Arguably, three trade groups have emerged at the center of healthcare system transformation efforts in the U.S.: the American Hospital Association (AHA), America’s Health Insurance Plans (AHIP) and the Pharmaceutical Research and Manufacturers of America (PhRMA). Others weigh in—the American Medical Association, AdvaMed, the American Public Health Association and others—but this trio is widely regarded as the Big Tents under which policy changes are pursued.

Each plays a unique advocacy role in the system, protecting their members’ turf from unwelcome regulation while fighting against restrictions that might limit their growth opportunities. Their focus is their members:

AHA

AHIP

PhRMA

Members

5000 hospitals & 43,000 individual members

125 Health Insurers

31 Manufacturers

Board Composition

26 (10 female)

33 (5 female)

25 (3 female)

Revenues (’22)

$138.8 Mil

$78.6 Mil

$568.3 Mil

Revenue chg. ’22 v. ‘21

+7.7%

-7.1%

-6.7

Margin (’22)

$6.6 Mil

$4.7 Mil

$-0.1%

Exec Comp % of ’22 Rev

8.4%

9.6%

3.9%

CEO (Tenure)

Richard J. Pollack (since 2015, with AHA 37 yrs.).

Mike Tuffin (since Jan 2024)Prior: SVP UHG, APCO

Stephen J. Ubl (since 2015)Prior: CEO AdvaMed, FAH

Direct Lobbying ‘23

$30.2 Mil

NA

$27.6 Mil

Total Industry Lobbying 2023 (includes all sources)

All three serve diverse memberships and are highly protective of their Big Tents. But each faces growing intramural pressure from member cohorts that seek special attention–especially their large and highly profitable members vs. the rest.

All three struggle with the notions of affordability, price transparency, profit, executive compensation and value. These terms appear frequently in their white papers and comment letters but each tent defines them differently.

All three depend on physicians to fund member revenues: they’re gatekeepers to member patients, referrals and prescriptions. Each Big Tent is focused on advocacy that enables physician interactions upon which member revenues can be sustainable and service disruption minimal. Thus, physician well-being is a concern to the Big Tents.

All blame factors outside their control for health costs escalation. The health habits of population, over-regulation and U.S. monetary policy are frequent targets. Projections by the CBO of annual health spending of 5.6% through 2032 are justified by the Big Tents as the net result of increased demand and flaws in the system’s incentives, legals protections and funding mechanisms. Each Big Tent is on the defensive about how they address costs and waste, and how their prices enable increased affordability.

All three spend heavily to influence lawmakers to avoid unwelcome regulation. Their spending for direct lobbying is multiplied by formal coalitions with friendly trade groups, political action committees, high net worth contributors and corporations. Coalition building is a major function in each Big Tent used against swings in public opinion of concern or against pending legislation that threaten member interests.

All three serve memberships that operate primarily with business-to-business (B2B) business models primarily. Each subordinates ‘consumerism’ to ‘patients, enrollees, and communities’ served by their members. Maximizing consumer (voter) good will and counter-messaging against hostile media coverage are core functions in each Big Tent.

All three favor incremental changes to the status quo over transformational reform of the system top to bottom. Wholesale change is unwelcome though the majority of U.S. adults say it’s fundamentally flawed and needs a fresh start.

In each campaign cycle, the Big Tents create playbooks based on possible election outcomes and potential issues they’ll confront. Each identifies possible political appointees to key government posts, committee appointments and legislative staff that with whom they’ll deal. Each reaches out to friendly think-tanks, ex-pats from previous government roles and research organizations to create favorable thought leadership for the talking heads they trust. And each lines up outside lobbyists to augment their staff.

The Boards of the Big Tent trio weigh in, but senior staff in each of the Big Tents drive the organization’s strategy. They’re experienced in advocacy, well-paid and often heavy-handed in dealing with critics.

Operationally, the 3 Big Tents have much in common. Strategically, they’re far apart and the gap appears to be widening. Each blames the other for medical inflation and unnecessary cost. Each alleges the others use unfair business practices to gain market advantages. And each thinks their vision for the future of the U.S. health system is accurate, complete and in the best interest of the public good.

And none of the three has put-forth a vision for the long-term future of the U.S. health system. Protecting the immediate interests of their members against unwelcome regulatory changes is their focus.

P.S. It can be argued that the American Medical Association is the Fourth Big Tent. However, fewer than a fourth of the million active practitioners are AMA members contrasted to the other Big Tents. Like the trio, AMA’s primary advocacy focus is its members: protecting against encroachment by non-physicians, maintenance of clinical autonomy, restrictions on the use of artificial intelligence in patient care and Medicare reimbursement rate changes are major concerns. And, akin to the others, the wider set of issues facing the system i.e. structure, funding, ownership, price transparency, workforce modernization et al. has gotten less attention.

As state hospital association leaders assemble in Big Sky, Montana this week, the environment for hospital-friendly legislation is threatening at best:

The public’s trust in hospitals has eroded. Hospital financial performance is a mixed bag: some are profitable and many aren’t. Congress thinks hospitals need more regulation to increase price transparency, require ownership disclosure, verify community benefits that justify tax exemptions and impose restrictions on hospital private equity investments. And programs through which state and federal health policies are authorized—HHS, CMS, FTC, FDA, CMMI et al—are in limbo as a result of the June 28, 2024 Chevron ruling by the Supreme Court.

At a federal level, the American Hospital Association has successfully fended-off a significant portion of proposed cuts to key programs (DSH, rural), delayed Congressional action against facility fees and site neutral payments, influenced improvement from April’s proposed 2025 Medicare rate from 2.6% to 2.9%, advanced legislation to protect healthcare workers and streamline prior authorization business practices by insurers. In most cases, it has pursued a unified agenda alongside its Coalition (America’s Essential Hospitals, the Federation of American Hospitals, the Catholic Health Association and the Association of American Medical Colleges , Children’s Hospital Association et al) and it has invested heavily in its lobbying: $6.46 million in the second quarter 2024 (plus $4.1 million by HCA, AAMC, Tenet and others).

At the state level, the attention hospitals get is equally intense but more complicated: It starts with money and demand: Examples:

State resources: 9 states don’t tax any income, regardless of the source (AL, FL, NV, NH, TN, SD, TX, WA, WY); 4 states don’t tax any retirement income: (IL, IA, MS, PA); 8 states tax social security benefits (CO, MN, MT, NM, RI, UT, VT, WV)

Population health status: WalletHub used 44 measures to assess each state and the District of Columbia on healthcare cost, access, and outcomes. WalletHub weighted the three categories equally. The Top 5: MN, RI, SD, IA, NH; the bottom 5: MS, AL, WV, GA, OK

There are Blue and Red states. Some are growing and some declining. All are integrating more diverse populations and divergence between low- and high-income household financial security and spending. The health system, and its hospitals, impact all.

Healthcare spending for state employees, Medicaid and dual eligible enrollees and public health programs consume a third or more of total state spending. And actions taken in states vis a vis ballot referenda, executive orders, administrative agency rulings and legislative actions result in wide variance in the regulatory environments for hospitals. Consider:

32 states have passed legislation to lower health system costs

31 states have CON requirements (24 of these have been revised since 2021).

15 states have passed laws to reduce or eliminate facility fees including hospitals

17 have passed legislative to increase competition in healthcare

23 passed legislation to reduce surprise medical bills

9 have passed legislation to address community benefit declarations by NFP hospital and health systems.

9 have passed legislation to reduce insurer prior authorization obstacles.

13 passed legislation involving reference pricing requirements for hospitals

8 states passed legislation requiring minimal levels of primary care services

24 modified their Certificate of Need programs

3 states have all-payer payment policies.

8 states have drug price control commissions/mechanisms to limit price increases.

And all are grappling with determinations about abortion services, drug formulary design for Medicaid, state health employee health costs, Medicaid eligibility and funding, staffing requirements in hospitals and nursing homes, rural health solvency, telehealth efficacy, insurer plan design restrictions, and scope of practice expansion for nurse practitioners, pharmacists and much more.

The advocacy environment for hospitals at the state and federal levels will be dicier going forward: the near-term macro-environment is unwelcoming for hospitals presumed to have returned to profitability after the pandemic.

It’s root in four convergent issues:

Economic Uncertainty: Last week’s BLS jobs report signaled softening of the economy and alarmed some thinking it a harbinger of a possible recession.

Middle East Tension: the Israeli-Palestinian conflict appears headed toward a broader regional conflict involving Lebanon, Iran and others.

Campaign 2024: hyper-partisanship coupled with disinformation on both sides lends to voter unrest: healthcare affordability, price transparency, consolidation, executive compensation and inequity are ripe targets.

Healthcare Workforce Disenchantment (including Physicians): Hospitals directly employ half of the physician workforce and 30% of total health industry employment. Labor-management tension in hospitals is mounting.

For hospitals, effective advocacy is imperative: the reservoir of good will enjoyed for decades is evaporating. Advertising “we’re there for you” is timely as rural providers need a lifeline, and public castigation of “corporate insurers and billionaire critics” necessary to rally supporters.

But beyond these, two things are clear:

The marketplace for “hospitals” is fundamentally different than the past requiring a clearer value proposition and fresh messaging.

And in states, hospitals will encounter unique opportunities and challenges in plotting strategies for their future. No two are alike.

Big Sky is a symbolic locale for this week’s meeting of state health executives: the Big Sky over hospitals is cloudy.

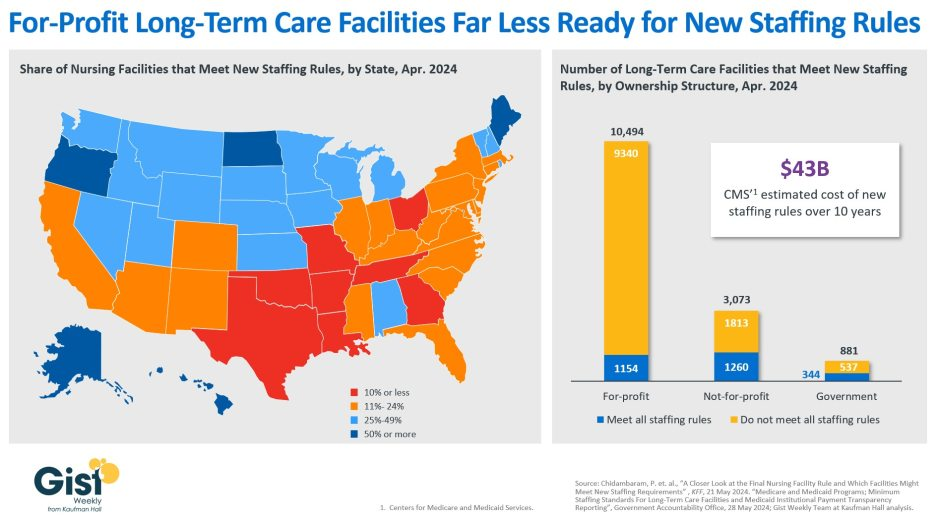

In late April, the Centers for Medicare & Medicaid Services (CMS) establishednew staffing standards for long-term care (LTC) facilities, mandating a minimum of 3.48 hours of nursing care per patient per day, with 33 minutes of that care from a registered nurse, at least one of whom must be always on site. The rule is slated to go into effect in two years for urban nursing homes and three years for rural nursing homes, with some facilities able to apply for hardship exemptions.

Although about one in five LTC facilities nationwide currently meet these staffing standards, staffing levels vary greatly by both state and facility ownership profile. In 28 states, fewer than a quarter of LTC facilities meet the new standards, and in eight states fewer than 10% of facilities are already in compliance.

Facilities in Texas are the least ready, with only 4% meeting the new staffing minimums. In terms of ownership structure, only 11% of for-profit facilities—which constitute nearly three quarters of all LTC facilities nationwide—have staffing levels that meet the new staffing minimums.

The Government Accountability Office projects this new rule will cost LTC facilities $43B over the first ten years, a significant expense at a time when recruiting and retaining nursing talent is already challenging.

Citing the risk of mass closures from facilities unable to comply, nursing home trade groups are suing to stop the mandate from going into effect, and there is also a bill advancing in the House that would repeal the staffing ratios.

That bill is backed by the American Hospital Association, which fears the mandate “would have serious negative, unintended consequences, not only for nursing home patients and facilities, but the entire health continuum.”

In February, the American Hospital Association and five other hospital organizations had urged the court to review the case. The current formula costs DHS hospitals more than a billion dollars each year, according to the AHA.

“The AHA is pleased that the Supreme Court agreed to consider this case,” said Chad Golder, AHA general counsel and secretary, by statement. “As we explained in our amicus brief urging the Court to grant certiorari, it is critical to hospitals and health systems that HHS interpret the DSH fraction consistently across the statute. The agency’s longstanding failure to do so has cost hospitals more than a billion dollars each year, directly harming the hospitals that serve America’s most vulnerable patients. We look forward to the Supreme Court rectifying this legal error next term.”

WHY THIS MATTERS

This case, and one heard by SCOTUS in 2002 called Becerra v. Empire Health Foundation, can be viewed as being two sides of the same coin. Both deal with a different portion of the DSH fraction that determines payment. The Empire Health case dealt with the Medicare portion. This latest case is about the Supplemental Security Income portion.

The AHA and other organizations have argued that HHS incorrectly adopted the view that a patient is entitled to Supplemental Security Income benefits only if the patient actually received cash SSI payments during a hospital stay. This interpretation is inconsistent with the court’s reasoning in Becerra v. Empire Health Foundation, the AHA said.

That 2022 decision said that patients are entitled to Medicare Part A benefits for purposes of the DSH formula if they qualify for the program, even if Medicare is not paying for their hospital stay.

“This case concerns a question that is critical to calculating the Medicare DSH fraction: When are patients ‘entitled to’ SSI benefits and so counted in the numerator? Is it when they are eligible for SSI benefits, or when they are actually receiving cash SSI benefits,” the AHA and other organizations wrote in their brief to the court.

THE LARGER TREND

In February, the American Hospital Association and five other national hospital associations representing hospitals urged the Court to review the case challenging how HHS applies Congress’ formula for calculating Disproportionate Share Hospital payments..

“The correct interpretation of the DSH formula is vitally important to America’s hospitals,” the brief said. “Although HHS has refused to share the data that would allow hospitals to accurately count the SSI-eligible patients whom the agency’s approach excludes, the available estimates suggest that hospitals will lose more than a billion dollars each year in DSH funds. What’s more, a hospital’s eligibility for DSH payments affects its entitlement to other federal benefits designed to help hospitals ‘provide a wide range of medical services’ to vulnerable populations. HHS’s error thus has far-reaching implications for hospitals, patients, and the American healthcare system.”

Becerra v. Empire Health Foundation was a United States Supreme Court case that in 2022 clarified calculations for the Medicare fraction — one of two fractions the Medicare program uses to adjust the rates paid to hospitals that serve a higher-than-usual percentage of low-income patients, according to SCOTUSblog. Those individuals “entitled to [Medicare Part A] benefits” are all those qualifying for the program, regardless of whether they receive Medicare payments for part or all of a hospital stay, the court ruled.

In Becerra v. Empire Health Foundation, the court ruled 5-4 that HHS had properly interpreted the underlying statute and reversed and remanded the decision of the United States Court of Appeals for the Ninth Circuit.

Last week, 2 important economic reports were released that provide a retrospective and prospective assessment of the U.S. health economy:

The CBO National Health Expenditure Forecast to 2032:

“Health care spending growth is expected to outpace that of the gross domestic product (GDP) during the coming decade, resulting in a health share of GDP that reaches 19.7% by 2032 (up from 17.3% in 2022). National health expenditures are projected to have grown 7.5% in 2023, when the COVID-19 public health emergency ended. This reflects broad increases in the use of health care, which is associated with an estimated 93.1% of the population being insured that year… During 2027–32, personal health care price inflation and growth in the use of health care services and goods contribute to projected health spending that grows at a faster rate than the rest of the economy.”

The Congressional Budget Office forecast that from 2024 to 2032:

National Health Expenditures will increase 52.6%: $5.048 trillion (17.6% of GDP) to $7,705 trillion (19.7% of GDP) based on average annual growth of: +5.2% in 2024 increasing to +5.6% in 2032

NHE/Capita will increase 45.6%: from $15,054 in 2024 to $21,927 in 2032

Physician services spending will increase 51.2%: from $1006.5 trillion (19.9% of NHE) to $1522.1 trillion (19.7% of total NHE)

Hospital spending will increase 51.6%: from $1559.6 trillion (30.9% of total NHE) in 2024 to $2366.3 trillion (30.7% of total NHE) in 2032.

Prescription drug spending will increase 57.1%: from 463.6 billion (9.2% of total NHE) to 728.5 billion (9.4% of total NHE)

The net cost of insurance will increase 62.9%: from 328.2 billion (6.5% of total NHE) to 534.7 billion (6.9% of total NHE).

The U.S. Population will increase 4.9%: from 334.9 million in 2024 to 351.4 million in 2032.

The Bureau of Labor Statistics CPI Report for May 2024 and Last 12 Months (May 2023-May2024):

“The Consumer Price Index for All Urban Consumers (CPI-U) was unchanged in May on a seasonally adjusted basis, after rising 0.3% in April… Over the last 12 months, the all-items index increased 3.3% before seasonal adjustment. More than offsetting a decline in gasoline, the index for shelter rose in May, up 0.4% for the fourth consecutive month. The index for food increased 0.1% in May. … The index for all items less food and energy rose 0.2% in May, after rising 0.3 % the preceding month… The all-items index rose 3.3% for the 12 months ending May, a smaller increase than the 3.4% increase for the 12 months ending April. The all items less food and energy index rose 3.4 % over the last 12 months. The energy index increased 3.7%for the 12 months ending May. The food index increased 2.1%over the last year.

Medical care services, which represents 6.5% of the overall CPI, increased 3.1%–lower than the overall CPI. Key elements included in this category reflect wide variance: hospital and OTC prices exceeded the overall CPI while insurance, prescription drugs and physician services were lower.

Physicians’ services CPI (1.8% of total impact): LTM: +1.4%

Hospital services CPI (1.0% of total impact): LTM: +7.3%

Prescription drugs (.9% of total impact) LTM +2.4%

Over the Counter Products (.4% of total impact) LTM 5.9%

Health insurance (.6% of total) LTM -7.7%

Other categories of greater impact on the overall CPI than medical services are Shelter (36.1%), Commodities (18.6%), Food (13.4%), Energy (7.0%) and Transportation (6.5%).

Three key takeaways from these reports:

The health economy is big and getting bigger. But it’s less obvious to consumers in the prices they experience than to employers, state and federal government who fund the majority of its spending. Notably, OTC products are an exception: they’re a direct OOP expense for most consumers. To consumers, especially renters and young adults hoping to purchase homes, the escalating costs of housing have considerably more impact than health prices today but directly impact on their ability to afford coverage and services. Per Redfin, mortgage rates will hover at 6-7% through next year and rents will increase 10% or more.

Proportionate to National Health Expenditure growth, spending for hospitals and physician services will remain at current levels while spending for prescription drugs and health insurance will increase. That’s certain to increase attention to price controls and heighten tension between insurers and providers.

There’s scant evidence the value agenda aka value-based purchases, alternative payment models et al has lowered spending nor considered significant in forecasts.

The health economy is expanding above the overall rates of population growth, overall inflation and the U.S. economy. GDP. Its long-term sustainability is in question unless monetary policies enable other industries to grow proportionately and/or taxpayers agree to pay more for its services. These data confirm its unit costs and prices are problematic.

As Campaign 2024 heats up with the economy as its key issue, promises to contain health spending, impose price controls, limit consolidation and increase competition will be prominent.

Public sector actions

will likely feature state initiatives to lower cost and spend taxpayer money more effectively.

Private sector actions

will center on employer and insurer initiatives to increase out of pocket payments for enrollees and reduce their choices of providers.

Thus, these reports paint a cautionary picture for the health economy going forward. Each sector will feel cost-containment pressure and each will claim it is responding appropriately. Some actually will.

PS: The issue of tax exemptions for not-for-profit hospitals reared itself again last week.

The Committee for a Responsible Federal Budget—a conservative leaning think tank—issued a report arguing the exemption needs to be ended or cut. In response,

the American Hospital Association issued a testy reply claiming the report’s math misleading and motivation ill-conceived.

This issue is not going away: it requires objective analysis, fresh thinking and new voices. For a recap, see the Hospital Section below.

Last week, RAND issued its latest assessment of hospital prices concluding…

“In 2022, across all hospital inpatient and outpatient services (including both facility and related professional claims), employers and private insurers paid, on average, 254% of what Medicare would have paid for the same services at the same facilities. State-level median prices have remained stable across the past three study rounds: 254 %of Medicare prices in 2018 (Round 3), 246%in 2020 (Round 4), and 253% in 2022 (Round 5—the current study).”

Like clockwork, the American Hospital Association issued its “Rebuke” of the report:

“In what is becoming an all too familiar pattern, the RAND Corporation’s latest hospital price report oversells and underwhelms. Their analysis — which despite much heralded data expansions — still represents less than 2% of overall hospital spending. This offers a skewed and incomplete picture of hospital spending. In benchmarking against woefully inadequate Medicare payments, RAND makes an apples-to-oranges comparison that presents an inflated impression of what hospitals are actually getting paid for delivering care while facing continued financial and other operational challenges.

In addition to the ongoing flaw of relying on a self-selected sample of data, their analysis is suspiciously silent on the hidden influence of commercial insurers in driving up health care costs for patients….”

It’s the 5th Edition of RAND’s Employer Transparency Report, each featuring slight methodology changes using Sage Transparency Commercial Claims Data developed for the Employer Forum of Indiana.

The debate over hospital prices is not new nor is RAND the only investigator. Since the Trump administration enacted its Executive Order 13877 (Improving Price and Quality Transparency in American Healthcare) June 24, 2019, numerous organizations have introduced price transparency tools to enable hospital price shopping i.e. Turquoise, Milliman, Leapfrog et al. The Biden administration continued the rule increasing its penalties for non-compliance and Congress has passed 3 laws with bipartisan support widening its application.

However, best-case results reflected as articulated by Larry Levitt, senior vice president of the Kaiser Family Foundation, have not been realized:

“App developers will go crazy developing shopping tools for patients, and patients will use those tools to search for the best deals. The public availability of prices will shame high-priced hospitals into lowering their prices because they’ll be so embarrassed.”

My take:

Academic researchers and economists have concluded that hospital price transparency has not led to reduced heath spending overall nor lower hospital prices. Per a recent systematic review: “No evidence was found for impact on the outcomes volume, availability or affordability. The overall lack of evidence on policies promoting price transparency is a clear call for further research… Price-aware patients chose less costly services that led to out-of-pocket cost savings and savings for health insurers; however, these savings did not translate into reductions in aggregate healthcare spending. Disclosure of list prices had no effect, however disclosure of negotiated prices prompted supply-side competition which led to decreases in prices for shoppable services.”

Per Wall Street Journal actuaries, hospital price increases account for 23% of annual health spending increases but vary widely based on factors other than their underlying costs. Determining how hospital prices are set remains beyond the scope of conventional pricing models.

Nonetheless, hospital price transparency is here to stay: public attention is likely to grow and sources– both accurate and misleading– will multiply. It’s safe for elected officials because it’s popular with voters. Per Patient Rights Advocate survey (December 2023), 93% of adults think hospitals should be required to post all prices ahead of scheduled services. It’s clearly seen as foundational to the Federal Trade Commission doctrines of consumer protection and competition. And it’s important to privately insured consumers—the majority of Americans– since 73% of their claims are for “shoppable services” though they trust payers more than hospitals for estimates of their out-of-pocket obligations in these transactions (61% vs. 22%).

In July 2018, I wrote:” Arguing price transparency in healthcare is a misguided effort is like arguing against clean air and healthy eating: it’s senseless.” It’s still true. Making the case that price transparency has a long way to go based on current offerings and utilization is legitimate.

The price transparency movement is gaining momentum in healthcare: though it still lacks widespread impact on spending today, it soon will.”

Hospitals are 30% of total U.S. health spending and almost 40% of the population uses at least one hospital service every year. Promoting “whole person care,” while touting quality war while disregarding affordability and price transparency for consumers seems inconsistent. Enabling consumers to easily access accurate prices—not just out-of-pocket estimates– is imperative for hospitals seeking long-term relevance and sustainability. And state and federal lawmakers, along with employers, should structure benefits that reward consumers directly for shopping discipline instead of allowing insurers to benefit alone.

Is the Juice worth the Squeeze for hospital price transparency efforts? To date, proponents say yes, opponents say no, and each side has valid concern about use by consumers. But unless one believes the role of consumers as purchasers and users of the system’s service will diminish in coming years, the safe bet is hospital price transparency will play a bigger role.

Hospitals with larger market shares were among the worst offenders, the Rand Corporation found.

Dive Brief:

Employers and private insurers continue to pay hospitals more for inpatient and outpatient services than Medicare would have reimbursed, according to a newstudy from policy think tankthe Rand Corporation.

In 2022, private insurers and employers paid on average 254% of what Medicare would have paid for the same care services — up from 224% two years prior.

Health systems often argue they hike up commercial rates to offset losses from government underpayments, according to the study. However, a hospital’s market share, rather than population of Medicare or Medicaid patients, more accurately predicted pricing, with larger health systems charging higher prices.

Dive Insight:

Since 2021, health systems and insurers have been required to post pricing information for their 300 most common procedures as the government pushes to make healthcare prices more transparent.

However, researchers have accused hospitals and insurers of failing to fully comply with the regulations.

The Rand study found inpatient prices for hospital services were 255% above what Medicare paid in 2022 while outpatient hospital service prices averaged 289%, according to the report, which was based on an analysis of 4,000 hospitals across 49 states.

Prices for services at outpatient ambulatory surgical centers was slightly lower at 170% of Medicare payments.

There were also differences in pricing by geography. Arkansas, Iowa, Massachusetts, Michigan and Mississippi kept relative prices below 200% of Medicare prices during the study period. However, others had relative prices above 300% of Medicare. Hospitals in Florida and Georgia negotiated the highest relative rates.

Price transparency could be a tool for administrators of employer-sponsored plans to better negotiate employee benefits. Although employer-sponsored plans cover 160 million Americans, researchers said employers operate at a disadvantage when negotiating prices with providers and insurers due to a lack of detailed pricing information.

“The widely varying prices among hospitals suggests that employers have opportunities to redesign their health plans to better align hospital prices with the value of care provided,” said Brian Briscombe, lead researcher for the Rand hospital price transparency project, in a statement. “However, price transparency alone will not lead to changes if employers do not or cannot act upon price information.”

State and federal policymakers could rebalance negotiations by cracking down on noncompetitive healthcare markets, placing limits on payments for out-of-network hospital care or allowing employers to buy into Medicare or other public options, the report said.

The nation’s largest hospital lobby, the American Hospital Association, has rejected previous analyses of pricing data — including reports from Patient Rights Advocate.

On Monday, Molly Smith, AHA’s vice president for policy, pushed back against the Rand study, saying it was “suspiciously silent on the hidden influence of commercial insurers in driving up health care costs for patients, as evidenced by issues like the recent concerning allegations against MultiPlan.”

Last week, Community Health Systems filed suit against MultiPlan alleging it had colluded with insurers to raise prices for patients and lower payments to providers. The lawsuit is the third against MultiPlan in under a year.

This is National Hospital week. It comes at a critical time for hospitals:

The U.S. economy is strong but growing numbers in the population face financial insecurity and economic despair. Increased out-of-pocket costs for food, fuel and housing (especially rent) have squeezed household budgets and contributed to increased medical debt—a problem in 41% of U.S. households today. Hospital bills are a factor.

The capital market for hospitals is tightening: interest rates for debt are increasing, private investments in healthcare services have slowed and valuations for key sectors—hospitals, home care, physician practices, et al—have dropped. It’s a buyer’s market for investors who hold record assets under management (AUM) but concerns about the harsh regulatory and competitive environment facing hospitals persist. Betting capital on hospitals is a tough call when other sectors appear less risky.

Utilization levels for hospital services have recovered from pandemic disruption and operating margins are above breakeven for more than half but medical inflation, insurer reimbursement, wage increases and Medicare payment cuts guarantee operating deficits for all. Complicating matters, regulators are keen to limit consolidation and force not-for-profits to justify their tax exemptions. Not a pretty picture.

And, despite all this, the public’s view of hospitals remains positive though tarnished by headlines like these about Steward Health’s bankruptcy filing last Monday:

The public is inclined to hold hospitals in high regard, at least for the time being. When asked how much trust and confidence they have in key institutions to “to develop a plan for the U.S. health system that maximizes what it has done well and corrects its major flaws,” consumers prefer for solutions physicians and hospitals over others but over half still have reservations:

A Great Deal

Some

Not Much/None

Health Insurers

18%

43%

39%

Hospitals

27%

52%

21%

Physicians

32%

53%

15%

Federal Government

14%

42%

44%

Retail Health Org’s

21%

51%

28%

The American Hospital Association (AHA) is rightfully concerned that hospitals get fair treatment from regulators, adequate reimbursement from Medicare and Medicaid and protection against competitors that cherry-pick profits from the health system.

It can rightfully assert that declining operating margins in hospitals are symptoms of larger problems in the health system: flawed incentives, inadequate funding for preventive and primary care, the growing intensity of chronic diseases, medical inflation for wages, drugs, supplies and technologies, the dominance of ‘Big Insurance’ whose revenues have grown 12.1% annually since the pandemic and more. And it can correctly prove that annual hospital spending has slowed since the pandemic from 6.2% (2019) to 2.2% (2022) in stark contrast to prescription drugs (up from 4% to 8.4% and insurance costs (from -5.4% to +8.5%). Nonetheless, hospital costs, prices and spending are concerns to economists, regulators and elected officials.

National health spending data illustrate the conundrum for hospitals: relative to the overall CPI, healthcare prices and spending—especially outpatient hospital services– are increasing faster than prices and spending in other sectors and it’s getting attention: that’s problematic for hospitals at a time when 5 committees in Congress and 3 Cabinet level departments have their sights set on regulatory changes that are unwelcome to most hospitals.

My take:

The U.S. market for healthcare spending is growing—exceeding 5% per year through the next decade. With annual inflation targeted to 2.0% by the Fed and the GDP expected to grow 3.5-4.0% annually in the same period, something’s gotta’ give. Hospitals represent 30.4% of overall spending today (virtually unchanged for the past 5 years) and above 50% of total spending when their employed physicians and outside activities are included, so it’s obvious they’ll draw attention.

Today, however, most are consumed by near-term concerns– reimbursement issues with insurers, workforce adequacy and discontent, government mandates– and few have the luxury to look 10-20 years ahead.

I believe hospitals should play a vital role in orchestrating the health system’s future and the role they’ll play in it. Some will be specialty hubs. Some will operate without beds. Some will be regional. Some will close. And all will face increased demands from regulators, community leaders and consumers for affordable, convenient and effective whole-person care.

For most hospitals, a decision to invest and behave as if the future is a repeat of the past is a calculated risk. Others with less stake in community health and wellbeing and greater access to capital will seize this opportunity and, in the process, disable hospitals might play in the process.

Near-term reactive navigation vs. long-term proactive orchestration–that’s the crossroad in front of hospitals today. Hopefully, during National Hospital Week, it will get the attention it needs in every hospital board room and C suite.

PS: Last week, I wrote about the inclination of the 18 million college kids to protest against the healthcare status quo (“Is the Health System the Next Target for Campus Unrest?” The Keckley Report May 6, 2024 www.paulkeckley.com). This new survey caught my attention:

According to the Generation Lab’s survey of 1250 college students released last week, healthcare reform is a concern. When asked to choose 3 “issues most important to you” from its list of 13 issues, healthcare reform topped the list. The top 5:

Health Reform (40%)

Education Funding and access (38%)

Economic fairness and opportunity (37%)

Social justice and civil rights (36%)

Climate change (35%)

If college kids today are tomorrow’s healthcare workforce and influencers to their peers, addressing the future of health system with their input seems shortsighted. Most hospital boards are comprised of older adults—community leaders, physicians, et al.

And most of the mechanisms hospitals use to assess their long-term sustainability is tethered to assumptions about an aging population and Medicare.

College kids today are sending powerful messages about the society in which they aspire to be a part. They’re tech savvy, independent politically and increasingly spiritual but not religious. And the health system is on their radar.

The Medicare trustees’ new projection for insolvency is five years later than previous forecasts, but budget hawks warned action is still needed to shore up the insurance program’s finances.

Dive Brief:

A key trust fund underpinning the massive Medicare program has a new insolvency date: 2036, according to a new report from the Medicare trustees.

That’s five years later than the go-broke date in last year’s report, thanks to more workers being paid higher wages causing more revenue to flow into the trust fund’s coffers, along with lower spending on pricey hospital and home health services.

Still, looming insolvency absent action in Washington remains a serious source of concern for the longevity of Medicare, which covers almost 67 million senior and disabled Americans, according to budget hawks.

Dive Insight:

Dire predictions in the annual Medicare trustees report have varied in the past few years. In 2020, in the early throes of COVID-19, the board predicted the Hospital Insurance Trust Fund fund would run out by 2026. That deadline was pushed back to 2028 and then 2031 in subsequent years’ reports, amid a broader economic rebound and more care shifting to cheaper outpatient settings.

Now, the trustees — a group comprised of the Treasury, Labor and HHS secretaries, along with the Social Security commissioner — are forecasting an additional five years of breathing room for Medicare solvency.

Along with the healthier economy, that’s in part due to the Inflation Reduction Act passed in 2022, which restrains price growth and allows Medicare to negotiate drug prices for certain Part B and Part D drugs, and should lower government spending in the program overall, according to the report.

The Hospital Insurance Trust Fund, which pays hospitals and providers of post-acute services, and also covers some of the cost of private Medicare Advantage plans, is mostly funded by payroll taxes, along with income from premiums.

The HI fund is separate from another trust fund that covers benefits for Medicare Parts B and D, including outpatient services and physician-administered drugs. That Supplemental Medical Insurance trust fund is largely funded by premiums and general revenue that resets each year and doesn’t face the same solvency concerns.

In 2023, HI income exceeded spending by $12.2 billion. Surpluses should continue through 2029, followed by deficits until the fund runs out entirely in 2036, according to the report.

At that point, the government won’t be able to pay full benefits for inpatient hospital visits, nursing home stays and home healthcare.

Spending is projected to grow substantially in Medicare largely due to demographic changes.

The number of Americans at the qualification age for Medicare is projected to reach 95 million by 2060, rising from 16% of the total population in 2018 to 23% at that time, according to the Census Bureau. As a result, beneficiaries in the program will swell as the number of workers paying into the trust fund shrinks.

The trustees forecast Medicare’s costs under current law will rise steadily from their current level of 3.8% of the gross domestic product, to 5.8% in 2048 and 6.2% by 2098.

To date, lawmakers have not allowed the Medicare trust fund to become depleted. But amid increasingly dire warnings from trustees and watchdogs urging the need to align spending with revenue, Congress has delayed taking action to improve Medicare’s finances, following bipartisan efforts to lower spending in the early 2010s.

The fund hasn’t met the trustees’ test for short-range financial adequacy since 2003, and has triggered funding warnings since 2018.

“The absurd part is that we’ve known insolvency was looming for quite some time. We’re driving straight into this mess despite all the warning bells and alarms that the Trustees and others have been ringing for decades now,” Maya MacGuineas, president of the Committee for a Responsible Federal Budget, said in a statement on the report.

Along with concerns about Medicare access and quality for seniors, physicians will also be heavily affected by Medicare insolvency, according to the report. Physician groups, which perennially slam Medicare for low payment rates as it is, used the report to lobby for spending reform to align reimbursement with the cost of practicing medicine.

The American Medical Association argued the report highlights the need for policy changes, such as linking the annual payment update for doctors to the Medicare Economic Index, a measure of practice cost inflation — a suggestion also supported by influential congressional advisory group MedPAC.

“It would be political malpractice for Congress to sit on its hands and not respond to this report,” AMA President Jesse Ehrenfeld said in a statement.

Federal entitlement programs like Medicare remain on shaky ground because lawmakers are loath to take steps to increase revenue (i.e. raise taxes) or lower spending (i.e. raise the age of eligibility), measures deeply unpopular with voters.

Last year, President Joe Biden pitched a plan to keep Medicare’s hospital trust fund solvent beyond 2050 without cutting benefits. The plan would further reduce what Medicare pays for prescription drugs and raise taxes on Americans earning over $400,000.

There has been no movement in Congress on the proposal. Yet in a statement Monday, Biden took credit for strengthening Medicare, while his campaign in an email reupped comments from Republican presidential candidate Donald Trump that if elected he would consider cutting Medicare and other entitlement programs. Trump, who later walked back the comments, has not proposed a plan to address Medicare’s shortfall.

Last Tuesday (April 23), the Federal Trade Commission (FTC) issued a 570-page final rule in a partisan 3-2 vote prohibiting employers from binding most American workers to post-employment non-competition agreements (the “Final Rule”):

“Pursuant to sections 5 and 6(g) of the Federal Trade Commission Act (“FTC Act”), the Federal Trade Commission (“Commission”) is issuing the Non-Compete Clause Rule (“the final rule”). The final rule provides that it is an unfair method of competition—and therefore a violation of section 5—for persons to, among other things, enter into non-compete clauses (“non-competes”) with workers on or after the final rule’s effective date. With respect to existing non-competes—i.e., non-competes entered into before the effective date—the final rule adopts a different approach for senior executives than for other workers. For senior executives (in policy setting/executive positions who earned more than $151,164 last year), existing non-competes can remain in force, while existing non-competes with other workers are not enforceable after the effective date.” (p.1)

“Concerns about non-competes have increased substantially in recent years in light of empirical research showing that they tend to harm competitive conditions in labor, product, and service markets. … When a company interferes with free competition for one of its former employee’s services, the market’s ability to achieve the most economically efficient allocation of labor is impaired. Moreover, employee-noncompetition clauses can tie up industry expertise and experience and thereby forestall new entry… competes by employers tends to negatively affect competition in labor markets, suppressing earnings for workers across the labor force—including even workers not subject to noncompete. This research has also shown that non-competes tend to negatively affect competition in product and service markets, suppressing new business formation and innovation… Yet despite the mounting empirical and qualitative evidence confirming these harms and the efforts of many States to ban them, non-competes remain prevalent in the U.S. economy. Based on the available evidence, the Commission estimates that approximately one in five American workers—or approximately 30 million workers—is subject to a non-compete. The evidence also indicates that employers frequently use non-competes even when they are unenforceable under State law.” (p.6)

On its home page, the FTC says “with a comprehensive ban on new non-competes, Americans could see an increase in wages, new business formation, reduced health care costs and more.”(www.ftc.gov)

The rule takes effect 120 days following its publication in the Federal Register and is applicable to every employer including specified operations in not-for-profit organizations (which represents the majority of hospitals, nursing homes and others). The agency noted it received 26,000 comment letters since the proposed rule was published January 19, 2023 including significant reaction from healthcare organizations. By the end of last week, two lawsuits were filed: one by the Chamber of Commerce in the United States District Court for the Eastern District of Texas and the second by a global tax services and software company in the Northern District of Texas – each challenging the Final Rule and arguing that the FTC lacked the authority. Others are likely to follow and its implementation will be delayed as arguments about its merits and the FTC’s standing to make the rule find their way thru the courts.

Special attention to hospitals and physicians in the rule

Notably, the use of non-competes in healthcare is a central theme in the rule, particularly in tax-exempt hospital and medical practice settings. Noting that one in 5 workers (30 million) and up to 45% of physicians work under non-compete agreements today, the Commissioners illustrated the need for the rule by inserting vignettes from 14 workers in their introduction: 4 of these were healthcare workers– 2 physicians and employees of a hospital and electronic health record provider (p.11-13). Throughout its exhaustive commentary, the Commissioners took issue with assertions by healthcare organizations about the potential negative consequences of the rule citing lack of empirical evidence to justify opposition claims. References to tax-exempt hospitals, their for-profit activities and their employment arrangements with physicians are frequent in the commentary justifying the application of the rule as follows:

“Many commenters representing healthcare organizations and industry trade associations stated that the Commission should exclude some or all of the healthcare industry from the rule because they believe it is uniquely situated in various ways. The Commission declines to adopt an exception specifically for the healthcare industry. The Commission is not persuaded that the healthcare industry is uniquely situated in a way that justifies an exemption from the final rule. The Commission finds use of non-competes to be an unfair method of competition that tends to negatively affect labor and product and services markets, including in this vital industry; the Commission also specifically finds that non-competes increase healthcare costs. Moreover, the Commission is unconvinced that prohibiting the use of non-competes in the healthcare industry will have the claimed negative effects.” (p.303)

Not surprisingly rule, responses from the hospital trade groups were swift, direct and harshly critical:

American Hospital Association (www.aha.org):” The FTC’s final rule banning non-compete agreements for all employees across all sectors of the economy is bad law, bad policy, and a clear sign of an agency run amok. The agency’s stubborn insistence on issuing this sweeping rule — despite mountains of contrary legal precedent and evidence about its adverse impacts on the health care markets — is further proof that the agency has little regard for its place in our constitutional order. Three unelected officials should not be permitted to regulate the entire United States economy and stretch their authority far beyond what Congress granted it–including by claiming the power to regulate certain tax-exempt, non-profit organizations. The only saving grace is that this rule will likely be short-lived, with courts almost certain to stop it before it can do damage to hospitals’ ability to care for their patients and communities.”

Federation of American Hospitals (www.fah.org):“This final rule is a double whammy. In n a time of constant health care workforce shortages, the FTC’s vote today threatens access to high-quality care for millions of patients.”

By contrast, the American Medical Association (www.ama-assn.org) response was positive, linking its support for the rule to AMA’s ethical principles of physician independence and clinical autonomy.

Four implicit messages to healthcare are evident in the rule

It is unlikely the rule will become law in its current form. Opposing trade groups, employers dependent on non-competes for protections of trade secrets and business relationships and many others will actively pursue its demise in courts actions. But a review of the text makes clear the FTC is intensely focused on competition and consumer protections in healthcare akin to its ongoing challenges to hospital consolidation.

Four messages emerge from the text of the rule:

1-‘The healthcare industry is a business which needs more regulation to protect consumers and its workforce by lowering costs and stimulating competition. ‘

“Many commenters representing healthcare organizations and industry trade associations stated that the Commission should exclude some or all of the healthcare industry from the rule because they believe it is uniquely situated in various ways. The Commission declines to adopt an exception specifically for the healthcare industry. The Commission is not persuaded that the healthcare industry is uniquely situated in a way that justifies an exemption from the final rule. The Commission finds use of non-competes to be an unfair method of competition that tends to negatively affect labor and product and services markets, including in this vital industry; the Commission also specifically finds that non-competes increase healthcare costs. Moreover, the Commission is unconvinced that prohibiting the use of non-competes in the healthcare industry will have the claimed negative effects.” (p.373)

2-‘Physicians play a unique role in healthcare and deserve protection.’

“Some healthcare businesses and trade organizations opposing the rule argued that, without non-competes, physician shortages would increase physicians’ wages beyond what the commenters view as fair. The commenters provided no empirical evidence to support these assertions, and the Commission is unaware of any such evidence. Contrary to commenters’ claim that the rule would increase physicians’ earnings beyond a “fair” level, the weight of the evidence indicates that the final rule will lead to fairer wages by prohibiting a practice that suppresses workers’ earnings by preventing competition; that is, the final rule will simply help ensure that wages are determined via fair competition. The Commission also notes that it received a large number of comments from physicians and other healthcare workers stating that non-competes exacerbate physician shortages.” (p.157)

“Hundreds of physicians and other commenters in the healthcare industry stated that non-competes negatively affect physicians’ ability to provide quality care and limit patient access to care, including emergency care. Many of these commenters stated that non-competes restrict physicians from leaving practices and increase the risk of retaliation if physicians object to the practices’ operations, poor care or services, workload demands, or corporate interference with their clinical judgment. Other commenters from the healthcare industry said that, like other industries, non-competes bar competitors from the market and prevent providers from moving to or starting competing firms, thus limiting access to care and patient choice. Physicians and physician organizations said non-competes contribute to burnout and job dissatisfaction, and said burnout negatively impacts patient care.” (p.202)

“…the Commission notes that while the study finds that non-competes make physicians more likely to refer patients to other physicians within their practice—increasing revenue for the practice—it makes no findings on the impact on the quality of patient care. The Commission further notes that pecuniary benefits to a firm cannot justify an unfair method of competition.” (p.206)

3.’Tax exempt hospitals that operate like for-profit entities deserve special scrutiny from regulators and are thus subject to the rule’s provisions.’

“Merely claiming tax-exempt status in tax filings is not dispositive. At the same time, if the Internal Revenue Service (“IRS”) concludes that an entity does not qualify for tax-exempt status, such a finding would be meaningful to the Commission’s analysis of whether the same entity is a corporation under the FTC Act.” (p.53)

“As stated in Part II.E, entities claiming tax exempt status are not categorically beyond the Commission’s jurisdiction, but the Commission recognizes that not all entities in the healthcare industry fall under its jurisdiction. “(p.374)

“While the Commission shares commenters’ concerns about consolidation in healthcare, it disagrees with commenters’ contention that the purported competitive disadvantage to for-profit entities stemming from the final rule would exacerbate this problem. As some commenters stated, the Commission notes that hospitals claiming tax-exempt status as nonprofits are under increasing public scrutiny. Public and private studies and reports reveal that some such hospitals are operating to maximize profits, paying multi-million-dollar salaries to executives, deploying aggressive collection tactics with low-income patients, and spending less on community benefits than they receive in tax exemptions.943 Economic studies by FTC staff demonstrate that these hospitals can and do exercise market power and raise prices similar to for-profit hospitals.944 Thus, as courts have recognized, the tax-exempt status as nonprofits of merging hospitals does not mitigate the potential for harm to competitive conditions.” (p.383)

“Conversely, many commenters vociferously opposed exempting entities that claim tax exempt status as nonprofits from coverage under the final rule. Several commenters contended that, in practice, many entities that claim tax-exempt status as nonprofits are in fact “organized to carry on business for [their] own profit or that of [their] members” such that they are “corporations” under the FTC Act. These commenters cited reports by investigative journalists to contend that some hospitals claiming tax-exempt status as nonprofits have excess revenue and operate like for-profit entities. A few commenters stated that consolidation in the healthcare industry is largely driven by entities that claim tax-exempt status as nonprofits as opposed to their for-profit competitors, which are sometimes forced to consolidate to compete with the larger hospital groups that claim tax-exempt status as nonprofits. Commenters also contended that many hospitals claiming tax-exempt status as nonprofits use self-serving interpretations of the IRS’s “community benefit” standard to fulfill requirements for tax exemption, suggesting that the best way to address unfairness and consolidation in the healthcare industry is to strictly enforce the IRS’s standards and to remove the tax-exempt status of organizations that do not comply. An academic commenter argued that the distinction between for-profit hospitals and nonprofit hospitals has become less clear over time, and that the Commission should presumptively treat hospitals claiming nonprofit tax-exempt status as operating for profit unless they can establish that they fall outside of the Commission’s jurisdiction.” (p.377-378)

“After carefully considering commenters’ arguments, the Commission declines to exempt for-profit healthcare employers or to exempt the healthcare industry altogether.” (p.380)

4. ‘The net impact of non-compete agreements is harmful to the workforce and the public. ‘

“The Commission finds that with respect to these workers, these practices are unfair methods of competition in several independent ways:

The use of non-competes is restrictive and exclusionary conduct that tends to negatively affect competitive conditions in labor markets.

The use of non-competes is restrictive and exclusionary conduct that tends to negatively affect competitive conditions in product and service markets.

The use of non-competes is exploitative and coercive conduct that tends to negatively affect competitive conditions in labor markets.

The use of non-competes is exploitative and coercive conduct that tends to negatively affect competitive conditions in product and service markets.” (p.105)

“The Commission notes that the vast majority of comments from physicians and other stakeholders in the healthcare industry assert that non-competes result in worse patient care. The Commission further notes that the American Medical Association discourages the use of non-competes because they “can disrupt continuity of care, and may limit access to care.” In addition, there are alternatives for improving patient choice and quality of care, and for retaining physicians, that burden competition to a much less significant degree than non-competes…commenters asserted that a ban on non-competes would upend healthcare labor markets, thereby exacerbating healthcare workforce shortages, especially in rural and underserved areas. A medical society argued that non-competes can allow groups to meet contractual obligations to hospitals, as physicians leaving can prevent the group from ensuring safe care. As the Commission notes, there are not reliable empirical studies of these effects, and these commenters do not provide any. However, the Commission notes that the rule will increase labor mobility generally, which makes it easier for firms to hire qualified workers.” (p.208)

“The Commission also noted that in three States—California, North Dakota, and Oklahoma—employers generally cannot enforce non-competes, so they must protect their investments using one or more of these less restrictive alternatives…Commenters provide no empirical evidence, and the Commission is unaware of any such evidence, to support the theory that prohibiting non-competes would increase consolidation or raise prices. “384

The bottom line:

Odds are this rule will not become law anytime soon allowing healthcare organizations to consider alternatives to the non-competes they use. Work-arounds for protection of intellectual property, talent acquisition, employment agreements are likely as HR professionals, benefits and compensation consultancies huddle to consider what’s next.

Those that operate in 3 states (CA, ND, OK) already face state reg’s limiting non-competes and more states are adding measures. As noted in the rule, the health systems in these states have not been debilitated by non-compete limitations nor empirical evidence of public/worker harm produced, so no harm no foul.

The bigger takeaways from this rule for healthcare—especially hospitals—are 2:

The rule may fuel already growing antipathy between the workforce and senior management. Physicians are frustrated and burned out. Mid-level clinicians, techs and nurses are not happy. The hourly workforce is insecure. The hospital workplace—its clinics, programs and services—is not a happy place these days. The rule might fuel increased union organizing activity among some work groups at a critical time when demand is high, utilization is increasing, resources are stretched, reimbursement is shrinking and conditions for solvency and sustainability in question for rural, safety net and community hospitals in areas of declining population. And employed physicians will push-back harder against pressure from their hospital and private equity partners to work harder and produce more. The rule gives physicians a moral premise on which to oppose employer demands, whether the rule is implemented in its current form or not.

And the second equally notable takeaway is the rule’s specific attention to tax-exempt hospitals that operate as “for-profit” organizations. The FTC Commissioners question their tax exemptions and their investor-owned competitors are happy they noticed. They’re joined by investigations in 5 Committee’s of Congress with Bipartisan support for a fresh look at their bona fide eligibility despite strong pushback by the American Hospital Association and others.

This rule was introduced as a proposed rule last year with a comment period of 90 days allowed. Fifteen months and 26,000 comments later, it’s the latest reminder that the future of healthcare is everyone’s business and hospitals and physicians see that future state differently.

In its summation, the FTC estimates that this final rule will lead to new business formation growing by 2.7% per year, create 8,500 additional new businesses annually, produce 17,000-29,000 patents for innovation, increase earnings for workers and lower health care costs by up to $194 billion over the next decade. Maybe.

What’s clear is that the FTC and regulators in DC and many states are watching the industry closely and many aren’t buying what we’re selling.