Companies are avoiding hard layoffs but still cutting jobs by reassigning employees to different roles — a trend dubbed “quiet cutting,”The Wall Street Journal reported Aug. 27.

From August 2022 to August 2023, mentions of “reassignment” or similar phrasing during company earnings calls more than tripled, according to data from financial research platform Alphasense. Companies that have embraced large-scale reassignments include Adidas, IBM, Adobe and Salesforce. In healthcare, at least 20 health systems have announced changes to executive ranks and leadership teams this year.

“Reassigning is definitely a huge part of the dynamic right now,” Andy Challenger, senior vice president at executive coaching firm Challenger, Gray & Christmas told the Journal.

Reassignments can be a strategic way for companies to cut costs by placing top talent — that they previously spent significant amounts of money on to recruit — in new roles that are better suited to help them meet future organizational goals. In many cases, reassignments could be a way for companies to avoid letting people go. On the other hand, it could be a soft nudge to get employees to quit, executive coaches and advisers told the Journal.

“They could be putting you out to pasture,” said Roberta Matuson, executive coach and adviser on human resources matters to businesses such as General Motors and Microsoft.

For employees to gauge whether a reassignment is a genuine move to avoid letting them go or a subtle push out the door, experts said they should consider whether the reassigned role is far below the pay and experience level of their original job, and whether the reassignment requires a big move when their employer knows relocation is not a realistic option, according to the Journal.

A number of hospitals and health systems are trimming their workforces or jobs due to financial and operational challenges.

Below are workforce reduction efforts or job eliminations that were announced within the past year and/or take effect later in 2023.

Editor’s Note: This webpage was updated Aug. 10 and will continue to be updated. Stories are listed under the month they were reported on by Becker’s.

August

The University of Arkansas for Medical Sciences is laying off 51 workers in support services, administration and service lines. Some previously open positions will also be left vacant, the Little Rock-based institution told the Becker’s in a prepared statement. Some job duties will be reassigned.

Springfield, Ill.-based Memorial Health is laying off hundreds of employees, including 20 percent of leadership positions. Affected employees represent 5 percent of Memorial’s total salary and benefits, according to a statement provided to Becker’s. The cuts focused on system leadership, administrative and support sectors.

Boone Health, a county-owned system based in Columbia, Mo., will cut 62 jobs, most of which are unfilled. Fifteen of the 62 positions are held by existing employees.

The in-home care arm of Syracuse, N.Y.-based St. Joseph’s Health, part of Livonia, Mich.-based Trinity Health, is closing in October, pending the discharge of all patients. The closure includes the termination of 71 employees. Mark McPherson, president and CEO of Trinity Health At Home, said 63 full and part-time positions are being eliminated, while the remaining eight were contingent positions.

July

Chapel Hill, N.C.-based UNC Health will lay off 246 employees. The reduction will occur after the organization ends services at a behavioral health facility in Raleigh on Sept. 30, according to a WARN notice filed July 21 with the North Carolina Department of Commerce.

Philadelphia-based Jefferson Health is reducing its workforce by about 400 positions. The reduction represents approximately 1 percent of the workforce.

Tupelo-based North Mississippi Health Services is moving forward with layoffs and job reassignments as part of its “redesign” plan to improve the organization’s financial picture, according to a message sent to NMHS employees and affiliated providers July 19. NMHS did not provide the number of affected positions or types of positions affected.

Allina Healthbegan layoffs affecting about 350 team members throughout the Minneapolis-based organization. The health system said the layoffs began July 17 and that most of the affected jobs are leadership and non-direct caregiving roles.

Middletown, N.Y.-based Garnet Healthlaid off 49 employees, including 25 leaders. The reductions represent 1.13 percent of the organization’s total workforce.

June

Coral Gables-based Baptist Health South Florida is offering its executives at the director level and above a “one-time opportunity” to apply for voluntary separation, according to a June 29 Miami Herald report. Decisions on buyout applications will be made during the summer.

MultiCare Health System, a 12-hospital organization based in Tacoma, Wash., will lay off 229 employees, or about 1 percent of its 23,000 staff members, including about two dozen leaders, as part of cost-cutting efforts, the health system said June 29. The layoffs primarily affect support departments, such as marketing, IT and finance.

Greensburg, Pa.-based Independence Health Systemlaid off 53 employees and has cut 226 positions — including resignations, retirements and elimination of vacant positions — since January, The Butler Eagle reported June 28. The 226 reductions began at the executive level, with 13 manager positions terminated in March.

Billings (Mont.) Clinic will lay off workers as part of a restructuring plan to address financial and operational headwinds in today’s healthcare environment, the organization confirmed. The layoffs are expected to affect approximately 27 or fewer positions.

Melbourne, Fla.-based Health First is eliminating some positions and leaving open ones vacant, Florida Today reported June 21. Seventeen jobs will be cut and 36 will be left unfilled, according to Paula Just, the health system’s chief experience officer.

Pittsburgh-based Highmark Healthlaid off 118 employees on June 21, including two from Allegheny Health Network, a spokesperson for the health system told Becker’s. The layoffs follow the health system’s cutbacks in March and April, according to the Pittsburgh Business Times. Highmark laid off 141 workers earlier this year.

Vibra Hospital of Western Massachusetts, a long-term-acute care hospital in Springfield, will lay off 87 employees by Aug. 15 ahead of the facility’s planned closure. About 30 patients will be relocated to Baystate Health’s Valley Springs Behavioral Health Hospital in Holyoke, Mass., which will open in August.

Cortez, Colo.-based Southwest Memorial Hospitallaid off nine people to help ensure the hospital is staffed appropriately, and create financial stability for the future, a spokesperson confirmed to Becker’s. The spokesperson, Chuck Krupa, said the layoffs occurred June 14 and included administrative workers. No bedside care positions were affected.

Henry Mayo Newhall Hospital in Valencia, Calif., is making “a little over 100” layoffs amid financial challenges, spokesperson Patrick Moody confirmed to Becker’s. Mr. Moody said the layoffs affect workers “in a wide range of hospital departments.” This includes some management-level employees. The hospital, which has about 1,800 employees total, is not providing specific numbers for specific job titles or departments.

Dartmouth Health is laying off 75 workers and eliminating 100 job vacancies. The layoffs came after the Lebanon, N.H.-based health system implemented a performance improvement plan in November.

Seattle Children’s is eliminating 135 leader roles, citing financial challenges. The management restructuring and reduction affects 1.5 percent of employees across the organization.

White Rock (Texas) Medical Centerlaid off 30 workers across 28 departments. The layoffs include clinical and administrative roles.

Jackson, Miss.-based St. Dominic Health Services is laying off 157 workers and ending behavioral health services. The reduction represents 5.5 percent of the hospital’s workforce.

Danville, Pa.-based Geisinger laid off 47 employees from its IT department. The reduction is part of a restructuring plan to offset high labor and supply costs.

Cascade Behavioral Health Hospital in Tukwila, Wash., is winding down operations and laying off 288 employees. The 137-bed psychiatric facility is slated to close by July 31.

Cambridge (Mass.) Health Alliance is laying off 69 employees, reducing the hours of 15 others and eliminating 170 open positions, according to The Boston Globe. The reductions are primarily in management, administrative and support areas, a health system spokesperson told Becker’s.

May

Wenatchee, Wash.-based Confluence Health has eliminated its chief operating officer amid restructuring efforts and financial pressures, the health system confirmed to Becker’s May 16.

Conemaugh Memorial Medical Center, a Duke LifePoint hospital in Johnstown, Pa., has laid off less than 1 percent of its workforce, the hospital confirmed to Becker’s May 15.

Community Health Network, a nonprofit health system based in Indianapolis, plans to cut an unspecified number of jobs as it restructures its workforce and makes organizational changes. The health system confirmed the job cuts in a statement shared with Becker’s on May 11. It did not say how many jobs would be cut or which positions would be affected.

New Orleans-based Ochsner Healtheliminated 770 positions, or about 2 percent of its workforce, on May 11. This is the largest layoff to date for the health system.

Cedars-Sinai Medical Centereliminated the positions of 131 employees and cut about two dozen other jobs at related Cedars-Sinai facilities, a spokesperson confirmed via a statement shared with Becker’s May 7. The Los Angeles-based organization said reductions represent less than 1 percent of the workforce and apply to management and non-management roles primarily in non-patient care jobs.

Rochester (N.Y.) Regional Health is eliminating about 60 positions. A statement from RRH said the changes affect less than one-half percent of the system population, mostly in nonclinical and management positions.

Memorial Health Systemlaid off fewer than 90 people, or less than 2 percent of its workforce.The Gulfport, Miss.-based health system said May 2 that most of the affected positions are nonclinical or management roles, and the majority do not involve direct patient care.

Monument Healthlaid off at least 80 employees, or about 2 percent of its workforce. The Rapid City, S.D.-based system said positions are primarily corporate service roles and will not affect patient services. Unfilled corporate service positions were also eliminated.

April

Habersham Medical Center in Demorest, Ga., laid off four executives. The layoffs are part of cost-cutting measures before the hospital joins Gainesville-based Northeast Georgia Health System in July, nowhaberbasham.com reported April 27.

Scripps Health is eliminating 70 administrative roles, according to WARN documents filed by the San Diego-based health system in March. The layoffs take effect May 8 and affect corporate positions in San Diego and La Jolla, Calif.

Trinity Health Mid-Atlantic, part of Livonia, Mich.-based Trinity Health, eliminated fewer than 40 positions, a spokesperson confirmed to Becker’s April 24. The layoffs represent 0.5 percent of the health system’s approximately 7,000-person workforce.

PeaceHealtheliminated 251 caregiver roles across multiple locations. The Vancouver, Wash.-based health system said affected roles include 121 from Shared Services, which supports its 16,000 caregivers in Washington, Oregon and Alaska.

Toledo, Ohio-based ProMedicaplans to lay off 26 skilled nursing support staff. The layoffs, effective in June, affect 20 employees who work remotely across the U.S, and six who work at the ProMedica Summit Center in Toledo, according to a Worker Adjustment and Retraining Notification filed April 18. Most affected positions support sales, marketing and administrative functions for the skilled nursing facilities, Promecia told Becker’s.

Northern Inyo Healthcare District, which operates a 25-bed critical access hospital in Bishop, Calif., anticipates eliminating about 15 positions, or less than 4 percent of its 460-member workforce, by April 21, a spokesperson confirmed to Becker’s. The layoffs include nonclinical roles within support and administration, according to a news release. No further details were provided about specific positions affected.

West Reading, Pa.-based Tower Health is eliminating 100 full-time equivalent positions. The move will affect 45 individuals, according to an April 13 news release the health system shared with Becker’s. The other 55 positions are either recently vacated or involve individuals who plan to retire in the coming weeks and months.

Grand Forks, N.D.-based Altru Health is trimming its executive team as its new hospital project moves forward. The health system is trimming its executive team from nine to six and incentivizing 34 other employees to take early retirement.

Tacoma, Wash.-based Virginia Mason Franciscan Healthlaid off nearly 400 employees, most of whom are in non-patient-facing roles. The job cuts affected less than 2 percent of the health system’s 19,000-plus workforce.

Katherine Shaw Bethea Hospital in Dixon, Ill., will lay off 20 employees, citing financial headwinds affecting health organizations across the U.S. It will also leave other positions unfilled to reduce expenses amid rising labor and supply costs and reductions in payments by insurance plans. Affected employees largely work in administrative support areas and not direct patient care.

Danbury, Conn.-based Nuvance Health will close a 100-bed rehabilitation facility in Rhinebeck, N.Y., resulting in 102 layoffs. The layoffs are effective April 12, according to the Daily Freeman.

March

Charleston, S.C.-based MUSC Health University Medical Centerlaid off an unspecified number of employees from its Midlands hospitals in the Columbia, S.C. area. Division President Terry Gunn also resigned after the facilities missed budget expectations by $40 million in the first six months of the fiscal year, The Post and Courier reported March 30.

Winston-Salem, N.C.-based Novant Healthlaid off about 50 workers, including C-level executives, the health system confirmed to Becker’s March 29. The layoffs affected Jesse Cureton, the health system’s executive vice president and chief consumer officer since 2013; Angela Yochem, its executive vice president and chief transformation and digital officer since 2020; and Paula Dean Kranz, vice president of innovation enablement and executive director of the Novant Health Innovation Labs.

Penn Medicine Lancaster (Pa.) General Health eliminated fewer than 65 jobs, or less than 1 percent of its workforce of about 9,700, the health system confirmed to Becker’s March 30. The layoffs include support, administrative and executive roles, and COVID-19-related support staff, spokesperson John Lines said, according to lancasteronline.com. Mr. Lines did not provide a specific number of affected workers.

McLaren St. Luke’s Hospital in Maumee, Ohio, will lay off 743 workers, including 239 registered nurses, when it permanently closes this spring. Other affected roles include physical therapists, radiology technicians, respiratory therapists, pharmacists and pharmacy support staff, and nursing assistants. The hospital’s COO is also affected, and a spokesperson for McLaren Health Care told Becker’s other senior leadership roles are also affected.

Bellevue, Wash.-based Overlake Medical Center and Clinicslaid off administrative staff, the health system confirmed to the Puget Sound Business Journal. The layoffs, which occurred earlier this year, included 30 workers across Overlake’s human resources, information technology and finance departments, a spokesperson said, according to the publication. This represents about 6 percent of the organization’s administrative workforce. Overlake’s website says it employs more than 3,000 people total.

Columbia-based University of Missouri Health Care is eliminating five hospital leadership positions across the organization, spokesperson Eric Maze confirmed to Becker’s March 20. Mr. Maze did not specify which roles are being eliminated saying that the organization won’t address individual personnel actions. According to MU Health Care, the move is a result of restructuring “to better support patients and the future healthcare needs of Missourians.”

Greensboro, N.C.-based Cone Healtheliminated 68 senior-level jobs. The job eliminations occurred Feb. 21, Cone Health COO Mandy Eaton told The Alamance News. Of the 68 positions eliminated, 21 were filled. Affected employees were offered severance packages.

The newly merged Greensburg, Pa.-based organization made up of Excela Health and Butler Health Systemeliminated 13 filled managerial jobs. The affected employees and positions are from across both sides of the new organization, Tom Chakurda, spokesperson for the Excela-Butler enterprise, confirmed to Becker’s. The positions were in various support functions unrelated to direct patient care.

Crozer Health, a four-hospital system based in Upland, Pa., is laying off roughly 215 employees amid financial challenges. The system announced the layoffs March 15 as part of its “operational restructuring plan” that “focuses on removing duplication in administrative oversight and discontinuing underutilized services.” Affected employees represent about 4 percent of the organization’s workforce.

Philadelphia-based Penn Medicine is eliminating administrative positions. The change is part of a reorganization plan to save the health system $40 million annually, the Philadelphia Business Journal reported March 13. Kevin Mahoney, CEO of the University of Pennsylvania Health System, told Penn Medicine’s 49,000 employees last week that changes include the elimination of a “small number of administrative positions which no longer align with our key objectives,” according to the publication. The memo did not indicate the exact number of positions that were eliminated.

Sovah Health, part of Brentwood, Tenn.-based Lifepoint Health, eliminated the COO positions at its Danville and Martinsville, Va., campuses. The responsibilities of both COO roles will now be spread across members of the existing administrative team.

Valley Health, a six-hospital health system based in Winchester, Va., eliminated 31 administrative positions. The job cuts are part of the consolidation of the organization’s leadership team and administrative roles.

Marshfield (Wis.) Clinic Health System said it would lay off 346 employees, representing less than 3 percent of its employee base.

Roseville, Calif.-based Adventist Health plans to go from seven networks of care to five systemwide to reduce costs and strengthen operations. The reorganization will result in job cuts, including reducing administration by more than $100 million.

Arcata, Calif.-based Mad River Community Hospital is cutting 27 jobs as it suspends home health services.

Hutchinson (Kan.) Regional Medical Centerlaid off 85 employees, a move tied to challenges in today’s healthcare environment.

January

Oklahoma City-based OU Healtheliminated about 100 positions as part of an organizational redesign to complete the integration from its 2021 merger.

Memorial Sloan Kettering Cancer Center announced it would lay off to reduce costs amid widespread hospital financial challenges. The layoffs are spread across 14 sites in New York City, and equate to about 1.8 percent of Memorial Sloan’s 22,500 workforce.

St. Louis-based Ascensioncompleted layoffs in Texas, the health system confirmed in January. A statement shared with Becker’s says the layoffs primarily affected nonclinical support roles. The health system declined to specify to Becker’s the number of employees or positions affected.

Chillicothe, Ohio-based Adena Health System announced it would eliminate 69 positions — 1.6 percent of its workforce — and send 340 revenue cycle department employees to Ensemble Health Partners’ payroll in a move aimed to help the health system’s financial stability.

Ascension St. Vincent’s Riverside in Jacksonville, Fla., will end maternity care at the hospital, affecting 68 jobs, according to a Workforce Adjustment and Retraining Notification filed with the state Jan. 17. The move will affect 62 registered nurses as well as six other positions.

Visalia, Calif.-based Kaweah Health said it aimed to eliminate 94 positions as part of a new strategy to reduce labor costs. The job cuts come in addition to previously announced workforce reductions; the health system already eliminated 90 unfilled positions and lowered its workforce by 106 employees.

Oklahoma City-based Integris Health said it would eliminate 200 jobs to curb expenses. The eliminations include 140 caregiver roles and 60 vacant jobs.

Toledo, Ohio-based ProMedica announced plans to lay off 262 employees, a move tied to its exit from a skilled-nursing facility joint venture late last year. The layoffs will take effect between March 10 and April 1.

Employees at Las Vegas-based Desert Springs Hospital Medical Center were notified of layoffs coming to the facility, which will transition to a freestanding emergency department. There are 970 employees affected. Desert Springs is part of the Valley Health System, a system owned and operated by King of Prussia, Pa.-based Universal Health Services.

Philadelphia-based Jefferson Health plans to go from five divisions to three in an effort to flatten management and become more efficient. The reorganization will result in an unspecified number of job cuts, primarily among executives.

December

Pikeville (Ky.) Medical Center said it would lay off 112 employees as it outsources its environmental services department. The 112 layoffs were effective Jan. 1, 2023.

Southern Illinois Healthcare, a four-hospital system based in Carbondale, announced it would eliminate or restructure 76 jobs in management and leadership. The 76 positions fall under senior leadership, management and corporate services. Included in that figure are 33 vacant positions, which will not be filled. No positions in patient care are affected.

Citing a need to further reduce overhead expenses and support additional investments in patient care and wages, Traverse City, Mich.-based Munson Health said it would eliminate 31 positions and leave another 20 jobs unfilled. All affected positions are in corporate services or management. The layoffs represent less than 1 percent of the health system’s workforce of nearly 8,000.

November

West Reading, Pa.-based Tower Health on Nov. 16 laid off 52 corporate employees as the health system shrinks from six hospitals to four. The layoffs, which are expected to save $15 million a year, account for 13 percent of Tower Health’s corporate management staff.

St. Vincent Charity Medical Center in Cleveland closed its inpatient and emergency room care Nov. 11, four days before originally planned — and laid off 978 workers in doing so. After the transition, the Sisters of Charity Health System will offer outpatient behavioral health, urgent care and primary care.

October

Sioux Falls, S.D.-based Sanford Healthannounced layoffs affecting an undisclosed number of staff in October, a decision its CEO said was made “to streamline leadership structure and simplify operations” in certain areas. The layoffs primarily affect nonclinical areas.

Generative AI applications can already help health systems improve margins, yet only 6% have a strategy ready.

At a Glance

In the wake of their most challenging financial year since 2020, US hospitals are desperately searching for margin improvements.

Generative AI can increase productivity and cost efficiency, but only 6% of health systems currently have a strategy.

Leading providers and payers will start with highly focused, low-risk generative AI use cases, generating the funds and experience for more transformative future applications.

While Covid-19 may no longer be dominating the global news cycle, healthcare providers and payers are still feeling its reverberations. More than half of US hospitals ended 2022 with a negative margin, marking the most difficult financial year since the start of the pandemic.

CEOs and CFOs remember the challenges all too well: The Omicron surge halted nonurgent procedures in the first half of the year, government support tapered off, and labor expenses ballooned amid staffing shortages. There was also the record-high inflation that continues to intensify margin pressures today. According to a recent Bain survey of health system executives, 60% cite rising costs as their greatest concern.

Payers and providers are now on the hunt for margin improvements. In our experience, the most successful companies won’t merely reduce costs, but also ramp up productivity. When done right, modest technology investments can accomplish both.

Artificial intelligence (AI) may hold part of the answer. With the costs to train a system down 1,000-fold since 2017, AI provides an arsenal of new productivity-enhancing tools at a low investment.

Many executives recognize the growing opportunity, especially with the recent rise of generative AI, which uses sophisticated large language models (LLMs) to create original text, images, and other content. It’s inspiring an explosion of ideas around use cases, from reviewing medical records for accuracy to making diagnoses and treatment recommendations.

Our survey reveals that 75% of health system executives believe generative AI has reached a turning point in its ability to reshape the industry. However, only 6% have an established generative AI strategy.

It’s time to play offense—or be forced to play defense later. But choosing from the laundry list of generative AI applications is daunting. Companies are at high risk of overinvesting in the wrong opportunities and underinvesting in the right ones, undermining future profitability, growth, and value creation. A wait-and-see approach is a tempting prospect.

However, we believe the next generation of leading healthcare companies will start today, with highly focused, low-risk use cases that boost productivity and cost efficiency. Over the next three to nine months, these companies will improve margins and learn how to implement a generative AI strategy, building up the funds and experience needed to invest in a more transformative vision.

Endless potential—and high hurdles

The excitement around generative AI may feel akin to the hype around other recent digital and technology developments that never quite rose to their promised potential. Well-intentioned, well-informed individuals are debating how much change will truly materialize in the next few years. While developments over the past six months have been a testament to the breakneck speed of change, nobody can accurately predict what the next six months, year, or decade will look like. Will new players emerge? Will we rely on different LLMs for different use cases, or will one dominate the landscape?

Despite the uncertainty, generative AI already has the power to alleviate some of providers’ biggest woes, which include rising costs and high inflation, clinician shortages, and physician burnout. Quick relief is critical, considering that the heightened risk of a recession will only compound margin pressures, and the US could be short 40,800 to 104,900 physicians by 2030, according to the Association of American Medical Colleges.

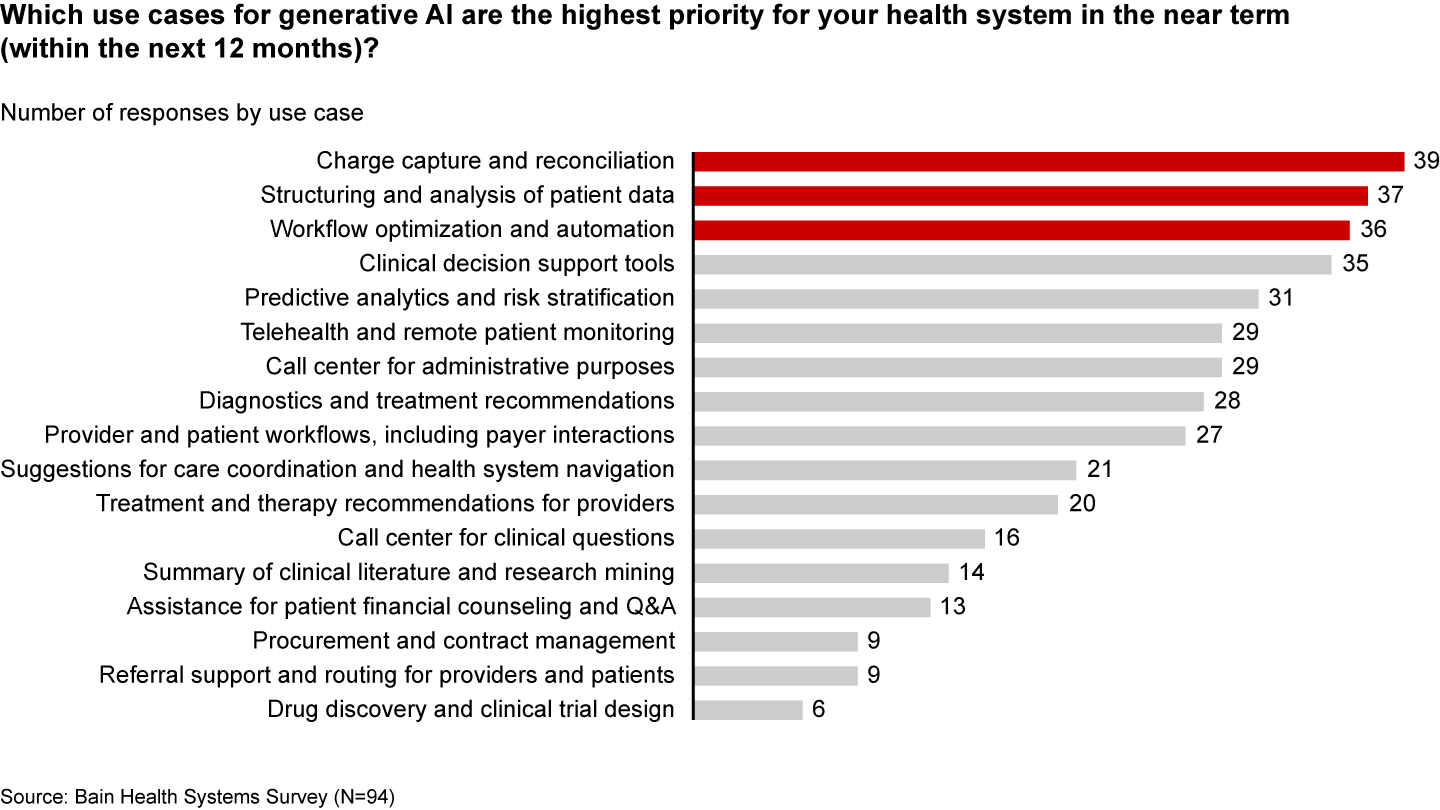

Many health systems are eyeing imminent opportunities to reduce administrative burdens and enhance operational efficiency. They rank improving clinical documentation, structuring and analyzing patient data, and optimizing workflows as their top three priorities (see Figure 1).

Figure 1

In the near term, generative AI can reduce administrative burdens and enhance efficiency

Some generative AI applications are already streamlining administrative tasks and allowing thinly stretched physicians to spend more time with patients. For instance, Doximity is rolling out a ChatGPT tool that can draft preauthorization and appeal letters. HCA Healthcare partnered with Parlance, a conversational AI-based switchboard, to improve its call center experience while reducing operators’ workload. And there are new announcements seemingly every week: Consider how healthcare software company Epic Systems is incorporating ChatGPT with electronic health records (EHRs) to draft response messages to patients, or how Google Cloud is launching an AI-enabled Claims Acceleration Suite for prior authorization processing.

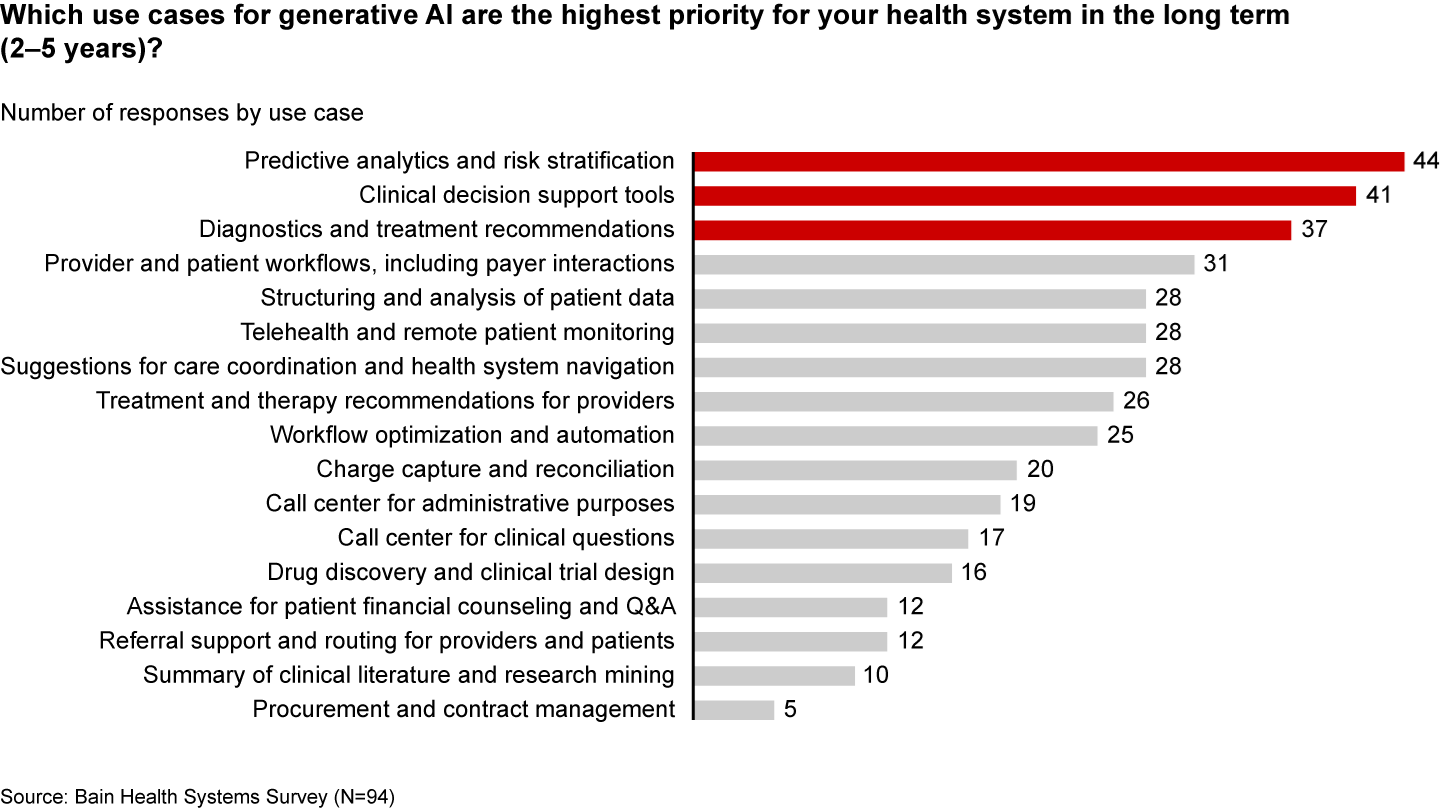

These applications only scratch the surface of potential. In the future, generative AI could profoundly transform care delivery and patient outcomes. Looking ahead two to five years, executives are most interested in predictive analytics, clinical decision support, and treatment recommendations (see Figure 2).

Figure 2

Predictive analytics, clinical decisions, and care recommendations are long-term generative AI priorities

It’s hard not to catch AI “fever.” But there are real challenges ahead. Some are already tackling the biggest questions: Organizations such as Duke Health, Stanford Medicine, Google, and Microsoft have formed the Coalition for Health AI to create guidelines for responsible AI systems. Even so, solutions to the greatest hurdles aren’t yet keeping up with the rapid technology development.

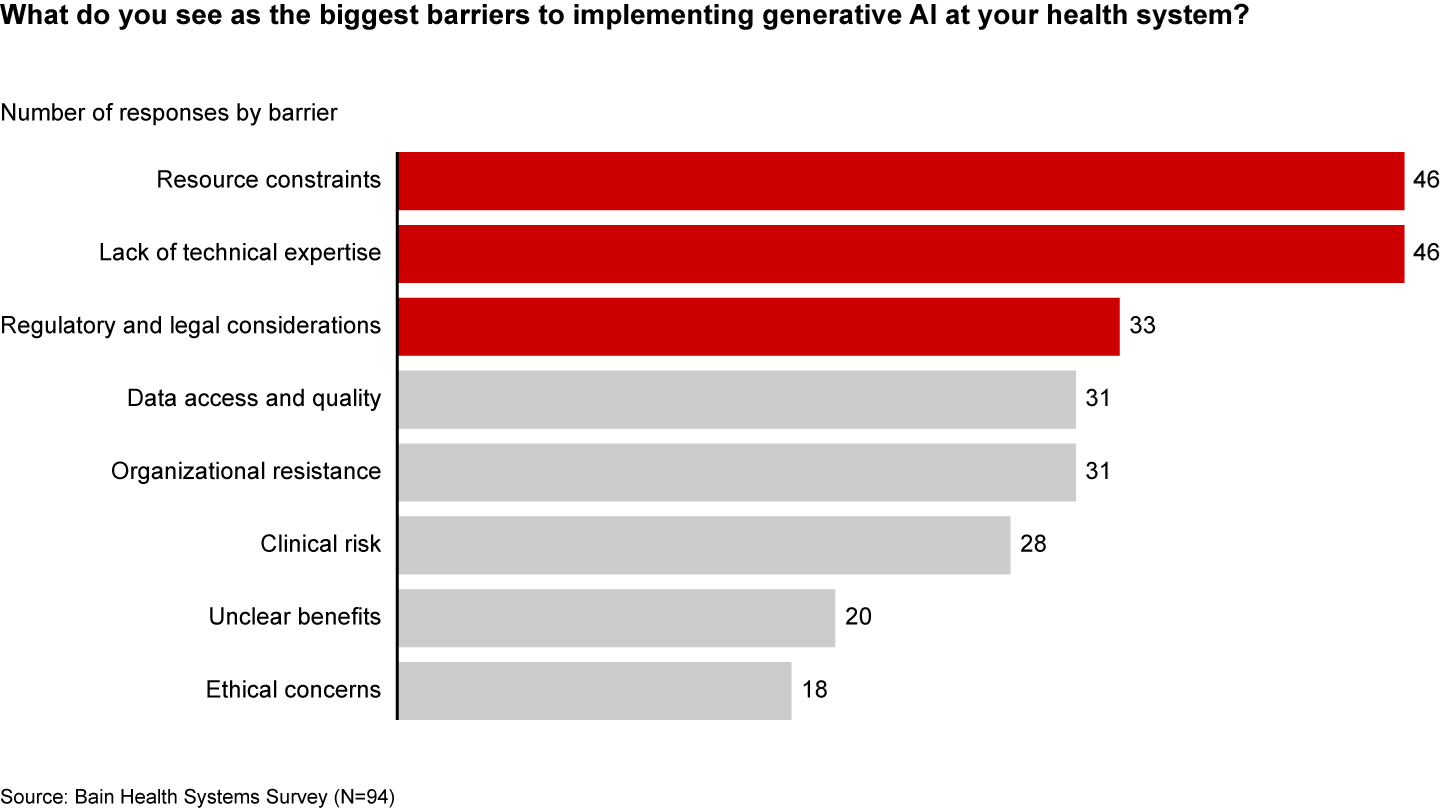

Resource and cost constraints, a lack of expertise, and regulatory and legal considerations are the largest barriers to implementing generative AI, according to executives (see Figure 3).

Figure 3

A lack of resources, expertise, and regulation are the biggest barriers to generative AI in healthcare

Even when organizations can overcome these hurdles, one major challenge remains: focus and prioritization. In many boardrooms, executives are debating overwhelming lists of potential generative AI investments, only to deem them incomplete or outdated given the dizzying pace of innovation. These protracted debates are a waste of precious organizational energy—and time.

Starting small to win big

Setting the bar too high is setting up for failure. It’s easy to get caught up, betting big on what seems like the greatest opportunity in the moment. But 12 months later, leaders often find themselves frustrated that they haven’t seen results or feeling as if they’ve made a misplaced bet. Momentum and investments slow, further hindering progress.

Leading companies are forming a more pragmatic strategy that considers current capabilities, regulations, and barriers to adoption. Their CEOs and CFOs work together to enforce four guiding principles:

Pilot low-risk applications with a narrow focus first. Tomorrow’s leaders are making no-regret moves to deliver savings and productivity enhancements in short order—at a time when they need it most. Gaining experience with currently available technology, they are testing and learning their way to minimum viable products in low-risk, repeatable use cases. These quick wins are typically in areas where they already have the right data, can create tight guardrails, and see a strong potential return on investment. Some, like call center and chatbot support, can improve the patient experience. However, given the current challenges around regulation and compliance, the most successful early initiatives are likely to be internally focused, such as billing or scheduling. Most importantly, executives prioritize initiatives by potential savings, value, and cost.

Decide to buy, partner, or build. CEOs will need to think about how to invest in different use cases based on availability of third-party technology and importance of the initiative.

Funnel cost savings and experience into bigger bets. As the technology matures and the value becomes clear, companies that generate savings, accumulate experience, and build organizational buy-in today will be best positioned for the next wave of more sophisticated, transformative use cases. These include higher-risk clinical activities with a greater need for accuracy due to ethical and regulatory considerations, such as clinical decision support, as well as administrative activities that require third-party integration, such as prior authorization.

Remember generative AI isn’t a strategy unto itself. To build a true competitive advantage, top CEOs and CFOs are selective and discerning, ensuring that every generative AI initiative reinforces and enables their overarching goals.

Some health systems are already seeing powerful results from relatively small, more practical investments. For instance, recognizing that clinicians were spending an extra 130 minutes per day outside of working hours on administrative tasks, the University of Kansas Health System partnered with Abridge, a generative AI platform, to reduce documentation burden. By summarizing the most important points from provider-patient conversations, Abridge is improving the quality and consistency of documentation, getting more patients in the door, and cutting down on pervasive physician burnout.

Although it will require some upfront investment, in the long run it will be more costly to underestimate the level and speed at which generative AI will transform healthcare. The next generation of leaders will start testing, learning, and saving today, putting them on a path to eventually revolutionize their businesses.

This annual look at high-impact trends affecting healthcare in the coming year is based on evaluation of current industry research data. Healthcare Finance Trendsfor2023 (Trends) explores eight themes identified by CommerceHealthcare® ranging across four areas:

Financial. Providers enter the year contending with multiple financial stress points. They will also seek growth in technology-enabled remote care.

Patient financial experience. The need to drive not only improvement but also personalization of the financial experience is paramount. A central role will be played by patient financing programs which will see growing demand in 2023.

Trust. Building trust with all constituencies is explored as a linchpin for long-term provider success. The latest findings on cybersecurity show that this contributor to trust will continue to consume leadership attention.

Digital transformation. Pursuit of digital-first operations is accelerating, with the finance area an important focus. Emerging payment modes are finding a home in healthcare’s digital finance landscape.

This report’s consistent message is that these trends intersect in ways that compound both the challenges and the upside potential of strategies that address them.

1. Multiple Financial Stress Points Will Constrain Options

Healthcare’s financial predicament for the next 12–18 months is being described in strong terms. Citing $450 billion of EBITDA that could be in jeopardy, more than half of the industry’s project profit pool by 2027, one analyst suggests “a gathering storm.” Another perceives “broad and serious threats” as “elevated expenses” erode margins and exact “a profound financial toll.” Fitch Ratings issued a “deteriorating” outlook for nonprofit health systems.

These financial headwinds are upending healthcare’s traditional status as “recession-proof.” It is helpful to probe the multiple forces in play, the urgent workforce management challenge, and the varied solution set.

Multiple stress factors at work

Observing that margins will be down 37% in 2022 relative to pre-pandemic, a recent stark assessment concluded, “U.S. hospitals are likely to face billions of dollars in losses — which would result in the most difficult year for hospitals and health systems since the beginning of the pandemic.”

A confluence of factors is exacerbating the stress for 2023:

Rising acuity levels. Over two-thirds of surveyed C-suite executives said patient health has worsened from pandemic-induced delayed care. The upshot, stated by 27% of CFOs, is rising expenses due to higher acuity. Inpatient days are projected to increase at an 8% rate over the coming decade.

Reimbursement gaps and inflation. Commercial and government reimbursement rates are not keeping pace with rising costs. Surging inflation is widening this gap. Hospitals are also reporting substantial insurer payment delays and denials.

Investment declines. Stock and bond market declines have removed a cushion for operating weakness. Market uncertainty will complicate 2023 portfolio management.

Persistent workforce concerns remain center stage

Burnout and shortages have disrupted the clinical workforce. Nearly 60% of physician, advanced practice provider and nurse survey respondents said their teams are not adequately staffed, and 40% lack resources to operate at full potential. Many providers face extreme to moderate shortages of allied health professionals.

The problem extends beyond the clinical. A survey saw 48% of respondents experiencing severe labor deficiencies in revenue cycle management (RCM) and billing, and one in four finance leaders must fill over 20 positions to be fully staffed.

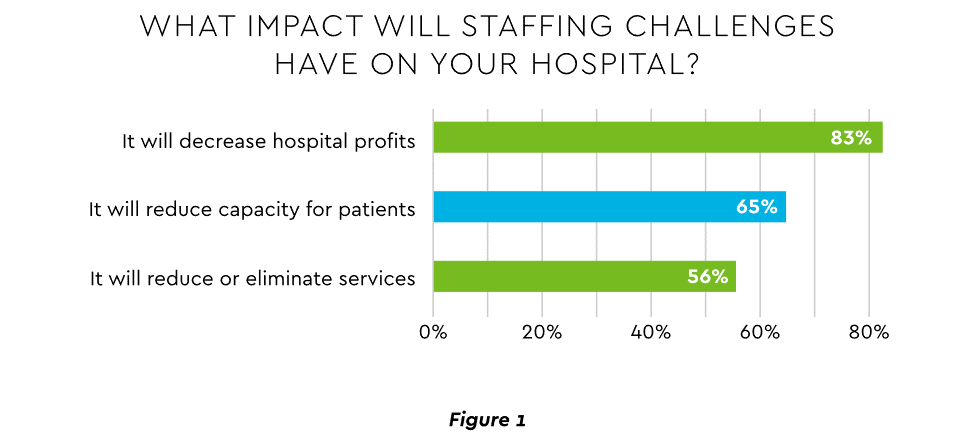

An executive outlook highlighted demonstrable impact on financial performance and growth from these workforce problems, citing reductions in profitability, capacity and service (Figure 1).1

Expenses. Hospital employee expense is expected to increase $57 billion from 2021 to 2022, with contract labor ballooning another $29 billion. Average weekly earnings are up 21.1% since early 2022. Half of medical practices budgeted higher staff cost-of-living increases in 2022. Shortages plague post-acute facilities as well. Their reduced capability to accept discharged patients is lengthening many hospitals’ patient stays.

Capacity constraint. Two-thirds of healthcare leaders identify “ability to meet demand” as their top workforce concern, suggesting a “looming capacity gap between future demand and labor supply.”

Range of measures being deployed

Health systems, hospitals and practices will vigorously pursue at least four direct actions to overcome the financial and staffing hurdles:

Cost cutting. Expense control will be paramount and “hospitals will be forced to take aggressive cost-cutting measures.” McKinsey estimates total industry administrative savings of $1 trillion through multiple aggressive changes.

Service line rationalization. Providers are rethinking how they deliver services to optimize efficiency. One path is utilizing “lower level” healthcare professionals in ways that free RNs and LPAs for more complex work suited to their top skills. Integrating remote care into the mix is another core element of the strategy.

Recruitment and retention programs. Attracting and retaining talent is crucial. Compensation is one avenue. Over two-thirds of organizations are offering signing bonuses for allied health professionals. Some are instituting value-based payments for physicians, offering salary floors to protect from drops in patient volume. CFOs and CNOs are joining forces to invest in nurse retention strategies.

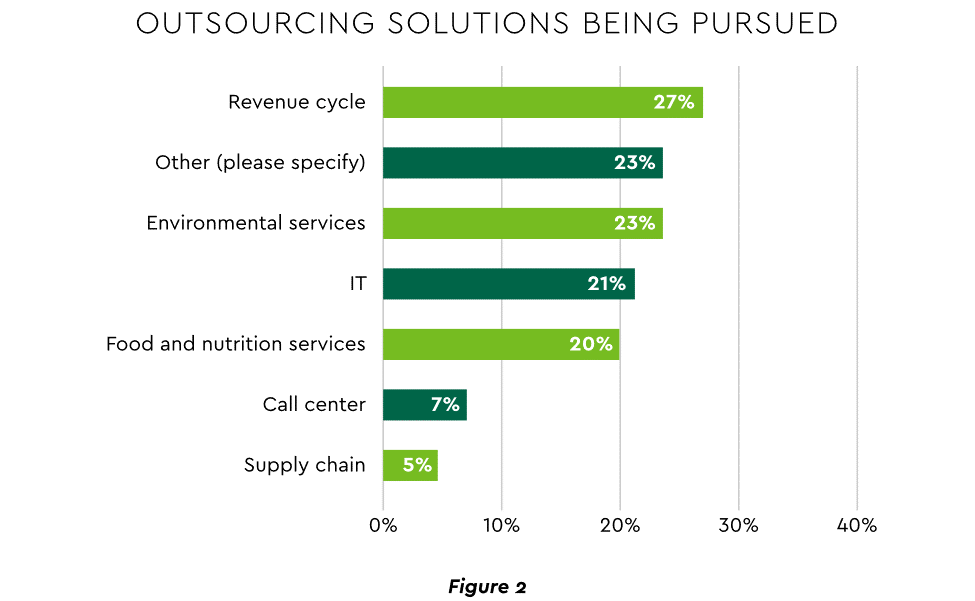

Staffing management. An increasingly popular tool to reduce labor cost and optimize staff resources is outsourcing. Figure 2 shows that RCM is leading the way among those using the solution.

2. Growth Strategies Favor Outpatient, Virtual, Acute Home Care

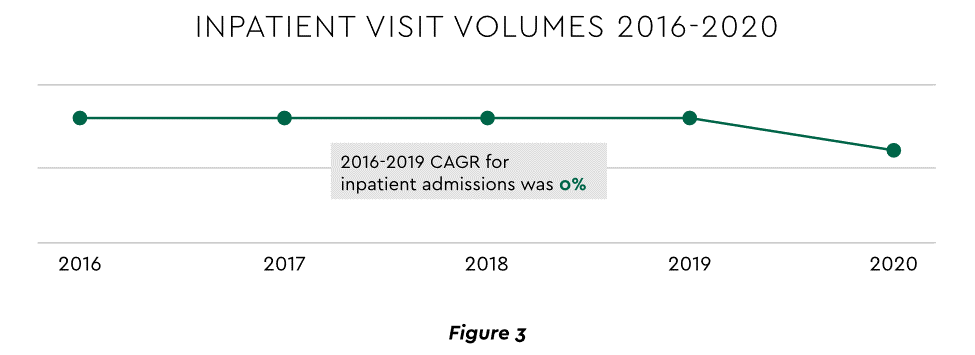

Pursuing top line growth in tandem with reining in expenses is essential. Inpatient volume growth has been tepid for several years ─ essentially flat in the 2016–20 period (Figure 3).

Leaders have been pivoting to outpatient and virtual care to diversify revenue streams. Two high-potential 2023 growth tracks in this sector merit deeper assessment.

Telehealth

Considerable evidence attests to strong commitment to telehealth and remote care. Sixty-three percent of physicians worldwide expect most consultations to be performed remotely within 10 years. Approximately 40% of health centers are using remote patient monitoring today. Consumers are also positive: 94% definitely or probably will use telehealth again, 57% prefer it for regular mental health visits and 61% use it for convenient care.

Telehealth is still in early stages of maturity. Only 4% of surveyed top executives consider their organization proficient at implementing remote care. Healthcare is also recognizing that a full telehealth ecosystem must be constructed. A physician leader explained that the industry’s early telehealth incarnations failed to build “virtual-only environments or really drive e-consults as a way of doing things.” A vital ecosystem demands alterations to current contracts, coding, collections, patient financing, staff training and other business practices.

Hospital-at-Home (HaH)

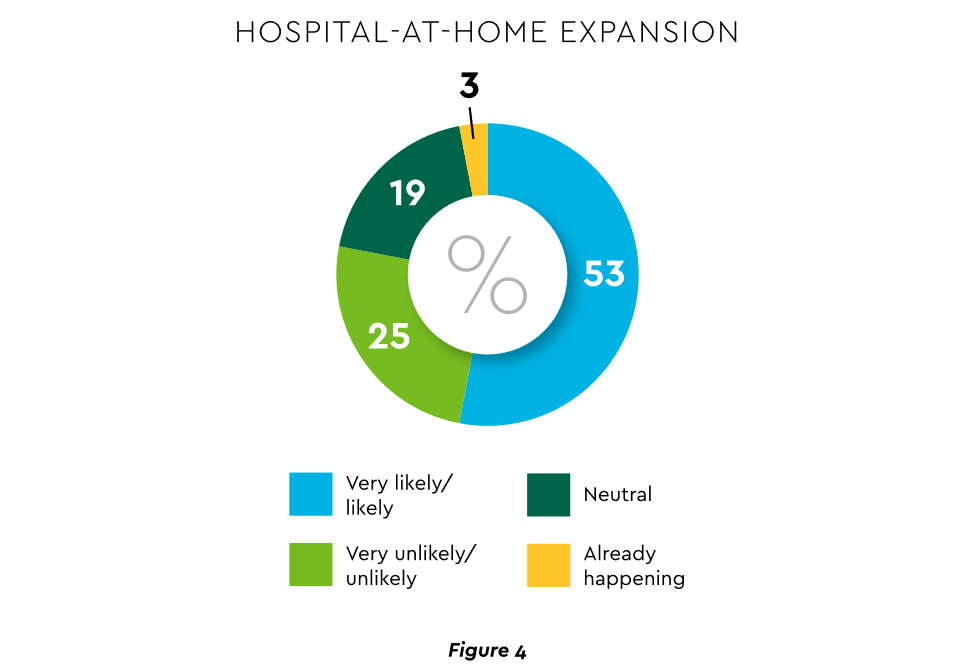

Health systems see particularly promising growth in the provision of acute care in patients’ home settings, including post-surgical and cancer treatment. The federal government has already allowed waivers to 114 systems and 256 hospitals to obtain inpatient-level reimbursement for acute care at home. However, these waivers were prompted by the pandemic and are slated to end in early 2023. The renewal uncertainty has stymied some activity and represents an overhang on the opportunity. However, enthusiasm appears strong, and 33% of hospitals in a recent poll said they would be prone to continue HaH even without renewal.

The forecasts are encouraging. Over half of hospitals believe it likely they will utilize HaH for at least half of their chronically ill patients over the next several years (Figure 4).

Harvesting the HaH potential will require implementation of current and emerging enabling technologies in remote monitoring, high-speed networks and artificial intelligence that generates algorithmic guidance for caregivers and patients alike.

3. Strong Drive to Improve and Personalize the Patient Financial Experience

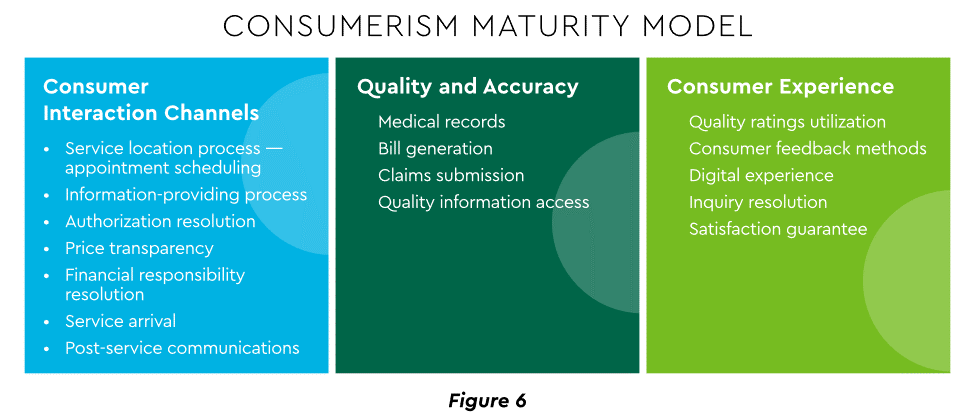

Today’s healthcare market dynamics place a premium on positive patient experiences. The goal is to deliver “an empathetic relationship between customers and brands built on what the customer wants and how they want to be treated.” It is a complex undertaking, with numerous touchpoints as captured in HFMA’s Consumerism Maturity Model (Figure 6).

An array of studies underscores the value proposition for intense provider focus on patient financial experience:

Sixty-one percent of consumers said that ease of making payments is very or somewhat important in decisions to continue seeing a doctor. Over half of patients also said text message reminders make them very or somewhat more likely to pay a bill faster than usual.

Thirty-five percent of respondents “have changed or would change healthcare providers to get a better digital patient administrative experience.”

A quality financial experience encompasses “simplified explanations, consolidated bills that match one’s health plan benefits, clear language displaying patient liability and payment options.”35

Significantly improving the financial experience requires a unified strategy, not just a collection of individual initiatives. Three threads to such a strategy will be prominent in 2023.

Using a Digital Front Door

Organizations have been moving swiftly to channel many patient financial transactions through an integrated Digital Front Door (DFD). This approach offers patients a singular online point of access and intelligent navigation to needed services. Growth is accelerating. A DFD is their patients’ first contact point for 55% of responding organizations, according to one technology survey. A leading forecaster sees 65% of patients engaging services via digital front doors by 2023.

Expanding price transparency

Mandates for full price transparency and “no surprises” billing are in effect, but estimates of compliance are mixed. An analysis of 2,000 hospitals determined that only 16% met the requirement to post an online “machine readable” file displaying clear charges for 300 “shoppable services.” Another assessment showed a more substantial 76% of hospitals had posted files, and 55% were deemed “complete.” One provision of interest to practices is the “good faith estimate” of expected charges required to be given to uninsured and self-pay individuals when they schedule visits. CommerceHealthcare® has worked with clients to enhance the patient financial experience by complementing their website pricing data with clear information on patient financing options and enrollment access. Bill pay information can also be added for one-stop guidance.

Personalizing the experience

Beyond choice and convenience, the deeper objective is truly personalized experiences throughout the care journey. The words of leading analysts best define the drive to personalize:

“Tomorrow’s healthcare experience will be built by patients tailoring their own experience.”

“By 2024, 30% of chronic care patients will truly own and openly leverage their personal health information to advocate for, secure, and realize better personalized care.”

Opportunities abound to personalize the patient financial experience. Automating manual processes establishes a foundation. Patient financing with no- or low-interest credit lines and flexible terms can produce monthly payment schedules tailored to each patient’s needs. Refunds can be made through multiple payment modes to meet varying patient preferences.

4. Evidence Underscores Growing Demand for Patient Financing

Emphasizing patient financing as part of the overall experience is powerful. Patients continue to struggle paying for care. Recent granular data details three related forces at work.

Meeting care costs difficult for many patients

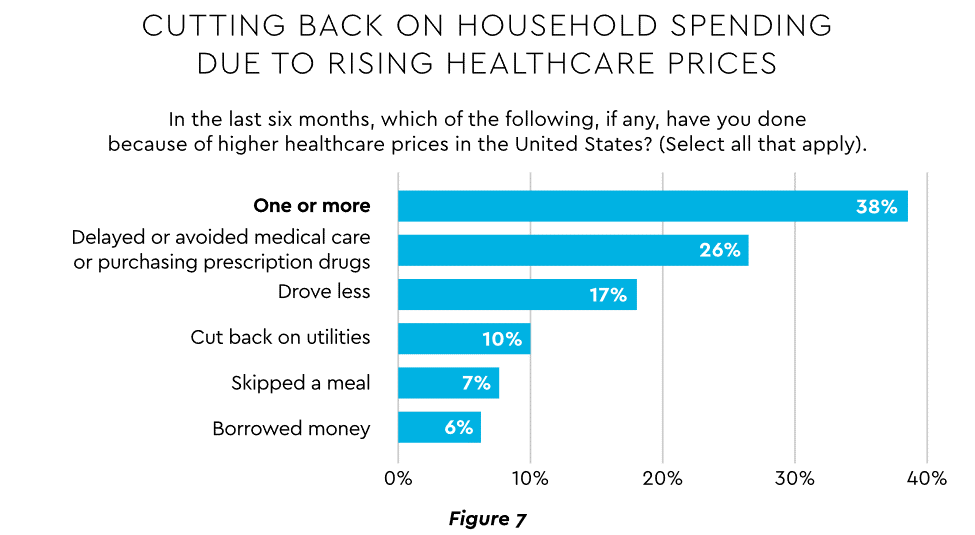

Commonwealth Fund found that 42% of individuals had problems paying medical bills or were paying off medical debt during the past year, while 49% were unable to pay an unexpected $1,000 medical bill.42 Health costs trigger reduction in a range of personal expenditures, led by deferring or avoiding care and drugs (Figure 7).

Twenty-eight percent of Americans now describe themselves as less prepared than last year to pay for routine or unanticipated care.

Patient obligation for care costs still rising

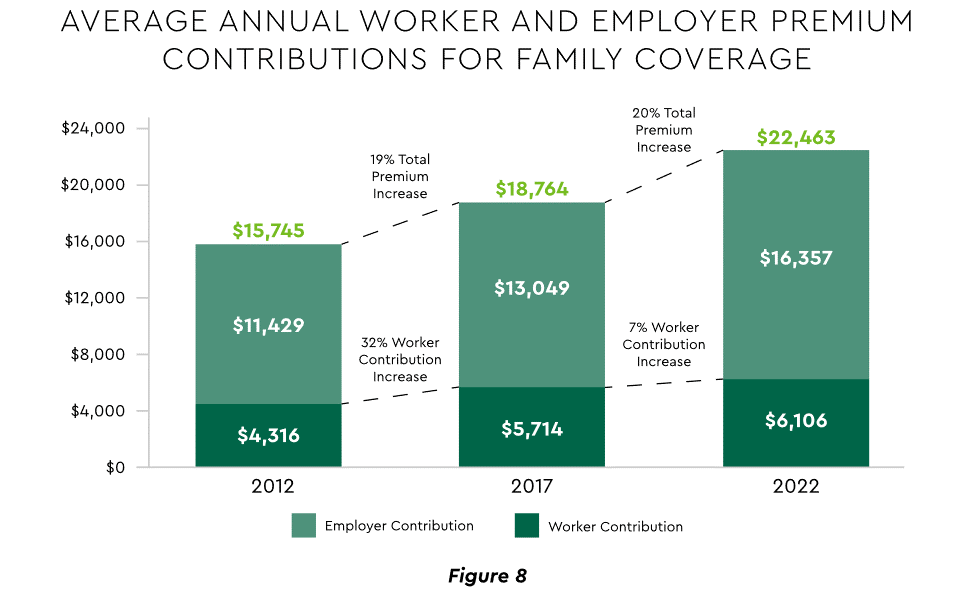

Patient obligation continues its upward march. Insurance premiums have climbed steadily for both the insured and their employers, and employees now pay over $6,000 annually on average for family coverage (Figure 8).45

High deductible health plans (HDHP) also place substantial burden on the patient. Through 2021, 28% of workers were enrolled in an HDHP with an average family deductible of $4,705. Employer satisfaction with these plans is high, auguring further expansion.

Providers feeling the financial effects

Patient payment difficulties are clearly impacting provider financials. A recent in-depth analysis uncovered substantial self-pay issues:

Self-pay accounts represented 60% of 2021 patient bad debt, up from 11% in 2018.

Nearly 18% of patient balances were over $7,500 and 17% over $14,000. Collections were noticeably lower at these balances.

Multiple chronic conditions add to the problem. A recent extensive analysis concluded: “Among individuals with medical debt in collections, the estimated amount increased with the number of chronic conditions ($784 for individuals with no conditions to $1,252 for individuals with 7–13).”

For their part, providers will be encouraged to broaden patient financing programs. Patients are certainly interested. When asked, 62% of consumers indicated they would use financing options or creative payment plans if available for large bill amounts. Many health systems, hospitals and practices will turn to outside help to satisfy the demand. A recent analysis recommended that health systems “consider keeping shorter-term payment plans in-house and extended term plans through external partnerships.”

Organizations will also need to step up their communications. A survey revealed that 64% of patients were unaware that their doctors and hospitals offered payment plans or financial help.

5. Building Trust Becoming a Critical Success Factor

Trust has emerged as a paramount issue today for most organizations as they encounter an “imperative to build trust and transparency among different stakeholder groups — employees, customers, suppliers, regulators and the communities in which they operate.” Healthcare is no exception, and the trust issue is growing in both complexity and urgency.

Healthcare’s trust gap

Trust in healthcare took a hit from the COVID-19 experience. A spring 2022 HFMA survey recorded 44% of finance leaders saying they perceived decreased patient trust. Between April 2020 and December 2021, the percentage of Americans who trusted information from doctors “a great deal” declined by 23%, from hospitals 21%, and from nurses 16%. The patient financial experience also faces “drivers of mistrust,” according to surveyed leaders who cited general payment confusion (58%), surprise billing (39%), high prices of commodity items (28%) and lack of price transparency (26%). Building trust reaps dividends. People who trust their providers are five times more likely to stay with them than those who are neutral or distrustful.

Strategies for building trust

Industry experts promote several approaches to galvanize trust among all constituencies:

Commitment. Embedding trust deeply in the organization requires full support from senior leadership.

Data transparency and governance. IDC predicts that “by end of 2023, 20% of expenses on care integration solutions will be centered around ‘trust’ to protect data, workflows and transactions.”

Reliance on fewer business partners. Many health systems, hospitals and practices are reducing their number of vendors in order to focus on a set of trusted long-term partners. For example, almost two-thirds of surveyed providers said they were seeking to streamline the number of software solutions over the next year.

The bank partner advantage

A provider’s banking relationship can yield valuable collaboration in the trust-building endeavor. Banks enjoy solid trust among consumers. As an example, 53.4% of consumers rated banks as most trusted to provide payment “super apps” and financial digital front doors ─ exceeding the next closest source by 10 points.

6. Cybersecurity in 2023: No Rest for the Weary

Cybersecurity is part of the trust calculus and has become an evergreen topic in healthcare. Compromised data and ransomware attacks are ongoing and leaders must continually refine their understanding in at least three areas: the overall security landscape, particular financially related considerations and contemporary security defenses.

The current landscape

The latest statistics quantify the cyber assault on healthcare:

Incidence. 89% of organizations suffered at least one attack in the past 12 months with the average number at 43.

Cost. A provider’s most serious attack costs an average of $4.4 million. IBM calculated healthcare’s average total cost of a breach at $10.1 million, up 42% since 2020.

Attack Characteristics. Healthcare data types most commonly compromised are personal (58%), medical (46%), and credentials (29%). Organizations have an exposure to an average of over 26,000 network-connected devices. A disturbing finding is that those healthcare institutions that paid ransom got back only 65% of their data in 2021.

Specific financial considerations

Finance leaders will also need awareness of the following:

Cyberattacks could affect credit ratings and are often a component of Environmental, Social and Governance assessments.

Financial outsourcing requires monitoring. A recent news story chronicled an accounts receivable firm’s breach that exposed individual information, account balances and payments.

Cyber insurance premiums are likely to increase substantially.

Responses/tools

Beyond a host of management and monitoring tools being deployed, a strategic philosophy is rapidly gaining ground. The “zero trust” model sounds counter to the trust-building mindset described earlier, but it has become essential. It “denies access to applications and data by default,” and 58% of hospitals and health systems have a zero trust initiative in place. Another 37% intend to implement one within 12–18 months.

Cybersecurity investment will challenge CFOs in 2023, especially in areas such as talent. Cybersecurity worker availability is estimated to satisfy only 68% of open positions. Banking partners will also be expected to play an important role. Over the years, major banks have become “leaders in enhancing cyber strategy and investing in cyber defenses, processes and talent.”

7. Digital Transformation of Finance In Focus

Digital transformation is fundamental to healthcare’s business and care delivery model changes. IBM’s website succinctly captures the goal, “Digital transformation means adopting digital-first customer, business partner, and employee experiences.” A leading forecaster believes 70% of healthcare organizations will rely on digital-first strategies by 2027.

Transformation efforts need to accelerate. One study showed that “digital, technology and analytics strategies exist for nearly all organizations, yet only 30% have begun to execute on those plans.”

One functional segment ramping up digital transformation is finance. According to a recent survey, 94% of CFOs and senior leaders stated that such efforts will be at the forefront of financial operations and strategy for 2023–2024, and 79% described it as an “absolute need” for “commercial stabilization and long-term survival of their healthcare organization.”

Advanced technology is gaining traction. Many see optimization in combining robotic process automation (RPA), artificial intelligence and machine learning to create “intelligent automation.” Together, these technologies create algorithms to automate decisions that guide “robotic” software to perform financial actions and thereby reduce manual labor.

Getting to digital-first in finance and across the enterprise has several critical success factors. These include sustained commitment, a platform-centric mindset and effective governance.

Commitment

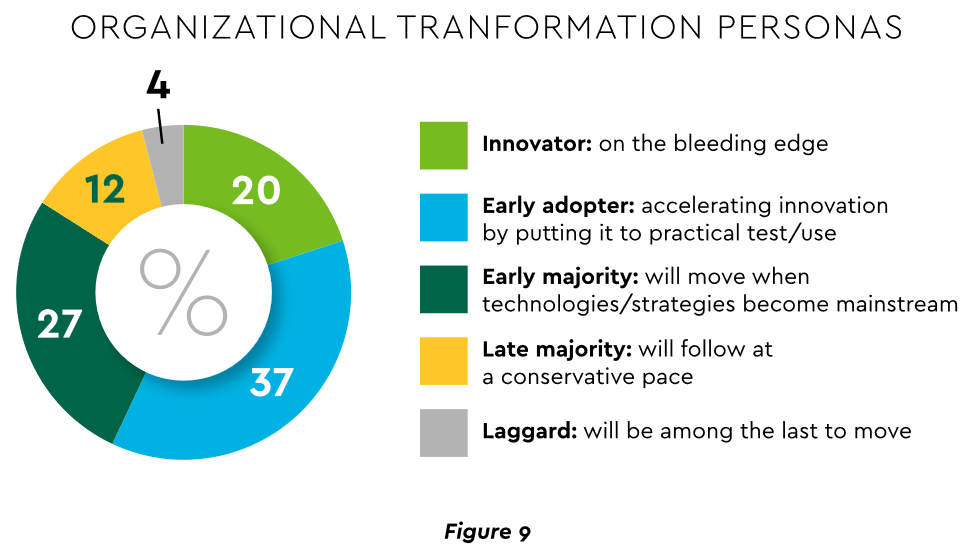

Some assert that few healthcare executives have “created digital strategies that look far enough into the future.” Speed of change is also important. Health systems, hospitals and practices exhibit varying risk appetites and change rates. When asked to self-identify “transformation personas,” a little over half regarded themselves as being on the innovative “early mover” end of the spectrum, while the remainder will adapt as technologies prove themselves (Figure 9). Slower organizations will likely need to increase the pace.

Implementing enterprise platforms rather than proliferating “point solutions” is obligatory. Organizations must be “prepared to compete in the platform economy as platform-based business models have changed the way we live, work and receive care.”

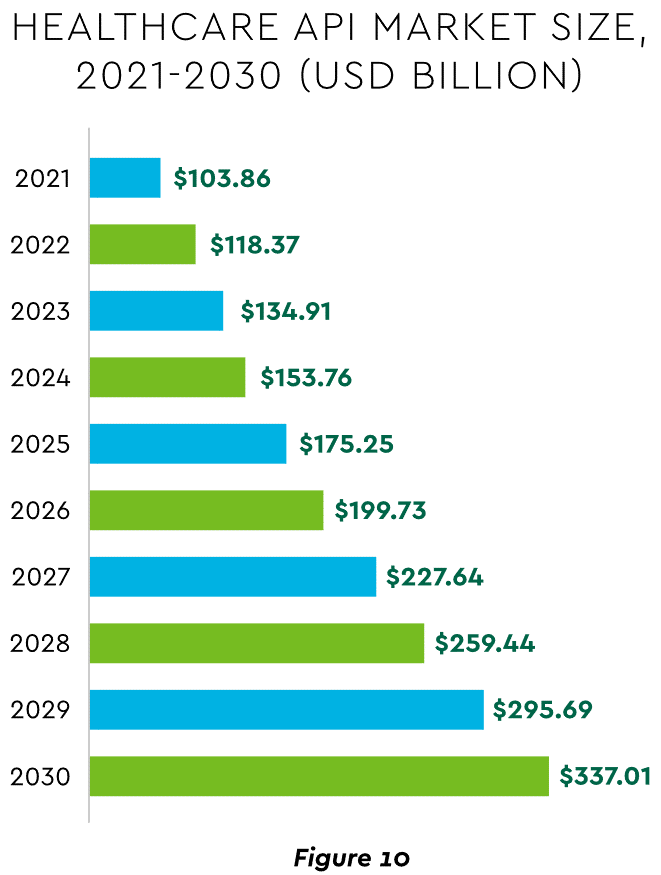

There are still too many tools and applications. A survey of top decision-makers at health systems found that 60% use over 50 software solutions just in operations (24% have over 150). System integration is one answer. Use of application programming interfaces (API) helps this effort substantially. API-first is fast becoming the norm among solution providers, with global API investment expected to nearly triple by 2030 (Figure 10)

Effective governance is vital to constructing a platform-based transformative model and to ensuring wide user adoption. Healthcare has seen the rise of new senior roles such as Chief Digital Officer and Chief Transformation Officer, positions focusing on initiatives like ownership of technology success at the department level and devising user incentives.

8. Digital Payments on the Horizon for Healthcare

A variety of emerging digital payment modes will further the transformation of finance. These payments are expected to grow almost 23% annually in healthcare. ACH payments have been on a strong upward trajectory in healthcare for several years, especially for business transactions. In 2021, ACH tallied a yearly increase of 18% in volume and 5% in dollars.

Notable technologies and payment rails to watch for expected crossover from consumer markets to healthcare include:

Mobile payments. The market for mobile payment technologies has been growing at a 16% compound annual clip and should reach $90 billion in 2023, powered by wide smartphone use, 5G networks and convenience. This category encompasses technologies such as e-wallets, forecasted to grow 23% annually worldwide through 2030.

Real-time payments (RTP). These digital transactions are settled nearly instantaneously through platforms such as The Clearing House. One forecast sees 30.4% compound RTP growth in the U.S. from 2022 to 2030.

Buy Now Pay Later (BNPL). This growing mode offers consumers short-term financing to stretch payments over several installments. A recent survey established that 23% of American adult respondents have used a BNPL service. BNPL is just entering healthcare and is currently regarded as an option for certain elective or cosmetic procedures or for specific individual credit scenarios.

Earned Wage Access (EWA). Using an RTP approach, employers are beginning to offer on-demand pay which enables “instant access to earned wages right after the work is performed, at the end of the shift, or upon completion of a project.” It is not a loan or advance pay. A 2021 poll conducted by Harris found that 83% of U.S. workers feel they should be able to access earned wages at the end of each day. Millennials were particularly interested: 80% would like daily automatic pay streaming to their bank accounts, and 78% said free EWA would boost loyalty to their employer. Given its pressing workforce concerns, healthcare is likely to find EWA a tool to promote retention.

Seeking the right use cases for these payment technologies offers many potential provider benefits.

Conclusion

The connected forces discussed and quantified here create major challenges to address in 2023. The strategic agenda calls for balancing tight cost control with investment in growth opportunities, significantly enhancing patient financial experience by meeting growing patient financial need, shoring up trusted relationships and cybersecurity, and accelerating the digital transformation of finance.

Of all the pandemic’s impacts still felt today, disruptions to the healthcare workforce and rising labor costs may be most impactful to current health system operations.

Over the next three editions of the Weekly Gist, we’ll be exploring the lingering effects of this workforce crisis, with a focus on nurse staffing and recruitment.

While wage increases helped reduce hospital registered nurse (RN) turnover rates from 27 percent in 2021 to 23 percent in 2022, nurses—along with hospital employees in general—are still changing jobs at higher rates than before the pandemic.

Over half of all hospitals still face nurse vacancy rates above 15 percent, a slight improvement from 2022 but still far more than before the pandemic.

While the worst of nursing turnover appears to have passed, the “rebasing” of wages (for nursing, 27 percent higher compared to 2019) will provide ongoing pressure to strained hospital margins.

Peter Drucker, the hall of fame management guru, once famously said that the hardest business organization to run in America was a hospital. If that comment was true so many years ago, imagine what Drucker would have to say about the difficulty of hospital management right now.

Hospital financial performance suffered significantly in 2022 and recovery during 2023 has been quite slow. This trend suggests the question,

“What steps are hospital C-suites taking to recover pre-Covid financial stability?”

Erik Swanson manages all analyses for our monthly Kaufman Hall Flash Report and he and I speculated that an industry-wide hospital recovery could not be achieved without reductions in force across the hospital ecosystem. Some research on our part determined that no official organization tracks hospital layoffs over time but we wondered if we could use our Flash Report data, which is provided to us by Syntellis Performance Solutions, to reach an informed conclusion.

What we were able to do was prepare three types of charts, as follows:

The first chart measures net employee percentage change by month. This chart shows whether overall hospital employment is increasing or decreasing over time and by how much.

The second chart attempts to establish the median turnover for hospitals over an annual period and then measure the deviation from that turnover rate. A greater deviation from what might be termed “normal turnover” suggests that an increasing number of hospitals are using reductions in force to more quickly reduce the cost of doing business.

The third chart shows average FTEs per occupied bed on a comparative basis looking at month-to-month and year-to-year statistics.

The first chart, Net Employee Percentage Change by Month, begins at January 1, 2018, and continues to March 1, 2023 (Figure 1). Overall additions to hospital employment remained generally positive through January 1, 2020. Overall hospital employment then went generally negative from March 2020 (the onset of Covid restrictions) to March 2022. The reductions in hospital employees during this period were likely the result of the “great resignation” during the worst of the Covid pandemic. But then, from July 2022 to March 2023, overall hospital employees demonstrated by the Flash Report dropped dramatically with an overall 2% decrease at the March 2023 date. This statistic suggests more than simply increased hospital turnover, but rather a formal layoff process initiated across many hospital organizations, along with aggressive management of contract labor.

Figure 1: Net Employee Percentage Change by Month

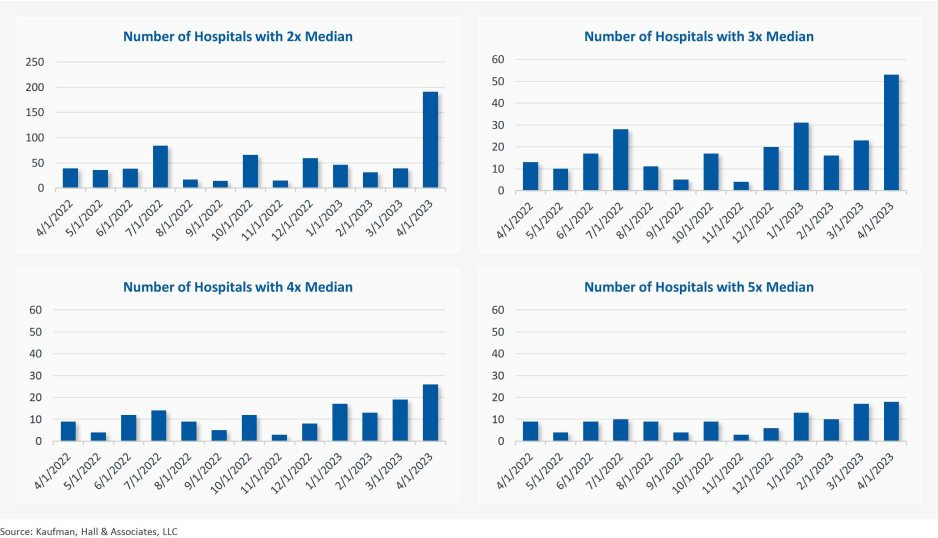

The second chart demonstrates the deviation from expected turnover at levels of 2x, 3x, 4x, and 5x by number of hospitals (Figure 2). No matter which measure you examine, the deviation of employees from expected turnover spiked significantly in April 2023 and even more so in May 2023. This again suggests the aggressive management of labor costs that likely could not occur without the intentional reduction of actual positions and/or the cost of these positions.

Figure 2: Number of Hospitals with Deviations from Expected Turnover at 2x, 3x, 4x, and 5x the Median

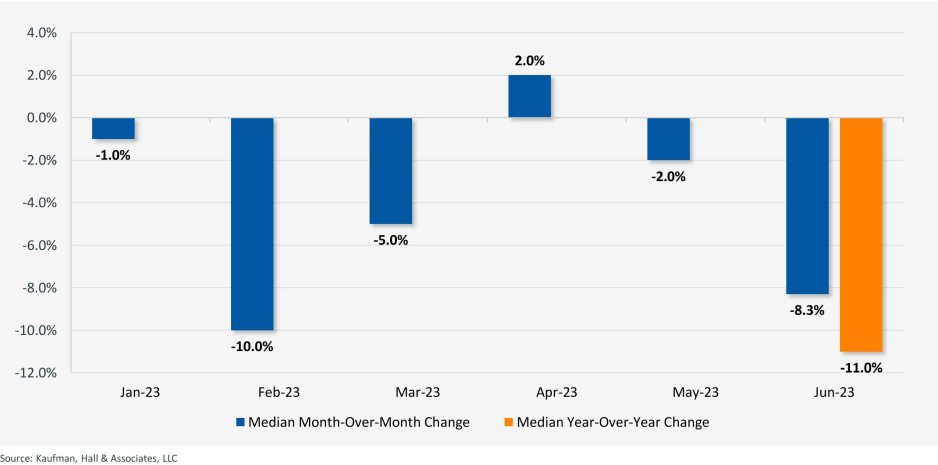

The last chart provides a remarkable set of observations (Figure 3). FTEs per adjusted occupied bed (AOB) declined by 8.3% between June 2023 and July 2023. The year-over-year variation for July 2023 was a decline of 11.01%. Our data further reveals that the FTE per AOB statistic has declined in five of the past six months on a month-over-month basis.

Figure 3: Median Change in FTEs per Adjusted Occupied Bed by Month

The conclusion here is that the return of the hospital industry to pre-Covid financial results has been no walk in the park. 2022 was, of course, a dismal financial year for the hospital industry. And while 2023 has shown improvement, the usual management steps to recovery have been only moderately effective. The data and analysis above demonstrate that C-suites across America are moving to stronger measures to assure the financial survivability and competitiveness of their organizations.

There is no revenue solve here, or at least not in the current environment: costs must come down and they must come down materially. From the sense and the trend of the data it would seem that hospital executive teams get the joke.

Fifty-four percent of CFOs say that their CEOs are asking them to focus on cost reduction while 40 percent indicate that their CEOs want them honing in on strategy and transformation, according to Deloitte’s “CFO Signals Survey 2Q 2023.”

More than one-quarter of CFOs in the survey reported that their CEOs are asking them to focus on working capital efficiency and risk management while over one-third of CFOs said their CEOs want them focused on strategy and transformation, performance management, revenue growth, investment and capital/financing.

Since 2010, Deloitte has surveyed leading CFOs representing some of North America’s largest companies to provide insight into the business environment, company priorities and expectations, finance priorities and CFOs’ priorities.

Participating CFOs represent diversified, large companies, with 81 percent of respondents reporting revenue in excess of $1 billion. Twenty-three percent are from companies with more than $10 billion in annual revenue, according to Deloitte.

Labor costs have spun out of control in the last few years as inflation set in and hospitals relied on contracted travel nurses to combat nationwide workforce shortages.

The secret to lowering labor costs now, hospital CEOs say, is putting a modern spin on a tried-and-true strategy: retention.

Dan Woods, CEO of El Camino Health in Mountain View, Calif., estimates the cost of recruiting a single nurse as being nearly $60,000, which drove his team’s decision to focus on reducing labor costs by decreasing turnover. The nurse turnover rate is around 22 percent nationally, but El Camino has achieved just 8 percent nurse turnover rate through a variety of retention efforts.

“We continue to chip away at our turnover rate by fostering a positive practice environment for our nurses,” said Mr. Woods. “We achieve this by creating structures and enabling processes so our staff are engaged in assisting with making changes within their practice environments. Also, our staffing and scheduling processes promote efficiency while meeting the needs of our staff, which is essential for retention.”

El Camino does have guardrails to ensure nurses don’t self-schedule overtime or other premium pay. Mr. Woods also mentioned positive labor relations as a retention tool.

“We just completed a new three-year agreement with our nursing union prior to the existing contract expiring and without strikes or the acrimony often associated with labor relations,” he said.

David Callendar, MD, president and CEO of Memorial Hermann Health System in Houston also recently told Becker’s the system is relying less on contract labor and increasing retention through its Well Together employee experience model, which allows employees to personalize programs and benefits to meet their individual needs.

“At Memorial Hermann, we believe that investing in our workforce is the most effective approach to managing labor costs,” said Dr. Callendar. “We accomplish this in three ways: one, creating a workplace where all feel valued and welcomed, and diversity is celebrated; two, investing in employee health and wellness programs; and three, providing professional development and career growth opportunities.”

Rochester (N.Y.) Regional Health is transforming its operating model and workforce strategy to offer more flexibility and build a culture valuing team members for retention.

“We’ve created a new in-house agency to significantly reduce our reliance on third-party contracts and improve staff integration within the health system to foster a more robust culture of collaboration, interdependency, alignment and system-ness,” said Richard Davis, PhD, CEO Of Rochester Regional.

Jeffrey P. Gold, chancellor of the University of Nebraska Medical Center in Omaha, said the academic medical center is focused on reducing the cost per unit of labor and lowering the number of units. The hospital is considering several tactics including additional training and mentorship, evaluating its benefits program and productivity across the organization.

The University of Nebraska Medical Center is also evaluating fixed labor cost departments and roles, and slowing or eliminating full-time employee growth to force innovation, organizational redesign, use of technology and productivity gains with staff retained.

Many hospitals are seeing wages increase within their markets, and increasing pay for existing team members is often less expensive than recruiting and onboarding new ones.

“Obviously, compensation is a key element of staffing, and we are working diligently to ensure that we are competitive within our market,” said R. Kyle Cramer, CEO of Day Kimball Health in Putnam, Conn. “Concurrently, we are evaluating how we staff our clinical areas and the mix of professionals we utilize to create a stronger level of team support and patient engagement. Ultimately we see stabilizing our workforce and reducing turnover through retaining strong members of our clinical and operational team as the key to effectively managing labor costs in this new era.”

Paula Ellis, DNP, interim CEO of F.W. Huston Medical Center in Winchester, Kan., said the critical access hospital has salaries in line with competitors but found benefits lagging. The hospital increased 401K match, provided better health insurance rates, improved tuition assistance and added competitive scholarships to keep employees engaged. The hospital also combined four positions into two.

“Staff were willing and able to take on new duties in exchange for a better schedule,” said Dr. Ellis. “We believe the best method to manage labor costs is to retain staff.”

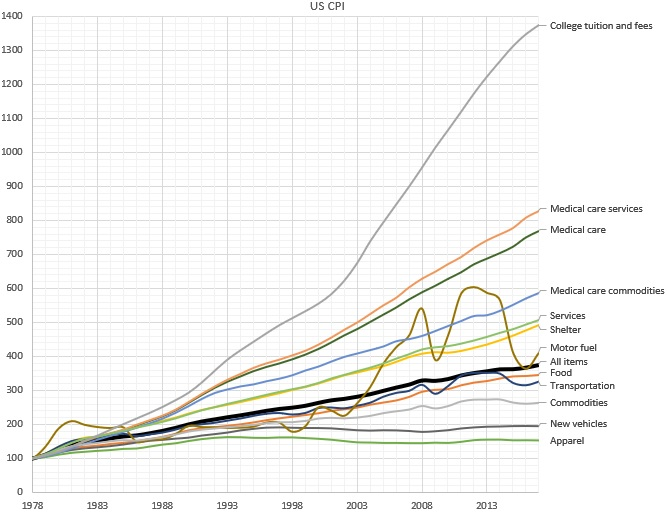

Why does the cost of education and healthcare services continue to rise rapidly, while the cost of goods rise much more slowly? According to economics theory, wages rise when there’s greater productivity; but a rise without an increase in productivity is referred to as “Baumol’s Cost Disease” . In an original study first published in 1966, economist William J. Baumol used the example of a string quartet to illustrate this idea: While the productivity of a given quartet has not increased over time over the last two hundred years, the salary (in nominal and real terms) has increased dramatically.

One way out of this trap is to turn services into goods. Employing a cobbler to make a pair of custom shoes, for instance, is expensive, so we buy factory made shoes: shoes as a good instead of as a service. In doing so, we accept some limitations: a finite set of styles and sizes to choose from; perhaps a less-than-perfect fit for each individual foot; limited styles and customizations — but with the positive trade off in favor of greatly decreased cost. In much the same way, we consume the “good” of the string quartet in the form of a digital recording of a musical piece, instead of the “service” of a live performance. In short, turning services into goods industrializes the process, increasing efficiency and reducing cost.

But is this seemingly alchemical transformation possible in healthcare?

Until today, it’s essentially been accepted as a given that this cost “disease” is incurable where there’s the need for professional, highly trained people performing services — industries like healthcare, education — and therefore drives some of the biggest cost crises of our day, that affect many people in countless ways.

To cure Baumol’s cost disease, we would have to transform the industry’s professional human labor into something that can be manufactured, commoditized, industrialized, and automated. While this has long been an issue in healthcare, for many good and bad reasons, the cure involves bringing more artificial intelligence (AI) to the industry. AI creates a new opportunity: to transform services into goods.

It’s no magic bullet for sure; even our own a16z partners Martin Casado and Matt Bornstein have argued that in enterprise companies, this won’t work, and that AI in this case effectively just replaces human services with different human services with few gains, given all the data cleanup and edge cases involved. But in healthcare, unlike in other industries — like social media content analysis, or self-driving cars — the kind of data labelling needed is actually already an intrinsic part of the healthcare system. In much the same way it is an intrinsic part of Google search — where people choose the most relevant link in the search results, and Google’s AI learns from this, improving with each search — whenever a doctor diagnoses a condition, prescribes a mediation, or interprets an x-ray, that information is then encoded into the electronic health record (EHR). Or, it’s in revenue cycle management — how all bills are paid in healthcare — where people currently perform the manual tasks of identifying what is billable, and to whom. Using AI to learn from these coders (the way, for example, Alpha Health does) means the human work — human labeling — is “free”, since it’s part of what we’re doing anyway.

What’s more, the data is high quality, because when all the doctors in the system are labellers, AI ensures every doctor has the very best teachers in the world — no single doctor alone could ever have that roster of mentors. Training is done on all patients, AI learns from everything, and everybody… and then outputs the results back out to everyone.

Of course, it’s not a total walk in the park; work needs to be done to integrate this data into the system. One you solve data labelling, you have to train with those labels. Data labelling is just one of the reasons AI based businesses are perceived to have low margins (often requiring an enormous amount of GPU or CPU time, and at great expense. But human training is also expensive: training must often be customized to individuals, and often needs to be redone as employees churn. Because computers are identical, training AI has no such challenges. If you compare the cost of AI training to the cost of executing a simple algorithm,AI training is expensive. If you compare the cost of AI training to the cost of human training, AI is cheap. And, AI training gets exponentially cheaper over time, because of Moore’s Law’s profoundly powerful compounding effects. So even if using AI is at cost parity with a service solution now, the eventual win is obvious. And to some degree, we can commoditize the AI itself as well, for more efficiency, by keeping customization low and training rare with AI.

Another complaint about AI’s ability to transform services into goods is what’s referred to as the “long tail of tasks.” This is the idea that AI won’t be useful if it can only perform a small fraction of what humans can. But in healthcare, even a small fraction of that long tail can have enormous impact. With the right, highly efficient training and labeling, AI can transform perhaps 5% of the human labor of analyzing bills and claims to automate from services to goods. By using AI to learn from medical billing — even just by triaging the “easy” and mundane cases (and escalating the “long tail” of more complex tasks to people as needed) — can bring a dramatic cost savings. Not to mention allowing people to focus on the more higher order aspects of the job, allowing them to deliver better results and service.

We’ve been waiting decades — maybe even centuries — for the ability to reverse Baumol’s Cost Disease in our most service-heavy, yet most critical, industries, such as healthcare.

The transformation of services into goods won’t occur overnight. But Baumol himself couldn’t have foreseen the revolution that AI is creating, any more than someone in the Renaissance anticipating a shoe factory and Moore’s Law since. If applied in the right places, with the right conditions, taking into account the hard realities of the healthcare system, AI can be a vastly powerful lever to pull. We may not cure Baumol’s Cost Disease overnight, but even a small gain in cost and time savings would have huge impacts in healthcare.

Billionaire investor Charlie Munger has been vocal in expressing his concerns about U.S. healthcare, stating that it is “shot through with rampant waste” and has become “immoral.”

Munger says there are substantial problems that need to be addressed, including the presence of unnecessary costs and inefficiencies that plague the medical field.

Drawing a vivid analogy at a Daily Journal Annual Meeting, Munger compared the experience of a dying old person in many American hospitals to that of a carcass on the plains of Africa. He painted a bleak picture, describing how vultures, jackals, hyenas and other scavengers swarm around the helpless creature.

In an attempt to address these issues, Berkshire Hathaway, Amazon.com Inc., and JPMorgan Chase joined forces to establish Haven Healthcare a venture that despite their combined efforts failed to achieve its objectives.

Some startups have seen success where they failed. iRemedy, for example, is a startup using artificial intelligence (AI) technology, that offers a solution to the healthcare system’s challenges through its large procurement marketplace. Its platform streamlines the supply chain, enabling faster and more affordable access to lifesaving supplies for doctors, hospitals and healthcare providers.

Munger, vice chairman of Berkshire Hathaway Inc., criticized the high costs and inefficiencies in medical care as both expensive and wrong. In a CNBC interview, he went on to claim that some medical providers artificially prolong death to increase their profits.

With over 35 years of experience as board chairman of Good Samaritan Hospital in Los Angeles, Munger expressed his belief that certain healthcare practices are absurd.

“A lot of the medical care we do deliver is wrong — so expensive and wrong. It’s ridiculous,” he said in a “Squawk Box” interview.

In 2018, Munger predicted that when Democrats gain control of all three branches of government, there will be a push for a single-payer healthcare system. He highlighted the need for a complete change forced by the government because of the severity of the issues in the current system. He suggested that a universal healthcare system with an opt-out option would be a reasonable solution.

Warren Buffett, Munger’s longtime investing partner, shares similar concerns regarding healthcare spending, referring to it as a “tapeworm on the economic system.” Buffett believes the private sector can make substantial contributions to cost-reduction efforts.