This week, Statpublished a scathing investigation into the way UnitedHealth Group subsidiary NaviHealth uses an algorithm, nH Predict, to deny Medicare Advantage (MA) patients access to rehabilitation services and long-term care. United set a target to keep rehab stays within one percent of nH Predict’s projection for the year.

Interviews with former case managers and access to internal documents reveal that NaviHealth employees faced disciplinary action and even termination if they approved care that strayed from these algorithmic recommendations.

UnitedHealthcare, the nation’s largest insurer, is now subject to a class-action lawsuit filed this week over these practices. But NaviHealth’s impact extends beyond just United beneficiaries, as other insurers, covering around 15M MA enrollees, also use its services.

The Gist:This article provides a stark example of what can happen when an artificial intelligence (AI) algorithm is used not to complement, but to replace, clinical judgment.

While profit incentives in US healthcare are nothing new, what’s pernicious about an algorithm like nH Predict is how it replaces individual patients, whose needs vary, with a theoretical “average patient”, whose health and life needs can be easily predicted by the handful of data points available to the insurer.

When patients fail to recover along expected timelines—that are imperfectly calculated by incomplete datasets—they’re the ones who suffer.

Hospitals and health systems are seeing some signs of stabilization in 2023 following an extremely difficult year in 2022. Workforce-related challenges persist, however, keeping costs high and contributing to issues with patient access to care. The percentage of respondents who report that they have run at less than full capacity at some time over the past year because of staffing shortages, for example, remains at 66%, unchanged from last year’s State of Healthcare Performance Improvement report. A solid majority of respondents (63%) are struggling to meet demand within their physician enterprise, with patient concerns or complaints about access to physician clinics increasing at approximately one-third (32%) of respondent organizations.

Most organizations are pursuing multiple strategies to recruit and retain staff. They recognize, however, that this is an issue that will take years to resolve—especially with respect to nursing staff—as an older generation of talent moves toward retirement and current educational pipelines fail to generate an adequate flow of new talent. One bright spot is utilization of contract labor, which is decreasing at almost two-thirds (60%) of respondent organizations.

Many of the organizations we interviewed have recovered from a year of negative or breakeven operating margins. But most foresee a slow climb back to the 3% to 4% operating margins that help ensure long-term sustainability, with adequate resources to make needed investments for the future. Difficulties with financial performance are reflected in the relatively high percentage of respondents (24%) who report that their organization has faced challenges with respect to debt covenants over the past year, and the even higher percentage (34%) who foresee challenges over the coming year. Interviews confirmed that some of these challenges were “near misses,” not an actual breach of covenants, but hitting key metrics such as days cash on hand and debt service coverage ratios remains a concern.

As in last year’s survey, an increased rate of claims denials has had the most significant impact on revenue cycle over the past year. Interviewees confirm that this is an issue across health plans, but it seems particularly acute in markets with a higher penetration of Medicare Advantage plans. A significant percentage of respondents also report a lower percentage of commercially insured patients (52%), an increase in bad debt and uncompensated care (50%), and a higher percentage of Medicaid patients (47%).

Supply chain issues are concentrated largely in distribution delays and raw product and sourcing availability. These issues are sometimes connected when difficulties sourcing raw materials result in distribution delays. The most common measures organizations are taking to mitigate these issues are defining approved vendor product substitutes (82%) and increasing inventory levels (57%). Also, as care delivery continues to migrate to outpatient settings, organizations are working to standardize supplies across their non-acute settings and align acute and non-acute ordering to the extent possible to secure volume discounts.

Survey Highlights

98% of respondents are pursuing one or more recruitment and retention strategies

90%have raised starting salaries or the minimum wage

73%report an increased rate of claims denials

71% are encountering distribution delays in their supply chain

70%are boarding patients in the emergency department or post-anesthesia care unit because of a lack of staffing or bed capacity

66% report that staffing shortages have required their organization to run at less than full capacity at some time over the past year

63% are struggling to meet demand for patient access to their physician enterprise

60% see decreasing utilization of contract labor at their organization

44%report that inpatient volumes remain below pre-pandemic levels

32% say that patients concerns or complaints about access to their physician enterprise are increasing

24%have encountered debt covenant challenges during the past 12 months

None of our respondents believe that their organization has fully optimized its use of the automation technologies in which it has already invested

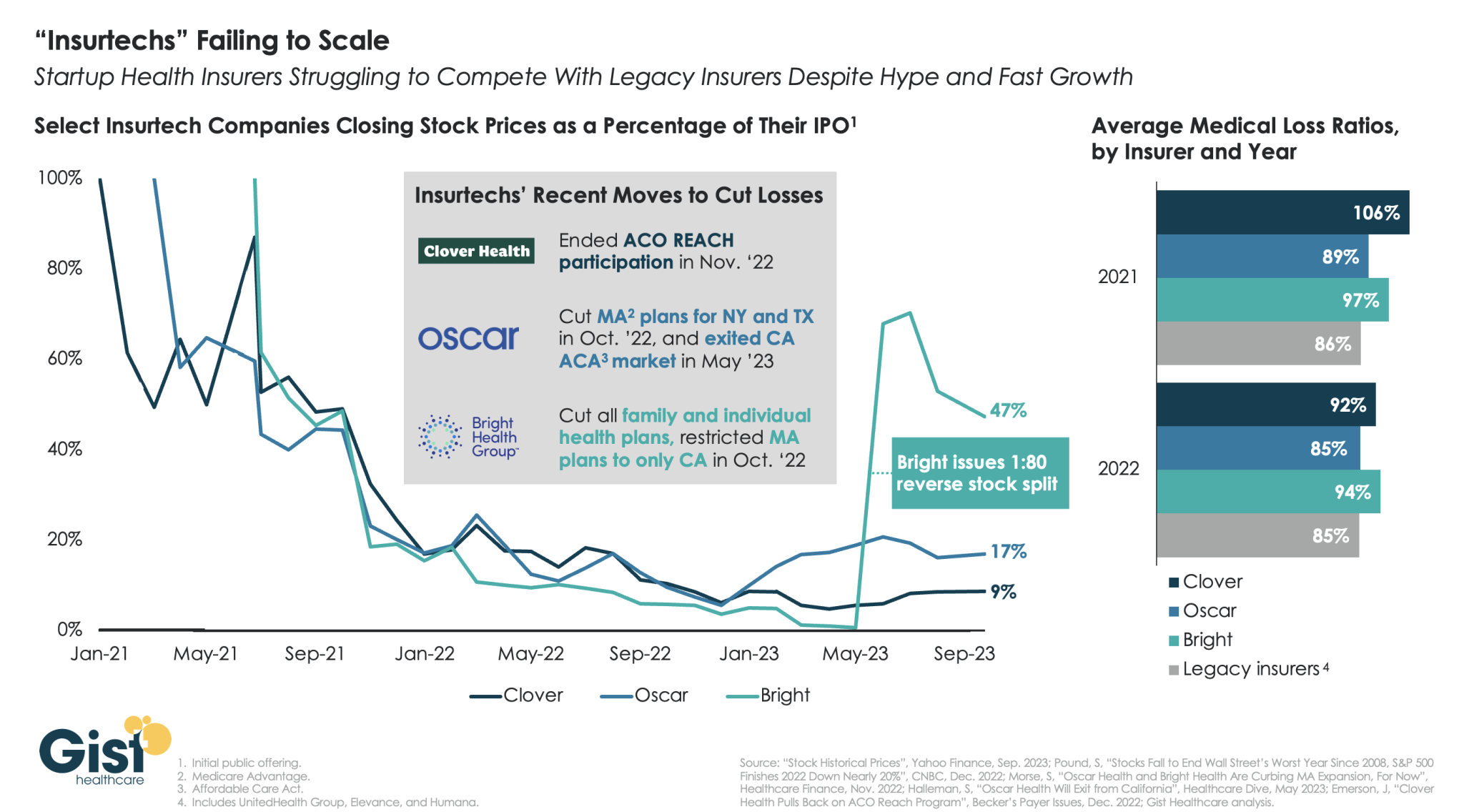

“Insurtechs” Clover Health, Oscar Health, and Bright Health all went public in the midst of the hot equity market of 2021. Investors were excited by the fast growth of these health insurer startups, and their potential to revolutionize an industry dominated by a few large players.

However, the hype has dissipated as financial performance has deteriorated. After growing at all costs during a period of low interest rates, changing market conditions directed investors to demand a pivot to profitability,which the companies have struggled to deliver—twoyears later,none of the three has turned a profit.

Oscar and Bright have cut back their market presence significantly, while Clover has mostly carried on while sustaining high losses. In the last two years, only Oscar has posted a medical loss ratio in line with other major payers, who meanwhile are reporting expectation-beating profits. While Oscar has shown signs of righting the ship since the appointment of former Aetna CEO Mark Bertolini,

the future of these small insurers remains uncertain. As their losses mount and they exit markets, they may become less desirable as acquisition targets for large payers.

With Medicare’s Annual Election Period (also known as Open Enrollment) beginning on October 15th, over 65 million adults across the United States will have until December 7th to decide whether they plan to renew or change their Medicare coverage. Beneficiaries choose between Traditional Medicare (TM) and a variety of Medicare Advantage (MA) plans and prescription drug coverage.

For this enrollment cycle, it is estimated that the average beneficiary will have over 40 plans to choose from, leading to complexity. For those who are dually eligible for both Medicare and Medicaid benefits, there is an even greater number of options for them to consider, especially if they live in areas where integrated options such as dual-eligible special needs plans and Medicare-Medicaid plans are available.

As the US population continues to age and the number of Medicare enrollees grow, it is important to understand how beneficiaries make their coverage decisions and ensure they are protected from any misinformation in the process.

Though already complex, the plan selection process for older adults is further complicated by the deceptive marketing tactics that brokers, agents, and third-party marketing organizations (TPMOs) have employed in recent years. In a recent study, the Commonwealth Fund identified how some of these practices are driven by the financial incentives associated with enrolling beneficiaries in particular MA plans.

Between robocalls and misleading television advertisements, many beneficiaries across the country have found themselves enrolled in MA plans they did not intend to enroll in, or that did not cover services or in-network providers that they were initially marketed. In a sweeping review of Medicare Open Enrollment-related television ads, Kaiser Family Foundation found that the majority of Open Enrollment-related advertisements last year promoted the Medicare logo and privately-operated hotlines, misleading beneficiaries into believing these were government sponsored ads and helplines.

Acknowledging the growing concerns and complaints among beneficiaries, the Centers for Medicare and Medicaid Services (CMS) announced that starting in 2024, Medicare-related television ads must be approved in advance of airing and cannot contain plan names or Medicare logos and images that misrepresent their organization or agency. Additional consumer protections included in the 2024 MA and Part D Final Rule will hold brokers, agents, and other TPMOs to higher standards of providing transparent, quality information. These activities include monitoring TPMO behavior, regulating how and when they market to beneficiaries, ensuring brokers review the full list of options and choices available to a beneficiary, and going through a detailed, standardized set of pre-enrollment questions. There is also an increased effort in getting beneficiaries to use some of the federally funded tools and resources available to assist in their coverage decisions.

Some of these tools include the Medicare.gov website, the CMS Medicare Plan Compare tool, and a 1-800-MEDICARE hotline to help inform beneficiaries about their benefits. However, a study by Hernandez et al. revealed that very few Medicare beneficiaries utilized these tools and often felt more comfortable discussing their options in-person with brokers or family members and friends, even though these sources may be biased or potentially inaccurate. Additionally, it is important to recognize that navigating these tools requires some degree of health literacy and technological proficiency, which may disproportionately affect those who are low-income, have lower levels of education, or are non-native English speakers.

The State Health Insurance Assistance Program (SHIP), however, is a free and unbiased resource for Medicare counseling that few beneficiaries are aware of. In 1990, the federal government implemented SHIPs to help support Medicare beneficiaries with free, one-to-one health insurance counseling and education within their communities. It is currently run by the Administration for Community Living (ACL). The ACL administers grants to states, who in turn provide funding to community-level subgrantees to maintain various networks of full-time, part-time, and/or volunteer counselors. The latest available data suggests that SHIPs provided assistance to 2.7 million Medicare beneficiaries from April 2018 through March 2019—just 4.5% of the eligible Medicare population.

While some states had greater success, serving over 10% of their eligible population, others were only able to reach as few as 2%. A 2018 evaluation of California’s SHIP, called HICAP (Health Insurance Counseling & Advocacy Program), highlighted the strengths of this community-based counseling system. HICAP reported high rates of engagement, citing their ability to deliver uniquely tailored counseling to beneficiaries in their native languages and through in-person or hybrid settings depending on the beneficiary’s condition or preferences. Moreover, strong marketing efforts via Spanish radio shows and mailing postcards were particularly effective in reaching “hard-to-locate” populations. However, the program did experience challenges given the variation in operations across locations, citing concerns over the recruitment, training and retention of volunteers and paid staff.

In recognition of SHIP’s potential to provide an unbiased alternative to brokers and combat misinformation, CMS finalized a requirement in the 2024 MA and Part D rule that TPMOs are to provide a disclaimer citing SHIP as an option for beneficiaries to obtain additional help (42 CFR § 422.2267(e )(41)). But despite SHIP’s promise, some beneficiary advocates have worried that the multi-tiered, volunteer, and part-time driven delivery model that characterizes most SHIPs leads to access and quality gaps. This is especially a concern among vulnerable beneficiaries who may live in low-income neighborhoods, have disabilities, or limited English proficiency. Given their historically low utilization rates and limited visibility, others have expressed concern that SHIPs may be ill-equipped to handle an increased demand for services in the coming year, due to more Medicare beneficiaries being advised of their existence through TPMO disclaimers. With the limited evidence about SHIP’s performance and outreach nationally, given the diffuse nature of the program, it will be important to understand some of the barriers and facilitators they face to delivering timely and accurate Medicare counseling.

The free and unbiased nature of the SHIP program presents a promising alternative to helping beneficiaries navigate complex plan choices for Open Enrollment. As MA enrollment increases and as plan choices become more complex, the SHIP program should be monitored for potential inequities in access to and quality of services based on area income.

For more information about your state’s SHIP program and to find a local Medicare counselor, please visit https://www.shiphelp.org/.

Medicare Advantage provides health coverage to more than half of the nation’s seniors, but a growing number of hospitals and health systems nationwide are pushing back and dropping the private plans altogether.

Among the most commonly cited reasons are excessive prior authorization denial rates and slow payments from insurers. Some systems have noted that most MA carriers have faced allegations of billing fraud from the federal government and are being probed by lawmakers over their high denial rates.

“It’s become a game of delay, deny and not pay,” Chris Van Gorder, president and CEO of San Diego-based Scripps Health, told Becker’s.

“Providers are going to have to get out of full-risk capitation because it just doesn’t work — we’re the bottom of the food chain, and the food chain is not being fed.”

In late September, Scripps began notifying patients that it is terminating Medicare Advantage contracts for its integrated medical groups, a move that will affect more than 30,000 seniors in the region. The medical groups, Scripps Clinic and Scripps Coastal, employ more than 1,000 physicians, including advanced practitioners.

Mr. Van Gorder said the health system is facing a loss of $75 million this year on the MA contracts, which will end Dec. 31 for patients covered by UnitedHealthcare, Anthem Blue Cross, Blue Shield of California, Centene’s Health Net and a few more smaller carriers. The system will remain in network for about 13,000 MA enrollees who receive care through Scripps’ individual physician associations.

“If other organizations are experiencing what we are, it’s going to be a short period of time before they start floundering or they get out of Medicare Advantage,” he said. “I think we will see this trend continue and accelerate unless something changes.”

Bend, Ore.-based St. Charles Health System has taken it a step further and is not only considering dropping all Medicare Advantage plans, but is also encouraging its older patients not to enroll in the private Medicare plans during the upcoming enrollment period in October.

The health system’s president and CEO, CFO and chief clinical officer cited high rates of denials, longer hospital stays and overall administrative burden for clinicians.

“We recognize changing insurance options may create a temporary burden for Central Oregonians who are currently on a Medicare Advantage plan, but we ultimately believe it is the right move for patients and for our health system to be sustainable into the future to encourage patients to move away from Medicare Advantage plans as they currently exist,” St. Charles Health CFO Matt Swafford said.

“I feel terrible for the patients in this situation; it’s the last thing we wanted to do, but it’s just not sustainable with these kinds of losses,” Mr. Van Gorder added. “Patients need to be aware of how this system works. Traditional Medicare is not an issue. With these other models, seniors need to be wary and savvy buyers.”

Here are six more recent examples of hospitals dropping Medicare Advantage contracts:

1. Adena Regional Medical Center is terminating its contract with Anthem BCBS’ Medicare Advantage and managed Medicaid plans in Ohio, effective Nov. 2. The flagship facility of Chillicothe, Ohio-based Adena Health System said rate negotiations between the organizations “have not been productive,” leading it to terminate its agreement with Anthem, whose parent company is Elevance Health.

2. Corvallis, Ore.-based Samaritan Health Servicesended its commercial and Medicare Advantage contracts with UnitedHealthcare. The five-hospital, nonprofit health system cited slow “processing of requests and claims” that have made it difficult to provide appropriate care to UnitedHealth’s members, which will be out of network with Samaritan’s hospitals on Jan. 9. Samaritan’s physicians and provider services will be out of network on Nov. 1, 2024.

3. Cameron (Mo.) Regional Medical Center stopped accepting Cigna’s MA plans in 2023 and plans to drop Aetna and Humana in 2024. It plans to continue Medicare Advantage contracts with UnitedHealthcare and BCBS, the St. Joseph News-Press reported in May. Cameron Regional CEO Joe Abrutz previously told the newspaper the decision stemmed from delayed reimbursements.

4. Stillwater (Okla.) Medical Centerended all in-network contracts with Medicare Advantage plans amid financial challenges at the 117-bed hospital. Humana and BCBS of Oklahoma were notified that their MA members would no longer receive in-network coverage after Jan. 1, 2023. The hospital said it made the decision after facing rising operating costs and a 22 percent prior authorization denial rate for Medicare Advantage plans, compared to a 1 percent denial rate for traditional Medicare.

5. Brookings (S.D.) Health System will no longer be in network with any Medicare Advantage plans in 2024, the Brookings Register reported. The 49-bed, municipally owned hospital said the decision was made to protect the financial sustainability of the organization.

6. Louisville, Ky.-based Baptist Health Medical Group went out of network with Humana’s Medicare Advantage and commercial plans on Sept. 22, Fox affiliate WDRB reported.

A number of health systems have recently noted increasing financial challenges for Medicare Advantage (MA) patient admissions.

One CFO shared, “our rates from MA plans are roughly on par with fee-for-service Medicare. Denials have always been a problem, making our [revenue] capture about 90 percent. But this year it’s dropped to 80 percent…it’s a crisis for us, given fast how MA volumes are growing.”

His team investigated the change and found the cause: mean length of stay for MA patients has jumped sharply. The rise was almost entirely due to difficulties in discharging patients to rehab and skilled nursing facilities.

Key insurers have narrowed their postacute networks, resulting in patients spending days waiting for a bed. “The payers told us they had focused the network on ‘high-performing’ providers. Our data and doctors’ experiences say otherwise. They chose a handful of facilities that are cheap, with questionable quality,” their CMO reported. Attempts to engage payers to solve the problem have gone nowhere:

“They have a disincentive to work with us on this. With case rates, they are saving money if patients are languishing in an expensive hospital bed rather than going to rehab.”

This system is exploring expedited placement and expanding their portfolio of home-based care and postacute offerings, while even considering guaranteeing payment themselves. If you’re having similar challenges or have found solutions to help with transitions of care, we’d love to hear from you and learn more.

Favorable selection of healthier beneficiaries led to overpayments in counties with high Medicare Advantage penetration, but benchmark changes could mitigate the impact.

Dive Brief:

Favorable selection of beneficiaries in Medicare Advantage is throwing off benchmarks used to set payments to those plans, resulting in billions of overpayments to the privatized insurance program for seniors, according to a study published this week in Health Affairs.

Healthier people are more likely to enroll in MA compared to traditional Medicare, leading to overpayment in counties with high levels of MA participation and underpayment in counties with less MA market penetration, the study found.

Overall, MA plans were overpaid by an average of $9.3 billion per year between 2017 and 2020. As seniors increasingly turn to MA plans, setting payment benchmarks based on traditional Medicare spending has become “less tenable” and requires reform, researchers argued.

Dive Insight:

Overpayments to MA plans are a growing concern for regulators and researchers as more seniors choose the increasingly popular coverage option. More than half of the eligible Medicare population is now enrolled in MA, a stark increase from 19% of the eligible population enrolled in 2007.

One analysis from the USC Schaeffer Center for Health Policy and Economics found overpayments could reach more than $75 billion this year due to the favorable selection of healthier beneficiaries, aggressive coding and quality bonuses.

MA plans are administered by private insurers and paid a set amount each month regardless of beneficiaries’ use of healthcare services. Those payment rates are set by benchmarks in each county every year alongside quality payments and risk scores based on beneficiaries’ health needs.

But those benchmarks, which are tied to risk-adjusted spending in traditional Medicare, may be contributing to overpayments to MA plans, as healthier people are more likely to choose MA and sicker seniors switch to traditional Medicare plans.

The distribution of MA beneficiaries has also shifted toward counties that were overpaid, according to the study.

In benchmark year 2020, 31.4% of MA beneficiaries lived in underpaid counties, while 68.6% lived in counties that were overpaid, the study found. There were more than 2,700 underpaid counties compared with just over 330 overpaid counties, highlighting the concentration of beneficiaries in counties with high MA market penetration.

In underpaid counties, underpayments totaled a loss of $407 per beneficiary, while overpayments reached an extra $762 per beneficiary in overpaid areas.

Overall, the Health Affairs study estimated that overpayments to MA plans reached $37.3 billion between 2017 and 2020.

The CMS could take action to improve its risk adjustment methodology, which doesn’t take into account favorable selection dynamics for MA, according to the study.

“The simplest strategy would be to allow risk adjustment to vary according to MA penetration, thereby flattening the relationship between traditional Medicare risk and spending across levels of MA penetration,” the authors wrote.

Federal regulators have moved to audit MA plans and are attempting to claw back billions in overpayments.

Insurers have pushed back on the rule. Humana, one of the largest providers of MA plans in the country, sued the HHS last week, arguing the regulation is unfair and should be vacated.

A hospital CEO recently relayed a story about challenges in access and coverage for pulmonology services in their market. A key group of pulmonologists there had scaled back hospital coverage and stopped seeing outpatients entirely.

“We’re hearing that they are spending almost all of their time seeing patients in skilled nursing facilities (SNFs),” she shared. Shortly after, we heard from another health system that their cardiologists had started rounding frequently in long-term care sites. This seemed unusual, given that payment for specialist consults in SNFs and other long-term care facilities is meager—it’s hard enough to find hospitalists or rehabilitation physicians to provide coverage and round at these sites.

However, it struck us that both of these health systems were located in markets with a high penetration of Medicare Advantage (MA) plans, and we wonder whether MA plans have increased payment to specialists to motivate them to consult in skilled nursing settings?

It’s unclear if policies have changed, but it would make sense. If a cardiologist could evaluate a patient in a SNF and avert an ambulance ride and hospital admission, the MA plan would save money.

But if health plans chose to do this at scale, it could prompt a significant shift in how some doctors spend their time, while leaving access gaps in other settings. If you’re seeing similar changes in your market, we’d be interested in hearing more!

Last week, the nation’s two largest Medicare Advantage insurers revealed that second quarter outpatient volumes were higher than anticipated, prompting a selloff of insurance stocks.

Minnetonka, MN-based UnitedHealth Group (UHG) executives said at a Goldman Sachs investor conference that increased outpatient utilization was driving up its medical loss ratio (MLR) to the high end of its annual target, surmising that a new wave of seniors were finally accessing elective procedures like joint replacements postponed throughout COVID.

Then, in an investor filling, Louisville, KY-based Humana noted that both outpatient and inpatient utilization levels were elevated, though it did not point to any specific causes. But not all insurers have experienced higher-than-expected utilization: Indianapolis, IN-based Elevance Health reported that its medical spending this year so far was in line with expectations, and it did not expect a surge in procedure demand.

The Gist: Health systems will find this news, especially Humana’s reports of elevated inpatient and emergency department volumes, as encouraging as the insurers consider it alarming. But the bulk of this outpatient volume isn’t necessarily returning to health systems, as the proliferation of insurer- and investor-backed ambulatory surgery centers has resulted in not only more, but also lower-cost, competition.

Health systems with significant ambulatory surgery center footprints, including Tenet and HCA, should be well-positioned to capture the volume return.