https://www.kaufmanhall.com/insights/blog/balance-sheet-bridge

Current Funding Environment

The healthcare financings that came in the past couple of weeks generally did well. Maturities seemed to do better than put bonds, and it remains important to pay attention to couponing and how best to navigate a challenging yield curve. But these are episodic indicators rather than trends, given that the scale of issuance remains muted. Other capital markets—like real estate—are becoming more active and offer competitive funding and different credit considerations relative to debt market options. Credit management continues to be the main driver of low external capital formation, but those looking for outside funding should spend time up front considering the full array of channels and structures.

This Part of the Crisis

And now it’s official. After JPMorgan acquired First Republic Bank—with a whole lot of help from the Federal Deposit Insurance Corporation—CEO Jamie Dimon declared, “this part of the crisis is over.” Not sure regional bank shareholders would agree, but from Mr. Dimon’s perspective the biggest bank got bigger, which made it a good day.

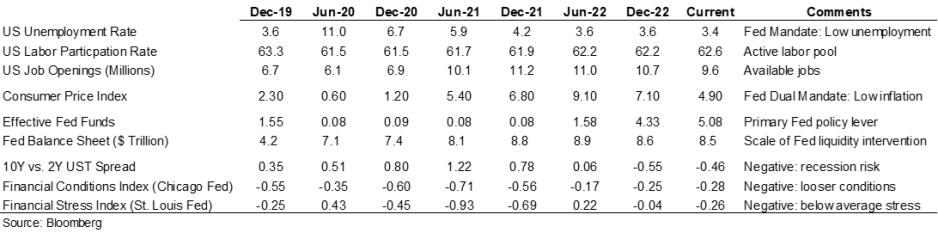

Last week the Federal Reserve raised rates another 25 basis points and the expectation (hope) seems to be that the Fed has reached the peak of its tightening cycle or will at least pause to see if constrictive forces like higher rates and regional bank balance sheet deflation slow activity enough to bring inflation back to the 2.0% Fed target. Assuming this is a pause point, it makes sense to check in on a few economic and market indicators.

Inflation is improving, although it remains well above the Fed’s 2.0% target range, and there are other indicators (like labor participation and unemployment) that have recovered some of the ground lost in 2020. But the weird part remains that this all seems quite civilized. To some, the Treasury curve spread continues to suggest a recession is looming, but in my neighborhood workers are still in short supply, restaurants are busy, and contractors are booked well into the future. Today’s ~3.36% 10-year Treasury rate is less than 100 basis points higher than the average since the start of the Fed interventionist era in 2008 and a whopping 257 basis points lower than the average since 1965. Think about how much capital has been raised in market environments much worse than now (including most of the modern-day healthcare inpatient infrastructure). Again, the main culprit in retarded capital formation is institutional credit management concerns rather than the funding environment.

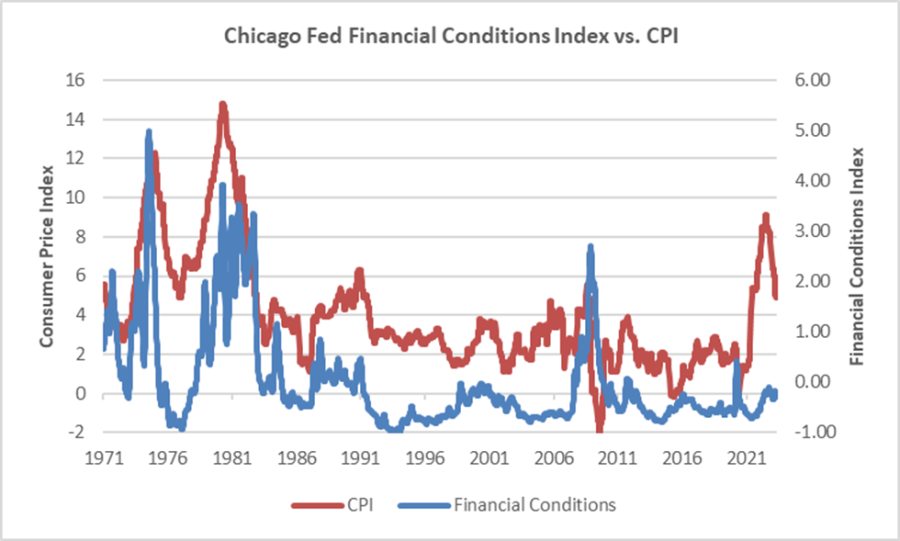

The major fallout from the Fed’s recent anti-inflation efforts seems concentrated with financial intermediaries rather than consumers (or workers), and the financial intermediary stress the Fed is relying on to help curb economic activity is grounded in their own balance sheet management decisions rather than deteriorating loan portfolios. We’ve looked at this before, but it bears repeating that in the “great inflation” of the 1970s, the Chicago Fed’s Financial Conditions Index reached its highest recorded points (higher means tighter than average conditions) and in this most recent inflationary cycle, that same index has remained consistently accommodative. Can you wring inflation out of a system while retaining relatively accommodative financial conditions? Which begs the question of whether any Fed pause is more about shifting priorities: downgrading the inflation fight in favor of moderating the financial intermediary threat? We might be living a remake of the 1970s version of stubborn inflation, which means that all the attendant issues—rolling volatility across operations, financing, and investing—might be sticking around as well.

Meanwhile, somewhere out in the Atlantic the debt ceiling storm is forming. Who knows whether it will make landfall as a storm or a hurricane, but it does remind us that the operative portion of the Jamie Dimon quote noted above is this part of the crisis is over. The next part of the long saga that is about us climbing out of a deep fiscal and monetary hole will roll in and new variations of the same central challenge will emerge for healthcare leaders.

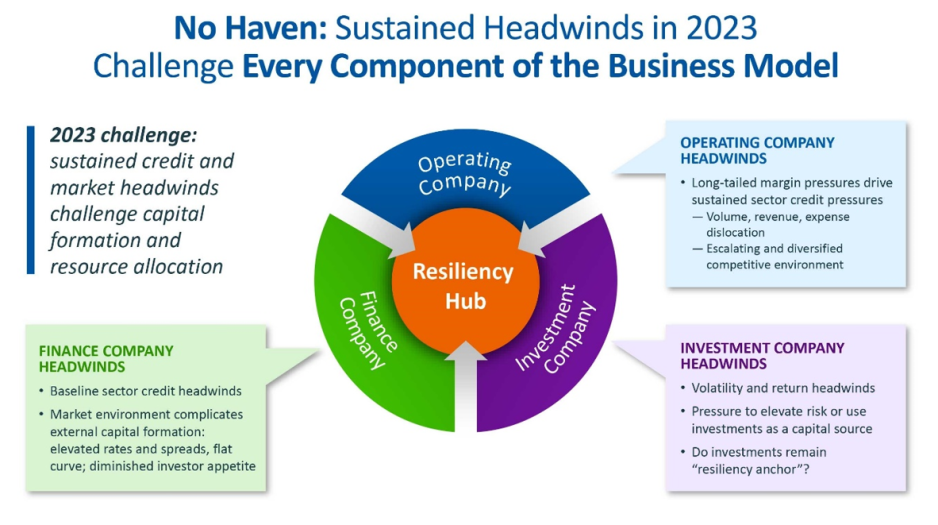

A Healthcare Makeover

Ken Kaufman has been advancing the idea that healthcare needs a “makeover” to align with post-COVID realities. Look for a piece from him on this soon, but the thesis is that reverting to a 2019 world isn’t going to happen, which means that restructuring is the only option. The most recent National Hospital Flash Report suggests improving margins, but they remain well below historical norms and the labor part of the expense equation is structurally higher. Where we are is not sustainable and waiting for a reversion is a rapidly decaying option.

My contribution to Ken’s argument is to reemphasize that balance sheet is the essential (only) bridge between here and a restructured sector and the journey is going to require very careful planning about how to size, position, and deploy liquidity, leverage, and investments. Of course, the central focus will be on how to reposition operations. But if organic cash generation remains anemic, the gap will be filled by either weakening the balance sheet (drawing down reserves, adding leverage, or adopting more aggressive asset allocation) or by partnering with organizations that have the necessary resources.

Organizations reach the point of greatest enterprise risk when the scale of operating challenges outstrips the scale of balance sheet resources. Missteps are manageable when the imbalance is the product of rapid growth but not when it is the result of deflating resources. If the core imperative is to remake operations, the co-equal imperative is continuously repositioning the balance sheet to carry you from here to whatever defines success.