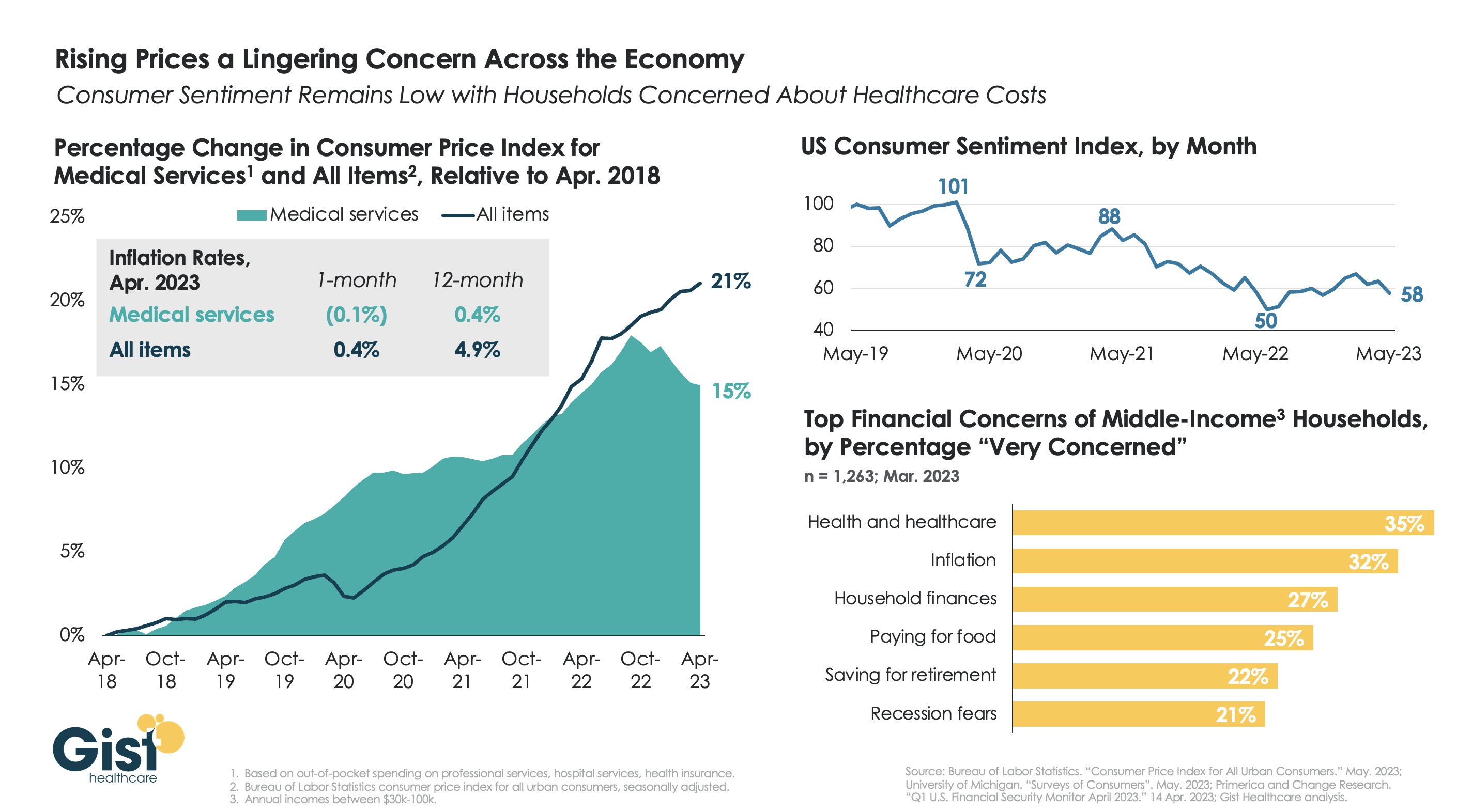

With the latest Bureau of Labor Statistics’ Consumer Price Index (CPI) report revealing the 12-month inflation rate in April 2023 rose again after hitting a recent low in March, we’re using this week’s graphic to show the cumulative picture on price and consumer sentiment changes across the last five years.

Since 2018, the CPI for all goods has risen 21 percent, while medical services have become 15 percent more expensive, in terms of consumer out-of-pocket spending. Leading into COVID, medical service prices were rising faster than general inflation, but the cumulative rise in the price of all goods caught up to medical services in early 2022.

Since December of last year, the price of medical services has actually experienced some deflation, partly due to a lagging decline in insurer profits. Reports of easing inflation had elicited a slight rebound in consumer sentiment, but last month’s 9 percent drop, the largest since June 2022, suggests this confidence is easily shaken.

Unfortunately for healthcare providers, according to a recent poll, fewer consumers worrying about elevated grocery and gas prices means that healthcare has reclaimed the top spot for household financial concerns.

A lack of data about Medicare Advantage plans means there are several unanswered questions about the program, according to an analysis from Kaiser Family Foundation.

The analysis, published April 25, breaks down the kinds of Medicare Advantage data not publicly available. Some missing data is not collected from insurers by CMS, and some data is collected by the agency but not available to the public.

Here are five questions researchers can’t answer without more data, according to Kaiser Family Foundation:

Insurers are not required to report how many enrollees use supplemental benefits and if members incur out-of-pocket costs with their supplemental benefits. Without this data, researchers can’t answer what share of enrollees use their supplemental benefits, how much members spend out of pocket for supplemental benefits, and if these benefits are working to achieve better health outcomes.

CMS does not require Medicare Advantage plans to report prior authorizations by type of service. Without more granular data, researchers can’t determine which services have the highest rates of denial and if prior authorization rates vary across insurers and plans.

Insurers are also not required to report the reasons for prior authorization denials to CMS. This leaves unanswered questions, including what is the most common reason for denials and if rates of denials vary across demographics.

Medicare Advantage plans do not report complete data on denied claims for services already provided. Without this data, researchers cannot determine how often payers deny claims for Medicare-covered services and reasons why these claims are denied.

CMS does not publish the names of employers or unions that receive Medicare funds to provide Medicare Advantage plans to retired employees. Without more data, researchers can’t tell which industries use Medicare Advantage most often and how rebates vary across employers.

This brief examines past-due medical debt among nonelderly adults and their families using nationally representative survey data collected in June 2022. The analysis assesses the share of adults ages 18 to 64 with past-due medical bills owed to hospitals and other health care providers as well as the actions taken by hospitals to collect payment or make bills easier to settle.

It focuses on the experiences of adults with family incomes below and above 250 percent of the federal poverty level (FPL), approximating the income cutoff used by many hospitals to determine eligibility for free and discounted care.

WHY THIS MATTERS

In their efforts to protect patients from medical debt, policymakers have increasingly focused on the role of hospital billing and collection practices, with particular scrutiny directed toward nonprofit hospitals’ provision of charity care. Understanding the experiences of people with past-due bills owed to hospitals and other providers can shed light on the potential for new consumer protections to alleviate debt burdens.

WHAT WE FOUND

More than one in seven nonelderly adults (15.4 percent) live in families with past-due medical debt. Nearly two-thirds of these adults have incomes below 250 percent of FPL.

Nearly three in four adults with past-due medical debt (72.9 percent) reported owing at least some of that debt to hospitals, including 27.9 percent owing hospitals only and 45.1 percent owing both hospitals and other providers. Adults with past-due hospital bills generally have much higher total amounts of debt than those with past-due bills only owed to non-hospital providers.

Most adults (60.9 percent) with past-due hospital bills reported that a collection agency contacted them about the debt, but much smaller shares reported that the hospital filed a lawsuit against them (5.2 percent), garnished their wages (3.9 percent), or seized funds from a bank account (1.9 percent).

Though about one-third (35.7 percent) of adults with past-due hospital bills reported working out a payment plan, only about one-fifth (21.7 percent) received discounted care.

Adults with incomes below 250 percent of FPL were as likely as those with higher incomes to experience hospital debt collection actions and to have received discounted care.

The concentration of past-due medical debt among families with low incomes and the large share who owe a portion of that debt to hospitals suggests that expanded access to hospital charity care and stronger consumer protections could complement health insurance coverage expansions and other efforts to mitigate the impact of unaffordable medical bills.

HOW WE DID IT

This analysis draws on data from the June 2022 round of the Urban Institute’s Health Reform Monitoring Survey (HRMS), a nationally representative, internet-based survey of adults ages 18 to 64 that provides timely information on health insurance coverage, health care access and affordability, and other health topics. Approximately 9,500 adults participated in the June 2022 HRMS.

Cindy Powers was driven into bankruptcy by 19 life-saving abdominal operations. Medical debt started stacking up for Lindsey Vance after she crashed her skateboard and had to get nine stitches in her chin. And for Misty Castaneda, open heart surgery for a disease she’d had since birth saddled her with $200,000 in bills.

These are three of an estimated 100 million Americans who have amassed nearly $200 billion in collective medical debt — almost the size of Greece’s economy — according to the Kaiser Family Foundation.

Now lawmakers in at least a dozen states and the U.S. Congress have pushed legislation to curtail the financial burden that’s pushed many into untenable situations: forgoing needed care for fear of added debt, taking a second mortgage to pay for cancer treatment or slashing grocery budgets to keep up with payments.

Some of the bills would create medical debt relief programs or protect personal property from collections, while others would lower interest rates, keep medical debt from tanking credit scores or require greater transparency in the costs of care.

In Colorado, House lawmakers approved a measure Wednesday that would lower the maximum interest rate for medical debt to 3%, require greater transparency in costs of treatment and prohibit debt collection during an appeals process.

If it became law, Colorado would join Arizona in having one of the lowest medical debt interest rates in the country. North Carolina lawmakers have also started mulling a 5% interest ceiling.

But there are opponents. Colorado Republican state Sen. Janice Rich said she worried that the proposal could “constrain hospitals’ debt collecting ability and hurt their cash flow.”

For patients, medical debt has become a leading cause of personal bankruptcy, with an estimated $88 billion of that debt in collections nationwide, according to the Consumer Financial Protection Bureau. Roughly 530,000 people reported falling into bankruptcy annually due partly to medical bills and time away from work, according to a 2019 study from the American Journal of Public Health.

Powers’ family ended up owing $250,000 for the 19 life-saving abdominal surgeries. They declared bankruptcy in 2009, then the bank foreclosed on their home.

“Only recently have we begun to pick up the pieces,” said James Powers, Cindy’s husband, during his February testimony in favor of Colorado’s bill.

In Pennsylvania and Arizona, lawmakers are considering medical debt relief programs that would use state funds to help eradicate debt for residents. A New Jersey proposal would use federal funds from the American Rescue Plan Act to achieve the same end.

Bills in Florida and Massachusetts would protect some personal property — such as a car that is needed for work — from medical debt collections and force providers to be more transparent about costs. Florida’s legislation received unanimous approval in House and Senate committees on its way to votes in both chambers.

In Colorado, New York, New Jersey, Illinois, Massachusetts and the U.S. Congress lawmakers are contemplating bills that would bar medical debt from being included on consumer reports, thereby protecting debtors’ credit scores.

Castaneda, who was born with a congenital heart defect, found herself $200,000 in debt when she was 23 and had to have surgery. The debt tanked her credit score and, she said, forced her to rely on her emotionally abusive husband’s credit.

For over a decade Castaneda wanted out of the relationship, but everything they owned was in her husband’s name, making it nearly impossible to break away. She finally divorced her husband in 2017.

“I’m trying to play catch-up for the last 20 years,” said Castaneda, 45, a hairstylist from Grand Junction on Colorado’s Western Slope.

Medical debt isn’t a strong indicator of people’s credit-worthiness, said Isabel Cruz, policy director at the Colorado Consumer Health Initiative.

While buying a car beyond your means or overspending on vacation can partly be chalked up to poor decision making, medical debt often comes from short, acute-care treatments that are unexpected — leaving patients with hefty bills that exceed their budgets.

For both Colorado bills — to limit interest rates and remove medical debt from consumer reports — a spokesperson for Democratic Gov. Jared Polis said the governor will “review these policies with a lens towards saving people money on health care.”

While neither bill garnered stiff political opposition, a spokesperson for the Colorado Hospital Association said the organization is working with sponsors to amend the interest rate bill “to align the legislation with the multitude of existing protections.”

The association did not provide further details.

To Vance, protecting her credit score early could have had a major impact. Vance’s medical debt began at age 19 from the skateboard crash, and then was compounded when she broke her arm soon after. Now 39, she has never been able to qualify for a credit card or car loan. Her in-laws cosigned for her Colorado apartment.

“My credit identity was medical debt,” she said, “and that set the tone for my life.”

The film “American Hospitals: Healing a Broken System” premiered in Washington, D.C., on March 29. This documentary exposes the inconvenient truths embedded within the U.S. healthcare system. Here is a dirty dozen of them:

Hospitals are largely unaccountable for poor clinical outcomes.

The cost of commercially insured care is multiples higher than the cost of government-insured care for identical procedures.

Customer service at hospitals is dreadful.

Frontline clinicians are overburdened and leaving the profession in droves.

Healthcare still operates the same way it has for the last one hundred years — delivering hierarchical, fragmented, hospital-centric, disease-centric, physician-centric “sick” care. Accordingly, healthcare business models optimize revenue generation and profitability rather than health outcomes. These factors explain, in part, why U.S. life expectancy has declined four of the five years and maternal deaths are higher today than a generation ago.

It’s hard to imagine that the devil itself could create a more inhumane, ineffective, costly and change-resistant system. Hospitals consume more and more societal resources to maintain an inadequate status quo. They’re a major part of America’s healthcare problem, certainly not its solution. Even so, hospitals have largely avoided scrutiny and the public’s wrath. Until now.

“American Hospitals” is now playing in theaters throughout the nation. It chronicles the pervasive and chronic dysfunction plaguing America’s hospitals. It portrays the devastating emotional, financial and physical toll that hospitals impose on both consumers and caregivers.

Despite its critical lens, “American Hospitals” is not a diatribe against hospitals. Its contributors include some of healthcare’s most prominent and respected industry leaders, including Donald Berwick, Elizabeth Rosenthal, Shannon Brownlee and Stephen Klasko. The film explores payment and regulatory reforms that would deliver higher-value care. It profiles Maryland’s all-payer system as an example of how constructive reforms can constrain healthcare spending and direct resources into more effective, community-based care.

The United States already spends more than enough on healthcare. It doesn’t need to spend more. It needs to spend more wisely. The system must downsize its acute and specialty care footprint and invest more in primary care, behavioral health, chronic disease management and health promotion. It’s really that simple.

My only critique of “American Hospitals” is many of its contributors expect too much from hospitals. They want them to simultaneously improve their care delivery and advance the health of their communities. This is wishful thinking. Health and healthcare are fundamentally different businesses. Rather than pivoting to population health, hospitals must focus all their efforts on delivering the right care at the right time, place and price.

If hospitals can deliver appropriate care more affordably, this will free up enormous resources for society to invest in health promotion and aligned social-care services. In this brave new world, right-sized hospitals deliver only necessary care within healthier, happier and more productive communities.

All Americans deserve access to affordable health insurance that covers necessary healthcare services without bankrupting them and/or the country. Let me restate the obvious. This requires less healthcare spending and more investments in health-creating activities. Less healthcare and more health is the type of transformative reform that the country could rally behind.

At issue is whether America’s hospitals will constructively participate in downsizing and reconfiguring the nation’s healthcare system. If they do so, they can reinvent themselves from the inside out and control their destinies.

Historically, hospitals have preferred to use their political and financial leverage to protect their privileged position rather than advance the nation’s well-being. Like Satan in Milton’s “Paradise Lost,” they have preferred to reign in hell rather than serve in heaven.

Pride comes before the fall. Woe to those hospitals that fight the nation’s natural evolution toward value-based care and healthier communities. They will experience a customer-led revolution from outside in and lose market relevance. Only by admitting and addressing their structural flaws can hospitals truly serve the American people.

April 1st marked the start date of a one-year window for state Medicaid offices to reassess their beneficiary rolls, as Medicaid’s continuous enrollment policy sunsets. Since the early days of the pandemic, the federal government has boosted state Medicaid funding by 6.2 percent, in exchange for a requirement that current Medicaid beneficiaries maintain eligibility, regardless of changes to their income or other qualifiers. This policy helped grow national Medicaid enrollment to a record 90M, but a projected 15M may now lose coverage through the redetermination process.

The Gist: After the US uninsured rate recently hit a record low, millions of Americans will now lose insurance coverage, at least temporarily.Of those no longer eligible for Medicaid, an estimated 2.7M will qualify for subsidized exchange plans, while around 400K in non-expansion states will have incomes too high for Medicaid and too low for exchange subsidies. The impact will vary in each state, both in terms of how quickly and how many Medicaid beneficiaries are disenrolled.

But in over half of states,at least one-fifth of those who will lose Medicaid coverage are projected to remain uninsured—a significant step backward in the effort to ensure universal coverage.

Communication from Medicaid offices and exchange plan navigators will be key to preventing as many people as possible from becoming uninsured.

Thursday marks the 13th anniversary of the signing of the Affordable Care Act– perhaps the most consequential healthcare legislation since LBJ’s passage of the Medicare Act in 1965. Except in healthcare circles, it will probably go unnoticed.

World events in the Ukraine and China President Xi Jinping’s visit to Russia will grab more media attention. At home, the ripple effects of Silicon Valley Bank’s bankruptcy and the stability of the banking system will get coverage and former President Trump’s arrest tomorrow will produce juicy soundbites from partisans and commentators. Thus, the birthday of Affordable Care Act, will get scant attention.

That’s regrettable: it offers an important context for navigating the future of the U.S. health system. Having served as an independent facilitator between the White House and private sector interests in 2009-2010, I recall vividly the events leading to its passage and the Supreme Court challenge that affirmed it:

The costs and affordability of healthcare and growing concern about the swelling ranks of uninsured were the issues driving its origin. Both political parties and every major trade group agreed on the issues; solving them not so easy.

Effective messaging from special interests about the ACA increased awareness of the law and calcified attitudes for or against. Misinformation/disinformation about the “Patient Protection and Affordable Care Act” morphed to a national referendum on insurance coverage and the cost-effectiveness of the ACA’s solution (Medicaid expansion, subsidies and insurance marketplaces). ‘Death panels. government run healthcare and Obamacare’ labels became targets for critics: spending by special interests opposed to the law dwarfed support by 7 to 1. Differences intensified: Emotions ran high. I experienced it firsthand. While maintaining independence and concerns about the law, I received death threats nonetheless. Like religion, the ACA was off-limits to meaningful discussion (especially among the majority who hadn’t read it).

And after Scott Brown’s election to the vacant Massachusetts seat held by Ted Kennedy in January, 2010, the administration shifted its support to a more-moderate Senate Finance Committee version of the law that did not include a public option or malpractice reforms in the House version. Late-night lobbying by White House operatives resulted in a House vote in favor of the Senate version with promises ‘it’s only the start’. Through amendments, executive orders, administrative actions and appropriations, it would evolve with the support of the Obama team. It passed along party lines with the CBO offering an optimistic view it would slow health cost escalation by reducing administrative waste, implementation of comparative effectiveness research to align evidence with care, increased insurance coverage, changing incentives for hospitals and physicians and more.

The Affordable Care Act dominated media coverage from August 2009 to March 2010. In the 2010 mid-term election, it was the issue that catapulted Republicans to net gains of 7 in the Senate, 63 in the House and 6 in Governor’s offices. And since, Republicans in Congress have introduced “Repeal and Replace” legislation more than 60 times, failing each time.

Today, public opinion about the ACA has shifted modestly: from 46% FOR and 40% against in 2010 to 55% FOR and 42% against now (KFF). The national uninsured rate has dropped from 15.5% to 8.6% and Medicaid has been expanded in 39 states and DC. Lower costs, increased affordability and quality improvements owing to the ACA have had limited success.

Key elements of the ACA have not lived up to expectations i.e. the Patient Centered Outcome Research Institute, the National Quality Strategy, Title V National Healthcare Workforce Task Force, CMMI’s alternative payment models and achievement of Level 3 interoperability goals vis a vis ONCHIT, CHIME et al. So, as the 2024 political season starts, the ACA will get modest attention by aspirants for federal office because it addressed big problems with blunt instruments. Most recognize it needs to be modernized based on trends and issues relevant to healthcare in 2030 and beyond.

Trends like…

Self-diagnostics and treatment by consumers (enabled by ChatGPT et al).

Data-driven clinical decision-making.

Integration of non-allopathic methodologies.

The science of wellbeing.

Complete price, cost and error transparency.

Employer and individual insurance coverage optimization.

And others.

Issues like….

The role and social responsibility of private equity in ownership and operation of services in healthcare delivery and financing.

The regulatory framework for local hospitals vs. Regional/nation health systems, and between investor-owned and not-for-profit sponsorship.

The role and resources for guided self-care management and virtual-care.

Innovations in care delivery services to vulnerable populations using technologies and enhanced workforce models.

Modernization of regulatory environments and rules of competition for fully integrated health systems, prescription drug manufacturers, health insurers, over-the counter therapies, food as medicine, physician ownership of hospitals, data ownership, tech infomediaries that facilitate clinical decision-making, self-care, professional liability and licensing and many others.

Integration of public health and local health systems.

The allocation of capital to the highest and best uses in the health system.

The sustainability of Medicare and role of Medicare Advantage.

The regulatory framework for disruptors”.

And many others.

These trends are not-easily monitored nor are the issues clear and actionable. Most are inadequately addressed or completely missed in the ACA.

Complicating matters, the political environment today is more complicated than in 2010 when the ACA became law. The economic environment is more challenging: the pandemic, inflation and economic downturn have taken their toll. Intramural tensions in key sectors have spiked as each fights for control and autonomy i.e. primary care vs. specialty medicine, investor-owned vs. not-for-profit hospitals, retail medicine & virtual vs. office-based services, carve-outs, direct contracting et al . Consolidation has widened capabilities and resources distancing big organizations from others. Today’s media attention to healthcare is more sophisticated. Employers are more frustrated. And the public’s confidence in the health system is at an all-time low.

“ACA 2.0” is necessary to the system’s future but unlikely unless spearheaded by community and business leaders left out of the 1.0 design process. The trends and issues are new and complicated, requiring urgent forward thinking.

US District Judge Reed O’Connor ruled on Thursday that the Affordable Care Act’s (ACA’s) requirement for most insurers to cover certain preventative care services without cost-sharing is unlawful. Judge O’Connor—who invalidated the entire ACA in 2018, before the Supreme Court reversed that ruling—had already sided with the plaintiffs in Braidwood vs. Becerra last September, on the grounds that mandatory coverage of HIV prevention treatment, also known as PrEP therapy, violated their religious beliefs. His latest ruling applies to the ACA-mandated preventive services that are compelled by the US Preventative Services Task Force (USPSTF), on the grounds of the task force’s makeup and the fact that some of its recommendations predate the ACA. Services covered for no cost today include screening tests for a variety of cancers, sexually transmitted infections, and diabetes. The ruling does not impact other ACA preventative care services, like contraceptive services and children’s immunizations, as they are based on the recommendations of other government advisory groups. The immediate impact of this week’s ruling is unclear, as the Biden administration has already filed an appeal and may seek to stay the ruling, while most insurance contracts are set on an annual basis.

The Gist: Given the reasoning laid out in Judge O’Connor’s Braidwood v. Becerra ruling last fall, this decision was expected. As with previous attempts to repeal the ACA that have come through his district, the ultimate fate of the ACA’s cost-free preventative care services will likely be decided by the US Supreme Court. It’s possible that the Court may find the narrow targeting of this case more reasonable, making no-cost preventive care coverage optional for employers.

If that happens, millions of Americans could again have to pay for some of the most common and highest-value healthcare services. That additional financial burden, along with tightening of health plan benefit designs, could create barriers to access and exacerbate health disparities.

Researchers estimate 15 million people will lose their Medicaid starting April 1 when states begin removing people from the low-income health insurance program for the first time in three years.

In March 2020, Congress banned states from removing people from Medicaid during the pandemic in exchange for more federal funding for state Medicaid programs. Medicaid enrollment is usually tied to people’s incomes, and individuals normally have to regularly prove they still qualify in what’s known as a redetermination. (In the 39 states and Washington, D.C., that have expanded Medicaid, a family of four has to make less than $40,000 to qualify. In non-expansion states, the cutoff is even lower.)

With redeterminations paused, Medicaid enrollment nationwide has grown from 71 million in February 2020 to an estimated 95 million in March 2023.Research shows Medicaid coverage is associated with better access to care, more financial security, better health and lower mortality. During the pandemic, beneficiaries have been able to enjoy these benefits without worrying about confirming their eligibility.

In December, Congress voted to let states restart the process of clearing their rolls on April 1, what’s sometimes referred to as “unwinding.”Lawmakers are giving states 14 months to redetermine millions of people’s eligibility — an unprecedented task made even more difficult by serious staffing and experience shortages in many Medicaid offices.

“It’s going to be a big lift,” said Sayeh Nikpay, a health policy researcher at the University of Minnesota and Tradeoffs Senior Research Advisor. “States have never had to do this many redeterminations this quickly before, and there’s a lot of uncertainty about what will happen.”

We asked Nikpay to pick out a few relevant studies to help us understand what is happening and how states and employers could keep more people insured. Here are three she identified as particularly helpful.

Two types of people will lose coverage

The Office of the Assistant Secretary for Planning and Evaluation, which provides research for the U.S. Department of Health and Human Services, released a report in August 2022 that estimated 15 million people will lose Medicaid coverage as a result of the unwinding. (The estimate is similar to another analysis by the independent Urban Institute.)

ASPE breaks those 15 million people into two groups. In the first group are people who make too much money to qualify for Medicaid. ASPE estimates there are about 8 million people in that category, and they should be able to get insurance through work or the Obamacare exchanges.

In the second group are roughly 7 million people ASPE estimates are still eligible but will lose coverage because of what’s called “administrative churn.”This can happen if the Medicaid office can’t get in touch with someone to confirm their eligibility because they’ve moved or changed their phone number or if they’re unable to make an in-person appointment because of work or child care responsibilities. (The Urban Institute projects about 4 million people will be in this group.)

These two groups represent a key tension to the unwinding process: States want to shed people who make too much money, but officials also know eligible people often lose coverage during redeterminations, and that danger is heightened given the scale and speed of this process.

Making the switch from Medicaid to private insurance

This next paper looks at the first group: the roughly 8 million people expected to move from Medicaid to private coverage, and specifically the roughly 4 million who are expected to get coverage through the Obamacare exchanges. Adrianna McIntyre, an assistant professor of health policy at Harvard, wrote in JAMA Health Forum in October 2022 about the most effective ways to move people from Medicaid onto private Obamacare plans.

There’s limited data on this, but based on the few studies available, McIntyre found that only 3 to 5 percent of people who leave Medicaid end up getting an Obamacare plan. Many policymakers are relying on the Obamacare exchanges to provide a life preserver to millions of people losing Medicaid coverage, but the research cited by McIntyre shows getting people into these plans is not guaranteed and will take focused effort by states.

McIntyre’s review cites several randomized controlled trials where states tested different ways of increasing enrollment in Obamacare plans. These studies found simple reminders from the state – like physical letters, emails and phone calls help – boost sign-ups anywhere from 7 to 16 percent.

But what really seems to make a difference is reminders plus connecting people to someone who can get them signed up while they are on the phone. In one of those trials published in 2022, people in California who got a reminder email and a call connecting them to enrollment assistance were almost 50% more likely to sign up for a plan. Such extra effort is obviously costly, and it may not be a priority or financially feasible for some states.

McIntyre’s review did not include any research on what employers can do to help their workers transition from Medicaid to work-based coverage, but based on the studies McIntyre cited, Nikpay said she thinks it’s a good idea for employers to make sure people know Medicaid could be going away and provide as much help as possible in getting new coverage.

Making it easier to stay on Medicaid can have other benefits

The final study looks at the second group of people expected to lose Medicaid coverage: the 7 million people who may lose coverage due to administrative churn even though they are still eligible.

Some states have tried to limit that churn, and researchers at the RAND Corporation evaluated New York’s effort. Starting in 2014, New York allowed people to stay on Medicaid without any redeterminations for 12 months once enrolled.

In addition to keeping more people on Medicaid for longer, researchers found that after this policy was in place, hospital admissions and monthly costs per beneficiary went down. The researchers can’t say whether the continuous enrollment policy directly caused these improved outcomes, but the findings suggest that avoiding administrative churn can help people stay covered without ballooning costs.

“It seems reasonable to me,” Nikpay said of the findings, “that making it easier to stay on Medicaid, even outside of a global pandemic, could benefit people’s health given what we know about how Medicaid affects people.”

A recent Urban Institute report highlights the issue of medical debt but fails to examine two of the chief driving forces of this debt: inadequate enrollment in comprehensive health care coverage and high-deductible health plans that intentionally push more costs onto patients. It also fails to appreciate the looming crisis when the public health emergency ends and Medicaid enrollment could plummet.

As the extent of medical debt shows, both the government and the private market is failing too many patients, leaving too many either uninsured or with subpar plans that expose too many people to bills they cannot afford to pay. While hospital financial assistance is crucial to helping many individuals of limited means access care, it is no substitute for a solution that gets to the root causes of medical debt.

Affordable, comprehensive health care coverage is the most important protection against medical debt. While the U.S. health care system has achieved record rates of coverage, significant gaps remain and new threats are on the horizon. One of the gaps is the failure by some states to expand Medicaid, while the most imminent threat is the potential loss of Medicaid coverage for millions of people as the public health emergency ends. We must ensure that every individual has access to some form of comprehensive coverage.

In doing so, we must put an end to deceptively inadequate health plans. These include short-term limited duration health plans and health sharing ministries that often appeal to consumers because they are cheaper and often marketed to appear comprehensive. The reason they are cheaper is because when you read the fine print you discover they cover fewer benefits and include few-to-no consumer protections, like required coverage of pre-existing conditions and limits on out-of-pocket costs. Subscribers for these types of plans often find themselves responsible for their entire medical bill without any help from their health plan and can accumulate significant medical debt.

Many of the same concerns apply to high-deductible health plans. These plans are specifically designed to increase patients’ financial exposure through high cost-sharing – the amount the subscriber must pay out-of-pocket. Yet, many individuals enrolled in these plans find they can’t manage the gap between what their insurance pays and what they themselves owe as a result. It’s not a mystery why high-deductible health plans contribute to medical debt.

Hospitals and other providers do not determine how much insured patients owe for their care. Instead, that amount is set by the health plan. While every hospital has a financial assistance policy to help those most in need, they can only help so much and so many. And no matter how generous, hospital financial assistance will never be a substitute for a health plan that covers preventive and necessary care at an affordable price on the front and back end of coverage.

We must tackle the problem of medical debt, and we must do so at the root: ensuring all individuals are enrolled in comprehensive health care coverage and ending deceptive marketing of health plans and unaffordable cost-sharing.

Potential solutions include:

Restricting the sale of high-deductible health plans to only those individuals with the demonstrated means to afford the associated cost-sharing.

Prohibiting the sale of health sharing ministry products and short-term limited duration plans that go longer than 90 days.

Lowering the maximum out-of-pocket cost-sharing limits.

Eliminating the use of deductibles and co-insurance and rely solely on flat co-payments, which are easier for patients to anticipate.

Removing providers from the collection of cost-sharing altogether and require that health plans collect directly from their enrollees the cost-sharing payments they impose. This approach would eliminate the vast majority of patient bills from providers altogether.

Moreover, the AHA has been actively engaged in identifying and promoting best practices in patient billing for decades. The AHA updated our voluntary patient billing guidance in 2020. The guidelines include assisting patients who cannot pay for the care they receive and protecting patients from certain debt collection practices, such as garnishment of wages, liens, interest on debt, adverse credit reporting and lawsuits. Most hospitals provide free care for patients with the most limited means as defined by income below 200% of the federal poverty limit. In the event of an unpaid bill, the Internal Revenue Service has prescribed an extensive series of steps and wait times that most hospitals must adhere to before taking any collection actions, which is a last resort.

Hospitals’ doors are always open to anyone who needs care, regardless of ability to pay. In total, hospitals and health systems of all types provided in 2020 more than $42 billion in uncompensated care, or care for which they received no payment.

Hospitals and health systems will continue to work to advance solutions that make care more affordable and accessible for all patients. But health plans must do their part by providing adequate coverage that does not subject patients to unaffordable bills and medical debt.