unfunded referrals from the We Care Manatee nonprofit for uninsured, low-income county residents, effective June 1, the Sarasota Herald-Tribune reported.

Emergency room access will be maintained in compliance with the federal Emergency Medical Treatment and Labor Act.

“Our projected deficit from unfunded care, beyond charity care, amounts to several millions of dollars,” Manatee Memorial wrote in a May letter to stakeholders, as reported by the Sarasota Herald-Tribune. “The significant cost of unreimbursed care is unsustainable. We continue to be a supportive community partner and will maintain open discussions with Manatee County regarding solutions, however, we need to make this difficult, yet responsible, fiscally prudent decision.”

In April, Manatee Memorial Hospital CEO Tom McDougal indicated the hospital’s funding for indigent care services was unsustainable. He noted that the hospital’s costs for charity, indigent and uninsured care rose by 47% over two years, reaching $21.2 million in 2023, with an additional $2.9 million in uncollectable care. Last year, the hospital received $2.7 million in indigent funding from Manatee County.

“Ladies and gentlemen, I simply can’t afford to keep doing this without being compensated for it,” Mr. McDougal said at the April 16 public county commission meeting. “It takes away care from other patients.”

McDougal made his remarks at a commission meeting focused on undocumented immigration, acknowledging that specific figures linking undocumented immigrants to the rise in charity care costs were not available. Six percent of patients in the hospital emergency room self-disclosed their status as undocumented immigrants, which Mr. McDougal believes is an undercount.

The latest changes follow Mr. McDougal’s “very uncomfortable decision,” as he put it, in February to stop oncology services and some surgeries for Manatee County health plan enrollees, as the hospital’s costs under the program reached $9 million in 2023, compared to the $2.7 million reimbursement from the county.

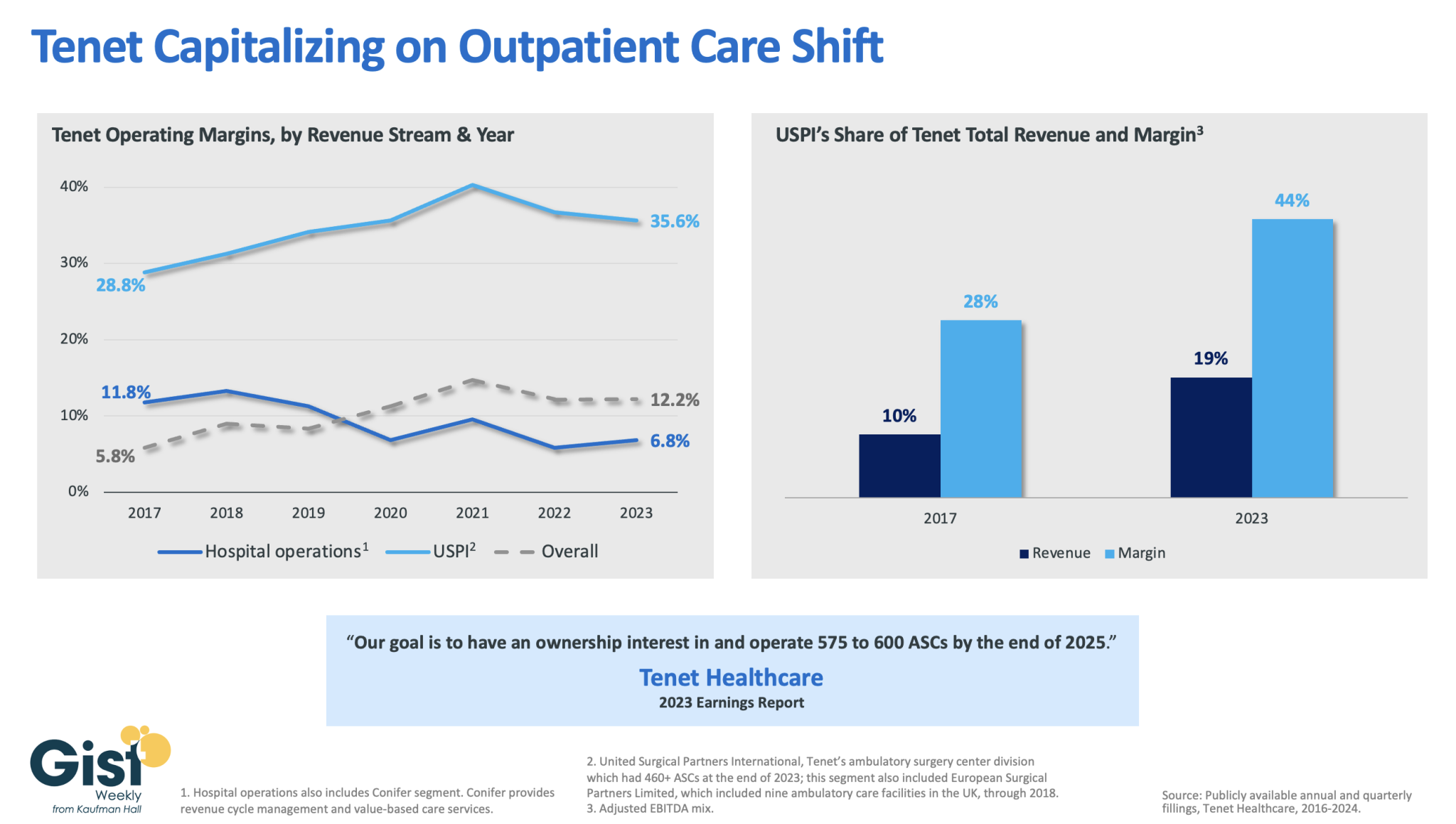

In this week’s graphic, we dive into recently released data on Tenet Healthcare’s 2023 financial performance. While the for-profit healthcare services company’s annual margin on hospital operations has declined since 2017, its overall profitability has more than doubled, thanks to strong performances from its ambulatory surgery center (ASC) chain,

United Surgical Partners International (USPI), which has consistently posted margins above 30 percent. Despite bringing in less than one fifth of Tenet’s total revenue, USPI is now responsible for almost half of Tenet’s overall margin.

Tenet has pursued this growth aggressively since buying USPI in 2015, swelling its ASC footprint from 249 locations in 2015 to more than 460 in 2023, with plans to increase that number to nearly 600 by the end of next year.

Tenet appears to be doubling down on its strategy of pursuing high-margin services over high-revenue services, especially as outpatient volumes are expected to far surpass growth in hospital-based care over the next decade.

In mid-January, General Catalyst (GC) and Summa Health announced the signing of a non-binding LOI for GC to acquire Summa, which, if consummated, would be a groundbreaking transaction. Summa Health is a vertically integrated not-for-profit health system located in Akron, Ohio that operates acute care hospitals, a network of health care services, a physician group practice, and a health plan. Like much of the health system sector, Summa has found the operating environment for the past couple of years to be challenging.

GC is a venture capital firm that had approximately $25B in assets under management at the end of 2022, across a dozen fund families and a number of sectors, including its Health Assurance funds, that have a stated mission of “creating a more proactive, affordable & equitable system of care.”

Health Assurance has investments in more than 150 digital health companies worldwide and has implemented working relationships with more than a dozen of the country’s most noteworthy health systems and hospital operators.

In October, GC announced the formation of a new venture called the Health Assurance Transformation Corporation (HATCo), for the purpose of providing financial and operational advisory assistance to health systems, including using GC’s suite of digital health companies. At that time, HATCo announced plans to buy a health system in order to drive transformation in the delivery of care by leveraging technology, updating workforce/staffing models, and becoming more proactive in creating revenue streams for health systems.

Their plans included an intent to streamline operations and find efficiencies using technology, as well as implementing value-based payment models, including fully capitated risk contracts to incentivize better utilization management, an initiative that requires significant data analytics.

GC had been looking for a system with market relevance and a sweet spot in terms of size – big enough to have a full complement of services, but nimble enough to accept significant change. In Summa, it has also found a system that maintains its own health plan, which GC can use to help accelerate the shift to capitated models.

The transaction that Summa and GC are contemplating is a new and innovative attempt at addressing the underlying problems that plague the acute care industry.

In particular, 1) a continued reliance on fee-for-service revenue when reimbursement has been pressured from every angle and rate increases have failed to keep pace with the rising cost of providing care, 2) capital to fund a growing list of competing needs, and 3) the challenges of staffing for quality in a tight market for clinical labor. Summa appears to be banking on the idea that GC and the data- and technology driven solutions that reside within their portfolio companies can ease those pressures.

HATCo’s proposed purchase of Summa requires a conversion of the health system to for profit. The purchase price of the health system will contribute to the corpus for a large foundation that will address social determinants of health in the Akron community, and the operating entities would become subsidiaries of HATCo.

HATCo has stated publicly that it will continue Summa’s existing charity care commitment, that Summa’s existing management team will stay in place, and the health system Board will continue to have local community representation. HATCo has also emphasized that it plans to hold Summa for an extended period and have it serve as a digital innovation testing ground and incubation site for new healthcare IT, where it believes that aligning incentives will drive financial improvement and better care.

Innovative approaches to meaningful problems should be applauded but there is skepticism.

Will bottom line pressures affect the quality of care?

Will the typical investment horizon of venture capital align with the time frames needed to prove these solutions are taking hold?

Health system evolution has traditionally been measured in decades, rather than the 5-7 year hold periods that private capital prefers. There are also perceived conflicts to consider as Summa will be paying the GC-owned companies for their services. Acute care hospitals are central elements of their communities and their constituents are broader than most companies, often including large workforces, union leadership, politicians, government regulators, and of course patients and their families.

This transaction will receive significant scrutiny with any number of constituents taking issue with a health system’s purchase by a venture capital firm. One hurdle is the conversion process itself, which requires review and approval by the Ohio Attorney General and regulators may want to impose restrictions on GCs ability to operate that are incompatible with its plans. The hurdles to closing are daunting, but the challenges facing health systems are equally daunting.

And while this proposed combination may not come to fruition, the need for innovative solutions remains.

The physician-led healthcare network formed to save hospitals from financial distress. Now, hospitals in its own portfolio need bailing out after years of alleged mismanagement.

Steward Health Care formed over a decade ago when a private equity firm and a CEO looking to disrupt a regional healthcare environment teamed up to save six Boston-based hospitals from the brink of financial collapse. Since that time, Steward has expanded from a handful of facilities to become the largest physician-led for-profit healthcare network in the country, operating 33 community hospitals in eight states, according to its own corporate site.

However, Steward has also found itself once again on the precipice of failure.

Steward’s ongoing issues in Massachusetts have played out in regional media outlets in recent weeks. Massachusetts Gov. Maura Healey warned there would be no bailout for Steward in an interview on WBUR’s Radio Boston.

The Massachusetts Department of Public Health said it is investigating concerns raised about Steward facilities and began conducting daily site inspections at some Steward sites to ensure patient safety beginning Jan. 31.

However, the tide may have begun to change. Steward executives said on Feb. 2 they had secured a deal to stabilize operations and keep Massachusetts hospitals open — for now. Steward will receive bridge financing under the deal and consider transferring ownership of one or more hospitals to other companies, a Steward spokesperson confirmed to Healthcare Dive on Feb. 7.

While politicians welcomed the news, some say Steward’s long term outlook in the state is uncertain. Other politicians sought answers for how a prominent system could seemingly implode overnight.

“I am cautiously optimistic at this point that [Steward] will be able to remain open, because it’s really critical they do,” said Brockton City Councilor Phil Griffin. “But they owe a lot of people a lot of money, so we’ll see.”

However, the business model wasn’t immediately a financial success. Steward didn’t turn a profit between 2011 and 2014, according to a 2015 monitoring report from the Massachusetts attorney general. Instead, Steward’s debt increased from $326 million in 2011 to $413 million at the end of the 2014 fiscal year, while total liabilities ballooned to $1.4 billion in the same period as Steward engaged in real estate sale and leaseback plays.

Under the 2010 deal, Steward agreed to assume Caritas’ debt and carry out $400 million in capital expenditures over four years to upgrade the hospitals’ infrastructure. However, that capital expenditure could come in part from financial engineering, such as monetizing Steward’s own assets, according to Zirui Song, associate professor of health care policy and medicine at the Harvard Medical School who has studied private equity’s impact on healthcare since 2019.

Cerberus did not contribute equity into Steward after making its initial investment of $245.9 million, according to the December 2015 monitoring report. Meanwhile, according to reporting at the time, de la Torre wanted to expand Steward. Steward was on its own to raise funds.

Such deals are typically short-sighted, Song explained. When hospitals sell their property, they voluntarily forfeit their most valuable assets and tend to be saddled with high rent payments.

Healthcare Dive spoke with four workers across Steward’s portfolio who said Steward’s emphasis on the bottom line negatively impacted the company’s operations for years.

Terra Ciurro worked in the emergency department at Steward Health Care-owned Odessa Regional Medical Center in January 2022 as a travel nurse. She recalled researching Steward and being attracted to the fact the company was physician owned.

“I remember thinking, ‘That’s all I need to know. Surely, doctors will have their heart in the right place,’” Ciurro said. “But yeah — that’s not the experience I had at all.”

The emergency department was “shabby, rundown and ill-equipped,” and management didn’t fix broken equipment that could have been hazardous, she said. Nine weeks into her 13-week contract and three hours before Ciurro was scheduled to work, Ciurro said her staffing agency called to cut her contract unceremoniously short. Steward hadn’t paid its bills in six months, and the agency was pulling its nurses, she said she was told.

In Massachusetts, Katie Murphy, president of the Massachusetts Nurses Association, which represents more than 3,000 registered nurses and healthcare professionals who work in eight Steward hospitals, said there were “signals” that Steward facilities had been on the brink of collapse for “well over a year.”

Steward hospitals are often “significantly” short staffed and lack supplies from the basics, like dressings, to advanced operating room equipment, said Murphy. While most hospitals in the region got a handle on staffing and supply shortages in the aftermath of the COVID pandemic, at Steward hospitals shortages “continued to accelerate,” Murphy said.

A review of Steward’s finances by BDO USA, a tax and advisory firm contracted last summer by the health system itself to demonstrate it was solvent enough to construct a new hospital in Massachusetts, showed Steward had a liquidity problem. The health system had few reserves on hand last year to pay down its debts owed to vendors, possibly contributing to the shortages. The operator carried only 10.2 days of cash on hand in 2023. In comparison, most healthy nonprofit hospital systems carried 150 days of cash on hand or more in 2022, according to KFF.

One former finance employee, who worked for Steward beginning around 2018, said that the books were routinely left unbalanced during her tenure. Each month, she made a list of outstanding bills to determine who must be paid and who “we can get away with holding off” and paying later.

Food, pharmaceuticals and staff were always paid, while all other vendors were placed on an “escalation list,” she said. Her team prioritized paying vendors that had placed Steward on a credit hold.

The worker permanently soured on Steward when she said operating room staff had to “make do” without a piece of a crash cart — which is used in the event of a heart attack, stroke or trauma.

She stopped referring friends to Steward facilities, telling them “Don’t go — if you can go anywhere else, don’t go [to Steward], because there’s no telling if they’ll have the supplies needed to treat you.”

Away from regulatory review

Massachusetts officials maintain that it hasn’t been easy to see what was happening inside Steward.

Steward is legally required to submit financial data to the MA Center for Health Information and Analysis (CHIA) and to the Massachusetts Registration of Provider Organizations Program (MA-RPO Program), according to a spokesperson from the Health Policy Commission, which analyzes the reported data. Under the latter requirement, Steward is supposed to provide “a comprehensive financial statement, including information on parent entities and corporate affiliates as applicable.”

However, Steward fought the requirements. During Stuart Altman’s tenure as the chair of the Commission from 2012 to 2022, Altman told Healthcare Dive that the for-profit never submitted documents, despite CHIA levying fines against Steward for non-compliance. Steward even sued CHIA and HPC for relief against the reporting obligations.

Steward is currently appealing a superior court decision and order from June 2023 that required it to comply with the financial reporting requirements and produce audited financial reports that cover the full health system, Mickey O’Neill, communications director for the HPC told Healthcare Dive. As of Feb. 6, Steward’s non-compliance remained ongoing, O’Neill said.

Without direct insight into Steward’s finances, the state was operating at a disadvantage, said John McDonough, professor of the practice of public health at The Harvard T.H. Chan School of Public Health. He added that some regulators saw a crisis coming generally, “but the timing was hard to predict.”

Altman gives his team even more of a pass for not spotting the Steward problem.

“There was no indication while I was there that Steward was in deep trouble,” Altman said. Although Steward was the only hospital system that failed to report financial data to the HPC, that alone had not raised red flags for him. “[CEO] Ralph [de la Torre] was just a very contrarian guy. He didn’t do a lot of things.”

Song and his co-author, Sneha Kannan, a clinical research fellow at Harvard Medical School, are hopeful that in the future, regulatory agencies can make better use of the data they collect annually to track changes in healthcare performance over time. They can potentially identify problem operators before they become crises.

“State legislators, even national legislators, are not in the habit of comparing hospitals’ performances on [quality] measures to themselves over time — they compare to hospitals’ regional partners,” Kannan said. “Legislators, Medicare, [and] CMS has access to that information.”

However, although there’s interest from regulators in scrutinizing healthcare quality more closely — particularly when private equity gets involved — a streamlined approach to analyzing such data is still a “ways off,” according to the pair. For now, all parties interviewed for this piece agreed that the best way to avoid being caught off guard by a failing system was to know how such implosions could occur.

“If there’s a lesson from [Steward],” McDonough ventured, “it is that the entire state health system and state government need to be much more wary of all for-profits.”

Last week, venture capital firm General Catalyst announced its plan to acquire Summa Health, an Akron, OH-based integrated delivery system with three hospitals, a large medical group, a health plan, and an annual revenue of around $2B. The terms of the deal were not disclosed, though General Catalyst previously indicated it aimed to spend $1-3B to acquire a health system.

Pending regulatory approval, Summa will convert to a for-profit entity and become a fully owned subsidiary of General Catalyst’s recently launched Health Assurance Transformation Corporation (HATCo).

HATCo, under the leadership of former Intermountain Health CEO Marc Harrison, was founded with the intention of acquiring a health system to serve as a blueprint for General Catalyst’s vision of healthcare transformation.

The Gist:While there’s a dearth of evidence for what kind of health system makes a good venture capital investment, Summa’s concentrated footprint of integrated delivery assets, robust Medicare Advantage plan, and position in an aging, yet competitive, market certainly seem attractive given HATCo’s stated goals.

If it closes, the partnership will provide Summa with an influx of capital and General Catalyst with a “proving ground” for both its vision of healthcare transformation and its portfolio of technology solutions. But while it’s one thing to get Summa’s board to sign on, General Catalyst will now have to reckon with other important stakeholders.

Summa’s physicians will be the gatekeepers of change at the local level, and their buy-in will be required for any continued push toward value-based care or successful product roll-out.

And, behind the scenes, General Catalyst will have to convince its investors that this longer-term play to rethink care delivery will offer financial returns worth the wait.

Jersey City, N.J.-based CarePoint Health and Hudson Regional Hospital in Secaucus, N.J., have signed a letter of intent to combine under a new management company, Hudson Health System, which will incorporate the acute care facilities of both organizations.

Hudson Health System would be a four-hospital system that includes both nonprofit and for-profit hospitals in an innovative new model and continue to be in-network with all major payers.

The transaction is expected to strengthen CarePoint’s financial position and improve patient care and outcomes across the hospitals, according to John Rimmer, CarePoint’s chief medical officer, said in a Jan. 12 news release.

“Hudson County is the most diverse and dynamic community in New Jersey, and its residents deserve nothing less than exceptional care, affordable access, the most advanced specialties and technology, and the highest caliber physicians to serve patients’ needs, especially the underserved communities that rely on our facilities,” said CarePoint President and CEO Achintya Moulick, MD, who will be president and CEO of Hudson Health System. “With adequate state support, I believe we can build a hospital system that will deliver on its core mission.”

The letter of intent is the precursor to a new organizational structure and operating plan that will require approval from the New Jersey State Department of Health. Hudson Health System would be a four-hospital system that includes Hudson Regional, Bayonne Medical Center, Hoboken University Medical Center and Christ Hospital in Jersey City.

“This new system expands our mutual impact far beyond and far sooner than what we could ever have achieved separately,” Hudson Regional CEO Nizar Kifaieh, MD, said. “The possibilities are enormous and will energize the entire medical community to deliver that much more to the patients.”

More details about Hudson Health System are expected to be announced in the coming days.

This discussion was recorded on November 16, 2023. This transcript has been edited for clarity.

Robert D. Glatter, MD: Welcome. I’m Dr Robert Glatter, medical advisor for Medscape Emergency Medicine. Joining me today is Dr Brian Miller, a hospitalist with Johns Hopkins University School of Medicine and a health policy expert, to discuss the current and renewed interest in physician-owned hospitals.

Welcome, Dr Miller. It’s a pleasure to have you join me today.

Brian J. Miller, MD, MBA, MPH: Thank you for having me.

History and Controversies Surrounding Physician-Owned Hospitals

Miller: Thank you. I should note that my views are my own and don’t represent those of Hopkins or the American Enterprise Institute, where I’m a nonresident fellow nor the Medicare Payment Advisory Commission, of which I’m a Commissioner.

The story about physician-owned hospitals is an interesting one. Hospitals turned into health systems in the 1980s and 1990s, and physicians started to shift purely from an independent model into a more organized group practice or employed model. Physicians realized that they wanted an alternative operating arrangement. You want a choice of how you practice and what your employment is. And as community hospitals started to buy physicians and also establish their own physician groups de novo, physicians opened physician-owned hospitals.

Physician-owned hospitals fell into a couple of buckets. One is what we call community hospitals, or what the antitrust lawyers would call general acute care hospitals: those offering emergency room (ER) services, labor and delivery, primary care, general surgery — the whole regular gamut, except that some of the owners were physicians.

The other half of the marketplace ended up being specialty hospitals: those built around a specific medical specialty and series of procedures and chronic care. For example, cardiac hospitals often do CABG, TAVR, maybe abdominal aortic aneurysm (triple A) repairs, and they have cardiology clinics, cath labs, a cardiac intensive care unit (ICU), ER, etc. There were also orthopedic surgical specialty hospitals, which were sort of like an ambulatory surgery center (ASC) plus several beds. Then there were general surgical specialty hospitals. At one point, there were some women’s health–focused specialty hospitals.

The hospital industry, of course, as you can understand, didn’t exactly like this. They had a series of concerns about what we would historically call cherry-picking or lemon-dropping of patients. They were worried that physician-owned facilities didn’t want to serve public payer patients, and there was a whole series of reports and investigations.

Around the time the Affordable Care Act passed, the hospital industry had many concerns about physician-owned specialty hospitals, and there was a moratorium as part of the 2003 Medicare Modernization Act. As part of the bargaining over the hospital industry support for the Affordable Care Act, they traded their support for, among other things, their number one priority, which is a statutory prohibition on new or expanded physician-owned hospitals from participating in Medicare. That included both physician-owned community hospitals and physician-owned specialty hospitals.

Glatter: I guess the main interest is that, when physicians have an ownership or a stake in the hospital, this is what the Stark laws obviously were aimed at. That was part of the impetus to prevent physicians from referring patients where they had an ownership stake. Certainly, hospitals can be owned by attorneys and nonprofit organizations, and certainly, ASCs can be owned by physicians. There is an ongoing issue in terms of physicians not being able to have an ownership stake. In terms of equity ownership, we know that certain other models allow this, but basically, it sounds like this is an issue with Medicare. That seems to be the crux of it, correct?

Miller: Yes. I would also add that it’s interesting when we look at other professions. When we look at lawyers, nonlawyers are actually not allowed to own an equity stake in a law practice. In many other professions, you either have corporate ownership or professional ownership, or the alternative is you have only professional ownership.I would say the hospital industry is one of the few areas where professional ownership not only is not allowed, but also is statutorily prohibited functionally through the Medicare program.

Unveiling the Dynamics of Hospital Ownership

Glatter: A recent study done by two PhDs looked at 2019 data on 20 of the most expensive diagnosis-related groups (DRGs). It examined the cost savings, and we’re talking over $1 billion in expenditures when you look at the data from general acute care hospitals vs physician-owned hospitals. This is what appears to me to be a key driver of the push to loosen restrictions on physician-owned hospitals. Isn’t that correct?

Miller: I would say that’s one of many components. There’s more history to this issue. I remember sitting at a think tank talking to someone several years ago about hospital consolidation as an issue. We went through the usual levers that us policy wonks go through. We talked about antitrust enforcement, certificate of need, rising hospital costs from consolidation, lower quality (or at least no quality gains, as shown by a New England Journal of Medicine study), and decrements in patient experience that result from the diseconomies of scale. They sort of pooh-poohed many of the policy ideas. They basically said that there was no hope for hospital consolidation as an issue.

Well, what about physician ownership? I started with my research team to comb through the literature and found a variety of studies — some of which were sort of entertaining, because they’d do things like study physician-owned specialty hospitals, nonprofit-owned specialty hospitals, and for-profit specialty hospitals and compare them with nonprofit or for-profit community hospitals, and then say physician-owned hospitals that were specialty were bad.

They mixed ownership and service markets right there in so many ways, I’m not sure where to start. My team did a systematic review of around 30 years of research, looking at the evidence base in this space. We found a couple of things.

We found that physician-owned community hospitals did not have a cost or quality difference, meaning that there was no definitive evidence that the physician-owned community hospitals were cheaper based on historical evidence, which was very old. That means there’s not specific harm from them. When you permit market entry for community hospitals, that promotes competition, which results in lower prices and higher quality.

Then we also looked at the specialty hospital markets — surgical specialty hospitals, orthopedic surgical specialty hospitals, and cardiac hospitals. We noted for cardiac hospitals, there wasn’t clear evidence about cost savings, but there was definitive evidence of higher quality, from things like 30-day mortality for significant procedures like treatment of acute MI, triple A repair, stuff like that.

For orthopedic surgical specialty hospitals, we noted lower costs and higher quality, which again fits with operationally what we would know. If you have a facility that’s doing 20 total hips a day, you’re creating a focused factory. Just like if you think about it for interventional cardiology, your boards have a minimum number of procedures that you have to do to stay certified because we know about the volume-quality relationship.

Then we looked at general surgical specialty hospitals. There wasn’t enough evidence to make a conclusive thought about costs, and there was a clear trend toward higher quality. I would say this recent study is important, but there is a whole bunch of other literature out there, too.

Exploring the Scope of Emergency Care in Physician-Owned Hospitals

One thing I want to bring up — and this is an important issue — is that the risk for patients has been talked about by the American Hospital Association and the Federation of American Hospitals, in terms of limited or no emergency services at such physician-owned hospitals and having to call 911 when patients need emergent care or stabilization. That’s been the rebuttal, along with an Office of Inspector General (OIG) report from 2008. Almost, I guess, three quarters of the patients that needed emergent care got this at publicly funded hospitals.

Miller: I’m familiar with the argument about emergency care. If you actually go and look at it, it differs by specialty market. Physician-owned community hospitals have ERs because that’s how they get their business. If you are running a hospital medicine floor, a general surgical specialty floor, you have a labor delivery unit, a primary care clinic, and a cardiology clinic. You have all the things that all the other hospitals have. The physician-owned community hospitals almost uniformly have an ER.

When you look at the physician-owned specialty hospitals, it’s a little more granular. If you look at the cardiac hospitals, they have ERs. They also have cardiac ICUs, operating rooms, etc. The area where the hospital industry had concerns — which I think is valid to point out — is that physician-owned orthopedic surgical specialty hospitals don’t have ERs. But this makes sense because of what that hospital functionally is: a factory for whatever the scope of procedures is, be it joint replacements or shoulder arthroscopy. The orthopedic surgical specialty hospital is like an ASC plus several hospital beds. Many of those did not have ERs because clinically it didn’t make sense.

What’s interesting, though, is that the hospital industry also operates specialty hospitals. If you go into many of the large systems, they have cardiac specialty hospitals and cancer specialty hospitals. I would say that some of them have ERs, as they appropriately should, and some of those specialty hospitals do not. They might have a community hospital down the street that’s part of that health system that has an ER, but some of the specialty hospitals don’t necessarily have a dedicated ER.

I agree, that’s a valid concern. I would say, though, the question is, what are the scope of services in that hospital? Is an ER required? Community hospitals should have ERs. It makes sense also for a cardiac hospital to have one. If you’re running a total joint replacement factory, it might not make clinical sense.

Glatter: The patients who are treated at that hospital, if they do have emergent conditions, need to have board-certified emergency physicians treating them, in my view because I’m an ER physician. Having surgeons that are not emergency physicians staff a department at a specialty orthopedic hospital or, say, a cancer hospital is not acceptable from my standpoint. That’s my opinion and recommendation, coming from emergency medicine.

Miller: I would say that anesthesiologists are actually highly qualified in critical care. The question is about clinical decompensation; if you’re doing a procedure, you have an anesthesiologist right there who is capable of critical care. The function of the ER is to either serve as a window into the hospital for patient volume or to serve as a referral for emergent complaints.

Glatter: An anesthesiologist — I’ll take issue with that — does not have the training of an emergency physician in terms of scope of practice.

Miller: My anesthesiology colleagues would probably disagree for managing an emergency during an operating room case.

Glatter: Fair enough, but I think in the general sense. The other issue is that, in terms of emergent responses to patients that decompensate, when you have to transfer a patient, that violates Medicare requirements. How is that even a valid issue or argument if you’re going to have to transfer a patient from your specialty hospital? That happens. Again, I know that you’re saying these hospitals are completely independent and can function, stabilize patients, and treat emergencies, but that’s not the reality across the country, in my opinion.

Miller: I don’t think that’s the case for the physician-owned specialty cardiac hospitals, for starters. Many of those have ICUs in addition to operating rooms as a matter of routine in addition to ERs. I don’t think that’s the case for physician-owned community hospitals, which have ERs, ICUs, medicine floors, and surgical floors. Physician-owned community hospitals are around half the market. Of that remaining market, a significant percentage are cardiac hospitals. If you’re taking an issue with orthopedic surgical specialty hospitals, that’s a clinical operational question that can and should be answered.

I’d also posit that the nonprofit and for-profit hospital industries also operate specialty hospitals. Any of these questions, we shouldn’t just be asking about physician-owned facilities; we should be asking about them across ownership types, because we’re talking about scope of service and quality and safety. The ownership in that case doesn’t matter. The broader question is, are orthopedic surgical specialty hospitals owned by physicians, tax-exempt hospitals, or tax-paying hospitals? Is that a valid clinical business model? Is it safe? Does it meet Medicare conditions of participation? I would say that’s what that question is, because other ownership models do operate those facilities.

Glatter: You make some valid points, and I do agree on some of them. I think that, ultimately, these models of care, and certainly cost and quality, are issues. Again, it goes back to being able, in my opinion, to provide emergent care, which seems to me a very important issue.

Miller: I agree that providing emergent care is an issue. It’s an issue in any site of care. The hospital industry posits that all hospital outpatient departments (HOPDs) have emergent care. I can tell you, having worked in HOPDs (I’ve trained in them during residency), the response if something emergent happens is to either call 911 or wheel the patient down to the ER in a wheelchair or stretcher. I think that these hospital claims about emergency care coverage —these are important questions, but we should be asking them across all clinical settings and say what is the appropriate scope of care provided? What is the appropriate level of acuity and ability to provide emergent or critical care? That’s an important question regardless of ownership model across the entire industry.

Deeper Dive Into Data on Physician-Owned Hospitals

Glatter: We need to really focus on that. I’ll agree with you on that.

There was a March 2023 report from Dobson | DaVanzo. It showed that physician-owned hospitals had lower Medicaid, dual-eligible, and uncompensated care and charity care discharges than full-service acute care hospitals. Physician-owned hospitals had less than half the proportion of Medicaid discharges compared with non–physician-owned hospitals. They were also less likely to care for dual-eligible patients overall compared with non–physician-owned hospitals.

In addition, when COVID hit, the physician-owned hospitals overall — and again, there may be exceptions — were not equipped to handle these patient surges in the acute setting of a public health emergency. There was a hospital in Texas that did pivot that I’m aware of — Renaissance Hospital, which ramped up a long-term care facility to become a COVID hospital — but I think that’s the exception. I think this report raises some valid concerns; I’ll let you rebut that.

Miller: A couple of things. One, I am not aware that there’s any clear market evidence or a systematic study that shows that physician-owned hospitals had trouble responding to COVID. I don’t think that assertion has been proven. The study was funded by the hospital industry. First of all, it was not a peer-reviewed study; it was funded by an industry that paid a consulting firm. It doesn’t mean that we still shouldn’t read it, but that brings bias into question. The joke in Washington is, pick your favorite statistician or economist, and they can say what you want and have a battle of economists and statisticians.

For example, in that study, they didn’t include the entire ownership universe of physician-owned hospitals. If we go to the peer-reviewed literature, there’s a great 2015 BMJ paper showing that the Medicaid payer mix is actually the same between physician-owned hospitals vs not. The mix of patients by ethnicity — for example, think about African American patients — was the same. I would be more inclined to believe the peer-reviewed literature in BMJ as opposed to an industry-funded study that was not peer-reviewed and not independent and has methodological questions.

Glatter: Those data are 8 years old, so I’d like to see more recent data. It would be interesting, just as a follow-up to that, to see where the needle has moved — if it has, for that matter — in terms of Medicaid patients that you’re referring to.

Miller: I tend to be skeptical of all industry research, regardless of who published it, because they have an economic incentive. If they’re selecting certain age groups or excluding certain hospitals, that makes you wonder about the validity of the study. Your job as an industry-funded researcher is that, essentially, you’re being paid to look for an answer. It’s not necessarily an honest evaluation of the data.

Glatter: I want to bring up another point about the Hospital Readmissions Reduction Program (HRRP) and the data on how physician-owned hospitals compared with acute care hospitals that are non–physician-owned and have you comment on that. The Dobson | DaVanzo study called into question that physician-owned hospitals treat fewer patients who are dual-eligible, which we know.

Miller: I don’t think we do know that.

Glatter: There are data that point to that, again, looking at the studies.

Miller: I’m saying that’s a single study funded by industry as opposed to an independent, academic, peer-reviewed literature paper. That would be like saying, during the debate of the Inflation Reduction Act (IRA), that you should read the pharmaceutical industries research but take any of it at pure face value as factual. Yes, we should read it. Yes, we should evaluate it on its own merits. I think, again, appropriately, you need to be concerned when people have an economic incentive.

The question about the HRRP I’m going to take a little broader, because I think that program is unfair to the industry overall. There are many factors that drive hospital readmission. Whether Mrs Smith went home and ate potato chips and then took her Lasix, that’s very much outside of the hospital industry’s control, and there’s some evidence that the HRRP increases mortality in some patient populations.

In terms of a quality metric, it’s unfair to the industry. I think we took an operating process, internal metric for the hospital industry, turned it into a quality metric, and attached it to a financial bonus, which is an inappropriate policy decision.

Rethinking Ownership Models and Empowering Clinicians

Glatter: I agree with you on that. One thing I do want to bring up is that whether the physician-owned hospitals are subject to many of the quality measures that full-service, acute care hospitals are. That really is, I think, a broader context.

Miller: Fifty-five percent of physician-owned hospitals are full-service community hospitals, so I would say at least half the market is 100% subject to that.

Glatter: If only 50% are, that’s already an issue.

Miller: Cardiac specialty hospitals — which, as I said, nonprofit and for-profit hospital chains also operate — are also subject to the appropriate quality measures, readmissions, etc. Just because we don’t necessarily have the best quality measurement in the system in the country, it doesn’t mean that we shouldn’t allow care specialization. As I’d point out, if we’re concerned about specialty hospitals, the concern shouldn’t just be about physician-owned specialty hospitals; it should be about specialty hospitals by and large. Many health systems run cardiac specialty hospitals, cancer specialty hospitals, and orthopedic specialty hospitals. If we’re going to have a discussion about concerns there, it should be about the entire industry of specialty hospitals.

I think specialty hospitals serve an important role in society, allowing for specialization and exploiting in a positive way the volume-quality relationship. Whether those are owned by a for-profit publicly traded company, a tax-exempt facility, or physicians, I think that is an important way to have innovation and care delivery because frankly, we haven’t had much innovation in care delivery. Much of what we do in terms of how we practice clinically hasn’t really changed in the 50 years since my late father graduated from medical school. We still have rounds, we’re still taking notes, we’re still operating in the same way. Many processes are manual. We don’t have the mass production and mass customization of care that we need.

When you have a focused factory, it allows you to design care in a way that drives up quality, not just for the average patient but also the patients at the tail ends, because you have time to focus on that specific service line and that specific patient population.

Physician-owned community hospitals offer an important opportunity for a different employment model. I remember going to the dermatologist and the dermatologist was depressed, shuffling around the room, sad, and I asked him why. He said he didn’t really like his employer, and I said, “Why don’t you pick another one?” He’s like, “There are only two large health systems I can work for. They all have the same clinical practice environment and functionally the same value.”

Physicians are increasingly burned out. They face monopsony power in who purchases their labor. They have little control. They don’t want to go through five committees, seven administrators, and attend 25 meetings just to change a single small process in clinical operations. If you’re an owner operator, you have a much better ability to do it.

Frankly, when many facilities do well now, when they do well clinically and do well financially, who benefits? The hospital administration and the hospital executives. The doctors aren’t benefiting. The nurses aren’t benefiting. The CNA is not benefiting. The secretary is not benefiting. The custodian is not benefiting. Shouldn’t the workers have a right to own and operate the business and do well when the business does well serving the community? That puts me in the weird space of agreeing with both conservatives and progressives.

Glatter: I agree with you. I think an ownership stake is always attractive. It helps with retention of employed persons. There’s no question that, when they have a stake, when they have skin in the game, they feel more empowered. I will not argue with you about that.

Miller: We don’t have business models where workers have that option in healthcare. Like the National Academy of Medicine said, one of the key drivers of burnout is the externalization of the locus of control over clinical practice, and the current business operating models guarantee an externalization of the locus of control over clinical practice.

If you actually look at the recent American Medical Association (AMA) meeting, there was a resolution to ban the corporate practice of medicine. They wanted to go more toward the legal professions model where only physicians can own and operate care delivery.

Miller: It’s not just doctors. I think nurses want a better lifestyle. The nurses are treated as interchangeable lines on a spreadsheet. The nurses are an integral part of our clinical team. Why don’t we work together as a clinical unit to build a better delivery system? What better way to do that than to have clinicians in charge of it, right?

My favorite bakery that’s about 30 minutes away is owned by a baker. It is not owned by a large tax-exempt corporation. It’s owned by an owner operator who takes pride in their work. I think that is something that the profession would do well to return to. When I was a resident, one of my colleagues was already planning their retirement. That’s how depressed they were.

I went into medicine to actually care for patients. I think that we can make the world a better place for our patients. What that means is not only treating them with drugs and devices, but also creating a delivery system where they don’t have to wander from lobby to lobby in a 200,000 square-foot facility, wait in line for hours on end, get bills 6 months later, and fill out endless paper forms over and over again.

All of these basic processes in healthcare delivery that are broken could have and should have been fixed — and have been fixed in almost every other industry. I had to replace one of my car tires because I had a flat tire. The local tire shop has an app, and it sends me SMS text messages telling me when my appointment is and when my car is ready. We have solved all of these problems in many other businesses.

We have not solved them in healthcare delivery because, one, we have massive monopolies that are raising prices, have lower quality, and deliver a crappy patient experience, and we have also subjugated the clinical worker into a corporate automaton. We are functionally drones. We don’t have the agency and the authority to improve clinical operations anymore. It’s really depressing, and we should have that option again.

I trust my doctor. I trust the nurses that I work with, and I would like them to help make clinical decisions in a financially responsible and a sensible operational manner. We need to empower our workforce in order to do that so we can recapture the value of what it means to be a clinician again.

The current model of corporate employment: massive scale, more administrators, more processes, more emails, more meetings, more PowerPoint decks, more federal subsidies. The hospital industry has choices. It can improve clinical operations. It can show up in Washington and lobby for increased subsidies. It can invest in the market and not pay taxes for the tax-exempt facilities. Obviously, it makes the logical choices as an economic actor to show up, lobby for increased subsidies, and then also invest in the stock market.

Improving clinical operations is hard. It hasn’t happened. The Bureau of Labor Statistics shows that the private community hospital industry has had flat labor productivity growth, on average, for the past 25 years, and for some years it even declined. This is totally atypical across the economy.

We have failed our clinicians, and most importantly, we have failed our patients. I’ve been sick. My relatives have been sick, waiting hours, not able to get appointments, and redoing forms. It’s a total disaster. It’s time and reasonable to try an alternative ownership and operating model. There are obviously problems. The problems can and should be addressed, but it doesn’t mean that we should have a statutory prohibition on professionals owning and operating their own business.

Glatter: There was a report that $500 million was saved by limiting or banning or putting a moratorium on physician-owned hospitals by the Congressional Budget Office.

The CBO is not transparent about what its assumptions are or its analysis and methods. As a researcher, we have to publish our information. It has to go through peer review. I want to know what goes into that $500 million figure — what the assumptions are and what the model is. It’s hard to comment without knowing how they came up with it.

Glatter: The points you make are very valid. Physicians and nurses want a better lifestyle.

Miller: It’s not even a better lifestyle. It’s about having a say in how clinical operations work and helping make them better. We want the delivery system to work better. This is an opportunity for us to do so.

Glatter: That translates into technology: obviously, generative artificial intelligence (AI) coming into the forefront, as we know, and changing care delivery models as you’re referring to, which is going to happen. It’s going to be a slow process. I think that the evolution is happening and will happen, as you accurately described.

Miller: The other thing that’s different now vs 20 years ago is that managed care is here, there, and everywhere, as Dr Seuss would say. You have utilization review and prior authorization, which I’ve experienced as a patient and a physician, and boy, is it not a fun process. There’s a large amount of friction that needs to be improved. If we’re worried about induced demand or inappropriate utilization, we have managed care right there to help police bad behavior.

Reforming Healthcare Systems and Restoring Patient-Centric Focus

Glatter: If you were to come up with, say, three bullet points of how we can work our way out of this current morass of where our healthcare systems exist, where do you see the solutions or how can we make and effect change?

Miller: I’d say there are a couple of things. One is, let business models compete fairly on an equal playing field. Let the physician-owned hospital compete with the tax-exempt hospital and the nonprofit hospital. Put them on an equal playing field. We have things like 340B, which favors tax-exempt hospitals. For-profit or tax-paying hospitals are not able to participate in that. That doesn’t make any sense just from a public policy perspective. Tax-paying hospitals and physician-owned hospitals pay taxes on investments, but tax-exempt hospitals don’t. I think, in public policy, we need to equalize the playing field between business models. Let the best business model win.

The other thing we need to do is to encourage the adoption of technology. The physician will eventually be an arbiter of tech-driven or AI-driven tools. In fact, at some point, the standard of care might be to use those tools. Not using those tools would be seen as negligence. If you think about placing a jugular or central venous catheter, to not use ultrasound would be considered insane. Thirty years ago, to use ultrasound would be considered novel. I think technology and AI will get us to that point of helping make care more efficient and more customized.

Those are the two biggest interventions, I would say. Third, every time we have a conversation in public policy, we need to remember what it is to be a patient. The decision should be driven not around any one industry’s profitability, but what it is to be a patient and how we can make that experience less burdensome, less expensive, or in plain English, suck less.

Glatter: Safety net hospitals and critical access hospitals are part of this discussion that, yes, we want everything to, in an ideal world, function more efficiently and effectively, with less cost and less red tape. The safety net of our nation is struggling.

Miller: I 100% agree. The Cook County hospitals of the world are deserving of our support and, frankly, our gratitude. Facilities like that have huge burdens of patients with Medicaid. We also still have millions of uninsured patients. The neighborhoods that they serve are also poorer. I think facilities like that are deserving of public support.

I also think we need to clearly define what those hospitals are. One of the challenges I’ve realized as I waded into this space is that market definitions of what a service market is for a hospital, its specialty type or what a safety net hospital is need to be more clearly defined because those facilities 100% are deserving of our support. We just need to be clear about what they are.

Regarding critical access hospitals, when you practice in a rural area, you have to think differently about care delivery. I’d say many of the rural systems are highly creative in how they structure clinical operations. Before the public health emergency, during the COVID pandemic, when we had a massive change in telehealth, rural hospitals were using — within the very narrow confines — as much telehealth as they could and should.

Rural hospitals also make greater use of nurse practitioners (NPs) and physician assistants (PAs). For many of the specialty services, I remember, your first call was an NP or a PA because the physician was downstairs doing procedures. They’d come up and assess the patient before the procedure, but most of your consult questions were answered by the NP or PA. I’m not saying that’s the model we should use nationwide, but that rural systems are highly innovative and creative; they’re deserving of our time, attention, and support, and frankly, we can learn from them.

Glatter: I want to thank you for your time and your expertise in this area. We’ll see how the congressional hearings affect the industry as a whole, how the needle moves, and whether the ban or moratorium on physician-owned hospitals continues to exist going forward.

Miller: I appreciate you having me. The hospital industry is one of the most important industries for health care. This is a time of inflection, right? We need to go back to the value of what it means to be a clinician and serve patients. Hospitals need to reorient themselves around that core concern. How do we help support clinicians — doctors, nurses, pharmacists, whomever it is — in serving patients? Hospitals have become too corporate, so I think that this is an expected pushback.

Glatter: Again, I want to thank you for your time. This was a very important discussion. Thank you for your expertise.

Robert D. Glatter, MD, is an assistant professor of emergency medicine at Zucker School of Medicine at Hofstra/Northwell in Hempstead, New York. He is a medical advisor for Medscape and hosts the Hot Topics in EM series.

Brian J. Miller, MD, MBA, MPH, is a hospitalist and an assistant professor of medicine at the Johns Hopkins University School of Medicine. He is also a nonresident fellow at the American Enterprise Institute. From 2014 – 2017, Dr Miller worked at four federal regulatory agencies: Federal Trade Commission (FTC), Federal Communications Commission (FCC), Centers for Medicare & Medicaid Services (CMS), and the Food & Drug Administration (FDA).

Private equity firms have drawn significant policy interest and scrutiny amid recent reports of surprise billing, rising out-of-pocket costs for patients and increased healthcare spending in the U.S., according to Health Affairs.

The Private Equity Stakeholder Project has found at least 386 hospitals in the U.S. that are owned by private equity firms.

Six things to know:

1. The 386 private equity–owned hospitals represent 9% of all private hospitals and 30% of all proprietary for-profit hospitals.

2. Thirty-four percent of private equity-owned hospitals serve rural populations.

3. Texas is the state with the most private equity-owned hospitals (85).

4. While New Mexico has fewer private equity-owned hospitals (17), it has the highest proportion of private equity-backed hospitals compared to all private non-government hospitals at 43%.

5. More than 24% of private equity-owned facilities are psychiatric hospitals.

6. A few private equity firms dominate the list, according to the Private Equity Stakeholder Project:

Apollo Global Management (LifePoint Health (Brentwood, Tenn.) and ScionHealth (Louisville, Ky.): 177 hospitals combined)

Equity Group Investments (Ardent Health Services (Nashville, Tenn): 30 hospitals)

One Equity Partners (Ernest Health (Albuquerque, N.M.): 27 hospitals)

GoldenTree Asset Management and Davidson Kempner (Quorum Health (Brentwood, Tenn.): 21 hospitals)

Bain Capital (Surgery Partners (Brentwood, Tenn.): 19 hospitals)

The nation’s largest for-profit hospital systems by revenue — HCA Healthcare, Community Health Systems, Tenet Healthcare and Universal Health Services —reported mixed results during the third quarter of 2023, despite announcing strong demand for patient services.

With the exception of HCA, each operator reported lower profits in the third quarter compared with the same period last year. Health systems CHS and HCA reported earnings that fell short of Wall Street expectations for revenue.

Major operators posted declining profits in the third quarter compared to the same period in 2022

Q3 net income in millions, by operator

Health System

Profit

Percent Change YOY

Community Health Systems

$−91

−117%

HCA Healthcare

$1,800

59%

Tenet Healthcare

$101

−23%

Universal Health Services

$167

−9%

Admissions rose across the board compared to the same period last year: Same facility equivalent admissions rose4.1% at HCA , 3.7% at CHS and 0.6% at Tenet,and adjusted admissions at acute hospitals rose 6.8% at UHS.

Although the for-profit operators began cost containment strategies earlier this year — recognizing that rising expenses, including costs of salary and wages, were pressuring hospital profitability post-pandemic — expenses also rose, with growth in salaries and benefit costs once again pressuring most operators’ revenue.

Hospital operators faced new challenges this quarter, executives said, including increased physician staffing fees and what hospital executives characterizedas aggressive behavior from payers.

Hospitals highlight rising physician fees

Rising physician fees were a topic of concern on earnings calls this quarter, with executives reporting fees that were 15% to 40% higher compared with the same period last year.

Third-party staffing firms charge hospitals physician fees, a percentage of physicians’ salaries, on top of the salaries themselves. Physician fees are separate but related to contract labor costs, which plagued hospitals during the COVID-19 pandemic as they attempted to stem staffing shortages.

Hospitals typically contract specialty hospitalist roles — like anesthesiologists, radiologists and emergency department physicians — and incur associated staffing costs.

Physician fees at HCA, the country’s largest hospital chain, grew 20% year over year in the third quarter, according to CFO Bill Rutherford.

Physician fees were up by as much as 40% at UHS — making up 7.6% of totaloperating expenses this quarter and surpassing the company’s initial projections for the year,CEOMarc Miller said during an earnings call. Historically, physician fees accounted for about 6% of UHS’ total expenses.

Likewise, Franklin, Tennessee-based CHS attributed some of its third-quarter losses to “increased rates for outsourced medical specialists,” according to a release on the operator’s earnings.

Tenet CEO Saum Sutaria noted that physician fee expenses were up 15% year over year, but said on an earnings call that the operator had spied rising physician fees during the pandemic, and had begun efforts to contain costs — including restructuring staffing contracts and in-sourcing critical physician services.

As a result, physician fee costs at Tenet had remained “relatively flat” from the second quarter to the third quarter this year, according to the Sutaria.

Physician fee increases may be a delayed consequence of the No Surprises Act, which went into effect in January of last year, experts say.

On an earnings call, UHS CFO Steve Filton said “the industry has largely had to reset itself” in wake of the law. Tenet and CHS executives echoed the sentiment, noting that the law had disrupted staffing firms’ business models and complicated payment processes.

The No Surprises Act prevents patients who unknowingly receive out-of-network care at an in-network facility from being stuck with unexpectedbills. However, the act has had unintended ripple effects, experts say.

Staffing firms and hospitals allege that the arbitration process created to resolve disputes between providers and insurers is unbalanced and incentivizes insurers to withhold reimbursement for care. In an August survey, over half of doctors reported insurers have either ignored decisions made by arbitrators or declined to pay claims in full.

In other cases, a backlog prevents claims from being adjudicated at all. Last year, the CMS found the federal arbitration process had only reached a payment determination in 15% of cases. Federal regulators have been forced to pause and restart the arbitration process multiple times in the wake of federal court decisions challenging arbitration methodology.

Although the act went into effect more than a year ago, many hospitals are just now feeling the strain, saidLoren Adler, associate director at the Brookings Institute’s Schaeffer Initiative on Health Policy.

That’s because most insurers, hospitals and medical groups operate on three-year contracts, according to Adler. Staffing firms, which have struggled since the No Surprises Act was enacted, have passed on costs to hospitals as contracts come up for negotiation and insurers charge firms higher rates.

In the face of rising costs, some hospitals may opt to follow Tenet and CHS and in-source physicians — either to retain contracts with physicians who worked with firms that have folded or because the passing of the No Surprises Act makes outsourcing less attractive.

CHS hired 500 physicians from staffing firm American Physician Partners after the company collapsed in July. CFO Kevin Hammons said on an earnings call that hiring the physicians had saved CHS “approximately $4 million sequentially compared to the subsidy payments previously paid” to the staffing firm.

However, in-sourcing may not be an effective cost containment strategy for all operators. HCA reported it was hemorrhaging money following its first-quarter majority stake purchase of staffing firm Valesco, which brought about 5,000 physicians onto its payroll. HCA CEO Sam Hazen said the system expects to lose $50 million per quarter on the venture through 2024, citing low payments as the primary issue.

Payer problems

Hospital executives also tied quarterly losses to aggressive behavior from insurers during third-quarter earnings calls.

UHS executives said payers were improperly denying high volumes of claims and disrupting payments to its hospitals, with UHS’ Miller characterizing insurers as “increasingly aggressive” during the third quarter. Though insurers had reduced their number of claims audits, denials and patient status changes during the early stages of the pandemic, payers were increasing denials and reviews, according to UHS’ Filton.

Tenet’s Sutaria said that claims denials were “excessive and inappropriate” during a third-quarter earnings call, adding that the hospital system was working to push back on the volume of claims denials.

Their number one strategy is to provide “excellent documentation” to refute denials quickly, Sutaria said.

Still, excessive claims denials can drive up administrative costs for hospitals, according to Matthew Bates, managing director at Kaufman Hall.

“That denial creates a lot more work, because now I have to deal with that bill two, three, four times to get through the denial process,” Bates said. “It starts to rapidly eat into the operating margins… [becoming] both a cashflow problem and an administrative costs burden.”

Executives across the four for-profit operators said they planned to negotiate with insurers to receive more favorable rates and limit the number of denials in subsequent quarters.

HCA’s Hazen said that it was important for HCA to maintain its in-network status with insurers “to avoid the surprise billing and that [independent dispute resolution] process,” but that it would work with its payers to get “reasonable rates” going forward.

Does hospital ownership matter? According to a study published last week in Health Affairs Scholar, NOT MUCH. That’s a problem for not-for-profit hospitals who claim otherwise.

58% of U.S. hospitals are not-for-profit hospitals; the rest are public (19%) or investor-owned (24%). In recent months, not-for-profit systems have faced growing antagonism from regulators and critics who challenge the worthwhileness of their tax exemptions and reasonableness of the compensation paid their top executives.

The lion’s share of this negative attention is directed at large, not-for-profit hospital system operators. Case in point: last week, Banner Health (AZ) joined the ranks of high-profile operators taken to task in the Arizona Republic for their CEO’s compensation contrasting it to not-for-profit sectors in which compensation is considerably lower.

Unflattering attention to NFP hospitals, especially the big-name systems, is unlikely to subside in the near-term. U.S. healthcare has become a winner-take-all battleground increasingly dominated by large-scale, investor-owned interests in hospitals, medical groups, insurance, retail health in pursuit of a piece of the $4.6 trillion pie.

The moral high ground once the domain of not-for-profit hospitals is shaky.

The NYU study examined whether hospital ownership influenced decisions made by consumers: they found “Fewer than one-third of respondents (29.5%) indicated that hospital status had ever been relevant to them in making decisions about where to seek care…significantly more important to respondents who indicated the lowest health literacy—74.7% of whom answered the key question affirmatively—than it was for people who indicated high health literacy, of whom only 18.3% found hospital ownership status to be relevant…also considerably more relevant for people working in health care than for those who did not work in health care (61.0% vs 24.5%)…

We found little evidence that hospital nonprofit status influenced Americans’ decisions about where to seek care. Ownership status was relevant for fewer than 30% of respondents and preference was greatest overall for public hospitals. Only 30–45% of respondents could correctly identify the ownership status of nationally recognized hospitals, and fewer than 30% could identify their local hospitals.

These findings suggest that contract failure does not currently provide a justification of nonprofit hospitals’ value; further scrutiny of tax exemption for nonprofit hospitals is warranted.”

Are NFP hospitals concerned? YES. It’s reality as systems address near term operational challenges and long-term questions about their strategies.

Last weekend, I facilitated the 4th Annual Chief Strategy Officers Roundtable in Austin TX sponsored by Lumeris. The group consisted of senior-level strategists from 11 not-for-profit systems and one for-profit. In one session, each reacted to 50 future state scenarios in terms of “likelihood” and “disruptive impact” in the NEAR term (3-5 years) and LONG TERM (8-10 years) using a 1 to 10 scale with 10 HI.

From these data and the discussion that followed, there’s consensus that the U.S. healthcare market is unlikely to change dramatically long-term, their short-term conditions will be tougher and their challenges unique.

‘Near-term cost containment is a priority. Hospitals are here-to-stay, but operating them will be harder.’

‘Increased scale and growth are necessary imperatives for their systems.’

‘Hospital systems will compete in a market wherein private capital and investor ownership will play a growing role, insurers will be hostile and value will the primary focus of cost-reduction by purchasers and policymakers.’

‘Distinctions betweennot-for-profit and for-profit hospitals are significant.’

‘Conditions for hospitals will be tougher as insurers play a stronger hand in shaping the future.’

Given the NYU study findings (above) concluding NFP ownership has marginal impact on hospital choices made by consumers, it’s understandable NFPs are anxious.

My take:

The issues facing not-for-profit hospitals in the U.S. are unique and complex. Per the commentary of the CSOs, their market conditions are daunting and major changes in their structure, funding and regulation unlikely.

That means lack of public understanding of their unique role is a conundrum.

Paul

PS: Issues about CEO compensation in healthcare are touchy and often unfair.

In every major NFP system, comp is set by the Independent Board Compensation Committee with outside consultative counsel. The vast majority of these CEOs aren’t in the job for the money joining their workforce in pursuit of the unique higher calling afforded service leaders in NFP healthcare.