Healthcare’s most recent billion-dollar deal took the industry by surprise, leaving medical experts and hospital leaders grappling to comprehend its implications.

In case you missed it, California-based Kaiser Foundation Health Plan and Hospitals, which make up the insurance and facilities half of Kaiser Permanente, announced the acquisition of Geisinger, a Pennsylvania-based health system once acknowledged by President Obama for delivering “high-quality care.”

Upon regulatory approval, Geisinger will become the first organization to join Risant Health, Kaiser Foundation’s newly created $5 billion subsidiary. According to Kaiser, the aim is to build “a portfolio of likeminded, nonprofit, value-oriented, community-based health systems anchored in their respective communities.”

Having spent 18 years as CEO of The Permanente Medical Group, the half of Kaiser Permanente responsible for the delivery of medical care, I took great interest in the announcement. And I wasn’t alone. My phone rang off the hook for weeks with calls from reporters, policy experts and healthcare executives.

After hundreds of conversations, here are the three most common questions I received about the acquisition—and the implications for doctors, insurers, health-system competitors and patients all over the country.

Question 1: Why did Kaiser acquire Geisinger?

Most callers wanted to know about Kaiser’s motivation, figuring there must’ve been more to the acquisition than the press release indicated. Although I don’t have inside information, I believe they were right. Here’s why:

Kaiser Permanente has a long and ongoing reputation for delivering nation-leading care. The organization has consistently earned the highest quality and patient-satisfaction rankings from the National Committee for Quality Assurance (NCQA), Leapfrog Group, JD Power and Medicare.

And yet, despite a 78-year history, dozens of hospitals and 13 million members across eight states, Kaiser Permanente is still considered a coastal—not national—health system. It maintains a huge market share in California and a strong presence in the Mid-Atlantic states, yet the organization has failed repeatedly to replicate that success in other geographies.

With that context, I see two compelling reasons why the Kaiser Foundation Health Plan and Hospitals wish to become a national brand:

- Influence. Elected officials and regulatory bodies often turn to healthcare’s biggest players to set legislative agendas and carve out national policy. At that table, there are a limited number of seats. By shedding its reputation as a “local” health system, Kaiser could earn one.

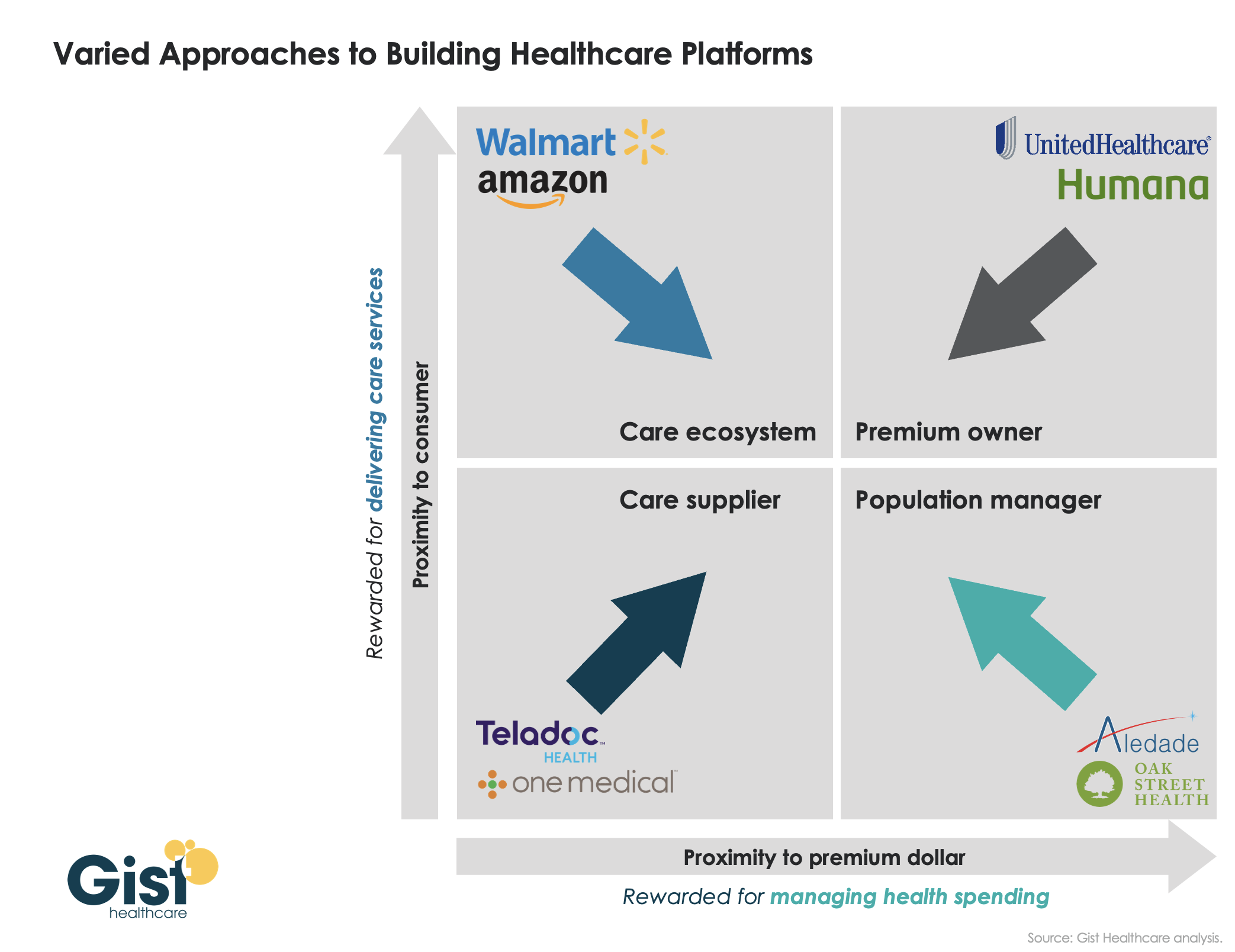

- Survival. In recent years, companies like Amazon, CVS and Walmart have been scooping up organizations that provide primary care, telehealth, home health and specialty care services. These “retail giants” are spending up to $13 billion per acquisition. And they’re consuming already-successful healthcare companies like One Medical, Oak Street Health, Signify, Pill Pack and many others. Like an army preparing for war, these corporate behemoths are amassing the components needed to battle the traditional healthcare incumbents and ultimately oust them entirely.

The Geisinger deal expands Kaiser’s footprint, adding 600,000 patients, 10 hospitals and 100 specialty and primary care clinics. These assets lend gravitas, even though Geisinger also comes with a 2022 operating loss of $239 million.

The lesson to draw from this first question is clear: size matters. The days of solo physicians and stand-alone hospitals are over. Nostalgia for medicine’s folksy, home-spun past is understandable but futile. To survive, healthcare players must get bigger quickly or team up with someone who can. That insight leads to the next question and lesson.

Question 2: How much value will Kaiser give Geisinger?

Almost everyone I’ve spoken with understands Kaiser’s desire for greater national influence, but they’re less sure how this deal will affect Geisinger Health.

Geisinger’s Pennsylvania-based hospitals and clinics have been locked in territorial battles for years with surrounding health systems. More recently, the pandemic, combined with staffing shortages and national inflation, have challenged Geisinger’s clinical performance and eroded its bottom line.

Assuming Kaiser plans to invest roughly $1 billion in each of the four to five health systems it’s planning to acquire, that surge in cash inflow will provide Geisinger with temporary financial safety. But the bigger question is how will Kaiser improve Geisinger’s value-proposition enough to grow its market share?

In public comments, Kaiser leaders spoke of the acquisition as an opportunity for Risant to “improve the health of millions of people by increasing access to value-based care and coverage, and raising the bar for value-based approaches that prioritize patient quality outcomes.”

Many of the experts I spoke with understand Kaiser’s value intent. But they question how Kaiser can could deliver on that promise since The Permanente Medical Group (TPMG) wasn’t involved in the deal.

If, hypothetically, Kaiser and Permanente leaders were to strike a deal to collaborate in the future, TPMG’s physician leaders could bring tremendous knowledge, experience and expertise to the table. Otherwise, I agree with those who’ve expressed doubt that Kaiser, alone, will be able to significantly improve Geisinger’s clinical performance.

Health plans and insurance companies play an important role in financing medical care. They possess rich data on performance and can offer incentives that boost access to higher-quality care. But insurers don’t work directly with individual doctors to coordinate medical care or advance clinical solutions on behalf of patients. And without strong physician leadership, the pace of positive change slows to a crawl. As a example, research conducted within The Permanente Medical Group found that it takes only three years to turn a proven clinical advance into standard practice—that’s nearly six times faster than the national average.

For decades, the secret sauce for Kaiser Permanente has been the cohesive success of its three parts: Kaiser Health Plan, Kaiser Foundation Hospitals and The Permanente Medical Group.

And KP’s results speak for themselves:

- 90% control of hypertension for members (compared to 60% for the rest of the country)

- 30% fewer deaths from heart attack and stroke (compared to the rest of the country)

- 20% fewer deaths from colon cancer

The big lesson: insurance, by itself, doesn’t drive major improvements in medicine. It must be a combined effort between forward-looking insurers and innovative, high-performing clinicians.

But there’s another takeaway here for doctors everywhere: now is the time to join forces with other clinicians in your community. Together, you can collaborate to improve clinical quality. You can augment access and make care more affordable for patients. Simultaneously, this is the time for the insurers and the retail giants to figure out which medical groups can deliver the best care and make the best partners. Neither side will flourish alone. And this leads to a third question and lesson.

Question 3: Will the deal work?

Almost all of my conversations ended with this query. I say it’s too early to tell. But as I look years down the road, one part of the deal, in particular, gives me doubt.

Today, Geisinger uses a hybrid reimbursement model—blending both “value-based” care payments with traditional “fee-for-service” insurance plans. In addition to offering its own coverage, it contracts with a variety of other insurance companies. Rarely have I seen this scattered approach succeed.

Most healthcare observers understand the inherent flaw in the “fee for service” (FFS) model is also its greatest appeal to providers: the more you do the more you earn. FFS is how nearly all financial transactions take place in America (i.e., provide a service, earn a fee). In medicine, however, this financial model results in frequent over-testing and over-treatment with minimal if any improvement in clinical outcomes, according to researchers.

The “value-based” alternative to FFS involves prepaying for care—a model often referred to as “capitation.” In short, capitation involves a single fee, paid upfront for all the medical care provided to a defined population of patients for one year based on their age and health status. The better an organization at preventing disease and avoiding complications from chronic illness, the greater its success in both clinical quality and affordability.

Within the small world of capitated healthcare payments, there’s an important element that often gets overlooked. It makes a big difference who receives that lump-sum payment.

In the case of Kaiser Permanente, capitated payments are made directly to the medical group and the physicians who are responsible for providing care. In almost every other health system, an insurance company collects capitated payments but then pays the medical providers on a fee-for-service basis. Even though the arrangement is referred to as capitated, the incentives are overwhelmingly tied to the volume of care (not the value of that care).

In a mixed-payment model, doctors and hospitals invariably prioritize the higher paying FFS patients over the capitated ones. When I think about these conflicting incentives, I’m reminded of a prominent medical group in California. It had a main entrance for its fee-for-service patients and a second, smaller one off to the side for capitated patients.

I doubt the time spent with the patient—or the overall care provided—was equal for both groups. When income is based on quantity of care, not quality, clinicians focus more on treating the complications of chronic disease and medical errors rather than preventing them in the first place. Geisinger has walked this tightrope in the past, but as economic pressures mount, I fear doctors will find the two sets of incentives conflicting and difficult to navigate.

The big lesson: as financial pressures mount, the most effective approaches of the past will likely fail in the future. All healthcare organizations will need to make a decision: keep trying to drive volume and prices up through FFS or shift to capitation. Getting caught in the middle is a prescription for failure.

Examining the healthcare acquisitions made by Amazon and CVS, it’s clear these giants have decided to move aggressively toward a model more like Kaiser Permanente’s—one that brings insurance, pharmacy, physicians and sophisticated IT systems under one roof. These companies, along with Walmart, are aggressively marching down a path toward capitation, focusing on Medicare Advantage (the value-based option for Americans 65+) as an entry point.

So far, Geisinger has hedged its bets by maintaining a hybrid revenue stream. I doubt they can do so successfully in the future. That brings us to a final question.

The biggest question remaining

Over the next decade, hospital systems, insurers and retailers will battle for healthcare supremacy. The most recent Kaiser-Geisinger deal reflects an industry that’s undergoing massive change as health systems face intensifying pressure to remain relevant.

The most important issue to resolve is whether these shifts will ultimately help or harm patients. I’m optimistic for a positive outcome.

Whether or not the retail giants displace the incumbents, they will redefine what it takes to win. For all their faults, companies like Amazon and Walmart care a lot about meeting the needs of customers—a mindset rarely found in today’s healthcare world. As these companies grow ever larger, they’ll place consumer-oriented demands on doctors and hospitals. This will require care providers to deliver higher quality care at more affordable prices.

The retailers will only do deals with the best of the best. And they’ll kick the underachievers to the curb. They’ll use their sophisticated IT systems to better coordinate and innovate medical care. Insurers, hospitals and doctors who fail to keep up will be left behind.

Over time, patients will find themselves with far more choices and control than they have today. And I’m optimistic that will be good for the health of our nation.