The confidential nature of the Biden administration’s drug price negotiations has made theprocess and outcome of thelong-sought Democratic policy goal something of a mystery.

Why it matters:

The administration is expected to announce the results of those negotiations this week, and there’s plenty of speculation about the actual savings that will be realized starting in 2026 — and how aggressive the Biden administration got on pharma in an election year.

Where it stands:

Drugmakers have indicated that the negotiated prices for this first 10 drugs won’t have much impact on their projected bottom lines.

But the results could hint at what’s to come in subsequent rounds, as the number of drugs up for negotiation expands, possibly to include blockbuster GLP-1 weight-loss drugs.

Context:

The Centers for Medicare and Medicaid Services last summer chose 10 drugs that account for some of the highest total costs for Medicare, including Bristol Myers Squibb and Pfizer’s blood-thinner Eliquis and Boehringer Ingelheim’s diabetes drug Jardiance.

CMS and drugmakers have been going back and forth since February on how to price the drugs. Meanwhile, the pharmaceutical industry and its allies have mounted a series of so far unsuccessful legal challenges to stop the talks.

Here are some key unanswered questions ahead of the announcement, expected Thursday morning:

What information will CMS release about the final drug prices? Analysts, policy experts and industry groups told Axios they’re watching for whether Medicare officials announce specific levels of savings they achieved on each drug.

If Medicare does announce levels of savings, it’ll matter whether they measure those against drugs’ current list prices, which are typically higher than what patients actually pay, or another figure that takes into account existing rebates and discounts, said TD Cowen analyst Rick Weissenstein.

Statutorily, Medicare officials have to release the final prices for the selected drugs by Sept. 1 and justify those prices by March 1.

“What data CMS chooses to release is a big question mark,” said Chris Meekins, an analyst at Raymond James.

How will pharmacy benefit middlemen and prescription drug insurance plans react to the new prices?

Medicare Part D insurers must cover all 10 selected drugs, but the Inflation Reduction Act doesn’t specify where they need to place the drugs on their formularies.

That could potentially lead to drug middlemen and insurers giving competing products more favorable placement on their formularies, said Lindsay Bealor Greenleaf, who leads federal and state policy at ADVI Health, which consults for pharmaceutical and biotech manufacturers.

CMS will require plans to justify their decision if they move the drugs to different tiers or add more restrictive utilization management tools, per KFF.

How will investors and drugmakersreact?

The release of the maximum fair drug prices could clarify how risk-averse large pharmaceutical companies need to be in future acquisitions of smaller biotech companies, said John Stanford, executive director of Incubate, the life sciences investor lobbying group.

How will Medicare-negotiated prices compare with international drug prices?

Branded drugs typically come with higher price tags in the United States than elsewhere in the world.

“I think it’s going to be very instructive to see how much the purchasing power of CMS gets us in terms of reduction,” said Anna Kaltenboeck, who leads the prescription drug reimbursement work at consulting firm ATI Advisory.

What’s next:

Negotiated prices will go into effect Jan 1., 2026. CMS will announce as many as 15 additional drugs for the second round of negotiation by Feb. 1, 2025.

The Affordable Care Act turned 14 on March 23. It has done a lot of good for a lot of people, but big changes in the law are urgently needed to address some very big misses and consequences I don’t believe most proponents of the law intended or expected.

At the top of the list of needed reforms: restraining the power and influence of the rapidly growing corporations that are siphoning more and more money from federal and state governments – and our personal bank accounts – to enrich their executives and shareholders.

I was among many advocates who supported the ACA’s passage, despite the law’s ultimate shortcomings. It broadened access to health insurance, both through government subsidies to help people pay their premiums and by banning prevalent industry practices that had made it impossible for millions of American families to buy coverage at any price. It’s important to remember that before the ACA, insurers routinely refused to sell policies to a third or more applicants because of a long list of “preexisting conditions” – from acne and heart disease to simply being overweight – and frequently rescinded coverage when policyholders were diagnosed with cancer and other diseases.

While insurance company executives were publicly critical of the law, they quickly took advantage of loopholes (many of which their lobbyists created) that would allow them to reap windfall profits in the years ahead – and they have, as you’ll see below.

I wrote and spoke frequently as an industry whistleblower about what I thought Congress should know and do, perhaps most memorably in an interview with Bill Moyers. During my Congressional testimony in the months leading up to the final passage of the bill in 2010, I told lawmakers that if they passed it without a public option and acquiesced to industry demands, they might as well call it “The Health Insurance Industry Profit Protection and Enhancement Act.”

A health plan similar to Medicare that could have been a more affordable option for many of us almost happened, but at the last minute, the Senate was forced to strip the public option out of the bill at the insistence of Sen. Joe Lieberman (I-Connecticut), who died on March 27, 2024. The Senate did not have a single vote to spare as the final debate on the bill was approaching, and insurance industry lobbyists knew they could kill the public option if they could get just one of the bill’s supporters to oppose it. So they turned to Lieberman, a former Democrat who was Vice President Al Gore’s running mate in 2000 and who continued to caucus with Democrats. It worked. Lieberman wouldn’t even allow a vote on the bill if it created a public option. Among Lieberman’s constituents and campaign funders were insurance company executives who lived in or around Hartford, the insurance capital of the world. Lieberman would go on to be the founding chair of a political group called No Labels, which is trying to find someone to run as a third-party presidential candidate this year.

The work of Big Insurance and its army of lobbyists paid off as insurers had hoped. The demise of the public option was a driving force behind the record profits – and CEO pay – that we see in the industry today.

The good effects of the ACA:

Nearly 49 million U.S. residents (or 16%) were uninsured in 2010. The law has helped bring that down to 25.4 million, or 8.3% (although a large and growing number of Americans are now “functionally uninsured” because of unaffordable out-of-pocket requirements, which President Biden pledged to address in his recent State of the Union speech).

The ACA also made it illegal for insurers to refuse to sell coverage to people with preexisting conditions, which even included birth defects, or charge anyone more for their coverage based on their health status; it expanded Medicaid(in all but 10 states that still refuse to cover more low-income individuals and families); it allowed young people to stay on their families’ policies until they turn 26; and it required insurers to spend at least 80% of our premiums on the health care goods and services our doctors say we need (a well-intended provision of the law that insurers have figured out how to game).

The not-so-good effects of the ACA:

As taxpayers and health care consumers, we have paid a high price in many ways as health insurance companies have transformed themselves into massive money-making machines with tentacles reaching deep into health care delivery and taxpayers’ pockets.

To make policies affordable in the individual market, for example, the government agreed to subsidize premiums for the vast majority of people seeking coverage there, meaning billions of new dollars started flowing to private insurance companies. (It also allowed insurers to charge older Americans three times as much as they charge younger people for the same coverage.) Even more tax dollars have been sent to insurers as part of the Medicaid expansion. That’s because private insurers over the years have persuaded most states to turn their Medicaid programs over to them to administer.

We invite you to take a look at how the ascendency of health insurers over the past several years has made a few shareholders and executives much richer while the rest of us struggle despite – and in some cases because of – the Affordable Care Act.

BY THE NUMBERS

In 2010, we as a nation spent $2.6 trillion on health care. This year we will spend almost twice as much – an estimated $4.9 trillion, much of it out of our own pockets even with insurance.

In 2010, the average cost of a family health insurance policy through an employer was $13,710. Last year, the average was nearly $24,000, a 75% increase.

The ACA, to its credit, set an annual maximum on how much those of us with insurance have to pay before our coverage kicks in, but, at the insurance industry’s insistence, it goes up every year. When that limit went into effect in 2014, it was $12,700 for a family. This year, it has increased by 48%, to $18,900. That means insurers can get away with paying fewer claims than they once did, and many families have to empty their bank accounts when a family member gets sick or injured. Most people don’t reach that limit, but even a few hundred dollars is more than many families have on hand to cover deductibles and other out-of-pocket requirements. Now 100 million Americans – nearly one of every three of us – are mired in medical debt, even though almost 92% of us are presumably “covered.” The coverage just isn’t as adequate as it used to be or needs to be.

Meanwhile, insurance companies had a gangbuster 2023. The seven big for-profit U.S. health insurers’ revenues reached $1.39 trillion, and profits totaled a whopping $70.7 billion last year.

SWEEPING CHANGE, CONSOLIDATION–AND HUGE PROFITS FOR INVESTORS

Insurance company shareholders and executives have become much wealthier as the stock prices of the seven big for-profit corporations that control the health insurance market have skyrocketed.

NOTE: The Dow Jones Industrial Average is listed on this chart as a reference because it is a leading stock market index that tracks 30 of the largest publicly traded companies in the United States.

REVENUES collected by those seven companies have more than tripled (up 346%), increasing by more than $1 trillion in just the past ten years.

PROFITS (earnings from operations) have more than doubled (up 211%), increasing by more than $48 billion.

The CEOs of these companies are among the highest paid in the country. In 2022, the most recent year the companies have reported executive compensation, they collectively made $136.5 million.

U.S. HEALTH PLAN ENROLLMENT

Enrollment in the companies’ health plans is a mix of “commercial” policies they sell to individuals and families and that they manage for “plan sponsors” – primarily employers and unions – and government/enrollee-financed plans (Medicare, Medicaid, Tricare for military personnel and their dependents and the Federal Employee Health Benefits program).

Enrollment in their commercial plans grew by just 7.65% over the 10 years and declined significantly at UnitedHealth, CVS/Aetna and Humana. Centene and Molina picked up commercial enrollees through their participation in several ACA (Obamacare) markets in which most enrollees qualify for federal premium subsidies paid directly to insurers.

While not growing substantially, commercial plans remain very profitable because insurers charge considerably more in premiums now than a decade ago.

(1) The 2013 total for CVS/Aetna was reported by Aetna before its 2018 acquisition by CVS. (2) Humana announced last year it is exiting the commercial health insurance business. (3) Enrollment in the ACA’s marketplace plans account for all of Molina’s commercial business.

By contrast, enrollment in the government-financed Medicaid and Medicare Advantage programs has increased 197% and 167%, respectively, over the past 10 years.

(1) The 2013 total for CVS/Aetna was reported by Aetna before its 2018 acquisition by CVS.

Of the 65.9 million people eligible for Medicare at the beginning of 2024, 33 million, slightly more than half, enrolled in a private Medicare Advantage plan operated by either a nonprofit or for-profit health insurer, but, increasingly, three of the big for-profits grabbed most new enrollees.

Of the 1.7 million new Medicare Advantage enrollees this year, 86% were captured by UnitedHealth, Humana and Aetna.

Those three companies are the leaders in the Medicare Advantage business among the for-profit companies, and, according to the health care consulting firm Chartis, are taking over the program “at breakneck speed.”

(1) The 2013 total for CVS/Aetna was reported by Aetna before its 2018 acquisition by CVS. (2,3) Centene’s and Molina’s totals include Medicare Supplement; they do not break out enrollment in the two Medicare categories separately.

It is worth noting that although four companies saw growth in their Medicare Supplement enrollment over the decade, enrollment in Medicare Supplement policies has been declining in more recent years as insurers have attracted more seniors and disabled people into their Medicare Advantage plans.

OTHER FEDERAL PROGRAMS

In addition to the above categories, Humana and Centene have significant enrollment in Tricare, the government-financed program for the military. Humana reported 6 million military enrollees in 2023, up from 3.1 million in 2013. Centene reported 2.8 million in 2023. It did not report any military enrollment in 2013.

Elevance reported having 1.6 million enrollees in the Federal Employees Health Benefits Program in 2023, up from 1.5 million in 2013. That total is included in the commercial enrollment category above.

At Cigna, Express Scripts’ pharmacy operations now contribute more than 70% to the company’s total revenues. Caremark’s pharmacy operations contribute 33% to CVS/Aetna’s total revenues, and Optum Rx contributes 31% to UnitedHealth’s total revenues.

WHAT TO DO AND WHERE TO START

The official name of the ACA is the Patient Protection and Affordable Care Act. The law did indeed implement many important patient protections, and it made coverage more affordable for many Americans.

But there is much more Congress and regulators must do to close the loopholes and dismantle the barriers erected by big insurers that enable them to pad their bottom lines and reward shareholders while making health care increasingly unaffordable and inaccessible for many of us.

Several bipartisan bills have been introduced in Congress to change how big insurers do business. They include curbing insurers’ use of prior authorization, which often leads to denials and delays of care; requiring PBMs to be more “transparent” in how they do business and banning practices many PBMs use to boost profits, including spread pricing, which contributes to windfall profits; and overhauling the Medicare Advantage program by instituting a broad array of consumer and patient protections and eliminating the massive overpayments to insurers.

And as noted above, President Biden has asked Congress to broaden the recently enacted $2,000-a-year cap on prescription drugs to apply to people with private insurance, not just Medicare beneficiaries. That one policy change could save an untold number of lives and help keep millions of families out of medical debt. (A coalition of more than 70 organizations and businesses, which I lead, supports that, although we’re also calling on Congress to reduce the current overall annual out-of-pocket maximum to no more than $5,000.)

I encourage you to tell your members of Congress and the Biden administration that you support these reforms as well as improving, strengthening and expanding traditional Medicare. You can be certain the insurance industry and its allies are trying to keep any reforms that might shrink profit margins from becoming law.

On Tuesday, health system leaders testified before the House Energy and Commerce Subcommittee onOversight and Investigations about potential changes to the 340B Drug Pricing Program.

The committee was receptive to witnesses’ claims that the program is essential to the financial survival of many systems, but representatives stated that “the status quo is not acceptable” and that they had a responsibility to “step in and provide oversight.”

There was little interest expressed in broad overhauls to the program, but both witnesses and representatives focused on how it could benefit from greater transparency, for example requiring hospitals to disclose 340B revenue, how savings are used, and which patient populations are served through the program.

Meanwhile, Republicans and Democrats in both houses have introduced multiple bills this session that focus on various aspects of the 340B program, including transparency.

The Gist: It’s encouraging to see members of congress recognize how essential the 340B program is to health system finances, and of the potential reforms on the table, increased transparency is a relatively palatable option.

Congress is exploring statutory tweaks to the program in response to the myriad legal challenges concerning it, many of which involve the Department of Health and Human Services. Several of these lawsuits stem from more than 20 major drugmakers restricting 340B discounts at contract pharmacies, which has led multiple states to enact legislation protecting these discounts, in turn prompting further lawsuits.

The mess of conflicting rulings these cases have produced so far is a clear sign that the 340B statute will be amended, and health system advocates should continue working with Congress to find solutions that preserve the integrity of the program.

As campaigns for November elections gear up for early voting and Congress considers bipartisan reforms to limit consolidation and enhance competition in U.S. healthcare, prospective voters are sending a cleat message to would-be office holders:

Healthcare Affordability must be addressed directly, transparently and now.

Polling by Gallup, Kaiser Family Foundation and Pew have consistently shown healthcare affordability among top concerns to voters alongside inflation, immigration and access to abortion. It is higher among Democratic-leaning voters but represents the majority in every socio-economic cohort–young and old, low and middle income and households with/without health insurance coverage., urban and rural and so on.

It’s understandable: household economic security is declining: per the Federal Reserve’s latest household finances report:

72% of US adults say they are doing well financially (down from 78% in 2021)

54% say they have emergency savings to cover 3 months expenses ($400)—down from high of 59% in 2015.

69% say their finances deteriorated in 2023. They’re paying more for groceries, fuel, insurance premiums and childcare.

Renters absorbed a 10% increase last year and mortgage interest spike has put home ownership beyond reach for 6 in 10 households

Thus, household financial security is the issue and healthcare expenses play a key role. Drug prices, hospital consolidation, price transparency and corporate greed will get frequent recognition in candidate rhetoric. “Reform” will be promised. And each sector in the industry will offer solutions that place the blame on others.

Granted, the U.S. health system lacks a uniform definition of healthcare affordability. It’s a flaw. In the Affordable Care Act, it was framed in the context of an individual’s eligibility for government-subsidized insurance coverage (8.39% adjusted gross income for households between 100% and 400% of the federal poverty level). But a broader application to the entire population was overlooked. Nonetheless, economists, regulators and consumers recognize the central role healthcare affordability plays in household financial security.

Handicapping the major players potential to win the hearts and minds of voters about healthcare affordability is tricky:

Each major sector has seen the ranks of its membership decrease and the influence (and visibility) of its bigger players increase. They’re easy targets for industry critics.

Each sector is seeing private equity and non-traditional players play bigger roles. The healthcare landscape is expanding beyond the traditional players.

Each sector is struggling to make their cases for incremental reforms while employers, legislators and consumers want more. Bipartisan support for anything is a rarity: an exception is antipathy toward healthcare consolidation and lack of price transparency.

All recognize that affordability is complicated. Unit cost and price increases for goods and services are the culprit: excess utilization is secondary.

Against this backdrop, here’s a scorecard on the current state of preparedness as each navigates affordability going into Campaign 2024:

Sector

Advantages

Disadvantages

Handicap Score1=Unprepared to5=Well Prepared

Hospitals

Community presence (employer, safety net) Economic impact Influence in Congress Scale: 30% of spending + direct employment of 52% of physicians Access to capital

Lack of costs & price transparency Unit costs inflation due to wage, supply chain & admin Shifting demand for core services. Low entry barriers for key services Regulator headwind (state, federal). Operating, governing culture Value proposition erosion with employers, pre-Medicare populations Consumer orientation

3

Physicians

Consumer trust Influence in Congress Shared savings (Medicare) Essentiality Specialization Access to technology

Care continuity Inadequacy of primary care Disorganization (fragmentation) Value of shared savings to general population (beyond Medicare) Culture: change-averse (education, licensing performance measurement, et al) Data: costs, outcomes

2

Drug Manufacturers

Increasing product demand Influence in Congress Public trust in drug efficacy Insurance structure that limits consumer price sensitivity to OOP Potential for AI -enabled discovery, market access Access to private capital Congress’ constraint on PBMs

Unit cost escalation Lack of price transparency Growing disaffection for FDA Long-term Basic Research Funding State Price Control Momentum Market access Restrictive Formulary Growth Transparency in Distributor-PBM business relationships Public perception of corporate greed

2

Health Insurers

Availability of claims, cost data Employer tax exemptions Growing government market Plan design: OOP, provider access Public association: coverage = financial security Access to private capital

Escalating premiums Declining group market Growing regulatory scrutiny (consolidation, data protection) Tension with health systems Value proposition erosion among government, employers, consumers

4

Retail Health

Non-incumbrance of restrictive regulatory framework Consumer acceptance Breadth of product opportunities Access to private capital Opportunity for care management (i.e. CVS- Epic) Operational orientation to consumers (convenience, pricing, et al) Potential with employers,

Lack of access, coordination with needed specialty care Threat of regulatory restraint on growth Risks associated with care management models

3

The biggest, investor-owned health insurers own the advantage today. As in other sectors, they’re growing faster than their smaller peers and enjoy advantages of scale and private capital access to fund their growth. A handful of big players in the other sectors stand-out, but their affordability solutions are, to date, not readily active.

In each sector above, there is consensus that a fundamental change in the structure, function and oversight of the U.S. health is eminent. In all, tribalism is an issue: publicly-owned, not for profits vs. investor-owned, independent vs. affiliated, big vs. small and so on.

Getting consensus to address affordability head on is hard, so not much is done by the sectors themselves. And none is approaching the solution in its necessary context—the financial security of a households facing unprecedented pressures to make ends meet. In all likelihood, the bigger, more prominent organizations in their ranks of these sectors will deliver affordability solutions well-above the lowest common denominators that are comfortable for most Thus, health care affordability will be associated with organizational brands and differentiated services, not the sectors from which their trace their origins. And it will be based on specified utilization, costs, outcome and spending guarantees to consumers and employers that are reasonable and transparent.

After UnitedHealth Group CEO Andrew Witty’s appearances at two congressional committee hearings last week, I had planned to write a story about what the lawmakers had to say. One idea I considered was to publish a compilation of some of the best zingers, and there were plenty, from Democrats and Republicans alike.

I reconsidered that idea because I know from the nearly half-century I have spent on or around Capitol Hill in one capacity or another that those zingers were carefully crafted by staffers who know how to write talking points to make them irresistible to the media. As a young Washington correspondent in the mid-to-late’70s, I included countless talking points in the stories I wrote for Scripps-Howard newspapers. After that, I wrote talking points for a gubernatorial candidate in Tennessee. I would go from there to write scads of them for CEOs and lobbyists to use with politicians and reporters during my 20 years in the health insurance business.

I know the game. And I know that despite all the arrows 40 members of Congress on both sides of the Hill shot at Witty last Wednesday, little if anything that could significantly change how UnitedHealth and the other big insurers do business will be enacted this year.

Money in politics is the elephant in any Congressional hearing room or executive branch office you might find yourself in (and it’s why I coauthored Nation on the Take with Nick Penniman).

You will hear plenty of sound and fury in those rooms but don’t hold your breath waiting for relief from ever-increasing premiums and out-of-pocket requirements and the many other barriers Big Insurance has erected to keep you from getting the care you need.

It is those same barriers doctors and nurses cite when they acknowledge the “moral injury” they incur trying to care for their patients under the tightening constraints imposed on them by profit-obsessed insurers, investors and giant hospital-based systems.

Funny not funny

Cartoonist Stephan Pastis captured the consequences of the corporate takeover of our government, accelerated by the Supreme Court’s 2010 landmark Citizens United vs. Federal Election Commission ruling, in his Pearls Before Swine cartoon strip Sunday.

Rat: Where are you going, Pig?

Pig: To a politician’s rally. I’m taking my magic translation box.

Rat: He doesn’t speak English?

Pig: He speaks politicianish. This translates it into the truth. Come see.

Politician: In conclusion, if you send me to Washington, I’ll clean up this corrupt system and fight for you everyday hard-working Americans. God bless you. God bless the troops. And God bless America.

Magic translation box: I am given millions of dollars by the rich and the powerful to keep this rigged system exactly as it is. Until you change that, none of this will ever change and we’ll keep hoping you’re too distracted to notice.

Politician’s campaign goon: We’re gonna need a word with you.

Magic translation box: This is too much truth for one comic strip. Prepare to be disappeared.

Rat: I don’t know him.

Back to Sir Witty’s time on the hot seat. It attracted a fair amount of media coverage, chock full of politicians’ talking points, including in The New York Times and The Washington Post. (You can read this short Reuters story for free.) Witty, of course, came equipped with his own talking points, and he followed his PR and legal teams’ counsel: to be contrite at every opportunity; to extol the supposed benefits of bigness in health care (UnitedHealth being by far the world’s largest health care corporation) all the while stressing that his company is not really all that big because it doesn’t, you know, own hospitals and pharmaceutical companies [yet]; and to assure us all that the fixes to its hacked claims-handling subsidiary Change Healthcare are all but in.

Congress? Meh. Paying for care? WTF!

Wall Street was relieved and impressed that Witty acquitted himself so well. Investors shrugged off the many barbs aimed at him and his vast international empire. By the end of the day Wednesday, the company’s stock price had actually inched up a few cents, to $484.11. A modest 2.7 million shares of UnitedHealth’s stock were traded that day, considerably fewer than usual.

Instead of punishing UnitedHealth, investors inflicted massive pain on its chief rival, CVS, which owns Aetna. On the same day Witty went to Washington, CVS had to disclose that it missed Wall Street financial analyst’s earnings-per-share expectations for the first quarter of 2024 by several cents. Shareholders’ furor sent CVS’ stock price tumbling from $67.71 to a 15-year low of $54 at one point Wednesday before settling at $56.31 by the time the New York Stock Exchange closed. An astonishing 65.7 million shares of CVS stock were traded that day.

Postscript: I do want to bring to your attention one exchange between Witty and Rep. Buddy Carter (R-Ga.) during the House Energy and Commerce committee hearing. Carter is a pharmacist who has seen firsthand how UnitedHealth’s virtual integration–operating health insurance companies with one hand and racking up physician practices and clinics with the other–and its PBM’s business practices have contributed to the closure of hundreds of independent pharmacies in recent years. He’s also seen patients walk away from the pharmacy counter without their medications because of PBMs’ out-of-pocket demands (often hundreds and thousands of dollars). And he’s seen other patients face life-threatenng delays because of industry prior authorization requirements. Carter was instrumental in persuading the Federal Trade Commission to investigate PBMs’ ownership and business practices. He told Witty:

I’m going to continue to bust this up…This vertical integration in health care in general has got to end.

Late last week, the Department of Health and Human Services (HHS) published a final rule establishing a new administrative dispute resolution process for the 340B drug discount program.

A panel, composed of government experts from the Office of Pharmacy Affairs, will resolve claims raised by covered entity providers about drugmakers overcharging them for 340B drugs, as well as claims from pharmaceutical companies that covered entities are diverting or duplicating discounts improperly. The new process, which will go into effect in mid-June, allows the panel to review claims on issues related to those pending in federal court. It’s intended to be “more accessible, administratively feasible, and timely” than a prior process established by HHS in 2020 that was paused after legal challenges.

The Gist:

This new 340B dispute resolution process is likely to see extensive use, as battles between providers and drugmakers over the drug discount program have heated up significantly in recent years. There are more than 50 ongoing court cases related to the program, many of which concern actions taken by at least 20 major drugmakers to restrict 340B sales to contract pharmacies. Although this new process may provide more effective dispute resolution, none of its decisions can be considered final until courts have settled the myriad cases before them.

On Monday, national supermarket giant Kroger announced that it had reached a definitive agreement to sell its specialty pharmacy business to insurer Elevance Health, which plans to fold the business into its CarelonRx pharmacy benefit manager (PBM) division. Kroger’s in-store retail pharmacies and walk-in clinics are not included in the deal, which could close in the second half of 2024. Kroger’s specialty pharmacy is the sixth largest by revenue, serving two percent of the US market. The planned sale comes as Kroger pursues a merger with rival supermarket chain Albertsons, which also operates a specialty pharmacy, although the Federal Trade Commission (FTC) recently announced that it’s challenging that merger.

The Gist: With total pharmacy spend up 25 percent since 2019, including a 34 percent growth for specialty drugs, Elevance is capitalizing on a booming market by pushing into pharmacy services, following last year’s acquisition of BioPlus, another specialty pharmacy.

Administering high-cost drugs to patients with rare or complex diseases, specialty pharmacies now account for more than half of all prescription drug spending despite making up only around two percent of total prescription volumes.

On Tuesday, the 8th US Circuit Court of Appeals ruled against the pharmaceutical industry after its PhRMA (The Pharmaceutical Research and Manufacturers of America) trade group sued to prevent Arkansas from requiring drug manufacturers to distribute discounted drugs to 340B contract pharmacies. The judge’s decision, seen as a win for hospitals, affirmed state authority to establish regulations on top of the federal 340B law, which does not actually reference contract pharmacies. A Louisiana law similar to Arkansas’ is currently being challenged.

The Gist:This rulingcould encourage other states to pass laws protecting 340B contract pharmacy discounts. Contract pharmacy sales have swelled in recent years, prompting at least 20 major drug manufacturers to refuse to provide 340B discounts for drugs dispensed through contract pharmacies.

This issue is currently the subject of myriad lawsuits as courts have issued conflicting rulings.

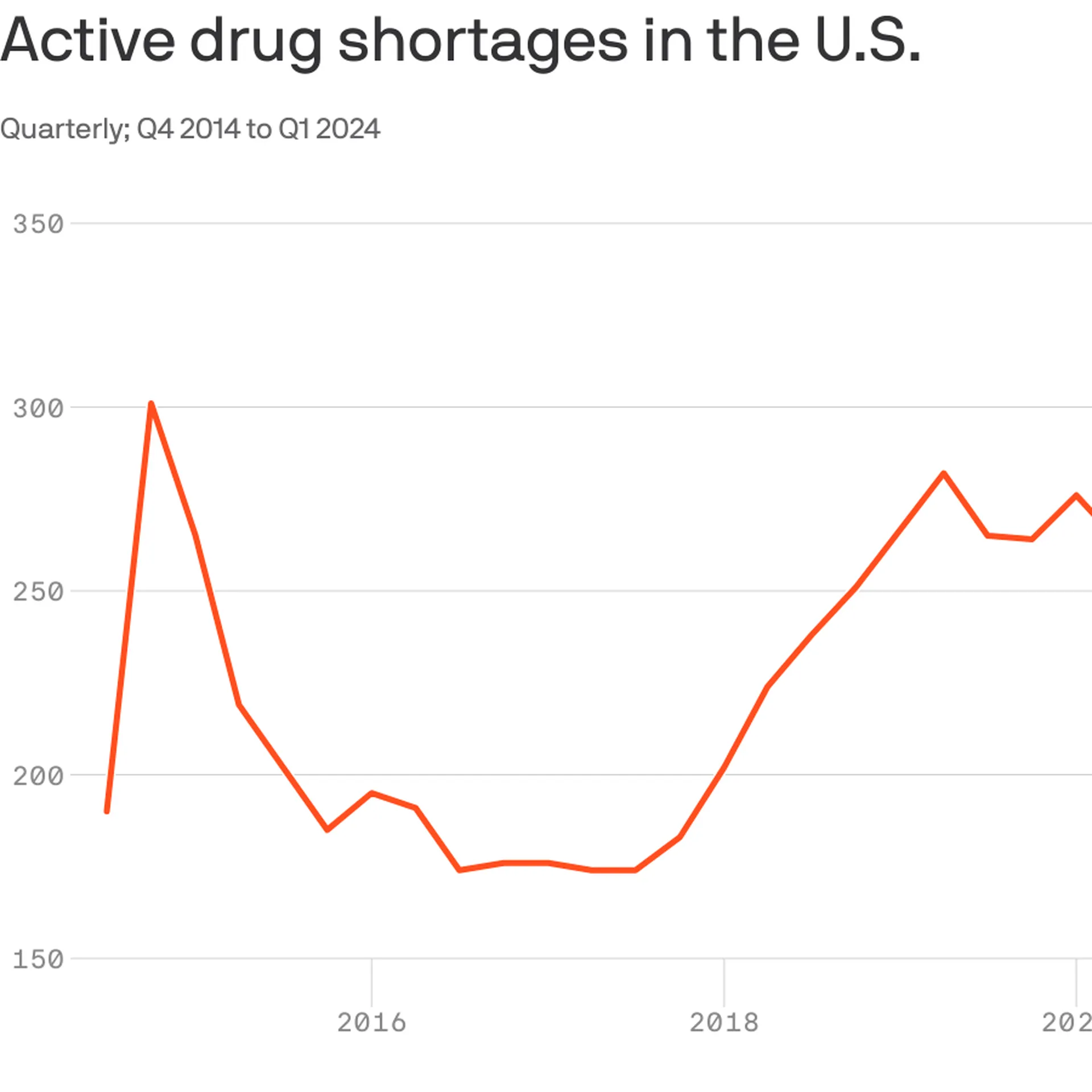

With 323 medicines in short supply, U.S. drug shortages have risen to their highest level since the American Society of Health-System Pharmacists began tracking in 2001.

Why it matters:

This high-water mark should energize efforts in Congress and federal agencies to address the broken market around what are often critical generic drugs, the organization says.

The Biden administration last week issued a drug-shortage plan that called on Congress to pass legislation that would reward hospitals for maintaining an adequate supply of key drugs, among other measures.

As a “first step,” Medicare yesterday proposed incentives for roughly 500 small hospitals to establish and maintain a six-month buffer stock of essential medicines.

The big picture:

Many of the issues behind shortages are tied to low prices for generics that leave manufacturers competing on price.

“It’s been a race to the bottom. We need more transparency around quality so that buyers have a reason to not chase the lowest price,” said Michael Ganio, senior director at the ASHP.

Drugmakers that can demonstrate safer, higher-quality manufacturing practices should earn a higher price, he said.

Manufacturing quality concerns in particular have fueled shortages of chemotherapy drugs and some antibiotics.

Between the lines: Other factors are also driving drug shortages.

Controlled substances, such as pain and sedation medications,account for12% of active shortages, which are tied to recent legal settlements and Drug Enforcement Administration changes to production limits, per ASHP.

Not surprisingly, the blockbuster category of anti-obesity drugs known as GLP-1s are in shortage largely because of outsized demand.

If you’re a U.S. health industry watcher, it would appear the $4.5 trillion system is under fire at every corner.

Pressures to lower costs, increase accessibility and affordability to all populations, disclose prices and demonstrate value are hitting every sector. Complicating matters, state and federal legislators are challenging ‘business as usual’ seeking ways to spend tax dollars more wisely with surprisingly strong bipartisan support on many issues. No sector faces these challenges more intensely than hospitals.

In 2022 (the latest year for NHE data from CMS), hospitals accounted for 30.4% of total spending ($1.35 trillion. While total healthcare spending increased 4.1% that year, hospital spending was up 2.2%–less than physician services (+2.7%), prescription drugs (+8.4%), private insurance (+5.9%) and the overall inflation rate (+6.5%) and only slightly less than the overall economy (GDP +1.9%). Operating margins were negative (-.3%) because operating costs increased more than revenues (+7.7% vs. 6.5%) creating deficits for most. Hardest hit: the safety net, rural hospitals and those that operate in markets with challenging economic conditions.

In 2023, the hospital outlook improved. Pre-Covid utilization levels were restored. Workforce tensions eased somewhat. And many not-for-profits and investor-owned operators who had invested their cash flows in equities saw their non-operating income hit record levels as the S&P 500 gained 26.29% for the year.

In 2024, the S&P is up 5.15% YTD but most hospital operators are uncertain about the future, even some that appear to have weathered the pandemic storm better than others. A sense of frustration and despair is felt widely across the sector, especially in critical access, rural, safety net, public and small community hospitals where long-term survival is in question.

The cynicism felt by hospitals is rooted in four conflicts in which many believe hospitals are losing ground:

Hospitals vs. Insurers:

Insurers believe hospitals are inefficient and wasteful, and their business models afford them the role of deciding how much they’ll pay hospitals and when based on data they keep private. They change their rules annually to meet their financial needs. Longer-term contracts are out of the question. They have the upper hand on hospitals.

Hospitals take financial risks for facilities, technologies, workforce and therapies necessary to care. Their direct costs are driven by inflationary pressures in their wage and supply chains outside their control and indirect costs from regulatory compliance and administrative overhead, Demand is soaring. Hospital balance sheets are eroding while insurers are doubling down on hospital reimbursement cuts to offset shortfalls they anticipate from Medicare Advantage. Their finances and long-term sustainability are primarily controlled by insurers. They have minimal latitude to modify workforces, technology and clinical practices annually in response to insurer requirements.

Hospitals vs. the Drug Procurement Establishment:

Drug manufacturers enjoy patent protections and regulatory apparatus that discourage competition and enable near-total price elasticity. They operate thru a labyrinth of manufacturers, wholesalers, distributors and dispensers in which their therapies gain market access through monopolies created to fend-off competition. They protect themselves in the U.S. market through well-funded advocacy and tight relationships with middlemen (GPOs, PBMs) and it’s understandable: the global market for prescription drugs is worth $1.6 trillion, the US represents 27% but only 4% of the world population.

And ownership of the 3 major PBMs that control 80% of drug benefits by insurers assures the drug establishment will be protected.

Prescription drugs are the third biggest expense in hospitals after payroll and med/surg supplies. They’re a major source of unexpected out-of-pocket cost to patients and unanticipated costs to hospitals, especially cancer therapies. And hospitals (other than academic hospitals that do applied research) are relegated to customers though every patient uses their products.

Prescription drug cost escalation is a threat to the solvency and affordability of hospital care in every community.

Hospitals vs. the FTC, DOJ and State Officials:

Hospital consolidation has been a staple in hospital sustainability and growth strategies. It’s a major focus of regulator attention. Horizontal consolidation has enabled hospitals to share operating costs thru shared services and concentrate clinical programs for better outcomes. Vertical consolidation has enabled hospitals to diversify as a hedge against declining inpatient demand: today, 200+ sponsor health insurance plans, 60% employ physicians directly and the majority offer long-term, senior care and/or post-acute services. But regulators like the FTC think hospital consolidation has been harmful to consumers and third-party data has shown promised cost-savings to consumers are not realized.

Federal regulators are also scrutinizing the tax exemptions afforded not-for-profit hospitals, their investment strategies, the roles of private equity in hospital prices and quality and executive compensation among other concerns. And in many states, elected officials are building their statewide campaigns around reining in “out of control” hospitals and so on.

Bottom line: Hospitals are prime targets for regulators.

Hospitals vs. Congress:

Influential members in key House and Senate Committees are now investigating regulatory changes that could protect rural and safety net hospitals while cutting payments to the rest. In key Committees (Senate HELP and Finance, House Energy and Commerce, Budget), hospitals are a target. Example: The Lower Cost, More Transparency Act passed in the the House December 11, 2023. It includes price transparency requirements for hospitals and PBMs, site-neutral payments, additional funding for rural and community health among more. The American Hospital Association objected noting “The AHA supports the elimination of the Medicaid disproportionate share hospital (DSH) reductions for two years. However, hospitals and health systems strongly oppose efforts to include permanent site-neutral payment cuts in this bill. In addition, the AHA has concerns about the added regulatory burdens on hospitals and health systems from the sections to codify the Hospital Price Transparency Rule and to establish unique identifiers for off-campus hospital outpatient departments (HOPDs).” Nonetheless, hospitals appear to be fighting an uphill battle in Congress.

Hospitals have other problems:

Threats from retail health mega-companies are disruptive. The public’s trust in hospitals has been fractured. Lenders are becoming more cautious in their term sheets. And the hospital workforce—especially its doctors and nurses—is disgruntled. But the four conflicts above seem most important to the future for hospitals.

However, conflict resolution on these is problematic because opinions about hospitals inside and outside the sector are strongly held and remedy proposals vary widely across hospital tribes—not-for profits, investor-owned, public, safety nets, rural, specialty and others.

Nonetheless, conflict resolution on these issues must be pursued if hospitals are to be effective, affordable and accessible contributors and/or hubs for community health systems in the future. The risks of inaction for society, the communities served and the 5.48 million (NAICS Bureau of Labor 622) employed in the sector cannot be overstated. The likelihood they can be resolved without the addition of new voices and fresh solutions is unlikely.

PS: In the sections that follow, citations illustrate the gist of today’s major message: hospitals are under attack—some deserved, some not. It’s a tough business climate for all of them requiring fresh ideas from a broad set of stakeholders.

PS If you’ve been following the travails of Mission Hospital, Asheville NC—its sale to HCA Healthcare in 2019 under a cloud of suspicion and now its “immediate jeopardy” warning from CMS alleging safety and quality concerns—accountability falls squarely on its Board of Directors. I read the asset purchase agreement between HCA and Mission: it sets forth the principles of operating post-acquisition but does not specify measurable ways patient safety, outcomes, staffing levels and program quality will be defined. It does not appear HCA is in violation with the terms of the APA, but irreparable damage has been done and the community has lost confidence in the new Mission to operate in its best interest. Sadly, evidence shows the process was flawed, disclosures by key parties were incomplete and the hospital’s Board is sworn to secrecy preventing a full investigation.

The lessons are 2 for every hospital:

Boards must be prepared vis a vis education, objective data and independent counsel to carry out their fiduciary responsibility to their communities and key stakeholders. And the business of running hospitals is complex, easily prone to over-simplification and misinformation but highly important and visible in communities where they operate.

Business relationships, price transparency, board performance, executive compensation et al can no longer to treated as private arrangements.