Physicians at the American Medical Association Annual Meeting called for an overhaul of the Medicare payment system, arguing that it is outdated and threatens the survival of independent practices and patients’ access to care.

“This cannot wait; we are past the breaking point. Congress must urgently address physician concerns about Medicare to account for inflation and the post-pandemic economic reality facing practices nationwide,” AMA President Jack Resneck Jr., MD, said in a June 12 news release. “Our patients are counting on us to deliver the message that access to health care is jeopardized by Medicare’s payment system. Being mad isn’t enough. We will develop a campaign — targeted and grass roots — that will drive home our message.”

Inflation, the pandemic, declining reimbursements and rising cost are making it more challenging for independent physicians to maintain their autonomy and are jeopardizing access to care, according to the AMA, which argues that CMS physician payments have declined 26 percent from 2001 to 2023 after accounting for inflation.

In January, the Medicare Payment Advisory Commission called for a physician payment update tied to the Medicare Economic Index for the first time, and, in April, a group of House members introduced a bill that would provide annual inflation updates to the Medicare fee schedule based on the index.

“Duct-taping the widening cracks of a dilapidated payment system has put us in this precarious situation,” Dr. Resneck said. “Physicians are united in our determination to build a solid foundation rather than further jury-rigging the system.”

Last week the Minnesota legislature passed a bill to initiate the creation of a public option health insurance plan available to state residents of all incomes. The bill funds an actuarial analysis of the policy and requires the state to apply for a Centers for Medicare and Medicaid Services (CMS) waiver to begin implementation by 2027. The public option plan will build upon MinnesotaCare, a state health plan currently covering residents with incomes below 200 percent of the federal poverty line.

The Gist: Minnesota joins Washington, Colorado, and Nevada as the fourth state to authorize a public option health plan. But unlike these other three states, whose public option programs rely on private payers to manage risk and administration with tighter price controls, Minnesota intends to create a “true” public option in which the government competes directly with private payers.

Analysis funded by a hospital and insurance trade group found that a public option could reduce Minnesota hospital revenues by more than $2B over 10 years, while only lowering the uninsured rate by half a percentage point.

Though Minnesota lawmakers were more concerned with lowering healthcare spending and improving health insurance affordability for state residents, the success of the program will depend in part on how it negotiates with providers, who justifiably fear a worsening payer mix that further threatens margins.

More than a year after the regulation went into effect, compliance with the hospital price transparency rule remains low, as hospitals are hesitant to invest in necessary software and resources.

The Centers for Medicare and Medicaid Services (CMS) established the hospital price transparency rule to help individuals know the cost of a hospital item or service before receiving it.

CMS proposed the price transparency rule in the 2020 Medicare Outpatient Prospective Payment System (OPPS) and Ambulatory Surgical Center (ASC) Payment System Proposed Rule. The rule came in response to rising healthcare costs. Policymakers implemented regulations that give consumers more control over what they pay for healthcare services.

The rule went into effect on January 1, 2021, but hospitals have been slow to comply with the regulation. Without consistent compliance from hospitals and health systems, the rule does little to protect consumers from high healthcare prices.

WHAT IS THE PRICE TRANSPARENCY RULE?

The price transparency rule requires hospitals to publish the costs of their items and services on a publicly available website in two ways.

First, hospitals must have a single machine-readable digital file with standard charges for all their items and services. Standard charges include gross charges, discounted cash prices, payer-specific negotiated chargers, and de-identified minimum and maximum negotiated charges.

Hospitals must also display standard charges of at least 300 shoppable services that consumers can schedule in advance. That information must be displayed in a consumer-friendly format that includes plain language descriptions. Hospitals should also group the services with related ancillary services.

Hospitals may offer an online price estimator tool instead of publishing standard charges for the most common shoppable services. According to CMS, the price estimator tool must provide estimates for as many of the 70 CMS-specified shoppable services that the hospital offers and any additional shoppable services to reach a total of 300 services.

In addition, the tool must allow consumers to receive an estimate of the amount they will have to pay for a given service. Hospitals must display the price estimator tool on their websites and make it accessible to the public for free. Consumers also need to be able to access the tool without creating a user account.

CMS established an enforcement plan to ensure hospitals comply with the price transparency rule. The agency planned to evaluate complaints made by individuals or entities, review analyses of noncompliance, and audit hospital websites. However, more than one year after the regulation went into effect, hospitals are still not complying with the price transparency rule.

PRICE TRANSPARENCY RULE COMPLIANCE

The price transparency regulation received immediate pushback from hospital and provider groups. Before the policy went into effect, the American Hospital Association (AHA) sued HHS over the rule, stating that it would confuse consumers and increase prices.

The Kaiser Family Foundation (KFF) analyzed data from the two largest hospitals in each state and the District of Columbia and found similar trends. For example, 80 percent of the hospitals provided gross charge information on a price estimator tool and a machine-readable file, but only 35 of the 102 hospitals displayed payer-specific negotiated rates.

According to an Insights analysis from Xtelligent Healthcare Media, hospital networks frequently had inaccessible machine-readable files and shoppable services. In addition, many hospitals required patients to provide personally identifiable information in exchange for pricing data and had machine-readable files that lacked the required charges.

PatientRightsAdvocate.org has been tracking hospital compliance with the price transparency rule since May 2021. Between May and July, the organization found that out of 500 randomly selected US hospitals, only 5.6 percent were compliant with the rule.

Under the 2022 Medicare OPPS rule, CMS shared the penalties for not complying with the price transparency rule. Hospitals with less than 30 beds would receive penalties of $300 per day, while hospitals with 31 or more beds would receive a $10 per bed per day penalty, with a maximum daily fine of $5,500.

However, hospitals have not received any penalties for noncompliance as of February 2022. CMS has sent around 345 warning notices to noncompliant hospitals since the rule went into effect, the agency told Becker’s Hospital Review.

The threat of financial penalties does not seem to be enough to ensure compliance, though.

Shortly after the rule took effect, noncompliant hospitals said they were not fully complying due to resource constraints and a limited understanding of the rule. Some hospitals also mentioned that they were waiting to see how their competitors responded to the rule before achieving compliance.

More than one year later, in April 2022, financial leaders expressed similar concerns regarding compliance. Revenue cycle leaders told KLAS that a top barrier to achieving compliance was the confusing and complex regulations included in the rule.

Price transparency compliance also requires significant investment in software and outside resources, the KLAS report noted. As hospitals and health systems struggle financially due to the COVID-19 pandemic, investing in price transparency software may not be a top priority.

In addition, revenue cycle leaders reported experiencing difficulties with the software used to publish machine-readable files and a master list of prices online.

Until CMS starts delivering monetary penalties for noncompliance or adjusts the regulation to reduce the financial burden for health systems, hospital compliance with the price transparency rule will likely remain slim.

Last week, Marlee Stark and I published an op-ed in the Arkansas Democrat Gazette on why the Arkansas Department of Human Services (DHS) should press pause on its Medicaid unwinding process. Earlier this month, DHS released its first report laying out how many people lost coverage in April, as the state resumed its redetermination process.

As we write,

According to DHS’ recent report, over 50,000 people were disenrolled for procedural reasons, like failure to return paperwork or requested information, or because the state didn’t have their correct address on file. Only 15 percent of those who were disenrolled were confirmed truly ineligible or said they no longer needed their coverage, likely because they acquired another source of coverage during the pandemic.

In our piece, we argue that DHS should take a look at why so many people are losing coverage even though they may still be eligible—and outline some of the consequences the state may face if it chooses not to do so.

Congressional Republicans and the White House reached a deal over the weekend to raise the debt ceiling that includes healthcare wins for both sides of the aisle, creating a path forward to prevent economic upheaval roughly a week before a potential federal default.

The 99-page agreement released Sunday to suspend the debt ceiling until January 2025 doesn’t include Medicaid work requirements, a key priority for the White House, but it does claw back billions of unspent COVID-19 relief funds.

The bill, which already faces opposition from some hard-right Republicans, could still be halted in Congress. The government could run out of money to meet its payment obligations as early as Monday without a debt ceiling increase, according to the Treasury Department, with a default threatening Medicare and Medicaid reimbursements to states and providers.

What’s in the agreement

The deal claws back roughly $30 billion in unspent pandemic relief fundsfrom dozens of programs under the CMS, National Institutes of Health and Centers for Disease Control and Prevention, among other agencies.

However, the White House did retain money for some COVID priorities. The Biden administration will retain about $5 billion to develop coronavirus vaccines and treatments in Project NextGen, and to cover the cost of those therapies for uninsured people, according to The New York Times.

The deal leaves healthcare-related federal entitlement programs mostly untouched, a key win touted by the White House in its messaging to Democrats. Despite being targeted by Republicans during negotiations, Medicare, Medicaid and the Inflation Reduction Act emerged unscathed.

Medicaid was particularly at risk. Though the final agreement excludes Medicaid work requirements, last month Republicans in the House passed a debt ceiling bill that would have included the controversial policy. Those requirements would have resulted in an estimated 600,000 people being booted from the safety-net insurance coverage, according to the Congressional Budget Office.

“One thing this budget deal suggests: Democrats won’t go along with Republican proposals to cut or impose restrictions on Medicaid,” tweeted Larry Levitt, executive vice president of health policy at the Kaiser Family Foundation.

If passed, however, the deal would enact work rules for people receiving federal food stamps and those on the family welfare benefits program. Veterans and homeless people would be exempt from food stamp work requirements.

Those provisions put food assistance at risk for very low-income older adults, and “will increase hunger and poverty among that group,” nonpartisan think tank the Center on Budget and Policy Priorities said in a statement on the bill.

The agreement also increases funding for the Cost of War Toxic Exposures Fund, created by bipartisan legislation last summer that expanded healthcare and disability benefits for veterans exposed to toxic burn pits.

The House Rules Committee, which includes a number of critics of House Speaker Kevin McCarthy, R-Calif., who spearhead the negotiations for Republicans, will discuss the legislation Tuesday afternoon.

A full House vote on the bill could come as soon as Wednesday. Senate Majority Leader Chuck Schumer, D-N.Y., has said the Senate will immediately move to consider the bill once it leaves the House.

Tomorrow, America’s Physician Groups (APG) will kick-off its Annual Spring Conference “Going the Distance” in San Diego with breakout sessions focused on wide ranging operational issues and 3 general sessions that address restoring trust in the profession, lessons from the pandemic and Medicare Advantage.

Next Thursday, the American Medical Association (AMA) will kick off its 5-day House of Delegates session in Chicago with a plethora of resolutions and votes on the docket and committee reports on issues like the ethical impact of private equity on physicians in private equity owned practices, health insurer payment integrity and much more.

These meetings are coincident with the expected resolution of the debt-ceiling dispute in Congress which essentially leaves current Medicare and Medicaid payments to physicians and others in tact through 2025. So, for at least the time being, surprises in insurer payments to physicians are not anticipated.

Nonetheless, it’s a critical time for APG and AMA as their members face unparalleled market pressures:

Trust in the profession has eroded. Media attention to its bad actors has expanded.

Settings have changed: the majority now work as employees of large groups owned by hospitals or private equity sponsors.

Consumer (patient) expectations about physician quality, access and service are more exacting.

Technologies that improve precision in diagnostics and therapies and integration of social determinants in care planning have altered where, how and by whom care is delivered.

Affordability and lack of price transparency are fundamental concerns for U.S. consumers (and voters), employers and Congress. While drug PBMs, hospitals and health insurers are a focus of attention, physicians are not far behind.

Private equity and retail giants are creatine formidable competition in primary and specialty care.

Media coverage of “bad actors” engaged in fraudulent activity (i.e. unnecessary care, medications, et al) has increased.

Operating losses in hospitals remain significant limiting hospital investments in their employed medical practices.

Both organizations remain steadfast in the belief that the future for U.S. healthcare is physician centric:

For APG, it’s anchored in a core belief that changing payer incentives from fee-for-service to value is the essential means toward the system’s long-term sustainability and effectiveness. (APG represents 335 physician organizations)

For AMA, “true north” is the profession’s designated role as caregivers and stewards of the public’s health and wellbeing. (AMA’s membership includes 22% of the nation’s 1.34 million practicing physicians, medical students and residents).

But market conditions have taken their toll on physician psyche even as CMS has altered its value agenda.

Physicians are highly paid professionals. Per Sullivan Cotter and Kaufman Hall, their finances took a hit during the pandemic and their finances in 2022-2023 has been stymied by inflationary pressures. Thus, most worry about their income and they’re hyper-sensitive to critics of their compensation.

Fueling their frustration, virtually all believe insurance companies are reimbursement bullies, hospitals spend too much on executive salaries (aka suits) and administration and not enough on patient care and patients are increasingly difficult and unreasonable. Most think the profession hasn’t done enough to protect them and 65% say they’re burned out. That’s where APG and AMA find themselves relative to their members.

My take:

The backdrop for the APG and AMA meetings in the next 2 weeks could not be more daunting. Inflationary pressures dog the health economy as each advances an advocacy agenda suitable to their member’s needs.

But something is missing: a comprehensive, coherent, visionary view of the health system’s future in the next 10-20 years wherein physicians will play a key role.

That view should include…

How value and affordability are defined and actualized in policies and practice.

How the caregiver workforce is developed, composed and evaluated based on shifting demand.

How incentives should be set and funding sourced and rationalized across all settings and circumstances of service.

How consumerism can be operationalized.

How prices and costs in every sector (including physician services) can become readily accessible.

How a seamless system of health can be built.

How physician training and performance can be modernized to participate effectively in the system’s future.

The U.S. health system’s future is not a repeat of its past. Recognizing this, physicians and the professional associations like APG and AMA that serve them have an obligation to define its future state NOW.

Some physicians are on the brink of despair; others are at the starting line ready to take on the challenge.

In the mid-1980’s, managed care advocate Dr. Paul Ellwood predicted that eventually, US healthcare would be dominated by perhaps a dozen vast national firms he called SuperMeds that would combine managed care based health insurance with care delivery systems. Ellwood was a leader of the “managed competition” movement which advocated for a private sector alternative to a federal government-run National Health Insurance system. Ellwood and colleagues believed that Kaiser Foundation Health Plans and other HMOs would be able to stabilize health costs and thus affordably extend care to the uninsured.

The US political system and market dynamics would not co-operate with Ellwood and his Jackson Hole Group’s vision. In the ensuing thirty-five years, healthcare has remained both highly fragmented and regional in focus. However, unbeknownst to most, during the past decade, as a result of a major merger and relentless smaller acquisitions, two SuperMeds were born- CVS/Aetna and UnitedHealth Group, that whose combined revenues comprise 14% of total US health spending.

CVS/Aetna is slightly larger than United, by dint of grocery sales in its drugstores and its vast Caremark pharmacy benefits management business. However, CVS’s Aetna health insurance arm is one third the size of United’s, and though CVS is rapidly scaling up its care delivery apparatus through its in-store Health Hubs, it remains is a tiny fraction of United’s care footprint. Despite being slightly smaller at the top line, United’s market capitalization is more than 3.5 times that of CVS.

United’s vast scope is difficult to comprehend because much of it is not visible to the naked eye, and the most rapidly growing businesses are partly nested inside United’s health insurance business.

United employs over 300 thousand people. At $287.6 billion total revenues in 2021, United exceeded 7% of total US health spending (though $8.3 billion are from overseas operations).

In 2021, United was $100 billion larger than the British National Health Service. It is more than three times the size of Kaiser Permanente, and five times the size of HCA, the nation’s largest hospital chain. United is both larger and richer than energy giant Exxon Mobil. United has over $70 billion in cash and investments, and is generating about $2 billion a month in operating cash flow.

Its highly regulated health insurance business is the visible tip of a rapidly growing iceberg. Revenue from United’s core health insurance business grew at 11% in 2021, compared to 14% growth in United’s diversified Optum subsidiary. Optum generated $155.6 billion in 2021 (of which 60% were from INSIDE United’s health insurance business). You can see the relationship of Optum’s three major businesses to United’s health insurance operations in Exhibit I.

Optum is the Key to United’s Growth

Understanding the role of Optum is key to understanding United’s business. It is remarkable how few of my veteran health care colleagues have any idea what Optum is or what it does. Optum was once a sort of dumping ground for assorted United acquisitions without a seeming core purpose. A private equity colleague once derided Optum as “The Island of Lost Toys”. Now, however, Optum is driving United’s growth, and generates billions of dollars in unregulated profits both from inside the highly regulated core health insurance business and from external customers.

Optum consists of three parts:Optum Health, its care delivery enterprise ($54 billion revenues in 2021), Optum Rx, its pharmacy benefits management enterprise ($91 billion revenues in 2021) and Optum Insight, a diversified business services enterprise ($12.2 billion in 2021). Virtually all of United’s acquisitions join one of these three businesses.

Optum Health: The Third Largest Care Delivery Enterprise in the US

By itself, Optum Health is almost the size of HCA ($54 billion in 2021 vs HCA’s $58.7 billion) and consists of a vast national portfolio of care delivery entities: large physician groups, urgent care centers, surgicenters, imaging centers, and now by dint of the recently announced $5.7 billion acquisition of LHC, home health agencies. Optum Health has studiously avoided acquiring beds of any kind: hospitals, nursing homes, etc. and likely will continue to do so. Optum Health’s physician groups not only generate profits on their own, but also provide powerful leverage for United to control health costs for its own subscribers, pushing down United’s highly visible and regulated Medical Loss Ratio (MLR), and increasing health plan profits.

Optum Health began in 2007 when United acquired Nevada-based Sierra Health, and thus became the new owner of a small multispecialty physician group which Sierra owned. The group did not belong in United’s health insurance business and came to rest over in Optum. Over the past twelve years, Optum Health has acquired an impressive percentage of the major capitated medical groups in the US- Texas’ WellMed, California’s HealthCare Partners (from DaVita), as well as Monarch, AppleCare and North American Medical Management, Massachusetts’ Reliant (formerly Fallon Clinic) and Atrius in Massachusetts (pending) , Kelsey Seybold Clinic (also pending) in Houston, TX and Everett Clinic and PolyClinic in Seattle.

Optum Health claims over 60 thousand physicians, though many of these are actually independent physicians participating in “wrap around” risk contracting networks. By comparison, Kaiser Permanente’s Medical Groups employ about 23 thousand physicians. United’s management claims that Optum Health provides continuing care to about 20 million patients, of whom 3 million are covered by some form of so-called “value based” contracts. Perhaps half of this smaller number are covered by capitated (percentage of premium-PMPM) contracts.

Optum Health straddles fierce competitive relationships between United’s health insurance business and competing health plans in well more than a dozen metropolitan areas. Almost half (44%) of Optum Health’s revenues come from providing care for health plans other than United.

When Optum acquires a large physician group, it acquires those groups’ contracts with United’s health insurance competitors, some of which contracts have been in place for decades. Premium revenues from other health plans, presumably capitation or per member per month (PMPM) revenues, are one-quarter of Optum Health’s $54 billion total revenues. These “external” premium revenues have quadrupled since 2018, largely for Medicare Advantage subscribers. Optum Health contributes about $4.5 billion in operating profit to United. It is impossible to determine from United’s disclosures how much of this profit comes from Optum Health’s services provided to United’s insured lives and how much from its medical groups’ extensive contracts with competing health plans.

Optum Health’s surgicenters and urgent care centers provide affordable alternatives to using expensive hospital outpatient services and emergency departments, potentially further reducing United medical expense. This creates obvious tensions with United’s hospital networks, since Optum Health can use its large medical practices and virtual care offerings to divert patients from hospitals to its own services, or else render those services unnecessary.

Though some observers have termed Optum/United’s business model “vertical integration”-ownership of the suppliers to and distributors of a firm’s product– Optum Health has actually grown less vertical since 2018, with revenues from competing health plans growing from 36% of total revenues in 2018 to 44% in 2021. A 2018 analysis by ReCon Strategy found at best a sketchy matchup between United’s health plan enrollment by market and its Optum Health assets (https://reconstrategy.com/2018/04/uniteds-medicare-advantage-footprint-and-optumcare-network-do-not-overlap-much-so-far/.

Optum Rx: The Nation’s Third Largest Pharmacy Benefits Management Business

Optum’s largest business in revenues is its Optum Rx pharmaceutical benefits management (PBM) business, which generates $91 billion in revenues, and processes over a billion pharmacy claims not only for United but also many competing insurers and employer groups. Pharmaceutical costs are a rapidly growing piece of total medical expenses, and controlling them is yet another source of largely unregulated profits for United; Optum Rx generated over $4.1 billion of operating profit in 2021.

Optum Rx is the nation’s third largest PBM business after Caremark, owned by CVS/Aetna and Express Scripts, owned by CIGNA, and processes about 21% of all scripts written in the US. Pharmacy benefits management firms developed more than two decades ago to speed the conversion of patients from expensive branded drugs to generics on behalf of insurers and self-funded employers. They were given a big boost by George Bush’s 2004 Medicare Part D Prescription Drug benefit, as a “pro-competitive” private sector alternative to Medicare directly negotiating prices with pharmaceutical firms.

Reducing drug spending is one key to United’s profitability. Since generics represent almost 90% of all prescriptions written, Optum Rx now relies on fees generated by processing prescriptions and on rebates from pharmaceutical firms to promote their costly branded drugs as preferred drugs on Optum Rx’s formularies. These rebates are determined based on “list” prices for those drugs vs. the contracted price for the PBMs, and are actual cash payments from manufacturers to PBMs.

Drug rebates represent a significant fraction of operating profits for health insurers that own PBMs, particularly for their older Medicare Advantage patients that use a lot of expensive drugs. Unfortunately, PBMs have incentives to inflate the list price, because rebates are caculated based on the spread between list prices and the contract pricel Unfortunately, this increases subscribers’ cash outlays, because patient cost shares are based on list prices.

Optum Rx generates about 39% of its revenues (and an undeterminable percentage of its profits) serving other health insurers and self-funded employers. Many of those self-funded employers demand that Optum pass through the rebates directly to them (even if it means being charged higher administrative fees!).

Unlike the situation with Optum Health, the “verticality” of Optum’s PBM business-the percentage of Optum revenues derived from serving United subscribers- has increased in the last seven years, to more than 60% of Optum Rx’s total business. What happens to the billions of dollars in rebates generated by Optum Rx is impossible to determine from United’s disclosures. However, our best guess is that pharmaceutical rebates represent as much as a quarter of United’s total corporate profits.

Optum Insight: “Intelligent” Business Solutions

The fastest growing and by far the most profitable Optum business is its business intelligence/business services/consulting subsidiary. Optum Insight was generated $12.2 billion in revenues in 2021, but a 27.9% operating margin, five times that of United’s health insurance business. Optum Insight is strategically vital to enhancing the profitability of United’s health insurance activities, but also generates outside revenues selling services to United’s health insurance competitors and hospital networks.

The core of Optum Insight is a business intelligence enterprise formerly known as Ingenix, which provided “big data” to United and other insurers about hospital and pricing behavior and utilization-crucial both for benefits design and administration. In 2009, Ingenix was accused by New York State of under reporting prices for out of network health services for itself and its clients, which had the effect of reducing its own medical reimbursements, and increasing patient cost shares. United signed a consent decree to alter Ingenix business practices and settled a raft of lawsuits filed on behalf of patients, physicians and employers. Its name was subsequently changed to Optum Insight.

By dint of aggressive acquisitions, Optum Insight has dramatically increased its medical claims management business, consulting services and business process outsourcing activities. . Most of United’s investment in artificial intelligence can be found inside Optum Insight. Big data plays a crucial role in United’s overall strategy. Optum Insight’s claims management software uses vast medical claims data bases and artificial intelligence/machine learning software to spot and deny medical claims for which documentation is inadequate or where services are either “inappropriate” or else not covered by an individual’s health plan. Providers also claim that the same software rejects as many as 20% of their claims, often for problems as tiny as a mis-spelled word or a missing data field.

Optum Insight software plays a crucial role in helping United’s health insurance plans manage their medical expense. Traditional health plan profitability is generated by reducing medical expense relative to collected premiums to increase underwriting profit. These profits are regulated, with highly variable degrees of rigor by state health insurance commissioners, and also by provisions of ObamaCare enacted in 2010.

Though its acquisition of Equian in 2019 and the proposed $13 billion acquisition of health information technology conglomerate Change Healthcare in 2021, United came within an eyelash of a near monopoly on “intelligent” medical claims processing software. The Justice Department challenged this latter acquisition and United may agree to divest Change’s claims processing software business as a condition of closing the deal. Even without the Change acquisition, Optum Insight processes hundreds of millions of medical claims annually not only for United’s health insurance business but for many of United’s competitors.

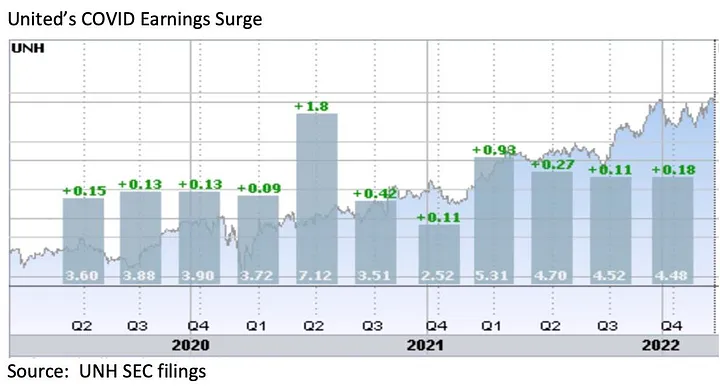

However, Optum Insight’s claims management system can also be used to increase MLR if medical expense unexpectedly declines, exposing the firm to federal requirement that it rebate excessive ‘savings’ to subscribers. This happened in 2020, when the COVID pandemic dramatically and unexpectedly added billions to United’s earnings due to hospitals suspending elective care. The chart below shows United’s 2Q2020 earnings per share almost doubling due to the precipitous drop in its medical claims expenses!

Hospital finance colleagues reported an immediate and substantial drop in medical claims denials from United and other carriers in the summer and fall of 2020. United’s quarterly profits dutifully and steeply declined in the subsequent two quarters, because its medical expenses sharply rebounded. The rise in

United’s medical expenses helped the firm avoid premium rebates to patients required by provisions of the ObamaCare legislation passed in 2010. The firm did voluntarily rebate about $1.5 billion to many of its customers in June, 2020.

However the most rapidly growing part of Optum Insight is its Optum 360 business process outsourcing business, which helps hospitals manage their billing and collections revenue cycle, as well as information technology operations, supply chain (purchasing and materials management) and other services. Through Optum 360, Optum Insight has signed five long term master contracts in the past two years’ worth many billions of dollars with care providers in California, Missouri and other states to provide a broad range of business services.

With all these different businesses, it is theoretically possible for one piece of Optum to be reducing a hospital’s cash flow by denying medical claims for United subscribers, while United’s health insurance network managers bargain aggressively to reduce the hospital’s reimbursement rates while yet another piece of Optum runs the billing and collection services for the same hospital and its employed physicians, while yet another piece of Optum competes with the hospital’s physicians and ambulatory services, diverting patients from its ERs and clinics, reducing the hospital’s revenues.

It is not difficult to imagine a future in which Optum/United offers hospital systems an Optum 360 outsourcing contract that run most of the business operations of a hospital system in exchange for preferred United health plan rates, an AI-enabled EZ pass on its medical claims denials and inpatient referrals from Optum physician groups and urgent care centers, at the expense of competing hospitals.

Managing these potential conflicts will be an increasing challenge as these various businesses grow, placing intense pressure on United’s leadership to get the various pieces of United to work together. To many anxious hospital executives, United resembles nothing so much as the Kraken, rising up out of the sea, surrounding and engulfing them- a powerful friend perhaps or a fearsome foe. As you might expect, United’s growing market power and growth has generated a fierce backlash in the hospital management community.

What Business is United Healthcare In?

United Healthcare is the most successful business in the history of American healthcare. The rapid growth of Optum and continued health insurance enrollment growth from government programs like Medicaid and Medicare has created a cash engine which generates nearly $2 billion a month in free cash flow. Optum’s portfolio has given United an impressive array of tools, unequalled in the industry, to improve its profitability and to reach into every corner of the US health system. United Healthcare is managed care on steroids.

United’s diversified portfolio of businesses gives the firm what a finance-savvy colleague termed “optionality”- the ability to redirect capital and management attention to areas of growth and away from areas that have ceased to grow, in the US or overseas. With its substantial investable capital, it will have the pick of the litter of the 11 thousand digital health companies as the overextended digital health market consolidates. United will be able to use its vast resources to build state-of-the-art digital infrastructure to reach and retain patients and manage their care.

United’s main short term business risks seem to be running out of accretive transactions effectively to deploy its growing horde of capital and managing the firm’s rising political exposure. United has had tremendous business discipline and has shied away from speculative acquisitions that are not immediately accretive to earnings. If its earnings growth falters, however, it will also encounter pressure from the investment community to increase dividends (presently about 1.2%) or share buybacks to bolster its share price, or else divest some or all of Optum in order to “maximize shareholder value”.

Answering the question, “What Business is United In” is simple: just about everything in health but hospitals and nursing homes.

Answering the questions- who are its customers and what do they want? — is a great deal harder. The customers United serves are in a sort of cold war with one another. United’s original business was protecting employers from health cost growth , and tempering the influence of hospitals and doctors by reducing their rates and utilization. By fostering so-called Consumer Directed Health Plans that expose many of their subscribers to very high front-end copayments, United and its health insurance brethren, have also increased their out-of-pocket costs, whether they have the savings to pay them or not.

There are also some ironies in United’s development. Optum Insight’s suite of hospital business services are designed to reduce administrative costs created in major part by United and other insurers’ medical claims data requirements. Its PBM business, originally intended to reduce drug spending by bargaining aggressively with pharmaceutical manufacturers has ended up pushing up drug list prices and consumer cost shares.

While presumably everybody benefits if United can somehow help patients become and remain healthy, it is still far from obvious how to do this. Managing all these markedly divergent customer needs will be a tremendous management challenge for whoever succeeds United’s reclusive (and very effective) 70 year old Chairman Stephen Hemsley.

What Does Society Get from this Vast Enterprise?

However, as Peter Drucker told a different generation of business giants, businesses are not entities unto themselves, accountable only to shareholders and customers. They are organs of society, and are expected to create social value. Americans are suspicious of vast enterprises, as businesses from Standard Oil, US Steel and ATT to Microsoft and Facebook have learned. As businesses grow and become more successful, public suspicion grows.

Private health insurers already face strident opposition from progressive Democrats, who believe that health coverage ought to be a public good, a right of citizenship provided publicly; in other words, that private health insurers have no business being in business. And large insurers like United also face intense opposition from hospitals and many physicians because they reduce their incomes and impose major administrative burdens upon them.

In the age of Twitter and TikTok, United is highly vulnerable to “event risks” that confirm the hostile narratives of the firm’s detractors that United is mainly about maximizing its own profits, not about improving the health of its subscribers or the communities it serves. It is not clear how many the tens of millions of United subscribers have warm and fuzzy feelings about their giant health insurer. Memories of the HMO backlash of the 1990’s reside in the firm’s corporate memory.

United has grown to its present immense scale largely without public knowledge. United has within its reach the capability of constraining overall health cost growth across dozens of metropolitan areas and regions, not merely cost growth for its own beneficiaries (roughly one in seven US citizens already get their health insurance through United). With its expanding digital health operations, it can deploy state of the art tools for helping United’s 50 million subscribers avoid illness and live healthier lives.

United also has the ability to damage the financial operations of beloved local hospitals and deny coverage to families, raising their out of pocket expenses. How United frames and defends its social mission and how it manages all the delicate and increasingly fraught customer relationships will determine its future, and in important ways, ours as well.

We caught up recently with a healthcare leader who had spent time in Atlanta in a previous role, and the conversation turned to last year’s closure of Atlanta Medical Center.

One major impact: the closure immediately left the Atlanta metro region, home to over 6M people, with only one Level 1 trauma center (a second Level 1 center opened an hour north of the city in February). “It’s devastating for the community to lose those services,” he shared, “but I also get why the health system made that choice, given how hard the economy has hit hospitals.” When all health systems are feeling the worst margin pressures in more than a decade, most would be reticent to step in and launch a new trauma program, which despite bringing prestige, is often a money-loser.

The conversation got us thinking about whether healthcare needs a new approach to securing essential services needed by the community which aren’t well supported by the payment system.

Our current model largely relies on nonprofit systems to meet the community need as a tenet of that status. But as one CMO shared, “If there’s more than one system in the market, we toss the responsibility back and forth like a hot potato.”

His solution: there needs to be top-down redesign of urgently needed critical services like trauma and behavioral health, as well as highly specialized services like transplant and pediatric subspecialty care, which he considered oversupplied in his market, with multiple subscale programs.

His hope was that health systems could cross competitive lines and collaborate to think about a rational approach to “regional healthcare master planning”, along with a new funding model.

It’s a tall order, he continued, but if health systems can’t find a solution on their own, they leave themselves open to government intervention that might mandate a solution—or further questions of the value communities are receiving from supporting nonprofit status.

While Congressional leaders play chicken with the debt ceiling this week, antipathy toward hospitals is mounting.

To be fair, hospitals are not alone: drug companies and PBMs share the distinction while health insurers, device companies, medical groups and long-term care providers enjoy less attention…for now.

Hospitals are soft targets. They’re also vulnerable.

They operate in a sector that’s labor intense, capital intense and highly regulated by federal, state and local governments. They’re high profile: many advertise regionally/nationally, all claim unparalleled clinical excellence and unfair treatment by health insurers.

Hospitals operate locally, so storylines like these get attention

In Minnesota, Mississippi and Pennsylvania, hospitals are in court alleging under-payments and/or adverse coverage policies by dominant insurers in their markets.

In NC, the state treasurer and others are challenging a unanimous State Senate vote last week granting the UNC Health System a waiver from antitrust concerns as it builds out its system.

In CA, nurses are striking for higher wages, improved work conditions in 5 HCA hospitals.

And in Nashville today, private equity-owned Envision will declare bankruptcy throwing its emergency room staffing contracts with hospitals into limbo.

The future for hospitals is unclear

Inpatient demand is shrinking/shifting. Outpatient, virtual, and in-home services demand is growing. Discontent among workers and employed physicians is palpable. Labor and supply chain costs wipe-out operating margins and price sensitivity among consumers and employers is soaring. Most are trying to survive any way they can. Some won’t.

Per Syntellis’ latest analysis, the tide may be turning:

Total hospital expenses rose for an 11th consecutive month, but growth in labor expenses slowed for the first three months of 2023; Total Expense rose 4.7% YOY for the month while Total Non-Labor Expense rose 5.5% YOY due to higher costs for drugs, supplies, and purchased services. Total Labor Expense was up 1.8% YOY — a slight uptick after YOY labor expense increases eased to less than 1% in January and February.

Hospital margins remained extremely narrow but inched back into the black for the first time in 15 months as revenue growth outpaced expense increases. The median, actual year-to-date Operating Margin was 0.4% for March, up from -1.1% in February.

Surgery expenses increased despite lower volumes, while levels of patient care remained relatively steady.

But no one knows for sure how long a full recovery will take, how debt ceiling negotiations will impact payments by Medicaid or Medicare or how court and antitrust actions by the DOJ will impact hospitals in the future.

What we know with a fair amount of confidence is this:

Bigger organizations in each sector—hospitals, drug & device manufacturers, medical groups, and health insurers—will have advantages others don’t.

Private equity will play a bigger role in the delivery and financing of care through strategic investments that drive low cost, high value alternatives for consumers and employers.

Regulators will enact selective price controls in targeted domains of the health system.

Large self-insured employers will be the primary catalyst for transformative changes.

Inpatient demand will shrink and tertiary services will be centralized in regulated hubs.

Structural remedies—convergence of social services and health systems, integration of financing and delivering care and direct alignment of insurer and provider incentives—will be key features of systemness choices to consumers and purchasing groups.

Most hospital boards of directors, especially not-for-profit organizations, are not prepared to calibrate the pace of these changes nor active in developing scenario possibilities for their future. That’s the place to start.

Post-pandemic recovery is not a technology-empowered 2.0 version of hospital operations: it is a fundamentally different business model based on new assumptions and bold leadership.

The national spotlight this week will be on the debt ceiling stand-off in Congress, the end of Title 42 that enables immigrants’ legal access to the U.S., the April CPI report from the Department of Labor and the aftermath of the nation’s 199th mass shooting this year in Allen TX.

The official end of the Pandemic Health Emergency (PHE) Thursday will also be noted but its impact on the health industry will be immediate and under-estimated.

The US Centers for Disease Control and Prevention (CDC) logged more than 104 million COVID-19 cases in the US as of late April and more than 11% of adults who had COVID-19 currently have symptoms of long COVID. It comes as the CDC say there’s a 20% chance of a Pandemic 2.0 in the next 2-5 years and the current death toll tops 1000/day in the U.S.

The Immediate impact:

The official end of the PHE means much of the cost for treating Covid will shift to private insurers; access to testing, vaccines and treatments with no out-of-pocket costs for the uninsured will continue through 2024. But enrollees in commercial plans, Medicare, Medicaid and the Children’s Health Insurance Program can expect more cost-sharing for tests and antivirals.

That means higher revenues for insurers, increased out of pocket costs for consumers and more bad debt for hospitals and physicians.

At the state level, Medicaid disenrollment efforts will intensify to alleviate state financial obligations for Covid-related health costs. In tandem, state allocations for SNAP benefits used by 1 in 4 long-covid victims will shrink as budget-belts tighten lending to hunger cliff.

That means less access to health programs in many states and more disruption in low-income households seeking care.

The Under-estimated Impact:

The end of the PHE enables politicians to shift “good will” toward direct care workers, home and Veteran’s health services and away from hospitals and specialty medicine who face reimbursement cuts and hostile negotiations with insurers. The April 18, 2023 White House Executive Order which enables increased funding for direct care workers called for prioritization across all federal agencies. Notably, in the PHE, hospitals received emergency funding to treat the Covid-19 patients while utilization and funding for non-urgent services was curtailed. Though the Covid-19 population is still significant, funding for hospitals is unlikely in lieu of in-home and social services programs for at risk populations.

A second unknown is this: As the ranks of the uninsured and under-insured swell, and as affordability looms as a primary concern among voters and employers, provider unpaid medical bills and “bad debt” increases are likely to follow.

Hostility over declining reimbursement between health insurers and local hospitals and medical groups will intensify while the biggest drug manufacturers, hospital systems and health insurers launch fresh social media campaigns and advocacy efforts to advance their interests and demonize their foes.

Loss of confidence in the system and a desire for something better may be sparked by the official end of the PHE. And it’s certain to widen antipathy between insurers and hospitals.

My take:

In this month’s Health Affairs, DePaul University health researchers reported results of their analysis of the association between hospital reimbursement rates and insurer consolidation:

“Our results confirm this prior work and suggest that greater insurer market power is associated with lower prices paid for services nationally. A critical question for policy makers and consumers is whether savings obtained from lower prices are passed on in the form of lower premiums. The relationship to premiums is theoretically ambiguous. It is possible that insurers simply retain the savings in the form of higher profits.”

What’s clear is health insurers are winners and providers—especially hospitals and physicians—are likely losers as the PHE ends. What’s also clear is policymakers are in no mood to provide financial rescue to either.

In the weeks ahead as the debt ceiling is debated, the Federal FY 2024 budget finalized and campaign 2024 launches, the societal value of the entire health system and speculation about its preparedness for the next pandemic will be top of mind.

For some—especially not-for-profit hospitals and insurers who benefit from tax exemptions in favor of community health obligations– it requires rethinking of long-term strategies to serve the public good. And it necessitates their Boards to alter capital and operating priorities toward a more sustainnable future.

The pandemic exposed the disconnect between local health and human services programs and inadequacy of local, state and federal preparedness Given what’s ahead, the end of the Pandemic Health Emergency seems ill-timed and short-sighted: the impact will further destabilize the health industry.

Paul

PS: Saturday, the Allen Premium Outlets, (Allen, TX) was the site of America’s 199th mass shooting this year:

this time, 8 innocents died and 7 remain hospitalized, 4 in critical condition. Sadly, it’s becoming a new normal, marked by public officials who offer “thoughts and prayers” followed by calls for mental health and gun controls. Local law enforcement is deified if prompt or demonized if not. But because it’s a “new normal,” the heroics of EMS, ED and hospitals escapes mention. Medical City Healthcare is where 2 of the 8 drew their last breaths while staff labored to save the other 7. At a time when hospitals are battered by bad press, they deserve recognition for work done like this every day.