When Congress passed pandemic-era enhancements to Affordable Care Act (ACA) premium subsidies in 2021, it wasn’t just a policy tweak — it was a lifeline. But unless lawmakers act, those subsidies will vanish on January 1, 2026.

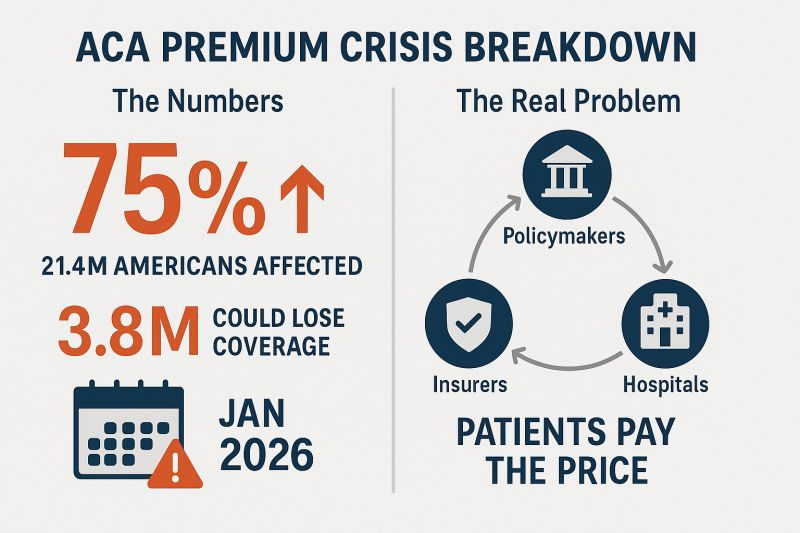

According to KFF, the average ACA enrollee could see premiums spike 75% overnight. For many, that will mean a choice between things like their health coverage and rent or food. The Congressional Budget Office estimates more than 4.2 million people could lose coverage over the next decade as a result. Below is where the expired subsidies will hurt the hardest:

1. Young adults… and their parents’ wallets

Young people who’ve aged out of their parents’ plans and buy coverage through the ACA marketplaces will see some of the steepest jumps.

If they decide to forgo coverage, as KFF Health News warns: The so-called “‘insurance cliff’ at age 26 can send young adults tumbling into being uninsured.”

The parents and families of these young adults could be left scrambling to cover unexpected medical bills — the kind that can derail a family’s finances for years.

2. Main street entrepreneurs

The ACA is the only real option for many small-business owners, freelancers and gig workers. These are the folks that conservatives say we should encourage to build and grow their own businesses who make up the backbone of Main Street. Losing the enhanced subsidies means many will face premiums hundreds of dollars higher per month. Some will be forced to close shop and turn to jobs at out-of-town corporations flush enough to afford to offer subsidized coverage to their workers, a direct hit to local economies.

3. States already in crisis

States aren’t in a position to plug the gap. Politico reports that California, Colorado, Maryland, Washington, and others are scrambling to soften the blow, but even the most ambitious state-level plans can’t replace hundreds of millions in lost federal funding.

And this comes right after Medicaid cuts in the One Big Beautiful Bill Act that will hit hospitals, clinics and low-income communities. In Washington state alone, officials expect premiums to jump 75% when the subsidies expire, with one in four marketplace enrollees dropping coverage. That means more uninsured patients showing up in ERs, less preventive care, and more strain on already struggling rural hospitals.

4. (Already) disappearing alternatives to Big Insurance

The ACA marketplaces aren’t just a safety net for individuals but also home to smaller non-profit and regional health plans that give Americans an alternative to the “Big 7” Wall Street-run insurance conglomerates. These community-rooted plans are already facing financial headwinds from shrinking enrollment and Medicaid funding cuts. When premiums spike in 2026, many could lose enough members to be forced out of the market entirely.

And here’s the real danger: The Big 7 can weather this storm. Their huge market capitalizations, government contracts, pharmacy benefit manager (PBM) divisions and sprawling care delivery businesses give them insulation from ACA marketplace losses. In fact, they may see this as an opportunity to buy up the smaller competitors that fail, which would further consolidate their dominance over our health care system. Or they could just decide to flee the ACA marketplace entirely because the population will skewer sicker and older, creating a death spiral that the big insurers will not want to touch. What little consumer choice exists outside the big corporate insurers could vanish, and even that could disappear.

5. <65 year olds

Perhaps the most vulnerable group will be Americans in their 50s and early 60s who lose their jobs or retire early (often not by choice) and find themselves too young for Medicare but facing incredibly high premiums on the individual market. Under ACA rules, insurers can charge older enrollees up to three times more than younger adults for the same coverage. The enhanced subsidies have been the only thing keeping many of these premiums within reach.

Take those subsidies away, and a 60-year-old who loses employer coverage could see their monthly premium shoot into four figures. For those living off severance, savings or reduced income, choosing to gamble with their health and wait it out until 65 may be the only option.

Congress knows the stakes. Will they act?

Making the subsidies permanent would cost $383 billion over 10 years, which would be a political hurdle for a Congress intent on deep budget cuts. But the cost of inaction is far higher, both in human and economic terms. These subsidies have kept coverage affordable for millions, fueled small business growth, and stabilized state health systems during one of the most turbulent economic periods in recent memory. Without them, the hit to many folks could be a Frazier-level K.O.

But let’s face it — what I’m advocating for isn’t perfect either. The prospect of extending these subsidies raises a question: Should taxpayers be footing the bill for health insurance premiums when insurance corporations are reporting tens of billions in annual profits and paying hefty dividends to shareholders?

The short answer, for now, unfortunately, is yes. Because this is the deck we’ve been dealt and we can’t let Americans fall into medical debt, lose their homes – or their lives. Extending the ACA subsidies is not pretty. But for Americans, it’s just a bob and weave.