It may already be too late to implement certain changes Republicans are insisting on as a condition for renewing to Affordable Care Act subsidies, further casting doubt on any congressional deal to extend the financial aid.

Why it matters:

GOP lawmakers have made clear that they need to see changes to the enhanced ACA tax credits at the center of the government shutdown fight in order to extend them.

But insurers, states and other experts say some changes could already be impossible for next year, with ACA enrollment due to begin in less than two weeks, on Nov. 1. The subsidies are due to expire at year’s end, absent further action.

What we’re hearing:

Extending the credits after Nov. 1 is still possible, experts say, but gets much harder if there are significant changes, such as capping eligibility at a certain income level or requiring recipients to make a minimum premium payment.

What they’re saying:

“I have zero confidence that there’s enough operational time for systems and issuers to be able to implement changes, significant changes,” said Jeanne Lambrew, a former key health adviser in the Obama White House and later a top health official in Maine.

Sen. Mike Rounds (R-S.D.), one of the GOP senators more open to some form of subsidy extension, acknowledged that the implementation timeline poses a problem.

“Good question, and that’s why a lot of us started talking about it in July,” Rounds told Axios, blaming Democrats for triggering the shutdown on Oct. 1.

“When you have a shutdown that just kind of kills the discussions,” he said.

Between the lines:

One possible workaround would be for Congress to extend the enhanced subsidies unchanged for one year and then have GOP changes take effect in 2027. It’s not clear if that would pass muster in the House and Senate.

Some insurers are warning about implementation challenges in trying to make major changes for 2026.

“Our recommendation would be [a] straight extension for 2026 so that you can get the tax credits updated immediately and get people covered,” said an insurance industry source, speaking on the condition of anonymity to share private conversations. “Then, if Congress wants to make changes, those should apply in 2027 or later.”

Devon Trolley, executive director of Pennsylvania’s ACA marketplace, said “at this point in the calendar, the lowest risk option is an extension of the same framework that the enhanced tax credits have today.”

“Some changes might be not possible to implement if they structure it in a very different, very complicated way in the near term,” she said. “But other changes might be.”

An added complication is that there is no solution in sight for satisfying Republican demands that additional language be added preventing the subsidies from funding elective abortions.

The bottom line:

Congressional Democrats have been urging Republicans to enter negotiations, saying time is running short, while the GOP counters that Democrats need to open the government first.

“We can’t do any of that if we’re not negotiating,” said Sen. Chris Murphy (D-Conn.) when asked about the time frame for changes to the tax credits.

“We’ve always understood there’s going to be a negotiation, but it’s only Republicans that are boycotting those negotiations.”

In a recent blog post, Looming Government Shutdown? A Brief Overview of Expiring Federal Authorizations, the Rockefeller Institute of Government detailed the health care policies and programs requiring an extension and, in some cases, funding by Congress. For over two weeks now, failure to reach agreement on a Continuing Resolution (CR) to keep the federal government fully funded has resulted in a temporary federal shutdown.

The debate is both highly nuanced and politically charged. It involves multiple healthcare issues. The House passed a CR (sometimes also referred to as an extender) that would largely continue current funding levels through November 21, 2025, but with some new spending items, such as additional funding for congressional member security. Thus far, the Senate majority has not had the votes to pass the extender.

Under Senate rules, 60 votes are required to overcome a filibuster. This necessitates at least seven Democratic senators to vote with the Republican majority for passage. Only three Democratic senators and one Independent have voted in favor of the House-passed extender to date, and one Republican did not vote with the majority. This leaves the current vote count at 56 out of the necessary 60 votes.

The Democrats are seeking an amendment to the Republican supported CR, which would fund the government through October 31, 2025. At the core of the current dispute, the Democratic minority is seeking, among other things, in its proposed amendments: (1) restorations of the health care cuts in the recently passed HR1—also known as the One Big Beautiful Bill Act (OBBBA), and (2) permanent extension of federal funding not included in HR1 for enhanced subsidies—known as advance premium tax credits (APTC). APTCs provide additional federal funding to lower the cost of health insurance coverage purchased through the Affordable Care Act (ACA) marketplaces. These enhanced APTC subsidies were initially authorized during the COVID pandemic and are set to expire at the end of 2025, unless extended. In essence, the disagreement is over the health care cuts HR1 made, which were followed by more restrictive regulations governing the purchase of health insurance coverage, and whether Congress will continue COVID-era enhanced subsidies.

Additionally, while not included in the broader media coverage, the Rockefeller Institute has previously highlighted October 1, 2025, as the scheduled implementation date for reductions to Disproportionate Share Hospital (DSH) payments. DSH provides federal funds to hospitals that serve a high number of low-income and uninsured patients to help cover their uncompensated care costs.1 Language delaying the cuts to DSH is in both the Republicans’ CR as well as the Democrats’ proposal.

Restoration of HR1 Cuts

Prior work by the Institute, as well as other commentators, has detailed the funding cuts and other changes included in HR1 and through federal regulation, and their adverse impacts on New York’s $300 billion healthcare economy.

The Democratic minority in the Senate is seeking restorations for all of the health provisions changed in HR1. Of the Democrats’ proposed restorations, three specific areas that have been the subject of the Republican majority’s criticism include proposals relating to the financing of healthcare for certain non-citizens (both lawfully residing and illegally residing). The proposals or restorations include: (1) permitting particular lawfully residing immigrants (persons residing under color of law, or “PRUCOL”) to purchase health insurance on the official ACA marketplace, who were excluded in HR1; (2) reversing the narrowed definition of PRUCOL in HR1; and (3) restoring the federal matching share of emergency Medicaid funding which was reduced in HR1.

These issues have been subject to oversimplification in public and political discourse. Prior Rockefeller Institute of Government writings have clearly detailed these programs and who is or is not eligible. At the core of the issue, with limited exception relating to the percentage of federal funding for emergency Medicaid,2 federal funds have always been prohibited from funding coverage for those who are not lawfully residing in New York or other states. However, HR 1 also significantly reduced federal funding for both emergency care, which is provided to undocumented persons during a life-threatening emergency, and for lawfully residing residents, like refugees and asylees, that was previously authorized.3

New York estimates the changes to the definition and eligibility for the tax credits in HR1, and the enhanced subsidy expiration that was not extended in HR1, would result in a loss of over $7.5 billion in funding to New York’s healthcare economy, beginning January 1, 2026. In particular, the change in HR1 removing certain immigrants from eligibility for APTC reduces available federal funding to the State. As a result of these changes, on September 10, 2025, New York made a request to terminate the Section 1332 State Innovation Waiver and return to the Basic Health Program, risking coverage for approximately 450,000 New Yorkers with incomes between 200 and 250 percent of the poverty limit who, as a result of the loss of funding will have to purchase coverage on the exchange, obtain coverage through their employer or become uninsured. The comment period for the notice concluded on October 10, 2025, and anticipated submission to CMS was scheduled for October 15, 2025.

Some portion of the restoration of HR1 cuts that are being proposed may, however, go to undocumented immigrants with respect to emergency Medicaid funding. Medicaid pays a share of the financing of emergency Medicaid services for persons with life-threatening or organ-threatening conditions—this was the case both before and after HR1. HR1 continues to fund emergency Medicaid, but reduces the federal share from 90 percent to 50 percent for certain adults.

According to New York State Department of Health data provided to the Empire Center for Public Policy, a think tank, as of March 2024, there are 480,000 noncitizens enrolled in the emergency Medicaid program. These are largely undocumented immigrants who are otherwise not eligible for Medicaid or the Essential Plan as a qualified alien, PRUCOL, or through any other program. Absent emergency Medicaid federal funding, however, hospitals would still be required to provide care in emergent situations under the Federal Emergency Medical Treatment and Labor Act (EMTALA ) without federal money to reimburse those hospitals for that care. EMTALA was a bipartisan bill that was signed by President Regan back in 1986. Among other things, EMTALA protects everyone—primarily US citizens—who need immediate emergency care by requiring hospitals to treat patients whether they have proof of identity or insurance, or not.

The debate in Washington over restoring cuts passed in HR1 may not be resolved in a CR. Despite the potential impacts on federal funding to New York associated with the currently passed CR in the House and, therein, maintaining HR1’s changes and funding cuts, there are other important elements that, if excluded from an agreement, would add to the impact of HR1 reductions.

This post summarizes two important issues that are of significant financial impact to New York, which could be important elements of a potential bipartisan compromise solution.

In addition to restoration of the health care cuts in HR1, a second key issue in the current federal shutdown relates to programs with significant financial impact to New York that were not addressed in HR1: continued funding for Enhanced Advance Premium Tax Credits (APTC), as well as extension of the Disproportionate Share Hospital (DSH) funding at current levels. A permanent extension of the enhanced APTCs was included in the Democrat minority CR, and both parties included an extension of current DSH funding in their respective proposals.

Enhanced APTC

Enhanced APTC federal funds are used to lower health insurance premium costs for qualified health plan (QHP) coverage purchased through ACA health marketplaces. The extension of enhanced APTC, which was not addressed in HR1, relates to enhanced subsidies for purchasing qualified health plan (QHP) coverage. Existing subsidies for those not enrolled in Medicaid, Medicare, or other coverage that provide financial assistance beyond what was authorized under the Affordable Care Act (ACA) are set to expire on December 31, 2025.

The enhanced APTC subsidies were initially authorized during COVID-19 in the American Rescue Plan Act (ARPA) and extended in the Inflation Reduction Act.4 Not only were the enhanced subsidies for purchasing health insurance coverage increased (for those who were already receiving a subsidy) through advance premium tax credits, but eligibility for subsidies was expanded to include those above 400 percent of the federal poverty limit ($62,600 for an individual and $128,600 for a family of four in 2025).

The extension of the enhanced APTC was neither included in HR1, nor was it included in the Republican’s continuing resolution. As a result, it has been less widely publicized component of the current healthcare debate in Washington than the proposals to restore reductions in funding for non-citizen care, in the Democrat version of the CR.

At present, it remains unclear if the COVID-era enhanced premium tax credits will be renewed by Congress. The CR proposed by the Congressional majority only provides continued funding of existing programs through November 21st and would not solve the subsidy cliff (a sudden and steep increase in premiums for those purchasing coverage in the individual or small group market) before open enrollment begins on November 1st. Despite the fact that this issue remains open in the federal funding debate, there has been strong public support as of late for extending enhanced APTC. Of those polled by the Kaiser Family Foundation between September 23 and September 29, 2025, 78 percent of respondents indicated Congress should extend the enhanced tax credits (92 percent of Democrats, 82 percent of independents and 59 percent of Republicans).

Moreover, in mid-late September, Republican Senator Lisa Murkowski (AK), who voted against the CR, proposed a two-year extension in efforts to reach agreement on the potential shutdown, and news outlets reported5 that Republican senators were working on legislation that would extend the subsidies. At present, it appears Senator Murkowski is the only sponsor of her bill (S. 2824), which would extend the subsidies for two years. There is also currently proposed legislation, the Bipartisan Premium Tax Credit Extension Act (H.R. 5145), which would extend the enhanced subsidies for one year, through December 31, 2026. As of October 9th, 2025, there are 27 bipartisan House co-sponsors, including three members of the New York Congressional Delegation sponsoring the bill: Representatives Suozzi (D, NY-3), Lawler (R, NY-17), LaLota (R, NY-1).

Absent legislative action, it is estimated by the Kaiser Foundation that the cost to purchase health insurance in the individual market could increase by over 75 percent nationally due to the subsidy expiration.

While New York and other states would be impacted, the enhanced subsidies have the greatest direct impact in the 10 remaining non-Medicaid expansion states: Alabama, Florida, Georgia, Kansas, Mississippi, South Carolina, Tennessee, Texas, Wisconsin, and Wyoming.6 These states account for 79 house majority votes (out of 106 associated with the 10 states in total).

Moreover, there are particular and significant portions of the population within and outside of these states that would be greatly impacted. According to Kaiser, nationally, “more than a quarter of farmers, ranchers, and agricultural managers had individual market health insurance coverage (the vast majority of which is purchased with a tax credit through the ACA Marketplaces). About half (48%) of working-age adults with individual market coverage are either employed by a small business with fewer than 25 workers, self-employed entrepreneurs, or small business owners. Middle-income people who would lose tax credits altogether are disproportionately early and pre-retirees, small business owners, and rural residents.

And while the ACA Marketplaces have doubled in size nationally since these enhanced tax credits became available, more than half of that growth is concentrated in Texas, Florida, Georgia, and North Carolina.”7

DSH Funding

Medicaid Disproportionate Share Hospital (DSH) payments are federal payments to hospitals that serve a high number of low-income and uninsured patients to help cover their uncompensated care costs. These payments are a critical form of financial assistance for “safety-net” hospitals, helping them remain financially stable and continue providing essential services to vulnerable populations. Federal law requires states to make these payments to qualifying hospitals, but there are overall and state-specific limits on the total amount of funding available.

Funding for the DSH program was set to expire on or about October 1, 2025. Extension of the DSH program was not included in HR1. As discussed below, the impact on “safety-net” hospitals in New York is significant.

Impact on New York

Expiration of Enhanced APTC

In 2022, the last time the Enhanced APTC subsidies were set to expire, New York State estimated that their expiration would increase premium costs for qualified health plan (QHP) enrollees by 58 percent and reduce funding to the Essential Plan by $600–$700 million.8 New York recently estimated the impact at 38 percent following passage of the House bill, which did not include the extension. According to NYSOH, the subsidy benefits nearly 140,000 New Yorkers and reduces coverage costs by $1,368 per person annually (previously $1,453 in 2022), which equates to over $200 million in federal funding that would be diverted from New Yorkers currently purchasing coverage on the exchange.

Additionally, New York has experienced higher-than-average premium increases in recent years, so when combined with reductions to subsidies, this may make it more difficult for people to afford to buy coverage and could further exacerbate the shrinking New York individual and small group health insurance markets. Premium increases in New York exceed national trends.9 Part of this in New York (as opposed to other states) is due to the use of various health-related taxes, which were detailed in How Health Care Policy in Washington Could Affect New York.

Rate increases for individual, small group, and large group health insurance for the 2026 plan year were reviewed and approved, with changes, by the Department of Financial Services (DFS) in August 2025. According to DFS, individual plans will increase by an average of 7.1 percent, while small group plans will increase by an average of 13 percent, both of which are significantly less than was requested by the insurers.

New York operates a Basic Health Program (BHP) option in the ACA, known as the Essential Plan (EP). The EP is a public health insurance program for New Yorkers with incomes above the maximum Medicaid eligibility (138 percent of the federal poverty limit) and below 200 percent of the poverty limit, or with the 1332 Waiver below 250 percent of the poverty limit (FPL). The BHP provision in the ACA only allows eligibility up to 200 percent FPL. Using a provision in section 1332 of the ACA that allows for federal regulators to make certain adjustments (or waivers), New York increased EP eligibility to 250 percent FPL. However, as a result of funding reductions enacted in the HR1, New York is currently seeking to reverse its waiver expansion, bringing the future maximum eligibility to 200 percent of the FPL.

Using January 2025 enrollment data, absent other changes, the estimated lost funding to the Essential Plan would jump from $1 billion to $1.2 billion. Changes enacted in HR1 (which the Democrats are currently seeking to reverse) reduce the value of the enhanced subsidies to New York by approximately one-third, as certain legally residing non-citizens are no longer eligible for any subsidies pursuant to the federal changes.10

Enhanced Premium Tax Credit—Impact of Expiration in New York 11

An extension or lack thereof of the subsidy has important implications for healthcare financing and access to coverage in the State of New York. At present, New York stands to lose $1.2 billion to $1.4 billion associated with the loss of the enhanced subsidies, including $1.0 billion to $1.2 billion currently used to provide low-cost coverage to 1.6 million persons with incomes between 138 and 250 percent of the poverty limit and nearly $200 million for 140,000 individuals purchasing coverage on New York State of Health (NYSOH).

Timing for Consumers

November 1, 2025, marks the beginning of the open enrollment period for purchasing coverage on a state or federally operated exchange for the 2026 plan year. Consumers can begin renewing plans beginning November 16, 2025, for those purchasing a qualified health plan on New York State of Health (NYSOH), with a December 15, 2025, deadline to enroll in coverage that begins on January 1, 2026.

In addition to NYSOH’s website and app, New York health insurance notices for the 2026 plan year are to be sent out by November 1, 2025, detailing premium information, including any applicable APTC. The notices will also list the income used for the automatic renewal determination in a section titled “How We Made Our Decision.” For enrollees who do not agree with the renewal determination, they can update their application on NYSOH between November 16, 2025, and December 15, 2025, to avoid a gap in coverage starting January 1, 2026.

Those rate notices are already being loaded into the plan systems and NYSOH online, as it takes some weeks to get the rate notices set and out to enrollees. If Congress does not act imminently to reauthorize the expanded APTC, consumers will receive notices that reflect 2026 premiums without the expanded APTC.

Indeed, NYSOH has already put online, as of October 1, 2025, the ‘Compare Plans’ and ‘Estimate Costs’ tool on the website, which allows consumers to look at plan options and evaluate costs. And, for consumers using the tool now, it already reflects that the Expanded APTCs will not be available for 2026.

Potential Enhanced APTC Compromise

There are three basic options available to Congress with some variation on duration with regard to the enhanced APTCs. Congress could:

Allow the enhanced APTCs to expire. If no compromise is reached, Congress could simply do nothing and funding for the Enhanced APTCs will stop at the end of 2025.

Extend the existing enhanced APTCs. The parties could compromise and extend the enhanced APTCs either permanently or temporarily to some date certain. As noted above, a bipartisan bill (H.R. 4541) would extend the enhanced APTCs for one year, and Senator Murkowski carries a bill in the Senate (S. 2824) that would extend the subsidies for two years. The Senate Democratic minority CR would extend the existing subsidies permanently.

Modify the eligibility criteria for enhanced APTCs. Currently, eligibility has no income limit as such, but the enhanced APTC subsidies ensure that no one spends more than 8.5 percent of income for the benchmark silver plan. Congress could make changes that include: (1) modifying the eligibility criteria to the level under the ACA to 400% of the federal poverty level (FPL); (2) adjusting the limit of the percent of income for the benchmark silver plan above (or below) 8.5 percent; or (3) some other rules that limit or expand income eligibility.

Congress could also explore options that modify the maximum amount a household would be required to contribute towards the cost of coverage (currently 8.5% for households above 400 percent of FPL) or limit the application of the marketplace coverage rule, which was detailed in a prior Rockefeller Institute of Government report.

Expiration of Disproportionate Share Hospital (DSH) Funding

Additionally, scheduled reductions to DSH funding, that absent a change to New York State law, would primarily affect the availability of DSH funding for New York City, which were delayed from starting in October 2025 to October 2026 through 2028 in the initial House Reconciliation bill, but not included in HR1, are effective October 1, 2025, absent a federal extension. The DSH reduction has been delayed by Congress more than a dozen times since enactment through the ACA.12

Under current law, the availability of $2.4 billion federal DSH funding to New York, or 15 percent of federal funding for DSH ($16 billion), would be reduced. DSH funding is matched by the state or locality (through an intergovernmental transfer), making New York’s total DSH program over $4.7 billion as of federal fiscal year 2025. The Medicaid and CHIP Payment and Access Commission (MACPAC) estimates New York State’s total DSH program, including federal and non-federal shares, would be reduced by $2.8 billion, which translates to a loss of $1.4 billion in federal DSH funding (or a nearly 59 percent reduction).

On September 23, 2019, immediately preceding the last government shutdown, CMS issued a final rule, finalizing the methodology to calculate the scheduled reductions to DHS funding, as initially enacted in the ACA, during the 2020 to 2025 period. It does not appear that the Trump administration has issued guidance related to implementation in 2025; however, the regulations track with the statute, meaning the Trump administration could implement the DSH reductions required under the ACA, absent agreement on a delay.

Like an extension of the enhanced subsidies for the APTCs, an extension (meaning a delay) of the DSH cuts is an important element for New York to avoid further significant loss of federal funding (in addition to the loss of funding as a result of HR1 and the potential expiration of the enhanced subsidies).

CONCLUSION

Multiple healthcare issues are at play in the Federal government shutdown.Democrats want to restore cuts and other actions made in HR1 in an effort to mitigate the impact on residents and the healthcare delivery system, including the State’s financial plan, while Republicans are not revisiting actions taken in HR1. Among others, requested cuts to be restored in HR1 include making certain legally residing non-citizens ineligible for federal funding to purchase comprehensive coverage on health insurance marketplaces, narrowing the definition of legally residing non-citizen for purposes of public program eligibility, and reducing the match rate for emergency Medicaid.

Two additional important issues are the impending expiration of enhanced subsidies for purchasing coverage on an official ACA marketplace and the impending implementation date for previously scheduled disproportionate share hospital (DSH) reductions. As referenced above, polling suggests that the extension of the subsidy has broad public support, and there is a bipartisan bill in Congress providing an extension. In the immediate days following the shutdown, positive polling around extending the enhanced APTC suggested there was a possibility of ending the shutdown with bipartisan support. While many states benefit from these subsidies, New Yorkers, more specifically, benefit from these subsidies on the exchange and in the Essential Plan, due to the State’s adoption of the Basic Health Program option for those with income slightly above Medicaid levels. While there is some coverage and indications of support regarding the enhanced APTC subsidies, the potential for the DSH cuts to be implemented is not in the mainstream media coverage.

Moreover, with regard to the enhanced APTC subsidies, we now see that the narrative from the Republican congressional majority is shifting,13 suggesting that the enhanced subsidies might not be part of resolving the current debate playing out in Washington.

Nevertheless, compromise is still possible, particularly in light of the disproportionate impact the expiration of the enhanced APTC will have on Republican-led states and the broad impact of the scheduled DSH reductions. One potential path to ending the shutdown where both sides could arguably claim victory would be to drop the demand for restoration of the health care cuts in HR1 in exchange for extending the enhanced APTC and again delaying the DSH cuts. While this potential “victory” would be a benefit to New York and reopen the federal government, that does not mean that the restoration of cuts enacted in HR1 would not also be important to New York in future negotiations.

It’s impossible to predict exactly where things are headed right now, but the Rockefeller Institute of Government continues to monitor developments in Washington, continuing past efforts to detail who and what is at stake in the current debates. This post is preceded by a series of healthcare reports, blogs, and podcasts by our health team, which include more information on the programs discussed in this post and related topics. More information can be found in these past works in the health series, which is available here.

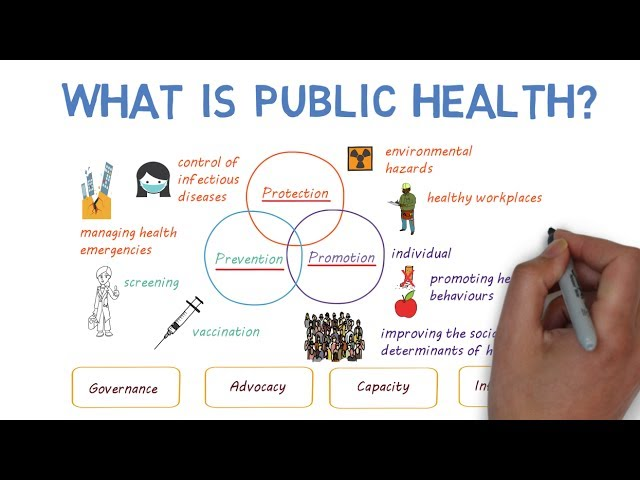

September 2025 marks a significant shift in U.S. health policy, especially its approach to the public’s health.

On September 9, the Make America Healthy Again (MAHA) Commission issued its first report pursuant to Executive Order 1421 which included 128 recommendations focused on reducing childhood chronic disease prevalence involving nutrition, chemical exposure, “over-medicalization” in pediatric care and more.

On September 19, the newly-appointed CDC Advisory Committee on Immunization Practices (ACIP) issued new guidance on MMRV, Hep B and Covid vaccines for the coming season.

On September 22, the FDA announced label updates for acetaminophen (Tylenol) during pregnancy urging caution. In response, the Blue Cross Blue Shield Association (BCBSA) and America’s Health Insurance Plans (AHIP) said they would not modify their coverage from prior guidance.

On September 26, HHS and the Food and Drug Administration (FDA) announced enforcement actions against misleading DTC prescription drug advertisements aimed at protecting consumers by increasing transparency and accuracy in drug marketing.

All these as Congress faces a federal government shutdown Tuesday where debate centers on the President’s proposed FY2026 budget that cuts CDC funding by 53% compared to FY2024, eliminates over 100 public health programs and elevates readiness risks for outbreaks (e.g., measles) and more. Neither side wants a shutdown. Both see political advantage in staying their courses:

Republicans enjoy strong MAGA support for federal spending cuts.

Democrats enjoy voter majority support for extending ACA subsidies and maintaining health programs like SNAP with eligibility/program improvements.

But neither party is trusted by the majority of voters. The public’s distaste for the political system is palpable. Confidence in Congress is at an all-time low (Gallup), and trust in the Centers for Disease Control has plummeted:

“KFF polls have shown a steady decline in the share of the public saying they trust the CDC to provide reliable information about vaccines and other topics, from a high of 85% at the onset of the COVID-19 pandemic to 57% in our latest poll in July. This drop was largely driven by Republicans, among whom the share trusting the CDC dropped from 90% in March 2020 to 40% in September 2023 before rebounding somewhat following President Trump’s 2024 election victory and Kennedy’s appointment as HHS Secretary. While trust among Democrats remained high throughout Joe Biden’s presidency, it began to decline in President Trump’s second term just as Republicans showed signs of increasing trust. As of July, Democrats remained more trusting of the CDC than Republicans, but it’s unclear how recent events might affect trust among partisans going forward.”

In June 2024, Jonathan Samet, Colorado School of Public Health) and Ross C. Brownson (Washington University) offered this view:

“Public health system” is an optimistic misnomer in the United States, as it is used in reference to a fragmented and loosely connected set of entities. Moreover, the public health system, which is itself not readily delimited, is part of a system of systems that encompasses at least governmental public health; community-based organizations; the health care sector; and the education, training, and research of the academic public health and medical enterprises. The organization, policies, and politics of public health in the United States present opportunities and challenges. In the current decentralized model of public health, governance and are distributed across more than3,300 state and local health departments. “

My take:

Public health is a vital part of the U.S. health system but a stepchild to its major players. In reality, the U.S. operates a dual system: one that serves those with insurance (public and private) and another for those without. Public health programs like SNAP, HeadStart, Federally Qualified Health Centers et. al., serve lower income and under-insured populations and integrate with local delivery systems emergency services and during mass-events like pandemics, mass-casualties and disease outbreaks. Funding for public health programs is 2-5% of total health spending shared between local, state and federal governments.

Studies show food, housing and income insecurity—areas targeted by public health– correlate to chronic disease prevalence and health costs. Unlike most developed systems of the world which operate at a lower cost and produce better population-health outcomes, our system perpetuates a structural divide between healthcare and public health. Integrating the two is a necessary strategy for system transformation, but a difficult task given entrenched animosity toward “the system” held by public health leaders and funding pressures. The bridge between public health and the healthcare delivery systems is a two-lane road with lots of potholes at the federal level, and sometimes better in local communities. But funding seems to be an afterthought unless local communities deem it vital.

Public health is an opportunity for industry leaders to demonstrate pursuit of the greater good. Most public health programs are under-funded and dependent on a patchwork of local, state and federal appropriations (sometimes augmented by philanthropy) to keep their doors open. A particular opportunity exists for not-for-profit hospitals and health systems who enjoy tax exemptions to pursue integration as the core community benefits strategy, offering community leaders a sensible basis for eliminating duplicative services, expanding preventive health services and reducing demand for unnecessary hospitalizations resulted from uncoordinated care.

As the federal shutdown is addressed this week in DC, public health officials will be watching closely. As noted on the American’s Public Health Association website (www.apha.org) “The health care industry treats people who are sick, while public health aims to prevent people from getting sick or injured in the first place. Public health also focuses on entire populations, while health care focuses on individual patients.” Both are necessary but responsibility and funding for the public’s health seems in limbo.

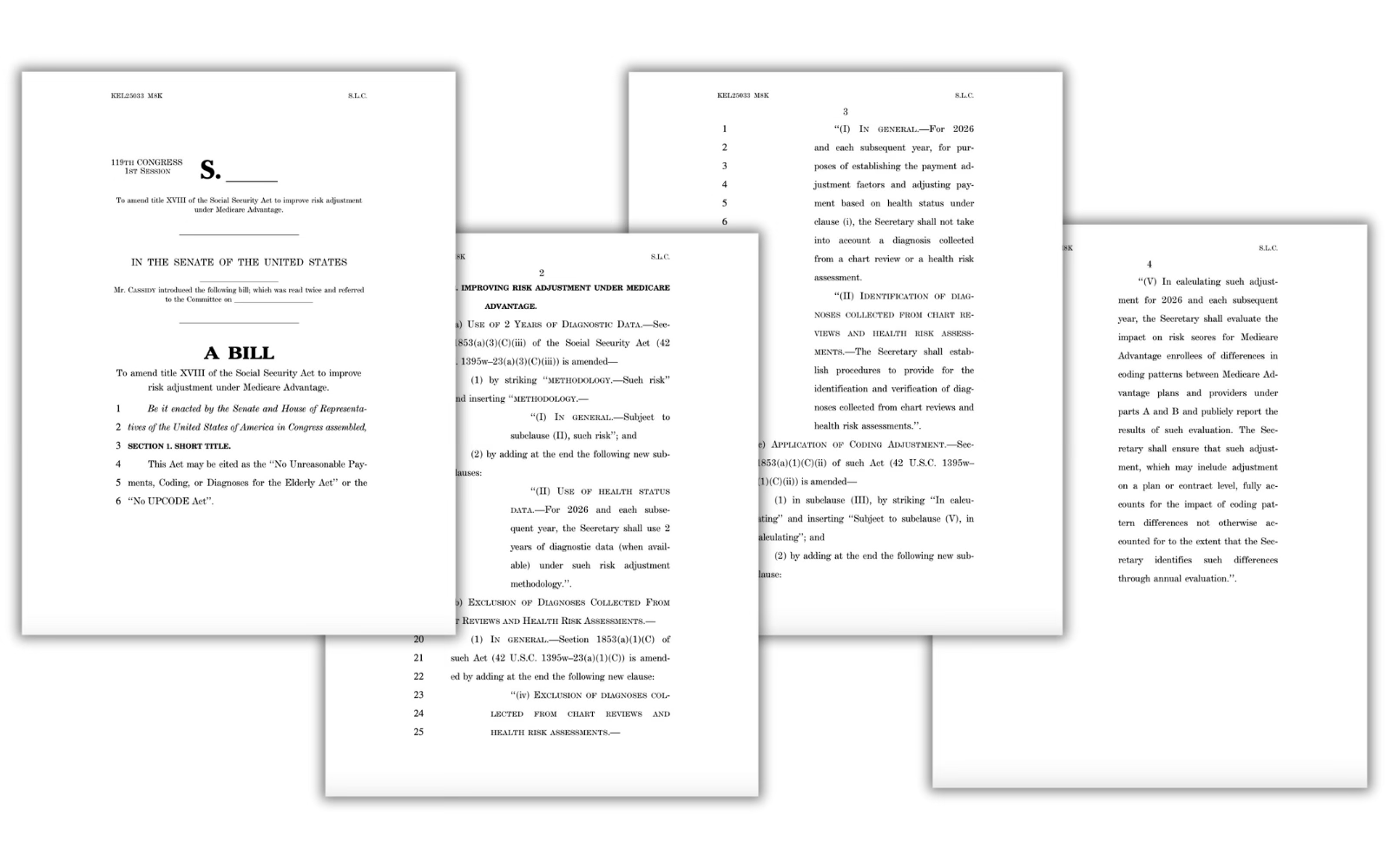

Medicare Advantage Majority and Better Medicare Alliance are flooding the zone with attacks against bipartisan legislation aimed at curbing health insurers’ “upcoding” maneuver.

HEALTH CARE un-covered readers were the first to tip me off to television attack ads against the bipartisan No UPCODE Act, sponsored by Senators Bill Cassidy (R-LA) and Jeff Merkley (D-OR). The ads in question, airing in the Washington D.C. media market, were paid for byMedicare Advantage Majority (MAM), which bills itself as a patient and provider coalition but has all the markings of a front group funded by the nation’s largest health insurers.

After a quick search through MAM’s YouTube channel, I think I found the ad I was tipped about. Titled “Voices,” the video features six seniors fawning over their Medicare Advantage plans – and it ends with a desperate plea to “oppose the No UPCODE Act” and “protect Medicare Advantage.”

MAM appears to have been propped up fairly recently – with their earliest ad (that I can find) from October 2024. All of their ads support Medicare Advantage. Some appear nonpartisan, while others are more overtly political, like the ad “Biden’s Playbook.” Here is a transcription of that ad:

“President Trump kept his promise to protect Medicare benefits for millions of American seniors. But now some in Congress want to take a page out of Joe Biden’s playbook and cut Medicare. These cuts threaten primary and preventative care that help keep millions of seniors healthy while also raising costs.

It’s a betrayal. It’s why people don’t trust Washington. Don’t let the politicians cut Medicare. Tell Congress to stand with President Trump and protect America’s seniors.”

None of MAM’s ads mention the expensive hidden fees, narrow networks of doctors and life-threatening prior-authorization hurdles often associated with private Medicare Advantage plans. Nor does it even hint at why Sen. Cassidy, a doctor and senior Republican leader and committee chair, introduced the No UPCODE Act in the first place: to reduce the tens of billions of dollars in overpayments to Medicare Advantage insurers and keep the Medicare Trust Fund solvent for years longer. Those overpayments – at least $84 billion this yearalone – is a leading reason why the Medicare Trust Fund is being depleted.

But Medicare Advantage Majority is not the only insurance industry front group flooding the zone.

I kid you not, while I was writing this very article I got a text from a different Big Insurance-funded group fear-mongering the same “cuts” to Medicare Advantage. As I’m typing away on my laptop, my phone dings… The first words in the text read: “ATTENTION NEEDED:”. The message had all the hallmarks of a cookie-cutter political blast that was cooked up by some DNC-alum or K Street PR strategist.

When I followed the prompt and clicked on the link, it took me to one of the industry’s most trusted hands in the Medicare Advantage fight, the Better Medicare Alliance (BMA) – one of my former colleagues’ most essential propaganda shops these days.

BMA is a slickly branded PR and lobbying shop that presents itself as a coalition of “advocates” working to protect seniors’ care, but it’s heavily funded by private insurers in the MA business who reap billions in those overpayments from taxpayers each year. BMA’s board has been stacked with Humana and UnitedHealth representatives and allies tied to medical schools like Emory and Meharry Medical College. For years, they’ve spent millions lobbying and propagating to protect MA insurers’ profits. This includes rallying against the No UPCODE Act since July; opposing CMS’ risk adjustment model in 2024 (which should help reduce some of the overpayments); and objecting vigorously to any Medicare Advantage plan payment reductions, year in and year out.

In short, BMA and MAM are both 501(c)(4) “social welfare” nonprofits used by Big Insurance as part policy shop, part lobbying arm, and part attack dog. Together, they make up a strategy for insurers that want to keep their MA cash cows gorging on your money.

None of this is new, though. It’s the same PR crap I used to fling back in the old days when I was an industry executive and had to peddle Medicare Advantage plans. (Its deliciously ironic that MAM had the audacity to use the term “playbook” in one of its ads. In my old job I used to help write the industry’s playbook.) Each fall we’d work with AHIP (formerly America’s Health Insurance Plans) to host “Granny Fly-Ins” in Washington, D.C. Industry money (actually, taxpayer money) would cover the fly-in expenses, and the seniors would trot around Capitol Hill to extol the supposed benefits of Medicare Advantage plans and dare lawmakers to tamper with it. And that tactic worked for years. Of course, this was all before texting existed.

The squeal tells the story

For years, MA insurers have exaggerated how sick their patients are on paper (making them seem sicker so they can get a bigger taxpayer-funded handout). Hence the term “upcoding.” And the sick joke is – unfortunately – the same insurers who profit most from this upcoding scheme are using their taxpayer loot to stop this bill from gaining traction.

I think the industry’s squeal tells the story.

Let’s be real: Big Insurance wouldn’t be running this PR and lobbying blitz unless this legislation really would do some major good for Americans. The No UPCODE Act is a strong, bipartisan step toward ending wasteful, fraudulent practices that funnel taxpayer money into the pockets of industry executives and Wall Street shareholders. This one bill could save taxpayers as much as $124 billion over the next decade and keep the Medicare Trust Fund solvent for years longer.

You can be sure, though, that people on Capitol Hill and the administration already know ads like these are industry-funded. They see them for what they really are — part of a well-financed intimidation campaign. A game. Running ads like these is the industry’s way of flaunting its power and a reminder that big money can and will be spent in Congressional campaigns — and possibly (again) even during the Super Bowl — to mislead voters.

So remember, when you see an ad or get a text from an organization like MAM or BMA – know that these organizations have a lot to lose if legislation like the No UPCODE Act becomes law. And spending your premium and tax dollars on text blasts and TV spots are well worth the investment – to them, anyway.

Congress on Wednesday enters the eighth day of the federal shutdown with neither party giving an inch and the path to a resolution nowhere in sight.

But something will have to give if lawmakers hope to reopen the government in any timely fashion, and that movement will likely be the result of external forces exerting pressure on one party — or both of them — to break the deadlock.

That’s been the case in the protracted shutdowns of years past, when a number of outside factors — from economic sirens to public frustration — have combined to compel lawmakers to cede ground and carry their policy battles to another day.

Public sentiment

Among the most recycled quotes on Capitol Hill is attributed to Abraham Lincoln: “Public sentiment is everything.” The trouble, in these early stages of the shutdown fight, is that the verdict is still out on where that sentiment will land.

That uncertainty has led both parties to dig in while they await more concrete evidence of which side is bearing the brunt of the blame. But those polls are coming, and if history is any indication, they will be a potent factor in forcing at least one side to shift positions for the sake of ending the shutdown.

That was the case in 2013, when Republicans demanding a repeal of ObamaCare saw their approval ratings plummet — and dropped their campaign after 16 days without winning any concessions. A similar dynamic governed the shutdown of 2018 and 2019 — the longest in history — when Republicans agreed to reopen the government without securing the border wall money they’d insisted upon.

A recent CBS poll found that 39 percent of voters blame Trump and Republicans for the shutdown; 30 percent blame congressional Democrats; and 31 percent blame both parties equally.

A Harvard/Harris poll also showed that more respondents blame Republicans, 53 to 47 percent, but nearly two-thirds believe Democrats should accept the GOP’s stopgap funding bill without a fix for the expiring Affordable Care Act premium subsidies.

The ambiguity of those sentiments has heightened the partisan blame game — and has given both sides an incentive to hold the line until a clearer picture emerges.

Air traffic controller issues

It was nearly seven years ago that the 35-day shutdown ended after travel chaos and short-staffing of air traffic controllers brought immense strain on the aviation sector — and trouble is already starting up again.

An uptick of air traffic controllers calling in sick Monday forced numerous flight delays and cancellations, prompting concerns that a reprisal of what happened in 2019 could be starting up again.

“We should all be worried,” said Sen. Mike Rounds (R-S.D.), who was part of informal rank-and-file talks last week about a possible resolution.

Transportation Security Administration workers and air traffic controllers are all considered essential workers, with the Department of Transportation announcing more than 13,000 controllers are set to work without pay during this shutdown.

Those calling in sick prompted delays at numerous big airports, including Denver International Airport and Newark Liberty International Airport. The Hollywood Burbank Airport went without any air traffic controller on-site for nearly six hours Monday.

Just like the record-setting 2019 shutdown, Democrats are counting on this issue creating problems for Trump and Republicans. Sen. Chris Van Hollen (D-Md.) told reporters that he and other local officials are holding a press event at Baltimore/Washington International Thurgood Marshall Airport on Wednesday to highlight the rising issue.

“It had a direct impact on people’s abilities to get around the country,” Van Hollen said of the 2019 shutdown issue. “Donald Trump shut down the government in his first term, and he needs to end the shutdown he ended in the second term.”

Frozen paychecks

The central, defining factor of any shutdown is the scaling back of federal services and the siloing of hundreds of thousands of federal employees. Some of those workers are deemed “essential,” meaning they still have to come to work, while others are furloughed, meaning they’ll stay at home. But both groups share the unenviable position of not being paid until the government reopens.

That reality will hit home Oct. 10, when the first round of federal paychecks will fail to go out. The most immediate impact, of course, is on those workers and their families, who will have to find alternative ways to pay bills and make ends meet.

But the pain will also reverberate through the broader economy, as federal workers stay at home and avoid the types of routine daily purchases — lunches, cabs, haircuts — that can make local economies hum.

The numbers are enormous.

The White House Council of Economic Advisers has estimated that every week of the shutdown will reduce the nation’s gross domestic product by $15 billion.

“This is resulting in crippling economic losses right now,” Speaker Mike Johnson (R-La.) warned Tuesday. “A monthlong shutdown would mean not just 750,000 federal civilian employees furloughed right now, but an additional 43,000 more unemployed Americans across the economy, because that is the effect, the ripple effect, that it has in the private sector.”

In a typical shutdown, furloughed workers receive back pay for the days lost during the impasse, providing a delayed bump in economic activity. But even that customary practice is now in question in the face of a threat from Trump’s budget office to withhold back pay for certain workers. Others, Trump has said, will be fired altogether.

The combination is sure to exacerbate a volatile economy that’s already been roiled by declining consumer confidence, sinking job creation and Trump’s tariffs. Whichever party suffers the blame for the economic strain will come under the most pressure to cave in the shutdown fight.

Military paychecks

Pay for members of the military has been a constant talking point in past shutdowns, and that’s no different this go-around.

Military service members could miss their paychecks Oct. 15, a date front and center for lawmakers.

Johnson huddled with Senate Republicans on Tuesday during their weekly policy luncheon and told reporters afterward that he is considering having the House vote on a bill to pay troops.

“I’m certainly open to that. We’ve done it in the past. We want to make sure our troops are paid,” Johnson said, noting one GOP member has filed legislation aimed at doing that. “We’re looking forward to processing all of this as soon as we gather everybody back up.”

The Speaker added that the shutdown would need to end by Monday in order to process the paychecks by Oct. 15.

One problem for Johnson, though, is that the House is not slated to return until Monday at the earliest, and he has indicated that he will keep the chamber out of session until the shutdown is over.

Democrats indicated they are also worried about those impacts, but say Johnson has bigger fish to fry.

“I’m concerned about all the impacts of a shutdown. … There’s a lot of impacts of a shutdown,” Sen. Chris Murphy (D-Conn.) said. “How on earth does Mike Johnson say anything with a straight face right now when he won’t even bring his members here to vote on anything? How does he know what he can deliver if his members aren’t even here?”

“It’s not worth listening to anything the Speaker says until he tells his people to get back and show up for work.”

Health care factors

Democrats have made health care the lynchpin of their opposition to the Republicans’ short-term spending bill, demanding a permanent extension of enhanced Affordable Care Act (ACA) subsidies set to expire at the end of the year.

Citing that expiration date, GOP leaders have refused to negotiate on the issue as part of the current debate, saying there’s time to have that discussion after the government opens up.

“That’s a Dec. 31 issue,” Johnson told reporters Tuesday.

But there are several related factors that will surface long before Jan. 1, and they could put pressure on GOP leaders to reconsider their position in the coming weeks.

For one thing, private insurance companies that sponsor plans on the ObamaCare marketplace are already sending out rate notices to inform patients of next year’s costs. Those rates are crunched based on current law — not predictions about what Congress might do later — meaning they’re being calculated under the assumption that the enhanced subsidies, which were established during the COVID-19 pandemic, will expire Jan. 1.

That distinction is enormous: If Congress doesn’t act, the average out-of-pocket premium for patients enrolled in ObamaCare marketplace plans would jump by 75 percent, according to KFF. Those are the figures patients are already getting in the mail. And faced with drastically higher rates, many are likely to buy lesser coverage next year — or no coverage at all.

Adding to the time squeeze, the ACA’s open enrollment period begins Nov. 1, meaning patients will begin making their decisions long before GOP leaders say they’re ready to act.

“Insurers aren’t waiting around to set rates for next year,” Senate Minority Leader Chuck Schumer (D-N.Y.) warned this week. “They’re doing it right now — not three months from now.”

Hospitals and health systems across the country are telling some Medicare and Medicaid patients that they can’t schedule telehealth appointments due to the federal government’s shutdown, now heading into its second week. That’s because Medicare reimbursement for telehealth expired on September 30, leaving health systems with the choice of pausing such visits or keeping them going in hopes of retroactive reimbursement after the shutdown ends.

Reimbursement for the Hospital at Home program, which allows patients to receive care without being admitted to a hospital, also lapsed with the shutdown. That led to providers scrambling to discharge patients under the program or admit them to a hospital. Mayo Clinic, for example, had to move around 30 patients from their homes in Arizona, Florida and Wisconsin to its facilities.

At issue in the government shutdown is healthcare, specifically tax credits for middle- and lower-income Americans that enable them to afford health insurance on the federal exchanges set up by the Affordable Care Act. Democrats want to extend those tax credits, which are set to expire at the end of the year, while Republicans want to reopen the government first and then negotiate about the tax credits in a final budget.

The impasse has prevented the Senate from overcoming a filibuster, despite a Republican majority. Around 24 million Americans get their health insurance through the ACA, and the loss of tax credits will cause their premiums to rise an average of 75%–and as high as 90% in rural areas–and likely cause at least 4 million people to lose coverage entirely.

The government’s closure has reverberated through its operations in healthcare. The Department of Health and Human Services has furloughed some 41% of its staff, making it harder to run oversight operations. CDC’s lack of staff will hinder surveillance of public health threats. And FDA won’t accept any new drug applications until funding is restored.

When the government might reopen remains unclear. Most shutdowns are relatively brief, but the longest one, which lasted 35 days, came during Donald Trump’s first term. Senate majority leader John Thune, R-S.D., and Speaker of the House Mike Johnson, R-La., have both said they won’t negotiate with Democrats, and the House won’t meet again until October 14.Bettors on Polymarket currently expect it to last until at least October 15. Pressure on Congress will increase after that date because there won’t be funds available to pay active military members.

Hospitals in rural and underserved areas could lose out on billions of dollars in federal funding if the government shutdown drags on.

Why it matters:

Many hospitals already run on tight margins and are bracing for fallout from Medicaid cuts and other changes in the One Big Beautiful Bill Act.

The big picture:

The immediate concern is health policies that expired when government funding lapsed at midnight Tuesday. Health providers and their lobbyists expect Congress will make providers whole in an eventual funding deal and reimburse claims made during the shutdown.

But that’s not a given. And uncertainty about how long the shutdown will go on is leaving some of the most financially vulnerable hospitals in limbo.

“There’s just that underlying fear of, oh my gosh, what if they can’t come together on any agreement to open the government again, and we all get looped into it,” said Kelly Lavin Delmore, health policy adviser and chair of government relations at Hooper Lundy Bookman.

State of play:

Safety-net hospitals face an $8 billion cut to Medicaid add-on payments in the absence of a government funding package.

The cuts to so-called disproportionate share hospital payments originate from the Affordable Care Act.

Congress has postponed the pay reductions more than a dozen times, but the most recent delay expired on Tuesday and Congress hasn’t signaled if or when it will step in.

The add-on payments are made quarterly, so hospitals may not feel immediate effects, even if Congress doesn’t further delay the cuts, according to the American Hospital Association. But state Medicaid agencies could let the cuts take place if they think lawmakers’ standoff will continue indeterminately, per AHA.

The uncertainty “really impacts that predictability and reliability as it relates to funding,” said Leonard Marquez, senior director of government relations and legislative advocacy at the Association of American Medical Colleges.

If the cuts do take effect, it would significantly hamper hospitals’ ability to care for their communities, Beth Feldpush, senior vice president of advocacy and policy at America’s Essential Hospitals, told Axios in a statement.

Additionally, two long-running programs that give pay bumps to rural hospitals expired on Wednesday.

One program adjusts Medicare payment upward for rural hospitals that discharge relatively few patients.

The other gives increased reimbursement rates to rural hospitals that have at least 60% of patients on Medicare.

They were designed to keep care available in communities that might otherwise not be able to support a hospital.

Both programs have expired in the past, only to be brought back to life with claims paid retroactively.

Zoom out:

Hospital industry groups have also been urging Congress to extend enhanced Affordable Care Act tax credits, which have become a flashpoint in the shutdown fight. Democrat lawmakers have so far refused to pass GOP-led funding proposals that don’t include a full extension of the subsidies.

What they’re saying:

AHA is urging Congress to find a bipartisan solution and reopen the government, a spokesperson told Axios.

“Patient care doesn’t go away with the loss of coverage and the loss of funding,” said Lisa Smith, vice president of advocacy and public policy for the Catholic Health Association.

“I just don’t know how long that’s going to be sustainable for our facilities that are really already operating on the margins.”

The Trump 2.0 administration is 8-months into its MAGA agenda. Summer has passed. Schools are open. Congress is in session. Campaign 2026 is underway. The economy is slowing and public sentiment is dropping.

For U.S. healthcare, it’s more bad news than good. The challenges are unprecedented. Most organizations—hospitals, medical groups, drug and device makers, infomediaries and solution providers, insurers, et al—are defaulting to lower risk bets since the long-term for the health system is unclear.

The good news is that the health system in the U.S. is big, fragmented, complex, expensive (5% CAGR spending increases thru 2034) and slow to change. It is highly regulated at local, state and federal levels, labor intense (20 million) and capital-dependent (government funding, private investment)—a trifecta nightmare for operators and goldmine for private investors who time the system for shareholders effectively. And it operates opaquely: business practices are hidden from everyday users and bona-fide measures of its effectiveness not widely applied or accepted.

The bad news is its long-term sustainability in its current form is suspect and its short-term success is dependent on adapting to key tenets in Trump Healthcare 2.0:

Trump Healthcare 2.0 is about reducing federal healthcare spending so federal deficits appear to be going down to voters in the mid-term election (November 3, 2026). Healthcare, which represents 27% of federal spending is an attractive target since a significant majority of all voters (especially MAGA Republicans) are dissatisfied with its performance and think is wasteful and inefficient. It views healthcare as a market where less government, more private innovation achieves more.

The effect of One Big Beautiful Bill Act cuts to Medicaid and marketplace subsidies and imposition of Make America Healthy Again dogma in CMS, CDC, FDA and FCC are popular in the MAGA base while problematic to states, hospitals, physicians and insurers whose business practices and clinical accountability will be more closely scrutinized.

The federal courts—SCOTUS, 13 circuit and 94 district courts– will support Trump Healthcare 2.0 policy changes in their decisions favoring state authority over federal rules, enabling White House executive orders and administrative actions against challenges and departmental directives that encourage competition, price transparency and cost reduction.

The FTC and DOJ will pro-actively pursue actions that reverse/disable collusion, horizontal and vertical consolidation in each sector deemed to raise prices and lower choices for consumers.

In the administration’s posturing for the mid-term election November 3, 2026, it’s assumed the economy and prices will be THE major issues to voters: healthcare affordability, housing costs and food prices will get heightened attention as a result. Thus, every healthcare organization board and leadership team should revisit short and long-term strategies, since traditional lag indicators re: utilization, regulations, structure, roles, responsibilities and funding are decreasingly predictive of the future.

Though every organization is different, there are 6 takeaways that merit particular attention as C suites and Boards re-evaluate strategies and timing:

Monitor the entire economy. The healthcare is 18% of the GDP; 82% of commerce falls outside its domain. Appropriations for healthcare compete with education, defense and public safety and health; household spending for healthcare competes with housing, food and transportation costs. The healthcare dollar is not insulated from competing priorities. If, as expected, the economy slows due to slowdowns in the job market and in housing, and if cuts to marketplace subsidies are enacted, healthcare spending will quickly and significantly drop though utilization will increase.

Follow clinical innovations carefully. Understand bench to bedside obstacles. The FDA will authorize 50-60 novel drugs and biologics and over 100 AI-enabled devices this year. Some will fundamentally alter care management processes; all will change costs and pricing. Those with short-term cost-reduction potential require consideration first. Given increased margin pressures, capital and operating budgets will reflect a more cautious and risk averse posture.

Manage fixed costs (more) aggressively and creatively. Direct costs reduction is not enough. Facilities and administrative functions are fair game and for outsourcing, partnerships and risk sharing with suppliers, vendors, advisors and even competitors.

Don’t underestimate price transparency. Prices matter. Consumers and regulator demand for price transparency from drugmakers, hospitals and insurers are inescapable. Justification and verification will be critical to trust and utilization.

Navigate AI strategically. The pace and effectiveness of Ai-enabled solutions will define winners and losers in each segment. And private capital—investors, partners—will bring those solutions to market.

Don’t discount public opinion. Consumer sentiment about the economy is low and dissatisfaction with the health system is high and increasing. Understanding root causes and initiating process improvement are starting points.

As I head back to DC today, the FY26 federal budget is in suspense as the GOP-controlled Senate and House debate a final version to avoid a shutdown next week. Physicians, public health and state officials will digest last week’s ACIP vaccine advisory recommendations and issue their own directives and insurers will file their plan revisions for 2026. That’s what lawmakers and trade groups will be watching.

But at the kitchen tables in at least 40% of America’s households, unpaid healthcare bills from hospitals, labs, doctor offices and set-aside cash for over-the-counter remedies and prescription drug co-pays are on the agenda. Student loan payments, escalating costs for groceries, housing, rent and child care and an unstable employment market are squeezing families. Budgeting for healthcare is more problematic for them than anything else because price are not accessible and charges are not known until after services are performed.

Trump Healthcare 2.0 is not transformational: it is transactional. It aims to simplify the system and facilitate changes certain to disrupt the status quo. Its locus of control, is Main Street USA. not Pennsylvania Ave, in DC.

Republicans’ sweeping Medicaid overhaul has left a lot of the heavy lifting to governors and state health officials as the program launches the biggest package of changes in its 60-year history.

Why it matters:

States working with hospitals, clinics and other providers will have to do more with less as they face about $1 trillion in program cuts and the likelihood of 10 million or more newly uninsured people from new work rules and other changes.

While the GOP views Medicaid as a waste-riddled program that’s due for a shakeup, the cuts will force painful tradeoffs at the local level as health systems also struggle with inflation, higher labor costs and rising medical costs.

“Congress left the dirty work to be done by the governors and state legislators, and that work will start very soon,” said Joan Alker, executive director of Georgetown University’s Center for Children and Families.

State of play:

Medicaid typically accounts for about 30% of a state’s budget each year. Spending goes up during tough economic times, and states are required to cover a set of mandatory benefits.

The fallout from the cuts will vary by state based on their reliance on certain funding mechanisms, like taxes on health care providers, and whether they’ve expanded Medicaid coverage under the Affordable Care Act.

The new work requirements only apply to people in the expansion group.

The biggest changes from the law will arrive in 2027. But states have already started planning for how they’ll implement work requirements, decide who’s eligible more frequently and cope with new restrictions on how they draw down federal funds.

They’ll also be competing for $50 billion in rural health funding that Congress added to the law — a sum that’s been widely criticized as inadequate.

“We are working day and night ever since this bill was passed,” New York’s Medicaid director, Amir Bassiri, said while speaking at a conference in Manhattan in July.

“Chances are we will not be able to mitigate all of the impacts of these changes, but we’re going to do everything in our power to do that.”

The other side:

The new dynamic will force states to think more critically about how taxpayer dollars are being spent in Medicaid, said Brian Blase, president of Paragon Health Institute and a White House official during the first Trump administration.

“I want there to be a real budget constraint so [states] have to grapple with the actual cost of these programs,” he said.

Zoom in:

Many states were already preparing austerity moves before President Trump signed the law. States faced with Medicaid budget crunches often cut or limit benefits they aren’t required to offer, like dental care or home- and community-based services.

Other strategies to adjust to the new era of Medicaid funding could include reducing Medicaid payment rates for providers or finding new sources of revenue like additional taxes.

A big focus is how well states will track whether recipients are either meeting a requirement to complete 80 hours of work, school or community service a month or are exempt from the rules.

Illinois, Missouri, Montana, North Dakota, New Mexico, Utah and Wisconsin have the highest risk of improperly kicking many eligible people off of Medicaid due to procedural issues, per a recent Georgetown Center for Children and Families report.

The report ranked state performance on eight key metrics, including how long Medicaid centers take to answer calls, how long the states take to process new applications and whether they renew eligibility automatically.

Between the lines:

Congress authorized $200 million in federal funds to help states modernize their infrastructure for determining whether people are eligible for Medicaid.

HHS communications director Andrew Nixon said $100 million of the funds will be allocated equally among states, while the other half will be divvied up based on the share of enrollees in the state that will be subject to work requirements.

“All funding decisions will be guided by efficiency and legal compliance,” he said in an email.

States are still waiting for guidance and regulations from Medicaid administrators on some of the policy changes, and what kinds of technology they can use to ease the burden of reporting work hours and verifying who’s eligible.

Even timelines for getting systems running are up in the air. The budget law gives the Centers for Medicare and Medicaid Services discretion to let states have up to two more years to get work requirements up and running.

What we’re watching:

What role health systems and Medicaid advocates have in states’ decision-making processes — and whether they can persuade state lawmakers to make up for some of the federal cuts with state funds.

“We’ve always said the cuts to Medicaid are … going to impact so many other parts of state budgets, and so that’s where the fight really is,” said Nicole Jorwic, chief program officer of Caring Across Generations, a nonprofit that advocated against Congress’ health care changes.

Privately administered Medicare Advantage (MA) has long been the subject of policy debate. To some, the once-nascent source of Medicare coverage is an important mechanism for injecting competition and innovation into the government-sponsored insurance program. To others, it represents an expensive and unnecessary alternative to directly administered traditional Medicare (TM).

After years of rapid growth, MA accounted for most program enrollments (33.6 million) and federal spending ($494 billion) in 2024.1 This has intensified some existing debates but also spurned increasing bipartisan agreements and interest in reforms. Politicians and policy experts who have historically supported MA, including some Republicans, have articulated greater openness to reforming the now-entrenched program.2 In effect, the debate has shifted from whether the MA program should be reformed to how it should be reformed and, critically, what the government should do with any savings. This Viewpoint discusses notable areas of consensus (and lack thereof) and the prospect of reforms from the Trump administration.

Areas of Growing Consensus

Several observations about MA are generally agreed upon.First, MA plans can use utilization management tools, like prior authorization, to constrain costs in ways that TM generally cannot. This reduces MA plans’ costs of covering Part A (hospital) and B (physician) benefits compared with a scenario where they imposed few constraints on utilization, like in TM. Policymakers also increasingly recognize the administrative burdens imposed on clinicians and restraints on patient access due to these tools, which have generated growing interest in reforms.

Second, and perhaps paradoxically, the federal government would spend less if all MA enrollees instead chose TM. This reflects several factors. MA plans are paid benchmark rates that are set above the fee-for-service spending in many counties. Plan payments can increase further due to the quality-bonus program. MA plans also have higher coding intensity, meaning the same beneficiary has more diagnoses recorded if they are enrolled in MA rather than TM. This increases risk scores and payments from the government (whether this reflects more accurate coding vs fraudulent behavior remains a source of debate). In addition, MA plans experience advantageous selection, meaning they attract enrollees who are relatively cheaper to cover conditional on their observable characteristics.3All told, the Medicare Payment Advisory Commission estimates that the federal government spends 20% more (or an estimated $84 billion in 2025) than if all enrollees chose TM.1 While the exact magnitude of difference is subject to debate, the basic conclusion is not.

Third, MA plans offer more generous benefits to enrollees, including lower out-of-pocket costs and coverage of additional benefits such as vision and dental services. This occurs because plans keep a portion of the difference between their bid and the benchmark rate. These rebates average $2255 annually per enrollee, which represents 17% of all spending on MA.1

Where Disagreements Remain

While there is growing acknowledgment of the fiscal costs of the MA program, there is disagreement or uncertainty about several questions that inform an appropriate policy response. First, there is debate about how valuable some supplemental benefits are to enrollees. While it is relatively straightforward to value reductions in premiums or cost sharing in MA plans, there is limited information about how often enrollees use many of the supplemental benefits. Some research suggests that use of certain extra benefits may not be much higher in MA plans.4

Partly because of this, it is uncertain how much payment reductions to MA plans will reduce benefits and, in turn, how much that reduces enrollee welfare. Some research suggests the last dollar spent on MA plans results in much less than a dollar’s worth of additional benefits, particularly in markets with limited competition between plans.5This suggests that reducing payments would initially lower plan profits but result in minimal welfare loss for enrollees. Even if true, it is not obvious when this tradeoff becomes more pronounced. Other research indicates the aggregate value of reduced cost sharing represents a large share of excess payments, suggesting reducing spending may quickly trigger benefit reductions.6 These effects may further depend on how policymakers chose to alter payments.

Finally,there remains significant disagreement about how to use any savings generated by program reforms. Democratic lawmakers often argue that savings should be used to increase TM benefits (eg, by adding dental benefits or imposing an out-of-pocket cap). Republicans are much more likely to pair spending reduction with policies that boost MA (eg, allowing MA plans to keep more of the savings if they bid below benchmarks). This predominantly reflects different preferences over the optimal structure of Medicare rather than empirical uncertainty.

Reform Possibilities From the Trump Administration

Many observers expect that the current administration will be relatively generous toward MA, as is typical of a Republican administration. This is particularly true given that the Centers for Medicare & Medicaid Services (CMS) administrator, Mehmet Oz, MD, has historically expressed support for MA plans. While major spending reductions may remain unlikely, early actions suggest the administration supports targeted reforms and is likely to test changes to the program’s design.

In his Senate confirmation, Oz was explicitly critical of strategic upcoding by insurers. Early policy decisions have been consistent with this view. The 2026 final payment notice for MA continues implementation of several policies that reduce MA payments. Notably, the Trump administration finalized implementation of an updated risk adjustment model that is designed to partly address coding intensity. For example, it eliminates approximately 2000 diagnosis codes that were judged to be most prone to upcoding. In conjunction with related changes, this is expected to decrease plan payment by 3.01%.7 CMS also announced the expansion of audits aimed at verifying the accuracy of diagnoses recorded by MA plans.8 This suggests the administration is willing to address strategic behavior by insurers, which they characterize as addressing waste, fraud, and abuse.8

However, the final payment notice also included higher payment increases for MA plans than was initially proposed by the Biden administration (5.06% vs 2.23%). After accounting for coding trends, realized payments are expected to increase by 7.16%. While consistent with an effort to boost MA enrollment, CMS noted that this change predominantly reflected the effects of higher-than-expected growth in per capita costs in TM, which mechanically increased payment updates. While CMS has some flexibility in payment updates, observers should use caution when using these upward revisions to infer the administration’s level of support for MA.

If the current administration is open to more novel and consequential reforms, they are likely to emerge from the Centers for Medicare & Medicaid Innovation (CMMI). While CMMI demonstration projects have historically focused on TM, the office can test changes to key features of MA that would significantly alter spending and incentives. Notably, Abe Sutton, JD, the director of the CMMI, recently highlighted the possibility of testing changes to risk scores, benchmarks, and quality measures, suggesting they are interested in taking advantage of this authority.9

With its place in the Medicare program now firmly established, MA has begun to attract more consistent interest in reform, even among Republican policymakers. This may reflect political considerations, as an unwillingness to act may provide an opportunity (and a source of budgetary savings) for future lawmakers to pursue alternative policy goals. Early signals from the Trump administration suggest they support program reforms, especially those targeting strategic behavior by insurers. Given the slim margins in Congress, it will be interesting to see if and how the administration uses CMMI’s authority to pursue substantive program changes.