Hospital consolidation continues to gather momentum across the country, with one state in particular, Pennsylvania, seeing more merger and acquisition activity than any other.

Here are seven hospital and health system deals announced or completed in Pennsylvania so far this year:

1. Risant Health, part of Kaiser Permanente,acquired Danville, Pa.-based Geisinger Health, a 10-hospital system, on March 31. Oakland, Calif.-based Kaiser said Risant plans to acquire four to five more community-based health systems over the next four to five years.

2. Washington (Pa.) Health, a two-hospital system, joined Pittsburgh-based UPMC in June. UPMC will invest at least $300 million over the next 10 years to improve services at the two hospitals, which have been rebranded as UPMC Washington and UPMC Greene hospitals.

3. WellSpan Healthacquired Lewisburg, Pa.-based Evangelical Community Hospital, effective July 8. York, Pa.-based WellSpan now includes eight hospitals and more than 21,000 team members, including 2,000 employed providers.

4. Philadelphia-based Jefferson Health and Allentown, Pa.-based Lehigh Valley Health Network merged Aug. 1. The combination created one of the 15 largest nonprofit health systems in the U.S., with 32 hospitals and more than 700 sites of care.

5. Doylestown (Pa.) Health and Philadelphia-based University of Pennsylvania Health System in August signed a definitive agreement for Doylestown to become part of Penn Medicine, a six-hospital system. Pending final federal and state approvals, the systems aim to integrate clinical care and operations by early 2025

6. Franklin, Tenn.-based Community Health Systemsplans to sell its three Pennsylvania hospitals to nonprofit organization WoodBridge Healthcare. The $120 million deal is anticipated to close in the fourth quarter.

7. Los Angeles-based Prospect Medical Holdings and CHA Partnerssigned a letter of intent in August for CHA to acquire Upland, Pa.-based Crozer Health. The proposed deal would involve transitioning Crozer’s four hospitals back to nonprofit status. CHA, which owns five hospitals in New Jersey, is working to reach a definitive agreement for the acquisition of Crozer.

Here are 67 health systems with strong operational metrics and solid financial positions, according to reports from credit rating agencies Fitch Ratings and Moody’s Investors Service released in 2024.

AdventHealth has an “AA” rating and stable outlook with Fitch. The rating is based on the Altamonte Springs, Fla.-based system’s competitive market position—especially in its core Florida markets—and its financial profile, Fitch said.

Advocate Health members Advocate Aurora Health and Atrium Health have “Aa3” ratings and positive outlooks with Moody’s. The ratings are supported by the Charlotte, N.C.-based system’s significant scale, strong market share across several major metro areas, and good financial performance and liquidity, Moody’s said.

AnMed Health has an “AA-” rating and stable outlook with Fitch. The rating reflects the Anderson, S.C.-based system’s strong and stable operating performance and leading market position in a sound service area, Fitch said.

Ann & Robert H. Lurie Children’s Hospital of Chicago has an “AA” rating and stable outlook with Fitch. The rating is supported by the system’s strong balance sheet with low leverage ratios derived from modest debt, Fitch said.

Atlantic Health System has an “Aa3” rating and stable outlook with Moody’s. The rating reflects the Morristown, N.J.-based system’s fundamental strengths, including strong operating performance with high single digit operating cash flow margins and favorable liquidity of over 300 days cash on hand, Moody’s said.

Avera Health has an “AA-” rating and a stable outlook with Fitch. The rating reflects the Sioux Falls, S.D.-based system’s strong operating risk and financial profile assessments, and significant size and scale, Fitch said.

BayCare Health System has an “AA” rating and stable outlook with Fitch. The Clearwater, Fla.-based system on June 30 moved to a new corporate legal structure, replacing a joint operating agreement between multiple hospitals that were responsible for the creation of BayCare in 1997. Fitch views the dissolution of the JOA and the move to the new structure as a credit positive.

Beacon Health System has an “AA-” rating and stable outlook with Fitch. Fitch said the rating reflects the strength of the South Bend, Ind.-based system’s balance sheet.

Bon Secours Mercy Health has an “AA-” rating and stable outlook with Fitch. The Cincinnati-based system has a favorable and stable payor mix, leading or secondary market share position in nine of its 11 U.S. markets with improving market share positions in eight, and adequate cash flows to support the system’s strategic plans, Fitch said.

BJC Health System has an “Aa2” rating and stable outlook with Moody’s. The St. Louis-based system reflects its reputation as a leading academic medical center with a long-standing affiliation with Washington University School of Medicine, Moody’s said.

Carle Health has an “AA-” rating and stable outlook with Fitch. The rating reflects the Urbana, Ill.-based system’s distinctly leading market position over a broad service area and Fitch’s expectation that the system will sustain its strong capital-related ratios in the context of the system’s midrange revenue defensibility and strong operating risk profile assessments.

Carilion Clinic has an “Aa3” rating and stable outlook with Moody’s. The rating reflects the Roanoke, Va.-based system’s scale, regional significance as a tertiary referral system with broad geographic capture, and a highly integrated physician base with a well-defined culture, Moody’s said.

Cedars-Sinai Health System has an “AA-” rating and a stable outlook with Fitch. The rating reflects the Los Angeles-based system’s consistent historical profitability and its strong liquidity metrics, historically supported by significant philanthropy, Fitch said.

Children’s Health has an “Aa3” rating and stable outlook with Moody’s. The rating reflects the Dallas-based system’s continued strong performance from a focus on high margin and tertiary services, as well as a distinctly leading market share, Moody’s said.

Children’s Hospital Medical Center of Akron (Ohio) has an “Aa3” rating and stable outlook with Moody’s. The rating reflects the system’s large primary care physician network, long-term collaborations with regional hospitals, and leading market position as its market’s only dedicated pediatric provider, Moody’s said.

Children’s Hospital of Orange County has an “AA-” rating and a stable outlook with Fitch. The rating reflects the Orange, Calif.-based system’s position as the leading provider for pediatric acute care services in Orange County, a position solidified through its adult hospital and regional partnerships, ambulatory presence, and pediatric trauma status, Fitch said.

Children’s Minnesota has an “AA” rating and stable outlook with Fitch. The rating reflects the Minneapolis-based system’s strong balance sheet, robust liquidity position, and dominant pediatric market position, Fitch said.

Cincinnati Children’s Hospital Medical Center has an “Aa2” rating and stable outlook with Moody’s. The rating is supported by its national and international reputation in clinical services and research, Moody’s said.

Cleveland Clinic has an “Aa2” rating and stable outlook with Moody’s. The rating reflects the system’s strength as an international brand in highly complex clinical care and research and centralized governance model, the ratings agency said.

Cook Children’s Medical Center has an “Aa2” rating and stable outlook with Moody’s. The ratings agency said the Fort Worth, Texas-based system will benefit from revenue diversification through its sizable health plan, large physician group, and an expanding North Texas footprint.

Corewell Health has an “Aa3” rating and stable outlook with Fitch. The rating reflects the Grand Rapids and Southfield, Mich.-based system’s significant scale as a provider and payer in Michigan, Moody’s said. The organization also has good and stable financial performance and liquidity.

El Camino Health has an “AA” rating and a stable outlook with Fitch. The rating reflects the Mountain View, Calif.-based system’s strong operating profile assessment with a history of generating double-digit operating EBITDA margins anchored by a service area that features strong demographics as well as a healthy payer mix, Fitch said.

Froedtert ThedaCare Health has an “AA” rating and stable outlook with Fitch. The rating reflects the Milwaukee-based system’s solid market position, track record of strong utilization and operations, and strong financial profile, Fitch said.

Hoag Memorial Hospital Presbyterian has an “AA” rating and stable outlook with Fitch. The Newport Beach, Calif.-based system’s rating is supported by its strong operating risk assessment, leading market position in its immediate service area, and strong financial profile, Fitch said.

Holland (Mich.) Hospital has an “AA-” rating and stable outlook with Fitch. The rating reflects Holland Hospital’s stable and strong liquidity and capital-related metrics despite sector-wide operating pressures, Fitch said.

Indiana University Health has an “AA” rating and stable outlook with Fitch. The rating reflects the Indianapolis-based health system’s sustained track record of strong operating margins, ratings agency said.

Inova Health System has an “Aa2” rating and stable outlook with Moody’s. The Falls Church, Va.-based system’s rating is anchored by its role as one of the largest health systems in Virginia with a leading market position in a rapidly growing region with unusually high commercial business, Moody’s said.

Inspira Health has an “AA-” rating and stable outlook with Fitch. The rating reflects Fitch’s expectation that the Mullica Hill, N.J.-based system will return to strong operating cash flows following the operating challenges of 2022 and 2023, as well as the successful integration of Inspira Medical Center of Mannington (formerly Salem Medical Center).

JPS Health Network has an “AA” rating and stable outlook with Fitch. The rating reflects the Fort Worth, Texas-based system’s sound historical and forecast operating margins, the ratings agency said.

Kaiser Permanente has an “AA-” rating and stable outlook with Fitch. The Oakland, Calif.-based system’s rating is driven by its strong financial profile, bolstered by a large and diversified revenue base, Fitch said.

Mass General Brigham has an “Aa3” rating and stable outlook with Moody’s. The rating reflects the Somerville, Mass.-based system’s strong reputation for clinical services and research at its namesake academic medical center flagships that drive excellent patient demand and help it maintain a strong market position, Moody’s said.

Mayo Clinic has an “Aa2” rating and stable outlook with Moody’s. The rating reflects the Rochester, Minn.-based system’s preeminent reputation for clinical care and research, including new discoveries and cutting-edge treatment, Moody’s said.

McLaren Health Care has an “AA-” rating and stable outlook with Fitch. The rating reflects the Grand Blanc, Mich.-based system’s leading market position over a broad service area covering much of Michigan, the ratings agency said.

McLeod Health has an “AA-” rating and stable outlook with Fitch. The Florence, S.C.-based system maintains a leading and growing market position in its primary service area and is expanding the Carolina’s Forest campus in an area that is expected to experience rapid growth over the coming years, Fitch said.

Med Center Health has an “AA-” rating and stable outlook with Fitch. The rating reflects the Bowling Green, Ky.-based system’s strong operating risk assessment and leading market position in a primary service area with favorable population growth, Fitch said.

Memorial Healthcare System has an “Aa3” rating and stable outlook with Moody’s. Moody’s said the rating reflects that the Hollywood, Fla.-based system will continue to benefit from good strategic positioning of its large, diversified geographic footprint.

Memorial Hermann Health System has an “Aa3” rating and stable outlook with Moody’s. The rating reflects the Houston-based system’s leading and expanding market position and strong demand in a growing region, Moody’s said.

Methodist Health System has an “Aa3” rating and stable outlook with Moody’s. Moody’s said the rating reflects the Dallas-based system’s consistently strong operating performance, excellent liquidity, and very good market position.

Monument Health has an “AA-” rating and stable outlook with Fitch. The ratings agency said the Rapid City, S.D.-based system has a dominant inpatient market position as the leading acute care provider in its geographically broad primary service area

Nationwide Children’s Hospital has an “Aa2” rating and stable outlook with Moody’s. The rating reflects the Columbus, Ohio-based system’s strong market position in pediatric services, growing statewide and national reputation, and continued expansion strategies.

Nicklaus Children’s Hospital has an “AA-” rating and stable outlook with Fitch. The rating is supported by the Miami-based system’s position as the “premier pediatric hospital in South Florida with a leading and growing market share,” Fitch said.

North Mississippi Health Services has an “AA” rating and stable outlook with Fitch. The rating reflects the Tupelo-based system’s strong cash position and strong market position with a leading market share in its primary services area, Fitch said.

Northwestern Memorial HealthCare has an “Aa2” rating and stable outlook with Moody’s. The rating reflects the Chicago-based system’s growing market position, single operating model and financial discipline, Moody’s said.

Novant Health has an “AA-” rating and stable outlook with Fitch. The ratings agency said the Winston-Salem, N.C.-based system’s recent acquisition of three South Carolina hospitals from Dallas-based Tenet Healthcare will be accretive to its operating performance as the hospitals are highly profited and located in areas with growing populations and good income levels.

Oregon Health & Science University has an “Aa3” rating and stable outlook with Moody’s. The rating reflects the Portland-based system’s top-class academic, research, and clinical capabilities, Moody’s said.

Orlando (Fla.) Health has an “AA-” rating and stable outlook with Fitch. The rating reflects the health system’s strong and consistent operating performance and a growing presence in a demographically favorable market, Fitch said.

Parkland Health has an “AA-” rating and stable outlook with Fitch. The rating reflects Fitch’s expectation that the Dallas-based system will remain the leading provider of public (safety net) services in the vast Dallas County service area, supported by its tax levy.

Phoenix Children’s has an “AA-” rating and stable outlook with Fitch. The rating reflects the system’s strong cash flow generation that has significantly improved its balance sheet in recent years, Fitch said.

Presbyterian Healthcare Services has an “AA” rating and stable outlook with Fitch. The Albuquerque, N.M.-based system’s rating is driven by a strong financial profile combined with a leading market position with broad coverage in both acute care services and health plan operations, Fitch said.

Rady Children’s Hospital has an “Aa3” rating and stable outlook with Moody’s. The San Diego-based system’s rating reflects its well-established strengths, including an “extremely high” market share in all of San Diego County, Moody’s said.

Rush University System for Health has an “AA-” rating and stable outlook with Fitch. The rating reflects the Chicago-based system’s strong financial profile and an expectation that operating margins will rebound despite ongoing macro labor pressures, the rating agency said.

Saint Francis Healthcare System has an “AA” rating and stable outlook with Fitch. The rating reflects the Cape Girardeau, Mo.-based system’s strong financial profile, characterized by robust liquidity metrics, Fitch said.

Saint Luke’s Health System has an “Aa2” rating and stable outlook with Moody’s. The Kansas City, Mo.-based system’s rating was upgraded from “A1” after its merger with St. Louis-based BJC HealthCare was completed in January.

Salem (Ore.) Health has an “AA-” rating and stable outlook with Fitch. The rating reflects the system’s dominant marketing position in a stable service area with good population growth and demand for acute care services, Fitch said.

Sarasota (Fla.) Memorial Health Care System has an “AA-” rating and stable outlook with Fitch. The rating reflects the system’s leading market position in a growing service area, robust historical operating cash flow levels and strong liquidity position, Fitch said.

Seattle Children’s Hospital has an “AA” rating and a stable outlook with Fitch. The rating reflects the system’s strong market position as the only children’s hospital in Seattle and provider of pediatric care to an area that covers four states, Fitch said.

SSM Health has an “AA-” rating and stable outlook with Fitch. The St. Louis-based system’s rating is supported by a strong financial profile, multistate presence and scale with good revenue diversity, Fitch said.

St. Elizabeth Medical Center has an “AA” rating and stable outlook with Fitch. The rating reflects the Edgewood, Ky.-based system’s strong liquidity, leading market position, and strong financial management, Fitch said.

St. Tammany Parish Hospital has an “AA-” rating and stable outlook with Fitch. The Covington, La.-based system has a strong operating risk assessment and very strong financial profile supported by consistently robust operating cash flows, Fitch said.

Stanford Health Care has an “Aa3” rating and positive outlook with Moody’s. The rating reflects the Palo Alto, Calif.-based system’s clinical prominence, patient demand, and its location in an affluent and well-insured market, Moody’s said.

UChicago Medicine has an “AA-” rating and stable outlook with Fitch. The rating reflects the system’s strong financial profile in the context of its broad and growing reach for high-acuity services, Fitch said.

University Health has an “AA+” rating and stable outlook with Fitch. The San Antonio-based system’s outlook is based on the Bexar County Hospital District’s significant tax margin, good cost management, and strong leverage position relative to its liquidity and outstanding debt.

University of Colorado Health has an “AA” rating and stable outlook with Fitch. The Aurora-based system’s rating reflects a strong financial profile benefiting from a track record of robust operating margins and the system’s growing share of a growth market anchored by its position as the only academic medical center in the state, Fitch said.

University of Kansas Health System has an “AA-” rating and stable outlook with Fitch. The rating reflects Kansas City-based system’s flagship hospital’s important presence as the only academic medical center in Kansas and a major provider of many high end and unique services to a large geographic area, Fitch said.

UW Health has an “Aa3” rating and stable outlook with Moody’s. The rating reflects the Madison, Wis.-based system’s strong clinical reputation, high acuity services, and important role as the academic medical center affiliated with the state’s flagship public university, Moody’s said.

VCU Health has an “Aa3” rating and stable outlook with Moody’s. The rating reflects the Richmond, Va.-based system’s status as one of Virginia’s leading academic medical centers and essential role as its largest safety net provider, supporting excellent patient demand at high acuity levels, Moody’s said.

Willis-Knighton Medical Center has an “AA-” rating and positive outlook with Fitch. The outlook reflects the Shreveport, La.-based system’s improving operating performance relative to the past two fiscal years combined with Fitch’s expectation for continued improvement in 2024 and beyond.

The New Jersey–based real estate firm has a record of buying, stabilizing and selling struggling hospitals, but at least one organization with a history with the company says they’re skeptical about CHA saving health care in Delco.

“It’s really just shocking that both CHA and another community would be interested in going down the same road that we’ve gone [down],” said Paul DiLorenzo, executive director of the Salem Health and Wellness Foundation.

Since its founding in 2008, CHA Partners has acquired and turned around five hospitals in New Jersey. The list includes the Barnert Medical Arts Complex in Paterson, the Greenville Medical Arts Complex in Jersey City, the William B. Kessler Medical Arts Complex in Hammonton and the Muhlenberg Medical Arts Complex in Plainfield.

The fifth and most recent hospital project involved the 2019 acquisition and revival of Salem Medical Center, formerly known as Memorial Hospital of Salem County. The hospital was on the brink of closure after years of a shrinking patient population and aging infrastructure.

“CHA offered to take over the hospital, but needed local support as a part of the initial investment,” DiLorenzo said.

Salem Health and Wellness Foundation, a nonprofit organization that supports public health and social services programs in the community, agreed to step in.

According to court documents, the foundation gave Salem Medical Center and CHA Partners about $39 million in grants and loans to save the local hospital.

The majority of the loan balances were forgiven and the Salem community foundation sued CHA Partners to recoup the rest. They won in court this past May, but DiLorenzo said the foundation has yet to receive any payments.

Now, as the real estate firm moves to acquire another hospital system — Crozer Health in Delco — DiLorenzo said anger “is an understatement.”

“It’s astounding to us that CHA would be negotiating to do that when they’re not doing anything in good faith to pay the bills that are owed to us and to make the people of Salem County whole again,” he said.

CHA Partners declined to comment on its pending deal with Crozer Health or its standing with Salem Health and Wellness Foundation, which was involved with just the single hospital in Salem and not any of the other four New Jersey hospitals that CHA has acquired and stabilized.

CHA recently signed a letter of intent to purchase the hospital system from Crozer Health’s parent company, Prospect Medical Holdings.

The real estate firm would transition the health system from for-profit to nonprofit status, according to Crozer officials who announced the preliminary, nonbinding deal to staff last week. Prospect will work with CHA over the next few months to complete a transfer of ownership, but until then, there are no guarantees of a completed sale.

Prospect and Crozer officials declined to comment specifically on CHA’s history with the hospital in Salem, New Jersey, and the Salem Health and Wellness Foundation. But in an announcement to staff, Crozer leadership described CHA as a company committed to “preserving health care and jobs in the communities it serves” and turning around hospitals, with “each dedicated to providing exceptional care to local residents.”

Following the recent news of a potential new buyer for the Crozer Health system, Pennsylvania state Sen. Tim Kearney released a statement Thursday with concerns about the potential deal.

“The health and well-being of our constituents in Delaware County must be the top priority,” Kearney said. “I am calling on the Attorney General to conduct a thorough analysis of this acquisition. CHA’s track record must be carefully examined to determine if it is indeed a responsible and suitable buyer that will prioritize the health care needs of our community.”

After their experience in Salem County, DiLorenzo echoed those precautions. And while he blames CHA for failing to pay his foundation back, he said this is all a symptom of widespread challenges facing the United States health care industry.

“Poor communities, poor rural communities in particular, are really struggling to make the equation of all this work,” DiLorenzo said. “You have low insurance reimbursement rates, you don’t have the number of people to create a volume, you have health care systems that you know are trying to make the investment in communities, but they can’t make the numbers work. So, this is something that’s bigger than just Salem or just Delaware County.”

WHYY News first reported last month that Prospect had found a potential buyer, but the identity of CHA Partners was not revealed until this past week. Prospect had also asked Pennsylvania officials for $100 million to $500 million in state funds to help finance the deal.

As state hospital association leaders assemble in Big Sky, Montana this week, the environment for hospital-friendly legislation is threatening at best:

The public’s trust in hospitals has eroded. Hospital financial performance is a mixed bag: some are profitable and many aren’t. Congress thinks hospitals need more regulation to increase price transparency, require ownership disclosure, verify community benefits that justify tax exemptions and impose restrictions on hospital private equity investments. And programs through which state and federal health policies are authorized—HHS, CMS, FTC, FDA, CMMI et al—are in limbo as a result of the June 28, 2024 Chevron ruling by the Supreme Court.

At a federal level, the American Hospital Association has successfully fended-off a significant portion of proposed cuts to key programs (DSH, rural), delayed Congressional action against facility fees and site neutral payments, influenced improvement from April’s proposed 2025 Medicare rate from 2.6% to 2.9%, advanced legislation to protect healthcare workers and streamline prior authorization business practices by insurers. In most cases, it has pursued a unified agenda alongside its Coalition (America’s Essential Hospitals, the Federation of American Hospitals, the Catholic Health Association and the Association of American Medical Colleges , Children’s Hospital Association et al) and it has invested heavily in its lobbying: $6.46 million in the second quarter 2024 (plus $4.1 million by HCA, AAMC, Tenet and others).

At the state level, the attention hospitals get is equally intense but more complicated: It starts with money and demand: Examples:

State resources: 9 states don’t tax any income, regardless of the source (AL, FL, NV, NH, TN, SD, TX, WA, WY); 4 states don’t tax any retirement income: (IL, IA, MS, PA); 8 states tax social security benefits (CO, MN, MT, NM, RI, UT, VT, WV)

Population health status: WalletHub used 44 measures to assess each state and the District of Columbia on healthcare cost, access, and outcomes. WalletHub weighted the three categories equally. The Top 5: MN, RI, SD, IA, NH; the bottom 5: MS, AL, WV, GA, OK

There are Blue and Red states. Some are growing and some declining. All are integrating more diverse populations and divergence between low- and high-income household financial security and spending. The health system, and its hospitals, impact all.

Healthcare spending for state employees, Medicaid and dual eligible enrollees and public health programs consume a third or more of total state spending. And actions taken in states vis a vis ballot referenda, executive orders, administrative agency rulings and legislative actions result in wide variance in the regulatory environments for hospitals. Consider:

32 states have passed legislation to lower health system costs

31 states have CON requirements (24 of these have been revised since 2021).

15 states have passed laws to reduce or eliminate facility fees including hospitals

17 have passed legislative to increase competition in healthcare

23 passed legislation to reduce surprise medical bills

9 have passed legislation to address community benefit declarations by NFP hospital and health systems.

9 have passed legislation to reduce insurer prior authorization obstacles.

13 passed legislation involving reference pricing requirements for hospitals

8 states passed legislation requiring minimal levels of primary care services

24 modified their Certificate of Need programs

3 states have all-payer payment policies.

8 states have drug price control commissions/mechanisms to limit price increases.

And all are grappling with determinations about abortion services, drug formulary design for Medicaid, state health employee health costs, Medicaid eligibility and funding, staffing requirements in hospitals and nursing homes, rural health solvency, telehealth efficacy, insurer plan design restrictions, and scope of practice expansion for nurse practitioners, pharmacists and much more.

The advocacy environment for hospitals at the state and federal levels will be dicier going forward: the near-term macro-environment is unwelcoming for hospitals presumed to have returned to profitability after the pandemic.

It’s root in four convergent issues:

Economic Uncertainty: Last week’s BLS jobs report signaled softening of the economy and alarmed some thinking it a harbinger of a possible recession.

Middle East Tension: the Israeli-Palestinian conflict appears headed toward a broader regional conflict involving Lebanon, Iran and others.

Campaign 2024: hyper-partisanship coupled with disinformation on both sides lends to voter unrest: healthcare affordability, price transparency, consolidation, executive compensation and inequity are ripe targets.

Healthcare Workforce Disenchantment (including Physicians): Hospitals directly employ half of the physician workforce and 30% of total health industry employment. Labor-management tension in hospitals is mounting.

For hospitals, effective advocacy is imperative: the reservoir of good will enjoyed for decades is evaporating. Advertising “we’re there for you” is timely as rural providers need a lifeline, and public castigation of “corporate insurers and billionaire critics” necessary to rally supporters.

But beyond these, two things are clear:

The marketplace for “hospitals” is fundamentally different than the past requiring a clearer value proposition and fresh messaging.

And in states, hospitals will encounter unique opportunities and challenges in plotting strategies for their future. No two are alike.

Big Sky is a symbolic locale for this week’s meeting of state health executives: the Big Sky over hospitals is cloudy.

Some of America’s largest hospital systems saw their financials soar in the first half of 2024. And yet, more than 700 facilities across the country still are at risk of closing.

Why it matters:

It’s a familiar tale of the rich getting richer, as big, mostly for-profit health systems see improved margins while smaller facilities in outlying areas are barely hanging on.

That could worsen access for some of the most vulnerable Americans — and hasten consolidation in an industry that’s been a magnet for M&A.

The big picture:

Health systems with big footprints, including large academic medical centers, have weathered the pandemic and economic headwinds and are seeing margins as good or better than before COVID-19.

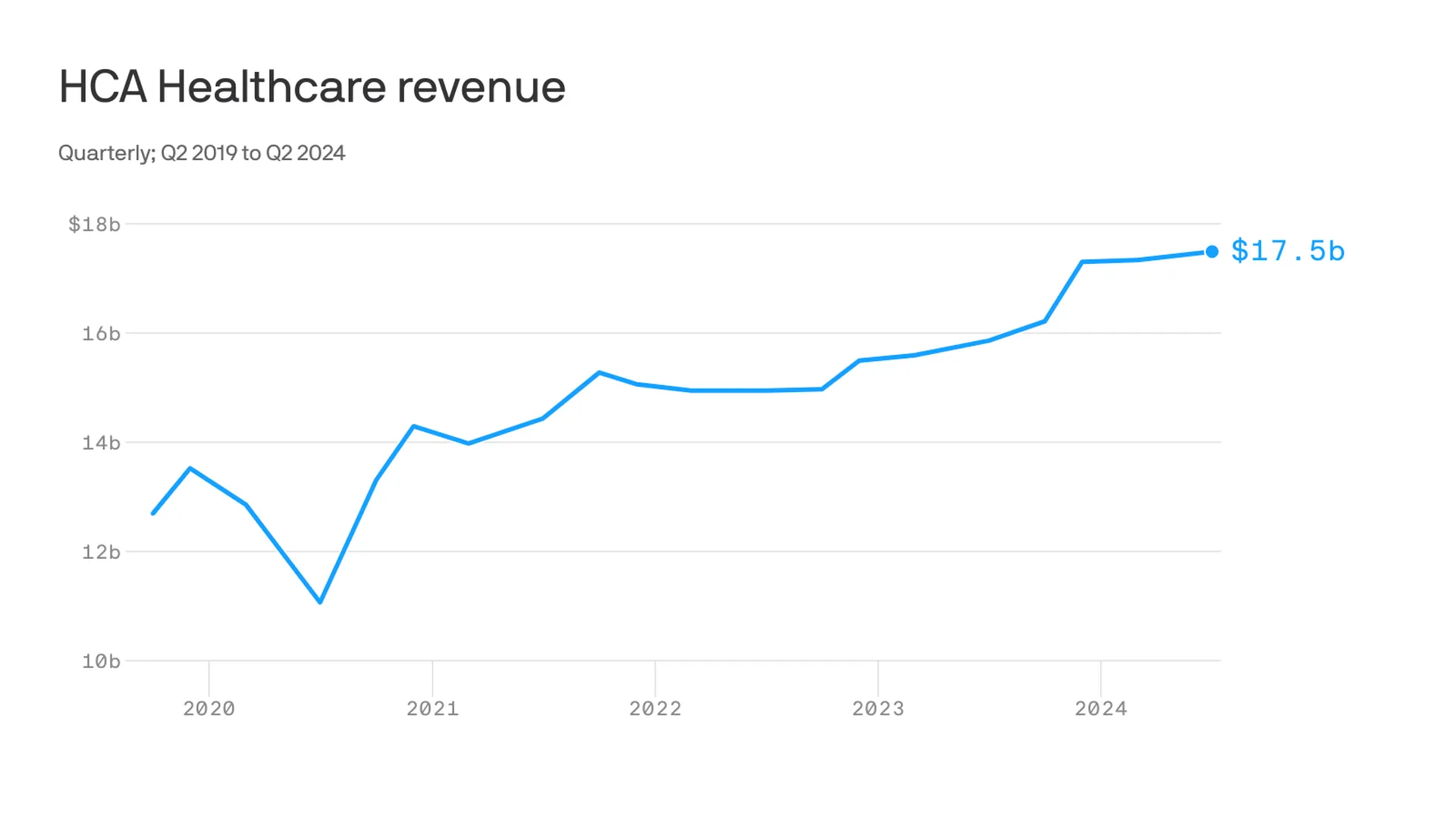

Nashville-based industry behemoth HCA Healthcare posted 23% year-over-year profit growth for the quarter, revising its forecast for the rest of the year, projecting it’ll reach as much as $6 billion. It posted a 10% year-over-year increase in revenue.

King of Prussia, Pennsylvania-based Universal Health Services similarly reported a strong quarter, posting nearly 69% growth on its bottom line over the same period last year while Dallas-based Tenet Healthcare reported a 111% jump in its net income over the same quarter last year.

Yes, but:

Smaller nonprofit hospitals, especially in rural areas, that made it through the crisis with the help of government aid are paring services like maternity wards and struggling to stay open.

“There are a lot of hospitals that survived, but their balance sheets are so weakened, their margin for error is basically zero at this point,” said Mike Eaton, senior vice president of strategy at population health company Navvis.

Hospitals that once could manage their expenses and the needs of communities are “going to really struggle to invest in what comes next,” he said.

Between the lines:

The biggest health systems have benefited from less volatility, seeing stabilizing drug prices and more predictable supply chains and labor costs, per a new report from Strata Decision Technology.

“It’s at least something you can manage to,” Steve Wasson, Strata’s chief data and intelligence officer, told Axios.

Revenues already were up thanks to renegotiated contracts health systems struck with payers last year, Wasson said.

There also have been changes on the federal side that boosted Medicare admissions and put some hospitals in line to be reimbursed for billions in underpayments from the 340B drug discount program.

Zoom in:

It’s all translated to operating margins that are up 17% year-to-date compared with the same time period in 2023, according to the latest Kaufman Hall National Hospital Flash Report.

Volumes as measured by hospital discharges per day are up 4% year-to-date.

Expenses per day are also up 6% year to date, including labor (4%), supplies (8%) and drugs (8%), but are far less volatile and thus easier to plan for, said Erik Swanson, senior vice president at Kaufman Hall.

But there’s a growing gulf between the top third of U.S. hospitals, which are seeing outsize growth, and the rest, Swanson said.

Threat level: A new report from the Center for Healthcare Quality and Payment Reform estimated 703 hospitals — or more than one-third of rural hospitals — are at risk of closure, based on Centers for Medicare and Medicaid Services financial information from July. Losses on privately insured patients are the biggest culprit.

“We’re looking at 50% of rural operating in the red. The situation is very challenging,” Michael Topchik, partner at Chartis Center for Rural Health, told Axios.

These smaller hospitals may still be there, but there will continue to be a steady erosion of the kinds of services they offer, such as obstetrics, cancer care and general surgery, he said.

What’s next:

Private equity investment in rural health care is already booming and with it, prospects for service and staffing cuts.

The South generally has the highest concentration of private equity-owned rural hospitals, often with lower patient satisfaction and fewer full-time staff compared with non-acquired hospitals, according to the Private Equity Stakeholder Project.

Congress is ramping up oversight of private equity investments in the sector, though most lawmakers are loath to take steps to actually halt deals.

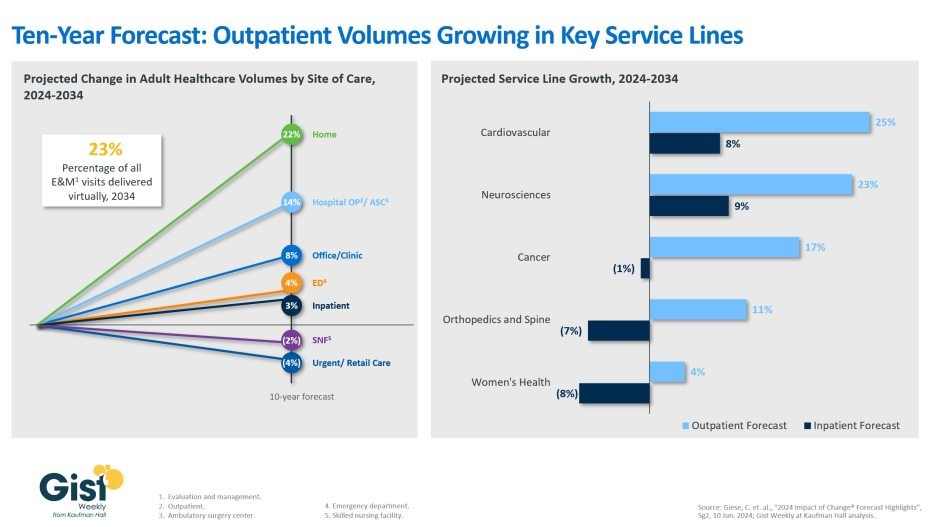

Using the latest data forecast from Sg2, a Vizient company, the graphic above illustrates how the outpatient shift will continue to accelerate through 2034.

Home-based care and outpatient services, including ambulatory surgery centers, are projected to be the fastest growing care sites over the next decade, with volumes increasing 22% and 14% respectively.

Sg2 forecasts that physician offices, emergency departments, and inpatient settings will experience more modest volumes increases, whereas skilled nursing facilities and retail care volumes are predicted to decline.

Additionally, although the initial outpatient procedural shift was largely focused on orthopedics, the next wave of outpatient volume growth will come from other service lines.

Driven by regulatory changes, as well as patient demand, outpatient cardiovascular volumes are expected to increase by 25% over the next decade, closely followed by neurosciences at 23%.

Continued health system investment into higher-acuity outpatient care remains crucial.

Over the weekend, President Biden called it quits and Democrats seemingly coalesced around Vice President Harris as the Party’s candidate for the White House. While speculation about her running mate swirls, the stakes for healthcare just got higher. Here’s why:

A GOP View of U.S. Healthcare

Republicans were mute on their plans for healthcare during last week’s nominating convention in Milwaukee. The RNC healthcare platform boils down to two aims: ‘protecting Medicare’ and ‘granting states oversight of abortion services. Promises to repeal and replace the Affordable Care Act, once the staple of GOP health policy, are long-gone as polls show the majority (even in Red states (like Texas and Florida) favor keeping it. The addition of Ohio Senator JD Vance to the ticket reinforces the party’s pro-capitalism, pro-competition, pro-states’ rights pitch.

To core Trump voters and right leaning Republicans, the healthcare industry is a juggernaut that’s over-regulated, wasteful and in need of discipline. Excesses in spending for illegal immigrant medical services ($8 billion in 2023), high priced drugs, lack of price transparency, increased out-of-pocket costs and insurer red tape stoke voter resentment. Healthcare, after all, is an industry that benefits from capitalism and market forces: its abuses and weaknesses should be corrected through private-sector innovation and pro-competition, pro-consumer policies.

A Dem View of Healthcare

By contrast, healthcare is more prominent in the Democrat’s platform as the party convenes for its convention in Chicago August 19. Women’s health and access to abortion, excess profitability by “corporate” drug manufacturers, hospitals and insurers, inadequate price transparency, uneven access and household affordability will be core themes in speeches and ads, with a promise to reverse the Dobb’s ruling by the Supreme Court punctuating every voter outreach.

Healthcare, to the Democratic-leaning voters is a right, not a privilege.

Its majority think it should be universally accessible, affordable, and comprehensive akin to Medicare. They believe the status quo isn’t working: the federal government should steward something better.

Here’s what we know for sure:

Foreign policy will be a secondary focus. The campaigns will credential their teams as world-savvy diplomats who seek peace and avoid conflicts. Nationalism vs. globalism will be key differentiator for the White House aspirants but domestic policies will be more important to most voters.

Healthcare reform will be a more significant theme in Campaign 2024 in races for the White House, U.S. Senate, U.S. House of Representatives and Governors. Dissatisfaction with the status quo and disappointment with its performance will be accentuated.

The White House campaigns will be hyper-negative and disinformation used widely (especially on healthcare issues). A prosecutorial tone is certain.

Given the consequence of the SCOTUS’ Chevron ruling limiting the role and scope of agency authority (HHS, CMS, FDA, CDC, et al), campaigns will feature proposed federal & state policy changes and potential Cabinet appointments in positioning their teams. Media speculation will swirl around ideologues mentioned as appointees while outside influencers will push for fresh faces and new ideas.

Consumer prices and inflation will be hot-button issues for pocketbook voters: the health industry, especially insurers, hospitals and drug companies, will be attacked for inattention to affordability.

Substantive changes in health policies and funding will be suspended until 2025 or later. Court decisions, Executive Orders from the White House/Governors, and appointments to Cabinet and health agency roles will be the stimuli for changes. Major legislative and regulatory policy shifts will become reality in 2026 and beyond. Temporary adjustments to physician pay, ‘blame and shame’ litigation and Congressional inquiries targeting high profile bad actors, excess executive compensation et al and state level referenda or executive actions (i.e. abortion coverage, price-containment councils, CON revisions et al) will increase.

Total healthcare spending, its role in the economy and a long-term vision for the entire system will not be discussed beneath platitudes and promises. Per the Congressional Budget Office, healthcare as a share of the U.S. GDP will increase from 17.6% today to 19.7% in 2032. Spending is forecast to increase 5.6% annually—higher than wages and overall inflation. But it’s too risky for most politicians to opine beyond acknowledgment that “they feel their pain.”

My take:

Regardless of the election outcome November 5, the U.S. healthcare industry will be under intense scrutiny in 2025 and beyond. It’s unavoidable.

Discontent is palpable. No sector in U.S. healthcare can afford complacency. And every stakeholder in the system faces threats that require new solutions and fresh voices.

Embattled Steward Health Care has canceled auctions for its hospitals in Ohio and Pennsylvania after it did not receive qualified bids for those facilities, according to a court filing.

The health system said in a document filed Sunday with a bankruptcy court in Texas that it is working to determine alternatives for those facilities, and expects to make an announcement at a later date. It had initially set a bid deadline for June 24 for these assets, which was later pushed back to July 15.

The system did reveal that it found potential buyers for one facility in Arkansas and another in Louisiana. Pafford Health Systems bid on the Arkansas-based Wadley Regional Medical Center for $200,000, while AHS South LLC is seeking to buy Louisiana hospital Glenwood Regional Medical Center for $500,000.

The buyers would have to take on the facilities’ liabilities, but would not be held to a rental agreement with Medical Properties Trust, Steward Health Care’s landlord.

The bid deadlines have been pushed back as high-profile potential sales have fallen through. Optum, for instance, had signed on to buy Steward’s physician group before walking away from the deal amid mounting criticism from lawmakers and others.

A hearing over these potential sales will be held on July 31, according to the court filing.

Meanwhile, the Senate Health, Education, Labor and Pensions (HELP) committee will hold a bipartisan vote on Thursday to determine whether to subpoena Steward CEO Ralph de la Torre to compel him to speak at a hearing on the health system’s struggles in September.

The HELP Committee previously invited de la Torre to testify but he declined, according to a statement from Chair Bernie Sanders, I-Vt., and Ranking Member Bill Cassidy, R-La.

UC Davis Medical Center in Sacramento, Calif., has broken ground on a $3.74 billion expansion that includes a 14-story hospital tower and a five-story medical pavilion.

The new tower will add nearly 1 million square feet of space to the existing medical center. It will include new operating rooms, an imaging center, facilities for pharmacy and burn care units, and about 334 private patient rooms.

More than 250 of the rooms are being designed for greater flexibility in the event of a patient surge such as a pandemic, wildfire or other disaster. These will easily convert into intensive-care-unit rooms with air isolation to treat patients of any level of hospitalization.

“We are building into this new tower some of the lessons we learned from the recent pandemic. As an example, three out of four of the rooms in this new tower can be easily converted to fully functional ICUs if needed, tripling our ICU capacity,” UC Davis Health CEO David Lubarsky said in a July 22 news release.

The current, 646-bed hospital will have between 675 and 700 inpatient beds when the project is completed in 2030.

“This project further harnesses the advantages of UC Davis Medical Center being Sacramento’s No. 1 hospital and delivering nationally ranked care,” Mr. Lubarsky said. “UC Davis Health is Sacramento County’s second-largest employer, and we’re making sure we are bringing not only healthcare, but jobs and community wealth-building to our surrounding neighborhoods.”

Medicare Advantage provides health coverage to more than half of the nation’s seniors, but some hospitals and health systems are opting to end their contracts with MA plans over administrative challenges.

Among the most commonly cited reasons are excessive prior authorization denial rates and slow payments from insurers.

In 2023, Becker’s began reporting on hospitals and health systems nationwide that dropped some or all of their Medicare Advantage contracts.

In January, the Healthcare Financial Management Association released a survey of 135 health system CFOs, which found that 16% of systems are planning to stop accepting one or more MA plans in the next two years. Another 45% said they are considering the same but have not made a final decision. The report also found that 62% of CFOs believe collecting from MA is “significantly more difficult” than it was two years ago.

Fifteen health systems dropping Medicare Advantage plans in 2024:

1. Canton, Ohio-based Aultman Health System‘s hospitals will no longer be in network with Humana Medicare Advantage after July 1, and its physicians will no longer be in network after Aug. 1.

3. Munster, Ind.-based Powers Health (formerly Community Healthcare System) went out of network with Humana and Aetna’s Medicare Advantage plans on June 1.

6. York, Pa.-based WellSpan Health stopped accepting Humana Medicare Advantage and UnitedHealthcare Medicare Advantage plans on Jan. 1. UnitedHealthcare D-SNP plans in some locations are still accepted.

7. Newark, Del.-based ChristianaCare is out of network with Humana’s Medicare Advantage plans as of Jan. 1, with the exception of home health services.

8. Greenville, N.C.-based ECU Health stopped accepting Humana’s Medicare Advantage plans in January.

9. Zanesville, Ohio-based Genesis Healthcare System dropped Anthem BCBS and Humana Medicare Advantage plans in January.

10. Corvallis, Ore.-based Samaritan Health Services’ hospitals went out of network with UnitedHealthcare’s Medicare Advantage plans on Jan. 9. Samaritan’s physicians and provider services will be out of network on Nov. 1.