Running a health system recently has proven to be a very hard job. Mounting losses in the face of higher operating expenses, softer than expected volumes, deferred capex, and strained C-suite succession planning are just a few of the immediate issues with which CEOs and boards must deal.

But frankly, none of those are the biggest strategic issue facing health systems. The biggest strategic issue is the reorganization of the American healthcare landscape into an ambulatory care business that emphasizes competing for covered lives at scale in lower cost and convenient settings of care. This shift in business model has significant ramifications, if you own and operate acute care hospitals.

Village MD and Optum are two of the organizations driving the business model shift. They are owned by large publicly traded companies (Walgreens and UnitedHealth Group, respectively). Both Optum and Village MD have had a string of announced major patient care acquisitions over the past few years, none of which is in the acute care space.

The future of American healthcare will likely be dominated by large well-organized and well-run multi-specialty physician groups with a very strong primary care component. These physician service companies will be payer agnostic and focused on value-based care, though will still be prepared to operate in markets where fee-for-service dominates. They will deliver highly coordinated care in lower cost settings than hospital outpatient departments. And these companies will be armed with tools and analytics that permit them to manage the care for populations of patients, in order to deliver both better health outcomes and lower costs.

At the same time this is happening, we are experiencing steady growth in Medicare Advantage. And along with it, a stream of primary care groups who operate purpose-built clinics to take full risk on Medicare Advantage populations. These companies include ChenMed, Cano Health and Oak Street, among others. These organizations use strong culture, training, and analytics to better manage care, significantly reduce utilization, and produce better health outcomes and lower costs.

Public and private equity capital are pouring into the non-acute care sectors, fueling this growth. As of the start of 2022, nearly three quarters of all physicians in the US were employed by either corporate entities (such as private equity, insurance companies, and pharmacy companies), or employed by health systems. And this employment trend has accelerated since the start of the pandemic. The corporate entities, rather than health systems, are driving this increasing trend. Corporate purchases of physician practices increased by 86% from 2019 to 2021.

What can health systems do? To succeed in the future, you must be the nexus of care for the covered lives in your community. But that does not mean the health system must own all the healthcare assets or employ all of the physicians. The health system can be the platform to convene these assets and services in the community. In some respects, it is similar to an Apple iPhone. They are the platform that convenes the apps. Some of those apps are developed and owned by Apple. But many more apps are developed by people outside of Apple, and the iPhone is simply the platform to provide access.

Creating this platform requires a change in mindset. And it requires capital. There are many opportunities for health systems to partner with outside capital providers, such as private equity, to position for the future – from both a capital and a mindset point of view.

The change in mindset, and the access to flexible capital, is necessary as the future becomes more and more about reorganizing into an ambulatory care business that emphasizes competing for covered lives at scale in lower cost and convenient settings of care.

Before 2006, Medicare Advantage in its current form didn’t exist. Now, the public-private program is expected to overtake traditional Medicare this year — how did it get here?

Medicare Advantage basics

Medicare is a federal insurance program that started in 1965 to primarily provide health coverage to Americans 65 and older.

Medicare Advantage is a federally-approved plan from a private insurance company that provides more coverage than traditional Medicare.

In 2022, 28.4 million people were enrolled in MA out of 58.6 million Medicare beneficiaries overall – or 48 percent.

Medicare is divided into four parts: A: Hospital insurance (hospital, skilled nursing, home health and hospice services) B: Medical insurance (outpatient services, physician visits, preventive screenings) C: Medicare Advantage D: Prescription drug insurance

The Centers for Medicare and Medicaid Services (CMS) oversees all Medicare plans. In 1997, Part C (MA) was created, and Part D was introduced in 2006.

Traditional Medicare includes Parts A and B, though Part B is optional. MA plans cover Parts A, B and D benefits.

When Congress created MA, it was initially called Medicare+Choice. In 2003, most Medicare+Choice plans were rebranded as Medicare Advantage.

Supplemental Medicare, or Medigap, are plans that can be purchased from commercial payers by traditional enrollees to cover more services.

Part C (MA) operates under a capitated fee, or when MA insurers are paid a set amount per beneficiary, and then pay for their health expenses. Traditional Medicare is fee-for-service, where providers are paid per service delivered.

If a provider accepts Medicare, enrollees are able to receive care there. MA members are typically confined to a select network of providers for non-emergency care, but coverage must meet or exceed traditional Medicare standards.

Terminology: Words and phrases associated with MA

Preferred Provider Organization (PPO): An MA plan with a large provider network that members pay less to use. Out-of-network providers can provide covered services for a higher cost, and emergency care is always covered. PPOs make up 40 percent of MA offerings in 2023.

Health Maintenance Organization (HMO): An MA plan where care is only covered with in-network providers, except for emergency care. HMOs account for 58 percent of MA offerings in 2023.

HMO-Point-of-Service (HMO-POS): HMO plans that allow some out-of-network services for a higher copayment.

Dual-Eligible Special Needs Plans (D-SNP): Special MA plans that provide coverage to beneficiaries eligible for both Medicare and Medicaid.

Private Fee-for-Service (PFFS): A fee-for-service MA plan that pays set amounts for care. Most PFFS plans have provider networks that charge less. They must cover out-of-network care, but usually at a higher cost – these make up less than 1 percent of plans.

Accountable Care Organization (ACO): A group of providers who join together to provide high-quality care to Medicare patients. ACO models are overseen by CMS, and several types now exist.

Prior authorization: Permission needed from the insurer for coverage, often for specialists or out-of-network care. Part D plans usually require PA for specialty drugs, but the process is plan specific.

Star ratings: An annual performance rating from CMS ranging from 1 to 5 stars, with 5 being the highest. Plans with four or more stars receive monetary bonuses that then must be used to improve benefits.

Medicare Advantage today

MA is expected to make up half of all Medicare enrollment in 2023. Under current growth, the program will hit 69 percent by 2030.

A record 3,998 MA plans are available nationwide in 2023, up 6 percent from the previous year.

The average beneficiary has 43 MA plans to choose from in 2023, up from 38 in 2022.

In 2023, 57 MA and Part D plans earned a five star designation, a decline from 2022, when 74 plans earned the designation.

The average star rating across all plans for 2023 is 4.15, down from 4.37 in 2022.

The top five reasons enrollees chose MA plans over traditional in 2022: More benefits: 24 percent Out-of-pocket limit: 20 percent Recommended by trusted people: 15 percent Offered by former employer: 11 percent Maintain same insurer: 9 percent

The largest MA insurers in 2022: UnitedHealthcare: 7 million Humana: 5.1 million BCBS plans: 4.1 million CVS Health/Aetna: 3.3 million Kaiser Permanente: 1.8 million Centene: 1.5 million Cigna: 540,000

The average monthly MA premium is projected to be $18 for 2023, down from $19.52 in 2022.

Part D average premiums for 2023 are expected to be $31.50, down from $32.08 in 2022.

The standard monthly premium for Part B enrollees is $164.90 for 2023, a decrease of $5.20 from 2022.

Traditional Medicare members spent about 7 percent more on average for healthcare compared to MA members in 2019, according to an AHIP study published Sept. 21.

MA members spent $1,965 less on average on out-of-pocket costs and premiums annually compared to traditional Medicare beneficiaries in 2019, an April 19 study from the Better Medicare Alliance found.

Around 16 percent of MA enrollees switch insurance after one year of enrollment, an Oct. 4 study in the American Journal of Managed Care found. Nearly half switched insurers by their fifth year.

MA enrollees received 9.2 percent fewer low-value services than their counterparts using traditional Medicare, a study published Sept. 9 in JAMA Open Network found.

About a third, or 31.6 percent, of the 57 MA plans that earned five stars in 2023 are a part of the Alliance of Community Health Plans, a trade group representing integrated payer-providers.

MA plans were the most likely health plans to use alternative payment models in 2022, with 57 percent using some kind of alternative payment. Of those, 35 percent used a risk-based model.

Half of the 13 percent of employers who offered retirement health benefits in 2022 did so through MA plans, up from 26 percent in 2017, according to a report from Kaiser Family Foundation published Dec. 1.

In 2023, 1,111 MA plans will offer extra benefits beyond vision, dental and hearing, which is up from 351 in 2020.

Percentage of MA plans offering extra benefits in 2022: Vision: 99 percent Hearing: 98 percent Fitness: 98 percent Dental: 96 percent Remote access: 72 percent Meals: 71 percent Acupuncture: 45 percent Transportation: 39 percent In-home support: 12 percent Bathroom safety: 9 percent Part B rebate: 7 percent Telemonitoring: 4 percent Plans with caregiver support: 4 percent

Geography

Texas saw the most growth in MA offerings from 2022 to 2023, with 42 more plans. That was followed by Florida (26) and Pennsylvania (21).

Alabama had the highest MA enrollment rate (53 percent of all Medicare) in 2022, while Wyoming had the lowest (6 percent).

In 34 percent of metropolitan areas, one payer controls more than half of the MA market, according to a 2022 AMA report. In 91 percent of metros, one payer controls at least 30 percent of the market.

Humana offers MA plans in 89 percent of U.S. counties in 2023, and UnitedHealthcare offers plans in 84 percent.

Number of counties payers offering MA plans in 2023: *There are 3,143 counties

Counties with the most MA plans available: 1. Summit County, Ohio: 87 T-2. Cuyahoga County, Ohio: 84 T-2. Medina County, Ohio: 84 T-4: Lake County, Ohio: 83 T-4: Stark County, Ohio: 83

Alaska, Montana, South Dakota and Wyoming have the least 5-star MA plans available, with one in 2022. New York and Ohio have the most 5-star plans, with 12 available.

Controversy

To date, nearly every major insurer has been accused of or settled allegations of MA fraud from the federal government. Payers have been accused of exploiting the program through elaborate coding schemes that make patients appear sicker on medical records than they actually are — thereby leading to higher payments from CMS. Insurers dispute these claims. MA overpayments to payers are estimated to have cost as much as $25 billion in 2020. Physicians told The Washington Post in June that it is common practice for payers and health systems to “data mine” a patient’s medical history if that individual is covered by MA because the program pays a set amount based on patient risk.

Some experts have said the issue stems from the flexibility of interpretation around current MA risk adjustment coding guidelines — others expect there to be increased scrutiny of the program in 2023.

Recent policy moves

CMS issued a proposed rule Dec. 6 that would require electronic prior authorization processes among MA organizations.

CMS is cracking down on deceptive marketing practices and no longer allows MA or Part D prescription drug plans to advertise on television without agency approval as of Jan. 1. The agency said it issued the new policy after reviewing thousands of beneficiary complaints regarding confusing, misleading or inaccurate information from plans — plan sponsors are also responsible for all marketing activities from brokers and third-party agencies.

CMS issued a proposed rule Dec. 14 to continue its efforts to overhaul prior authorization and marketing practices around MA and Part D plans, along with adding health equity measures to star ratings and boosting behavioral health network adequacy requirements.

A CMS rule revising MA and Part D marketing and communication regulations went into effect June 28 to increase oversight over third-party marketing organizations.

Two nonprofit insurers, Long Beach, CA-based SCAN Group and Portland, OR-based CareOregon, have agreed to merge. The new organization—which will take the name HealthRight Group, while retaining the SCAN and CareOregon brands in local markets—will have $6.8B in annual revenue and cover around 800K lives.

Continuing their previous areas of focus, SCAN will cater primarily to Medicare Advantage (MA) beneficiaries, and CareOregon will prioritize serving managed Medicaid enrollees. Executives from both companies cited scale as the primary motivation for the merger, with the companies aiming to both strengthen their foothold in current markets and expand their reach into new ones.

The deal, which still needs approval from state regulators, is expected to close in 2023.

The Gist: HealthRight stands to be a strong player in the booming government-backed, managed care market in states currently dominated by large payers like Kaiser Permanente and UnitedHealthcare.

SCAN has differentiated itself with services dedicated to underserved populations, including creating a MA plan designed for LGBTQ+ seniors, and offering California’s only integrated dual-eligible, special needs plans. We expect the addition of CareOregon’s 319K managed Medicaid members to provide a larger platform for these targeted initiatives, and we wouldn’t be surprised to see more nonprofit insurers joining forces with HealthRight to better compete with current market heavyweights.

On Tuesday, the Centers for Medicare and Medicaid Services (CMS) announced a proposed rule that aims to streamline the prior authorization process by requiring certain payers to establish a method for electronic transmission, shorten response time for physician requests, and provide a reason for denials. This rule replaces one proposed in December 2020 that was never finalized.

In addition to applying to Medicaid and Affordable Care Act exchange plans, the new rule would also apply to Medicare Advantage plans, which the previous rule did not. If finalized, it will take effect in 2026.

The Gist: Managing prior authorization requests is one of providers’ greatest sources of frustration, with over 80 percent of physicians rating it as “very or extremely burdensome” in a recent Medical Group Management Association survey.

Not only would patients would benefit from faster turnarounds, but even major payers agree that the status quo is suboptimal, and payer advocacy organization AHIP has signaled support for transmitting prior authorization requests electronically.

The challenge for regulators will be to strike a balance that satisfies the competing interests of payers and providers—turnaround time is likely to be a sticking point—but the one good thing about a system that no one likes is that there’s plenty of room for improvement.

More and more employer and union-sponsored retiree health plans are offering Medicare-eligible coverage through Medicare Advantage (MA), a new analysis finds.

The analysis from the Kaiser Family Foundation, released Thursday, comes as MA is expected to surpass traditional Medicare in total enrollment for 2023 and more insurers enter the lucrative market. Employers and unions are turning to MA in a bid to control retiree healthcare costs.

“For some large employers, the shift to Medicare Advantage appears to be a strategy to maintain benefits for their retirees, without terminating coverage or adopting other changes that more directly shift costs onto retirees,” the analysis said. “However, the shift to Medicare Advantage has implications for retirees that extend beyond supplemental benefits.”

Kaiser relied on data from its 2022 employer health benefits survey of large private and nonfederal public employers. It showed that half of the large employers with 200 or more workers are offering health benefits to retirees through an MA contract, nearly double the 26% doing the same in 2017. Another 44% that offer MA coverage to retirees don’t give them another choice in coverage.

Among the companies with 2,000 or more employers, 60% offered benefits through an MA plan. The top reason such companies turn to MA is to combat higher costs, with 42% citing it as a reason compared with 14% for flexibility for enrollees.

Unlike traditional Medicare, MA relies on provider networks and cost management tools to cut down on costs. Kaiser warned that this shift toward MA has some unintended consequences for retirees.

“This approach has potential to restrict retirees’ access to doctors and hospitals, depending on the plan’s provider network, and subject retirees to cost management tools, such as prior authorization, that may limit access to Medicare-covered services,” the analysis said.

Kaiser cited a recent move by New York City to move its city worker retirees to an MA plan, a decision that is on hold after the insurers Elevance Health and Empire Blue Cross Blue Shield dropped out, according to a published report on The City news site.

The MA market has grown in popularity among seniors in recent years. The program has also received heightened scrutiny surrounding overpayments to plans based on inaccurate risk scores and aggressive marketing tactics by agents and brokers.

It’s open enrollment season again. From now through Dec. 7, about 65 million Americans are facing the annual question of which Medicare options will give them the best health coverage. An onslaught of television and radio ads, emailed promotions, texts and mailers serve as reminders, though not necessarily clarifying ones.

“It’s a very consequential decision, and the most important thing is to be informed,” said Jeannie Fuglesten Biniek, a senior policy analyst at the Kaiser Family Foundation and a co-author of a recent literature review comparing Medicare Advantage and traditional Medicare.

If you are navigating this decision for yourself or for a loved one, here are some of the important factors to consider.

Medicare — the federally funded health care program — has been in place since 1965. Since then, an expanding array of Medicare Advantage plans have become available. For 2023, the typical beneficiary can choose from 43 Advantage plans, the Kaiser Family Foundation has reported.

Medicare Advantage plans, like traditional Medicare, are funded by the federal government, but they are offered though private insurance companies, which receive a set payment for each enrollee. The idea is to help control costs by allowing these insurers, who must cover the same services as traditional Medicare, to keep some of the federal payment as profit if they can provide care less expensively.

The biggest providers of Advantage plans are Humana and United Healthcare, and they and others market aggressively to persuade seniors to sign up or switch plans. A new U.S. Senate report found that some of these Advantage plan practices are deceptive; for example, some marketing firms sent Medicare beneficiaries mailers made to look like government websites or letters. This has confused many seniors, and Medicare officials have promised to increased policing.

But the marketing has paid off for insurers. The proportion of eligible Medicare beneficiaries enrolled in Medicare Advantage plans has hit 48 percent. By next year, most beneficiaries will likely be Advantage enrollees.

The two plans operate quite differently, and the health and financial consequences can be dramatic. Each has, well, advantages — and disadvantages.

Jeannie Fuglesten Biniek, a senior policy analyst at the Kaiser Family Foundation, is a co-author of a recent literature review comparing Medicare Advantage and traditional Medicare. One important finding, Dr. Biniek said: “Both Medicare Advantage and traditional Medicare beneficiaries reported that they were satisfied with their care — a large majority in both groups.”

Advantage plans offer simplicity. “It’s one-stop shopping,” she added. “You get your drug plan included, and you don’t need a separate supplemental policy,” the kind that traditional Medicare beneficiaries often buy, frequently called Medigap policies.

Medicare Advantage may appear cheaper, because many plans charge low or no monthly premiums. Unlike traditional Medicare, Advantage plans also cap out-of-pocket expenses. Next year, you’ll pay no more than $8,300 in in-network expenses, excluding drugs — or $12,450 with the kind of plan that permits you to also use out-of-network providers at higher costs.

Only about one-third of Advantage plans (called P.P.O.s, or preferred provider organizations) allow that choice, however. “Most plans operate like an H.M.O. — you can only go to contracted providers,” said David Lipschutz, the associate director of the Center for Medicare Advocacy.

Advantage enrollees may also be drawn to the plan by benefits that traditional Medicare can’t offer. “Vision, dental and hearing are the most popular,” Mr. Lipschutz said, but plans may also include gym memberships or transportation.

“We caution people to look at what the scope of the benefits actually are,” he added. “They can be limited, or not available, to everyone in the plan. Dental care might cover one cleaning and that’s it, or it may be broader.” Most Advantage enrollees who use these benefits still wind up paying most dental, vision or hearing costs out of pocket.

One big downside is that these insurers require “prior authorization,” or approval in advance, for many procedures, drugs or facilities.

“Your doctor or the facility says that you need more care” — in a hospital or nursing home, say — “but the plan says, ‘No, five days, or a week, two weeks, is fine,’” said David Lipschutz, the associate director of the Center for Medicare Advocacy. Then you must either forgo care or pay out of pocket.

Advantage participants who are denied care can appeal, and those who do so see the denials reversed 75 percent of the time, according to a 2018 report by the Department of Health and Human Services’s Office of Inspector General. But only about 1 percent of beneficiaries or providers file appeals, “which means there’s a lot of necessary care that enrollees are going without,” Mr. Lipschutz said.

Another report this spring by the inspector general’s office determined that 13 percent of services denied by Advantage plans met Medicare coverage rules and would have been approved under traditional Medicare.

Advantage plans can also be problematic if you are traveling or spending part of each year away from home. If you live in Philadelphia but get sick on vacation in Florida, all local providers may be out of network. Check to see how the plan you’re using or considering treats such situations.

“The big pro is that there are no networks,” Jeannie Fuglesten Biniek, a senior policy analyst at the Kaiser Family Foundation, said of traditional Medicare. “You can see any doctor that accepts Medicare,” as most do, and use any hospital or clinic. Traditional Medicare beneficiaries also largely avoid the delays and frustrations of prior authorization.

But traditional Medicare sets no cap on out-of-pocket expenses, and its 20 percent co-pay can add up quickly for hospitalizations or expensive tests and procedures. So most beneficiaries rely on supplemental insurance to cover those costs; either they buy a Medigap policy or they have supplementary coverage through an employer or Medicaid. Medigap policies are not inexpensive; a Kaiser Family Foundation survey found that they average $150 to $200 a month.

The Kaiser literature review found that traditional Medicare beneficiaries experienced fewer cost problems than Advantage beneficiaries if they had supplementary Medigap policies — but if they didn’t, they were more likely to report problems like delaying care for cost reasons or having trouble paying medical bills.

Traditional Medicare also provides somewhat better access to high-quality hospitals and nursing homes. David Meyers, a health services researcher at Brown University, and his colleagues have been tracking differences between original Medicare and Medicare Advantage for years, using data from millions of people.

In general, patients with high needs — people who were frail, limited in activities of daily living or had chronic conditions — were more apt to switch to traditional Medicare than those who were not high-need.

“When you’re healthier, you may run into fewer of the limitations of networks and prior authorization,” Dr. Meyers said. “When you have more complex needs, you come up against those more frequently.”

Another downside to traditional Medicare, though, is that it does not include drug coverage. For that, you need to buy a separate Part D plan.

Unlike most Medicare Advantage plans, traditional Medicare does not include drug coverage. For that, you must buy a separate Part D plan.

For 2023, beneficiaries can typically choose between 24 stand-alone Part D plans, at premiums that range from $6 to $111 a month and average $43 for policies available nationwide, said Juliette Cubanski, the deputy director of the program on Medicare policy at the Kaiser Family Foundation.

“If you’re the person who doesn’t take many medications or only uses generics, the best strategy might be to sign up for the plan with the lowest premium,” Dr. Cubanski said. “But if you take a lot of medications, the most important thing is whether the drugs you take, especially the most expensive ones, are covered by the plan.”

Different plans cover different drugs (which can change from year to year) and place them in different pricing tiers, so how much you pay for them varies. And, to make comparisons more dizzying, certain pharmacy chains are “preferred” by certain plans, so you could pay more at CVS than at Walmart for the same drug, or vice versa.

How does Part D work? First, most stand-alone plans have a deductible: $505 in 2023. You pay that amount out of pocket before coverage kicks in.

Then, a Part D plan, either stand-alone or as part of a Medicare Advantage plan, usually establishes five tiers for drugs. The cheapest two tiers, for generic drugs, could be free or run up to about $20 per prescription. Next comes a tier for preferred brand-name drugs, probably $30 to $45 per prescription in 2023.

Drugs on the next highest tier, for nonpreferred brand-name drugs, usually involve coinsurance — paying a percentage of the drug’s list price — rather than a flat co-pay. For national stand-alone plans, that ranges from 34 to 50 percent, Dr. Cubanski said.

Drugs that cost more than $830 a month are considered specialty drugs, the highest-priced tier. You only pay 25 percent of the price, but because these are so expensive, your costs rise.

Once your total drug costs reach $4,660 (for 2023), including out of pocket costs and what your plan paid, you have entered the so-called coverage gap phase and will pay 25 percent of the cost, regardless of tier.

Finally, when your costs reach $7,400 — including what you’ve paid, plus the value of manufacturer discounts — you have hit the threshold for catastrophic coverage. After that, you pay just 5 percent.

Switching between Medicare Advantage plans is fairly easy. But switching from traditional Medicare to an Advantage plan can cause a major problem: You relinquish your Medigap policy, if you had one. Then, if you later grow dissatisfied and want to switch back from Advantage to traditional Medicare, you may not be able to replace that policy. Medigap insurers can deny your application or charge high prices based on factors like pre-existing conditions.

(There are some exceptions. For instance, people who drop a Medigap policy to enroll in an Advantage plan for the first time can repurchase it, or buy another Medigap policy, if they switch back to traditional Medicare within a year.)

“Many people think they can try out Medicare Advantage for a while, but it’s not a two-way street,” said David Lipschutz, the associate director of the Center for Medicare Advocacy. Except in four states that guarantee Medigap coverage at set prices — New York, Massachusetts, Connecticut and Maine — “it’s one type of insurance that can discriminate against you based on your health,” he said.

In 2020, only 3 in 10 Medicare beneficiaries compared their current plans with others, a recent Kaiser Family Foundation survey reported. Even fewer beneficiaries changed plans, which might reflect consumer satisfaction — or the daunting task of trying to evaluate the pluses and minuses.

You will find plenty of information on the Medicare.gov website, including the Part D plan finder, where you can input the drugs you take and see which plan gives you the best and most economical coverage. The toll-free 1-800-MEDICARE number can also assist you.

Perhaps the best resources, however, are the federally funded State Health Insurance Assistance Programs, where trained volunteers can help consumers assess both Medicare and drug plans.

These programs “are unbiased and don’t have a pecuniary interest in your decision making,” said David Lipschutz, the associate director of the Center for Medicare Advocacy. But their appointments tend to fill up quickly at this time of year, and the annual open enrollment period ends on Dec. 7. Don’t delay.

Driven in large part by the growth of Medicare Advantage, a number of startups are vying to create the next value-based care model for senior care in patients’ homes, Axios’ Sarah Pringle reports.

Why it matters: As we recently reported in our Elder Care Crisis Deep Dive, there is a shortfall of enough cash and caregivers to handle the massive amount of aging baby boomers reaching their senior years.

“The cool thing about value-based care?” General Atlantic managing director Robb Vorhoff said. “There’s hundreds of business models.”

Reality check: Scaling remains a challenge for new models looking to shake up the senior care market.

“There are a lot of options out there that you don’t know about,” Town Hall Venture’s Andy Slavitt says. “Some are the best-kept secrets; some are not worth knowing about.”

Be smart: While most elderly adults would prefer to age in place, there is still a need for institutional care settings like nursing homes, which presents its own major challenges, Sarah writes.

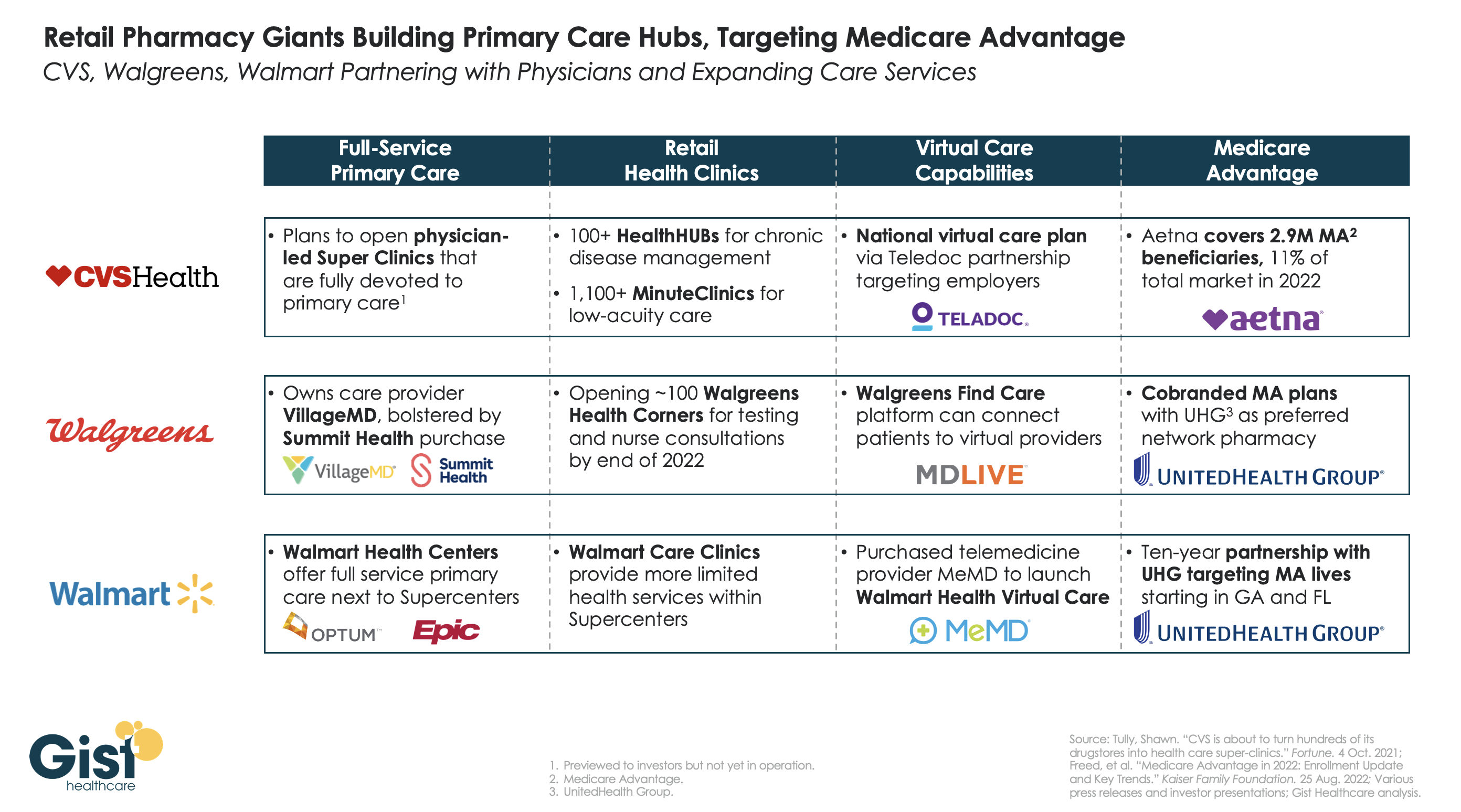

Retailers and insurers are building out their primary care strategies in a bid to become the new front door for patients seeking healthcare services, especially seniors on highly profitable Medicare Advantage (MA) plans. In the graphic above, we examine the capabilities of three of the largest pharmacy chains—CVS Health, Walgreens, and Walmart—to deliver full-service primary care across in-person and virtual settings.

CVS pioneered the pivot to care provision in 2006 with its acquisition of MinuteClinic, which now has over 1,000 locations. The company has further expanded its concept of pairing retail and pharmacy services with primary care by opening over 100 HealthHUBs, which provide an expanded slate of care services. However, CVS lags competitors in the rollout of full-service primary care practices, with its proposed physician-led Super Clinics still stuck in the planning stages.

Walgreens, with its majority stake in VillageMD (on track for 200 co-branded practices by the end of the year) and the recent acquisition of Summit Health (which operates another 370 primary and urgent care clinics) has assembled the most impressive primary care footprint of the three companies.

Walmart, the largest by number of stores but also the newest to healthcare, has opened more than 25 Walmart Health Centers, a step up from earlier experimentation with in-store care clinics, offering more services and partnering with Epic Systems to integrate electronic health records.

CVS’s key advantage over its competitors comes from its payer business, having acquired Aetna in 2018, now the fourth-largest MA payer by membership. Walgreens and Walmart have both aligned themselves with UnitedHealth Group (UHG) to participate in MA, with Walmart having struck a ten-year partnership to steer UHG MA beneficiaries to Walmart Health Centers in Florida and Georgia.

While aligning with UHG expands the reach of these retail giants into MA risk, UHG, whose OptumHealth division is by far the largest employer of physicians nationwide, remains the healthcare juggernaut most poised to unseat incumbent providers as the home for consumers’ healthcare needs.

In their latest article scrutinizing the MA program, New York Times reporters Reed Abelson and Margot Sanger-Katz highlight MA marketing practices brought to light in a recent report from the Senate Finance Committee. Complaints to the Centers for Medicare and Medicaid Services (CMS) about MA marketing more than doubled from 2020 to 2021, as agents and brokers took advantage of oversight rules relaxed during the Trump administration. Some of the most egregious alleged abuses include agents switching seniors into new plans without their consent and exploiting individuals with cognitive impairments.

The Gist: Media interest is finally catching up to the building legislative and regulatory pressure on Medicare Advantage. While earlier reporting has highlighted how plans can inflate payments from Medicare, this new story shows how the process of selecting a plan can be fraught for the seniors enrolled.

Plan design is confusing even for industry insiders, so it is no surprise that seniors might find themselves ‘choosing’ plans that omit key providers, or even drug coverage they already rely on, particularly after being badgered or misled by agents and brokers.

Many of the regulatory fixes highlighted in the report can be implemented directly by CMS, but insurers, who remember the managed care backlash of the 90s, shouldn’t wait to tighten the reins on questionable marketing practices, lest they risk losing public support for one of their most lucrative business lines.