Cartoon – At $3,000 per Night

The government shutdown has left many federal workers furloughed, caused nationwide flight delays, left small businesses unable to access loans and put nonprofit services in jeopardy. It’s only expected to get worse.

As Congress remains deadlocked over passing a stopgap measure to reopen the government, thousands of Americans are at risk of losing benefits from the Supplemental Nutrition Assistance Program (SNAP); the Special Supplemental Nutrition Program for Women, Infants, and Children (WIC); and other programs at the beginning of November.

An additional burden on Americans is the start of open enrollment for the Affordable Care Act (ACA), also known as ObamaCare, on Nov. 1, where they will see more costly health insurance premium plans unless lawmakers act.

Democrats and Republicans have spent weeks pointing fingers at each other, with no deal in sight. The Senate on Tuesday failed to advance a Republican stopgap measure to end the shutdown for the 13th time, while the House was out of session and President Trump was traveling abroad.

With uncertainty around the shutdown’s timeline growing day by day, here are six ways Americans will start to feel more of the shutdown’s impact.

At least 670,000 federal workers have been furloughed while about 730,000 are working without pay as of Oct. 24, according to data from the Bipartisan Policy Center, a think tank based in Washington, D.C. The center estimates that if the shutdown continues through the beginning of December, federal civilian employees will miss roughly 4.5 million paychecks.

The American Federation of Government Employees (AFGE), the nation’s largest federal workers union, urged Congress to pass a “clean” funding measure known as a continuing resolution to reopen the government. AFGE President Everett Kelley said in an Oct. 27 statement, “No half measures, and no gamesmanship. Put every single federal worker back on the job with full back pay — today.”

However, House and Senate Democrats have resisted pressure from the union.

“I get where they’re coming from. We want the shutdown to end too. But fundamentally, if Trump and Republicans continue to refuse to negotiate with us to figure out how to lower health care costs, we’re in the same place that we’ve always been,” Sen. Tina Smith (D-Minn.) told The Hill on Tuesday.

The U.S. Department of Agriculture (USDA) said benefits won’t be issued on Nov. 1 for SNAP, a program that helps low-income families afford food. Nearly 42 million Americans rely on SNAP benefits every month, according to data from the USDA.

Though the USDA formed a plan earlier this year that said the department is obligated to use contingency funds to pay out benefits during a shutdown, it has since been deleted. The USDA wrote in a memo this month that the contingency fund is only designed for emergencies such as “natural disasters like hurricanes, tornadoes, and floods, that can come on quickly and without notice.”

Democratic officials in more than two dozen states sued the Trump administration this week, arguing the USDA is legally required to tap into those funds. But House Speaker Mike Johnson (R-La.) has claimed those funds are not “legally available.”

Families who rely on WIC, a program that provides food aid and other services to low-income pregnant and postpartum women, infants, and children younger than 5 years old, could also face trouble. The White House had provided $300 million to WIC to keep the program afloat in early October. But 44 organizations signed on to an Oct. 24 letter from the National WIC Association to the White House requesting an additional $300 million in emergency funds, warning that “numerous states are projected to exhaust their resources for WIC benefits” on Nov. 1.

Payday is coming up at the end of this week for members of the military.

Earlier this month, Trump directed Defense Secretary Pete Hegseth to “use all available funds” to pay troops. Officials ended up reallocating $8 billion in unspent funds meant for Pentagon research and development efforts toward service members’ paychecks. The administration also received a $130 million donation from a private donor to help cover military members’ paychecks.

Vice President Vance said he believes active-duty service members will get paid this Friday. But Treasury Secretary Scott Bessent told CBS News’s Margaret Brennan on Sunday that troops could go without pay on Nov. 15 if the shutdown continues.

Senate Democrats blocked a bill sponsored by Sen. Ron Johnson (R-Wis.) earlier this month to pay active-duty members and other essential federal workers.

At the center of the shutdown fight is the ACA subsidies, which are set to expire at the end of this year. Democrats have been urging Republicans to extend the subsidies, arguing that ACA health insurance premium costs will increase if no action is taken.

Americans can choose their insurance plans for next year on the federal Affordable Care Act exchange website starting Saturday. An analysis from KFF found that without the subsidies extended, Americans will see their marketplace premium payments increase by 114 percent.

Republicans have been firm in their position of reopening the government first before discussing the ACA subsidies.

“The expiring ObamaCare subsidy at the end of the year is a serious problem. If you look at it objectively, you know that it is subsidizing bad policy. We’re throwing good money at a bad, broken system, and so it needs real reforms,” Speaker Johnson said at a Monday press conference.

About 140 Head Start programs across 41 states and Puerto Rico serving more than 65,000 children could go dark if the shutdown goes past Nov 1., according to a joint statement from more than 100 national, state and local organizations focused on childhood education and development.

“Without funding, many of these programs will be forced to close their doors, leaving children without care, teachers without pay, and parents without the ability to work,” the statement says.

Head Start programs are designed to help low-income families and their children from birth to age 5 with a focus on health and wellness services, family well-being and engagement and early learning, according to its website.

Diane Yentel, president and CEO of the National Council of Nonprofits, told The Hill in a statement that the shutdown has forced many nonprofits to halt their operations because of frozen federal reimbursements and grants.

The nonprofits include those handling wildfire recovery in Colorado, housing vulnerable youth in Utah and helping with conservation work in Montana, Yentel said. Many federal workers without pay have also turned to their local food banks, further putting a financial strain on nonprofits.

“With the November 1 cutoff of SNAP and WIC looming, the situation will get even worse. Nonprofit food banks are already facing rising grocery costs and increased demand, including from federal workers and military families,” Yentel said. “If millions of Americans suddenly lose access to these life-saving nutrition programs, local nonprofits will be overwhelmed, and far too many seniors, children, and families will go without help.”

The Trump administration has made a flurry of recent moves aimed at lowering the cost of prescription drugs, including cutting deals with some of America’s top drugmakers and launching a new website to help consumers shop for the best available prices. We recently asked 10 experts — including health economists, drug policy scholars and industry insiders — to evaluate the likely impact of those maneuvers. Their verdict: Most are unlikely to deliver substantive savings, at least based on what we know today.

So, we followed up: If those moves won’t work, what could the administration do that would make a meaningful dent in America’s drug spending?

Here are three key ideas from the experts:

1. Expand Medicare’s new power to directly negotiate prices with drugmakers.

Compared to Trump’s recent ad hoc approach to cutting confidential deals with individual drug companies, some experts say building on Medicare’s new power to negotiate could offer a more sweeping, and potentially lasting, path to savings.

For example, Trump’s team could use the price negotiations to seek steeper discounts than the Biden administration did. Federal officials could also establish a more transparent and predictable formula for future negotiations — similar to the approaches used by other nations — and publish that framework so private insurance plans could use it to drive better deals with drugmakers, too.

Finally, the White House could urge lawmakers to loosen some of the limits Democrats in Congress placed on this power when they passed the law back in 2022. Medicare can currently only negotiate the price of drugs that have been on the market for at least several years — often after the medicines have already made drug companies billions of dollars.

Ideally, said Vanderbilt professor Stacie Dusetzina, “you would negotiate a value-based price at the time a product arrives on the market” — that’s what nations like France and England do.

2. Identify and fix policies that encourage wasteful spending on medicines.

“There are policies within everything — from the tax code to Medicare and Medicaid to health insurance regulations — that are driving up drug prices in this country,” said Michael Cannon, who directs health policy studies at the Cato Institute.

One example Cannon sees as wasteful: the formula that Medicare uses to pay for drugs administered by doctors, such as chemotherapy infusions. Those doctors typically get paid 106% of the price of whichever medicine they prescribe, creating a potential incentive to choose those that are most expensive — even in cases where cheaper alternatives might be available.

And that, according to Cannon, is just the tip of the “policy failure” iceberg.

The Trump administration is taking early steps to reform at least one federal drug-pricing policy, known as 340B, which lets some hospitals and clinics purchase drugs at a discount. More than $60 billion a year now flow through this program, whose growth has exploded in recent years. But researchers, auditors and lawmakers like Republican Sen. Bill Cassidy have questioned where all of that money is going and whether it’s making medicines affordable for as many patients as it should.

3. Speed up access to cheaper generic drugs.

Generic drugs — cheaper, copycat versions of brand-name medicines — can slash costs for patients and insurers by as much as 80% once they come to market. But this price-plunging competition often takes more than a decade to arrive.

That’s, in part, because drug companies have found a host of ways to game the U.S. patent system to protect and prolong their monopolies. Law professor Rachel Sachs at Washington University in St. Louis suggested Trump not only close those loopholes, but also make its own creative use of patents.

Federal officials could, for example, invoke an obscure law known as Section 1498, she said. That provision allows the U.S. government to effectively infringe on a patent to buy or make on the cheap certain medicines that meet an extraordinary need of the country. Sachs suggested that the drug semaglutide — the active ingredient in Ozempic, Wegovy and several other weight-loss medicines — might make for an ideal target.

“The statutory authority is already there for them to do it,” Sachs said. “It’s not clear to me why they haven’t.”

Semaglutide, which earned drugmakers more than $20 billion last year alone, will otherwise remain under patent in the U.S. until early next decade.

The Trump administration issued an executive order back in April signaling at least a high level of interest in some of these ideas — and a host of others, too. On the other hand, Trump and Congressional Republicans have made moves this year that have weakened some of these potential cost-cutting tools, such as Medicare’s power to negotiate drug prices. A key provision of July’s ‘Big Beautiful Bill,’ for example, shielded more medicines from those negotiations, eroding the government’s potential savings by nearly $9 billion over the next decade.

We should all get a better read soon on just how interested this administration is in cutting prices: Federal officials are expected to announce the results of their latest round of Medicare negotiations by the end of November.

We learned yesterday that the average cost of a family health insurance policy through an employer reached nearly $27,000 this year, 6% higher than what it cost in 2024. As if that weren’t alarming enough, researchers are predicting that the total likely will soar toward $30,000 next year because of rising medical costs and the unrelenting pressure insurers are under from Wall Street to increase their profits. Small businesses will be hit the hardest.

Despite repeated assurances from insurers that we can count on them to hold down the cost of health care – and consequently the premiums they charge – there are now many years of evidence – from researchers like KFF, which tracks annual changes in employer-sponsored coverage – that they have not and cannot deliver on their promises.

Nevertheless, Big Insurance is doing just fine financially as they force America’s employers and workers to shell out increasingly absurd amounts of money for policies that actually cover less than they did ten years ago. A health insurance policy today is generally less valuable than it was a decade ago because families have to spend more and more money out of their own pockets every year before their coverage kicks in. In addition, they are far more likely to be notified that their insurers will not cover the care their doctors say they need.

When you look at KFF’s reports over time, you’ll see that the cost of a family policy has increased 60% since 2014 when it cost an average of $16,834. That is a rate of increase much higher than general inflation and also higher than medical inflation.

Not only has the total cost of an employer-sponsored plan skyrocketed, so has the share of premiums workers must pay. This year, employers deducted an average of $6,850 from their workers’ paychecks for family coverage, up from $4,823 in 2014, a 42% increase.

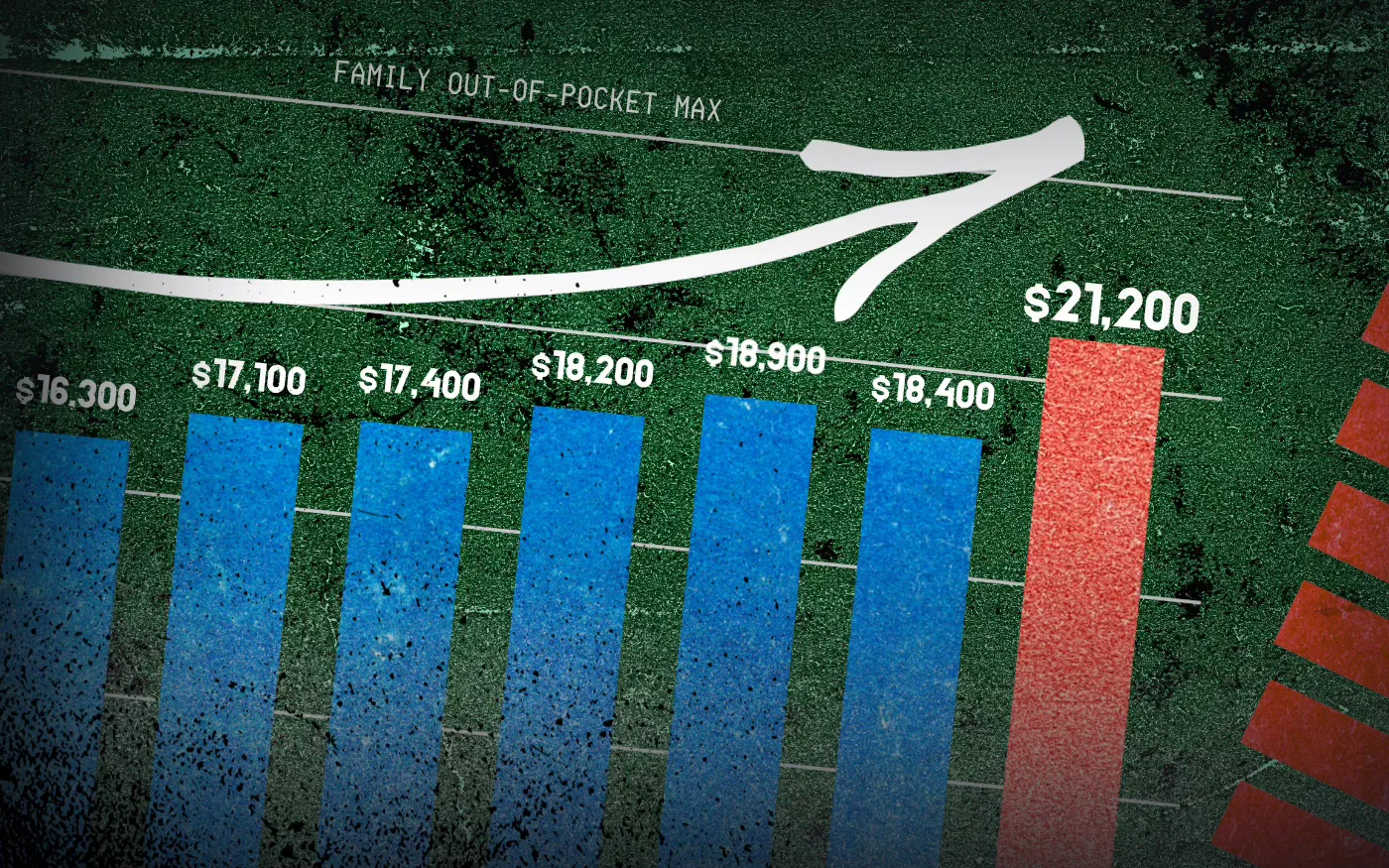

And as premiums have risen, so has the amount of money workers and their dependents are required to spend out of their pockets in deductibles, copayments and coinsurance. The Affordable Care Act, to its credit, instituted a cap on out-of-pocket expenses in 2014, but that cap has been increasing annually along with premiums. (The U.S. Department of Health & Human Services sets the out-of-pocket max every year, pegging it to the average increase in premiums.)

In 2014 the out-of-pocket cap for a family policy was $12,700. Next year, it will rise to $21,200 – a 67% increase. And keep in mind that the cap only applies to in-network care. If you go out of your insurer’s network or take a medication not covered under your policy, you can be on the hook for hundreds or thousands more. While most employer-sponsored plans have caps that are considerably lower, many individuals and families reach the legal max every year.

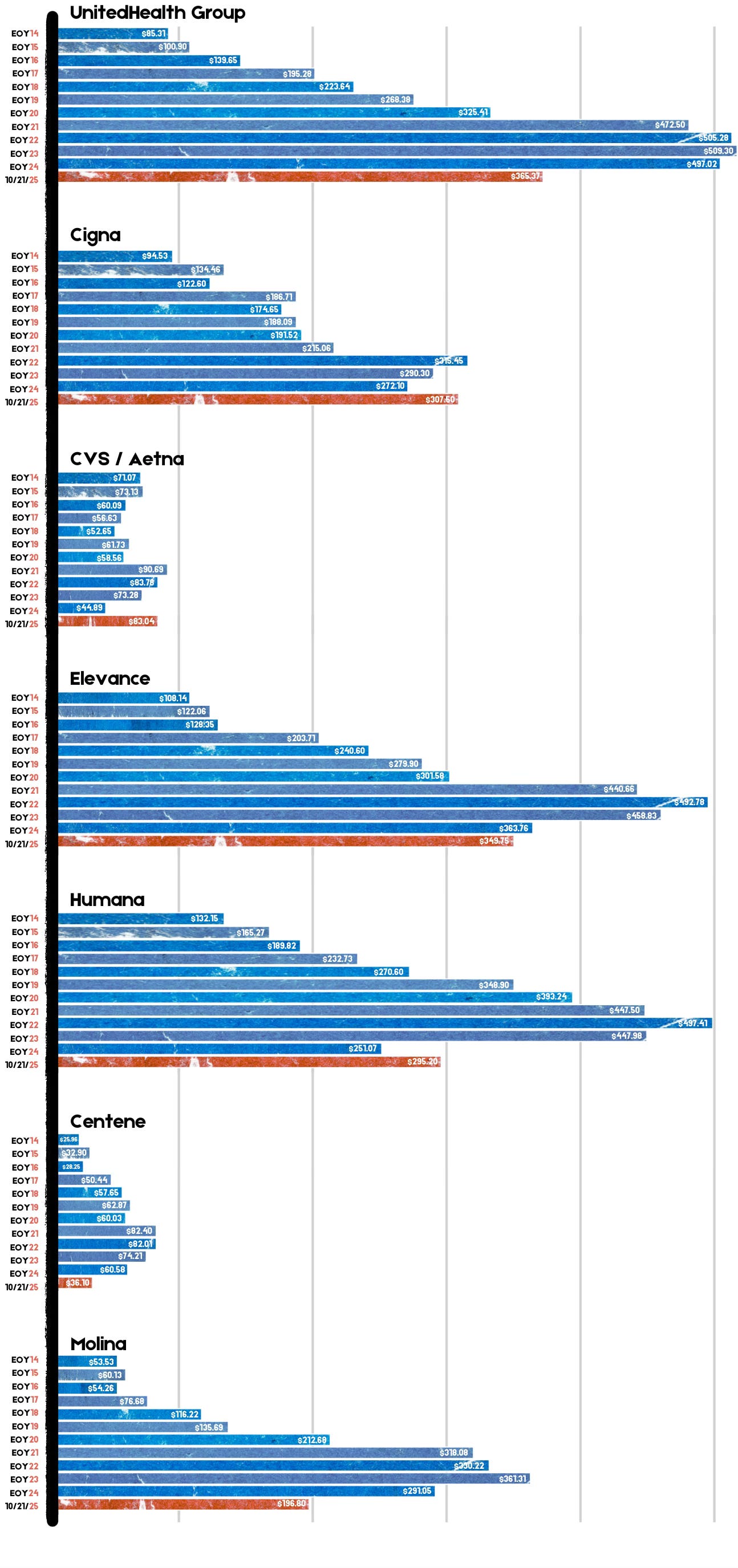

Meanwhile, the seven biggest for-profit health insurers have made hundreds of billions in profits since 2014 as they have jacked up premiums and out-of-pocket requirements and erected numerous barriers, including the aggressive use of prior authorization, that make it more difficult for Americans to get the care and medications they need. Collectively, those seven companies made $71.3 billion in profits last year alone. That was up slightly from $70.7 billion in 2023. Insurers said their 2024 profits were somewhat depressed because more of their health plan enrollees went to the doctor and picked up their prescriptions last year. Investors were furious that insurers couldn’t keep that from happening, as you’ll see in the charts below. Many of them sold some or all of their shares, sending insurers’ stock prices down. But overall, the stock prices of the big insurance conglomerates have increased steadily over the years as we and our employers have had to spend more for policies that cover less.

For example, UnitedHealth Group, the biggest of the seven, saw its stock price increase 483% between 2014 and 2024 – from $85.31 a share on Dec. 31, 2014, to $497.02 on Dec. 31, 2024. Most of the other companies saw similar growth in their shares over that time period.

By contrast, the Dow Jones Industrial Average increased 139% (from $17,823.07 to $42,544.22), and the S&P 500 increased 186% (from $2,058.90 to $5,881.63) during the same period.

Back to those premiums and out-of-pocket requirements. While the KFF numbers pertain to employer-sponsored coverage, people who have to buy health insurance on their own – mostly through the ACA (Obamacare) marketplace – have experienced similar increases. Most Americans who buy their insurance there could not possibly afford it if not for subsidies provided by the federal government on a sliding scale, which is based on income. The most generous subsidies have been available since 2014 to people with income up to 150% of the federal poverty level (FPL). During the pandemic, Congress expanded – or “enhanced” – the subsidies to make them available to people with incomes up to 400% of FPL. Those enhanced subsidies are scheduled to expire at the end of this year. Whether to let them expire or extend them is at the center of the ongoing government shutdown. Most Democrats are insisting they be extended while most Republicans want them to end. It’s important to note that the federal money goes to insurance companies, not to people enrolled in their health plans.

If the enhanced subsidies do end, millions of Americans who get their health insurance through the ACA marketplace will drop their coverage because the premiums will be unaffordable for them and their families. In Pennsylvania where I live, premiums for policies bought on the state’s insurance exchange are expected to increase 102% next year because of the anticipated end of the subsidies and premium inflation.

More than 24 million Americans now get their coverage through the ACA marketplace, primarily because their employers cannot offer health insurance as an employee benefit anymore. Over the past several years, a growing number of small businesses have stopped offering subsidized coverage to their workers because of the expense. Just slightly more than half of U.S. businesses are still in the game. The rest simply can’t afford the premiums. Small businesses can expect an average increase of 11% next year with some of them facing increases of 32%.

It is becoming more clear every passing year that the U.S. has one of the most insidious ways of rationing care. It is rationed based on a person’s ability to pay far more than on a person’s need for care. And among those most disadvantaged by the current system are hard-working low- and middle-income Americans with chronic conditions and those who suddenly get sick or injured.

While the Affordable Care Act prohibited insurers from charging people with pre-existing conditions more than healthier people, insurers have figured out a back door way to discriminate against them: by making them pay hundreds or thousands of dollars out of their own pockets every year – in addition to their premiums – and also by refusing to cover treatments and medications their doctors say they need.

Now you know why Big Insurance is doing so well while the rest of us are getting

Physicians for a National Health Program (PNHP) — in collaboration with Johns Hopkins University researchers — just released a report titled “No Real Choices: How Medicare Advantage Fails Seniors of Color”. It confirms that the handover of public programs like Medicare Advantage (MA) to Big Insurance doesn’t close racial, ethnic and economic health gaps — it deepens them.

PNHP’s researchers found that communities of color are being steered into MA plans not because they’re better — but because they’re cheaper upfront. This dynamic, dubbed the “Gap Trap,” means that affordability is driving people into coverage that often denies care, delays treatment and locks them into narrow networks.

“Medicare Advantage squanders billions, harms seniors and exacerbates racial inequities,” Dr. Diljeet K. Singh, gynecologic oncologist and president of Physicians for a National Health Program, said. “Americans need universal health Care which removes profit-motivated conflicts of interest, abolishes co-pays and deductibles, ends prior authorization burdens and guarantees protection from medical bankruptcy.”

HEALTH CARE un-covered is a reader-supported publication. To receive new posts and support our work, consider becoming a free or paid subscriber.

Medicare Advantage is the health care equivalent of the subprime mortgage crisis — except the fine print here is costing Americans’ lives and depleting the Medicare Trust Fund.

When Big Insurance boasts about “diverse” enrollment in MA, this report reminds us: “Diversity” is often just a buzzword used for PR reasons and has nothing to do with seniors receiving the care they deserve — especially when it is used as cover for a business model that profits from inequity.

The PNHP report finds:

As a reminder, even with the racial and ethnic issues aside, Medicare Advantage already severely restricts seniors’ access to providers, imposes unnecessary prior authorization hurdles that often result in deadly delays and denials — and cost taxpayers at least $84 billion more each year than original Medicare. Meanwhile, original, traditional Medicare does not even have networks; almost all doctors participate and few treatments are subject to prior authorization.

PNHP’s report shows that despite insurers’ endless “health equity” pledges and glossy diversity campaigns, MA remains a rigged game that leaves millions of seniors — disproportionately people of color — with worse access, inferior care and fewer real choices.

Big Insurance’s MA plans are shaped by the same market incentives that have long rewarded exclusion and sorting risk, and – if history tells us anything – sorting has always leaned on racial dimensions. As the report sums it up:

“Regardless of the reasons, any system that traps and harms people — particularly in ways that map onto centuries of racial injustice — cannot be a solution to health inequity.”

It may already be too late to implement certain changes Republicans are insisting on as a condition for renewing to Affordable Care Act subsidies, further casting doubt on any congressional deal to extend the financial aid.

Why it matters:

GOP lawmakers have made clear that they need to see changes to the enhanced ACA tax credits at the center of the government shutdown fight in order to extend them.

What we’re hearing:

Extending the credits after Nov. 1 is still possible, experts say, but gets much harder if there are significant changes, such as capping eligibility at a certain income level or requiring recipients to make a minimum premium payment.

What they’re saying:

“I have zero confidence that there’s enough operational time for systems and issuers to be able to implement changes, significant changes,” said Jeanne Lambrew, a former key health adviser in the Obama White House and later a top health official in Maine.

Between the lines:

One possible workaround would be for Congress to extend the enhanced subsidies unchanged for one year and then have GOP changes take effect in 2027. It’s not clear if that would pass muster in the House and Senate.

Devon Trolley, executive director of Pennsylvania’s ACA marketplace, said “at this point in the calendar, the lowest risk option is an extension of the same framework that the enhanced tax credits have today.”

An added complication is that there is no solution in sight for satisfying Republican demands that additional language be added preventing the subsidies from funding elective abortions.

The bottom line:

Congressional Democrats have been urging Republicans to enter negotiations, saying time is running short, while the GOP counters that Democrats need to open the government first.