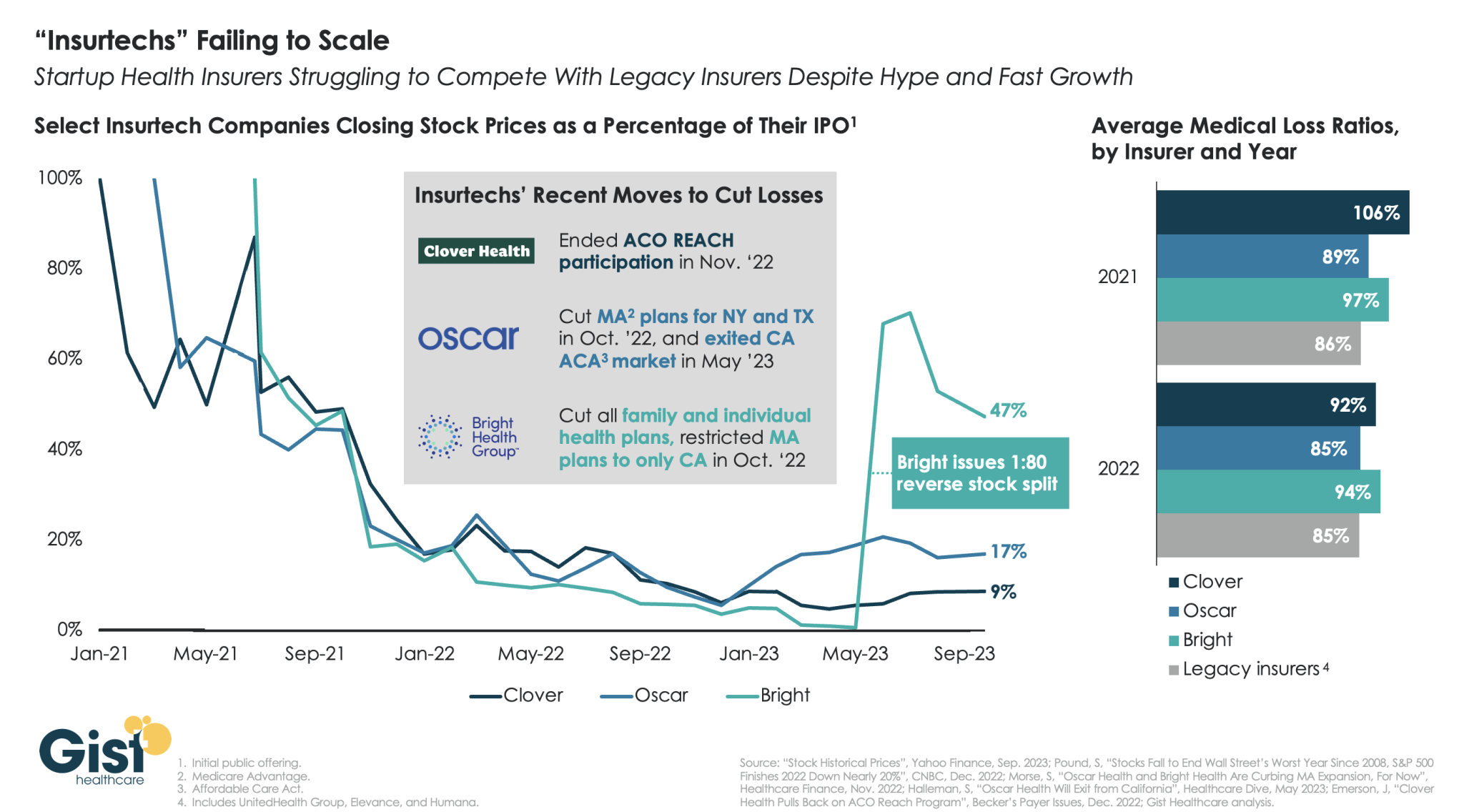

“Insurtechs” Clover Health, Oscar Health, and Bright Health all went public in the midst of the hot equity market of 2021. Investors were excited by the fast growth of these health insurer startups, and their potential to revolutionize an industry dominated by a few large players.

However, the hype has dissipated as financial performance has deteriorated. After growing at all costs during a period of low interest rates, changing market conditions directed investors to demand a pivot to profitability,which the companies have struggled to deliver—twoyears later,none of the three has turned a profit.

Oscar and Bright have cut back their market presence significantly, while Clover has mostly carried on while sustaining high losses. In the last two years, only Oscar has posted a medical loss ratio in line with other major payers, who meanwhile are reporting expectation-beating profits. While Oscar has shown signs of righting the ship since the appointment of former Aetna CEO Mark Bertolini,

the future of these small insurers remains uncertain. As their losses mount and they exit markets, they may become less desirable as acquisition targets for large payers.

This is Part 2 of a series by Cain Brothers about the first-ever collaboration conference between health systems and private equity (PE) investment firms. Part 1 of this series addressed the conference’s who, what and where. This commentary will focus on the why. We will explore the underlying forces uniting health systems with private equity during this period of unprecedented industry disruption.

Why Health Systems and PE Need Each Other

On June 13 and 14, 2023, Cain Brothers hosted the first-ever collaboration conference between health systems and private equity (PE) investment firms. Timing, market dynamics and opportunity aligned. The conference was an over-the-moon success. Along with its sponsors, Cain Brothers will seek to expand the conference and align initiatives through the coming years.

Why Now? Healthcare is Stuck and Needs Solutions

As a society, the U.S. is spending ever-higher amounts of money while its population is getting sicker. A maldistribution of facilities and practitioners creates inequitable access to healthcare services in lower-income communities with the highest levels of chronic disease.

New competitors and business models along with unfavorable macro forces, including high inflation, aging demographics and deteriorating payer mixes, are fundamentally challenging health systems’ status quo business practices.

Governments, particularly the federal government, have become healthcare’s largest payers, funding over 40% of healthcare’s projected $4.7 trillion expenditure in 2023. Individual patients often get lost in the massive payment shuffle between payers and providers.

Meanwhile, governments’ pockets are emptying. As a percentage of GDP, U.S. government debt obligations have grown from 55% in 2001 to 124% currently. With rising interest rates and the commensurate increase in debt service costs, as well as an aging population, there is little to suggest that new funding sources will emerge to fund expansive healthcare expenditures. Scarcity reigns where resources for healthcare providers were once plentiful.

As a consequence, the healthcare industry is entering a period of more fundamental economic limitations. Delaying transformation and expecting society to fund ongoing excess expenditure is not a sustainable long-term strategy. Current economic realities are forcing a dramatic reallocation of resources within the healthcare industry.

The healthcare industry will need to do more with less. Pleading poverty will fall on deaf ears. There will be winners and losers. The nation’s acute care footprint will shrink. For these reasons, health systems are experiencing unprecedented levels of financial distress. Indeed, parts of the system appear on the verge of collapse, particularly in medically underserved rural and urban communities.

More of the same approaches will yield more of the same dismal results. Waking up to this existential challenge, enlightened health systems have become more open to new business models and collaborative partnerships.

Necessity Stimulates Innovation

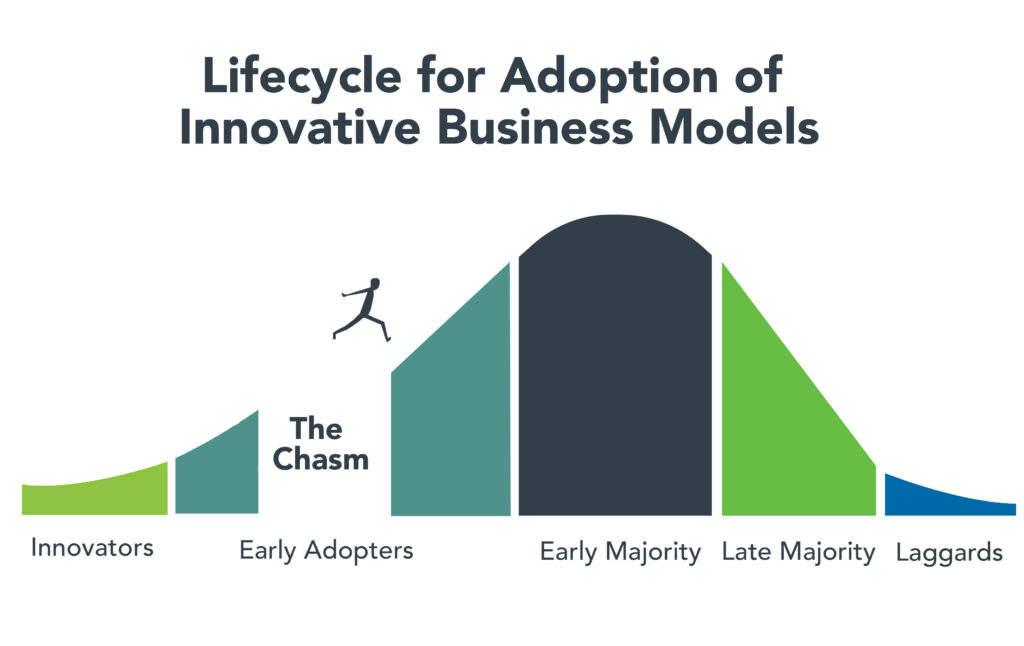

Two disruptive and value-based business models are on the verge of achieving critical mass. They are risk-bearing “payvider” companies (e.g. Kaiser, Oak Street Health and others) and consumer-friendly, digital-savvy delivery platforms (e.g. OneMedical and innumerable point-solution companies).

Value-based care providers and their investors have the scars and bruises to show for challenging entrenched business practices reliant on fee-for-service (FFS) business models and administrative services only (ASO) contracting. Incumbents have protected their privileged market position well through market leverage and outsized political influence.

Despite market resistance, “payvider” and digital platform companies are emerging from the proverbial “innovators’ chasm.” More early adopters, including those health systems attending the Nashville conference, are embracing value-creating business models. The chart below illustrates the well-trodden path innovation takes to achieve market penetration.

Ironically, during this period of industry disruption, health systems understand they need to deliver greater value to customers to maintain market relevance. It will require great execution and overcoming legacy practices to develop business platforms that incorporate the following value-creating capabilities:

Decentralized care delivery (to make care more accessible and lower cost).

Root-cause treatment of chronic conditions.

Integrated physical and mental healthcare services.

Consistent, high-quality consumer experience.

Coordinated service delivery.

Standardized protocols that improve care quality and outcomes.

A truly patient/customer-centric operating orientation.

It’s not what to do, it’s how to get it done that creates the vexing conundrum. Solutions require collaboration. Platform business models replete with strategic partnerships are emerging. Paraphrasing an African proverb, it’s going to take a village to fix healthcare. That’s why the moment for health systems and PE firms to collaborate is now.

PE to the Rescue?

Private equity has become the dominant investment channel for business growth across industries and nations. According to a recent McKinsey report, PE has more than $11.7 trillion in assets under management globally. This is a massive number that has grown steadily. PE changes markets. It turbocharges productivity. It is a relentless force for value creation.

By investing in a wide spectrum of asset classes, private equity has become a vital source of investment returns for pensions, endowments, sovereign wealth funds and insurance companies. Healthcare, given its size and inefficiencies, is a target-rich environment for PE investment and returns. This explains the PE’s growing interest in working with health systems to develop mutually beneficial, value-creating healthcare enterprises.

Despite reports to the contrary, PE firms must invest for the long term. Unlike the stock market, where investors can buy and sell a stock within a matter of seconds, PE firms do not have that luxury. To generate a return, they must acquire and grow businesses over a period of years to create suitable exit strategies.

Money talks. By definition, all buyers of new companies value their purchase more than the capital required for the acquisition. In making purchase decisions, buyers evaluate businesses’ past performance. They also assess how the new business will perform under their stewardship. PE or PE-backed acquirers also consider which future buyers will be most likely acquire the company after a five-plus year development period.

PE’s investment approach can align well with health systems looking to create sustainable long-term businesses tied to their brands and market positioning. PE firms buy and build companies that attract customers, employees and capital over the long term, far beyond their typical five- to seven-year ownership period. Health systems that partner with PE firms to develop companies are the logical acquirers of those companies if they succeed in the marketplace. In this way, a rising valuation creates value for both health systems and their PE partners.

It is important to note that not all PE are created the same. Like health systems, PE firms differ in size, market orientation, investment theses, experience and partner expectations. Given this inherent diversity, it takes time, effort and a shared commitment to value creation for health systems and PE firms to determine whether to become strategic partners. Not all of these partnerships will succeed, but some will succeed spectacularly.

For health system-PE partnerships to work, the principals must align on strategic objectives, governance, performance targets and reporting guidelines. Trust, honest communication and clear expectations are the key ingredients that enable these partnerships to overcome short-term hurdles on the road to long-term success.

Conclusion: Time to Slay Healthcare’s Dragons

Market corrections are hard. As a nation, the U.S. has invested too heavily in hospital-centric, disease-centric, volume-centric healthcare delivery. The result is a fragmented, high-cost system that fails both consumers and caregivers. The marketplace is working to reallocate resources away from failing business practices and into value-creating enterprises that deliver better care outcomes at lower costs with much less friction.

Progressive health systems and PE firms share the goal of creating better healthcare for more Americans. Cain Brothers is committed to advancing collaboration between health systems and PE-backed companies. In addition to the Nashville conference, the firm has combined its historically separate corporate and non-profit coverage groups to foster idea exchange, expand sector understanding and deliver higher value to clients.

The ability to connect and collaborate effectively with private equity to advance business models will differentiate winning health systems. In a consolidating industry, this differentiation is a prerequisite for sustaining competitiveness. It’s adapt or die time. Health systems that proactively embrace transformation will control their future destiny. Those that fail to do so will lose market relevance.

The future of healthcare is not a zero-sum equation. Markets evolve by creating more complex win-win arrangements that create value for customers. No industry requires restructuring more than healthcare. As a nation and an industry, we have the capacity to fix America’s broken healthcare system. The real question is whether we have the collective will, creativity and resourcefulness to power the transformation. We believe the answer to that question is yes.

Paraphrasing Rev. Theodore Parker, the economic arc of the marketplace is long but it bends toward value. Together, health systems and PE firms can power value-creation and transformation more effectively than either sector can do independently. Each needs the other to succeed. Slaying healthcare’s dragons will not be easy but it is doable. It’s going to take a village to fix healthcare.

Costco is now offering members online health checkups for as low as $29.

The retailer is offering the new service in partnership with Sesame, a direct-to-consumer health care marketplace that connects medical providers nationwide with consumers.

Sesame, in a release, said Costco members beginning Monday can book health care visits directly through their memberships in all 50 states.

The New York-based company said its platform doesn’t accept health insurance because it primarily caters to uninsured Americans and those with high-deductible plans who prefer to pay cash for their health care. It said its model helps keep prices of services low for its users.

The services listed on Costco Pharmacy’s homepage, include virtual primary care visits for $29, health checkups (a standard lab panel and a virtual follow-up consultation with a provider) for just $72 and online mental health visits for $79.

“Quality, great value, and low price are what the Costco brand is known for,” David Goldhill, Sesame’s co-founder and CEO, said in a statement. “When it comes to health care, Sesame also delivers high quality and great value – and a low price that will be appreciated by Costco Members when it comes to their own care.”

Amazon, in August, announced that its virtual clinic was now also available nationwide. Amazon Clinic launched last November offering 24/7 access to third-party health-care providers directly on Amazon’s website and mobile app.

Amazon customers, through the clinic, can access telehealth treatment for dozens of common conditions, such as pink eye, urinary tract infections and hair loss, the retailer said.

Other retailers, including CVS to Walgreens to Walmart, have made similar moves.

Blue Shield of California announced a plan to diversify its pharmacy benefit management (PBM) contracts in a bid to improve transparency and reduce costs.

Instead of relying on Woonsocket, RI-based CVS Health’s Caremark as its sole PBM, the health plan and its 4.8M members will be served by five companies, including Amazon Pharmacy for at-home deliveries, Mark Cuban Cost Plus Drugs Company (MCCPDC) for a transparent pricing model, and Prime Therapeutics for negotiations with pharmaceutical companies.

Caremark will remain responsible for Blue Shield’s specialty pharmacy needs, which CVS noted in an investor filing represents over 50 percent of nationwide pharmacy benefit spending.

Blue Shield intends to implement this new system by 2025, and is targeting savings of $500M annually, which translates to 10 to 15 percent of its current spending.

The Gist: Whether Blue Shield saves money with this initiative depends on the whether the benefit of competition in its PBM contracts outweighs the costs of more complex coordination between vendors.

Keeping half of its business tied up with CVS through specialty pharmacy will further limit the potential impact. Nonetheless, it’s noteworthy that pharmacy disruptors like Amazon and MCCPDC have found a major health plan willing to work with them.

Consumers, employers, payers without PBMs, and members of Congress are increasingly dissatisfied with the current pharmacy benefit market structure, and Blue Shield’s move could serve as a catalyst for future shakeups.

Value-based healthcare, the holy grail of American medicine, has three parts: excellent clinical quality, convenient access and affordability for all.

And as with the holy grail of medieval legend, the quest for value-based care has been filled with failure.

In the 20th century, U.S. medical groups and hospital systems could—at best—achieve two elements of value-based care, but always at the sacrifice of the third. Until recently, American medicine lacked the clinical knowhow, technology and operational excellence to accomplish all three, simultaneously. We now have the tools. The only thing missing is “system-ness.”

What Is System-ness?

System-ness is the effective and efficient coordination of healthcare’s many parts: outpatient and inpatient, primary and specialty care, financing and care delivery, prevention and treatment.

By bringing these disparate pieces together within a well-functioning system, healthcare providers have the opportunity to maximize clinical outcomes, weed out waste, lower overall costs and provide greater levels of convenience and access.

Who Are The Search Parties?

In the future, system-ness will be the variable that determines whether healthcare transformation is led by (a) incumbent health systems like Kaiser Permanente and Geisinger Health or (b) the retail giants like Amazon, CVS and Walmart. The latter group has become an ever-growing threat in the healthcare arms race, quickly amassing their own (though still modest) systems of care through billion-dollar acquisitions.

Although both the incumbents and new entrants will struggle to implement value-based care on a national scale, the victor stands to earn hundreds of billions of dollars in added revenue and tens of billions in profits.

To better understand the power of system-ness, and the challenges all organizations will face in providing it, here are three examples of value-based-care solutions implemented successfully by Kaiser Permanente.

1. Preventing Problems, Managing Disease

Research demonstrates that preventive medicine and early intervention reduce heart attacks, strokes and cancer. Yet our nation falls far short in these areas when compared to its global peers.

One example is hypertension, the leading cause of strokes and a major contributor to heart attacks. With help from doctors, nearly all patients can keep high blood pressure under control. Yet, nationally, hypertension is controlled only 60% of the time.

We see similarly poor rates of performance when it comes to prevention and screening for cancers of the colon, breast and lung.

Undoing these troubling trends requires system-ness. In Kaiser Permanente, 90% of patients had their blood pressure controlled and were screened for cancer. Getting there required a comprehensive electronic health record, a willingness for every doctor (regardless of specialty) to focus on prevention, leadership that communicated the value of prevention and a salary structure that rewarded group excellence.

2. Continuous Care, Without Interruption

Most doctors’ offices are open Monday to Friday during normal business hours—only one-fourth of the time that a medical problem might occur.

At night and on weekends, patients have no choice but to visit ERs. There, they often wait hours for care, surrounded by people with communicable diseases. Their non-emergent problems generate bills 12-times higher than if they’d waited to be seen in a doctor’s office.

There’s a better way. In large-enough medical groups, hundreds of clinicians can provide round-the-clock care on a rotating, virtual basis—using video to assess patients and make evidence-based recommendations.

This approach, pioneered by physicians in the Mid-Atlantic Permanente Medical group, solved the patient’s problem immediately 70% of the time without a trip to the ER and, for the other 30%, enabled coordination of medical care with the ER staff.

3. Specialized Medicine, Immediate Attention

When a primary care physician needs added expertise (from a dermatologist, urologist or orthopedist), it’s usually the responsibility of the patient to make their own specialty appointments, check with insurance for coverage and provide their medical records.

This takes hours or days to coordinate and can delay care by weeks, resulting in avoidable complications.

But in a well-structured system, there’s no need to wait. Using telehealth tools at Kaiser Permanente, primary care doctors can connect instantly with dozens of different specialists—often while the patient is still in the exam room. Once connected, the specialist evaluates the patient and provides immediate expertise.

This way, care is not only faster and less expensive, but also better coordinated. Data from within Kaiser Permanente show that these virtual consultations resolve the patient’s problem 40% of the time without having to schedule another appointment. For the other 60%, the diagnostic process can begin immediately.

The Foundations For System-ness

Few organizations in the U.S. can or do offer these system-based improvements. Doing so requires skilled physician leadership, a shift in the financial model and a willingness to accept risk.

In fact, most organizations across the U.S. that claim to operate “value-based” systems actually rely on doctors who are scattered across the community, disconnected from each other and paid on the basis of volume (fee-for-service) rather than value (capitation).

As a result, patient care is fragmented and uncoordinated, leading to repeated tests and ineffective treatments, thus increasing medical costs and compromising medical outcomes.

Value-based care (superior quality, access and affordability) requires teams of clinicians working together as one—all paid on a capitated basis.

Without capitation, dermatologists will insist on seeing every patient in their office where they can bill insurance five-times more than with a tele-dermatology visit. And gastroenterology specialists will insist that all patients have colonoscopy rather than recommending low-risk patients do a safe, convenient, at-home colon cancer screening (called a fecal immunochemical test or “FIT”) at 5% of the cost.

In these cases, individual doctors don’t consciously make care inconvenient for patients. Rather, it is the only choice they have when working in a fee-for-service payment model. Ultimately, system-ness is best achieved when health systems are integrated, prepaid, tech-enabled and physician-led.

Amazon, CVS, Walmart Know About Systems

These three companies are global leaders in “system-ness,” at least in retail. Combined, they have a market cap of $1.88 trillion, employ 3.4 million Americans and are looking to take a slice of U.S. healthcare’s $4.3 trillion annual expenditures.

Already, they manage complex order-entry and fulfillment systems. They use technology to streamline everything from customer service to supply-chain management. They are led through a clear and effective reporting structure.

In terms of competing for healthcare’s holy grail, these are huge competitive advantages compared to today’s uncoordinated, individualized, leaderless healthcare industry.

As retailers vie to bring their system knowhow to American medicine, they are acquiring the pieces needed to compete with the healthcare incumbents. They’ve spent tens of billions of dollars on medical groups that are committed to value-based care (One Medical, Oak Street Health, etc.). They’ve also spent massive sums on home-health companies (Signify) and on pharmacies (PillPak), along with expanding their in-store, at-home and online care options. Many of these care-delivery subsidiaries are focused on Medicare Advantage, the capitated half of Medicare where financial success is dependent on high quality medical care provided at lower cost.

What’s more, all these retailers have a national presence with brick-and mortar facilities in nearly every community in the country—a leg up on nearly every existing health system.

Who Will Win—And Why?

Trying to pick the victor in the battle to transform American medicine at this point is like selecting the winner of a heavy-weight championship boxing match after three evenly matched rounds. Intangibles like stamina, courage and willingness to absorb pain have yet to be tested.

In The Innovator’s Dilemma, the late Clayton Christensen examined historical battles between incumbent organizations and new entrants. After analyzing dozens of industries, he concluded new entrants routinely become the victors because the incumbents move too slowly and fail to embrace the need for major change.

And from that perspective, if I had to wager, I’d put my money on the retail giants.

But there’s an even more worrisome potential outcome: neither those inside nor outside of healthcare will make the necessary investments or accept the risk of leading systemic change. As a result, the movement toward value-based healthcare will stall and die.

In that context, purchasers of healthcare (businesses, the government and patients) will encounter a difficult reality: over the next eight years, medical costs will nearly double, creating an unaffordable and unsustainable scenario. As a result, our nation will likely experience reduced medical coverage, increased rationing, ever-longer delays for care and a growth in health disparities.

If that day arrives, our country will regret its inaction.

For decades, research studies and news stories have concluded the American system is ineffective,

too expensive and falling further behind its international peers in important measures of performance: life expectancy, chronic-disease management and incidence of medical error.

As patients and healthcare professionals search for viable alternatives to the status quo, a recent mega-merger is raising new questions about the future of medicine.

In April, Kaiser Permanente acquired Geisinger Health under the banner of newly formed Risant Health. With more than 185 years of combined care-delivery experience, Kaiser and Geisinger have long been held up as role models of the value-based care movement.

Eyeing the development, many speculated whether this deal will (a) ignite widespread healthcare transformation or (b) prove to be a desperate attempt at relevance (Kaiser) or survival (Geisinger).

Whether incumbents like Kaiser Permanente and Geisinger can lead a national healthcare transformation or are displaced by new entrants will depend largely on whether they can deliver value-based care on a national scale.

In Search Of Healthcare’s Holy Grail

Value-based care—the simultaneous provision of high quality, convenient and affordable medical care—has long been the aim of leading health systems like Kaiser, Geisinger, Mayo Clinic, Cleveland Clinic and dozens more.

But results to-date have often failed to match the vision.

The need for value-based care is urgent. That’s because U.S. health and economic problems are expected to get worse, not better, over the next decade. According to federal governmental actuaries, healthcare expenditures will rise from $4.2 trillion today to $7.2 trillion by 2031. At that time, these costs are predicted to consume an estimated 19.6% of the U.S. Gross Domestic Product.

Put simply: The U.S. will nearly double the cost of medical care without dramatically improving the health of the nation.

For decades, health policy experts have pointed out the inefficiencies in medical care delivery. Research has estimated that inappropriate tests and ineffective procedures account for more than 30% of all money spent on American medical care.

This combination of troubling economics and untapped opportunity explain why value-based care has become medicine’s holy grail. What’s uncertain is whether the transformation in healthcare delivery and financing will be led from inside or outside the healthcare system.

Where The Health-System Hopes Hang

For years, Kaiser Permanente has led the nation in clinical quality and patient outcomes based on independent, third-party research via the National Committee for Quality Assurance (NCQA) and Medicare Star ratings. Similarly, Geisinger was praised by President Obama for delivering high-quality care at a cost well below the national average.

And yet, these organizations, and many other highly regarded national and regional health systems, are extremely vulnerable to disruption, especially when their strategy and operational decisions fail to align.

Kaiser, for its part, has struggled with growth while Geisinger’s care-delivery strategy has proven unsuccessful in recent years. Failed expansion efforts forced KP to exit multiple U.S. markets, including New York, North Carolina, Kansas and Texas. More recently, several of its existing regions have failed to grow market share and weakened financially.

Meanwhile, Geisinger has fallen on hard times after decades of market domination. As Bob Herman reported in STAT News: “Failed acquisitions, antitrust scrutiny, leadership changes, growing competition from local players, and a pandemic that temporarily upended how patients got care have forced Geisinger to abandon its independence. The system is coming off a year in which it lost $240 million from its patient care and insurance operations.”

Putting the pieces together, I believe the Kaiser-Geisinger deal represents an industry undergoing massive change as health systems face intensifying pressure from insurers and a growing threat from retailers like Amazon, CVS and Walmart. This upcoming battle over the future of value-based care represents a classic conflict between incumbents and new entrants.

Can The World’s Largest Companies Disrupt U.S. Healthcare?

Retail giants, including Amazon, Walmart and CVS, are among the nation’s 10 largest companies based on annual revenue.

They have a broad geographic presence and strong relationships with almost all self-funded businesses. Nearly all have acquired the necessary healthcare pieces—including clinicians, home-health services, pharmacies, insurance arms and electronic medical record systems—to replace the current medical system.

And yet, while these companies expand into medical care and financing, their core businesses are struggling, resulting in announced store closures and layoffs. As newcomers to the healthcare market, they have been forced to pay premium dollars to acquire parts of the delivery system. All have a steep learning curve ahead of them.

The Challenge Of Healthcare Transformation

American medicine is a conglomerate of monopolies(insurers, hospitals, drug companies and private-equity-owned medical practices). Each works to maximize its own revenue and profit. All are unwilling to innovate in ways that benefit patients when doing so comes at the sacrifice of financial performance.

One problem stands at the center of America’s soaring healthcare costs: the way doctors, hospitals and drug companies are paid.

The dominant payment methodology in the United States, fee-for-service, rewards healthcare providers for charging higher prices and increasing the number (and complexity) of services offered—even when they provide no added value.

The message to doctors and hospitals is clear: The more you do, and the greater market control you have, the higher your income and profit. This is the antithesis of value-based care.

The alternative to fee-for-service payments, capitation, involves paying a single, up-front sum to the providers of care (doctors and hospitals) to cover the total annual cost for a population of patients. This model, unlike fee-for-service, rewards effectiveness and efficiency. Capitation creates incentives to prevent disease, reduce complications from chronic illness, and diminish the inefficiencies and redundancies present in care delivery. Capitated health systems that can prevent heart attacks, strokes and cancer better than others are more successful financially as a result.

However, it’s harder than it sounds to translate what’s best for patients into everyday decisions and actions. It’s one thing to accept a capitated payment with the intent to implement value-based care. It’s another to put in place the complex operational improvements needed for success. Here are the roadblocks that Kaiser-Geisinger will face, followed by those the retail giants will encounter.

3 Challenges For Kaiser-Geisinger:

Involving Clinical Experts. Kaiser Permanente is a two-part organization and when the insurance half (Kaiser) decided to acquire Geisinger, it did so without input or involvement from the half of the organization responsible for care-delivery (Permanente). This spells trouble for Geisinger, which must navigate a complex turnaround without the operational expertise or processes from Permanente that, in the past, helped Kaiser Permanente grow market share and lead the nation in clinical quality.

Going All In. To meet the healthcare needs of most its patients, Geisinger relies on community doctors who are paid on a fee-for-service basis. Generally, the fee-for-service model is predicated on the assumption that higher quality and greater convenience require higher prices and increased costs. With Geisinger’s distributed model, it’ll be very difficult to deliver consistent, value-based care.

Inspired Leadership. Major improvements in care delivery require skilled leadership with the authority to drive clinical change. In Kaiser Permanente, that comes through the medical group and its physician CEO. In Geisinger’s hybrid model, independent doctors have no direct oversight or central accountability structure. Although Risant Health could be an engine for value-based medical care, it’s more likely to serve the role of a “holding company,” capable of recommending operational improvements but incapable of driving meaningful change.

3 Challenges For The Retail Giants:

More Medical Offerings. Amazon, Walmart and CVS are successfully acquiring primary care (and associated telehealth) services. But competing with leading health systems will require a more wholistic, system-based approach to keep medical care affordable. This won’t be easy. To avoid ineffective, expensive specialty and hospital services, they will need to hire their own specialists to consult with their primary care doctors. And they will have to establish centers of excellence to provide heart surgery, cancer treatment, orthopedic care and more with industry-leading outcomes. But to meet the day-to-day and emergent needs of patients, they also will have to establish contracts with specialists and hospitals in every community they serve.

Capitalizing On Capitation. Already, the retail giants have acquired organizations well-versed in delivering patient care through Medicare Advantage, a capitated alternative to traditional (fee-for-service) Medicare plans. It’s a good start. But the retailers must do more than dip a toe in value-based care models. They must find ways to gain sufficient experience with capitation and translate that success into value-based contracts with self-funded businesses, which insure tens of millions of patients.

Defining Leadership. Without an effective and proven clinical leadership structure, the retail giants will be no more effective than their mainstream competitors when it comes to implementing improvements and shifting the culture of medicine to one that is customer- and service-focused.

Be they incumbents or new entrants, every contender will hit a wall if they cling to today’s failing care delivery model. The secret ingredient, which most lack and all will need to embrace in the future, is system-ness.

For all of the hype surrounding value-based care, fragmentation and fee-for-service are far more common in American healthcare today than integration and capitation.

Part two of this article will focus on how these different organizations—one set inside and one set outside of medicine—can make the leap forward with system-ness. And, in the end, you’ll see who is most likely to emerge victorious.

Pay attention to the media coverage around artificial intelligence, and it’s easy to get the sense that technologies such as chatbots pose an “existential crisis” to everything from the economy to democracy.

These threats are real, and proactive regulation is crucial. But it’s also important to highlight AI’s many positive applications, especially in health care.

Consider the Mayo Clinic, the largest integrated, nonprofit medical practice in the world, which has created more than 160 AI algorithms in cardiology, neurology, radiology and other specialties. Forty of those have already been deployed in patient care.

To better understand how AI is used in medicine, I spoke with John Halamka, a physician trained in medical informatics who is president of Mayo Clinic Platform. As he explained to me, “AI is just the simulation of human intelligence via machines.”

Halamka distinguished between predictive and generative AI. The former involves mathematical models that use patterns from the past to predict the future; the latter uses text or images to generate a sort of human-like interaction.

It’s that first type that’s most valuable to medicine today. As Halamka described, predictive AI can look at the experiences of millions of patients and their illnesses to help answer a simple question: “What can we do to ensure that you have the best journey possible with the fewest potholes along the way?”

For instance, let’s say someone is diagnosed with Type 2 diabetes. Instead of giving generic recommendations for anyone with the condition, an algorithm can predict the best care plan for that patient using their age, geography, racial and ethnic background, existing medical conditions and nutritional habits.

This kind of patient-centered treatment isn’t new; physicians have long been individualizing recommendations. So in this sense, predictive AI is just one more tool to aid in clinical decision-making.

The quality of the algorithm depends on the quantity and diversity of data. I was astounded to learn that the Mayo Clinic team has signed data-partnering agreements with clinical systems across the United States and globally, including in Canada, Brazil and Israel. By the end of 2023, Halamka expects the network of organizations to encompass more than 100 million patients whose medical records, with identifying information removed, will be used to improve care for others.

Predictive AI can also augment diagnoses. For example, to detect colon cancer, standard practice is for gastroenterologists to perform a colonoscopy and manually identify and remove precancerous polyps. But some studies estimate that 1 in 4 cancerous lesions are missed during screening colonoscopies.

Predictive AI can dramatically improve detection. The software has been “trained” to identify polyps by looking at many pictures of them, and when it detects one during the colonoscopy, it alerts the physician to take a closer look. One randomized controlled trial at eight centers in the United States, Britain and Italy found that using such AI reduced the miss rate of potentially cancerous lesions by more than half, from 32.4 percent to 15.5 percent.

Halamka made a provocative statement that within the next five years, it could be considered malpractice not to use AI in colorectal cancer screening.

But he was also careful to point out that “it’s not AI replacing a doctor, but AI augmenting a doctor to provide additional insight.” There is so much unmet need that technology won’t reduce the need for health-care providers; instead, he argued, “we’ll be able to see more patients and across more geographies.”

Generative AI, on the other hand, is a “completely different kind of animal,” Halamka said. Some tools, such as ChatGPT, are trained on un-curated materials found on the internet. Because the inputs themselves contain inaccurate information, the models can produce inappropriate and misleading text. Moreover, whereas the quality of predictive AI can be measured, generative AI models produce different answers to the same question each time, making validation more challenging.

At the moment, there are too many concerns over quality and accuracy for generative AI to direct clinical care. Still, it holds tremendous potential as a method to reduce administrative burden. Some clinics are already using apps that automatically transcribe a patient’s visit. Instead of creating the medical record from scratch, physicians would edit the transcript, saving them valuable time.

Though Halamka is clearly a proponent of AI’s use in medicine, he urges federal oversight. Just as the Food and Drug Administration vets new medications, there should be a process to independently validate algorithms and share results publicly. Moreover, Halamka is championing efforts to prevent the perpetuation of existing biases in health care in AI applications.

This is a cautious and thoughtful approach. Just like any tool, AI must be studied rigorously and deployed carefully, while heeding the warning to “first, do no harm.”

Nevertheless, AI holds incredible promise to make health care safer, more accessible and more equitable.

Walmart Health opened three new clinics in Jacksonville, Fla., starting June 6 as the company continues its push into retail healthcare, the Florida Times-Union reported.

The retail giant now has more than 30 Walmart Health centers across Florida, Arkansas, Georgia, Illinois and Texas, with plans to grow to 77 by the end of 2024 and expand into Arizona and Missouri.

Florida is one of Walmart Health’s biggest markets, with 22 coming to the state by fall 2023. They are also located in the Orlando and Tampa metro areas. They include medical, dental, vision, hearing and behavioral health services.

“With only one primary care doctor per 1,380 Florida residents, these Walmart Health centers will help address the demand for care in three major cities in the Sunshine State,” David Carmouche, MD, senior vice president of omnichannel care offerings for Walmart, said in a 2022 Times-Unionstory. “We are part of these communities, and we are excited to bring more options for in-person and telehealth care services to our neighbors. We’re making healthcare available when and where you may need it.”

Not-for-profit hospitals and health systems rely on three interdependent functions to contribute to the financial resilience of the organization: namely, the ability to withstand adverse changes to these core functions and continue to provide services to the community (Figure above).

The Operating Function:

The Operating Function manages the portfolio of clinical services and strategic initiatives that define the charitable mission of the organization. Clinical services generate patient revenue, and if that revenue creates a positive margin (i.e., exceeds expenses), that excess is invested back into the health system. Operating margins are, on average, very low in not-for-profit healthcare. For example, for the not-for-profit hospitals and health systems rated by Moody’s Investors Service, median operating margins from 2017–2021 ranged between 2.1% and 2.9%. These rated organizations represent only a few hundred of the thousands of hospitals and health systems in the country and are among the most financially healthy. A 2018 study of a wider group of more than 2,800 hospitals found an average clinical operating margin of -2.7%.

The Finance Function:

Because the positive margins generated by the Operating Function are rarely enough to support the intensive capital needs of maintaining and improving acute-care facilities, care delivery models, and technology, not-for-profit health systems rely on the Finance Function for internal and external capital formation. The Finance Function builds cash reserves and secures external financing

(e.g., bond proceeds, bank lines of credit) to support the capital spending needs of the organization. The cash reserves maintained by the Finance Function also help the organization meet daily expenses at times when expenses exceed revenues.

The Investment Function:

Not-for-profit hospitals and health systems will also endeavor to invest some of their cash reserves to generate returns that, first, act as an additional hedge against potential risks that could disrupt operations or cash flow, and second, pursue independent returns. Any independent returns generated serve as an important supplement to revenues generated through the Operating Function.

The three functions described above are common to all not-for-profit organizations. The main differences are mostly within the Operating Function. In higher education, for example, tuition revenue takes the place of clinical revenue. While higher education also maintains enterprise risk, the Operating Function for colleges and universities is less vulnerable to volume swings as enrollment is typically steady and predictable. Likewise, higher education is less labor intensive than healthcare.

Financial reserves include all liquid cash resources and unrestricted investments held in the Finance and Investment Functions. These reserves are equivalent to the emergency funds individuals are encouraged to maintain to help them meet living expenses for six to twelve months in case of a job loss or other disruption to income.

Absolute reserve levels are important, as discussed above, but they must also be viewed relative to a hospital’s daily operating expenses. A common

metric used to describe these reserves is Days Cash on Hand. If an organization has 250 Days Cash on Hand, that means that it would be able to meet its operating expenses for 250 days if revenue was suddenly shut off. The size of Days Cash on Hand will be proportionate to the size of the hospital and health system. Some of the largest not-for-profit health systems have annual operating expenses approaching $30 billion annually: meeting those expenses for 250 days would require Days Cash on Hand of more than $20 billion.

The shutdown that occurred in the early days of the pandemic (March through May 2020) is an example of a time when cash flow nearly shut off for most hospitals (except for emergency care). Reserves, measured in absolute and relative terms such as Days Cash on Hand, allowed hospitals that were nearly empty to maintain staffing and operations throughout the period. Other hospitals that were inundated with patients during the initial surge were able to fund increased staffing and personal protective equipment costs through their reserves. Other examples of how reserves provide a buffer

against unexpected events include natural disasters such as hurricanes, tornadoes, deep freezes, and wildfires, which can require the temporary shutdown of operations; cyberattacks, which can halt a hospital’s ability to provide services; a defunct payer that is unable to reimburse hospitals for care already provided; or an escalation in labor costs as experienced by many during 2022.

Without the reserves to pay for contract labor or premium pay, many hospitals would have undoubtedly had to close or limit services to their community.

KEY TAKEAWAYS

Financial reserves are created through the interdependent relationship of operating, finance, and investment functions in not-for-profit health systems.

These reserves build financial resilience: the ability to withstand adverse changes to core functions and continue to provide services to the community.

Financial reserves play an important role in supplementing any shortfalls in revenue or capital formation in one or more of these three functions.

Financial reserves are equivalent to individual emergency funds—both are intended to cover expenses if income or revenue flows are significantly disrupted.

A common metric used to describe financial reserves is Days Cash on Hand: an organization’s combined liquid, unrestricted cash resources and investments, measured by how many days these reserves could cover operating expenses if cash flows were suddenly shut off.

Financial reserves, measured in absolute and relative terms such as Days Cash on Hand, allowed hospitals that were nearly empty during the early days of the pandemic to maintain staffing and operations throughout the period. Other hospitals that were inundated with patients during the initial surge were able to fund increased staffing and personal protective equipment costs through their reserves.

A Comparison: Financial Reserves and Higher Education Not-for-Profits

Not-for-profit hospitals and health systems are not alone in their reliance on financial reserves; most not-for-profit organizations carry reserves that enable them to maintain operations and make needed investments even in times of weaker operating performance. Higher education is probably most comparable to healthcare, with significant overlaps between the two sectors. Moody’s Investors Service, one of the three major rating agencies, notes that 16% of its rated higher education institutions have affiliated academic medical centers (AMCs), and revenue from patient care at these AMCs contributes to 28% of the overall revenues for the higher education sector.

The magnitude of Days Cash on Hand levels varies by industry; financial reserves maintained by private not-for-profit higher education

institutions, for example, are significantly greater than those maintained by not-for-profit hospitals and health systems. For comprehensive private universities across all rating categories, Moody’s reports median Days Cash on Hand in 2021 of 498 days for assets that could be liquidated within a year. This compares with a median 265 Days Cash on Hand in 2021 across all freestanding hospitals, single-state, and multi-state healthcare systems rated by Moody’s.

Financial reserves are a critical measure of financial health across both healthcare and higher education. They help ensure that not-for-profit colleges, universities, hospitals, and health systems can continue to fulfill their vital societal functions when operations are disrupted, or when they are experiencing a period of sustained financial distress.

American Hospitals is the fourth in a series of documentaries produced by the Unfinished Business Foundation, founded by Richard Master, CEO of MCS Industries Inc., who took a deep dive into the economics of the U.S. health-care system after his company was hit year after year with double-digit health insurance rate increases.

Master teamed up with filmmaker Vincent Mondillo to produce Fix It: Healthcare at the Tipping Point; Big Pharma: Market Failure; Big Money Agenda: Democracy on the Brink, and now, American Hospitals.

A provocative look at the cost and inequities of American Hospitals, often more motivated by money and power than in providing for the health needs of individuals and the communities they were founded to serve. From the filmmakers behind the hit documentaries Fix It: Healthcare at the Tipping Point, Big Money Agenda, and Big Pharma.

Learn more and find out where to see the latest film at fixithealthcare.com/events