Sen. Bernie Sanders (I-Vt.) is urging Senate Democrats to unite behind an expansive health care proposal in the party’s negotiations with Republicans to extend Affordable Care Act tax credits.

Why it matters:

GOP leaders have promised Democrats a vote on the expiring tax credits next month as part of their deal to end the government shutdown.

Sanders wants the Democratic proposal to extend the ACA tax credits, repeal $1 trillion in GOP health care cuts, expand Medicare and lower prescription drug prices, he said in a letter to colleagues late Monday.

Republicans, however, have signaled that any deal to extend the tax credits must be short term and require reforms.

Premiums will more than double for millions of ACA enrollees next year if Congress does not renew enhanced marketplace subsidies by year’s end, according to a new analysis.

The big picture:

Democratic leaders have argued that the government shutdown has made health care a top political issue.

Sanders, the top Democrat on the Senate Health, Education, Labor and Pensions Committee, said Democrats must make proposals that address “systemic deficiencies.”

“We should not be defending a system which is not only, by far, the most expensive in the world, but one which numerous international studies describe as one of the worst,” Sanders wrote to Democratic senators.

Sanders’ HELP committee is expected to be involved in negotiations with Republicans over a potential bipartisan deal to extend the credits next month.

A spokesperson for Senate Minority Leader Chuck Schumer (D-N.Y.) said: “The bill Democrats bring to the floor will be a caucus product.”

Between the lines:

Sanders acknowledged in his letter that his Medicare For All proposal “does not yet have majority support” in the caucus. But he said his latest proposal included “much-needed reforms.”

Sanders also encouraged Democrats to propose investments to expand primary care services, ban stock buybacks and dividends and substantially reduce CEO compensation in the health care industry.

Republicans are taking a harder line against extending enhanced Affordable Care Act subsidies — and doubling down on an alternative plan that would send the money directly to consumers.

Why it matters:

President Trump’s opposition to an extension makes it increasingly unlikely that Republicans will agree to renew the tax credits, even though it’s not clear how the GOP alternative would work or whether the party can reach a consensus.

Driving the news:

Trump wrote on Truth Social on Tuesday that the “only” plan he will support is “sending the money directly back to the people,” and that Congress should not “waste your time” on anything else, like a subsidy extension.

Trump didn’t elaborate on how his plan would work. The ACA already gives people financial help in buying insurance.

Some GOP proposals envision giving people money for a health savings account on top of existing ACA coverage, mitigating concerns about healthy people leaving the market.

Senate health committee Chair Bill Cassidy (R-La.) outlined a plan on Monday that would redirect the enhanced subsidy money to an HSA to help pay out-of-pocket costs for people who chose bronze-level ACA plans, which tend to have high deductibles.

He argued the move would direct money away from insurance companies and to consumers, and empower them to shop for health services.

Anotherpossible outcome would be allowing people to buy cheaper, skimpier coverage that doesn’t comply with the ACA’s benefit requirements. Some policy experts warn that would destabilize the ACA markets, by prompting an exodus of healthier people.

That would leave a sicker risk pool and prompt insurers to raise premiums, resulting in a “death spiral,” said Larry Levitt, executive vice president for health policy at KFF.

By contrast, “I don’t think there’s any risk of, you know, a collapse or death spiral, from what Senator Cassidy is talking about,” Levitt said, though without the enhanced subsidies there would still be “potentially millions of people who just won’t be able to afford insurance at all.”

Between the lines:

Senate Majority Leader John Thune (R-S.D.) wouldn’t rule out a bipartisan solution when asked about Trump’s comments on Tuesday, saying “we’ll see” how negotiations go and that “there’s an openness” to a deal on the GOP side.

He said the biggest obstacle, though, could be whether Democrats agree to apply the Hyde Amendment to the subsidies and add restrictions on using the funds for abortions.

The intrigue:

Cassidy is framing his plan as the most realistic option, given White House and House GOP leadership resistance to the subsidies.

“The president is not going to sign a straightforward extension of premium tax credits,” Cassidy said. “So if you actually want something which can pass and get a vote on the House floor, then what the president is proposing is actually a better way.”

Yes, but:

Democrats believe mounting public concern about rising health costs gives them the upper hand pushing for a subsidy extension.

“Sending people a few thousand dollars while doing nothing to lower health care costs is a scheme to help the ultra-wealthy at the expense of working people with cancer or pre-existing conditions,” Senate Democratic Leader Chuck Schumer said in response to Trump’s comments.

“Americans want Congress to extend the ACA tax credits to keep health insurance premiums from skyrocketing on January 1,” he added.

The big picture:

The war of words is further diminishing the chances that a group of moderates in both parties can find a bipartisan agreement to extend the subsidies with some modifications favored by Republicans, like an income cap and anti-fraud measures.

House GOP leaders have also been criticizing the subsidies. House Majority Leader Steve Scalise (R-La.) said on Fox News on Sunday that the party would be bringing forward legislation in the coming weeks on other ways to lower costs, like expanding HSAs or cracking down on pharmacy benefit managers.

The Senate Finance Committee will hold a hearing Wednesday morning on health care costs, giving senators a chance to stake out their positions further in public.

The bottom line:

It’s unlikely that Trump’s plan would gain the necessary 60 Senate votes to advance. But it could give Republican senators political cover if they oppose a subsidy extension.

Republicans could still opt to use the reconciliation process to pass a bill with a simple majority. Though the White House floated the idea on Tuesday, it’s not clear if any GOP-only plan has the votes to pass.

Layoff trends in 2025 indicate an increase in job cuts compared to 2024, with US employers announcing nearly 950,000 cuts through September, the highest number since 2020. Key drivers include cost-cutting measures, the strategic implementation of artificial intelligence (AI), and a cooling labor market.

Key Trends

Elevated Numbers: Total US job cuts through October 2025 were over one million, a 65% increase from the same period in 2024. October 2025 had the highest number of layoffs for that month in 22 years.

AI as a Primary Driver: AI adoption is a leading cause for job cuts as companies restructure for efficiency and reallocate resources. Companies like Amazon and Intel have cited AI as a reason for significant workforce reductions.

“Forever Layoffs”: A new trend involves smaller, more regular rounds of layoffs (fewer than 50 people) that create ongoing worker anxiety and impact company culture. These rolling cuts often stay out of headlines but contribute significantly to the overall job cuts.

Method of Notification: The process is becoming more impersonal, with many employees being notified of their termination via email or phone call rather than in-person meetings.

Hiring Slowdown: Alongside the layoffs, there has been a sharp drop in hiring plans, with planned hires for the year at their lowest level since 2011.

Affected Industries

While tech has been significantly impacted since late 2022, other industries are also facing substantial cuts in 2025:

Technology: Remains a leading sector for cuts as companies continue to restructure after pandemic-era overhiring and focus on AI.

Retail and Warehousing: Companies like Target and UPS are cutting thousands of jobs due to changing consumer demands, automation, and a push for efficiency.

Energy and Manufacturing: Oil giants such as Chevron and BP are making cuts as part of cost-reduction strategies and market consolidation.

Finance and Consulting: Firms like PwC and Morgan Stanley are trimming staff, citing factors like low attrition rates and the need to realign resources.

Media and Communications: Companies like CNN and the Washington Post have made cuts to pivot toward digital services and reduce costs.

Economic Context

The overall U.S. labor market remains relatively healthy despite the uptick in layoffs, though it is showing signs of cooling. The unemployment rate has inched up, and consumer sentiment has declined. The Federal Reserve is monitoring the situation and has implemented interest rate cuts to help stabilize the job market.

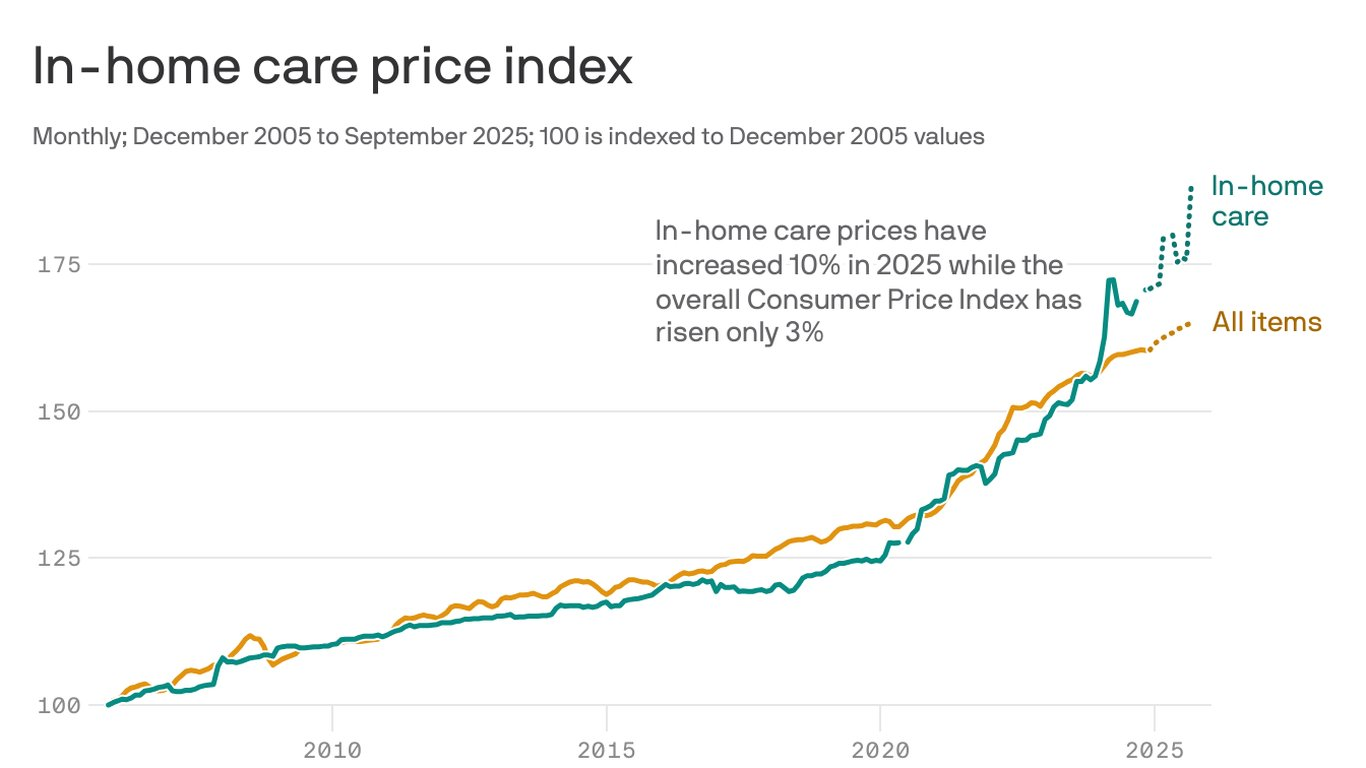

The cost of hiring help to care for an elderly or a sick person at home is skyrocketing.

Why it matters:

A labor shortage and surging demand from an aging population was already driving up prices, and nowthe White House’s crackdown on immigration and funding cuts are making things worse.

By the numbers:

So far this year, the price of in-home care for the elderly, disabled or convalescent at home is up 10%, compared with a rise of 3% for prices overall, according to government data.

From just August to September, prices for home health care spiked a staggering 7%.

Zoom in:

Rising prices and the limited availability of people who do this work are pushing families to make hard choices. Some will put relatives and loved ones into institutions, a more expensive and often less desirable option than staying at home.

Others will drop out of the workforce or cut back their hours to care for parents, relatives or partners.

The supply of workers is not keeping up with demand, Matthew Nestler, senior economist at KPMG, writes in a post. “That hurts workers and their families, employers and the overall U.S. economy.”

Friction point:

Last year, employment was surging in home health care, with an average of 13,500 jobs added each month.

But after the Trump administration immigration crackdown began in January, employment dropped off, falling into negative territory for three consecutive months in the spring, Nestler noted this summer.

This isn’t a matter of demand falling, but a cutoff in supply, he explained.

How it works:

Immigrants make up 1 in 3 workers in home care settings, per data from KFF, a health care research organization.

The severe crackdown this year on undocumented immigrants and the Trump administration’s removal of legal status from workers who are here from Venezuela and other countries are making it hard to find workers, says Mollie Gurian, vice president of policy and government affairs at LeadingAge, an aging-services nonprofit.

“The supply of workers was already so low,” she says. With fewer folks available, the companies that provide these service are raising prices to put pressure on demand. Others are raising prices in anticipation of cuts to Medicaid funding, she says.

The big picture:

At the same time that the supply of people to do this work is falling, the number of Americans who need care is rising, as a silver tsunami of baby boomers ages.

The bottom line:

We are only at the very beginning of a dramatic demographic shift, Nestler says.

Elder care is a “ticking time bomb that no one’s talking about.”

The government shutdown has left many federal workers furloughed, caused nationwide flight delays, left small businesses unable to access loans and put nonprofit services in jeopardy. It’s only expected to get worse.

As Congress remains deadlocked over passing a stopgap measure to reopen the government, thousands of Americans are at risk of losing benefits from the Supplemental Nutrition Assistance Program (SNAP); the Special Supplemental Nutrition Program for Women, Infants, and Children (WIC); and other programs at the beginning of November.

An additional burden on Americans is the start of open enrollment for the Affordable Care Act (ACA), also known as ObamaCare, on Nov. 1, where they will see more costly health insurance premium plans unless lawmakers act.

Democrats and Republicans have spent weeks pointing fingers at each other, with no deal in sight. The Senate on Tuesday failed to advance a Republican stopgap measure to end the shutdown for the 13th time, while the House was out of session and President Trump was traveling abroad.

With uncertainty around the shutdown’s timeline growing day by day, here are six ways Americans will start to feel more of the shutdown’s impact.

Federal employees

At least 670,000 federal workers have been furloughed while about 730,000 are working without pay as of Oct. 24, according to data from the Bipartisan Policy Center, a think tank based in Washington, D.C. The center estimates that if the shutdown continues through the beginning of December, federal civilian employees will miss roughly 4.5 million paychecks.

The American Federation of Government Employees (AFGE), the nation’s largest federal workers union, urged Congress to pass a “clean” funding measure known as a continuing resolution to reopen the government. AFGE President Everett Kelley said in an Oct. 27 statement, “No half measures, and no gamesmanship. Put every single federal worker back on the job with full back pay — today.”

“I get where they’re coming from. We want the shutdown to end too. But fundamentally, if Trump and Republicans continue to refuse to negotiate with us to figure out how to lower health care costs, we’re in the same place that we’ve always been,” Sen. Tina Smith (D-Minn.) told The Hill on Tuesday.

SNAP and WIC

The U.S. Department of Agriculture (USDA) said benefits won’t be issued on Nov. 1 for SNAP, a program that helps low-income families afford food. Nearly 42 million Americans rely on SNAP benefits every month, according to data from the USDA.

Though the USDA formed a plan earlier this year that said the department is obligated to use contingency funds to pay out benefits during a shutdown, it has since been deleted. The USDA wrote in a memo this month that the contingency fund is only designed for emergencies such as “natural disasters like hurricanes, tornadoes, and floods, that can come on quickly and without notice.”

Democratic officials in more than two dozen states sued the Trump administration this week, arguing the USDA is legally required to tap into those funds. But House Speaker Mike Johnson (R-La.) has claimed those funds are not “legally available.”

Families who rely on WIC, a program that provides food aid and other services to low-income pregnant and postpartum women, infants, and children younger than 5 years old, could also face trouble. The White House had provided $300 million to WIC to keep the program afloat in early October. But 44 organizations signed on to an Oct. 24 letter from the National WIC Association to the White House requesting an additional $300 million in emergency funds, warning that “numerous states are projected to exhaust their resources for WIC benefits” on Nov. 1.

Military pay

Payday is coming up at the end of this week for members of the military.

Earlier this month, Trump directed Defense Secretary Pete Hegseth to “use all available funds” to pay troops. Officials ended up reallocating $8 billion in unspent funds meant for Pentagon research and development efforts toward service members’ paychecks. The administration also received a $130 million donation from a private donor to help cover military members’ paychecks.

Vice President Vance said he believes active-duty service members will get paid this Friday. But Treasury Secretary Scott Bessent told CBS News’s Margaret Brennan on Sunday that troops could go without pay on Nov. 15 if the shutdown continues.

Senate Democrats blocked a bill sponsored by Sen. Ron Johnson (R-Wis.) earlier this month to pay active-duty members and other essential federal workers.

ACA subsidies

At the center of the shutdown fight is the ACA subsidies, which are set to expire at the end of this year. Democrats have been urging Republicans to extend the subsidies, arguing that ACA health insurance premium costs will increase if no action is taken.

Americans can choose their insurance plans for next year on the federal Affordable Care Act exchange website starting Saturday. An analysis from KFF found that without the subsidies extended, Americans will see their marketplace premium payments increase by 114 percent.

Republicans have been firm in their position of reopening the government first before discussing the ACA subsidies.

“The expiring ObamaCare subsidy at the end of the year is a serious problem. If you look at it objectively, you know that it is subsidizing bad policy. We’re throwing good money at a bad, broken system, and so it needs real reforms,” Speaker Johnson said at a Monday press conference.

Head Start

About 140 Head Start programs across 41 states and Puerto Rico serving more than 65,000 children could go dark if the shutdown goes past Nov 1., according to a joint statement from more than 100 national, state and local organizations focused on childhood education and development.

“Without funding, many of these programs will be forced to close their doors, leaving children without care, teachers without pay, and parents without the ability to work,” the statement says.

Head Start programs are designed to help low-income families and their children from birth to age 5 with a focus on health and wellness services, family well-being and engagement and early learning, according to its website.

Nonprofits

Diane Yentel, president and CEO of the National Council of Nonprofits, told The Hill in a statement that the shutdown has forced many nonprofits to halt their operations because of frozen federal reimbursements and grants.

The nonprofits include those handling wildfire recovery in Colorado, housing vulnerable youth in Utah and helping with conservation work in Montana, Yentel said. Many federal workers without pay have also turned to their local food banks, further putting a financial strain on nonprofits.

“With the November 1 cutoff of SNAP and WIC looming, the situation will get even worse. Nonprofit food banks are already facing rising grocery costs and increased demand, including from federal workers and military families,” Yentel said. “If millions of Americans suddenly lose access to these life-saving nutrition programs, local nonprofits will be overwhelmed, and far too many seniors, children, and families will go without help.”

The Trump administration has made a flurry of recent moves aimed at lowering the cost of prescription drugs, including cutting deals with some of America’s top drugmakers and launching a new website to help consumers shop for the best available prices. We recently asked 10 experts — including health economists, drug policy scholars and industry insiders — to evaluate the likely impact of those maneuvers. Their verdict: Most are unlikely to deliver substantive savings, at least based on what we know today.

So, we followed up: If those moves won’t work, what could the administration do that would make a meaningful dent in America’s drug spending?

Here are three key ideas from the experts:

1. Expand Medicare’s new power to directly negotiate prices with drugmakers.

Compared to Trump’s recent ad hoc approach to cutting confidential deals with individual drug companies, some experts say building on Medicare’s new power to negotiate could offer a more sweeping, and potentially lasting, path to savings.

For example, Trump’s team could use the price negotiations to seek steeper discounts than the Biden administration did. Federal officials could also establish a more transparent and predictable formula for future negotiations — similar to the approaches used by other nations — and publish that framework so private insurance plans could use it to drive better deals with drugmakers, too.

Finally, the White House could urge lawmakers to loosen some of the limits Democrats in Congress placed on this power when they passed the law back in 2022. Medicare can currently only negotiate the price of drugs that have been on the market for at least several years — often after the medicines have already made drug companies billions of dollars.

Ideally, said Vanderbilt professor Stacie Dusetzina, “you would negotiate a value-based price at the time a product arrives on the market” — that’s what nations like France and England do.

2. Identify and fix policies that encourage wasteful spending on medicines.

“There are policies within everything — from the tax code to Medicare and Medicaid to health insurance regulations — that are driving up drug prices in this country,” said Michael Cannon, who directs health policy studies at the Cato Institute.

One example Cannon sees as wasteful: the formula that Medicare uses to pay for drugs administered by doctors, such as chemotherapy infusions. Those doctors typically get paid 106% of the price of whichever medicine they prescribe, creating a potential incentive to choose those that are most expensive — even in cases where cheaper alternatives might be available.

And that, according to Cannon, is just the tip of the “policy failure” iceberg.

The Trump administration is taking early steps to reform at least one federal drug-pricing policy, known as 340B, which lets some hospitals and clinics purchase drugs at a discount. More than $60 billion a year now flow through this program, whose growth has exploded in recent years. But researchers, auditors and lawmakers like Republican Sen. Bill Cassidy have questioned where all of that money is going and whether it’s making medicines affordable for as many patients as it should.

3. Speed up access to cheaper generic drugs.

Generic drugs — cheaper, copycat versions of brand-name medicines — can slash costs for patients and insurers by as much as 80% once they come to market. But this price-plunging competition often takes more than a decade to arrive.

That’s, in part, because drug companies have found a host of ways to game the U.S. patent system to protect and prolong their monopolies. Law professor Rachel Sachs at Washington University in St. Louis suggested Trump not only close those loopholes, but also make its own creative use of patents.

Federal officials could, for example, invoke an obscure law known as Section 1498, she said. That provision allows the U.S. government to effectively infringe on a patent to buy or make on the cheap certain medicines that meet an extraordinary need of the country. Sachs suggested that the drug semaglutide — the active ingredient in Ozempic, Wegovy and several other weight-loss medicines — might make for an ideal target.

“The statutory authority is already there for them to do it,” Sachs said. “It’s not clear to me why they haven’t.”

Semaglutide, which earned drugmakers more than $20 billion last year alone, will otherwise remain under patent in the U.S. until early next decade.

The Trump administration issued an executive order back in April signaling at least a high level of interest in some of these ideas — and a host of others, too. On the other hand, Trump and Congressional Republicans have made moves this year that have weakened some of these potential cost-cutting tools, such as Medicare’s power to negotiate drug prices. A key provision of July’s ‘Big Beautiful Bill,’ for example, shielded more medicines from those negotiations, eroding the government’s potential savings by nearly $9 billion over the next decade.

We should all get a better read soon on just how interested this administration is in cutting prices: Federal officials are expected to announce the results of their latest round of Medicare negotiations by the end of November.

It may already be too late to implement certain changes Republicans are insisting on as a condition for renewing to Affordable Care Act subsidies, further casting doubt on any congressional deal to extend the financial aid.

Why it matters:

GOP lawmakers have made clear that they need to see changes to the enhanced ACA tax credits at the center of the government shutdown fight in order to extend them.

But insurers, states and other experts say some changes could already be impossible for next year, with ACA enrollment due to begin in less than two weeks, on Nov. 1. The subsidies are due to expire at year’s end, absent further action.

What we’re hearing:

Extending the credits after Nov. 1 is still possible, experts say, but gets much harder if there are significant changes, such as capping eligibility at a certain income level or requiring recipients to make a minimum premium payment.

What they’re saying:

“I have zero confidence that there’s enough operational time for systems and issuers to be able to implement changes, significant changes,” said Jeanne Lambrew, a former key health adviser in the Obama White House and later a top health official in Maine.

Sen. Mike Rounds (R-S.D.), one of the GOP senators more open to some form of subsidy extension, acknowledged that the implementation timeline poses a problem.

“Good question, and that’s why a lot of us started talking about it in July,” Rounds told Axios, blaming Democrats for triggering the shutdown on Oct. 1.

“When you have a shutdown that just kind of kills the discussions,” he said.

Between the lines:

One possible workaround would be for Congress to extend the enhanced subsidies unchanged for one year and then have GOP changes take effect in 2027. It’s not clear if that would pass muster in the House and Senate.

Some insurers are warning about implementation challenges in trying to make major changes for 2026.

“Our recommendation would be [a] straight extension for 2026 so that you can get the tax credits updated immediately and get people covered,” said an insurance industry source, speaking on the condition of anonymity to share private conversations. “Then, if Congress wants to make changes, those should apply in 2027 or later.”

Devon Trolley, executive director of Pennsylvania’s ACA marketplace, said “at this point in the calendar, the lowest risk option is an extension of the same framework that the enhanced tax credits have today.”

“Some changes might be not possible to implement if they structure it in a very different, very complicated way in the near term,” she said. “But other changes might be.”

An added complication is that there is no solution in sight for satisfying Republican demands that additional language be added preventing the subsidies from funding elective abortions.

The bottom line:

Congressional Democrats have been urging Republicans to enter negotiations, saying time is running short, while the GOP counters that Democrats need to open the government first.

“We can’t do any of that if we’re not negotiating,” said Sen. Chris Murphy (D-Conn.) when asked about the time frame for changes to the tax credits.

“We’ve always understood there’s going to be a negotiation, but it’s only Republicans that are boycotting those negotiations.”

In a recent blog post, Looming Government Shutdown? A Brief Overview of Expiring Federal Authorizations, the Rockefeller Institute of Government detailed the health care policies and programs requiring an extension and, in some cases, funding by Congress. For over two weeks now, failure to reach agreement on a Continuing Resolution (CR) to keep the federal government fully funded has resulted in a temporary federal shutdown.

The debate is both highly nuanced and politically charged. It involves multiple healthcare issues. The House passed a CR (sometimes also referred to as an extender) that would largely continue current funding levels through November 21, 2025, but with some new spending items, such as additional funding for congressional member security. Thus far, the Senate majority has not had the votes to pass the extender.

Under Senate rules, 60 votes are required to overcome a filibuster. This necessitates at least seven Democratic senators to vote with the Republican majority for passage. Only three Democratic senators and one Independent have voted in favor of the House-passed extender to date, and one Republican did not vote with the majority. This leaves the current vote count at 56 out of the necessary 60 votes.

The Democrats are seeking an amendment to the Republican supported CR, which would fund the government through October 31, 2025. At the core of the current dispute, the Democratic minority is seeking, among other things, in its proposed amendments: (1) restorations of the health care cuts in the recently passed HR1—also known as the One Big Beautiful Bill Act (OBBBA), and (2) permanent extension of federal funding not included in HR1 for enhanced subsidies—known as advance premium tax credits (APTC). APTCs provide additional federal funding to lower the cost of health insurance coverage purchased through the Affordable Care Act (ACA) marketplaces. These enhanced APTC subsidies were initially authorized during the COVID pandemic and are set to expire at the end of 2025, unless extended. In essence, the disagreement is over the health care cuts HR1 made, which were followed by more restrictive regulations governing the purchase of health insurance coverage, and whether Congress will continue COVID-era enhanced subsidies.

Additionally, while not included in the broader media coverage, the Rockefeller Institute has previously highlighted October 1, 2025, as the scheduled implementation date for reductions to Disproportionate Share Hospital (DSH) payments. DSH provides federal funds to hospitals that serve a high number of low-income and uninsured patients to help cover their uncompensated care costs.1 Language delaying the cuts to DSH is in both the Republicans’ CR as well as the Democrats’ proposal.

Restoration of HR1 Cuts

Prior work by the Institute, as well as other commentators, has detailed the funding cuts and other changes included in HR1 and through federal regulation, and their adverse impacts on New York’s $300 billion healthcare economy.

The Democratic minority in the Senate is seeking restorations for all of the health provisions changed in HR1. Of the Democrats’ proposed restorations, three specific areas that have been the subject of the Republican majority’s criticism include proposals relating to the financing of healthcare for certain non-citizens (both lawfully residing and illegally residing). The proposals or restorations include: (1) permitting particular lawfully residing immigrants (persons residing under color of law, or “PRUCOL”) to purchase health insurance on the official ACA marketplace, who were excluded in HR1; (2) reversing the narrowed definition of PRUCOL in HR1; and (3) restoring the federal matching share of emergency Medicaid funding which was reduced in HR1.

These issues have been subject to oversimplification in public and political discourse. Prior Rockefeller Institute of Government writings have clearly detailed these programs and who is or is not eligible. At the core of the issue, with limited exception relating to the percentage of federal funding for emergency Medicaid,2 federal funds have always been prohibited from funding coverage for those who are not lawfully residing in New York or other states. However, HR 1 also significantly reduced federal funding for both emergency care, which is provided to undocumented persons during a life-threatening emergency, and for lawfully residing residents, like refugees and asylees, that was previously authorized.3

New York estimates the changes to the definition and eligibility for the tax credits in HR1, and the enhanced subsidy expiration that was not extended in HR1, would result in a loss of over $7.5 billion in funding to New York’s healthcare economy, beginning January 1, 2026. In particular, the change in HR1 removing certain immigrants from eligibility for APTC reduces available federal funding to the State. As a result of these changes, on September 10, 2025, New York made a request to terminate the Section 1332 State Innovation Waiver and return to the Basic Health Program, risking coverage for approximately 450,000 New Yorkers with incomes between 200 and 250 percent of the poverty limit who, as a result of the loss of funding will have to purchase coverage on the exchange, obtain coverage through their employer or become uninsured. The comment period for the notice concluded on October 10, 2025, and anticipated submission to CMS was scheduled for October 15, 2025.

Some portion of the restoration of HR1 cuts that are being proposed may, however, go to undocumented immigrants with respect to emergency Medicaid funding. Medicaid pays a share of the financing of emergency Medicaid services for persons with life-threatening or organ-threatening conditions—this was the case both before and after HR1. HR1 continues to fund emergency Medicaid, but reduces the federal share from 90 percent to 50 percent for certain adults.

According to New York State Department of Health data provided to the Empire Center for Public Policy, a think tank, as of March 2024, there are 480,000 noncitizens enrolled in the emergency Medicaid program. These are largely undocumented immigrants who are otherwise not eligible for Medicaid or the Essential Plan as a qualified alien, PRUCOL, or through any other program. Absent emergency Medicaid federal funding, however, hospitals would still be required to provide care in emergent situations under the Federal Emergency Medical Treatment and Labor Act (EMTALA ) without federal money to reimburse those hospitals for that care. EMTALA was a bipartisan bill that was signed by President Regan back in 1986. Among other things, EMTALA protects everyone—primarily US citizens—who need immediate emergency care by requiring hospitals to treat patients whether they have proof of identity or insurance, or not.

The debate in Washington over restoring cuts passed in HR1 may not be resolved in a CR. Despite the potential impacts on federal funding to New York associated with the currently passed CR in the House and, therein, maintaining HR1’s changes and funding cuts, there are other important elements that, if excluded from an agreement, would add to the impact of HR1 reductions.

This post summarizes two important issues that are of significant financial impact to New York, which could be important elements of a potential bipartisan compromise solution.

In addition to restoration of the health care cuts in HR1, a second key issue in the current federal shutdown relates to programs with significant financial impact to New York that were not addressed in HR1: continued funding for Enhanced Advance Premium Tax Credits (APTC), as well as extension of the Disproportionate Share Hospital (DSH) funding at current levels. A permanent extension of the enhanced APTCs was included in the Democrat minority CR, and both parties included an extension of current DSH funding in their respective proposals.

Enhanced APTC

Enhanced APTC federal funds are used to lower health insurance premium costs for qualified health plan (QHP) coverage purchased through ACA health marketplaces. The extension of enhanced APTC, which was not addressed in HR1, relates to enhanced subsidies for purchasing qualified health plan (QHP) coverage. Existing subsidies for those not enrolled in Medicaid, Medicare, or other coverage that provide financial assistance beyond what was authorized under the Affordable Care Act (ACA) are set to expire on December 31, 2025.

The enhanced APTC subsidies were initially authorized during COVID-19 in the American Rescue Plan Act (ARPA) and extended in the Inflation Reduction Act.4 Not only were the enhanced subsidies for purchasing health insurance coverage increased (for those who were already receiving a subsidy) through advance premium tax credits, but eligibility for subsidies was expanded to include those above 400 percent of the federal poverty limit ($62,600 for an individual and $128,600 for a family of four in 2025).

The extension of the enhanced APTC was neither included in HR1, nor was it included in the Republican’s continuing resolution. As a result, it has been less widely publicized component of the current healthcare debate in Washington than the proposals to restore reductions in funding for non-citizen care, in the Democrat version of the CR.

At present, it remains unclear if the COVID-era enhanced premium tax credits will be renewed by Congress. The CR proposed by the Congressional majority only provides continued funding of existing programs through November 21st and would not solve the subsidy cliff (a sudden and steep increase in premiums for those purchasing coverage in the individual or small group market) before open enrollment begins on November 1st. Despite the fact that this issue remains open in the federal funding debate, there has been strong public support as of late for extending enhanced APTC. Of those polled by the Kaiser Family Foundation between September 23 and September 29, 2025, 78 percent of respondents indicated Congress should extend the enhanced tax credits (92 percent of Democrats, 82 percent of independents and 59 percent of Republicans).

Moreover, in mid-late September, Republican Senator Lisa Murkowski (AK), who voted against the CR, proposed a two-year extension in efforts to reach agreement on the potential shutdown, and news outlets reported5 that Republican senators were working on legislation that would extend the subsidies. At present, it appears Senator Murkowski is the only sponsor of her bill (S. 2824), which would extend the subsidies for two years. There is also currently proposed legislation, the Bipartisan Premium Tax Credit Extension Act (H.R. 5145), which would extend the enhanced subsidies for one year, through December 31, 2026. As of October 9th, 2025, there are 27 bipartisan House co-sponsors, including three members of the New York Congressional Delegation sponsoring the bill: Representatives Suozzi (D, NY-3), Lawler (R, NY-17), LaLota (R, NY-1).

Absent legislative action, it is estimated by the Kaiser Foundation that the cost to purchase health insurance in the individual market could increase by over 75 percent nationally due to the subsidy expiration.

While New York and other states would be impacted, the enhanced subsidies have the greatest direct impact in the 10 remaining non-Medicaid expansion states: Alabama, Florida, Georgia, Kansas, Mississippi, South Carolina, Tennessee, Texas, Wisconsin, and Wyoming.6 These states account for 79 house majority votes (out of 106 associated with the 10 states in total).

Moreover, there are particular and significant portions of the population within and outside of these states that would be greatly impacted. According to Kaiser, nationally, “more than a quarter of farmers, ranchers, and agricultural managers had individual market health insurance coverage (the vast majority of which is purchased with a tax credit through the ACA Marketplaces). About half (48%) of working-age adults with individual market coverage are either employed by a small business with fewer than 25 workers, self-employed entrepreneurs, or small business owners. Middle-income people who would lose tax credits altogether are disproportionately early and pre-retirees, small business owners, and rural residents.

And while the ACA Marketplaces have doubled in size nationally since these enhanced tax credits became available, more than half of that growth is concentrated in Texas, Florida, Georgia, and North Carolina.”7

DSH Funding

Medicaid Disproportionate Share Hospital (DSH) payments are federal payments to hospitals that serve a high number of low-income and uninsured patients to help cover their uncompensated care costs. These payments are a critical form of financial assistance for “safety-net” hospitals, helping them remain financially stable and continue providing essential services to vulnerable populations. Federal law requires states to make these payments to qualifying hospitals, but there are overall and state-specific limits on the total amount of funding available.

Funding for the DSH program was set to expire on or about October 1, 2025. Extension of the DSH program was not included in HR1. As discussed below, the impact on “safety-net” hospitals in New York is significant.

Impact on New York

Expiration of Enhanced APTC

In 2022, the last time the Enhanced APTC subsidies were set to expire, New York State estimated that their expiration would increase premium costs for qualified health plan (QHP) enrollees by 58 percent and reduce funding to the Essential Plan by $600–$700 million.8 New York recently estimated the impact at 38 percent following passage of the House bill, which did not include the extension. According to NYSOH, the subsidy benefits nearly 140,000 New Yorkers and reduces coverage costs by $1,368 per person annually (previously $1,453 in 2022), which equates to over $200 million in federal funding that would be diverted from New Yorkers currently purchasing coverage on the exchange.

Additionally, New York has experienced higher-than-average premium increases in recent years, so when combined with reductions to subsidies, this may make it more difficult for people to afford to buy coverage and could further exacerbate the shrinking New York individual and small group health insurance markets. Premium increases in New York exceed national trends.9 Part of this in New York (as opposed to other states) is due to the use of various health-related taxes, which were detailed in How Health Care Policy in Washington Could Affect New York.

Rate increases for individual, small group, and large group health insurance for the 2026 plan year were reviewed and approved, with changes, by the Department of Financial Services (DFS) in August 2025. According to DFS, individual plans will increase by an average of 7.1 percent, while small group plans will increase by an average of 13 percent, both of which are significantly less than was requested by the insurers.

New York operates a Basic Health Program (BHP) option in the ACA, known as the Essential Plan (EP). The EP is a public health insurance program for New Yorkers with incomes above the maximum Medicaid eligibility (138 percent of the federal poverty limit) and below 200 percent of the poverty limit, or with the 1332 Waiver below 250 percent of the poverty limit (FPL). The BHP provision in the ACA only allows eligibility up to 200 percent FPL. Using a provision in section 1332 of the ACA that allows for federal regulators to make certain adjustments (or waivers), New York increased EP eligibility to 250 percent FPL. However, as a result of funding reductions enacted in the HR1, New York is currently seeking to reverse its waiver expansion, bringing the future maximum eligibility to 200 percent of the FPL.

Using January 2025 enrollment data, absent other changes, the estimated lost funding to the Essential Plan would jump from $1 billion to $1.2 billion. Changes enacted in HR1 (which the Democrats are currently seeking to reverse) reduce the value of the enhanced subsidies to New York by approximately one-third, as certain legally residing non-citizens are no longer eligible for any subsidies pursuant to the federal changes.10

Enhanced Premium Tax Credit—Impact of Expiration in New York 11

An extension or lack thereof of the subsidy has important implications for healthcare financing and access to coverage in the State of New York. At present, New York stands to lose $1.2 billion to $1.4 billion associated with the loss of the enhanced subsidies, including $1.0 billion to $1.2 billion currently used to provide low-cost coverage to 1.6 million persons with incomes between 138 and 250 percent of the poverty limit and nearly $200 million for 140,000 individuals purchasing coverage on New York State of Health (NYSOH).

Timing for Consumers

November 1, 2025, marks the beginning of the open enrollment period for purchasing coverage on a state or federally operated exchange for the 2026 plan year. Consumers can begin renewing plans beginning November 16, 2025, for those purchasing a qualified health plan on New York State of Health (NYSOH), with a December 15, 2025, deadline to enroll in coverage that begins on January 1, 2026.

In addition to NYSOH’s website and app, New York health insurance notices for the 2026 plan year are to be sent out by November 1, 2025, detailing premium information, including any applicable APTC. The notices will also list the income used for the automatic renewal determination in a section titled “How We Made Our Decision.” For enrollees who do not agree with the renewal determination, they can update their application on NYSOH between November 16, 2025, and December 15, 2025, to avoid a gap in coverage starting January 1, 2026.

Those rate notices are already being loaded into the plan systems and NYSOH online, as it takes some weeks to get the rate notices set and out to enrollees. If Congress does not act imminently to reauthorize the expanded APTC, consumers will receive notices that reflect 2026 premiums without the expanded APTC.

Indeed, NYSOH has already put online, as of October 1, 2025, the ‘Compare Plans’ and ‘Estimate Costs’ tool on the website, which allows consumers to look at plan options and evaluate costs. And, for consumers using the tool now, it already reflects that the Expanded APTCs will not be available for 2026.

Potential Enhanced APTC Compromise

There are three basic options available to Congress with some variation on duration with regard to the enhanced APTCs. Congress could:

Allow the enhanced APTCs to expire. If no compromise is reached, Congress could simply do nothing and funding for the Enhanced APTCs will stop at the end of 2025.

Extend the existing enhanced APTCs. The parties could compromise and extend the enhanced APTCs either permanently or temporarily to some date certain. As noted above, a bipartisan bill (H.R. 4541) would extend the enhanced APTCs for one year, and Senator Murkowski carries a bill in the Senate (S. 2824) that would extend the subsidies for two years. The Senate Democratic minority CR would extend the existing subsidies permanently.

Modify the eligibility criteria for enhanced APTCs. Currently, eligibility has no income limit as such, but the enhanced APTC subsidies ensure that no one spends more than 8.5 percent of income for the benchmark silver plan. Congress could make changes that include: (1) modifying the eligibility criteria to the level under the ACA to 400% of the federal poverty level (FPL); (2) adjusting the limit of the percent of income for the benchmark silver plan above (or below) 8.5 percent; or (3) some other rules that limit or expand income eligibility.

Congress could also explore options that modify the maximum amount a household would be required to contribute towards the cost of coverage (currently 8.5% for households above 400 percent of FPL) or limit the application of the marketplace coverage rule, which was detailed in a prior Rockefeller Institute of Government report.

Expiration of Disproportionate Share Hospital (DSH) Funding

Additionally, scheduled reductions to DSH funding, that absent a change to New York State law, would primarily affect the availability of DSH funding for New York City, which were delayed from starting in October 2025 to October 2026 through 2028 in the initial House Reconciliation bill, but not included in HR1, are effective October 1, 2025, absent a federal extension. The DSH reduction has been delayed by Congress more than a dozen times since enactment through the ACA.12

Under current law, the availability of $2.4 billion federal DSH funding to New York, or 15 percent of federal funding for DSH ($16 billion), would be reduced. DSH funding is matched by the state or locality (through an intergovernmental transfer), making New York’s total DSH program over $4.7 billion as of federal fiscal year 2025. The Medicaid and CHIP Payment and Access Commission (MACPAC) estimates New York State’s total DSH program, including federal and non-federal shares, would be reduced by $2.8 billion, which translates to a loss of $1.4 billion in federal DSH funding (or a nearly 59 percent reduction).

On September 23, 2019, immediately preceding the last government shutdown, CMS issued a final rule, finalizing the methodology to calculate the scheduled reductions to DHS funding, as initially enacted in the ACA, during the 2020 to 2025 period. It does not appear that the Trump administration has issued guidance related to implementation in 2025; however, the regulations track with the statute, meaning the Trump administration could implement the DSH reductions required under the ACA, absent agreement on a delay.

Like an extension of the enhanced subsidies for the APTCs, an extension (meaning a delay) of the DSH cuts is an important element for New York to avoid further significant loss of federal funding (in addition to the loss of funding as a result of HR1 and the potential expiration of the enhanced subsidies).

CONCLUSION

Multiple healthcare issues are at play in the Federal government shutdown.Democrats want to restore cuts and other actions made in HR1 in an effort to mitigate the impact on residents and the healthcare delivery system, including the State’s financial plan, while Republicans are not revisiting actions taken in HR1. Among others, requested cuts to be restored in HR1 include making certain legally residing non-citizens ineligible for federal funding to purchase comprehensive coverage on health insurance marketplaces, narrowing the definition of legally residing non-citizen for purposes of public program eligibility, and reducing the match rate for emergency Medicaid.

Two additional important issues are the impending expiration of enhanced subsidies for purchasing coverage on an official ACA marketplace and the impending implementation date for previously scheduled disproportionate share hospital (DSH) reductions. As referenced above, polling suggests that the extension of the subsidy has broad public support, and there is a bipartisan bill in Congress providing an extension. In the immediate days following the shutdown, positive polling around extending the enhanced APTC suggested there was a possibility of ending the shutdown with bipartisan support. While many states benefit from these subsidies, New Yorkers, more specifically, benefit from these subsidies on the exchange and in the Essential Plan, due to the State’s adoption of the Basic Health Program option for those with income slightly above Medicaid levels. While there is some coverage and indications of support regarding the enhanced APTC subsidies, the potential for the DSH cuts to be implemented is not in the mainstream media coverage.

Moreover, with regard to the enhanced APTC subsidies, we now see that the narrative from the Republican congressional majority is shifting,13 suggesting that the enhanced subsidies might not be part of resolving the current debate playing out in Washington.

Nevertheless, compromise is still possible, particularly in light of the disproportionate impact the expiration of the enhanced APTC will have on Republican-led states and the broad impact of the scheduled DSH reductions. One potential path to ending the shutdown where both sides could arguably claim victory would be to drop the demand for restoration of the health care cuts in HR1 in exchange for extending the enhanced APTC and again delaying the DSH cuts. While this potential “victory” would be a benefit to New York and reopen the federal government, that does not mean that the restoration of cuts enacted in HR1 would not also be important to New York in future negotiations.

It’s impossible to predict exactly where things are headed right now, but the Rockefeller Institute of Government continues to monitor developments in Washington, continuing past efforts to detail who and what is at stake in the current debates. This post is preceded by a series of healthcare reports, blogs, and podcasts by our health team, which include more information on the programs discussed in this post and related topics. More information can be found in these past works in the health series, which is available here.

The U.S. health industry revolves around a flawed presumption: individuals and families are dependent on the health system to make health decisions on their behalf. It’s as basic as baseball and apple pie in our collective world view.

It’s understandable. Consumers think the system is complex. They believe the science on which diagnostics and therapeutics are based requires specialized training to grasp. They think health insurance is a hedge against unforeseen bills that can wipe them out. And they think everything in healthcare is inexplicably expensive.

This view justifies the majority of capital investments, policy changes and competitive strategies by organizations geared to protecting traditional roles and profits. It justifies guardianship of scope of practice limits controlled by medical societies because patients trust doctors more than others. It justifies pushback by hospitals, insurers and drug companies against pro-price transparency regulations arguing out-of-pocket costs matter more. It justifies mainstream media inattention to the how the health system operates preferring sensationalism (medical errors, price sticker shock, fraud) over more complicated issues. And it justifies large and growing disparities in healthcare workforce compensation ranging from hourly workers who can’t afford their own healthcare to clinicians and executives who enjoy high six figure base compensation and rich benefits awarded by board compensation committees.

It’s a flawed presumption. It’s the unintended consequence of a system designed around sick care for the elderly that working age populations are obliged to fund. Healthcare organizations should pivot because this view is a relic of healthcare’s past. Consider:

Most consumers think the health system is fundamentally flawed because it prioritizes its business interests above their concerns and problems.

Most think technologies—monitoring devices, AI, et al– will enable them to own their medical records, self-diagnose and monitor their health independently.

And most –especially young and middle age consumers—think their healthcare spending should be predictable and prices transparent.

In response, most organizations in healthcare take cautious approaches i.e. “affordability” is opined as a concern but defined explicitly by few if any. “Value” is promised but left to vague, self-serving context and conditions. “Quality” is about affiliations, capabilities and processes for which compliance can be measured but results (outcomes, diagnostic accuracy, efficacy, savings, coverage adequacy, et al) — hardly accessible. And so on.

For starters, the industry must address its prices, costs and affordability in the broader context of household discretionary spending. Healthcare’s insiders are prone to mistaken notions that the household healthcare spend is somehow insulated from outside forces: that’s wrong. Household healthcare expenditures constitute 8.3% of the monthly consumer price index (CPI); housing is 35.4%, food is 13.6% and energy is 6.4%. In the last 12 months, the overall CPI increased 2.9%, healthcare services increased 4.2%, housing increased 3.6%, food increased 3.2% and energy costs increased only 0.2%. In that same period, private industry wages increased 1.0% and government wages increased 1.2%. Household financial pressures are real and pervasive. Thus, healthcare services costs are complicit in mounting household financial anxiety.

The pending loss of marketplace subsidies and escalating insurance premiums means households will be expected to spend more for healthcare. Housing market instability that hits younger and lower-middle income households hardest poses an even larger threat to household financial security and looms large in coming months. Utilization of healthcare products and services in households during economic downturns shrinks some, but discretionary spending for health services—visits, procedures, tests, premiums, OTC et al—shrinks substantially as those bills take a back seat to groceries, fuel, car payments, student loan debt, rent/mortgage payments and utilities in most households.

Healthcare organizations must rethink their orientations to patients, enrollees and users. All must embrace consumer-facing technologies that empower individuals and households to shop for healthcare products and services deliberately. In this regard, some insurers and employers seem more inclined than providers and suppliers, but solutions are not widely available. And incentives to stimulate households to choose “high value” options are illusory. Data show carrots to make prudent choices work some, but sticks seem to stimulate shopping for most preference-sensitive products and services.

The point is this: the U.S. economy is slowing. Inflation is a concern and prices for household goods and necessary services are going up. The U.S. health industry can ill-afford to take a business-as-usual approach to how our prices are set and communicated, consumer debt collection (aka “rev cycle”) is managed and how capital and programmatic priorities are evaluated.

Net Promoter Scores, Top 100 Recognition and Star Ratings matter: how organizations address household financial pressures impacts these directly and quickly. And, as never before, consumer sentiment toward healthcare’s responsiveness to their financial pressures is at an all-time low. It’s the imperative that can’t be neglected.

September 2025 marks a significant shift in U.S. health policy, especially its approach to the public’s health.

On September 9, the Make America Healthy Again (MAHA) Commission issued its first report pursuant to Executive Order 1421 which included 128 recommendations focused on reducing childhood chronic disease prevalence involving nutrition, chemical exposure, “over-medicalization” in pediatric care and more.

On September 19, the newly-appointed CDC Advisory Committee on Immunization Practices (ACIP) issued new guidance on MMRV, Hep B and Covid vaccines for the coming season.

On September 22, the FDA announced label updates for acetaminophen (Tylenol) during pregnancy urging caution. In response, the Blue Cross Blue Shield Association (BCBSA) and America’s Health Insurance Plans (AHIP) said they would not modify their coverage from prior guidance.

On September 26, HHS and the Food and Drug Administration (FDA) announced enforcement actions against misleading DTC prescription drug advertisements aimed at protecting consumers by increasing transparency and accuracy in drug marketing.

All these as Congress faces a federal government shutdown Tuesday where debate centers on the President’s proposed FY2026 budget that cuts CDC funding by 53% compared to FY2024, eliminates over 100 public health programs and elevates readiness risks for outbreaks (e.g., measles) and more. Neither side wants a shutdown. Both see political advantage in staying their courses:

Republicans enjoy strong MAGA support for federal spending cuts.

Democrats enjoy voter majority support for extending ACA subsidies and maintaining health programs like SNAP with eligibility/program improvements.

But neither party is trusted by the majority of voters. The public’s distaste for the political system is palpable. Confidence in Congress is at an all-time low (Gallup), and trust in the Centers for Disease Control has plummeted:

“KFF polls have shown a steady decline in the share of the public saying they trust the CDC to provide reliable information about vaccines and other topics, from a high of 85% at the onset of the COVID-19 pandemic to 57% in our latest poll in July. This drop was largely driven by Republicans, among whom the share trusting the CDC dropped from 90% in March 2020 to 40% in September 2023 before rebounding somewhat following President Trump’s 2024 election victory and Kennedy’s appointment as HHS Secretary. While trust among Democrats remained high throughout Joe Biden’s presidency, it began to decline in President Trump’s second term just as Republicans showed signs of increasing trust. As of July, Democrats remained more trusting of the CDC than Republicans, but it’s unclear how recent events might affect trust among partisans going forward.”

In June 2024, Jonathan Samet, Colorado School of Public Health) and Ross C. Brownson (Washington University) offered this view:

“Public health system” is an optimistic misnomer in the United States, as it is used in reference to a fragmented and loosely connected set of entities. Moreover, the public health system, which is itself not readily delimited, is part of a system of systems that encompasses at least governmental public health; community-based organizations; the health care sector; and the education, training, and research of the academic public health and medical enterprises. The organization, policies, and politics of public health in the United States present opportunities and challenges. In the current decentralized model of public health, governance and are distributed across more than3,300 state and local health departments. “

My take:

Public health is a vital part of the U.S. health system but a stepchild to its major players. In reality, the U.S. operates a dual system: one that serves those with insurance (public and private) and another for those without. Public health programs like SNAP, HeadStart, Federally Qualified Health Centers et. al., serve lower income and under-insured populations and integrate with local delivery systems emergency services and during mass-events like pandemics, mass-casualties and disease outbreaks. Funding for public health programs is 2-5% of total health spending shared between local, state and federal governments.

Studies show food, housing and income insecurity—areas targeted by public health– correlate to chronic disease prevalence and health costs. Unlike most developed systems of the world which operate at a lower cost and produce better population-health outcomes, our system perpetuates a structural divide between healthcare and public health. Integrating the two is a necessary strategy for system transformation, but a difficult task given entrenched animosity toward “the system” held by public health leaders and funding pressures. The bridge between public health and the healthcare delivery systems is a two-lane road with lots of potholes at the federal level, and sometimes better in local communities. But funding seems to be an afterthought unless local communities deem it vital.

Public health is an opportunity for industry leaders to demonstrate pursuit of the greater good. Most public health programs are under-funded and dependent on a patchwork of local, state and federal appropriations (sometimes augmented by philanthropy) to keep their doors open. A particular opportunity exists for not-for-profit hospitals and health systems who enjoy tax exemptions to pursue integration as the core community benefits strategy, offering community leaders a sensible basis for eliminating duplicative services, expanding preventive health services and reducing demand for unnecessary hospitalizations resulted from uncoordinated care.

As the federal shutdown is addressed this week in DC, public health officials will be watching closely. As noted on the American’s Public Health Association website (www.apha.org) “The health care industry treats people who are sick, while public health aims to prevent people from getting sick or injured in the first place. Public health also focuses on entire populations, while health care focuses on individual patients.” Both are necessary but responsibility and funding for the public’s health seems in limbo.