Following rumors of a potential merger reported last month by the Wall Street Journal, the paper shared this week that Bloomfield, CT-based Cigna is no longer pursuing an acquisition of Louisville, KY-based Humana.

According to insiders, the $140B merger was scuttled when the two health insurance giants couldn’t agree on price and other terms.

Instead, Cigna announced that it will be focusing on smaller, bolt-on acquisitions, and is reportedly still considering divesting its Medicare Advantage business.

Cigna also announced $10B of stock buybacks to assuage shareholders, who reacted negatively to the rumored deal, dropping the company’s stock price by nearly 10 percent since merger rumors surfaced.

The Gist: While there are several reasons why this deal may have been called off—Wall Street’s adverse reaction, antitrust concerns, leaking of the talks before the parties were ready—this likely isn’t the end of either payer’s pursuit of greater scale, as both stand in UnitedHealth Group’s giant shadow.

Given Cigna and Humana have each had potential mergers with other payers blocked by the courts, and federal antitrust scrutiny is only increasing, we’re wondering if each may be also looking at nontraditional partners (as Humana explored with Walmart in 2018), though the universe of companies with an interest in a vertically-integrated insurance and care business—and deep enough pockets—is small.

After signing a letter of intent in late May, St. Louis, MO-based BJC HealthCare and Kansas City, MO-based Saint Luke’s Health System announced on Wednesday that they have signed a definitive merger agreement, having received the necessary regulatory approvals.

Based on opposite sides of the “Show-Me State,” the systems’ markets do not directly overlap. The merger, expected to close on Jan. 1, 2024, will create a $10B revenue, 28-hospital system spanning Missouri, southern Illinois, and eastern Kansas. The two systems plan to retain their respective brands and will be dually headquartered in St. Louis and Kansas City.

The Gist: BJC and Saint Luke’s are following in the footsteps of other recent mergers involving large health systems with no geographic overlap, which regulators have allowed to move forward. However, recent history shows there’s more to closing a deal than just passing regulatory muster.

Both the Sanford-Fairview and UnityPoint-Presbyterian mergers were called off earlier this year for non-regulatory reasons, including the concerns of local stakeholders.

Given the difficult financial environment and the growing threat of vertically integrated payers, health systems looking to pursue scale strategies must ensure they will actually realize the promise these combinations may hold.

According to a Wall Street Journal exclusive published this Wednesday, Bloomfield, CT-based Cigna and Louisville, KY-based Humana, two of the nation’s largest health insurers, are exploring a merger that could close as soon as the end of this year.

With Cigna valued at around $83B and Humana at roughly $62B, their potential combination would be the largest domestic merger of the year, not just in healthcare, but across all industries.

According to anonymous insiders, the companies are discussing a cash-and-stock deal, but nothing has been finalized. Should an agreement be reached, the merger is expected to receive close attention from antitrust authorities. Both Humana and Cigna have attempted to merge with rival insurers over the past decade, only to see the deals blocked on antitrust grounds.

The Gist: This would be a blockbuster deal, putting the combined entity on par with CVS Health and UnitedHealth Group.

Though Cigna and Humana have relatively little direct overlap in their health insurance businesses—Humana recently announced it will exit the commercial group business to focus on its more successful Medicare Advantage (MA) offerings and Cigna, mostly a commercial insurer, is reportedly shopping its much smaller MA business—their respective pharmacy benefit managers (PBMs) may be an antitrust sticking point. (By market share, Cigna’s Express Scripts is the second-largest PBM, while Humana’s CenterWell Pharmacy is fourth.)

Given the Biden administration’s focus on targeting potentially anticompetitive healthcare mergers, as well as rising Congressional scrutiny around PBMs, this potential merger is sure to face many hurdles prior to closing.

This week we showcase data from a recent American Antitrust Institute study on the growth of private equity (PE)-backed physician practices, and the impact of this growth on market competition and healthcare prices.

From 2012 to 2021, the annual number of practice acquisitions by private equity groups increased six-fold, especially in high-margin specialties. During this same time period, the number of metropolitan areas in which a single PE-backed practice held over 30 percent market share rose to cover over one quarter of the country.

These “hyper-concentrated” markets are especially prevalent in less-regulated states with fast-growing senior populations, like Arizona, Texas, and Florida.

The study also found an association between PE practice acquisitions and higher healthcare prices. In highly concentrated markets, certain specialties, like gastroenterology, were able to raise prices rise by as much as 18 percent.

While new Federal Trade Commission proposals demonstrate the government’s renewed interest in antitrust enforcement, it may be too little, too late to mitigate the impact of specialist concentration in many states.

Last week the Department of Justice (DOJ) and the Federal Trade Commission (FTC) proposed thirteen new merger guidelines that, if finalized, would provide federal regulators greater ability to scrutinize mergers across all industries, including healthcare.

The guidelines expand which mergers could be potentially illegal and therefore worth probing, including those with lower monetary value and those in which the newly combined organization would control 30 percent or greater market share, and would increase scrutiny on transactions that are part of a series of multiple acquisitions by an organization. They also seek to limit the ability of an organization to justify an acquisition on the grounds that the weaker party in the deal would be unable to continue to operate. Comments on the guidelines are being accepted until September 18.

The Gist: To date, federal regulators have struggled to prevent non-traditional mergers between companies that provide different services, operate in different markets, or are below the monetary threshold for review.

The proposed guidelines would significantly increase FTC and DOJ scrutiny at all levels of hospital mergers, and also jeopardize physician and other care asset acquisitions by health systems, payers, and private equity-backed organizations. They are the latest from the Biden Administration in a recent, multi-part push to reduce consolidation through greater antitrust enforcement.

This effort includes last month’s proposal to add additional reporting requirements for mergers outlined in the Hart-Scott-Rodino Act, as well as the FTC’s move earlier this month to withdraw two antitrust policy statements focused on healthcare markets that both agencies say are now “outdated.” Those now-rescinded statements provided guidance on antitrust safety zones, including for accountable care organizations participating in the Medicare Shared Savings Program and for mergers between two hospitals in which one is much smaller.

A detailed report, published by a group of organizations including the American Antitrust Institute, provides one of the highest-quality examinations of the growth of private equity (PE)-backed physician practices, and the impact of this growth on market competition and healthcare prices.

From 2012 to 2021, the annual number of practice acquisitions by private equity groups increased six-fold, and the number of metropolitan areas in which a single PE-backed practice held over 30 percent market share rose to cover over one quarter of the country. (Check out figure 3B at the bottom of page 20 in the report to see if you live in one of those markets.)

The study also found an association between PE practice acquisitions and higher healthcare prices and per-patient expenditures. In highly concentrated markets, certain specialties, like gastroenterology, saw prices rise by as much as 18 percent.

The Gist: As the report highlights, one of the greatest barriers to assessing PE’s impact on physician practices is the lack of transparency around acquisitions and ownership structures. This analysis brings us closer to understanding the scope of the issue, and makes a strong case for regulatory and legislative intervention.

Recent proposed changes to federal premerger disclosure requirements offer a good start, but many practice acquisitions are still too small to flag review, and slowing future acquisitions will do little to unwind the market concentration already emerging.

PE is also not the sole actor contributing to healthcare consolidation, and proposed remedies may target the activities of payers and health systems considered anti-competitive as well.

Last Thursday, the Senate Finance Committee heard testimony from experts who offered damning testimony about hospital consolidation (excerpts below). Committee Chair Ron Wyden (D-OR) gaveled the session to order with this commentary:

“I’d like to talk about health care costs and quality. Advocates for proposed mergers often say they will bring lower health costs due to increased efficiency. Time after time, it’s simply not proven to be the case. When hospitals merge, prices go up, not down. When insurers merge, premiums go up, not down. And quality of care is not any better with this higher cost. “

Ranking Member Mike Crapo (R-ID) offered a more conciliatory assessment in his opening statement: “In exploring and addressing these problems, we have the opportunity to build on our efforts to improve medication access and affordability by taking a broader look at the health care system through a similarly bipartisan, consensus-based lens…We need to examine the drivers of consolidation, as well as its effects on care quality and costs, both for patients and taxpayers. We also need to develop focused, bipartisan and bicameral solutions that reduce out-of-pocket spending while protecting access to lifesaving services.”

Congress’ concern about consolidation in healthcare is broad-based. Pharmacy benefits managers and health insurers face similar scrutiny. Drug price control referenda have passed in several states and a federal cap was included in the Inflation Reduction Act.

The reality is this: the entire U.S. health system is on trial in the court of public opinion for ‘careless disregard for affordability’. And hospitals are seen as part of the problem justifying consolidation as a defense mechanism.

What followed in this 3-hour hearing was testimony from 3 experts critical of hospital consolidation, a Colorado community hospital CEO who opined to competition with big hospital systems and a Peterson Foundation spokesperson who offered that data access and transparency are necessary to mitigate consolidation’s downside impact.

None of their testimony was surprising. Nor were questions from the 25 members of the committee. It’s a narrative that played out in House Energy and Commerce and Ways and Means Committee hearings last month. It’s likely to continue.

Often, Congressional Hearings on healthcare issues amount to little more than political theatre. In this one, four key themes emerged:

Consolidation among hospitals has adversely impacted quality of care and affordability of healthcare. Prices have gone up without commensurate improvements in quality harming consumers.

Larger organizations use horizontal and vertical integration to strengthen their positions relative to smaller competitors. Physician employment by hospitals is concerning. Rural and safety net hospitals are impaired most.

Anti-trust efforts, price transparency mandates, data sharing and value-based programs have not been as effective as anticipated.

Physicians are victims of consolidation and corporatization in U.S. healthcare. They’re paid less because others are paid more.

While committee members varied widely in the intensity of their animosity toward hospitals, a consensus emerged that the hospital status quo is not working for voters and consumers.

My take:

Consolidation is part of everyday life. Last Tuesday’s bombshell announcement of the merger of the PGA Tour and the Saudi Arabia’s Public Investment Fund caught the golfing world by surprise. Anti-trust issues and monopolistic behaviors are noticed by voters and lawmakers. Hospital consolidation is no exception festering suspicions among lawmakers and voters that the public’s good is ill-served. And studies showing that charity care among not-for-profit hospitals is lower than for-profit confuse and complicate.

As I listened to the hearing, I had questions…

Were all relevant perspectives presented?

Was the information provided by witnesses and cited in Committee member questioning accurate?

Will meaningful action result?

But having testified before Congressional Committees, I find myself dismissive of most hearings which seem heavy on political staging but light on meaningful insight. Many are little more than political theatre. Hospital consolidation seems different. There seems to be growing consensus that it’s harmful to some and costly to all.

Sadly, this hearing is the latest evidence that the good will built by hospital heroics in the pandemic is now forgotten. It’s clear hospital consolidation is an issue that faces strong and increased headwinds with evidence mounting—accurate or not– showing more harm than good.

BJC HealthCare of St. Louis and Saint Luke’s Health System of Kansas City are exploring a merger that would yield a 28-hospital, $10 billion, integrated, academic health system, the nonprofits announced Wednesday.

The two have signed a nonbinding letter of intent and “are working toward reaching a definitive agreement in the coming months” with a targeted close before the end of the year, they said. The cross-market deal would be subject to regulatory review and other customary closing conditions.

“Together with Saint Luke’s, we have an exciting opportunity to reinforce our commitment to providing extraordinary care to Missourians and our neighboring communities,” BJC HealthCare President and CEO Richard Liekweg said in the announcement. “Amid the rapidly changing health care landscape, this is the right time to build on our established relationship with Saint Luke’s. With an even stronger financial foundation, we will further invest in our teams, advance the use of technologies and data to support our providers and caregivers and improve the health of our communities.”

Both systems are based in Missouri but “serve distinct geographic markets,” they said.

St. Louis-based BJC Healthcare’s footprint is spread across the greater St. Louis, southern Illinois and southeast Missouri regions. It comprises 14 hospitals including two (Barnes-Jewish and St. Louis Children’s) affiliated with Washington University School of Medicine. It also operates multiple health service organizations providing home health, long-term care, workplace health and other offerings.

Kansas City, Missouri-based Saint Luke’s is a faith-based system with 14 hospitals and more than 100 offices throughout western Missouri and parts of Kansas. It also provides home care and hospice, adult and children’s behavioral care and a senior living community.

Should the deal close, both systems would continue to serve their existing markets and maintain their branding. The joined organization would be run from dual headquarters with BJC’s Liekweg as CEO but an initial board chair hailing from Saint Luke’s.

The organizations said their combination will expand the services available to patients and provide an estimated $1 billion in annual community benefits. The arrangement would also fuel clinical and academic research while supporting greater workforce investment.

“Our integrated health system, with complementary expertise and team of world-class physicians and caregivers, will set a new national standard for medical education and research,” Saint Luke’s President and CEO Melinda Estes, M.D., said in the announcement. “Through our decade-long relationship as a member of the BJC Collaborative, we’ve established mutual trust and respect, so the opportunity to come together as a single integrated system that can accelerate innovation to better serve patients is a logical next step.”

Years of health system consolidation have led to increased scrutiny from regulators and lawmakers, who have worried that mergers can harm competition. To date, however, efforts to block announced deals have been limited to situations where the parties are operating in the same geographic markets.

Larger, cross-market deals like BJC and Saint Luke’s have become more common in the past year, potentially due to the opportunity to distribute operational risks with limited regulatory scrutiny, analysts have noted.

Multiple health policy researchers have warned that these deals are relatively understudied and, according to some prior analyses, very rarely translate to the quality and consumer cost savings often touted by health systems.

Pennsylvania unions have filed a complaint with the Department of Justice alleging integrated hospital giant UPMC is abusing its dominant market position to suppress wages and retain workers.

On Thursday, SEIU Healthcare Pennsylvania and a coalition of labor unions filed a 55-page complaint against UPMC, the largest private employer in the state, saying the hospital system’s size has allowed it to stamp out wage growth, “drastically increase” workload and keep workers from departing to other jobs.

The unions are asking federal regulators to investigate UPMC for antitrust violations, citing its dominance of the healthcare market in select regions of Pennsylvania. UPMC denied allegations of wage suppression.

Dive Insight:

The Pittsburgh-based system has seen a rise in labor complaints, according to the unions, as the system has grown into its 41-hospital footprint through a series of mergers and acquisitions. UPMC, which also operates 800 doctors offices and clinics and a handful of health insurance offerings, reported $26 billion in operating revenue last year.

Attempts in the last decade to organize UPMC’s hourly workers have been unsuccessful, according to SEIU.

Matt Yarnell, president of SEIU Healthcare Pennsylvania, called the complaints groundbreaking on a Thursday call with reporters, saying that no entity has ever filed a complaint arguing that mobility restrictions and labor violations are anticompetitive, and in violation of antitrust law.

The complaint alleges that, for every 10% increase in market share, the wages of UPMC workers falls 30 to 57 cents an hour on average. UPMC hospital workers face an average 2% wage gap compared to non-UPMC facilities, according to a study cited in the complaint.

In addition, the labor groups allege that UPMC’s staffing ratios have fallen over the past decade, resulting in its staffing ratios being 19% lower on average compared with non-UPMC care sites as of 2020.

The unions are going after UPMC for being a “monopsony,” or a company that controls buying in a given marketplace, including controlling a large number of jobs. UPMC has some 92,000 workers, according to the complaint, and has cut off avenues of competition through non-compete agreements, in addition to preventing employees from unionizing.

“If, as we believe, UPMC is insulated from competitive market pressures, it will be able to keep workers’ wages and benefits — and patient quality — below competitive levels, while at the same time continually imposing further restraints and abuses on workers to maintain its market dominance,” the complaint states. “Because we believe this conduct is contrary to Section 2 of the Sherman Act, we respectfully urge the Department of Justice to investigate UPMC and take action to halt this conduct.”

In response to the allegations, UPMC said it has the highest entry-level pay of any provider in the state, and offers “above-industry” employee benefits. UPMC’s average wage is more than $78,000, Paul Wood, UPMC’s chief communications officer, told Healthcare Dive in a statement.

“There are no other employers of size and scope in the regions UPMC serves that provide good paying jobs at every level and an average wage of this magnitude,” Wood said.

Healthcare workers are increasingly pushing for better working conditions and pay amid the COVID-19 pandemic, as hospitals grapple with recruitment and retention issues driven by burnout and heightened labor costs.

In the mid-1980’s, managed care advocate Dr. Paul Ellwood predicted that eventually, US healthcare would be dominated by perhaps a dozen vast national firms he called SuperMeds that would combine managed care based health insurance with care delivery systems. Ellwood was a leader of the “managed competition” movement which advocated for a private sector alternative to a federal government-run National Health Insurance system. Ellwood and colleagues believed that Kaiser Foundation Health Plans and other HMOs would be able to stabilize health costs and thus affordably extend care to the uninsured.

The US political system and market dynamics would not co-operate with Ellwood and his Jackson Hole Group’s vision. In the ensuing thirty-five years, healthcare has remained both highly fragmented and regional in focus. However, unbeknownst to most, during the past decade, as a result of a major merger and relentless smaller acquisitions, two SuperMeds were born- CVS/Aetna and UnitedHealth Group, that whose combined revenues comprise 14% of total US health spending.

CVS/Aetna is slightly larger than United, by dint of grocery sales in its drugstores and its vast Caremark pharmacy benefits management business. However, CVS’s Aetna health insurance arm is one third the size of United’s, and though CVS is rapidly scaling up its care delivery apparatus through its in-store Health Hubs, it remains is a tiny fraction of United’s care footprint. Despite being slightly smaller at the top line, United’s market capitalization is more than 3.5 times that of CVS.

United’s vast scope is difficult to comprehend because much of it is not visible to the naked eye, and the most rapidly growing businesses are partly nested inside United’s health insurance business.

United employs over 300 thousand people. At $287.6 billion total revenues in 2021, United exceeded 7% of total US health spending (though $8.3 billion are from overseas operations).

In 2021, United was $100 billion larger than the British National Health Service. It is more than three times the size of Kaiser Permanente, and five times the size of HCA, the nation’s largest hospital chain. United is both larger and richer than energy giant Exxon Mobil. United has over $70 billion in cash and investments, and is generating about $2 billion a month in operating cash flow.

Its highly regulated health insurance business is the visible tip of a rapidly growing iceberg. Revenue from United’s core health insurance business grew at 11% in 2021, compared to 14% growth in United’s diversified Optum subsidiary. Optum generated $155.6 billion in 2021 (of which 60% were from INSIDE United’s health insurance business). You can see the relationship of Optum’s three major businesses to United’s health insurance operations in Exhibit I.

Optum is the Key to United’s Growth

Understanding the role of Optum is key to understanding United’s business. It is remarkable how few of my veteran health care colleagues have any idea what Optum is or what it does. Optum was once a sort of dumping ground for assorted United acquisitions without a seeming core purpose. A private equity colleague once derided Optum as “The Island of Lost Toys”. Now, however, Optum is driving United’s growth, and generates billions of dollars in unregulated profits both from inside the highly regulated core health insurance business and from external customers.

Optum consists of three parts:Optum Health, its care delivery enterprise ($54 billion revenues in 2021), Optum Rx, its pharmacy benefits management enterprise ($91 billion revenues in 2021) and Optum Insight, a diversified business services enterprise ($12.2 billion in 2021). Virtually all of United’s acquisitions join one of these three businesses.

Optum Health: The Third Largest Care Delivery Enterprise in the US

By itself, Optum Health is almost the size of HCA ($54 billion in 2021 vs HCA’s $58.7 billion) and consists of a vast national portfolio of care delivery entities: large physician groups, urgent care centers, surgicenters, imaging centers, and now by dint of the recently announced $5.7 billion acquisition of LHC, home health agencies. Optum Health has studiously avoided acquiring beds of any kind: hospitals, nursing homes, etc. and likely will continue to do so. Optum Health’s physician groups not only generate profits on their own, but also provide powerful leverage for United to control health costs for its own subscribers, pushing down United’s highly visible and regulated Medical Loss Ratio (MLR), and increasing health plan profits.

Optum Health began in 2007 when United acquired Nevada-based Sierra Health, and thus became the new owner of a small multispecialty physician group which Sierra owned. The group did not belong in United’s health insurance business and came to rest over in Optum. Over the past twelve years, Optum Health has acquired an impressive percentage of the major capitated medical groups in the US- Texas’ WellMed, California’s HealthCare Partners (from DaVita), as well as Monarch, AppleCare and North American Medical Management, Massachusetts’ Reliant (formerly Fallon Clinic) and Atrius in Massachusetts (pending) , Kelsey Seybold Clinic (also pending) in Houston, TX and Everett Clinic and PolyClinic in Seattle.

Optum Health claims over 60 thousand physicians, though many of these are actually independent physicians participating in “wrap around” risk contracting networks. By comparison, Kaiser Permanente’s Medical Groups employ about 23 thousand physicians. United’s management claims that Optum Health provides continuing care to about 20 million patients, of whom 3 million are covered by some form of so-called “value based” contracts. Perhaps half of this smaller number are covered by capitated (percentage of premium-PMPM) contracts.

Optum Health straddles fierce competitive relationships between United’s health insurance business and competing health plans in well more than a dozen metropolitan areas. Almost half (44%) of Optum Health’s revenues come from providing care for health plans other than United.

When Optum acquires a large physician group, it acquires those groups’ contracts with United’s health insurance competitors, some of which contracts have been in place for decades. Premium revenues from other health plans, presumably capitation or per member per month (PMPM) revenues, are one-quarter of Optum Health’s $54 billion total revenues. These “external” premium revenues have quadrupled since 2018, largely for Medicare Advantage subscribers. Optum Health contributes about $4.5 billion in operating profit to United. It is impossible to determine from United’s disclosures how much of this profit comes from Optum Health’s services provided to United’s insured lives and how much from its medical groups’ extensive contracts with competing health plans.

Optum Health’s surgicenters and urgent care centers provide affordable alternatives to using expensive hospital outpatient services and emergency departments, potentially further reducing United medical expense. This creates obvious tensions with United’s hospital networks, since Optum Health can use its large medical practices and virtual care offerings to divert patients from hospitals to its own services, or else render those services unnecessary.

Though some observers have termed Optum/United’s business model “vertical integration”-ownership of the suppliers to and distributors of a firm’s product– Optum Health has actually grown less vertical since 2018, with revenues from competing health plans growing from 36% of total revenues in 2018 to 44% in 2021. A 2018 analysis by ReCon Strategy found at best a sketchy matchup between United’s health plan enrollment by market and its Optum Health assets (https://reconstrategy.com/2018/04/uniteds-medicare-advantage-footprint-and-optumcare-network-do-not-overlap-much-so-far/.

Optum Rx: The Nation’s Third Largest Pharmacy Benefits Management Business

Optum’s largest business in revenues is its Optum Rx pharmaceutical benefits management (PBM) business, which generates $91 billion in revenues, and processes over a billion pharmacy claims not only for United but also many competing insurers and employer groups. Pharmaceutical costs are a rapidly growing piece of total medical expenses, and controlling them is yet another source of largely unregulated profits for United; Optum Rx generated over $4.1 billion of operating profit in 2021.

Optum Rx is the nation’s third largest PBM business after Caremark, owned by CVS/Aetna and Express Scripts, owned by CIGNA, and processes about 21% of all scripts written in the US. Pharmacy benefits management firms developed more than two decades ago to speed the conversion of patients from expensive branded drugs to generics on behalf of insurers and self-funded employers. They were given a big boost by George Bush’s 2004 Medicare Part D Prescription Drug benefit, as a “pro-competitive” private sector alternative to Medicare directly negotiating prices with pharmaceutical firms.

Reducing drug spending is one key to United’s profitability. Since generics represent almost 90% of all prescriptions written, Optum Rx now relies on fees generated by processing prescriptions and on rebates from pharmaceutical firms to promote their costly branded drugs as preferred drugs on Optum Rx’s formularies. These rebates are determined based on “list” prices for those drugs vs. the contracted price for the PBMs, and are actual cash payments from manufacturers to PBMs.

Drug rebates represent a significant fraction of operating profits for health insurers that own PBMs, particularly for their older Medicare Advantage patients that use a lot of expensive drugs. Unfortunately, PBMs have incentives to inflate the list price, because rebates are caculated based on the spread between list prices and the contract pricel Unfortunately, this increases subscribers’ cash outlays, because patient cost shares are based on list prices.

Optum Rx generates about 39% of its revenues (and an undeterminable percentage of its profits) serving other health insurers and self-funded employers. Many of those self-funded employers demand that Optum pass through the rebates directly to them (even if it means being charged higher administrative fees!).

Unlike the situation with Optum Health, the “verticality” of Optum’s PBM business-the percentage of Optum revenues derived from serving United subscribers- has increased in the last seven years, to more than 60% of Optum Rx’s total business. What happens to the billions of dollars in rebates generated by Optum Rx is impossible to determine from United’s disclosures. However, our best guess is that pharmaceutical rebates represent as much as a quarter of United’s total corporate profits.

Optum Insight: “Intelligent” Business Solutions

The fastest growing and by far the most profitable Optum business is its business intelligence/business services/consulting subsidiary. Optum Insight was generated $12.2 billion in revenues in 2021, but a 27.9% operating margin, five times that of United’s health insurance business. Optum Insight is strategically vital to enhancing the profitability of United’s health insurance activities, but also generates outside revenues selling services to United’s health insurance competitors and hospital networks.

The core of Optum Insight is a business intelligence enterprise formerly known as Ingenix, which provided “big data” to United and other insurers about hospital and pricing behavior and utilization-crucial both for benefits design and administration. In 2009, Ingenix was accused by New York State of under reporting prices for out of network health services for itself and its clients, which had the effect of reducing its own medical reimbursements, and increasing patient cost shares. United signed a consent decree to alter Ingenix business practices and settled a raft of lawsuits filed on behalf of patients, physicians and employers. Its name was subsequently changed to Optum Insight.

By dint of aggressive acquisitions, Optum Insight has dramatically increased its medical claims management business, consulting services and business process outsourcing activities. . Most of United’s investment in artificial intelligence can be found inside Optum Insight. Big data plays a crucial role in United’s overall strategy. Optum Insight’s claims management software uses vast medical claims data bases and artificial intelligence/machine learning software to spot and deny medical claims for which documentation is inadequate or where services are either “inappropriate” or else not covered by an individual’s health plan. Providers also claim that the same software rejects as many as 20% of their claims, often for problems as tiny as a mis-spelled word or a missing data field.

Optum Insight software plays a crucial role in helping United’s health insurance plans manage their medical expense. Traditional health plan profitability is generated by reducing medical expense relative to collected premiums to increase underwriting profit. These profits are regulated, with highly variable degrees of rigor by state health insurance commissioners, and also by provisions of ObamaCare enacted in 2010.

Though its acquisition of Equian in 2019 and the proposed $13 billion acquisition of health information technology conglomerate Change Healthcare in 2021, United came within an eyelash of a near monopoly on “intelligent” medical claims processing software. The Justice Department challenged this latter acquisition and United may agree to divest Change’s claims processing software business as a condition of closing the deal. Even without the Change acquisition, Optum Insight processes hundreds of millions of medical claims annually not only for United’s health insurance business but for many of United’s competitors.

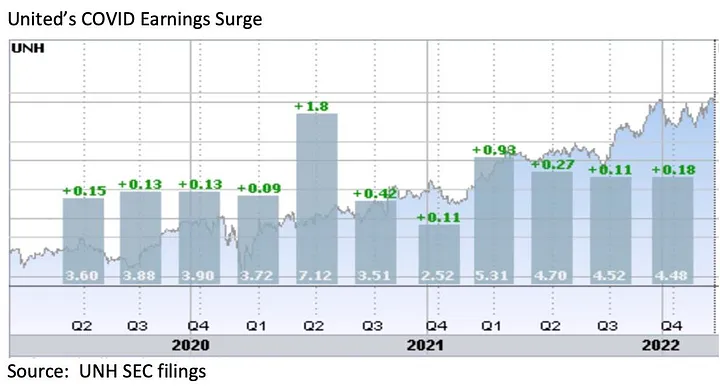

However, Optum Insight’s claims management system can also be used to increase MLR if medical expense unexpectedly declines, exposing the firm to federal requirement that it rebate excessive ‘savings’ to subscribers. This happened in 2020, when the COVID pandemic dramatically and unexpectedly added billions to United’s earnings due to hospitals suspending elective care. The chart below shows United’s 2Q2020 earnings per share almost doubling due to the precipitous drop in its medical claims expenses!

Hospital finance colleagues reported an immediate and substantial drop in medical claims denials from United and other carriers in the summer and fall of 2020. United’s quarterly profits dutifully and steeply declined in the subsequent two quarters, because its medical expenses sharply rebounded. The rise in

United’s medical expenses helped the firm avoid premium rebates to patients required by provisions of the ObamaCare legislation passed in 2010. The firm did voluntarily rebate about $1.5 billion to many of its customers in June, 2020.

However the most rapidly growing part of Optum Insight is its Optum 360 business process outsourcing business, which helps hospitals manage their billing and collections revenue cycle, as well as information technology operations, supply chain (purchasing and materials management) and other services. Through Optum 360, Optum Insight has signed five long term master contracts in the past two years’ worth many billions of dollars with care providers in California, Missouri and other states to provide a broad range of business services.

With all these different businesses, it is theoretically possible for one piece of Optum to be reducing a hospital’s cash flow by denying medical claims for United subscribers, while United’s health insurance network managers bargain aggressively to reduce the hospital’s reimbursement rates while yet another piece of Optum runs the billing and collection services for the same hospital and its employed physicians, while yet another piece of Optum competes with the hospital’s physicians and ambulatory services, diverting patients from its ERs and clinics, reducing the hospital’s revenues.

It is not difficult to imagine a future in which Optum/United offers hospital systems an Optum 360 outsourcing contract that run most of the business operations of a hospital system in exchange for preferred United health plan rates, an AI-enabled EZ pass on its medical claims denials and inpatient referrals from Optum physician groups and urgent care centers, at the expense of competing hospitals.

Managing these potential conflicts will be an increasing challenge as these various businesses grow, placing intense pressure on United’s leadership to get the various pieces of United to work together. To many anxious hospital executives, United resembles nothing so much as the Kraken, rising up out of the sea, surrounding and engulfing them- a powerful friend perhaps or a fearsome foe. As you might expect, United’s growing market power and growth has generated a fierce backlash in the hospital management community.

What Business is United Healthcare In?

United Healthcare is the most successful business in the history of American healthcare. The rapid growth of Optum and continued health insurance enrollment growth from government programs like Medicaid and Medicare has created a cash engine which generates nearly $2 billion a month in free cash flow. Optum’s portfolio has given United an impressive array of tools, unequalled in the industry, to improve its profitability and to reach into every corner of the US health system. United Healthcare is managed care on steroids.

United’s diversified portfolio of businesses gives the firm what a finance-savvy colleague termed “optionality”- the ability to redirect capital and management attention to areas of growth and away from areas that have ceased to grow, in the US or overseas. With its substantial investable capital, it will have the pick of the litter of the 11 thousand digital health companies as the overextended digital health market consolidates. United will be able to use its vast resources to build state-of-the-art digital infrastructure to reach and retain patients and manage their care.

United’s main short term business risks seem to be running out of accretive transactions effectively to deploy its growing horde of capital and managing the firm’s rising political exposure. United has had tremendous business discipline and has shied away from speculative acquisitions that are not immediately accretive to earnings. If its earnings growth falters, however, it will also encounter pressure from the investment community to increase dividends (presently about 1.2%) or share buybacks to bolster its share price, or else divest some or all of Optum in order to “maximize shareholder value”.

Answering the question, “What Business is United In” is simple: just about everything in health but hospitals and nursing homes.

Answering the questions- who are its customers and what do they want? — is a great deal harder. The customers United serves are in a sort of cold war with one another. United’s original business was protecting employers from health cost growth , and tempering the influence of hospitals and doctors by reducing their rates and utilization. By fostering so-called Consumer Directed Health Plans that expose many of their subscribers to very high front-end copayments, United and its health insurance brethren, have also increased their out-of-pocket costs, whether they have the savings to pay them or not.

There are also some ironies in United’s development. Optum Insight’s suite of hospital business services are designed to reduce administrative costs created in major part by United and other insurers’ medical claims data requirements. Its PBM business, originally intended to reduce drug spending by bargaining aggressively with pharmaceutical manufacturers has ended up pushing up drug list prices and consumer cost shares.

While presumably everybody benefits if United can somehow help patients become and remain healthy, it is still far from obvious how to do this. Managing all these markedly divergent customer needs will be a tremendous management challenge for whoever succeeds United’s reclusive (and very effective) 70 year old Chairman Stephen Hemsley.

What Does Society Get from this Vast Enterprise?

However, as Peter Drucker told a different generation of business giants, businesses are not entities unto themselves, accountable only to shareholders and customers. They are organs of society, and are expected to create social value. Americans are suspicious of vast enterprises, as businesses from Standard Oil, US Steel and ATT to Microsoft and Facebook have learned. As businesses grow and become more successful, public suspicion grows.

Private health insurers already face strident opposition from progressive Democrats, who believe that health coverage ought to be a public good, a right of citizenship provided publicly; in other words, that private health insurers have no business being in business. And large insurers like United also face intense opposition from hospitals and many physicians because they reduce their incomes and impose major administrative burdens upon them.

In the age of Twitter and TikTok, United is highly vulnerable to “event risks” that confirm the hostile narratives of the firm’s detractors that United is mainly about maximizing its own profits, not about improving the health of its subscribers or the communities it serves. It is not clear how many the tens of millions of United subscribers have warm and fuzzy feelings about their giant health insurer. Memories of the HMO backlash of the 1990’s reside in the firm’s corporate memory.

United has grown to its present immense scale largely without public knowledge. United has within its reach the capability of constraining overall health cost growth across dozens of metropolitan areas and regions, not merely cost growth for its own beneficiaries (roughly one in seven US citizens already get their health insurance through United). With its expanding digital health operations, it can deploy state of the art tools for helping United’s 50 million subscribers avoid illness and live healthier lives.

United also has the ability to damage the financial operations of beloved local hospitals and deny coverage to families, raising their out of pocket expenses. How United frames and defends its social mission and how it manages all the delicate and increasingly fraught customer relationships will determine its future, and in important ways, ours as well.