Last week Johnson & Johnson followed Merck, Bristol Myers Squibb, and Astellas Pharma by filing a lawsuit against the Biden administration in federal court over the Medicare Drug Price Negotiation Program, established through the 2022 Inflation Reduction Act. PhRMA, the industry trade group, and the US Chamber of Commerce have also filed suits.

The lawsuits claim that the program violates the First and Fifth Amendments by compelling speech, and taking private property for public use without just compensation. The US Chamber of Commerce also filed a motion earlier this month requesting a preliminary injunction.

This flurry of legal activity comes just a month before the Centers for Medicare & Medicaid Services is due to publish its list of the first ten drugs selected for negotiations. The makers of those drugs will then have a month to decide if they will participate in negotiations, risking significant financial penalties if they do not. Any negotiated prices would take effect in 2026.

The Gist:Theability for Medicare to negotiate drug prices is a key pillar of the Biden administration’s healthcare agenda, one the President plans to tout in his upcoming reelection campaign. But the pharmaceutical industry’s legal challenges—multiple, separate suits in different federal courts nationwide—are destined for the Supreme Court if these cases generate conflicting rulings, which is likely. A protracted legal fight will delay or potentially alter the program before it is fully implemented.

On Tuesday, the White House issued a proposal to enhance the 2008 Mental Health Parity and Addiction Equity Act, which requires insurers to cover mental healthcare at the same level as physical care.

Health plans would be required to evaluate mental health coverage policies, including network size, prior authorization rules, and out-of-network payment policies.

The proposal also includes closing a loophole in the original law that excludes non-federal government health plans from these parity standards.

The Gist: Fewer than half of the one in five US adults experiencing mental illness in 2020 received care for their illness, and fewer than one in 10 received treatment for a substance abuse disorder.

But while insurance companies’ failure to establish adequate mental health networks is part of the problem, there are other, larger access issues at play, including the nationwide shortage of mental health clinicians, many of whom don’t accept insurance.

Forget “repeal and replace,” an oft-repeated Republican rallying cry against the Affordable Care Act.

House Republicans have advanced a package of bills that could reduce health insurance costs for certain businesses and consumers, partly by rolling back some consumer protections. Rather than outright repeal, however, the subtler effort could allow more employers to bypass the landmark health insurance overhaul’s basic benefits requirements and most state standards.

At the same time, the Biden administration seeks to undo some of the previous administration’s health insurance rules, proposing to retighten regulations for short-term plans.

Health policy experts aren’t surprised. Most of the GOP policy ideas have long drawn Republican support, have raised concern from Democrats about reduced consumer protections, and could fall under the theme: Everything old is new again.

Association Health Plans. Self-insurance. Giving workers money to buy their own individual coverage instead of offering a group plan. These are the buzzwords and, ultimately, revolve around one issue, said Joseph Antos, a senior fellow at the American Enterprise Institute, a Washington, D.C.-based think tank.

“The real problem is the rising cost of health care. Always has been,” he said. And that problem, he added, is larger than the proposed solutions.

“It’s not clear that this kind of an approach would substantially help very many people,” Antos said.

The latest round of rules and legislation comes as the ACA — passed in 2010 — is now cemented in the system. More than 16 million people enrolled in their own plans this year, and millions more are getting coverage through expanded Medicaid in all but 10 states, leading to an all-time-low uninsured rate.

But even with enhanced subsidies for ACA health plans, initially approved in the American Rescue Plan and extended through 2025 by the Inflation Reduction Act, some people still struggle to afford deductibles or other costs, and employers — especially small ones — have long wrestled with rising insurance costs and the ability to offer coverage at all.

So, what is on the table in Washington? First, a caveat: Little is likely to happen in an election year.

While the Biden administration’s proposed regulations on short-term plans are likely to go into effect, either this year or early next, the GOP’s House-passed legislation — dubbed the CHOICE Arrangement Act, for Custom Health Option and Individual Care Expense — is unlikely to win favor in the Democratic-controlled Senate. If Republicans were to retake the Senate and White House, though, it illustrates the health policy direction they could take.

Here are the broad issues on the radar:

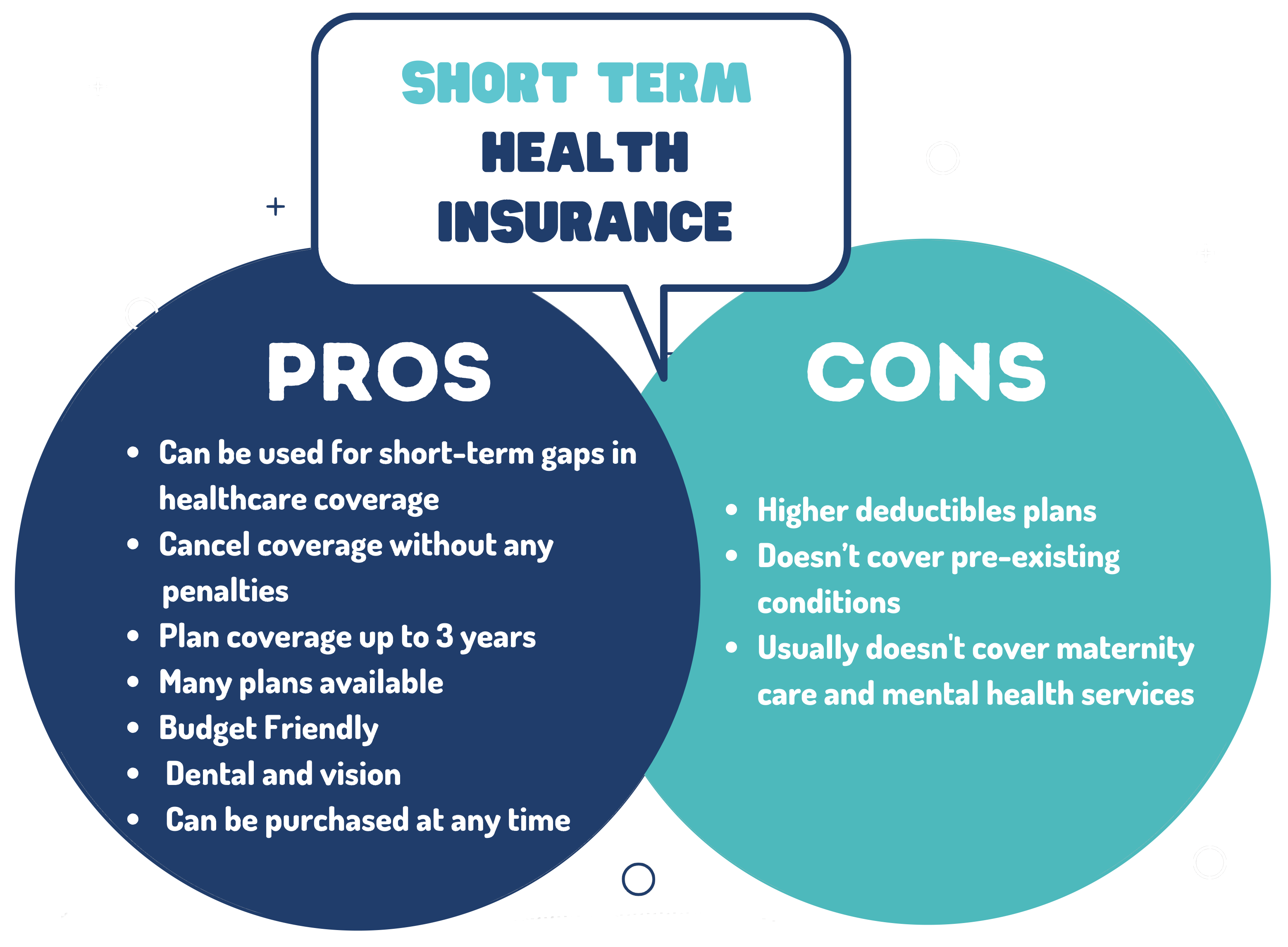

From the President’s Desk: Limits on Short-Term Policies

These types of plans have been sold for decades, often as a stopgap measure for people between jobs.

They can be far less expensive than more traditional coverage because short-term plans vary widely and “run the gamut from comprehensive policies to fairly minimal policies,” said Louise Norris, an insurance broker who regularly writes about health policy.

The plans don’t have to cover all the benefits required of ACA plans, for example, and can bar coverage for preexisting medical conditions, can set annual or lifetime limits, and often don’t include maternity care or prescription drugs. Despite notices warning of such policies’ limitations, consumers may not realize what isn’t covered until they try to use the plan.

Concerned that people would choose this option instead of more comprehensive and more expensive insurance offered through the ACA, President Barack Obama’s administration set rules limiting the policy terms to three months.

President Donald Trump’s administration loosened those rules, allowing plans to again be sold as 364-day policies, and adding the ability for insurers to renew them for up to three years. Now President Joe Biden, whose representatives have called such plans “junk insurance,” proposes reining those in again, restricting policies to four months, at most.

The Biden proposal cites estimates from the Congressional Budget Office and the Joint Committee on Taxation that about 1.5 million people are enrolled in such plans.

Michael Cannon, director of health policy studies at the Cato Institute, a Washington, D.C.-based libertarian think tank, decried the proposed rule in an opinion piece published by The Hill. He wrote that the Biden proposal removes an important lower-cost alternative and could leave some consumers facing “sky-high medical bills for up to one year” if their policies expire between open enrollment periods for ACA plans.

The real fight comes down to defining “short-term,” said John McDonough, a professor of public health practice at the Harvard T.H. Chan School of Public Health in Boston, who worked on the original ACA legislation.

Progressives and Democrats support the view that “short-term” should end after four months and “then people go into an ACA plan or Medicaid,” he said. “Republicans and conservatives would like this to be an alternative permanent coverage model for folks, some of whom legitimately know what they are getting and are willing to roll the dice.”

Association Health Plans, Self-Insurance, and Other Workplace Issues

Meanwhile, the House-passed CHOICE Arrangement Act, among other things, would allow more self-employed people and businesses to band together to buy Association Health Plans, which are essentially large group plans purchased by multiple employers.

These can be less expensive because they don’t have to meet all ACA requirements, such as covering a specified set of benefits that includes hospitalization, prescription drugs, and mental health care. Historically, some also have had solvency issues and state regulators have investigated claims of false advertising by certain association plans.

Another piece of the legislation would help more small employers self-insure, which also allows them to bypass many ACA requirements and most state insurance rules.

Both proposals represent a “chipping away at the foundation edges of the ACA structure,” said McDonough.

The package also codifies Trump-era regulations allowing employers to provide workers with tax-free contributions to shop for their own insurance, so long as it is an ACA-qualified plan, a benefit known as an individual coverage Health Reimbursement Account.

The CHOICE Arrangement Act “will go a long way toward reducing insurance costs for employers, ensuring that workers continue to have access to high-quality, affordable health care,” said Rep. Tom Cole (R-Okla.) in prepared remarks as the bill went before the House Committee on Rules in June.

Giving workers a set amount of money to buy their own coverage allows employees to choose what works best for them, supporters say. Critics warn that many workers may be unprepared to shop and that the effort by some employers might prove discriminatory.

”Firms may find strategies to shift sicker workers to HRAs, even with guardrails in the legislation meant to prevent this,” according to a blog post from the Center on Budget and Policy Priorities.

Not so, said Robin Paoli, executive director of the HRA Council, a nonprofit advocacy organization whose members include insurers, employers, and other organizations that support such individual accounts.

Employers have some discretion in choosing which groups of employees are offered such accounts, often based on geography, but cannot create a group made up solely of “people over 65, or a class of sick people,” said Paoli. “The rules absolutely prohibit discrimination based on age or health condition.”

The other two ideas — associations and the self-insured proposal — have drawn opposition from the National Association of Insurance Commissioners, which wrote to House leaders that the package “threatens the authority of states to protect consumers and markets” because it affects the ability of states to regulate such plans.

Current law allows businesses in the same industry to band together to buy coverage, essentially creating a larger pool that then can, theoretically, wield more negotiating clout and get better rates.

The House legislation would make changes to allow more self-employed people and businesses that aren’t in the same industry to do the same.

Some policy experts said expanding access to association plans and self-insurance to smaller businesses might adversely affect some workers by drawing healthier people out of the overall market for small-group insurance and potentially raising premiums for those who remain.

“The big picture of what these bills do is allow [employers and] insurance companies to get out from under the ACA standards and protections and offer cheaper insurance to younger and healthier employee groups,” said Sabrina Corlette, a researcher and the co-director of the Center on Health Insurance Reforms at Georgetown University.

But attorney Christopher Condeluci, who worked with GOP lawmakers in drafting the legislation, takes a different view. The entire GOP package, he said, represents “improvements to the status quo” that are needed because small businesses and individuals are confronting “health costs continuing to rise” and “out-of-pocket costs continuing to increase.”

A detailed report, published by a group of organizations including the American Antitrust Institute, provides one of the highest-quality examinations of the growth of private equity (PE)-backed physician practices, and the impact of this growth on market competition and healthcare prices.

From 2012 to 2021, the annual number of practice acquisitions by private equity groups increased six-fold, and the number of metropolitan areas in which a single PE-backed practice held over 30 percent market share rose to cover over one quarter of the country. (Check out figure 3B at the bottom of page 20 in the report to see if you live in one of those markets.)

The study also found an association between PE practice acquisitions and higher healthcare prices and per-patient expenditures. In highly concentrated markets, certain specialties, like gastroenterology, saw prices rise by as much as 18 percent.

The Gist: As the report highlights, one of the greatest barriers to assessing PE’s impact on physician practices is the lack of transparency around acquisitions and ownership structures. This analysis brings us closer to understanding the scope of the issue, and makes a strong case for regulatory and legislative intervention.

Recent proposed changes to federal premerger disclosure requirements offer a good start, but many practice acquisitions are still too small to flag review, and slowing future acquisitions will do little to unwind the market concentration already emerging.

PE is also not the sole actor contributing to healthcare consolidation, and proposed remedies may target the activities of payers and health systems considered anti-competitive as well.

Last Friday, the Department of Health and Human Services, the Treasury Department, and the Department of Labor jointly issued several proposed rules to shore up consumer healthcare protections, including reversal of a Trump administration policy that allowed consumers to enroll in short-term health plans, which were intended to serve as limited coverage options during transitional periods, for up to three years. Approximately 3M people were enrolled in these plans in 2019.

A new rule would limit consumer access to these plans to just three months, with an optional one-month extension, while also requiring payers to disclose clearly how their plans fall short of comprehensive health insurance.

The Gist: In an expected move, theBiden administration continues its unwinding of the Trump-era policies it sees as undermining the Affordable Care Act’s (ACA’s) mission of guaranteeing robust, accessible insurance for all.

Short-term plans, which were granted an exemption from the ACA requirement that health plans cover ten essential health benefits, have been found to discriminate against people with pre-existing conditions, revoke coverage for enrollees retroactively, and generate excess surprise bills due to their limited networks.

Five recent Supreme Court rulings have reset the context for U.S. jurisprudence for years to come and open a can of worms for healthcare operators.

Last year’s SCOTUS decision ruling in Dobbs v. Jackson Women’s Health (June 24, 2022) set the tone: in its 6-3 decision, the high court determined that that access to abortion is a state issue, not federal thus nullifying the 50-year-old legal precedent in Roe v. Wade and reversing 2 lower court rulings.

On June 1, 2023, in the United States v. Supervalu, petitioners sued SuperValu and Safeway under the False Claims Act (FCA) alleging they defrauded the Medicare and Medicaid by knowingly filing false claims. Essentially, the plaintiffs sought financial remedy because the retailers’ prices were not explicitly and specifically “usual and customary” prices. In its unanimous ruling, SCOTUS agreed that “the phrase ‘usual and customary’ is open to interpretation, but reasoned that “such facial ambiguity alone is not sufficient to preclude a finding that respondents knew their claims were false.”

On June 29, 2023, in Students for Fair Admissions, Inc. v. President and Fellows of Harvard College, the court ruled 6-3 that affirmative action policies at Harvard and the University of NC that consider an applicant’s race in college admissions are unconstitutional.

On June 30, 2023, in 303 Creative LLC v. Elenis (June 30, 2023) By a vote of 6-3, SCOTUS ruled that the First Amendment right of free speech prohibits Colorado from forcing a website designer to create expressive designs speaking messages with which the designer disagrees.

On June 30, 2023, in Department of Education v. Brown: By a unanimous vote, SCOTUS ruled that the 2 plaintiffs lacked standing to “Article III standing to assert a procedural challenge to the student-loan debt-forgiveness plan adopted by the Secretary of Education pursuant to Higher Education Relief Opportunities for Students Act of 2003 (HEROES Act).” In effect, the court vacated and remanded the judgment of the United States Court of Appeals for the 5th Circuit because it felt Myra Brown and Alexander Taylor (plaintiffs) did not prove that any injury suffered from not having their loans forgiven. Therefore, the court had no jurisdiction to address their procedural claim.

Each of these is specific to a circumstance but collectively they expose industries like healthcare to greater compliance risk, potential court challenges and operational complexity. Here’s an example:

The 58-year-old Kennedy-era legal precedent of affirmative action to redress racial inequity was the focus in Students for Fair Admissions, Inc. v. President and Fellows of Harvard College. SCOTUS essentially sided with plaintiffs who argued affirmative action violates the 14th Amendment’s Equal Protection guarantee. In healthcare, research shows access to the healthcare system is disproportionately inaccessible to persons of color, especially if they’re poor. They improve when individuals are treated by clinicians of the same race but only about 5% of doctors in America are Black, compared to 12% of the general population and only 6% of doctors in the U.S. are Hispanic while the group accounts for nearly almost 20% of the general population.

Notwithstanding the uncanny similarities between higher education and healthcare (both have raised prices above GDP and overall inflation rates for 2 decades, both jealously protect their reputations against outside transparency and unflattering report cards, both feature competition between public and private institutions and both face questions about the value of their efforts), the issue of diversity is central in both. Affirmative action is a means to that end, but at least for now and in higher education, it’s not constitutional.

Might workforce diversity and clinician training efforts be stymied by the prospect of court challenges? Might “affirmative action” in healthcare be replaced by “holistic review” to enable consideration of an applicant’s life or quality of character as some conservative jurists have suggested?

My take:

Affirmative action per the example above is only one of many constructs widely accepted in healthcare today where court challenges may alter the future. Individual rights and free speech including online medical advice, the role of state governments, fraud and abuse and other domains are equally exposed.

It’s clear this court is not threatened by legal precedent nor cautious about public opinion on touchy issues. Thus, immediate imperatives for healthcare organizations are these:

Revisit legal precedents on which the ways we operate are based: Roles and responsibilities in US healthcare are sacrosanct and protected by legal precedent: Physicians diagnose and treat; others don’t. Insurers pay claims but don’t practice medicine. Not for profit hospitals serve community needs in exchange for tax-exemption. Public health programs that serve the poor are funded by local and state governments. Employer sponsored benefits underwrite the system’s profitability and fund its hospital Part A obligations and so on. Might a conservative court revisit these in the context of the constitution’s “general welfare” purpose and redirect its focus, roles and structure?

Revisit terms and phrases where consensus is presumed but specific definition is lacking: Just as SCOTUS recognized ambiguity in applying terms like “usual and customary” in its Supervalu-Safeway ruling, it is likely to challenge other widely used phrases used in healthcare that often lack specific referents i.e., quality, safety, efficacy, effectiveness, community benefit, charity care, evidence-based care, cost-effectiveness, not-for-profit, competition, value” and many others. Might SCOTUS force the industry to more specifically define its most widely used phrases in order to justify its claims?

For everyone in healthcare, these rulings open a can of worms. Compliance risk assessments, scenario plan updates required!

On Tuesday, the US Preventative Services Task Force (USPSTF), which is appointed by an arm of the Department of Health and Human Services, finalized guidance that all adults ages 19 to 64 should be routinely screened for anxiety, even in the absence of symptoms. Last fall, USPSTF proposed a draft version of this guidance, and also finalized its recommendation that children and adolescents ages 8-18 be screened for anxiety. The task force found that anxiety screening for seniors, as well as suicide-risk screening for all adults, lacked conclusive evidence of effectiveness.

The Gist: Policymakers and providers are right to respond to the nationwide increase in anxiety and depression brought on by the pandemic, and regular screenings will help quantify the scope of a problem we face.

However, given the pervasive undersupply of behavioral health practitioners, widespread screenings will only lead to better care if access to treatment can be scaled.

Solutions that take advantage of telemedicine’s success in behavioral health, combined with the tools—and time—to manage mild anxiety in the primary care setting, are critical to provide support for a coming wave of newly identified patients.

This month, a panel of expert advisers recommended the Food and Drug Administration (FDA) grant full approval to Leqembi, a drug developed by Eisai and Biogen that targets amyloid plaques in the brain that are linked to the development of Alzheimer’s.

The drug was found to slow cognitive decline in patients by 27 percent over 18 months, though not without some serious side effects, including brain swelling and bleeding. While Leqembi received accelerated FDA approval in January 2023, it is now likely to become the first Alzheimer’s drug that slows the progression of the disease to secure full FDA approval. The Centers for Medicare and Medicaid Services (CMS) recently announced that it intends to cover this new class of Alzheimer’s drugs, as long as prescribing physicians participate in patient registries designed to continue collecting data about the drugs and their efficacy. The FDA is expected to make a final decision on Leqembi by early July.

The Gist: In addition to risks of patient harm, much of the controversy around Leqembi surrounds its $27K list price. Payers, especially Medicare, are worried that it will balloon spending while exposing patients to unaffordable cost-sharing.

With the number of Americans diagnosed annually with Alzheimer’s and other dementias projected to double by 2050, Leqembi has the potential both to help millions and to drive unsustainable spending patterns, and it will be difficult to achieve the former without the latter.

But with full approval likely, a coming frenzy of investor activity to launch memory treatment centers for drug infusion services, capitalizing on the expected huge demand for the drug, seems inevitable.

Two important reports released last Wednesday point to a disconnect in how policymakers are managing the U.S. economy and how the health economy fits.

Report One: The Federal Reserve Open Market Meeting

At its meeting last week, the Governors of the Federal Open Market Committee (FOMC) voted unanimously to keep the target range for the federal funds rate at 5% to 5.25%–the first time since last March that the Fed has concluded a policy meeting without raising interest rates.

In its statement by Chairman Powell, the central bank left open the possibility of additional rate hikes this year which means interest rates could hit 5.6% before trending slightly lower in 2024.

In conjunction with the (FOMC) meeting, meeting participants submitted projections of the most likely outcomes for each year from 2023 to 2025 and over the longer run:

Median

2023

2024

2025

Longer Run

Longer Run Range

% Change in GDP

1.1

1.1

1.8

1.8

1.6-2.5

Unemployment rate &

4.1

4.5

4.5

4.0

3.6-4.4

PCE Inflation rate

3.2

2.5

2.1

2.0

2.0

Core PCE Inflation

3.9

2.6

2.2

*

*

*Longer-run projections for core PCE inflation are not collected.

Notes re: the Fed’s projections based on these indicators:

The GDP (a measure of economic growth) is expected to increase 1% more this year than anticipated in its March 2023 analysis while estimates for 2024 were lowered just slightly by 0.1%. Economic growth will continue but at a slower pace.

The unemployment rate is expected to increase to 4.1% by the end of 2023, a smaller rise in joblessness than the previous estimate of 4.5%. (As of May, the unemployment rate was 3.7%). Unemployment is returning to normalcy impacting the labor supply and wages.

inflation: as measured by the Personal Consumption Expenditures index, will be 3.2% at the end of 2023 vs. 3.3% they previously projected. By the end of 2024, it expects inflation will be 2.5% reaching 2.1% at the end of 2025. Its 2.0% target is within reach on or after 2025 barring unforeseen circumstances.

Core inflation projections, which excludes energy and food prices, increased: the Fed now anticipates 3.9% by the end of 2023–0.3% above the March estimate. Price concerns will continue among consumers.

Based on these projections, two conclusions about nation’s monetary policy may be deduced the Fed’s report and discussion:

The Fed is cautiously optimistic about the U.S. economy in for the near term (through 2025) while acknowledging uncertainty exists.

Interest rates will continue to increase but at a slower rate than 2022 making borrowing and operating costs higher and creditworthiness might also be under more pressure.

Report Two: CMS

On the same day as the Fed meeting, the actuaries at the Centers for Medicare and Medicaid Services (CMS) released their projections for overall U.S. national healthcare spending for the next several years:

“CMS projects that over 2022-2031, average annual growth in NHE (5.4%) will outpace average annual growth in gross domestic product (GDP) (4.6%), resulting in an increase in the health spending share of GDP from 18.3% in 2021 to 19.6% in 2031. The insured percentage of the population is projected to have reached a historic high of 92.3% in 2022 (due to high Medicaid enrollment and gains in Marketplace coverage). It is expected to remain at that rate through 2023. Given the expiration of the Medicaid continuous enrollment condition on March 31, 2023 and the resumption of Medicaid redeterminations, Medicaid enrollment is projected to fall over 2023-2025, most notably in 2024, with an expected net loss in enrollment of 8 million beneficiaries. If current law provisions in the Affordable Care Act are allowed to expire at the end of 2025, the insured share of the population is projected to be 91.2%. In 2031, the insured share of the population is projected to be 90.5%, similar to pre-pandemic levels.”

The report includes CMS’ assumptions for 4 major payer categories:

Medicare Part D: Several provisions from the Inflation Reduction Act (IRA) are expected to result in out-of-pocket savings for individuals enrolled in Medicare Part D. These provisions have notable effects on the growth rates for total out-of-pocket spending for prescription drugs, which are projected to decline by 5.9% in 2024, 4.2% in 2025, and 0.2% in 2026.

Medicare: Average annual expenditure growth of 7.5% is projected for Medicare over 2022-2031. In 2022, the combination of fee-for-service beneficiaries utilizing emergent hospital care at lower rates and the reinstatement of payment rate cuts associated with the Medicare Sequester Relief Act of 2022 resulted in slower Medicare spending growth of 4.8% (down from 8.4% in 2021).

Medicaid: On average, over 2022-2031, Medicaid expenditures are projected to grow by 5.0%. With the end of the continuous enrollment condition in 2023, Medicaid enrollment is projected to decline over 2023-2025, with most of the net loss in enrollment (8 million) occurring in 2024 as states resume annual Medicaid redeterminations. Medicaid enrollment is expected to increase and average less than 1% through 2031, with average expenditure growth of 5.6% over 2025-2031.

Private Health Insurance: Over 2022-2031, private health insurance spending growth is projected to average 5.4%. Despite faster growth in private health insurance enrollment in 2022 (led by increases in Marketplace enrollment related to the American Rescue Plan Act’s subsidies), private health insurance expenditures are expected to have risen 3.0% (compared to 5.8% in 2021) due to lower utilization growth, especially for hospital services.

And for the 3 major recipient/payee categories:

Hospitals: Over 2022-2031, hospital spending growth is expected to average 5.8% annually. In 2023, faster growth in hospital utilization rates and accelerating growth in hospital prices (related to economy wide inflation and rising labor costs) are expected to lead to faster hospital spending growth of 9.3%. For 2025-2031, hospital spending trends are expected to normalize (with projected average annual growth of 6.1%) as there is a transition away from pandemic public health emergency funding impacts on spending.

Physicians and Clinical Services: Growth in physician and clinical services spending is projected to average 5.3% over 2022-2031. An expected deceleration in growth in 2022, to 2.4% from 5.6% in 2021, reflects slowing growth in the use of services following the pandemic-driven rebound in use in 2021. For 2025-2031, average spending growth for physician and clinical services is projected to be 5.7%, with an expectation that average Medicare spending growth (8.1%) for these services will exceed that of average Private Health Insurance growth (4.6%) partly as a result of comparatively faster growth in Medicare enrollment.

Prescription Drugs: Total expenditures for retail prescription drugs are projected to grow at an average annual rate of 4.6% over 2022-2031. For 2025-2031, total spending growth on prescription drugs is projected to average 4.8%, reflecting the net effects of key IRA provisions: Part D benefit enhancements (putting upward pressure on Medicare spending growth) and price negotiations/inflation rebates (putting downward pressure on Medicare and out-of-pocket spending growth).

Thus, CMS Actuaries believe spending for healthcare will be considerably higher than the growth of the overall economy (GDP) and inflation and become 19.6% of the total US economy in 2031. And it also projects that the economy will absorb annual spending increases for hospitals (5.8%) physician and clinical services (5.3%) and prescription drugs (4.6%).

My take:

Side-by-side, these reports present a curious projection for the U.S. economy through 2031: the overall economy will return to a slightly lower-level pre-pandemic normalcy and the healthcare industry will play a bigger role despite pushback from budget hawks preferring lower government spending and employers and consumers frustrated by high health prices today.

They also point to two obvious near-term problems:

1-The Federal Reserve pays inadequate attention to the healthcare economy. In Chairman Powell’s press conference following release of the FOMC report, there was no comment relating healthcare demand or spending to the broader economy nor a question from any of the 20 press corps relating healthcare to the overall economy. In his opening statement (below), Chairman Powell reiterated the Fed’s focus on prices and called out food, housing and transportation specifically but no mention of healthcare prices and costs which are equivalent or more stressful to household financial security:

“Good afternoon. My colleagues and I remain squarely focused on our dual mandate to promote maximum employment and stable prices for the American people…My colleagues and I are acutely aware that high inflation imposes hardship as it erodes purchasing power, especially for those least able to meet the higher costs of essentials like food, housing, and transportation. We are highly attentive to the risks that high inflation poses to both sides of our mandate, and we are strongly committed to returning inflation to our 2% objective.”

2-Congress is reticent to make substantive changes in Medicare and other healthcare programs despite its significance in the U.S. economy. It’s politically risky. In the June 2 Congressional standoff to lift the $31.4 debt ceiling, cuts to Medicare and Social Security were specifically EXCLUDED. Medicare is 12% of mandated spending in the 2022 federal budget and is expected to grow from a rate of 4.8% in 2022 to 8% in 2023—good news for investors in Medicare Advantage but concerning to consumers and employers facing higher prices as a result.

Even simplifying the Medicare program to replace its complicated Parts A, B, C, and D programs or addressing over-payments to Medicare Advantage plans (in 2022, $25 billion per MedPAC and $75 billion per USC) is politically tricky. It’s safer for elected officials to support price transparency (hospitals, drugs & insurers) and espouse replacing fee for service payments with “value” than step back and address the bigger issue: how should the health system be structured and financed to achieve lower costs and better health…not just for seniors or other groups but everyone.

These two realities contribute to the disconnect between the Fed and CMS. Looking back 20 years across 4 Presidencies, two economic downturns and the pandemic, it’s also clear the health economy’s emergence did not occur overnight as the Fed navigated its monetary policy. Consider:

National health expenditures were $1.366 trillion (13.3% of GDP) in 2000 and $4.255 billion in 2021 (18.3% of the GDP). This represents 210% increase in nominal spending and a 37.5% increase in the relative percentage of the nation’s GDP devoted to healthcare. No other sector in the economy has increased as much.

In the same period, the population increased 17% from 282 million to 334 million while per capita healthcare spending increased 166% from $4,845 to $12,914. This disproportionate disconnect between population and health spending growth is attributed by economists to escalating unit costs increases for the pills, facilities, technologies and specialty-provider services we use—their underlying cost escalation notably higher than other industries.

There were notable changes in where dollars were spent: hospitals were unchanged (from $415 billion/30.4% of total spending to $1.323 trillion/31.4% of total spending), physician services shrank (from $288.2 billion/21.1% of total spending to 664.6 billion/15.6% pf total spending), prescription drugs were unchanged (from $122.3 billion/8.95% to $378 billion/8.88% of total spending) and public health increased slightly (from $43 billion/$3.2% of total spending to $187.6 billion/4.4% of total spending).

And striking differences in sources of funding: out of pocket spending shrank from $193.6/14.2% of payments to $433 billion/10.2% % of payments; private insurance shrank from $441 billion/32.3% of payments to $1.21 trillion/28.4% of total payments; Medicare grew from $224.8 billion/16.5% of payments to $900.8 billion/21.2% of payments; Medicaid + CHIP grew from $203.4 billion/14.9% to $756.2 billion/17.8% of payments; and Veterans Health grew from $19.1 billion/1.4% of payments to $106.0 billion/2.5% of payments.

Thus, if these trends continue…

Aggregate payments to providers from government programs will play a bigger role and payments from privately insured individuals and companies will play a lesser role.

Hospital price increases will exceed price increases for physician services and prescription drugs.

Spending for healthcare will (continue to) exceed overall economic growth requiring additional funding from taxpayers, employers and consumers AND/OR increased dependence on private investments that require shareholder return AND/OR a massive restructure of the entire system to address its structure and financing.

What’s clear from these reports is the enormity of the health economy today and tomorrow, the lack of adequate attention and Congressional Action to address its sustainability and the range of unintended, negative consequences on households and every other industry if left unattended. It’s illustrative of the disconnect between the Fed and CMS: one assumes it controls the money supply while delegating to the other spending and policies independent of broader societal issues and concerns.

The health economy needs fresh attention from inside and outside the industry. Its impact includes not only the wellbeing of its workforce and services provided its users. It includes its direct impact on household financial security, community health and the economic potential of other industries who get less because healthcare gets more.

Securing the long-term sustainability of the U.S. economy and its role in world affairs cannot be appropriately addressed unless its health economy is more directly integrated and scrutinized. That might be uncomfortable for insiders but necessary for the greater good. Recognition of the disconnect between the Fed and CMS is a start!

Billionaire investor Charlie Munger has been vocal in expressing his concerns about U.S. healthcare, stating that it is “shot through with rampant waste” and has become “immoral.”

Munger says there are substantial problems that need to be addressed, including the presence of unnecessary costs and inefficiencies that plague the medical field.

Drawing a vivid analogy at a Daily Journal Annual Meeting, Munger compared the experience of a dying old person in many American hospitals to that of a carcass on the plains of Africa. He painted a bleak picture, describing how vultures, jackals, hyenas and other scavengers swarm around the helpless creature.

In an attempt to address these issues, Berkshire Hathaway, Amazon.com Inc., and JPMorgan Chase joined forces to establish Haven Healthcare a venture that despite their combined efforts failed to achieve its objectives.

Some startups have seen success where they failed. iRemedy, for example, is a startup using artificial intelligence (AI) technology, that offers a solution to the healthcare system’s challenges through its large procurement marketplace. Its platform streamlines the supply chain, enabling faster and more affordable access to lifesaving supplies for doctors, hospitals and healthcare providers.

Munger, vice chairman of Berkshire Hathaway Inc., criticized the high costs and inefficiencies in medical care as both expensive and wrong. In a CNBC interview, he went on to claim that some medical providers artificially prolong death to increase their profits.

With over 35 years of experience as board chairman of Good Samaritan Hospital in Los Angeles, Munger expressed his belief that certain healthcare practices are absurd.

“A lot of the medical care we do deliver is wrong — so expensive and wrong. It’s ridiculous,” he said in a “Squawk Box” interview.

In 2018, Munger predicted that when Democrats gain control of all three branches of government, there will be a push for a single-payer healthcare system. He highlighted the need for a complete change forced by the government because of the severity of the issues in the current system. He suggested that a universal healthcare system with an opt-out option would be a reasonable solution.

Warren Buffett, Munger’s longtime investing partner, shares similar concerns regarding healthcare spending, referring to it as a “tapeworm on the economic system.” Buffett believes the private sector can make substantial contributions to cost-reduction efforts.

A recent investigation conducted by Kaiser Health News-NPR shed light on the alarming reality of medical debt in the United States. The study reveals that over 100 million Americans are burdened with medical debt, placing a significant financial strain on their lives. Further analysis of the data reveals that approximately one-fourth of American adults carrying this debt owe more than $5,000.

What makes this issue even more concerning is the fact that it is not primarily driven by a lack of insurance coverage. Contrary to popular belief, the majority of people grappling with medical debt are not uninsured. Instead, it is the problem of being underinsured that is prevalent.

Many people have health insurance plans that do not offer sufficient coverage, leaving them vulnerable to high out-of-pocket expenses and accumulating medical debt.