Renton, Wash.-based Providence had its second downgrade in less than a week amid higher expenses that helped lead to steeper-than-expected losses and an expectation of a multiyear recovery.

The rating downgrade from “A+” to “A” applies to the system’s long-term rating as well as to various bonds it holds, S&P Global said March 21. The outlook is negative.

“The negative outlook reflects our view of the steep operating losses that management must address over the next year to put the organization on a path to better cash flow and break-even margins,” S&P said.

The rating downgrade follows a similar move by Fitch March 17.

Positive fundamentals such as its diversified services and robust strategic plan, as well as its leading market positions in all seven of its regionally centered markets, stands Providence in good stead, S&P added.

Providence, a 51-hospital system, recently reported a fiscal 2022 operating loss of $1.7 billion.

Here are 14 health systems with strong operational metrics and solid financial positions, according to reports from credit rating agencies Fitch Ratings, Moody’s Investors Service and S&P Global.

1. Ascension has an “AA+” rating and stable outlook with Fitch. The St. Louis-based system’s rating is driven by multiple factors, including a strong financial profile assessment, national size and scale with a significant market presence in several key markets, which produce unique credit features not typically seen in the sector, Fitch said.

2. Berkshire Health has an “AA-” rating and stable outlook with Fitch. The Pittsfield, Mass.-based system has a strong financial profile, solid liquidity and modest leverage, according to Fitch.

3. ChristianaCare has an “Aa2” rating and stable outlook with Moody’s. The Newark, Del.-based system has a unique position with the state’s largest teaching hospital and extensive clinical depth that affords strong regional and statewide market capture, and it is expected to return to near pre-pandemic level margins over the medium term, Moody’s said.

4. Cone Health has an “AA” rating and stable outlook with Fitch. The rating reflects the expectation that the Greensboro, N.C.-based system will gradually return to stronger results in the medium term, the rating agency said.

5. Harris Health System has an “AA” rating and stable outlook with Fitch. The Houston-based system has a “very strong” revenue defensibility, primarily based on the district’s significant taxing margin that provides support for operations and debt service, Fitch said.

6. Johns Hopkins Medicine has an “AA-” rating and stable outlook with Fitch. The Baltimore-based system has a strong financial role as a major provider in the Central Maryland and Washington, D.C., market, supported by its excellent clinical reputation with a regional, national and international reach, Fitch said.

7. Orlando (Fla.) Health has an “AA-” and stable outlook with Fitch. The system’s upgrade from “A+” reflects the continued strength of the health system’s operating performance, growth in unrestricted liquidity and excellent market position in a demographically favorable market, Fitch said.

8. Rady Children’s Hospital has an “AA” rating and stable outlook with Fitch. The San Diego-based hospital has a very strong balance sheet position and operating performance and is also a leading provider of pediatric services in the growing city and tri-county service area, Fitch said.

9. Rush System for Health has an “AA-” and stable outlook with Fitch. The Chicago-based system has a strong financial profile despite ongoing labor issues and inflationary pressures, Fitch said.

10. Salem (Ore.) Health has an “AA-” rating and stable outlook with Fitch. The system has a “very strong” financial profile and a leading market share position, Fitch said.

11. TriHealth has an “AA-” rating and stable outlook with Fitch. The rating reflects the Cincinnati-based system’s strong financial and operating profiles, as well as its broad reach, high-acuity services and stable market position in a highly fragmented and competitive market, Fitch said.

12. UCHealth has an “AA” rating and stable outlook with Fitch. The Aurora, Colo.-based system’s margins are expected to remain robust, and the operating risk assessment remains strong, Fitch said.

13. University of Kansas Health System has an “AA-” rating and stable outlook with S&P Global. The Kansas City-based system has a solid market presence, good financial profile and solid management team, though some balance sheet figures remain relatively weak to peers, the rating agency said.

14. Willis-Knighton Health System has an “AA-” rating and stable outlook with Fitch. The Shreveport, La.-based system has a “dominant inpatient market position” and is well positioned to manage operating pressures, Fitch said.

This week, a health system CFO referenced the thoughts we shared last week about many hospitals rethinking physician employment models, and looking to pull back on employing more doctors, given current financial challenges. He said, “We’ve employed more and more doctors in the hope that we’re building a group that will allow us to pivot to total cost management.

But we can’t get risk, so we’ve justified the ‘losses’ on physician practices by thinking we’re making it up with the downstream volume the medical group delivers.

But the reality now is that we’re losing money on most of that downstream business. If we just keep adding doctors that refer us services that don’t make a margin, it’s not helping us.”

While his comment has myriad implications for the physician organization, it also highlights a broader challenge we’ve heard from many health system executives: a smaller and smaller portion of the business is responsible for the overall system margin.

While the services that comprise the still-profitable book vary by organization (NICU, cardiac procedures, some cancer management, complex orthopedics, and neurosurgery are often noted), executives have been surprised how quickly some highly profitable service lines have shifted. One executive shared, “Orthopedics used to be our most profitable service line. But with rising labor costs and most of the commercial surgeries shifting outpatient, we’re losing money on at least half of it.”

These conversations highlight the flaws in the current cross-subsidy based business model. Rising costs, new competitors, and a challenging contracting environment have accelerated the need to find new and sustainable models to deliver care, plan for growth and footprint—and find a way to get paid that aligns with that future vision.

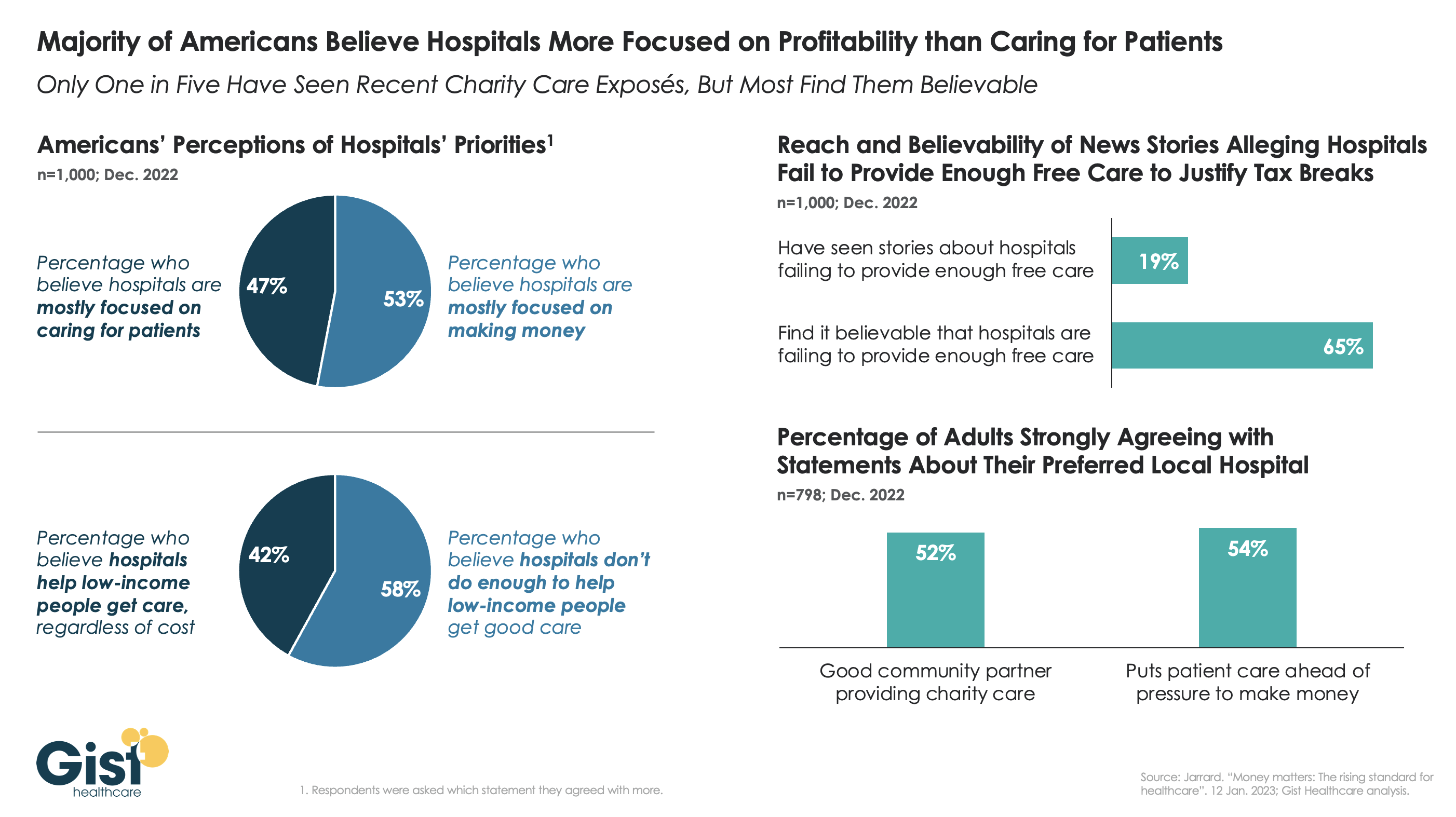

Health systems have recently been the subject of high-profile media accusations that they prioritize “profits over patients”, as an unflattering New York Times series has framed it.

New consumer survey data from strategic healthcare communications consulting firm Jarrard Inc. shows that while consumers find some merit in these claims, they tend to see their local hospital in a better light. As shown in the graphic above, a majority of US adults believe that, on a national level, hospitals are more focused on making money than caring for patients, and that they don’t do enough to help low-income people access high quality care.

Despite only one in five survey participants having seen news stories alleging hospitals fail to provide enough charity care in exchange for tax breaks, 65 percent of survey respondents find those allegations believable.

But while the consumer perception of hospitals may be suffering nationally, the responses were quite different when consumers were asked about their preferred local hospital. More than half strongly agreed that their preferred local hospital is a good community partner—one that puts patient care ahead of making money.

(Just as with Congress: people love to criticize the institution, while continuing to return their own representatives to Washington.) While the negative national attention can be disheartening, at the end of the day, to consumers,healthcare is local, and health systems must continue to build direct consumer relationships to strengthen patient loyalty.

Workforce problems in U.S. hospitals are troublesome enough for the American College of Healthcare Executives to devote a new category to them in its annual survey on hospital CEOs’ concerns. In the latest survey, executives identified “workforce challenges” as the No. 1 concern for the second year in a row.

Financial challenges, which consistently held the top spot for 16 years in a row until 2021, were listed the second-most pressing concern in the American College of Healthcare Executives’ annual survey.

Although workforce challenges were not seen as the most pressing concern for 16 years, they rocketed to the top quickly and rather universally for healthcare organizations in the past two years. Most CEOs (90 percent) ranked shortages of registered nurses as the most pressing within the category of workforce challenges, followed by shortages of technicians (83 percent) and burnout among non-physician staff (80 percent).

Here are the most concerning issues hospital CEOs ranked in 2022, along with the score of how pressing CEOs find each issue.

1. Workforce challenges (includes personnel shortages and staff burnout, among other issues) — 1.8

2. Financial challenges — 2.8

3. Behavioral health and addiction issues — 5.2

4. Patient safety and quality — 5.9

5. Governmental mandates — 5.9

6. Access to care — 6.0

7. Patient satisfaction — 6.6

8. Physician-hospital relations — 7.6

9. Technology — 7.7

10. Population health management — 8.6

11. Reorganization (mergers and acquisitions, partnerships and restructuring) — 8.7

Within financial challenges, most CEOs (89 percent) ranked increasing costs for staff and supplies as the most pressing, followed by operating costs (66 percent) and Medicaid reimbursement (63 percent). CEOs are less concerned about price transparency and moving away from fee-for-service.

Seventy-eight percent of CEOs ranked lack of appropriate facilities/programs as most pressing within the category of behavioral health and addiction issues. That was followed by lack of funding for addressing behavioral health and addiction issues (77 percent).

The results are based on a survey administered to CEOs of community hospitals (non-federal, short-term, non-specialty hospitals). ACHE asked respondents to rank 11 issues affecting their hospitals in order of how pressing they are. Results are based on responses from 281 executives.

Here is a summary of recent credit rating downgrades, going back to the last Becker’s roundup on Jan. 17.

Operating concerns and a bleak financial outlook for some resulted in the following changes:

Geisinger Health System (Danville, Pa.): Moody’s Investors Service downgraded Geisinger Health System’s outstanding bonds from “A1” to “A2” Feb. 13 amid expectations of continued cash flow weakness.

The outlook for the system, which has about $1.3 billion in debt, is stable.

Marshfield (Wis.) Clinic Health System: The system suffered a credit downgrade because of recent operating losses and amid expectations of no immediate financial improvement.

The S&P Global move Feb. 7 to downgrade the system to “BBB+” from “A-” follows a similar move from Fitch Jan. 18.

Marshfield signed a memorandum of understanding with Duluth, Minn.-based Essentia Health to discuss a potential merger Oct. 12 that would include 25 hospitals.

Tower Health (West Reading, Pa.): Troubled Tower Health, which is currently undergoing a strategic review and selling off several assets, suffered a rating downgrade on its bonds, S&P Global reported Feb. 6, adding that the outlook is negative.

“The downgrade reflects Tower Health’s significant ongoing operating losses that are expected to continue in fiscal 2023, and a steep decline in unrestricted reserves to a level that we view as highly vulnerable,” said S&P Global Ratings credit analyst Anne Cosgrove.

Fairview Health (Minneapolis): Moody’s Investors Service downgraded the revenue bond ratings of Fairview Health from “A3” to “Baa1.”

The downgrade reflects Moody’s projection that weak operating performance will be challenging to overcome due to increased labor costs and lower inpatient volume. Inflation and annual transfers to the University of Minnesota in Minneapolis will also hamper margins, Moody’s said.

Roseville, Calif.-based Adventist Health plans to go from seven networks of care to five systemwide to reduce costs and strengthen operations, according to a Feb. 15 news release shared with Becker’s.

Under the reorganization, Adventist Health will have separate networks for Northern California, Central California, Southern California, Oregon and Hawaii.

“Reducing the number of care networks strengthens our operational structure and broadens the meaning and purpose of our network model as well as the geographical span of one Adventist Health,” Todd Hofheins, COO of Adventist Health, said in the release. “This also reduces overhead and administrative costs.”

The reorganization will result in job cuts, including reducing administration by more than $100 million.

“Our commitment to rural and urban healthcare remains steadfast, and we are expanding to other locations to invest and transform the integrated delivery of care,” Kerry Heinrich, president and CEO of Adventist Health, said in the release.

Specifically, the health system has a recently approved affiliation agreement for Mid-Columbia Medical Center in The Dalles, Ore., to join Adventist Health, the health system said. The agreement is pending final regulatory and state approvals.

Meanwhile, Adventist Health filed a Worker Adjustment and Retraining Notification Act notice with California officials Feb. 15.

Adventist Health will eliminate job functions and positions for employees at its corporate office campus along with some remote roles, the notice states.

Layoffs from Adventist Health began Feb. 1 and will continue into April, according to the notice.

Adventist Health said it has provided all affected employees 60 days’ written notice of the layoff. The health system expects about 59 employees to be separated from employment with Adventist Health.

Employees affected by the layoffs include administrative directors, directors, managers and project managers, among others.

“We recognize that these changes impact people’s lives and want to respect each affected individual,” Joyce Newmyer, chief people officer for Adventist Health, said in the health system’s release. “We will make every effort to identify other opportunities for team members impacted.”

Chicago-based CommonSpirit Health, one of the largest healthcare systems in the country operating 138 hospitals in 21 states, has reported $451 million in operating losses for the six-month period ending Dec. 31.

Those figures compared with operating losses of $47 million for the same period in the prior year. Overall income for the second half of 2022 totaled a $213 million loss, but there was a gain of $200 million in the final quarter as stronger investment returns kicked in.

Staffing expenses continue to be a “major challenge,” CommonSpirit said. While salaries and benefits decreased $80 million in the final quarter, there was an overall increase of $140 million, or 1.7 percent, in such expenses over the second half of the year.

“We are meeting our challenges head on by scaling programs that drive growth, create a better experience for patients, and support our employees,” CFO Dan Morissette said in a statement. “At the same time we are working hard to reduce our costs so we can sustain these essential services in the long term.”

CommonSpirit estimated costs from its October cybersecurity event at approximately $150 million. The health system held $14.6 billion in debt as of Dec. 31.

Here are four health systems that recently had their credit rating upgraded by Fitch Ratings, Moody’s Investors Service or S&P Global Ratings:

1. Cooper University Health Care received upgrades from both S&P and Moody’s. S&P upgraded the Camden, N.J.-based system from “BBB+” to “A-,” praising Cooper for its focus on cost containment, revenue improvement, expanding market share and developing key services to gain more tertiary referrals and limit outpatient migration to Philadelphia academic medical centers.

Moody’s raised the system’s bond ratings from “Baa1” to “A3” and said it expects Cooper’s operating margins will be maintained through execution of its performance improvement plan and strong growth in key service lines.

2. Loma Linda (Calif.) University Medical Center’s rating was raised to “BB+” from “BB” by Fitch. “The upgrade … incorporates LLUMC’s major new hospital, which is now open, and the system has been operating in their new environment for more than one year, removing a considerable risk factor,” Fitch said in a report.

3. Mercy Health’s credit rating was upgraded from “A-” to “A” by Fitch. The rating agency said the Rockford, Ill.-based system’s operating profile is expected to remain strong in the longer term.

4. Orlando (Fla.) Health’s rating was upgraded to “AA-” from “A+” by Fitch. The ratings agency said in a report the bump “reflects the continued strength of OHI’s operating performance, growth in unrestricted liquidity and excellent market position in a demographically favorable market.”

Franklin, Tenn.-based Community Health Systems, one of the largest for-profit health systems in the country,reported $179 million net income in 2022, a 51.4 percent drop from the $368 million net income reported the prior year.

The drop was driven by a decline in net operating revenues, fewer inpatient admissions and what CHS termed “unfavorable changes” in payer mix.

Total operating costs and expenses for the year ended Dec. 31 were $11.4 billion, up from $11 billion in 2021. Net operating revenues were $12.2 billion in 2022, down slightly from $12.4 billion the prior year.

Net income in the final three months of the year totaled $446 million compared with $223 million in the same period in 2021.

“We were pleased with our progress during the final quarter of the year, including solid volume growth in admissions, adjusted admissions and surgeries,” CEO Tim Hingtgen said in a statement. “We also significantly reduced contract labor from its peak in early 2022 while improving overall employee recruitment and retention levels.”

CHS, which owns or leases 79 affiliated hospitals with approximately 13,000 beds and operates more than 1,000 sites of care, also released guidance for 2023, predicting annual revenues of between $12.2 billion and $12.6 billion. Such figures compare with $12.2 billion in 2022.

The system, which is also predicting a net loss in 2023 between 0.05 and 0.65 a share, recorded long-term debt of $11.6 billion as of Dec. 31 compared with $12.1 billion at the same time in 2021.