After covering the Medicare privatization crisis for over two years, an investigative reporter takes a step back and examines what’s at stake.

Medicare, the country’s largest and arguably most successful health care program, is under duress, weakened by decades of relentless efforts by insurance companies to privatize it.

A rapidly growing Medicare Advantage market — now 52% of Medicare beneficiaries, up from 37% in 2018 — controlled by some of the largest and most powerful corporations in the world, threatens to both drain the trust fund and eliminate Medicare’s most important and controversial component: its ability to set prices.

It is not an overstatement to call it a heist of historic proportions, endangering the health not only of the more than 65 million seniors and people with disabilities who depend on Medicare but all Americans who benefit from the powerful role that Medicare has historically played in reining in health care costs.

The giant corporations that dominate Medicare Advantage have rigged the system to maximize payments from our government to the point that they are now being overpaid between $88 billion and $140 billion a year. The overpayments could soar to new heights if the insurers get their way and eliminate traditional Medicare.

All of America’s seniors and disabled people who depend on Medicare could soon be moved to a managed care model of ever-tightening networks, relentless prior authorization requirements and limited drug formularies. The promise of a humane health care system for all would be sacrificed at the altar of the almighty insurer dollar.

The Medicare Payments Advisory Commission (MedPAC), the independent congressional agency tasked with overseeing Medicare, last month released a searing report which found that Medicare spends 22% more per beneficiary in Medicare Advantage plans than if those beneficiaries had been enrolled in traditional fee-for-service Medicare. That’s up from a 6% estimate in the prior year.

A similar cost trend exists for diagnosis coding.

Medicare Advantage plans and their affiliated providers increasingly upcoded diagnoses to get higher reimbursements. In 2024, overpayments due to upcoding could total $50 billion, according to MedPAC, up from $23 billion in 2023. These enormous overpayments drive up the cost of premiums — MedPAC’s conservative estimate is that the premiums paid to Medicare out of seniors’ Social Security checks will be $13 billion higher in 2024 because of those overpayments.

There is evidence that Americans and lawmakers are starting to wake up.

Medicare Advantage enrollment growth slowed considerably in 2023. Support within the Democratic Party for Medicare Advantage is cratering. In 2022, 147 House Democrats signed an industry-backed letter supporting Medicare Advantage. This year, just 24 House Democrats signed the letter. Earlier this month, the Biden administration cut Medicare Advantage base payments for the second year in a row(while still increasing payments overall), over the fierce opposition of the insurance lobby. The investment bank Stephens called Biden’s decision a “highly adverse” outcome for insurers. Wall Street has taken note, punishing the stock price of the largest Medicare Advantage insurers, with Barron’s noting that Wall Street’s “love affair” with Humana is “ending in tears.” The cargo ship is turning. It is up to us to determine if that will be enough.

We can’t attack a problem if we don’t know how to diagnose it. I spoke with some of the most knowledgeable critics of Medicare Advantage about the danger the rapid expansion of Medicare privatization presents to the American public.

Rick Gilfillan is a medical doctor who in 2010 became the first director of the Center for Medicare and Medicaid Innovation (CMMI). He would go on to serve as CEO of Trinity Health from 2013 to 2019. In 2021 he launched an effort to halt the involuntary privatization of Medicare benefits.

“Right now, all investigations are finding tremendous overpayments,” Gilfillan said. “The overpayments are based on medical diagnoses that may or may not be meaningful from a patient care standpoint. Insurers are using chart reviews, nurse home visits and AI software to find as many diagnoses as possible and thereby inflate the health risks of the patients and the premium they get from Medicare. The overpayments are just outrageous,” he said.

The problem could get worse if the Supreme Court curtails the powers of regulatory agencies, as it may do this year. “It would make a huge difference in what CMS would be able to do,” Gilfillan said.

The logic behind Medicare privatization is that seniors and people with disabilities use too much care, egged on by their doctors. If true, a solution could have been to enforce the Stark Law, which bans physicians from having financial relationships with providers they refer to, or other anti-kickback statutes. States could also enforce laws 33 of them have enacted that prohibit the “corporate practice of medicine.”

Instead, health insurers were invited and incentivized by previous administrations to compete with the original Medicare program and “manage” beneficiaries’ care. Under this model— set in its modern form in 2003 — Medicare Advantage insurers are paid a rate based on a complex risk modeling process and estimated costs.

But Medicare Advantage plans have never been cheaper than traditional Medicare, as MedPAC has repeatedly pointed out.

This is a far more complex approach than the fee-for-service model in which CMS sets prices in health care in a public and transparent manner, Gilfillan notes. The prices negotiated by Medicare Advantage companies, by contrast, are not disclosed.

“With fee-for-service, a patient is provided a service, treatment or medication. The physician who provides the service charges a specific amount for that service,” Gilfillan said. “And then Medicare pays whatever it decided it was worth for that service. The benefit is you pay for what you get.”

Some Medicare Advantage plans use a “capitated” approach in paying primary care physicians. The amount is based on the premium they receive for the patient. The more codes submitted, the higher the capitation, the greater the profit. That approach is having far-reaching economic impacts on health care, said Hayden Rooke-Ley, an Oregon-based lawyer and health care consultant who co-authored a recent New England Journal of Medicine article on the corporatization of primary care. It is the capitation model, he says, that drives the rampant upcoding among Medicare Advantage plans.

From Horizontal to Vertical

“An undercovered aspect of Medicare Advantage is the way it is fueling vertical consolidation” in the insurance business, Rooke-Ley added, noting that until recent years, insurers bulked up by buying smaller competitors (known as horizontal integration). “With so much government money, we’re seeing insurance companies restructuring themselves as vertically integrated conglomerates [through the acquisition of physician practices, clinics and pharmacy operations] to become even more profitable, especially in Medicare Advantage.”

“A key part of this strategy is to own primary care practices,” he said, citing Humana’s partnership with the private-equity firm Welsh Carson to become the largest owner of Medicare-based primary care, CVS/Aetna’s acquisition of Oak Street, and UnitedHealth’s roll up of doctors practices across the country.

As Rooke-Ley explained, control of primary care allows insurance companies to more easily manipulate “risk scores” to increase payments from the government by claiming patients are in worse health than they really are.

“The easiest way to increase risk scores, short of simply fabricating diagnosis codes, is to control the behavior of physicians and other clinicians,” he said.

“When an insurance company owns the physician practice, it can configure workflows, technology, and incentives to drive risk coding.

UnitedHealth, for example, can preferentially schedule Medicare Advantage patients – and it can choose to reach out to health plan enrollees it identifies with its data as having high ‘coding opportunities.’ It can require its doctors to go to risk-code training, and it can prohibit doctors from closing their notes before they address all the ‘suggested’ diagnosis codes.”

“While Medicare Advantage insurance companies tout all their provider acquisitions as investments in value-based care, the concern is that it’s really just looking like a game of financialization,” Rooke-Ley said. “MA was supposed to save Medicare money, but the exact opposite has happened.

According to MedPAC, the government will over-subsidize MA to the tune of $88 billion this year, with $54 billion of that due to excess risk coding relative to what we see in traditional Medicare. That’s a staggering amount of money that could go directly to patients and clinicians by strengthening traditional Medicare.”

Two Possible Futures

There are two options for the future of Medicare, said Dr. Ed Weisbart, former chief medical officer of the pharmacy benefit manager Express Scripts, which Cigna bought in 2018, who now leads the Missouri chapter of Physicians for a National Health Program.

In one future, he said, “We will change the trajectory and get rid of the profiteers, and manage to divert the funds that are being profiteered to patient care.”

In another future, the business practices of Medicare Advantage plans “will be unfettered and more damaging and harmful than they are today,” he said. “If we continue on this course we’ll find an increasingly polarized health care system that caters increasingly to the wealthy and privileged. The barriers to care will be worse.”

The Affordable Care Act turned 14 on March 23. It has done a lot of good for a lot of people, but big changes in the law are urgently needed to address some very big misses and consequences I don’t believe most proponents of the law intended or expected.

At the top of the list of needed reforms: restraining the power and influence of the rapidly growing corporations that are siphoning more and more money from federal and state governments – and our personal bank accounts – to enrich their executives and shareholders.

I was among many advocates who supported the ACA’s passage, despite the law’s ultimate shortcomings. It broadened access to health insurance, both through government subsidies to help people pay their premiums and by banning prevalent industry practices that had made it impossible for millions of American families to buy coverage at any price. It’s important to remember that before the ACA, insurers routinely refused to sell policies to a third or more applicants because of a long list of “preexisting conditions” – from acne and heart disease to simply being overweight – and frequently rescinded coverage when policyholders were diagnosed with cancer and other diseases.

While insurance company executives were publicly critical of the law, they quickly took advantage of loopholes (many of which their lobbyists created) that would allow them to reap windfall profits in the years ahead – and they have, as you’ll see below.

I wrote and spoke frequently as an industry whistleblower about what I thought Congress should know and do, perhaps most memorably in an interview with Bill Moyers. During my Congressional testimony in the months leading up to the final passage of the bill in 2010, I told lawmakers that if they passed it without a public option and acquiesced to industry demands, they might as well call it “The Health Insurance Industry Profit Protection and Enhancement Act.”

A health plan similar to Medicare that could have been a more affordable option for many of us almost happened, but at the last minute, the Senate was forced to strip the public option out of the bill at the insistence of Sen. Joe Lieberman (I-Connecticut), who died on March 27, 2024. The Senate did not have a single vote to spare as the final debate on the bill was approaching, and insurance industry lobbyists knew they could kill the public option if they could get just one of the bill’s supporters to oppose it. So they turned to Lieberman, a former Democrat who was Vice President Al Gore’s running mate in 2000 and who continued to caucus with Democrats. It worked. Lieberman wouldn’t even allow a vote on the bill if it created a public option. Among Lieberman’s constituents and campaign funders were insurance company executives who lived in or around Hartford, the insurance capital of the world. Lieberman would go on to be the founding chair of a political group called No Labels, which is trying to find someone to run as a third-party presidential candidate this year.

The work of Big Insurance and its army of lobbyists paid off as insurers had hoped. The demise of the public option was a driving force behind the record profits – and CEO pay – that we see in the industry today.

The good effects of the ACA:

Nearly 49 million U.S. residents (or 16%) were uninsured in 2010. The law has helped bring that down to 25.4 million, or 8.3% (although a large and growing number of Americans are now “functionally uninsured” because of unaffordable out-of-pocket requirements, which President Biden pledged to address in his recent State of the Union speech).

The ACA also made it illegal for insurers to refuse to sell coverage to people with preexisting conditions, which even included birth defects, or charge anyone more for their coverage based on their health status; it expanded Medicaid (in all but 10 states that still refuse to cover more low-income individuals and families); it allowed young people to stay on their families’ policies until they turn 26; and it required insurers to spend at least 80% of our premiums on the health care goods and services our doctors say we need (a well-intended provision of the law that insurers have figured out how to game).

The not-so-good effects of the ACA:

As taxpayers and health care consumers, we have paid a high price in many ways as health insurance companies have transformed themselves into massive money-making machines with tentacles reaching deep into health care delivery and taxpayers’ pockets.

To make policies affordable in the individual market, for example, the government agreed to subsidize premiums for the vast majority of people seeking coverage there, meaning billions of new dollars started flowing to private insurance companies. (It also allowed insurers to charge older Americans three times as much as they charge younger people for the same coverage.) Even more tax dollars have been sent to insurers as part of the Medicaid expansion. That’s because private insurers over the years have persuaded most states to turn their Medicaid programs over to them to administer.

We invite you to take a look at how the ascendency of health insurers over the past several years has made a few shareholders and executives much richer while the rest of us struggle despite – and in some cases because of – the Affordable Care Act.

BY THE NUMBERS

In 2010, we as a nation spent $2.6 trillion on health care. This year we will spend almost twice as much – an estimated $4.9 trillion, much of it out of our own pockets even with insurance.

In 2010, the average cost of a family health insurance policy through an employer was $13,710. Last year, the average was nearly $24,000, a 75% increase.

The ACA, to its credit, set an annual maximum on how much those of us with insurance have to pay before our coverage kicks in, but, at the insurance industry’s insistence, it goes up every year. When that limit went into effect in 2014, it was $12,700 for a family. This year, it has increased by 48%, to $18,900. That means insurers can get away with paying fewer claims than they once did, and many families have to empty their bank accounts when a family member gets sick or injured. Most people don’t reach that limit, but even a few hundred dollars is more than many families have on hand to cover deductibles and other out-of-pocket requirements.

Now 100 million Americans – nearly one of every three of us – are mired in medical debt, even though almost 92% of us are presumably “covered.” The coverage just isn’t as adequate as it used to be or needs to be.

Meanwhile, insurance companies had a gangbuster 2023. The seven big for-profit U.S. health insurers’ revenues reached $1.39 trillion, and profits totaled a whopping $70.7 billion last year.

SWEEPING CHANGE, CONSOLIDATION–AND HUGE PROFITS FOR INVESTORS

Insurance company shareholders and executives have become much wealthier as the stock prices of the seven big for-profit corporations that control the health insurance market have skyrocketed.

NOTE: The Dow Jones Industrial Average is listed on this chart as a reference because it is a leading stock market index that tracks 30 of the largest publicly traded companies in the United States.

REVENUES collected by those seven companies have more than tripled (up 346%), increasing by more than $1 trillion in just the past ten years.

PROFITS (earnings from operations) have more than doubled (up 211%), increasing by more than $48 billion.

The CEOs of these companies are among the highest paid in the country. In 2022, the most recent year the companies have reported executive compensation, they collectively made $136.5 million.

U.S. HEALTH PLAN ENROLLMENT

Enrollment in the companies’ health plans is a mix of “commercial” policies they sell to individuals and families and that they manage for “plan sponsors” – primarily employers and unions – and government/enrollee-financed plans (Medicare, Medicaid, Tricare for military personnel and their dependents and the Federal Employee Health Benefits program).

Enrollment in their commercial plans grew by just 7.65% over the 10 years and declined significantly at UnitedHealth, CVS/Aetna and Humana. Centene and Molina picked up commercial enrollees through their participation in several ACA (Obamacare) markets in which most enrollees qualify for federal premium subsidies paid directly to insurers.

While not growing substantially, commercial plans remain very profitable because insurers charge considerably more in premiums now than a decade ago.

(1) The 2013 total for CVS/Aetna was reported by Aetna before its 2018 acquisition by CVS. (2) Humana announced last year it is exiting the commercial health insurance business. (3) Enrollment in the ACA’s marketplace plans account for all of Molina’s commercial business.

By contrast, enrollment in the government-financed Medicaid and Medicare Advantage programs has increased 197% and 167%, respectively, over the past 10 years.

(1) The 2013 total for CVS/Aetna was reported by Aetna before its 2018 acquisition by CVS.

Of the 65.9 million people eligible for Medicare at the beginning of 2024, 33 million, slightly more than half, enrolled in a private Medicare Advantage plan operated by either a nonprofit or for-profit health insurer, but, increasingly, three of the big for-profits grabbed most new enrollees. Of the 1.7 million new Medicare Advantage enrollees this year, 86% were captured by UnitedHealth, Humana and Aetna. Those three companies are the leaders in the Medicare Advantage business among the for-profit companies, and, according to the health care consulting firm Chartis, are taking over the program “at breakneck speed.”

(1) The 2013 total for CVS/Aetna was reported by Aetna before its 2018 acquisition by CVS. (2,3) Centene’s and Molina’s totals include Medicare Supplement; they do not break out enrollment in the two Medicare categories separately.

It is worth noting that although four companies saw growth in their Medicare Supplement enrollment over the decade, enrollment in Medicare Supplement policies has been declining in more recent years as insurers have attracted more seniors and disabled people into their Medicare Advantage plans.

OTHER FEDERAL PROGRAMS

In addition to the above categories, Humana and Centene have significant enrollment in Tricare, the government-financed program for the military. Humana reported 6 million military enrollees in 2023, up from 3.1 million in 2013. Centene reported 2.8 million in 2023. It did not report any military enrollment in 2013.

Elevance reported having 1.6 million enrollees in the Federal Employees Health Benefits Program in 2023, up from 1.5 million in 2013. That total is included in the commercial enrollment category above.

At Cigna, Express Scripts’ pharmacy operations now contribute more than 70% to the company’s total revenues. Caremark’s pharmacy operations contribute 33% to CVS/Aetna’s total revenues, and Optum Rx contributes 31% to UnitedHealth’s total revenues.

WHAT TO DO AND WHERE TO START

The official name of the ACA is the Patient Protection and Affordable Care Act. The law did indeed implement many important patient protections, and it made coverage more affordable for many Americans. But there is much more Congress and regulators must do to close the loopholes and dismantle the barriers erected by big insurers that enable them to pad their bottom lines and reward shareholders while making health care increasingly unaffordable and inaccessible for many of us.

Several bipartisan bills have been introduced in Congress to change how big insurers do business.

And as noted above, President Biden has asked Congress to broaden the recently enacted $2,000-a-year cap on prescription drugs to apply to people with private insurance, not just Medicare beneficiaries. That one policy change could save an untold number of lives and help keep millions of families out of medical debt. (A coalition of more than 70 organizations and businesses, which I lead, supports that, although we’re also calling on Congress to reduce the current overall annual out-of-pocket maximum to no more than $5,000.)

I encourage you to tell your members of Congress and the Biden administration that you support these reforms as well as improving, strengthening and expanding traditional Medicare. You can be certain the insurance industry and its allies are trying to keep any reforms that might shrink profit margins from becoming law.

If a picture is worth a thousand words, a video, if done well, can be worth thousands more.

Regular readers of HEALTH CARE un-covered know we have published lots of words about the barriers health insurance companies have erected that make it harder and harder for patients to get the care their doctors know they need.

It’s a perfect example of how something that was designed to protect patients from inappropriate and unnecessary care has been weaponized by health insurers to pad their bottom lines.

Prior authorization in today’s world all too often serves as a bureaucratic barrier, requiring patients and their doctors to obtain approval in advance from insurers before certain treatments, medications, or procedures will be covered.

While insurance companies argue that prior authorization helps control costs and ensure appropriate care, the reality is far grimmer.

Both patients and their health care providers suffer the consequences. Patients frequently face delays in receiving necessary treatments or medications, exacerbating their health conditions and causing unnecessary stress and anxiety. Many forgo needed care altogether due to the complexities and frustrations of navigating the prior authorization process. This practice not only undermines patients’ trust in their health care providers but also compromises their health, often leading to worsened conditions and, tragically, sometimes irreversible harm.

The burden of prior authorization falls heavily on clinicians and their office staff who must spend valuable time and resources navigating the bureaucratic red tape imposed by insurers. This administrative burden not only detracts from patient care but also contributes to physician burnout, dissatisfaction and moral crisis, according to many doctors.

Ultimately, the health insurance industry’s prioritization of profit over patient well-being is evident in its insistence on maintaining these barriers to care, perpetuating a system that defaults to financial gain at the expense of human lives.

The New York Times video cuts to the chase. Prior authorization, as practiced today by insurance companies, is “medical injustice disguised as paperwork.”

It’s no secret I feel strongly that “Medicare Advantage for All” is not a healthy end goal for universal health care coverage in our country. But I also recognize there are many folks, across the political spectrum, who see the program as one that has some merit. And it’s not going away anytime soon. To say the insurance industry has clout in Washington is an understatement.

As politicians in both parties increase their scrutiny of Medicare Advantage, and the Biden administration reviews proposed reforms to the program, I think it’s important to highlight common-sense, achievable changes with broad appeal that would address the many problems with MA and begin leveling the playing field with the traditional Medicare program.

1. Align prior authorization MA standards with traditional Medicare

Since my mother entered into an MA plan more than a decade ago, I’ve watched how health insurers have applied practices from traditional employer-based plans to MA beneficiaries. For many years, insurers have made doctors submit a proposed course of treatment for a patient to the insurance company for payment pre-approval — widely known as “prior authorization.”

While most prior authorization requests are approved, and most of those denied are approved if they are appealed, prior authorization accomplishes two things that increase insurers’ margins.

The practice adds a hurdle between diagnosis and treatment and increases the likelihood that a patient or doctor won’t follow through, which decreases the odds that the insurer will ultimately have to pay a claim. In addition, prior authorization increases the length of time insurers can hold on to premium dollars, which they invest to drive higher earnings. (A considerable percentage of insurers’ profits come from the investments they make using the premiums you pay.)

Last year, the Kaiser Family Foundation found the level of prior authorization requests in MA plans increased significantly in recent years, which is partially the result of the share of services subject to prior authorization increasing dramatically. While most requests were ultimately approved (as they were with employer-based insurance plans), the process delayed care and kept dollars in insurers’ coffers longer.

The outrage generated by older Americans in MA plans waiting for prior authorization approvals has moved the Biden administration to action.

Beginning in 2024, MA plans may be no more restrictive with prior authorization requirements than traditional Medicare.

That’s a significant change and one for which Health and Human Services Secretary Xavier Becerra should be lauded.

But as large provider groups like the American Hospital Association have pointed out, the federal government must remain vigilant in its enforcement of this rule. As I wrote about recently with the implementation of the No Surprises Act, well-intentioned legislation and implementation rules put in place by regulators can have little real-world impact if insurers are not held accountable. It’s important to note, though, that federal regulatory agencies must be adequately staffed and resourced to be able to police the industry and address insurers’ relentless efforts to find loopholes in federal policy to maximize profits. Congress needs to provide the Department of Health and Human Services with additional funding for enforcement activities, for HHS to require transparency and reporting by insurers on their practices, and for stakeholders, especially providers and patients, to have an avenue to raise concerns with insurers’ practices as they become apparent.

2. Protect seniors from marketing scams

If it’s fall, it’s football season. And that means it’s time for former NFL quarterback Joe Namath’s annual call to action on the airwaves for MA enrollment.

As Congresswoman Jan Schakowsky and I wrote about more than a year ago, these innocent-appearing advertisements are misleading at their best and fraudulent at their worst. Thankfully, this is another area the Biden administration has also been watching over the past year.

CMS now prohibits the use of ads that do not mention a specific plan name or that use the Medicare name and logos in a misleading way, the marketing of benefits in a service area where they are not available, and the use of superlatives (e.g., “best” or “most”) in marketing when not substantiated by data from the current or prior year.

As part of its efforts to enforce the new marketing restrictions, the Center for Medicare and Medicaid Services for the first time evaluated more than 3,000 MA ads before they ran in advance of 2024 open enrollment. It rejected more than 1,000 for being misleading, confusing, or otherwise non-compliant with the new requirements. These types of reviews will, I hope, continue.

CMS has proposed a fixed payment to brokers of MA plans that, if implemented, would significantly improve the problem of steering seniors to the highest-paying plan — with the highest compensation for the insurance broker. I think we can all agree brokers should be required to direct their clients to the best product, not the one that pays the broker the most. (That has been established practice for financial advisors for many years.) CMS should see this rule through, and send MA brokers profiteering off seniors packing.

A bonus regulation in this space to consider: banning MA plan brokers from selling the contact information of MA beneficiaries. Ever wonder why grandma and grandpa get so many spam calls targeting their health conditions? This practice has a lot to do with it. And there’s bipartisan support in Congress for banning sales of beneficiary contact information.

In addition, just as drug companies have to mention the potential side effects of their medications, MA plans should also be required to be forthcoming about their restrictions, including prior authorization requirements, limited networks, and potentially high out-of-pocket costs, in their ads and marketing materials.

3. Be real about supplemental benefits

Tell me if this one sounds familiar. The federal government introduced flexibility to MA plans to offer seniors benefits beyond what they can receive in traditional Medicare funded primarily through taxpayer dollars.

Those “supplemental” benefits were intended to keep seniors active and healthy. Instead, insurers have manipulated the program to offer benefits seniors are less likely to use, so more of the dollars CMS doles out to pay for those benefits stay with payers.

Many seniors in MA plans will see options to enroll in wellness plans, access gym memberships, acquire food vouchers, pick out new sneakers, and even help pay for pet care, believe it or not — all included under their MA plan. Those benefits are paid for by a pot of “rebate” dollars that CMS passes through to plans, with the presumed goal of improving health outcomes through innovative uses.

There is a growing sense, though, that insurers have figured out how to game this system. While some of these offerings seem appealing and are certainly a focus of marketing by insurers, how heavily are they being used? How heavily do insurers communicate to seniors that they have these benefits, once seniors have signed up for them? Are insurers offering things people are actually using? Or are insurers strategically offering benefits that are rarely used?

Those answers are important because MA plans do not have to pay unused rebate dollars back to the federal government.

CMS in 2024 is requiring insurers to submit detailed data for the first time on how seniors are using these benefits. The agency should lean into this effort and ensure plan compliance with the reporting. And as this year rolls on, CMS should be prepared to make the case to Congress that we expect the data to show that plans are pocketing many of these dollars, and they are not significantly improving health outcomes of older Americans.

4. Addressing coding intensity

If you’re a regular reader, you probably know one of my core views on traditional Medicare vs. Medicare Advantage plans. Traditional Medicare has straightforward, transparent payment, while Medicare Advantage presents more avenues for insurers to arbitrarily raise what they charge the government. A good example of this is in higher coding per patient found in MA plans relative to Traditional Medicare.

An older patient goes in to see their doctor. They are diagnosed, and prescribed a course of treatment. Under Traditional Medicare, that service performed by the doctor is coded and reimbursed. The payment is generally the same no matter what conditions or health history that patient brought into the exam room. Straightforward.

MA plans, however, pay more when more codes are added to a diagnosis.

Plans have advertised this to doctors, incentivizing the providers to add every possible code to a submission for reimbursement. So, if that same patient described above has diabetes, but they’re being treated for an unrelated flu diagnosis, the doctor is incentivized by MA to add a code for diabetes treatment. MA plans, in turn, get paid more by the government based on their enrollee’s health status, as determined based on the diagnoses associated with that individual.

Extrapolate that out across tens of millions of seniors with MA plans, and it’s clear MA plans are significantly overcharging the federal government because of over-coding.

One solution I find appealing: similar to fee-for-service, create a new baseline for payments in MA plans to remove the incentive to add more codes to submissions. Proposals I’ve seen would pay providers more than traditional Medicare but without creating the plan-driven incentive for doctors to over-code.

5. Focusing in on Medicare Advantage network cuts in rural areas

Rural America is older and unhealthier than the national average. This should be the area where MA plans should experience the highest utilization.

Instead, we’re seeing that the aggressive practices insurers use to maximize profits force many rural hospitals to cancel their contracts with MA plans. As we wrote about at length in December, MA is becoming a ghost benefit for seniors living in rural communities. The reimbursement rates these plans pay hospitals in rural communities are significantly lower than traditional Medicare. That has further stressed the low margins rural hospitals face.

As Congressional focus on MA grows, I predict more bipartisan recommendations to come forth that address the growing gap between MA plan payments and what hospitals need to be paid in rural areas.

If MA is not accepted by providers in older, rural America, then truly, what purpose does it serve?

Last Monday, two lawsuits were filed that strike at a fundamental challenge facing the U.S. health system:

In the District Court of NJ, a class action lawsuit (ANN LEWANDOWSKI v THE PENSION & BENEFITS COMMITTEE OF JOHNSON AND JOHNSON) was filed against J&J alleging the company had mismanaged health benefits in violation of the Employee Retirement Income Security Act (“ERISA”). As noted in the 74-page filing “This case principally involves mismanagement of prescription-drug benefits. “Over the past several years, defendants breached their fiduciary duties and mismanaged Johnson and Johnson’s prescription-drug benefits program, costing their ERISA plans and their employees millions of dollars in the form of higher payments for prescription drugs, higher premiums, higher deductibles, higher coinsurance, higher copays, and lower wages or limited wage growth… Defendants’ mismanagement is most evident in (but not limited to) the prices it agreed to pay one of its vendors—its Pharmacy Benefits Manager (“PBM”)—for many generic drugs that are widely available at drastically lower prices.”

The issue is this: what liability risk does a self-insured employer have in providing health benefits to their employees?

Is the structure of the plan, the selection of providers and vendors, and costs and prices experienced by employees subject to litigation? What’s the role of the employer in protecting employees against unnecessary costs?

On the same day, in the District Court of Eastern Wisconsin, an 85-page class action lawsuit was filed against Advocate-Aurora Health (AAH) claiming it “uses its market power to raise prices, limit competition and harm consumers in Wisconsin:

Forces commercial health plans to include all its “overpriced facilities” in-network even when they would prefer to include only some facilities.

Goes to “extreme efforts to drive out innovative insurance products that save commercial health plans and their members money.”

Suppresses competition through “secret and restrictive contract terms that have been the subject of bipartisan criticism.”

Acquires new facilities, which then allows it to raise prices due to reduced competition

… without intervention, the health system will continue to use “anticompetitive contracting and negotiating tactics to raise prices on Wisconsin commercial health plans and their members and use those funds for aggressive acquisitions and executive compensation.”

The issue is this: is a health system’s liable when its consolidation activities result in higher prices for services provided communities and employers in communities where they operate?

Is there a direct causal relationship between a system’s consolidation activities and their prices, and how should alleged harm be measured and remedied?

Two complicated issues for two reputable mega-players in the U.S. health system. Both lawsuits were brought as class actions which guarantees widespread media attention and a protracted legal process. And each contributes directly to the gradual erosion of public trust in the health system since the plaintiffs essentially claim the business practices of J&J and Advocate-Aurora willfully harm the individuals they pledge to serve.

In the November 2023 Keckley Poll, I asked the sample of 817 U.S. adults to assess the health system overall. The results were clear:

69% think the system is fundamentally flawed and in need of major change vs. 7% who think otherwise.

60% believe it puts its profits above patient care vs. 13% who disagree.

74% think price controls are needed vs. 7% who disagree.

83% believe having health insurance that’s ‘affordable and comprehensive’ is essential to financial security vs 3% who disagree.

52% feel confident in their ability to navigate the U.S. system “when I have a problem” vs. 32% who have mixed feelings and 16% who aren’t.

And 76% think politicians avoid dealing with healthcare issues because they’re complex and politically risky vs/ 6% who think they tackle them head-on.

The poll also asked their level of trust and confidence in five major institutions “to develop a plan for the U.S. health system that maximizes what it has done well and corrects its major flaws.”

Clearly, trust and confidence in the health system is low, and expectations about solutions fall primarily on hospitals and doctors. Lawsuits like these widen suspicion that the industry’s dominated first and foremost by Big Businesses focused on their own profitability before all else. And they pose particular problems for sectors in healthcare dominated by not-for-profit and public ownership i.e. hospitals, home care, public health agencies and others.

My take

These lawsuits address two distinct issues: the roles of employers in designing their health benefits for employees including the use of PBMs, and the justification for consolidation of hospital and ancillary services in markets.

But each lawsuit s predicated on a legal theory that prices set by organizations are geared more to corporate profits than public good and justifiable costs.

Pricing is the Achilles of the health system. Pushback against price transparency by some, however justified, has amplified exposure to litigation risk like these two and contributed to the public’s loss of trust in the system.

It is unlikely greater price transparency and business practice disclosures by J&J and Advocate-Aurora could have avoided these lawsuits, but it’s clearly a message that needs consideration in every organization.

Healthcare organizations and their trade groups can no longer defend against lack of transparency by defaulting to the complexity of our supply chains and payment systems. They’re excuses. The realities of generative AI and interoperability assure information driven healthcare that’s publicly accessible and inclusive of prices, costs, outcomes and business practices. In the process, the public’s interest will heighten and lawsuits will increase.

Private equity firms have drawn significant policy interest and scrutiny amid recent reports of surprise billing, rising out-of-pocket costs for patients and increased healthcare spending in the U.S., according to Health Affairs.

The Private Equity Stakeholder Project has found at least 386 hospitals in the U.S. that are owned by private equity firms.

Six things to know:

1. The 386 private equity–owned hospitals represent 9% of all private hospitals and 30% of all proprietary for-profit hospitals.

2. Thirty-four percent of private equity-owned hospitals serve rural populations.

3. Texas is the state with the most private equity-owned hospitals (85).

4. While New Mexico has fewer private equity-owned hospitals (17), it has the highest proportion of private equity-backed hospitals compared to all private non-government hospitals at 43%.

5. More than 24% of private equity-owned facilities are psychiatric hospitals.

6. A few private equity firms dominate the list, according to the Private Equity Stakeholder Project:

Apollo Global Management (LifePoint Health (Brentwood, Tenn.) and ScionHealth (Louisville, Ky.): 177 hospitals combined)

Equity Group Investments (Ardent Health Services (Nashville, Tenn): 30 hospitals)

One Equity Partners (Ernest Health (Albuquerque, N.M.): 27 hospitals)

GoldenTree Asset Management and Davidson Kempner (Quorum Health (Brentwood, Tenn.): 21 hospitals)

Bain Capital (Surgery Partners (Brentwood, Tenn.): 19 hospitals)

This week, Statpublished a scathing investigation into the way UnitedHealth Group subsidiary NaviHealth uses an algorithm, nH Predict, to deny Medicare Advantage (MA) patients access to rehabilitation services and long-term care. United set a target to keep rehab stays within one percent of nH Predict’s projection for the year.

Interviews with former case managers and access to internal documents reveal that NaviHealth employees faced disciplinary action and even termination if they approved care that strayed from these algorithmic recommendations.

UnitedHealthcare, the nation’s largest insurer, is now subject to a class-action lawsuit filed this week over these practices. But NaviHealth’s impact extends beyond just United beneficiaries, as other insurers, covering around 15M MA enrollees, also use its services.

The Gist:This article provides a stark example of what can happen when an artificial intelligence (AI) algorithm is used not to complement, but to replace, clinical judgment.

While profit incentives in US healthcare are nothing new, what’s pernicious about an algorithm like nH Predict is how it replaces individual patients, whose needs vary, with a theoretical “average patient”, whose health and life needs can be easily predicted by the handful of data points available to the insurer.

When patients fail to recover along expected timelines—that are imperfectly calculated by incomplete datasets—they’re the ones who suffer.

Saturday, Congress voted overwhelming (House 335-91, Senate 88-9) to keep the government funded until Nov. 17 at 2023 levels. No surprise. Congress is supposed to pass all 12 appropriations bills before the start of each fiscal year but has done that 4 times since 1970—the last in 1997. So, while this chess game plays out, the health system will soldier on against growing recognition it needs fixing.

In Wednesday night’s debate, GOP Presidential aspirant Nicki Haley was asked what she would do to address the spike in personal bankruptcies due to medical debt. Her reply:

“We will break all of it [down], from the insurance company, to the hospitals, to the doctors’ offices, to the PBMs [pharmacy benefit managers], to the pharmaceutical companies. We will make it all transparent because when you do that, you will realize that’s what the problem is…we need to bring competition back into the healthcare space by eliminating certificate of need systems… Once we give the patient the ability to decide their healthcare, deciding which plan they want, that is when we will see magic happen, but we’re going to have to make every part of the industry open up and show us where their warts are because they all have them”

It’s a sentiment widely held across partisan aisles and in varied degrees among taxpayers, employers and beyond. It’s a system flaw and each sector is complicit.

What seems improbable is a solution that rises above the politics of healthcare where who wins and loses is more important than the solutions themselves.

Perhaps as improbable as the European team’s dominating performance in the 44th Ryder Cup Championship played in Rome last week especially given pre-tournament hype about the US team.

While in Rome last week, I queried hotel employees, restaurant and coffee shop owners, taxi drivers and locals at the tournament about the Italian health system. I saw no outdoor signage for hospitals and clinics nor TV ads for prescriptions and OTC remedies. Its pharmacies, clinics and hospitals are non-descript, modest and understated. Yet groups like the World Health Organization (WHO) and the Organization for Economic Cooperation Development (OECD) rank Servizio Sanitario Nazionale (SSN), the national system authorized in December 1978, in the top 10 in the world (The WHO ranks it second overall behind France).

“It covers all Italian citizens and legal foreign residents providing a full range of healthcare services with a free choice of providers. The service is free of charge at the point of service and is guided by the principles of universal coverage, solidarity, human dignity, and health. In principle, it serves as Italy’s public healthcare system.” Like U.S. ratings for hospitals, rankings for the Italian system vary but consistently place it in the top 15 based on methodologies comparing access, quality, and affordability.

The U.S., by contrast, ranks only first in certain high-end specialties and last among developed systems in access and affordability.

Like many systems of the world, SSN is governed by a national authority that sets operating principles and objectives administered thru 19 regions and two provinces that deliver health services under an appointed general manager. Each has significant independence and the flexibility to determine its own priorities and goals, and each is capitated based on a federal formula reflecting the unique needs and expected costs for that population’s health.

It is funded throughnational and regional taxes, supplemented by private expenditure and insurance plans and regions are allowed to generate their own additional revenue to meet their needs. 74% of funding is public; 26% is private composed primarily of consumer out-of-pocket costs. By contrast, the U.S. system’s funding is 49% public (Medicare, Medicaid et al), 24% private (employer-based, misc.) and 27% OOP by consumers.

Italians enjoy the 6th highest life expectancy in the world, as well as very low levels of infant mortality. It’s not a perfect system: 10% of the population choose private insurance coverage to get access to care quicker along with dental care and other benefits. Its facilities are older, pharmacies small with limited hours and hospitals non-descript.

But Italians seem satisfied with their system reasoning it a right, not a privilege, and its absence from daily news critiques a non-concern.

Issues confronting its system—like caring for its elderly population in tandem with declining population growth, modernizing its emergency services and improving its preventive health programs are understood but not debilitating in a country one-fifth the size of the U.S. population.

My take:

Italy spends 9% of its overall GDP on its health system; the $4.6 trillion U.S spends 18% in its GDP on healthcare, and outcomes are comparable. Our’s is better known but their’s appears functional and in many ways better.

Should the U.S.copy and paste the Italian system as its own? No. Our societies, social determinants and expectations vary widely. Might the U.S. health system learn from countries like Italy? Yes.

Questions like these merit consideration:

Might the U.S. system perform better if states had more authority and accountability for Medicare, CMS, Veterans’ health et al?

Might global budgets for states be an answer?

Might more spending on public health and social services be the answer to reduced costs and demand?

Might strict primary care gatekeeping be an answer to specialty and hospital care?

Might private insurance be unnecessary to a majority satisfied with a public system?

Might prices for prescription drugs, hospital services and insurance premiums be regulated or advertising limited?

Might employers play an expanded role in the system’s accountability?

Can we afford the system long-term, given other social needs in a changing global market?

Comparisons are constructive for insights to be learned. It’s true in healthcare and professional golf. The European team was better prepared for the Ryder Cup competition. From changes to the format of the matches, to pin placements and second shot distances requiring precision from 180-200 yards out on approach shots: advantage Europe. Still, it was execution as a team that made the difference in its dominating 16 1/2- 11 1/2 win —not the celebrity of any member.

The time to ask and answer tough questions about the sustainability of the U.S. system and chart a path forward. A prepared, selfless effort by a cross-sector Team Healthcare USA is our system’s most urgent need. No single sector has all the answers, and all are at risk of losing.

Team USA lost the Ryder Cup because it was out-performed by Team Europe: its data, preparation and teamwork made the difference.

Today, there is no Team Healthcare USA: each sector has its stars but winning the competition for the health and wellbeing of the U.S. populations requires more.

An article published this week in Stat documents private equity’s move into the cardiovascular space. There’s reason to suspect private equity ownership could exacerbate cardiology’s overuse problem, according to several cardiologists and researchers. Studies has found private equity acquisition results in more patients, more visits per patient, and higher charges.

Outpatient atherectomies have become a poster child for overutilization, with the volume billed to Medicare more than doubling from 2011-2021.

The Gist: Fueled by the growing number of states allowing outpatient cardiac catheterization, all signs point to cardiovascular practices being the next specialty courted for PE rollups.

However, the service line brings more complexities to deal structure and future returns than recent targets like dermatology and orthopedics. Heart and vascular groups are more heterogeneous, and less profitable medical management of conditions like congestive heart failure accounts for a greater portion of patient volume. Much more of the medical group business is intertwined with inpatient care, and, unlike other proceduralists, around 80 percent of cardiologists are already employed by health systems. While that doesn’t mean health systems are safe from cardiologists seceding for the promise of PE windfalls,

the closer PE firms get to the “heart” of medicine, the more they’ll find their standard playbook at odds with the broad spectrum of care that cardiovascular specialists provide—and the more they’ll find that partnering with local hospitals will be non-negotiable to maintain the book of business.

In the mid-1980’s, managed care advocate Dr. Paul Ellwood predicted that eventually, US healthcare would be dominated by perhaps a dozen vast national firms he called SuperMeds that would combine managed care based health insurance with care delivery systems. Ellwood was a leader of the “managed competition” movement which advocated for a private sector alternative to a federal government-run National Health Insurance system. Ellwood and colleagues believed that Kaiser Foundation Health Plans and other HMOs would be able to stabilize health costs and thus affordably extend care to the uninsured.

The US political system and market dynamics would not co-operate with Ellwood and his Jackson Hole Group’s vision. In the ensuing thirty-five years, healthcare has remained both highly fragmented and regional in focus. However, unbeknownst to most, during the past decade, as a result of a major merger and relentless smaller acquisitions, two SuperMeds were born- CVS/Aetna and UnitedHealth Group, that whose combined revenues comprise 14% of total US health spending.

CVS/Aetna is slightly larger than United, by dint of grocery sales in its drugstores and its vast Caremark pharmacy benefits management business. However, CVS’s Aetna health insurance arm is one third the size of United’s, and though CVS is rapidly scaling up its care delivery apparatus through its in-store Health Hubs, it remains is a tiny fraction of United’s care footprint. Despite being slightly smaller at the top line, United’s market capitalization is more than 3.5 times that of CVS.

United’s vast scope is difficult to comprehend because much of it is not visible to the naked eye, and the most rapidly growing businesses are partly nested inside United’s health insurance business.

United employs over 300 thousand people. At $287.6 billion total revenues in 2021, United exceeded 7% of total US health spending (though $8.3 billion are from overseas operations).

In 2021, United was $100 billion larger than the British National Health Service. It is more than three times the size of Kaiser Permanente, and five times the size of HCA, the nation’s largest hospital chain. United is both larger and richer than energy giant Exxon Mobil. United has over $70 billion in cash and investments, and is generating about $2 billion a month in operating cash flow.

Its highly regulated health insurance business is the visible tip of a rapidly growing iceberg. Revenue from United’s core health insurance business grew at 11% in 2021, compared to 14% growth in United’s diversified Optum subsidiary. Optum generated $155.6 billion in 2021 (of which 60% were from INSIDE United’s health insurance business). You can see the relationship of Optum’s three major businesses to United’s health insurance operations in Exhibit I.

Optum is the Key to United’s Growth

Understanding the role of Optum is key to understanding United’s business. It is remarkable how few of my veteran health care colleagues have any idea what Optum is or what it does. Optum was once a sort of dumping ground for assorted United acquisitions without a seeming core purpose. A private equity colleague once derided Optum as “The Island of Lost Toys”. Now, however, Optum is driving United’s growth, and generates billions of dollars in unregulated profits both from inside the highly regulated core health insurance business and from external customers.

Optum consists of three parts:Optum Health, its care delivery enterprise ($54 billion revenues in 2021), Optum Rx, its pharmacy benefits management enterprise ($91 billion revenues in 2021) and Optum Insight, a diversified business services enterprise ($12.2 billion in 2021). Virtually all of United’s acquisitions join one of these three businesses.

Optum Health: The Third Largest Care Delivery Enterprise in the US

By itself, Optum Health is almost the size of HCA ($54 billion in 2021 vs HCA’s $58.7 billion) and consists of a vast national portfolio of care delivery entities: large physician groups, urgent care centers, surgicenters, imaging centers, and now by dint of the recently announced $5.7 billion acquisition of LHC, home health agencies. Optum Health has studiously avoided acquiring beds of any kind: hospitals, nursing homes, etc. and likely will continue to do so. Optum Health’s physician groups not only generate profits on their own, but also provide powerful leverage for United to control health costs for its own subscribers, pushing down United’s highly visible and regulated Medical Loss Ratio (MLR), and increasing health plan profits.

Optum Health began in 2007 when United acquired Nevada-based Sierra Health, and thus became the new owner of a small multispecialty physician group which Sierra owned. The group did not belong in United’s health insurance business and came to rest over in Optum. Over the past twelve years, Optum Health has acquired an impressive percentage of the major capitated medical groups in the US- Texas’ WellMed, California’s HealthCare Partners (from DaVita), as well as Monarch, AppleCare and North American Medical Management, Massachusetts’ Reliant (formerly Fallon Clinic) and Atrius in Massachusetts (pending) , Kelsey Seybold Clinic (also pending) in Houston, TX and Everett Clinic and PolyClinic in Seattle.

Optum Health claims over 60 thousand physicians, though many of these are actually independent physicians participating in “wrap around” risk contracting networks. By comparison, Kaiser Permanente’s Medical Groups employ about 23 thousand physicians. United’s management claims that Optum Health provides continuing care to about 20 million patients, of whom 3 million are covered by some form of so-called “value based” contracts. Perhaps half of this smaller number are covered by capitated (percentage of premium-PMPM) contracts.

Optum Health straddles fierce competitive relationships between United’s health insurance business and competing health plans in well more than a dozen metropolitan areas. Almost half (44%) of Optum Health’s revenues come from providing care for health plans other than United.

When Optum acquires a large physician group, it acquires those groups’ contracts with United’s health insurance competitors, some of which contracts have been in place for decades. Premium revenues from other health plans, presumably capitation or per member per month (PMPM) revenues, are one-quarter of Optum Health’s $54 billion total revenues. These “external” premium revenues have quadrupled since 2018, largely for Medicare Advantage subscribers. Optum Health contributes about $4.5 billion in operating profit to United. It is impossible to determine from United’s disclosures how much of this profit comes from Optum Health’s services provided to United’s insured lives and how much from its medical groups’ extensive contracts with competing health plans.

Optum Health’s surgicenters and urgent care centers provide affordable alternatives to using expensive hospital outpatient services and emergency departments, potentially further reducing United medical expense. This creates obvious tensions with United’s hospital networks, since Optum Health can use its large medical practices and virtual care offerings to divert patients from hospitals to its own services, or else render those services unnecessary.

Though some observers have termed Optum/United’s business model “vertical integration”-ownership of the suppliers to and distributors of a firm’s product– Optum Health has actually grown less vertical since 2018, with revenues from competing health plans growing from 36% of total revenues in 2018 to 44% in 2021. A 2018 analysis by ReCon Strategy found at best a sketchy matchup between United’s health plan enrollment by market and its Optum Health assets (https://reconstrategy.com/2018/04/uniteds-medicare-advantage-footprint-and-optumcare-network-do-not-overlap-much-so-far/.

Optum Rx: The Nation’s Third Largest Pharmacy Benefits Management Business

Optum’s largest business in revenues is its Optum Rx pharmaceutical benefits management (PBM) business, which generates $91 billion in revenues, and processes over a billion pharmacy claims not only for United but also many competing insurers and employer groups. Pharmaceutical costs are a rapidly growing piece of total medical expenses, and controlling them is yet another source of largely unregulated profits for United; Optum Rx generated over $4.1 billion of operating profit in 2021.

Optum Rx is the nation’s third largest PBM business after Caremark, owned by CVS/Aetna and Express Scripts, owned by CIGNA, and processes about 21% of all scripts written in the US. Pharmacy benefits management firms developed more than two decades ago to speed the conversion of patients from expensive branded drugs to generics on behalf of insurers and self-funded employers. They were given a big boost by George Bush’s 2004 Medicare Part D Prescription Drug benefit, as a “pro-competitive” private sector alternative to Medicare directly negotiating prices with pharmaceutical firms.

Reducing drug spending is one key to United’s profitability. Since generics represent almost 90% of all prescriptions written, Optum Rx now relies on fees generated by processing prescriptions and on rebates from pharmaceutical firms to promote their costly branded drugs as preferred drugs on Optum Rx’s formularies. These rebates are determined based on “list” prices for those drugs vs. the contracted price for the PBMs, and are actual cash payments from manufacturers to PBMs.

Drug rebates represent a significant fraction of operating profits for health insurers that own PBMs, particularly for their older Medicare Advantage patients that use a lot of expensive drugs. Unfortunately, PBMs have incentives to inflate the list price, because rebates are caculated based on the spread between list prices and the contract pricel Unfortunately, this increases subscribers’ cash outlays, because patient cost shares are based on list prices.

Optum Rx generates about 39% of its revenues (and an undeterminable percentage of its profits) serving other health insurers and self-funded employers. Many of those self-funded employers demand that Optum pass through the rebates directly to them (even if it means being charged higher administrative fees!).

Unlike the situation with Optum Health, the “verticality” of Optum’s PBM business-the percentage of Optum revenues derived from serving United subscribers- has increased in the last seven years, to more than 60% of Optum Rx’s total business. What happens to the billions of dollars in rebates generated by Optum Rx is impossible to determine from United’s disclosures. However, our best guess is that pharmaceutical rebates represent as much as a quarter of United’s total corporate profits.

Optum Insight: “Intelligent” Business Solutions

The fastest growing and by far the most profitable Optum business is its business intelligence/business services/consulting subsidiary. Optum Insight was generated $12.2 billion in revenues in 2021, but a 27.9% operating margin, five times that of United’s health insurance business. Optum Insight is strategically vital to enhancing the profitability of United’s health insurance activities, but also generates outside revenues selling services to United’s health insurance competitors and hospital networks.

The core of Optum Insight is a business intelligence enterprise formerly known as Ingenix, which provided “big data” to United and other insurers about hospital and pricing behavior and utilization-crucial both for benefits design and administration. In 2009, Ingenix was accused by New York State of under reporting prices for out of network health services for itself and its clients, which had the effect of reducing its own medical reimbursements, and increasing patient cost shares. United signed a consent decree to alter Ingenix business practices and settled a raft of lawsuits filed on behalf of patients, physicians and employers. Its name was subsequently changed to Optum Insight.

By dint of aggressive acquisitions, Optum Insight has dramatically increased its medical claims management business, consulting services and business process outsourcing activities. . Most of United’s investment in artificial intelligence can be found inside Optum Insight. Big data plays a crucial role in United’s overall strategy. Optum Insight’s claims management software uses vast medical claims data bases and artificial intelligence/machine learning software to spot and deny medical claims for which documentation is inadequate or where services are either “inappropriate” or else not covered by an individual’s health plan. Providers also claim that the same software rejects as many as 20% of their claims, often for problems as tiny as a mis-spelled word or a missing data field.

Optum Insight software plays a crucial role in helping United’s health insurance plans manage their medical expense. Traditional health plan profitability is generated by reducing medical expense relative to collected premiums to increase underwriting profit. These profits are regulated, with highly variable degrees of rigor by state health insurance commissioners, and also by provisions of ObamaCare enacted in 2010.

Though its acquisition of Equian in 2019 and the proposed $13 billion acquisition of health information technology conglomerate Change Healthcare in 2021, United came within an eyelash of a near monopoly on “intelligent” medical claims processing software. The Justice Department challenged this latter acquisition and United may agree to divest Change’s claims processing software business as a condition of closing the deal. Even without the Change acquisition, Optum Insight processes hundreds of millions of medical claims annually not only for United’s health insurance business but for many of United’s competitors.

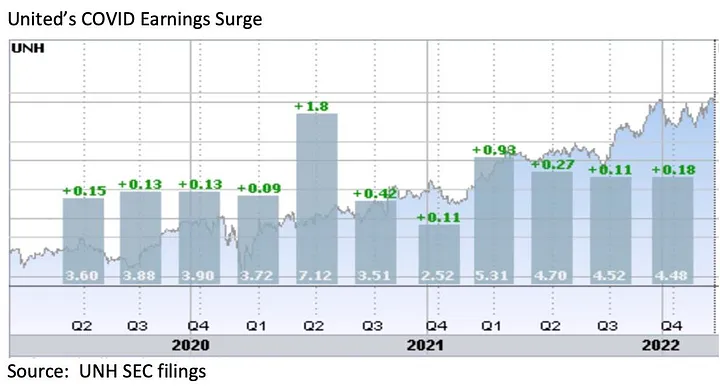

However, Optum Insight’s claims management system can also be used to increase MLR if medical expense unexpectedly declines, exposing the firm to federal requirement that it rebate excessive ‘savings’ to subscribers. This happened in 2020, when the COVID pandemic dramatically and unexpectedly added billions to United’s earnings due to hospitals suspending elective care. The chart below shows United’s 2Q2020 earnings per share almost doubling due to the precipitous drop in its medical claims expenses!

Hospital finance colleagues reported an immediate and substantial drop in medical claims denials from United and other carriers in the summer and fall of 2020. United’s quarterly profits dutifully and steeply declined in the subsequent two quarters, because its medical expenses sharply rebounded. The rise in

United’s medical expenses helped the firm avoid premium rebates to patients required by provisions of the ObamaCare legislation passed in 2010. The firm did voluntarily rebate about $1.5 billion to many of its customers in June, 2020.

However the most rapidly growing part of Optum Insight is its Optum 360 business process outsourcing business, which helps hospitals manage their billing and collections revenue cycle, as well as information technology operations, supply chain (purchasing and materials management) and other services. Through Optum 360, Optum Insight has signed five long term master contracts in the past two years’ worth many billions of dollars with care providers in California, Missouri and other states to provide a broad range of business services.

With all these different businesses, it is theoretically possible for one piece of Optum to be reducing a hospital’s cash flow by denying medical claims for United subscribers, while United’s health insurance network managers bargain aggressively to reduce the hospital’s reimbursement rates while yet another piece of Optum runs the billing and collection services for the same hospital and its employed physicians, while yet another piece of Optum competes with the hospital’s physicians and ambulatory services, diverting patients from its ERs and clinics, reducing the hospital’s revenues.

It is not difficult to imagine a future in which Optum/United offers hospital systems an Optum 360 outsourcing contract that run most of the business operations of a hospital system in exchange for preferred United health plan rates, an AI-enabled EZ pass on its medical claims denials and inpatient referrals from Optum physician groups and urgent care centers, at the expense of competing hospitals.

Managing these potential conflicts will be an increasing challenge as these various businesses grow, placing intense pressure on United’s leadership to get the various pieces of United to work together. To many anxious hospital executives, United resembles nothing so much as the Kraken, rising up out of the sea, surrounding and engulfing them- a powerful friend perhaps or a fearsome foe. As you might expect, United’s growing market power and growth has generated a fierce backlash in the hospital management community.

What Business is United Healthcare In?

United Healthcare is the most successful business in the history of American healthcare. The rapid growth of Optum and continued health insurance enrollment growth from government programs like Medicaid and Medicare has created a cash engine which generates nearly $2 billion a month in free cash flow. Optum’s portfolio has given United an impressive array of tools, unequalled in the industry, to improve its profitability and to reach into every corner of the US health system. United Healthcare is managed care on steroids.

United’s diversified portfolio of businesses gives the firm what a finance-savvy colleague termed “optionality”- the ability to redirect capital and management attention to areas of growth and away from areas that have ceased to grow, in the US or overseas. With its substantial investable capital, it will have the pick of the litter of the 11 thousand digital health companies as the overextended digital health market consolidates. United will be able to use its vast resources to build state-of-the-art digital infrastructure to reach and retain patients and manage their care.

United’s main short term business risks seem to be running out of accretive transactions effectively to deploy its growing horde of capital and managing the firm’s rising political exposure. United has had tremendous business discipline and has shied away from speculative acquisitions that are not immediately accretive to earnings. If its earnings growth falters, however, it will also encounter pressure from the investment community to increase dividends (presently about 1.2%) or share buybacks to bolster its share price, or else divest some or all of Optum in order to “maximize shareholder value”.

Answering the question, “What Business is United In” is simple: just about everything in health but hospitals and nursing homes.

Answering the questions- who are its customers and what do they want? — is a great deal harder. The customers United serves are in a sort of cold war with one another. United’s original business was protecting employers from health cost growth , and tempering the influence of hospitals and doctors by reducing their rates and utilization. By fostering so-called Consumer Directed Health Plans that expose many of their subscribers to very high front-end copayments, United and its health insurance brethren, have also increased their out-of-pocket costs, whether they have the savings to pay them or not.

There are also some ironies in United’s development. Optum Insight’s suite of hospital business services are designed to reduce administrative costs created in major part by United and other insurers’ medical claims data requirements. Its PBM business, originally intended to reduce drug spending by bargaining aggressively with pharmaceutical manufacturers has ended up pushing up drug list prices and consumer cost shares.

While presumably everybody benefits if United can somehow help patients become and remain healthy, it is still far from obvious how to do this. Managing all these markedly divergent customer needs will be a tremendous management challenge for whoever succeeds United’s reclusive (and very effective) 70 year old Chairman Stephen Hemsley.

What Does Society Get from this Vast Enterprise?

However, as Peter Drucker told a different generation of business giants, businesses are not entities unto themselves, accountable only to shareholders and customers. They are organs of society, and are expected to create social value. Americans are suspicious of vast enterprises, as businesses from Standard Oil, US Steel and ATT to Microsoft and Facebook have learned. As businesses grow and become more successful, public suspicion grows.

Private health insurers already face strident opposition from progressive Democrats, who believe that health coverage ought to be a public good, a right of citizenship provided publicly; in other words, that private health insurers have no business being in business. And large insurers like United also face intense opposition from hospitals and many physicians because they reduce their incomes and impose major administrative burdens upon them.

In the age of Twitter and TikTok, United is highly vulnerable to “event risks” that confirm the hostile narratives of the firm’s detractors that United is mainly about maximizing its own profits, not about improving the health of its subscribers or the communities it serves. It is not clear how many the tens of millions of United subscribers have warm and fuzzy feelings about their giant health insurer. Memories of the HMO backlash of the 1990’s reside in the firm’s corporate memory.

United has grown to its present immense scale largely without public knowledge. United has within its reach the capability of constraining overall health cost growth across dozens of metropolitan areas and regions, not merely cost growth for its own beneficiaries (roughly one in seven US citizens already get their health insurance through United). With its expanding digital health operations, it can deploy state of the art tools for helping United’s 50 million subscribers avoid illness and live healthier lives.

United also has the ability to damage the financial operations of beloved local hospitals and deny coverage to families, raising their out of pocket expenses. How United frames and defends its social mission and how it manages all the delicate and increasingly fraught customer relationships will determine its future, and in important ways, ours as well.