Last week was notable for healthcare because current events thrust it into the limelight…

Hospitals and emergency responders in Maine: Media attention to Gaza and the Speaker-less U.S. House of Representatives was temporarily suspended as the deaths of 18 in the U.S.’ 36h mass shooting in Lewiston, Maine took center stage. The immediate overload on Lewiston’s Central Maine Medical Center and Mass General where the 13 injured were treated (including 4 still hospitalized) drew media attention—largely gone by Friday when the shooter’s death by suicide was confirmed.

The New Speaker of the House: The GOP House of Representatives elected Mike Johnson, the 4-term Representative from Shreveport to the post vacant since October 3.

Johnson is no stranger to partisan positions on healthcare issues. As Chairman of the conservative-leaning Republican Steering Committee from 2019-2021, he led the group’s platform to dismantle the Affordable Care Act and supports a national restriction on abortions despite Senate GOP Leader McConnell’s preference it be left to states to decide.

With the prospect of a government shutdown November 17 due to inaction on the FY2024 federal budget, the 52-year-old lawyer faces delicate maneuvering around $106 billion proposed for Israel, the Ukraine, Taiwan and border security alongside appropriations for the health system that consumes 28% of entire federal outlays.

Health organizational business strategy announcements: Friction between physicians and hospital officials in Asheville (Mission) and Minnesota (Allina) attracted national coverage and brought attention to staffing, cultural and financial circumstances in these prominent organizations. —and on the heels of the Kaiser Permanente strike settlement. The divorce from Mass General by Dana Farber in Boston and announcements by GNC, Best Buy, Optum (re-branding NaviHealth) and Sanofi hit last week’s news cycle.

And indirectly, the 3Q 2023 GDP report by the Department of Commerce raised eyebrows: it was up 4.9%–far higher than expected prompting speculation that the Federal Open Market Committee (FOMC) will raise interest rates (again) at its meeting this week or next month. That means borrowing costs for struggling hospitals, nursing homes and consumers needing loans will go up along with household medical debt.

As news cycles go, this one was standard fare for healthcare: with the exception of business plan announcements by organizations or as elements of tragedies like Lewiston, Gaza or a pandemic,

the business of the health system—how it operates is largely uncovered and often subject to misinformation or disinformation.

That’s the problem: it’s background noise to most voters who can be stoked to action over a single issue when prompted by special interests (i.e., Abortion rights, surprise billing, price transparency et al) but remain inattentive and marginally informed about the bigger role it plays in our communities and country and where it’s heading long-term.

The narrative common to most boils down to these:

The U.S. health system is good, but it’s complicated. ‘How good’ depends on your insurance and your health—both are key.

The U.S. health system is expensive and profitable. It pays its executives well and its frontline workers unfairly.

The delivery system focuses on the sick and injured; prevention and public health matter less.

Hospitals and physicians are vital to the system; health insurers keep their costs down.

The U.S. system pays lip service to “customer service” and ‘engaged consumers.” It is spin not supported by actions.

The U.S. system needs to change dramatically.

In the next 3 weeks, attention will be on the federal budget: healthcare will be in the background unless temporarily an element of a mass tragedy. Each trade group will tout its accomplishments to regulators and pimp their advocacy punch list. Each company will gin-out news releases and commentary about the future of the system will default to think tanks and focused on a single issue of interest.

That’s the problem. In this era of social media, polarization, and mass transparency, these old ways of communicating no longer work. Left unattended, they undermine the value proposition on which the U.S. system is based.

Six individuals and the owners of two small businesses sued the federal government, arguing that the ACA provision “makes it impossible” for them to purchase health insurance for themselves or their employees that excludes free preventive care. The plaintiffs argue that they do not want or need such care. They specifically name the medication PrEP (used to prevent the spread of HIV), contraception, the HPV vaccine, and screening and behavioral counseling for sexually transmitted diseases and substance use; however, they seek to invalidate the entire ACA preventive benefit package.

A federal trial court judge agreed with some of their claims and invalidated free coverage of more than 50 services, including lung, breast, and colon cancer screenings and statins to prevent heart disease.

This ruling, which is currently being appealed, strips free preventive services coverage from more than 150 million privately insured people and approximately 20 million Medicaid beneficiaries who are covered under the ACA’s Medicaid expansion.

This suit was first filed in 2020. The plaintiffs in the case, Braidwood Management v. Becerra, continue to oppose the entire preventive benefit package, which consists of four service bundles: services rated “A” or “B” by the United States Preventive Services Task Force (USPSTF); routine immunizations recommended by the Advisory Committee on Immunization Practices (ACIP); evidence-informed services for children recommended by the Health Resources and Services Administration (HRSA); and evidence-informed women’s health care recommended by HRSA. The trial judge invalidated all benefits recommended by the USPSTF after March 23, 2010, the date the ACA became law. (The court also exempted the plaintiffs on religious grounds from their obligation to cover PrEP.) The Fifth Circuit put the trial court’s decision on temporary hold while the case is on appeal.

The Fifth Circuit, one of the nation’s most conservative appeals courts, will hear the Biden administration’s appeal of the trial court’s USPSTF ruling and the entirety of the plaintiffs’ original challenge, thereby putting all four coverage guarantees in play. The court also will hear whether the ruling should apply only to the plaintiffs or to all Americans.

The trial court held that the USPSTF lacks the legal status necessary under the Constitution to make binding coverage decisions, and that the Secretary of the U.S. Department of Health and Human Services (HHS) — who can make such binding decisions — lacks the power to rectify matters by formally adopting USPSTF recommendations. The judge concluded that federal law fails to require that members be presidential nominees confirmed by the Senate under the Appointments Clause; in the judge’s view, this means that members are not politically accountable for their decisions, which is constitutionally problematic. The judge also ruled that federal law makes the USPSTF the final coverage arbiter, which means that the HHS Secretary, who is nominated and confirmed under the Appointments Clause and thus politically accountable, cannot cure the constitutional problem by ratifying USPSTF recommendations.

On appeal, the Biden administration argues that the USPSTF passes constitutional muster because the HHS Secretary, who oversees the Task Force, is a nominated and confirmed constitutional officer. Alternatively, the administration argues the appeals court should interpret the statute as allowing the HHS Secretary to ratify USPSTF recommendations, since the law specifies that USPSTF members are independent of political pressure only “to the extent practicable.” The administration makes similar arguments on behalf of ACIP and HRSA.

The plaintiffs argue that secretarial ratification cannot cure the constitutional problems with all three advisory bodies. According to the plaintiffs, none of the advisory bodies has the status of constitutional officers demanded by the Appointments Clause, and so their recommendations must remain recommendations only, unenforceable by HHS on insurers, health plans, and state Medicaid programs.

The second issue is the scope of the remedy if the law is found unconstitutional. The trial court did not limit its holding to the four individual plaintiffs and two companies who sued, but instead applied its order nationwide. The Biden administration argues that, if the coverage guarantee is unconstitutional, the court only should prohibit HHS from enforcing the preventive services provision against the plaintiffs who brought the lawsuit and should allow the coverage guarantee to remain in force for the rest of the country. Citing an amicus brief filed by the American Public Health Association and public health deans and scholars, the administration argues that barring HHS from enforcing the preventive services requirement nationwide “pose[s] a grave threat to the public health” by decreasing Americans’ access to lifesaving preventive services. The plaintiffs argue that a nationwide prohibition is necessary, the broader public interest in free preventive coverage is irrelevant, and insurers will voluntarily continue to offer free preventive coverage if people want it.

The administration’s arguments on appeal have attracted amicus briefs by bipartisan economic scholars, organizations concerned with health equity and preventive health, health care organizations, and 23 states.

Crucially, the economists point out that, prior to the ACA, comprehensive free preventive coverage was extremely limited because it is not in insurers’ interest to make a long-term economic investment in members’ health. Indeed, prior to the ACA, insurers did not even uniformly cover the basic screenings for newborns to detect treatable illnesses and conditions.

Amicus briefs supporting the plaintiffs have been filed by Texas and an organization dedicated to “protecting individual liberties . . . against government overreach.” All briefing will be complete by November 3, 2023, with oral argument thereafter. A decision is likely in early to mid-2024. Whatever the outcome, expect a Supreme Court appeal given the size of the stakes in the case.

Late last week, the Congressional Budget Office (CBO) released its analysis of the Center for Medicare and Medicaid Innovation (CMMI)’s spending outlays, revealing that in its first decade of operations it produced a $5.4B net increase in federal spending instead of a projected $2.8B reduction.

Moreover, CBO revised its CMMI projection for 2021-2030 from a $77.5B net spending reduction to a $1.3B increase, predicting CMMI may only begin to generate annual savings in 2031. CBO says its updated projections largely reflect revised expectations on CMMI’s ability to identify and scale models that actually reduce Medicare spending.

CMMI was created by the Affordable Care Act (ACA) in 2010 to test new payment models and other initiatives for reducing the federal government’s healthcare costs, but of the nearly 50 models it has run, only four have become permanent programs.

The Gist: This critical report confirms what many in the healthcare world already believed: the ACA’s value-based care initiatives have largely struggled to reduce Medicare spending.

There are plenty of policy factors to blame, including the lack of mandatory participation for providers and conflicting incentives across care models, but one factor left out of the CBO report is CMMI’s disproportionate emphasis on accountable care organizations (ACOs) to produce meaningful cost savings, even as years of data proved otherwise.

ACOs are designed to reduce spending primarily through utilization management, but research has shown that prices, not utilization, are responsible for the US’s high medical spend relative to other countries.

While CMMI’s mission is still laudable and important, the center must make good on its 2021 “strategic refresh” if it hopes to continue receiving Congressional support.

Short-term, limited-duration insurance (STLDI) plans are exempt from the Affordable Care Act’s (ACA) essential benefit coverage requirements and from prohibitions on medical underwriting.

This means that consumers with preexisting conditions can be denied coverage and anyone who purchases such a plan may lack coverage for key services.

In August 2018, under the Trump administration, the U.S. Department of Health and Human Services revised the definition of short-term plans to include coverage with an initial term of less than 12 months that could be renewed for up to 36 months. While the purported goal of this change was to increase coverage and reduce uninsured rates, our analysis indicates that it did not accomplish this: coverage did not increase and the uninsured rate did not drop.

In July 2023, the Biden administration issued a notice to limit the initial duration of short-term plans to three months, with an option to renew for one additional month. This change was intended to ensure that people purchasing insurance coverage have meaningful protection and to preserve the preexisting condition protections in the ACA.

In 2019, the Congressional Budget Office (CBO), using its forecast model (data were not yet available), estimated that 1.5 million people would purchase short-term plans and that 500,000 would gain coverage (relative to being uninsured). Our analysis suggests that these forecasts substantially overstated the effects of the rule change; far fewer people enrolled in STLDI plans and the enrollment that did occur was from people moving off marketplace coverage.

There is no evidence that the number of uninsured people declined because these plans became available.

Using data from the American Community Survey and marketplace enrollment from the Centers for Medicare and Medicaid Services (CMS), we assessed whether the loosening of STLDI regulations (under the Trump administration) led to increased enrollment in off-marketplace nongroup coverage in states that permitted sales compared to those that did not. Plans sold off the marketplace include STLDI as well as ACA-compliant plans, grandfathered coverage, health care sharing ministries, and fixed indemnity plans. Next, we looked to see whether the Trump-era regulations increased nongroup insurance coverage altogether (including marketplace coverage) in these states. Finally, we looked to see whether the broader availability of STLDI was associated with lower uninsured rates. We examined coverage patterns for adults ages 26 to 64 and then focused on young men ages 26 to 35, who may be most sensitive to the presence of regulations similar to those in the ACA because they are less likely to have preexisting conditions or to seek comprehensive coverage.

In 2017, 2.6 million adults ages 26 to 64, about 1.6 percent of that population, purchased private nongroup insurance outside the marketplace. By 2020, about 270,000 more people were enrolled in off-marketplace nongroup plans, across all states, than had been in 2017. There was a larger increase in off-marketplace nongroup enrollment among all adults and among young adults (we cannot separate young men in the CMS data) in states that permitted the sale of STLDI coverage, compared to those that prohibited it. This is consistent with the evidence of growth in sales of these plans. Across all states, about 160,000 more young adults, ages 26 to 34, held off-marketplace nongroup coverage in 2020 than in 2017.

The ACS data show that off-marketplace plans largely substituted for marketplace plans in states that permitted the sale of STLDI. Patterns of enrollment in nongroup plans overall were very similar in states with and without STLDI plans available for purchase over this period. While nongroup coverage was consistently more popular in states with no restrictions, between 2017 and 2020 enrollment in nongroup plans declined slightly more in states where STLDI plans were available for purchase than in those where they were not. The same pattern of marginally greater declines held for young men (and young adults) in states where STLDI plans were available.

Nongroup coverage was slightly higher in states where STLDI plans were available for sale, but the overall uninsured rate is much higher in these states, primarily because many did not expand Medicaid eligibility.

The gap in uninsured rates between states with STLDI plans available and those in which they were not available widened through 2018, narrowed slightly in 2019, and rose again in 2020. Patterns among young men were similar.

The lack of reliable information on STLDI plans and the small size of the market make it difficult to draw strong inferences about how changes in regulations affected participation. Nonetheless, by comparing states where the 2018 regulatory changes took effect and those where they did not, we are able to rule out any notable effects. A modest number of people — no more than one-fifth of the 1.5 million the CBO projected — are likely to have enrolled in STLDI plans that became available after the Trump administration’s regulatory change. This enrollment mainly appears to have displaced marketplace coverage.

There is no evidence that the broader availability of STLDI plans had any meaningful effect on nongroup coverage in general or on uninsurance, either in the full population or among young men.

This suggests that the Biden administration’s proposed tightening of STLDI is unlikely to have substantial negative effects on nongroup coverage or uninsurance. Instead, limiting STLDI will likely strengthen the health insurance marketplaces that offer reliable, comprehensive nongroup coverage.

Were you better off in 2022 than you were in 2017? I was for a lot of reasons. One thing that didn’t change over those five years, though, was my health insurance status. I had health insurance in 2017, and I had health insurance in 2022. And I still have health insurance today.

So do most Americans. In fact, according to the U.S. Census Bureau’s latest report on health insurance coverage in the U.S., 92.1% of us had some form of health insurance in 2022. That’s about 304 million people, per the report.

Conversely, 7.9% of us were uninsured last year. That’s a little more than 25.9 million people. That’s down from 8.3% and about 27.2 million people in 2021.

Some may see the decrease in both the percentage and number of uninsured as good news. And it is. Any time the uninsured figures go down, that’s good.

The bad news is, we’re back where we were in 2017. That’s also when 7.9% of us, or about 25.6 million people, were uninsured. Five years of trying to get more people insured and nothing to show for it.

The number of people with any type of private health insurance (employer-based or direct-purchase) crept up to 216.5 million last year from 216.4 million in 2021. The number of people with any type of public health insurance (Medicare, Medicaid, etc.) rose to 119.1 million last year from 117.1 million in 2021. Both headed in the right direction but too slow to push the uninsured rate significantly down.

If we want to get serious about achieving universal coverage, let’s get serious about it. If we don’t want to get serious about it because most of us already have health insurance, the only useful purpose of the Census Bureau’s annual reports on health insurance is to show us how little we really care.

It feels as though November 5, 2024 is far away, but for both Democrats and Republicans, the election is now. On the issue of healthcare, the two parties’ approaches differ sharply.

Think back to the behemoth effort by Republicans to “repeal and replace” the Affordable Care Act six years ago, an effort that left them floundering for a replacement, basically empty-handed. Recall the 2022 midterms, when their candidates in 10 of the tightest House and Senate races uttered hardly a peep about healthcare.

That reticence stood in sharp contrast to Democrats who weren’t shy about reiterating their support for abortion rights, simultaneously trying hard to ensure that Americans understood and applauded healthcare tenets in the Inflation Reduction Act.

As The Hill noted in early August, sounds like the same thing is happening this time around as America barrels toward November 2024. The publication said it reached to 10 of the leading Republican candidates about their plans to reduce healthcare costs and make healthcare more affordable, and only one responded: Rep. Will Hurd (R-Texas).

Healthcare ‘A Very Big Problem’

Maybe the party thinks its supporters don’t care. But, a Pew Research poll from June showed 64% of us think healthcare affordability is a “very big problem,” superseded only by inflation. In that research, 73% of Democrats and 54% of Republicans thought so.

Chuck Coughlin, president and CEO of HighGround, an Arizona-based public affairs firm, told The Hill that the results aren’t surprising.

“If you’re a Republican, what are you going to talk about on healthcare?” he said.

Observers note that the party has homed in on COVID-lockdowns, transgender medical rights, and yes, abortion.

Plans won’t offer coverage for preexisting conditions, maternity care, or prescription drugs, and they can set limits on coverage. The plans will make it easier for small employers to self-insure, so they don’t have to adhere to ACA or state insurance rules.

CHOICE would let large groups come together to buy Association Health Plans, said NPR, which noted that in the past, there have been “issues” with these types of plans.

Insurance experts say that the act takes a swing at the very foundation of the ACA. As one analyst described it, the act intends to improve America’s healthcare “through increased reliance on the free market and decreased reliance on the federal government.”

Democrats Tout Reduce-Price Prescriptions

Meanwhile, on Aug. 29, President Joe Biden spoke proudly in The White House: “Folks, there’s a lot of really great Republicans out there. And I mean that sincerely…But we’ll stand up to the MAGA Republicans who have been trying for years to get rid of the Affordable Care Act and deny tens of millions of Americans access to quality, affordable healthcare.” Current ACA enrollment is higher than 16 million.

He said that Big Pharma charges Americans more than three times what other countries charge for medications. And on that date, he announced that “the (Inflation Reduction Act) law finally gave Medicare the power to negotiate lower prescription drug prices.” He wasn’t shy about saying that this happened without help from “the other team.”

The New York Times said it feels this push for lower healthcare costs will be the centerpiece of his re-election campaign. The announcement confirmed that his administration will negotiate to lower prices on 10 popular—and expensive drugs—that treat common chronic illnesses.

It said previous research shows that as many as 80% of Americans want the government to have the power to negotiate.

The president also said that “Next year, Medicare will select more drugs for negotiation.” He added that his administration “is cracking down on junk health insurance plans that look like they’re inexpensive but too often stick consumers with big hidden fees.” And it’s tackling the extensive problem of surprise medical bills.

Earlier, on August 11, Biden and fellow Democrats celebrated the first anniversary of the PACT Act, legislation that provides healthcare to veterans exposed to toxic burn pits while serving. He said more than 300,000 veterans and families have received these services, with more than 4 million screened for toxic exposure conditions.

Push for High-Deductible Plans

Republicans want to reduce risk of high-deductible plans and make them more desirable—that responsibility is on insurers. According to Politico, these plans count more than 60 million people as members, and feature low premiums and tax advantages. The party said plans will also help lower inflation when people think twice about seeking unneeded care.

The plans’ low monthly premiums offer comprehensive preventive care coverage: physicals, vaccinations, mammograms, and colonoscopies, and have no co-payments, Politico said. The “but” in all this is that members will pay their insurers’ negotiated rate when they’re sick, and for medicines and surgeries. Minimum deductible is $1,500 or $3,000 for families—and can be even higher.

Members can fund health savings accounts but can’t fund flexible spending accounts. Proponents cite more access to care, and reduced costs due to promotion of preventive care. Nay-sayers worry about lower-income members facing costly bills due to insufficient coverage.

Republican Candidates Diverge on Medicaid

The American Hospital Association (AHA) doesn’t love these high deductible plans. It explained that members “find they can’t manage the gap between what their insurance pays and what they themselves owe as a result,” and that, AHA said, contributes to medical debt—something the association wants to change.

An Aug. 3 Opinion in JAMA Health Forum pointed out other ways the two parties diverge on healthcare. For example, the piece cited Biden’s incentives for Medicaid expansion. In contrast, Florida Governor Ron DeSantis, a Republican presidential candidate, has not worked to offer Medicaid to all lower-income residents under the ACA. Former Governor Nikki Haley of South Carolina feels the same, doing nothing. However, former New Jersey Governor Chris Christie has expanded it, as did former Vice President Mike Pence, when he governed Indiana.

Undoubtedly, as in presidential elections past, healthcare will be at least a talking point, with Democrats likely continuing to make it a central focus, as before.

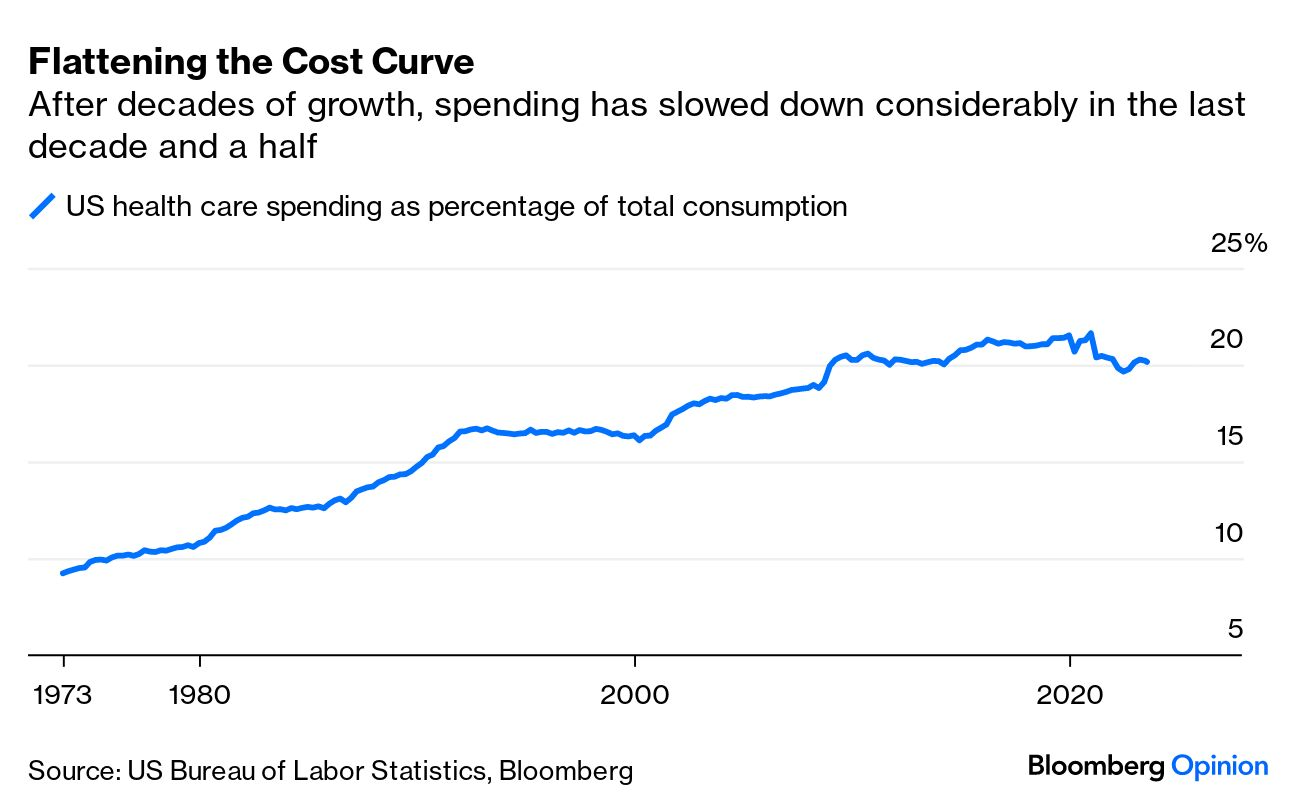

A piece published this week in the New York Times documents how Medicare spending per beneficiary has flattened since the early 2010s, coming in below projections by nearly $4T.

While the authors run through possible explanations, including changes made by the Affordable Care Act and to the Medicare Advantage program, the proliferation of effective cholesterol and blood-pressure medications, and fewer breakthroughs in new, expensive drug classes, they acknowledge that scholars have not reached a consensus on the primary drivers of this trend.

Beyond academic debate, there is also no agreement on how long the flattened spending pattern will hold—or what factors might reignite rapid cost growth.

The Gist:

Whatever the causes of this phenomenon, it has helped avert the kind of Medicare austerity measures that dominated political debates on the program in past decades.

We assume some of this flattening has to do with the fact that the average age of Medicare beneficiaries has dropped as Baby Boomers have entered the program in droves, given that younger beneficiaries are much less costly to insure.

In coming decades, the average age of Medicare beneficiaries will increase, along with their care costs, and the total number of Medicare beneficiaries will continue to rise.

By 2053, seniors will make up over 22 percent of the population and over 40 percent of the projected federal budget will be spent on programs for them.

The GOP Presidential debate marked the unofficial start of the 2024 Presidential campaign. With the exception of continued funding for Ukraine, style points won over issue distinctions as each of the 8 White House aspirants sought to make the cut to the next debate September 27 at the Reagan Library in Simi Valley, CA.

For the candidates in Milwaukee, it’s about “Stayin’ Alive” per the BeeGee’s hit song: that means avoiding self-inflicted harm while privately raising money to keep their campaigns afloat. And, based on Debate One, with the exception of abortion, that means they’ll not face questions about their positions on the litany of issues that dominate healthcare these days i.e., drug prices, hospital consolidation, price transparency, workforce burnout and many others. In Milwaukee, healthcare was essentially ‘out of sight our of mind’ to the moderators and debaters despite being 18% of the U.S. economy and its biggest employer.

For now, each will enlist ghostwriters to produce position papers for their websites, and, on occasion, reporters will press for specifics to test their grasp on a topic but that’s about it. Based on last Wednesday’s 2-hour event, it’s unlikely general media outlets like Fox News (which also hosts Debate Two) will explore healthcare issues except for abortion.

That means healthcare will be subordinated to the economy, inflation, immigration and crime—the top issues to GOP voters—for most of the Presidential primary season.

Next November, voters will also elect 34 US Senators, 435 members of the House of Representatives, 11 Governors and their representatives in 85 state legislative bodies. This will be the first election cycle after reapportionment of votes in the United States Electoral College following the 2020 United States census. Swing states (WI, MI, PA, NV, AZ, GA, FL, OH, CO, VA) will again be keys to the Presidential results since demographics and population shifts have increased the concentrations of each party’s core voters in so-called Blue States and Red States:

The Democratic voter core is diverse, educated and culturally liberal with its strongest appeal to African-Americans, Latinos, women, educated professionals and urban voters. Blue States are predominantly in the Northeast, Upper Midwest and West Coast regions.

The Republican voter core consists of rural white voters, evangelicals, the elderly, and non-college educated adults. Red States are predominantly in the South and Southwest.

The increased concentrations of Blue or Red voters in certain states and regions has contributed to political polarization in the U.S. electorate and presents an unusual challenge to healthcare. Per Gallup: “Political polarization since 2003 has increased most significantly on issues related to federal government power, global warming and the environment, education, abortion, foreign trade, immigration, gun laws, the government’s role in providing healthcare, and income tax fairness. Increased polarization has been less evident on certain moral issues and satisfaction with the state of race relations.”

Thus, healthcare issues are increasingly subject to hyper partisanship and often misinformation.

Given the limited knowledge voters have on most health issues and growing prevalence of social media fueled misinformation, political polarization creates echo chambers in healthcare—one that thinks the system works for those who can afford it and another that thinks that’s wrong.

It’s dicey for politicians: it’s political malpractice to offer specific solutions on anything, especially healthcare. It’s safer to attack its biggest vulnerabilities—affordability and equitable access—even though they mean something different in every echo chamber.

My take:

Barring a second Covid pandemic or global conflict with Russia/China, it’s unlikely healthcare issues will be prominent in Campaign 2024 at the national level except for abortion. At least through the May primary season, here’s the political landscape for healthcare:

Affordability and inequitable access will be the focus of candidate rhetoric at the national level: Trust and confidence in the U.S. health system has eroded. That’s fertile political turf for critics.

In Congress, the fiercest defenders of the status quo have joined efforts to impose restrictions on consolidation and price transparency for hospitals and price controls for prescription drugs. There’s Bipartisan acknowledgement that inequities in accessing care are significant and increasing, especially in minority and low income populations. They differ over the remedy. Employers expect their health costs to increase at least 8% next year and blame hospitals and drug companies for price gauging and want Congress to do more. 85% of Democrats think “the government should insure everyone” vs. 33% of Republican voters which calcifies inaction in a divided Congress though. Opposition to the Affordable Care Act (2010) has softened and Medicaid expansion has passed in 40 Blue and Red states.

In the 2024 election cycle, remedies for increased access and more affordability will pit Republicans calling for more competition, consumerism and transparency and Democrats calling for more government funding, regulation and fairness.

But more important, voter and employer frustration with partisan bickering sans solutions will set the stage for the vigorous debate about a single payer system in 2026 and after,

State elections will give more attention to healthcare issues than the Presidential race: That’s because Governors and state legislators set direction on issues like abortion rights, drug price controls, Medicaid funding, scope of practice allowances and others.

Increasingly, state Attorney’s General and Treasurers are weighing in on consolidation and spending. States referee workforce issues like nurse staffing requirements and others. And ballot referenda on healthcare issues trail only public education as a focus of grassroots voter activity. At the top of that list is abortion rights:

In 25 states and DC, there are no restrictions on access; in 14 states, abortion is banned and in 11 abortions—both procedures and medication—are legal, but with gestational limits from 6 weeks (GA), to between 12 and 22 weeks (AZ, UT, NE, KS, IA, IN, OH, NC, SC, FL). It’s an issue that divides legislators and increasingly delineates Blue and Red states and in many states remains unsettled.

Other healthcare issues, like ageism, will surface in Campaign 2024 in the context of other topics: Finally, healthcare will factor into other issues: Example: The leading Presidential candidates are seniors: President Biden was the oldest person to assume the office at age 78 and would be would be 86 at the end of his second term. Former President Trump was 70 when elected in 2016 and would be 81 if elected when his second term ends.

The majority of Americans are concerned about the impact of age on fitness to serve among aspirants for high office: cognitive impairment, dementia, physical limitations et al. will be necessary talking points in campaigns and media coverage. Similarly, cybersecurity looms as a focus where healthcare’s data-rich dependence is directly impacted. Growing concern about climate and the food supply, sourcing of raw good and materials from China used in drug manufacturing and many other headlines will infer healthcare context.

Summary:

Healthcare will be on the ballot in 2024 and might very well make the difference in who wins and loses in many state and local elections.

It will make a difference in the Presidential campaign as part of the economy and a major focus of government spending. Beyond abortion, the lack of attention to other aspects of the health system in the Milwaukee debate last week should in no way be interpreted as a pass for healthcare insiders.

Voters are restless and healthcare is contributing. Healthcare is far from ‘out of sight, out of mind’ in Campaign 2024.

Five years ago, I started the Fixing Healthcare podcast with the aim of spotlighting the boldest possible solutions—ones that could completely transform our nation’s broken medical system.

But since then, rather than improving, U.S. healthcare has fallen further behind its global peers, notching far more failures than wins.

In that time, the rate of chronic disease has climbed while life expectancy has fallen, dramatically. Nearly half of American adults now struggle to afford healthcare. In addition, a growing mental-health crisis grips our country. Maternal mortality is on the rise. And healthcare disparities are expanding along racial and socioeconomic lines.

Reflecting on why few if any of these recommendations have been implemented, I don’t believe the problem has been a lack of desire to change or the quality of ideas. Rather, the biggest obstacle has been the immense size and scope of the changes proposed.

To overcome the inertia, our nation will need to narrow its ambitions and begin with a few incremental steps that address key failures. Here are three actionable and inexpensive steps that elected officials and healthcare leaders can quickly take to improve our nation’s health:

1. Shore Up Primary Care

Compared to the United States, the world’s most-effective and highest-performing healthcare systems deliver better quality of care at significantly lower costs.

One important difference between us and them: primary care.

In most high-income nations, primary care makes up roughly half of the physician workforce. In the United States, it accounts for less than 30% (with a projected shortage of 48,000 primary care physicians over the next decade).

Primary care—better than any other specialty—simultaneously increases life expectancy while lowering overall medical expenses by (a) screening for and preventing diseases and (b) helping patients with chronic illness avoid the deadliest and most-expensive complications (heart attack, stroke, cancer).

But considering that it takes at least three years after medical school to train a primary care physician, to make a dent in the shortage over the next five years the U.S. government must act immediately:

The first action is to expand resident education for primary care. Congress, which authorizes the funding, would allocate $200 million annually to create 1,000 additional primary-care residency positions each year. The cost would be less than 0.2% of federal spending on healthcare.

The second action requires no additional spending. Instead, the Centers for Medicare & Medicaid Services, which covers the cost of care for roughly half of all American adults, would shift dollars to narrow the $108,000 pay gap between primary care doctors and specialists. This will help attract the best medical students to the specialty.

Together, these actions will bolster primary care and improve the health of millions.

2. Use Technology To Expand Access, Lower Costs

A decade after the passage of the Affordable Care Act, 30 million Americans are without health insurance while tens of millions more are underinsured, limiting access to necessary medical care.

Furthermore, healthcare is expected to become even less affordable for most Americans. Without urgent action, national medical expenditures are projected to rise from $4.3 trillion to $7.2 trillion over the next eight years, and the Medicare trust fund will become insolvent.

With costs soaring, payers (businesses and government) will resist any proposal that expands coverage and, most likely, will look to restrict health benefits as premiums rise.

Almost every industry that has had to overcome similar financial headwinds did so with technology. Healthcare can take a page from this playbook by expanding the use of telemedicine and generative AI.

At the peak of the Covid-19 pandemic, telehealth visits accounted for 69% of all physician appointments as the government waived restrictions on usage. And, contrary to widespread fears at the time, patients and doctors rated the quality, convenience and safety of these virtual visits as excellent. However, with the end of Covid-19, many states are now restricting telemedicine, particularly when clinicians practice in a different state than the patient.

To expand telemedicine use—both for physical and mental health issues—state legislators and regulators will need to loosen restrictions on virtual care. This will increase access for patients and diminish the cost of medical care.

It doesn’t make sense that doctors can provide treatment to people who drive across state lines, but they can’t offer the same care virtually when the individual is at home.

Similarly, physicians who faced a shortage of hospital beds during the pandemic began to treat patients in their homes. As with telemedicine, the excellent quality and convenience of care drew praise from clinicians and patients alike.

Building on that success, doctors could combine wearable devices and generative AI tools like ChatGPT to monitor patients 24/7. Doing so would allow physicians to relocate care—safely and more affordably—from hospitals to people’s homes.

Translating this technology-driven opportunity into standard medical practice will require federal agencies like the FDA, NIH and CDC to encourage pilot projects and facilitate innovative, inexpensive applications of generative AI, rather than restricting their use.

3. Reduce Disparities In Medical Care

American healthcare is a system of haves and have-nots, where your income and race heavily determine the quality of care you receive.

Black patients, in particular, experience poorer outcomes from chronic disease and greater difficulty accessing state-of-the-art treatments. In childbirth, black mothers in the U.S. die at twice the rate of white women, even when data are corrected for insurance and financial status.

Generative AI applications like ChatGPT can help, provided that hospitals and clinicians embrace it for the purpose of providing more inclusive, equitable care.

Previous AI tools were narrow and designed by researchers to mirror how doctors practiced. As a result, when clinicians provided inferior care to Black patients, AI outputs proved equally biased. Now that we understand the problem of implicit human bias, future generations of ChatGPT can help overcome it.

The first step will be for hospitals leaders to connect electronic health record systems to generative AI apps. Then, they will need to prompt the technology to notify clinicians when they provide insufficient care to patients from different racial or socioeconomic backgrounds. Bringing implicit bias to consciousness would save the lives of more Black women and children during delivery and could go a long way toward reversing our nation’s embarrassing maternal mortality rate (along with improving the country’s health overall).

The Next Five Years

Two things are inevitable over the next five years. Both will challenge the practice of medicine like never before and each has the potential to transform American healthcare.

First, generative AI will provide patients with more options and greater control. Faced with the difficulty of finding an available doctor, patients will turn to chatbots for their physical and psychological problems.

Already, AI has been shown to be more accurate in diagnosing medical problems and even more empathetic than clinicians in responding to patient messages. The latest versions of generative AI are not ready to fulfill the most complex clinical roles, but they will be in five years when they are 30-times more powerful and capable.

Second, the retail giants (Amazon, CVS, Walmart) will play an ever-bigger role in care delivery. Each of these retailers has acquired primary care, pharmacy, IT and insurance capability and all appear focused on Medicare Advantage, the capitated option for people over the age of 65. Five years from now, they will be ready to provide the businesses that pay for the medical coverage of over 150 million Americans the same type of prepaid, value-based healthcare that currently isn’t available in nearly all parts of the country.

American healthcare can stop the current slide over the next five years if change begins now. I urge medical leaders and elected officials to lead the process by joining forces and implementing these highly effective, inexpensive approaches to rebuilding primary care, lowering medical costs, improving access and making healthcare more equitable.

Influential conservative policy groups are sketching out health care plans for a potential Republican administration over a year before the election.

Why it matters:

Republicans have moved on from the “repeal and replace” — the Affordable Care Act didn’t even get a mention in the first GOP presidential debate last week — but still haven’t settled on new health care agenda.

Republican-aligned groups are stepping in to build out ideas for a party platform that may not be as ambitious as an ACA replacement but could still shift health care policy in a conservative direction on everything from Medicaid to abortion to public health.

Context:

The early push to define the next GOP health agenda partly stems from Republicans’ inability to agree on an ACA alternative after former President Trump was elected, despite years of promises to overhaul the 2010 health care law. The GOP policy experts also said they want to avoid repeating the Trump administration’s failure to plan health care executive actions and key staffing decisions before taking office.

“A large part of it comes from the experience of 2017. There wasn’t a clear agenda that was ready to go,” said Brian Blase, a former Trump administration health official who’s now president of the right-leaning Paragon Health Institute.

Details:

Conservative think tanks are looking to advance some long-held conservative goals like transforming Medicaid’s open-ended entitlement into block grants, but there’s also a new generation of Trump alumni who hope to revive some of his administration’s policies.

These include initiatives like encouraging businesses to form association health plans, and pushing even further on price transparency and curbing higher payments to hospitals’ outpatient departments.

Some are also drawing up plans for limiting the CDC’s power over public health policy in reaction to what they view as the agency’s failed response to the COVID-19 pandemic.

Zoom in:

Paragon Health, as well as the Heritage Foundation and America First Policy Institute, are the primary conservative think tanks now drafting health regulations, policy plans and recruiting personnel who could serve in a Republican administration.

A roadmap from Paragon envisions a burst of rulemaking at the beginning of a new administration, mostly through the Department of Health and Human Services.

Meanwhile, the America First Policy Institute, founded by Trump administration alumni in 2021, has put forward a 12-part health policy agenda it describes as “radical incrementalism.”

That’s an acknowledgement that they’re not planning a major health care overhaul, but a belief that significant changes are possible in the current structure, said former Louisiana Gov. Bobby Jindal, who chairs the group’s health policy division.

“We are advocating specific policies that try to reform our health care system in a very specific direction that empowers patients … that makes health care more affordable, accessible, that improves outcomes by giving control back to individual patients working with their providers, not government agencies and programs. But, we’re not trying to write the next 3,000-page bill,” Jindal said.

Some of those incremental ideas they hope could get bipartisan support, such as broadening health savings accounts for those with chronic conditions, expanding telehealth flexibilities for providers across state lines, implementing transparency for pharmacy benefit managers and speeding up deployment of biosimilars.

The Heritage Foundation has also detailed policy proposals and recently joined more than 70 other conservative groups to launch an initiative called Project 2025 to develop a governing agenda.

One of those Heritage policy proposals laid out earlier this year illustrates how a future GOP president could overhaul HHS.

Heritage’s plan contains the most detailed ideas for how the next GOP president — who would be the first since the demise of Roe v. Wade — could implement anti-abortion policies, cut off Medicaid funding to Planned Parenthood, and roll back Biden administration initiatives aimed at increasing access to abortion.

The group also envisions splitting CDC into two agencies — one for research and data collection and another for making public health recommendations with “severely confined ability” to influence policy.

What we’re watching: The GOP presidential candidates themselves have said relatively little so far about their plans for the health care system. That could eventually change, given Americans’ concern over health care costs.