https://www.healthcaredive.com/news/hospital-price-transparency-push-draws-industry-ire-but-effects-likely-lim/557536/

Far-reaching rules mandating industry price transparency could mark a major shift, but experts are skeptical the efforts will meaningfully lower prices for patients without a more fundamental system overhaul.

President Donald Trump’s executive order signed Monday directs HHS and other federal departments to begin rulemaking to require hospitals and payers to release information based on their privately negotiated rates. Providers would also have to give patients estimates of their out-of-pocket costs before a procedure.

The moves come amid efforts from the federal government and Congress to push the healthcare industry to address patient anger over high prices, particularly regarding what medical bills they can expect to receive.

Many details must still be worked out as HHS and CMS craft their proposals, but providers and payers were quick to condemn any notion of making negotiated rates public. A legal challenge to the rules is also likely.

Many policy analysts and economists said that while price transparency is good in theory, current evidence shows patients don’t take advantage of pricing information now available, said Ateev Mehrotra, associate policy of healthcare policy and Harvard Medical School.

Patients are wary of going against a doctor’s advice to undergo a certain procedure or test, and to get it done at a certain facility. A difference in price may not be enough to sway them.

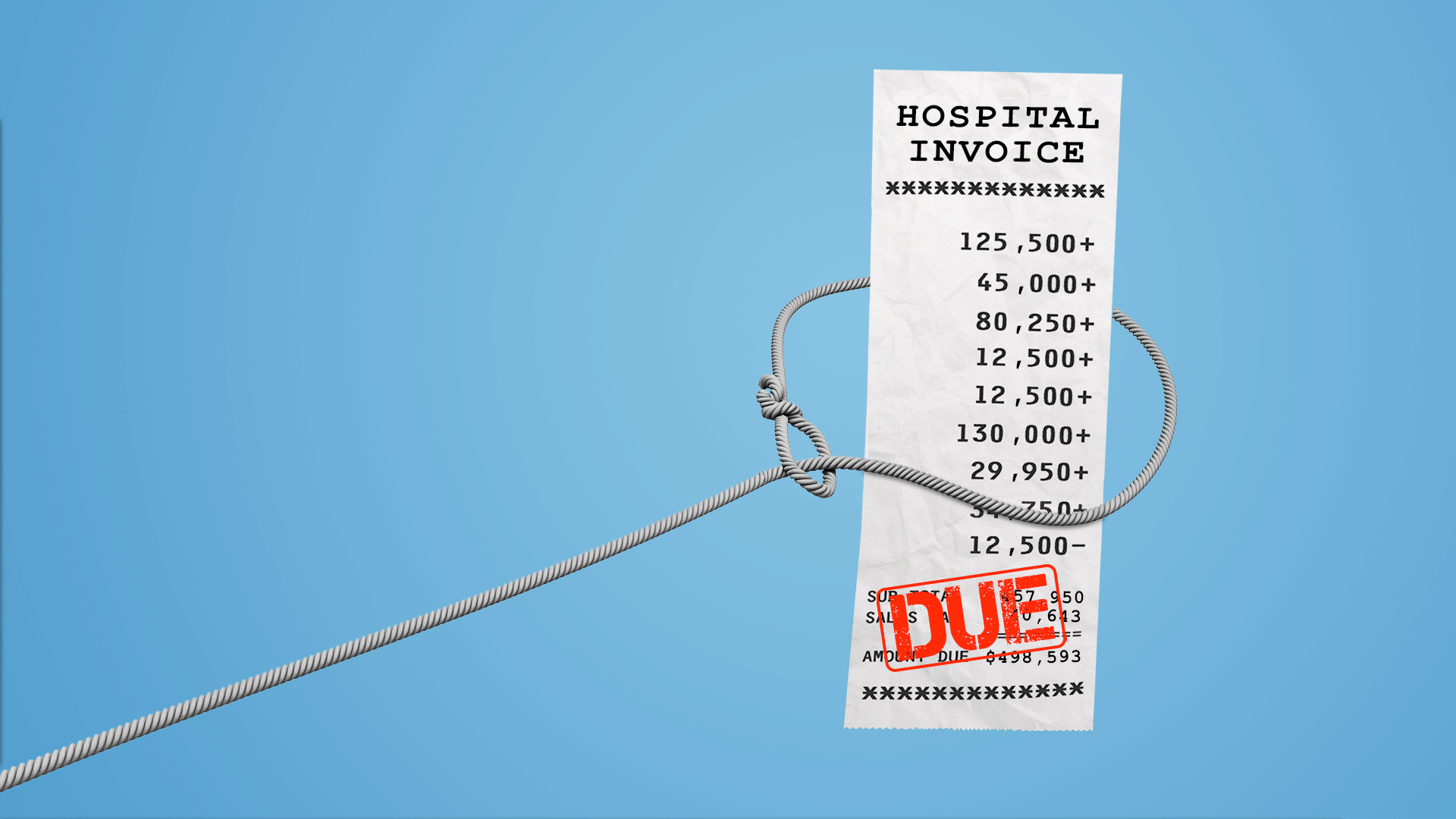

Also, the healthcare system has so many moving parts and unique elements that understanding a medical bill and how the price was calculated is daunting, to say the least.

“That complexity hinders the ability of people to effectively shop for care,” Mehrotra told Healthcare Dive “It’s not like going to Amazon and buying a toothbrush or whatever.”

What the order actual does

The executive order has two main directives:

- Within 60 days, HHS must propose a regulation “to require hospitals to publicly post standard charge information, including charges and information based on negotiated rates and for common or shoppable items and services, in an easy-to-understand, consumer-friendly, and machine-readable format using consensus-based data standards that will meaningfully inform patients’ decision making and allow patients to compare prices across hospitals.”

- Within 90 days, HHS and the Departments of Labor and Treasury must solicit comment on a proposal “to require healthcare providers, health insurance issuers, and self-insured group health plans to provide or facilitate access to information about expected out-of-pocket costs for items or services to patients before they receive care.”

The order also outlines smaller steps, including a report from HHS on how the federal government and private companies are impeding quality and price transparency in healthcare and another on measures the White House can take to deter surprise billing.

It also directs federal agencies to increase access to de-identified claims data (an idea strongly favored by policy analysts and researchers) and requires HHS to identify priority databases to be publicly released.

The order requests the Secretary of the Treasury expand coverage options for high-deductible health plans and health savings accounts. It specifically asks the department to explore using HSA funds for direct primary care, an idea Senate HELP Committee Chairman Lamar Alexander, R-Tenn., said he “especially like[d].”

Industry pushes back

The order itself wastes no time in pointing the finger at industry players for current patient frustrations with the system. “Opaque pricing structures may benefit powerful special interest groups, such as large hospital systems and insurance companies, but they generally leave patients and taxpayers worse off than would a more transparent system,” according to the document.

As expected, payer and provider groups slammed any attempt to force them to reveal the rates they negotiate behind closed doors, though they expressed appreciation for the general push toward more transparency.

The American Hospital Association shied away from strong language as details are still being worked out, but did say “publicly posting privately negotiated rates could, in fact, undermine the competitive forces of private market dynamics, and result in increased prices.”

The Federation of American Hospitals took a similar tone in a statement from CEO Chip Kahn. “If implementing regulations take the wrong course, however, it may undercut the way insurers pay for hospital services resulting in higher spending,” he said.

Both hospital groups highlighted more transparency for patient out-of-pocket costs and suggests the onus should be on payers to communicate information on cost-sharing and co-insurance.

Mollie Gelburd, associate director of government affairs at MGMA, which represents physician groups, said doctors don’t want to be in the position of explaining complex insurance terms and rules to a patient.

“While physicians should be encouraged to talk to patients about costs, to unnecessarily have them be doing all this education when they should be doing clinical care, that sort of gets concerning,” she said.

Practices are more concerned about payer provider directories and their accuracy, something not addressed in the executive order. Not having that type of information can be detrimental for a patient seeking care and further regulation in the area could help, Gelburd said.

Regardless, providers will likely view with frustration any regulations that increase their reporting and paperwork burdens, she said.

“I think the efficacy of pricing transparency and reducing healthcare costs, the jury is still out on that,” she said. “But if you have that onerous administrative requirement, that’s certainly going to drive up costs for those practices, especially those smaller practices.”

Payer lobby America’s Health Insurance Plans was quick to voice its opposition to the order.

CEO Matt Eyles said in a statement disclosing privately negotiated rates would “reduce incentives to offer lower rates, creating a floor — not a ceiling — for the prices that hospitals would be willing to accept.” He argued that current tools payers use to inform patients of cost expectations, such as cost calculators, are already offering meaningful help.

AHIP also said the order works against the industry’s efforts to shift to paying for quality instead of quantity. “Requiring price disclosure for thousands of hospital items, services and procedures perpetuates the old days of the American health care system paying for volume over value,” he said. “We know that is a formula for higher costs and worse care for everyone.”

Limited effects

One potential effect of making rates public is that prices would eventually trend toward equalization. That wouldn’t necessarily reduce costs, however, and could actually increase them for some patients. A payer able to negotiate a favorable rate for a specific patient population in a specific geographic area might lose that advantage, for example, Christopher Holt, director of healthcare policy at the conservative leaning American Action Forum, told Healthcare Dive.

John Nicolaou of PA Consulting told Healthcare Dive consumers will need help deciphering whatever information is made available however. Reams of data could offer the average patient little to no insight without payer or third-party tools to analyze and understand the information.

“It starts the process, just publishing that information and just making it available,” he said. “It’s got to be consumable and actionable, and that’s going to take a lot more time.”

The order does require the information being made public be “easy-to-understand” and able to “meaningfully inform patients’ decision making and allow patients to compare prices across hospitals.” That’s far easier said than done, however, Harvard’s Mehrotra said. “We haven’t seen anybody able to put this information in a usable way that patients are able to effectively act upon,” he said.

Holt said patients are also limited in their ability to shop around for healthcare, considering they often have little choice in what insurance company they use. People with employer-based plans typically don’t have the option to switch, and those in the individual market can only do so once a year.

Another aspect to consider is the limited reach of the federal government. CMS can require providers and payers in the Medicare Advantage program, for example, to meet price transparency requirements, but much of the licensing and regulations for payer and providers comes at the state level.

Waiting for details, lawsuits

One of the biggest questions for payers and providers in the wake of Monday’s announcement is how far exactly the rulemaking from HHS will go in mandating transparency. One one end, the requirements could stick close to giving patients information about their expected out-of-pocket costs without revealing the details of payer-provider negotiations. Full transparency, on the other hand, would mean publishing the now-secret negotiated rates for anyone to see.

“I think it’s the start of a much longer process,” Holt said. “It’s going to depend a lot on how much information is going to be required to be divulged and how that’s going to be collected.”

It’s almost certain that as soon as any concrete efforts at implementation are made, lawsuits will follow.

That’s what happened after Ohio passed a price transparency law in 2015 that required providers give patients information on out-of-pocket costs before a procedure — a proposal the executive order also puts forward.

The law still has not been enforced, as it has been caught up in the courts. The Ohio Hospital Association and Ohio State Medical Association sued over the law, arguing it was too vague and could lead to a delay in patient care.