The Supreme Court has upheld the constitutionality of the Affordable Care Act in a decision released this morning.

The Republican state plaintiffs, led by Texas, have failed to show they have standing to attack as unconstitutional the ACA’s minimum essential coverage provision, the justices said.

“Therefore, we reverse the Fifth Circuit’s judgment in respect to standing, vacate the judgment, and remand the case with instructions to dismiss,” they said.

Justice Stephen Breyer delivered the majority opinion, in which Chief Justice John Roberts and Justices Clarence Thomas, Sonia Sotomayor, Elena Kagan, Brett Kavanaugh and Amy Coney Barrett joined.

Justice Samuel Alito filed the dissenting opinion in which Judge Neil Gorsuch joined.

In the past year, cost was a bigger factor driving Americans to skip recommended healthcare than fear of contracting COVID-19, according to a report released June 1 by Patientco, a revenue cycle management company focusing on patient payment technology.

Patientco surveyed 3,116 patients and 46 healthcare providers, finding 34 percent of female patients and 30 percent of male patients have avoided care in the past year citing concerns about out-of-pocket costs.

Below are three more notable findings from the report:

Healthcare affordability is not an issue that affects only Americans with low incomes, as 85 percent of patients with household incomes greater than $175,000 are less likely to defer care when flexible payment options are offered.

Across all ages, income levels and education levels, most patients said they struggled to understand their medical bills and what they owed. Nearly two-thirds of patients said they did not understand their explanation of benefits, did not know what they should do with the information in their explanation of benefits, or waited too long to obtain their explanation of benefits.

Forty-five percent of patients said they would need financial assistance for medical bills that exceed $500, and 66 percent of patients said the same for medical bills that exceed $1,000.

The U.S. Supreme Court is heading into the last month of its current term with one major healthcare case, the move to invalidate the ACA, yet to be decided, The New York Times reported June 1.

A coalition of Republican-leaning states, led by Texas, have asked the court to strike down the ACA, signed into law in 2010. The states argue that the entire ACA is invalid because, in December 2017, Congress eliminated the law’s tax penalty for failing to purchase health insurance. The states argue that the individual mandate requiring Americans to gain health insurance or pay a penalty is inseparable from the rest of the law and became unconstitutional when the tax penalty was eliminated.

The Supreme Court heard oral arguments in the case in November, and at least five Supreme Court justices indicated support for not striking down the entire ACA.

The court is expected to rule on the matter before its nine-month term ends at the end of June, Reuters reported.

President Biden released his budget proposal for fiscal year 2022 on Friday, clocking in at a whopping $6T of federal spending on programs aimed at making sweeping investments in infrastructure, education, and social services, and banking on hefty government borrowing at low interest rates to fuel a major overhaul of the American economy.

The proposal includes big increases in discretionary spending, including raising funding for the Department of Health and Human Services (HHS) by 23.4 percent, to $133.7B, the largest increase in almost two decades. The budget bolsters funding for a variety of healthcare programs, but notably includes specifics on only two major increases in mandatory healthcare spending: making permanent the temporary subsidy increases for individual coverage that are part of the American Rescue Plan Act ($163B); and expanding home- and community-based services in Medicaid ($400B). Both of those proposals were announced earlier this year as part of Biden’s twin recovery packages for infrastructure and social programs.

Notably absent, apart from statements of general support, are any details for implementing a “public option” health plan, or for lowering the Medicare eligibility age to 60—two healthcare proposals that figured prominently in Biden’s campaign platform. Nor are there specifics on lowering spending on prescription drugs, another key area of interest among lawmakers. Like all presidential budgets, the Biden document is simply a statement of priorities, providing a starting point for negotiations in Congress.

But the relatively narrow scope of the healthcare proposals—as hefty as their price tags are—indicates that the White House is likely not willing to throw down over a major overhaul of coverage, at least while Congress is so closely divided. While there are bills afloat in both the House and Senate to more aggressively expand coverage, we’d expect this summer’s legislative horse-trading to result in something resembling what’s in the President’s budget—and not much more.

“Medicare at 60” and a national public option are likely on hold, at least until after the 2022 midterm elections.

Average benchmark premiums for plans on the Affordable Care Act’s exchanges have fallen for the third straight year, according to a new analysis.

Researchers at the Urban Institute, a left-leaning think tank, found that the average benchmark premium on the exchanges fell by 1.7% for 2021. That follows decreases of 1.2% in 2019 and 3.2% in 2020.

By contrast, premiums for employer-sponsored plans increased by 4% in both 2019 and 2020, according to the report. Data for 2021 on the employer market are not yet available, the researchers said.

The national average benchmark premium was $443 per month for a 40-year-old nonsmoker, according to the report, before accounting for any tax credits.

The researchers found much significant variation in premium levels between states, though the difference in growth rates was smaller. Minnesota reported the lowest average benchmark premium at $292 per month, and the highest was in Wisconsin at $782 per month.

Average benchmark premiums topped $500 in 10 states, according to the report.

One of the key trends that’s slowing premium growth is increasing competition in the exchanges, as many insurers are expanding their offerings or returning to the marketplaces to offer plans, according to the report.

“New entrants included national and regional insurers, Medicaid insurers, and small start-up insurers,” the researchers wrote.

“Medicaid insurers are those who operated exclusively in the Medicaid managed-care market before 2014; they have increased their participation in the Marketplaces over time. Medicaid insurers are experienced in establishing narrow, low-cost provider networks that allow them to offer lower premiums than other insurers.”

UnitedHealthcare, for example, participated in just four regions included in the study in 2017, but had upped its participation to 11 for 2021. Aetna participated in three regions included in the study in 2017 before fully exiting the exchanges; CVS Health CEO Karen Lynch told investors earlier this year that the insurer plans to return to the marketplaces in 2022.

Several states have also launched programs that aim to lower premiums, according to the report. These include reinsurance programs, which have been rolled out in 12 states as of this year. Some states have also expanded Medicaid in recent years, which leads to some low-income people with costly health needs switching to that program, the researchers said.

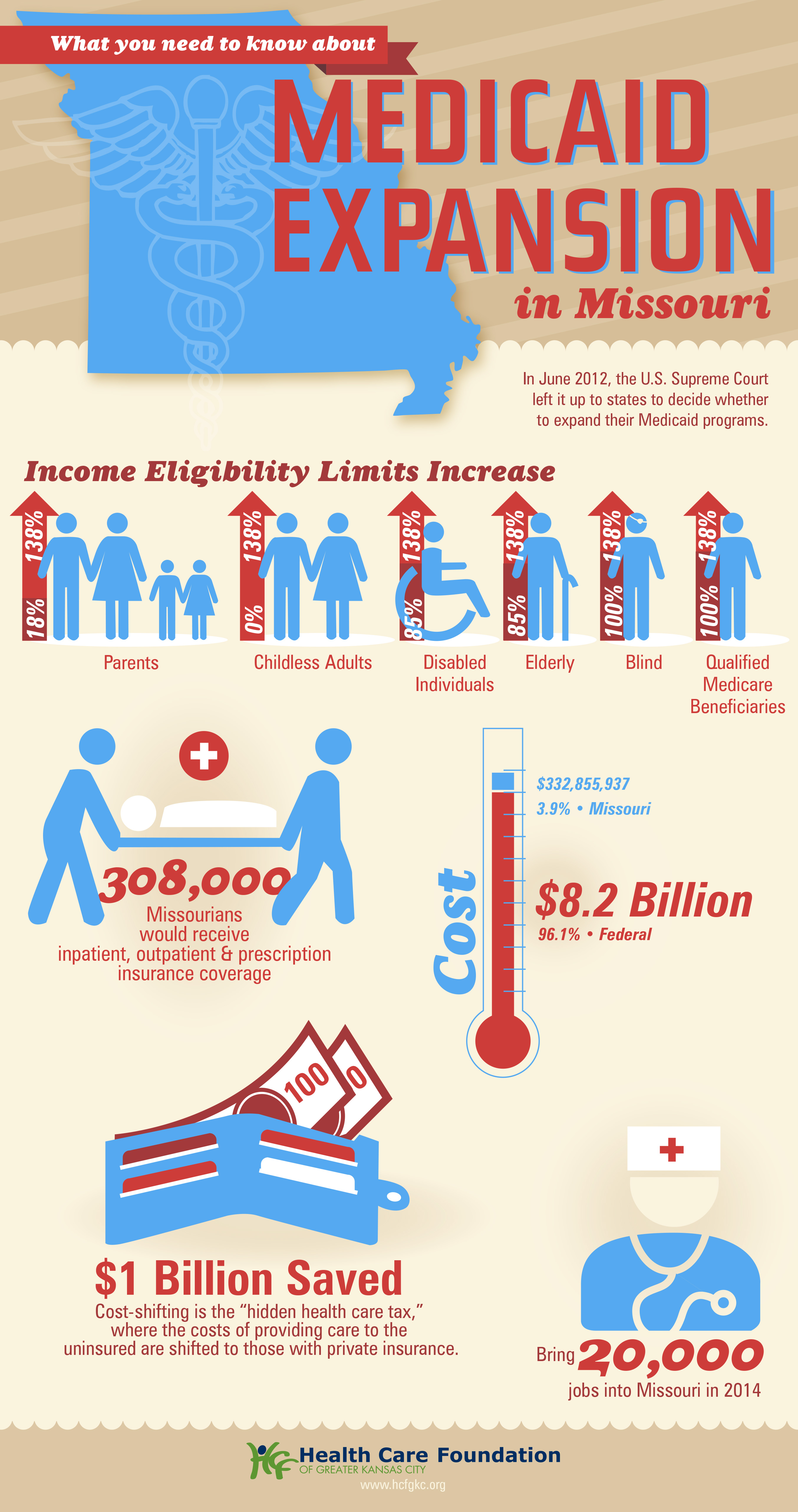

Missouri Gov. Mike Parson announced Thursday that his state would not expand Medicaid coverage to 275,000 residents who will become eligible on July 1st, despite a 2020 ballot initiative in which a majority of the state’s voters approved the expansion. Because the Missouri legislature has blocked funding for the expansion, Parson declared that the state’s Medicaid program, MO HealthNet, would run out of money if it moved forward.

The legislature’s decision to block funding was bolstered by an appeals court opinion last year, which challenged the expansion because the ballot initiative did not include a funding mechanism for widening coverage.

Under the Affordable Care Act (ACA), the federal government would have picked up 90 percent of the cost of expanding Medicaid in the state, in addition to boosting funding for existing Medicaid enrollees by 5 percent, thanks to a measure in the recent American Rescue Plan Act.

The governor’s decision leaves in place one of the strictest Medicaid eligibility standards in the nation: a family of three in Missouri must earn less than 21 percent of the federal poverty level—$5,400 per year—in order to qualify for coverage. The expansion measure would have opened the program to childless adults, and raised the eligibility limit to 138 percent of the federal poverty level.

The Missouri Hospital Association called the decision an “affront” to voters, pointing out that the state is currently running a budget surplus, and could easily allocate funds for the expansion. The status of Medicaid expansion in Missouri, which would become the 38th state to undertake expansion since the ACA’s passage, will ultimately be decided by court ruling, according to observers.

Meanwhile, like other states (mostly in the Southeast) that have resisted Medicaid expansion,Missouri will continue to see tax dollars flow out of the state to fund benefits in states that have expanded eligibility—despite the express will of voters. Given ample evidence that Medicaid expansion boosts access to care, health status, and health system sustainability,it’s nearly unfathomable that the politics of “Obamacare” continue to complicate the extension of this critical safety-net program.

We’ve closely tracked Colorado’s pursuit of its own public option insurance plan, which seems now to have reached a compromise that will allow a bill to move forward, according to reporting from Colorado Public Radio. The saga began two years ago when state legislators passed a law requiring Democratic Governor Jared Polis’ administration to develop a public option proposal. Amid the pandemic and broad industry opposition, progress stalled last year on the proposal. Lawmakers picked up the proposal this session, and have made progress on a compromise bill now poised to pass the state’s Democratic legislature.

Unlike the earlier version, the new legislation would not lay the groundwork for a government-run insurance option, but rather would force insurers to offer a plan in which the benefits and premiums are defined and regulated by the state. The bill would also allow the state to regulate how much hospitals and doctors are paid.

In the current version,hospital reimbursement is set at a minimum of 155 percent of Medicare rates, and premiums are expected to be 18 percent lower than the current average. While state Republicans and some progressive Democrats are still opposed, the Colorado Hospital Association and State Association of Health Plans are neutral on the bill, largely eliminating industry opposition.

The role hospitals played in fighting the pandemic surely paved the way toward the compromise bill, which is viewed as much more friendly to providers than the previous proposal.With the Biden administration unlikely to pursue Medicare expansion or a national public option, we expect more Democratic-run states to pursue these sorts of state-level efforts to expand coverage.

In the wake of the pandemic, providers are well-positioned to negotiate—and should use the goodwill they’ve generated to explore more favorable terms, rather than resorting to their usual knee-jerk opposition to these kinds of proposals.