UnitedHealth executives made a valiant attempt yesterday to persuade investors that they have figured out how to improve customer service and keep Congress and the incoming Trump administration from passing laws that could shrink the company’s profit margins – and maybe even the company itself – but Wall Street wasn’t buying.

During their first call with investors since the murder of UnitedHealthcare CEO Brian Thompson, the company’s top brass pointed the finger of blame for rising health care costs everywhere but at themselves – primarily at hospitals and pharmaceutical companies – and made statements that simply were not true. Investors clearly did not find their comments reassuring or credible. By the end of the day shares of UnitedHealth’s stock were down more than 6% to $510.59. That marked a continuation of a slide that began after the stock price peaked at $630.73 on November 11 – a decline of almost 20%.

In a little more than two months, the company has lost an astonishing $110 billion in market capitalization, and shareholders have lost an enormous amount of the money they invested in UnitedHealth.

Earlier yesterday morning, the company released fourth-quarter and full-year 2024 earnings, which were slightly higher on a per share basis than Wall Street financial analysts had expected: $6.81 per share in the fourth quarter compared to analysts’ consensus estimate of $6.73 for the quarter. But the company posted lower revenue during the last three months of 2024 than analysts had expected. While revenue was up 7% over the same quarter in 2023, to $100.8 billion, analysts had expected revenue to grow to $101.6 billion.

And on a full-year basis, the company’s net profits fell an eye-popping 36%, from $22.4 billion in 2023 to $14.4 billion last year.

Bottom line: the company, which until last year had grown rapidly, actually shrank in some respects, especially in the division that operates the company’s health plans. UnitedHealthcare, which Thompson led, saw its revenue increase slightly but its profits fall. The other big division, Optum, which among other things owns and operates numerous physician practices and clinics and one of the country’s largest pharmacy benefit managers (PBMs), fared much better.

While Optum’s 2024 revenue was lower than UnitedHealthcare’s ($253 billion and $298 respectively), it made far more in profits on an operating basis ($16.7 billion and $15.6 respectively).

Optum’s operating profit margin was 6.6% while UnitedHealthcare’s was 5.2%.

The company’s executives blamed higher health care utilization, especially by people enrolled in its Medicare Advantage plans, for the decline in profits.

Witty and CFO John Rex pointed the finger of blame at hospitals and drug companies for rising medical prices. And they obscured the huge amounts of money the company’s PBM, Optum Rx, extracts from the pharmacy supply chain. While the company chose not to break out exactly how much of Optum’s revenues of $298 billion came from Optum Rx, it appears that more than half of it was contributed by the PBM. The company did note that Optum Rx revenues increased 15% during 2024.

Nevertheless, Witty and Rex blamed drug makers for high prices.

They also said that they would be changing the PBM’s business practices to pass through rebate discounts from drug makers to its customers, claiming that it already passes through 98% of them and will reach 100% by 2028. That clearly was a talking point aimed at Washington, where there is significant bipartisan support for legislation that would require all PBMs to do so. Despite UnitedHealth’s claim, there is no external verification to back up that they are passing 98% of rebates back to customers.

Another claim the executives made that is not true is that the Medicare Advantage program saves taxpayers money. Numerous government reports have shown the opposite, that the federal government spends considerably more on people enrolled in Medicare Advantage plans than those enrolled in the traditional Medicare program.

Reports have estimated that UnitedHealthcare, which is the largest Medicare Advantage company, and other MA plans are overpaid between $80 billion and $140 billion a year.

There is also growing bipartisan support to reform the Medicare Advantage program to reduce both the overpayments and the excessive denials of care at UnitedHealthcare and other MA insurers.

While company executives might be hoping that their fortunes will improve during the second Trump administration, Trump recently joined some Republican members of Congress, like Rep. Buddy Carter of Georgia, who are calling for significant reforms, especially to pharmacy benefit managers.

At a news conference last month, Trump promised to “knock out” those middlemen in the pharmacy supply chain.

“We are paying far too much, because we are paying far more than other countries,” he said. “We have laws that make it impossible to reduce [drug costs] and we have a thing called a ‘middleman’ … that makes more money than the drug companies, and they don’t do anything except they’re middlemen. We are going to knock out the middleman.”

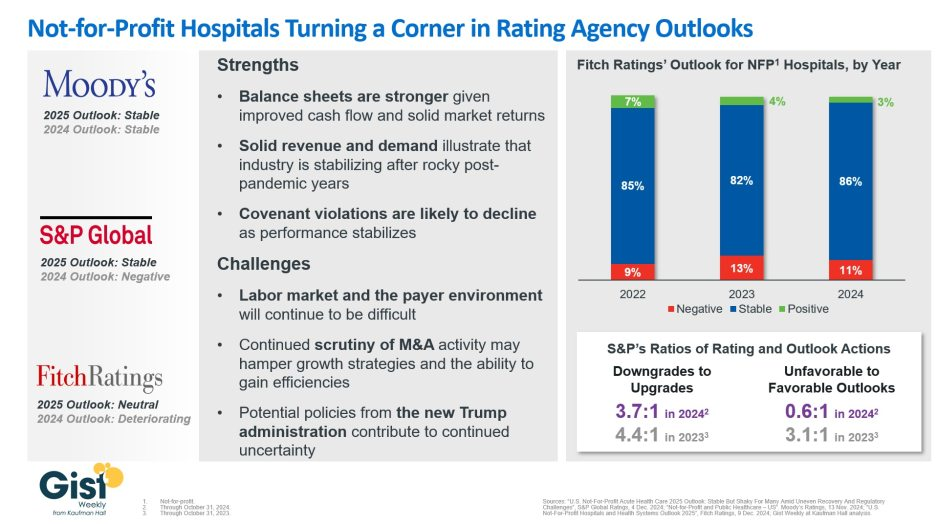

In late 2023, S&P Global and Fitch Ratings viewed the not-for-profit (NFP) hospital sector as negative or deteriorating, reflecting the difficult financial position many were in following the pandemic.

In recent weeks, S&P and Fitch upgraded their 2025 sector outlook for NFP hospitals to stable and neutral respectively, joining Moody’s Ratings, which held stable from last year.

This week’s graphic illustrates the rating agencies’ latest views on NFP hospitals, which point to a promising but uneven recovery for the industry.

Overall, the reports detail that stronger balance sheets, solid revenues, and improved demand have reduced the likelihood of covenant violations and strengthened NFP hospitals’ positions.

However, challenges persist that could impede further progress. The labor market, payer environment, antitrust enforcement, and a new administration all present complications for the continued recovery of NFP hospitals. Nonetheless, the reports indicate significant improvement for the industry since the post-pandemic ratings downturn.

Fitch’s report noted that the share of NFP hospitals with a stable outlook has reached a three-year high. Meanwhile, S&P reported that there are now almost twice as many NFP hospitals with favorable outlooks compared to unfavorable ones, a dramatic flip from 2023, which had a 3.1:1 ratio of unfavorable to favorable outlooks.

These ratings changes reflect the hard work put in by NFP hospitals across the country to improve their financial performance and find new ways to serve their communities sustainably.

However, the recovery remains “shaky” and incomplete, and hospitals still face a long road ahead as they reconfigure to a new normal.

The Affordable Care Act turned 14 on March 23. It has done a lot of good for a lot of people, but big changes in the law are urgently needed to address some very big misses and consequences I don’t believe most proponents of the law intended or expected.

At the top of the list of needed reforms: restraining the power and influence of the rapidly growing corporations that are siphoning more and more money from federal and state governments – and our personal bank accounts – to enrich their executives and shareholders.

I was among many advocates who supported the ACA’s passage, despite the law’s ultimate shortcomings. It broadened access to health insurance, both through government subsidies to help people pay their premiums and by banning prevalent industry practices that had made it impossible for millions of American families to buy coverage at any price. It’s important to remember that before the ACA, insurers routinely refused to sell policies to a third or more applicants because of a long list of “preexisting conditions” – from acne and heart disease to simply being overweight – and frequently rescinded coverage when policyholders were diagnosed with cancer and other diseases.

While insurance company executives were publicly critical of the law, they quickly took advantage of loopholes (many of which their lobbyists created) that would allow them to reap windfall profits in the years ahead – and they have, as you’ll see below.

I wrote and spoke frequently as an industry whistleblower about what I thought Congress should know and do, perhaps most memorably in an interview with Bill Moyers. During my Congressional testimony in the months leading up to the final passage of the bill in 2010, I told lawmakers that if they passed it without a public option and acquiesced to industry demands, they might as well call it “The Health Insurance Industry Profit Protection and Enhancement Act.”

A health plan similar to Medicare that could have been a more affordable option for many of us almost happened, but at the last minute, the Senate was forced to strip the public option out of the bill at the insistence of Sen. Joe Lieberman (I-Connecticut), who died on March 27, 2024. The Senate did not have a single vote to spare as the final debate on the bill was approaching, and insurance industry lobbyists knew they could kill the public option if they could get just one of the bill’s supporters to oppose it. So they turned to Lieberman, a former Democrat who was Vice President Al Gore’s running mate in 2000 and who continued to caucus with Democrats. It worked. Lieberman wouldn’t even allow a vote on the bill if it created a public option. Among Lieberman’s constituents and campaign funders were insurance company executives who lived in or around Hartford, the insurance capital of the world. Lieberman would go on to be the founding chair of a political group called No Labels, which is trying to find someone to run as a third-party presidential candidate this year.

The work of Big Insurance and its army of lobbyists paid off as insurers had hoped. The demise of the public option was a driving force behind the record profits – and CEO pay – that we see in the industry today.

The good effects of the ACA:

Nearly 49 million U.S. residents (or 16%) were uninsured in 2010. The law has helped bring that down to 25.4 million, or 8.3% (although a large and growing number of Americans are now “functionally uninsured” because of unaffordable out-of-pocket requirements, which President Biden pledged to address in his recent State of the Union speech).

The ACA also made it illegal for insurers to refuse to sell coverage to people with preexisting conditions, which even included birth defects, or charge anyone more for their coverage based on their health status; it expanded Medicaid(in all but 10 states that still refuse to cover more low-income individuals and families); it allowed young people to stay on their families’ policies until they turn 26; and it required insurers to spend at least 80% of our premiums on the health care goods and services our doctors say we need (a well-intended provision of the law that insurers have figured out how to game).

The not-so-good effects of the ACA:

As taxpayers and health care consumers, we have paid a high price in many ways as health insurance companies have transformed themselves into massive money-making machines with tentacles reaching deep into health care delivery and taxpayers’ pockets.

To make policies affordable in the individual market, for example, the government agreed to subsidize premiums for the vast majority of people seeking coverage there, meaning billions of new dollars started flowing to private insurance companies. (It also allowed insurers to charge older Americans three times as much as they charge younger people for the same coverage.) Even more tax dollars have been sent to insurers as part of the Medicaid expansion. That’s because private insurers over the years have persuaded most states to turn their Medicaid programs over to them to administer.

We invite you to take a look at how the ascendency of health insurers over the past several years has made a few shareholders and executives much richer while the rest of us struggle despite – and in some cases because of – the Affordable Care Act.

BY THE NUMBERS

In 2010, we as a nation spent $2.6 trillion on health care. This year we will spend almost twice as much – an estimated $4.9 trillion, much of it out of our own pockets even with insurance.

In 2010, the average cost of a family health insurance policy through an employer was $13,710. Last year, the average was nearly $24,000, a 75% increase.

The ACA, to its credit, set an annual maximum on how much those of us with insurance have to pay before our coverage kicks in, but, at the insurance industry’s insistence, it goes up every year. When that limit went into effect in 2014, it was $12,700 for a family. This year, it has increased by 48%, to $18,900. That means insurers can get away with paying fewer claims than they once did, and many families have to empty their bank accounts when a family member gets sick or injured. Most people don’t reach that limit, but even a few hundred dollars is more than many families have on hand to cover deductibles and other out-of-pocket requirements. Now 100 million Americans – nearly one of every three of us – are mired in medical debt, even though almost 92% of us are presumably “covered.” The coverage just isn’t as adequate as it used to be or needs to be.

Meanwhile, insurance companies had a gangbuster 2023. The seven big for-profit U.S. health insurers’ revenues reached $1.39 trillion, and profits totaled a whopping $70.7 billion last year.

SWEEPING CHANGE, CONSOLIDATION–AND HUGE PROFITS FOR INVESTORS

Insurance company shareholders and executives have become much wealthier as the stock prices of the seven big for-profit corporations that control the health insurance market have skyrocketed.

NOTE: The Dow Jones Industrial Average is listed on this chart as a reference because it is a leading stock market index that tracks 30 of the largest publicly traded companies in the United States.

REVENUES collected by those seven companies have more than tripled (up 346%), increasing by more than $1 trillion in just the past ten years.

PROFITS (earnings from operations) have more than doubled (up 211%), increasing by more than $48 billion.

The CEOs of these companies are among the highest paid in the country. In 2022, the most recent year the companies have reported executive compensation, they collectively made $136.5 million.

U.S. HEALTH PLAN ENROLLMENT

Enrollment in the companies’ health plans is a mix of “commercial” policies they sell to individuals and families and that they manage for “plan sponsors” – primarily employers and unions – and government/enrollee-financed plans (Medicare, Medicaid, Tricare for military personnel and their dependents and the Federal Employee Health Benefits program).

Enrollment in their commercial plans grew by just 7.65% over the 10 years and declined significantly at UnitedHealth, CVS/Aetna and Humana. Centene and Molina picked up commercial enrollees through their participation in several ACA (Obamacare) markets in which most enrollees qualify for federal premium subsidies paid directly to insurers.

While not growing substantially, commercial plans remain very profitable because insurers charge considerably more in premiums now than a decade ago.

(1) The 2013 total for CVS/Aetna was reported by Aetna before its 2018 acquisition by CVS. (2) Humana announced last year it is exiting the commercial health insurance business. (3) Enrollment in the ACA’s marketplace plans account for all of Molina’s commercial business.

By contrast, enrollment in the government-financed Medicaid and Medicare Advantage programs has increased 197% and 167%, respectively, over the past 10 years.

(1) The 2013 total for CVS/Aetna was reported by Aetna before its 2018 acquisition by CVS.

Of the 65.9 million people eligible for Medicare at the beginning of 2024, 33 million, slightly more than half, enrolled in a private Medicare Advantage plan operated by either a nonprofit or for-profit health insurer, but, increasingly, three of the big for-profits grabbed most new enrollees.

Of the 1.7 million new Medicare Advantage enrollees this year, 86% were captured by UnitedHealth, Humana and Aetna.

Those three companies are the leaders in the Medicare Advantage business among the for-profit companies, and, according to the health care consulting firm Chartis, are taking over the program “at breakneck speed.”

(1) The 2013 total for CVS/Aetna was reported by Aetna before its 2018 acquisition by CVS. (2,3) Centene’s and Molina’s totals include Medicare Supplement; they do not break out enrollment in the two Medicare categories separately.

It is worth noting that although four companies saw growth in their Medicare Supplement enrollment over the decade, enrollment in Medicare Supplement policies has been declining in more recent years as insurers have attracted more seniors and disabled people into their Medicare Advantage plans.

OTHER FEDERAL PROGRAMS

In addition to the above categories, Humana and Centene have significant enrollment in Tricare, the government-financed program for the military. Humana reported 6 million military enrollees in 2023, up from 3.1 million in 2013. Centene reported 2.8 million in 2023. It did not report any military enrollment in 2013.

Elevance reported having 1.6 million enrollees in the Federal Employees Health Benefits Program in 2023, up from 1.5 million in 2013. That total is included in the commercial enrollment category above.

At Cigna, Express Scripts’ pharmacy operations now contribute more than 70% to the company’s total revenues. Caremark’s pharmacy operations contribute 33% to CVS/Aetna’s total revenues, and Optum Rx contributes 31% to UnitedHealth’s total revenues.

WHAT TO DO AND WHERE TO START

The official name of the ACA is the Patient Protection and Affordable Care Act. The law did indeed implement many important patient protections, and it made coverage more affordable for many Americans.

But there is much more Congress and regulators must do to close the loopholes and dismantle the barriers erected by big insurers that enable them to pad their bottom lines and reward shareholders while making health care increasingly unaffordable and inaccessible for many of us.

Several bipartisan bills have been introduced in Congress to change how big insurers do business. They include curbing insurers’ use of prior authorization, which often leads to denials and delays of care; requiring PBMs to be more “transparent” in how they do business and banning practices many PBMs use to boost profits, including spread pricing, which contributes to windfall profits; and overhauling the Medicare Advantage program by instituting a broad array of consumer and patient protections and eliminating the massive overpayments to insurers.

And as noted above, President Biden has asked Congress to broaden the recently enacted $2,000-a-year cap on prescription drugs to apply to people with private insurance, not just Medicare beneficiaries. That one policy change could save an untold number of lives and help keep millions of families out of medical debt. (A coalition of more than 70 organizations and businesses, which I lead, supports that, although we’re also calling on Congress to reduce the current overall annual out-of-pocket maximum to no more than $5,000.)

I encourage you to tell your members of Congress and the Biden administration that you support these reforms as well as improving, strengthening and expanding traditional Medicare. You can be certain the insurance industry and its allies are trying to keep any reforms that might shrink profit margins from becoming law.

On the one hand, the alternative to traditional Medicare is still popular among consumers, who have been lured by the promises of lower out-of-pocket costs and increased supplemental benefits.

On the other hand,Medicare Advantage profitability is on the decline, as shown in recent quarterly reports from the large insurers. The headwinds, executives said during recent earnings calls, have been due to greater than expected utilization of benefits and lower than expected reimbursement from the government.

Adding to MA’s margin challenges are providers who are making the decision to cut their ties with MA plans rather than deal with delays in prior authorization and claims payments.

Moody’s Investors Service said this year, and an HFMAsurvey from March indicates 19% of health systems have discontinued at least one Medicare Advantage plan, while 61% are planning to or considering dropping Medicare Advantage payers.

Until recently, the story of Medicare Advantage was one of ascendancy. Just last year it hit a milestone: More than half of eligible Medicare beneficiaries are now in MA plans. So why is business taking a step back?

WHY THIS MATTERS

There are many factors at play, but a big one is the 3.7% rate increase for 2025 that Medicare Advantage plans will receive from the Centers for Medicare and Medicaid Services. The federal government is projected to pay between $500 and $600 billion in Medicare Advantage payments to private health plans, according to the 2025 Advance Notice for the Medicare Advantage and Medicare Part D Prescription Drug Programs released in April.

The payment rate was considered inadequate by insurers, who were also troubled over other key factors, including a 0.16% reduction in the Medicare Advantage benchmark rate for 2025, which represents a 0.2% decrease.

“AHIP has strong concerns that the estimated growth rate in the Advance Notice – an average of 2.44% – will lead to benchmark changes that are insufficient to cover the cost of caring for 33 million MA beneficiaries in 2025,” AHIP president and CEO Mike Tuffin said in April. “The estimate does not reflect higher utilization and cost trends in the healthcare market that are expected to continue into 2025.”

According to Karen Iapoce, vice president Government Programs at ZeOmega, the cost of running an MA business is increasing due to the burdens being placed on health plans.

“If you sit inside with a health plan, they’re asked to do a lot with not as much bandwidth as they had before,” said Iapoce. “For example, health equity requires plans to have new regulatory guidance they need to meet. There’s a host of measures around health equity. Our plans are not in the business of really understanding how to manage transportation, how to manage housing, so they’re working with other entities. This requires an expert to sit in with the health plan … and then track and report. On the business end, they want to show an ROI, but that could be six months or a year down the line.”

Because of that, she said, the benchmark rate is likely insufficient to cover the projected increase in administrative and other costs. Iapoce said the benchmark rates represent the maximum amount that will be paid to a person in a given county; this is used as a reference point for calculation. If a plan is higher than the benchmarks, the premiums end up going to the beneficiary. More commonly, the plans bid below the benchmark, and the difference represents the rebate plans will receive. But they also factor into risk adjustment.

“The plans are getting into these contract negotiations, so they have to know what goes into that benchmark,” said Iapoce. “I might not be a high utilizer, but you may be. If we’re bringing in a community of high utilizers, there’s no one offsetting that. There’s no balance.”

Richard Gundling, senior vice president, content and professional practice guidance at HFMA, said MA plans started running into these issues when the program crossed over the threshold of more than 50% of beneficiaries.

“When a Medicare Advantage plan comes in, then all the extra administrative burdens come into play,” said Gundling. “So you have prior authorizations, all the issues around lack of payment and denials. Patients get caught in the middle, and in particular elderly patients think they’re still on traditional Medicare.

“It used to be that healthier beneficiaries went into Medicare Advantage,” he added. “Sicker beneficiaries tended to stay in traditional Medicare. That’s not the case anymore, and so there’s a higher spend.”

Gundling said beneficiaries are likely flocking to MA with visions of lower costs and increased benefits such as eyeglasses and hearing aids, and many don’t realize the tradeoffs, such as prior authorizations and network restrictions.

MA remains popular with seniors, but studies show the plans cost the government more money than original Medicare.

A 2023 Milliman report showed annual estimated healthcare costs per beneficiary are $3,138, compared to $5,000 for traditional fee-for-service Medicare, and over $5,700 if a traditional Medicare beneficiary also buys a Medigap plan.

MA membership has grown nationally at an annual rate of 8% to approximately 32 million, while traditional Medicare has declined at an average annual rate of 1%. As that has happened the percentage of people choosing MA has grown to 49% from 28%, data shows.

Yet Medicare Advantage profitability is on the decline, Moody’s found in February. That’s largely because of a significant spike in utilization for most of the companies, which Moody’s expects will result in lower full-year MA earnings for insurers. Adding to that is lower reimbursement rates for the first time in years that are likely to remain weaker in 2025 and 2026, which is credit negative.

Moody’s analysts contend that MA may have “lost its luster,” citing as evidence Cigna’s efforts to sell its MA business, even after a failed merger with Humana.Cigna this past winter announced it had entered into a definitive agreement to sell its Medicare Advantage, Supplemental Benefits, Medicare Part D and CareAllies businesses to Health Care Service Corporation (HCSC) for about $3.7 billion.

Iapoce said Medicare Advantage may be a victim of its own success.

“Because of all this great promotion about what a Medicare Advantage plan can do for you, you’re seeing an increase in enrollment, or more people moving over, and the demographics are starting to change,” she said.

For many consumers, the appeal of an MA plan is the same as that of an online retailer like Amazon, said Iapoce. Such retailers offer one-stop shopping for a variety of goods, and the perception is that MA essentially offers one-stop shopping for a variety of healthcare services and benefits.

But while this massive shift is happening, it puts providers in an awkward position, said Iapoce.

“Their reimbursement is almost being dictated, in essence, by a health plan,” she said. “It almost feels like the payer has the upper hand over the provider. Think: I’m a provider. It’s my job to get this female with this particular age and condition a mammogram, and the health plan has told me to get her a mammogram. But you, as the health plan, get the money for it. I, as the provider … what am I getting? What’s it doing for me? It becomes this very tense situation, and the provider is probably the entity that is running on the thinnest of staff.”

Gundling expects that despite some “growing pains,” MA will remain viable and continue to grow.

“Nobody’s going to stay still,” said Gundling. CMS has to consider, ‘Are we paying the health plans appropriately for the types of patients they have?’ And then health plans will need to look at their medical utilization rules – ‘Are we overdoing pre-authorization or denying things appropriately?’ And providers need to say, ‘This is a market we need to continue to grow.’

“There’s still going to be a role for it,” he said. “It’s just that we’ve introduced a larger population into it, and I think that’s where a lot of the surprises come in.”

THE LARGER TREND

CVS reportedearlier this month that healthcare-benefits medical costs, primarily due to higher-than-expected Medicare Advantage utilization, came in approximately $900 million above expectations.

Last month, Humana said it expected membership may take a hit from future Medicare Advantage pricing resulting from the CMS payment rate notice. Humana is actively evaluating plan level pricing decisions and the expected impact to membership, president and COO James Rechtin said on the call.

Elevance Health, formerly Anthem, reported a 12.2% earnings increase for Q1, but company margins have not been as affected as those insurers that are heavily invested in the MA market. Fewer of its members are in MA plans compared to other large insurers Humana, CVS Health or UnitedHealth Group, executives said.

Speaking of Andrew Witty, the UnitedHealth chief spurred a freakout last week on Wall Street after he said the company was beginning to see a “disturbance” in its Medicaid medical costs. More people on Medicaid are going to the doctor and hospital, which eats into the insurance company’s profits.

The biggest insurers that run state Medicaid programs — UnitedHealth, Elevance Health, Centene, and Molina Healthcare — all saw their stocks take a dive after Witty’s disclosure. For the past year, the surge in medical services has mostly been confined to older adults in Medicare Advantage plans.

Wall Street largely did not account for that trend creeping into Medicaid, which covers low-income people.

This switch is largely a function of the government’s Medicaid “redeterminations” process, Centene CEO Sarah London said at a banking conference Friday. During the pandemic, states didn’t have to kick people off Medicaid if they no longer were eligible. But over the past year, states had to redetermine if someone still qualified for coverage, and to boot those that no longer did. As fewer people remain enrolled in Medicaid, the ones who have stayed are sicker and are getting more care.

Looking ahead, London told investors not to worry. That’s because Centene and other insurers will get more money from state Medicaid programs (translation: taxpayers) over the next several months, through routine payment updates, to match how sick its enrollees are. The explanation worked: The stocks of all the Medicaid insurers rose on Friday.

“We know how to do this,” London said. “This dynamic of redeterminations is unprecedented right now because of the scale. But matching rates to acuity in Medicaid is normal course.”

I wrote Monday about how the additional Medicare claims CVS/Aetna paid during the first three months of this year prompted a massive selloff of the company’s shares, sending the stock price to a 15-year low.

During CVS’s May 1 call with investors, CEO Karen Lynch and CFO Thomas Cowhey assured them the company had already begun taking action to avoid paying more for care in the future than Wall Street found acceptable.

Among the solutions they mentioned:

Ratcheting up the process called prior authorization that results in delays and denials of coverage requests from physicians and hospitals; kicking doctors and hospitals out of its provider networks; hiking premiums; slashing benefits; and abandoning neighborhoods where the company can’t make as much money as investors demand.

On Tuesday at the Bank of America Securities Healthcare Conference, Cowhey doubled down on that commitment to shareholders and provided a little more color about what those actions would look like and how many human beings would be affected. As Modern Healthcare reported:

Headed into next year, Aetna may adjust benefits, tighten its prior authorization policies, reassess its provider networks and exit markets, CVS Chief Financial Officer Tom Cowhey told investors. It will also reevaluate vision, dental, flexible spending cards, fitness and transportation benefits, he said. Aetna is also working with its employer Medicare Advantage customers on how to appropriately price their business, he said.

Could we lose up to 10% of our existing Medicare members next year? That’s entirely possible, and that’s OK because we need to get this business back on track,” Cowhey said.

Insurers use the word “members” to refer to people enrolled in their health plans. You can apply for “membership” and pay your dues (premiums), but insurers ultimately decide whether you can stay in their clubs. If they think you’re making too many trips to the club’s buffet or selecting the most expensive items, your membership can–and will–be revoked.

That mention of “employer Medicare Advantage customers” stood out to me and should be of concern to people like New York Mayor Eric Adams, who was sold on the promise that the city could save millions by forcing municipal retirees out of traditional Medicare and into an Aetna Medicare Advantage plan. A significant percentage of Aetna’s Medicare Advantage “membership” includes people who retired from employers that cut a deal with Aetna and other insurers to provide retirees with access to care. Despite ongoing protests from thousands of city retirees, Adams has pressed ahead with the forced migration of retirees to Aetna’s club. He and the city’s taxpayers will find out soon that Aetna will insist on renegotiating the deal.

Back to that 10%. Aetna now has about 4.2 million Medicare Advantage “members,” but it has decided that around 420,000 of those human beings must be cut loose. Keep in mind that those humans are not among the most Internet-savvy and knowledgeable of the bewildering world of health insurance. Many of them have physical and mental impairments. They will be cast to the other wolves in the Medicare Advantage business.

Welcome to a world in which Wall Street increasingly calls the shots and decides which health insurance clubs you can apply to and whether those clubs will allow you to get the tests, treatments and medications you need to see another sunrise.

As Modern Healthcare noted, Aetna is not alone in tightening the screws on its Medicare Advantage members and setting many of them adrift. Humana, which has also greatly disappointed Wall Street because of higher-than-expected health care “utilization,” told investors it would be taking the same actions as Aetna.

But Aetna in particular has a history of ruthlessly cutting ties with humans who become a drain on profits. As I wrote in Deadly Spin in 2010:

Aetna was so aggressive in getting rid of accounts it no longer wanted after a string of acquisitions in the 1990s that it shed 8 million (yes, 8 million) enrollees over the course of a few years. The Wall Street Journal reported in 2004 that Aetna had spent more than $20 million to install new technology that enabled it “to identify and dump unprofitable corporate accounts.” Aetna’s investors rewarded the company by running up the stock price.

I added this later in the book:

One of my responsibilities at Cigna was to handle the communication of financial updates to the media, so I knew just how important it was for insurers not to disappoint investors with a rising MLR [medical loss ratio, the ratio of paid claims to revenues]. Even very profitable insurers can see sharp declines in their stock prices after admitting that they had failed to trim medical expenses as much as investors expected. Aetna’s stock price once fell more than 20% in a single day after executives disclosed that the company had spent slightly more on medical claims during the most recent quarter than in a previous period. The “sell alarm” was sounded when the company’s first quarter MLR increased to 79.4% from 77.9% the previous year.

I could always tell how busy my day was going to be when Cigna announced earnings by looking at the MLR numbers. If shareholders were disappointed, the stock price would almost certainly drop, and my phone would ring constantly with financial reporters wanting to know what went wrong.

May 1 was a deja-vu-all-over-again day for Aetna. You can be certain the company’s flacks had a terrible day–but not as terrible as the day coming soon for Aetna’s members when they try to use their membership cards.

Speaking of Lynch, one of the people commenting on the piece I wrote Monday suggested I might have been a bit too tough on Lynch, who I know and liked as a human being when we both worked at Cigna. The commenter wrote that:

After finishing Karen S. Lynch’s book, “Taking Up Space,” I came to the conclusion that she indeed has a very strong conscience and sense of responsibility, not totally to shareholders, but more importantly to the insured people under Aetna and the customers of CVS.”

I don’t doubt Karen Lynch is a good person, and I know she is someone whose rise to become arguably the business world’s most powerful woman was anything but easy, as the magazine for alumni of Boston College, her alma mater, noted in a profile of her last year. Quoting from a speech she delivered to CVS employees a few years earlier, Daniel McGinn wrote:

Lynch began with a story to illustrate why she was so passionate about health care. She described how she’d grown up on Cape Cod as the third of four children. Her parents’ relationship broke up when she was very young and her father disappeared, leaving her mom, Irene, a nurse who struggled with depression, as a single parent. In 1975, when Lynch was 12, Irene took her own life, leaving the four children effectively orphaned.

During her speech, several thousand employees listened in stunned silence as Lynch explained how her mom’s life might have turned out differently if she’d had access to better medical treatment, or if there’d been less stigma and shame about getting help for depression. She then talked about how an insurance company like Aetna could play a role in reducing that stigma, increasing access to care, and helping people live with mental illness.

I’m sure when she goes home at night these days, Lynch worries about what will happen to those 420,000 other humans who will soon be scrambling to get the care they need or to find another club that will take them. Their lives most definitely will turn out differently to appease the rich people who control her and the rest of us.

But she is stuck in a job whose real bosses–investors and Wall Street financial analysts–care far more about the MLR, earnings per share and profit margins than the fate of human beings less fortunate than they are.

However, the nonprofit provider and health plan warned subsequent quarters may be less profitable as expenses are projected to climb.

Dive Brief:

Nonprofit hospital and health plan giant Kaiser Permanente reported a $7.4 billion net gain for the first quarter ended March 31, compared to an income of $1.2 billion reported in the same period last year.

The Oakland, California-based operator’s earnings were boosted by its completed acquisition of Geisinger Health, which netted Kaiser a one-time operating gain of $4.6 billion.

Kaiser reported a quarterly operating margin of 3.4%, but noted the first quarter tends to be its strongest due to the timing of the open enrollment cycle. Kaiser predicts revenues will remain steady during subsequent quarters but expenses will likely rise.

Dive Insight:

Kaiser operates 40 hospitals, according to its website, and serves nearly 12.6 million health plan members as of the first quarter.

During the quarter, Kaiser subsidiary Risant Health — a nonprofit health network created last year to independently buy and operate other nonprofit health systems — completed its purchase of Geisinger Health. Kaiser received a one-time payment, boosting earnings. Net income for the quarter excluding the Geisinger transaction was $2.7 billion.

Kaiser increased its operating income year over year by more than 300% to total $935 million. Still, the nonprofit provider said that figure fell short of income logged prior to the pandemic.

Continued cost pressures from high utilization, care acuity and rising prices of goods and services drove quarterly expenses up 6% year over year to total $26.5 billion.

Kaiser has conducted at least three rounds of layoffssince the fall. It most recently cut 76 employees at the beginning of this month, a spokesperson confirmed to Healthcare Dive.

The cuts were done to “reduce costs across our organization,” and primarily impacted information technology and marketing roles, the spokesperson said via email.

Kaiser is not on a hiring freeze, the spokesperson noted. The organization has increased headcount by 5% since 2022 and has open positions currently listed online.

The Wall Street Journal also reported this weekend that Kaiser is attempting to sell $3.5 billion of its private investment holdings due to liquidity issues, citing sources familiar. Kaiser may attempt to sell further holdings later in 2024, according to the report.

Kaiser did not respond to requests for comment by press time about the possible sale.

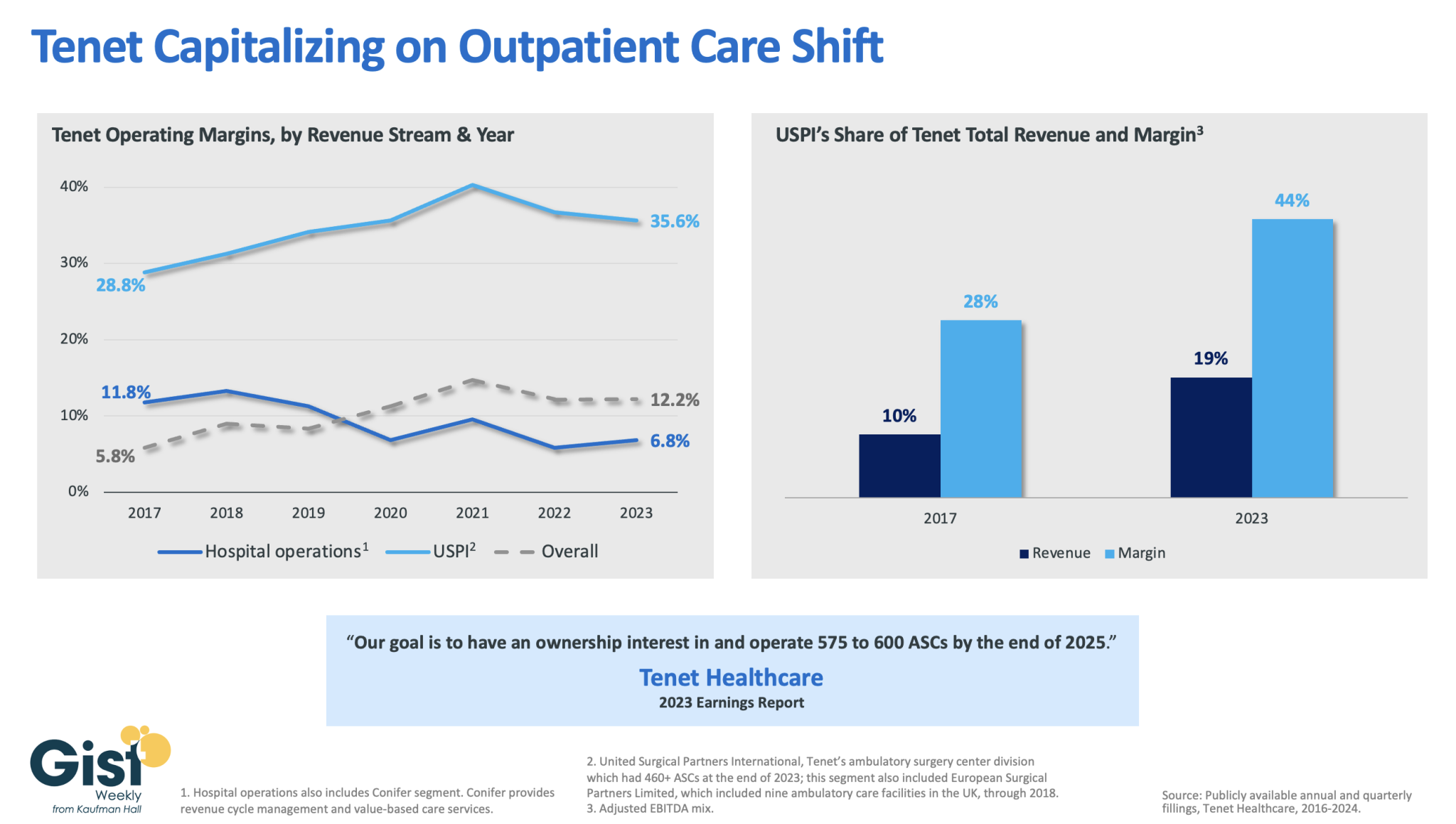

In this week’s graphic, we dive into recently released data on Tenet Healthcare’s 2023 financial performance. While the for-profit healthcare services company’s annual margin on hospital operations has declined since 2017, its overall profitability has more than doubled, thanks to strong performances from its ambulatory surgery center (ASC) chain,

United Surgical Partners International (USPI), which has consistently posted margins above 30 percent. Despite bringing in less than one fifth of Tenet’s total revenue, USPI is now responsible for almost half of Tenet’s overall margin.

Tenet has pursued this growth aggressively since buying USPI in 2015, swelling its ASC footprint from 249 locations in 2015 to more than 460 in 2023, with plans to increase that number to nearly 600 by the end of next year.

Tenet appears to be doubling down on its strategy of pursuing high-margin services over high-revenue services, especially as outpatient volumes are expected to far surpass growth in hospital-based care over the next decade.

Here are 23 health systems with strong operational metrics and solid financial positions, according to reports from credit rating agencies Fitch Ratings and Moody’s Investors Service released in 2024.

Avera Health has an “AA-” rating and a stable outlook with Fitch. The rating reflects the Sioux Falls, S.D.-based system’s strong operating risk and financial profile assessments, and significant size and scale, Fitch said.

Cedars-Sinai Health System has an “AA-” rating and a stable outlook with Fitch. The rating reflects the Los Angeles-based system’s consistent historical profitability and its strong liquidity metrics, historically supported by significant philanthropy, Fitch said.

Children’s Health has an “Aa3” rating and stable outlook with Moody’s. The rating reflects the Dallas-based system’s continued strong performance from a focus on high margin and tertiary services, as well as a distinctly leading market share, Moody’s said.

Children’s Hospital Medical Center of Akron (Ohio) has an “Aa3” rating and stable outlook with Moody’s. The rating reflects the system’s large primary care physician network, long-term collaborations with regional hospitals and leading market position as its market’s only dedicated pediatric provider, Moody’s said.

Children’s Hospital of Orange County has an “AA-” rating and a stable outlook with Fitch. The rating reflects the Orange, Calif.-based system’s position as the leading provider for pediatric acute care services in Orange County, a position solidified through its adult hospital and regional partnerships, ambulatory presence and pediatric trauma status, Fitch said.

Cook Children’s Medical Center has an “Aa2” rating and stable outlook with Moody’s. The ratings agency said the Fort Worth Texas-based system will benefit from revenue diversification through its sizable health plan, large physician group, and an expanding North Texas footprint.

El Camino Health has an “AA” rating and a stable outlook with Fitch. The rating reflects the Mountain View, Calif.-based system’s strong operating profile assessment with a history of generating double-digit operating EBITDA margins anchored by a service area that features strong demographics as well as a healthy payer mix, Fitch said.

JPS Health Network has an “AA” rating and stable outlook with Fitch. The rating reflects the Fort Worth, Texas-based system’s sound historical and forecast operating margins, the ratings agency said.

Mass General Brigham has an “Aa3” rating and stable outlook with Moody’s. The rating reflects the Somerville, Mass.-based system’s strong reputation for clinical services and research at its namesake academic medical center flagships that drive excellent patient demand and help it maintain a strong market position, Moody’s said.

McLaren Health Care has an “AA-” rating and stable outlook with Fitch. The rating reflects the Grand Blanc, Mich.-based system’s leading market position over a broad service area covering much of Michigan, the ratings agency said.

Med Center Health has an “AA-” rating and stable outlook with Fitch. The rating reflects the Bowling Green, Ky.-based system’s strong operating risk assessment and leading market position in a primary service area with favorable population growth, Fitch said.

Novant Health has an “AA-” rating and stable outlook with Fitch. The ratings agency said the Winston-Salem, N.C.-based system’s recent acquisition of three South Carolina hospitals from Dallas-based Tenet Healthcare will be accretive to its operating performance as the hospitals are highly profited and located in areas with growing populations and good income levels.

Oregon Health & Science University has an “Aa3” rating and stable outlook with Moody’s. The rating reflects the Portland-based system’s top-class academic, research and clinical capabilities, Moody’s said.

Orlando (Fla.) Health has an “AA-” rating and stable outlook with Fitch. The rating reflects the health system’s strong and consistent operating performance and a growing presence in a demographically favorable market, Fitch said.

Presbyterian Healthcare Services has an “AA” rating and stable outlook with Fitch. The Albuquerque, N.M.-based system’s rating is driven by a strong financial profile combined with a leading market position with broad coverage in both acute care services and health plan operations, Fitch said.

Rush University System for Health has an “AA-” rating and stable outlook with Fitch. The rating reflects the Chicago-based system’s strong financial profile and an expectation that operating margins will rebound despite ongoing macro labor pressures, the rating agency said.

Saint Francis Healthcare System has an “AA” rating and stable outlook with Fitch. The rating reflects the Cape Girardeau, Mo.-based system’s strong financial profile, characterized by robust liquidity metrics, Fitch said.

Saint Luke’s Health System has an “Aa2” rating and stable outlook with Moody’s. The Kansas City, Mo.-based system’s rating was upgraded from “A1” after its merger with St. Louis-based BJC HealthCare was completed in January.

Salem (Ore.) Health has an”AA-” rating and stable outlook with Fitch. The rating reflects the system’s dominant marketing positive in a stable service area with good population growth and demand for acute care services, Fitch said.

Seattle Children’s Hospital has an “AA” rating and a stable outlook with Fitch. The rating reflects the system’s strong market position as the only children’s hospital in Seattle and provider of pediatric care to an area that covers four states, Fitch said.

SSM Health has an “AA-” rating and stable outlook with Fitch. The St. Louis-based system’s rating is supported by a strong financial profile, multistate presence and scale with good revenue diversity, Fitch said.

University of Colorado Health has an “AA” rating and stable outlook with Fitch. The Aurora-based system’s rating reflects a strong financial profile benefiting from a track record of robust operating margins and the system’s growing share of a growth market anchored by its position as the only academic medical center in the state, Fitch said.

Willis-Knighton Medical Center has an “AA-” rating and positive outlook with Fitch. The outlook reflects the Shreveport, La.-based system’s improving operating performance relative to the past two fiscal years combined with Fitch’s expectation for continued improvement in 2024 and beyond.

Pittsburgh-based UPMC reported a $198 million operating loss (-0.7% margin) in 2023, down from a $162 million gain (0.6% margin) in 2022, according to financial documents published Feb. 28.

UPMC attributed the swing from operating income to loss to various factors, including increased labor and supply costs, increases in medical claims expense due to higher utilization and certain legal settlements.

Revenue for the health system increased 8.5% year over year to $27.7 billion and expenses rose 10% to $27.9 billion. Under expenses, labor costs increased 6.4% to $9.7 billion and supply costs were up 11% to $7.4 billion.

After accounting for nonoperating items, such as investment returns, UPMC ended 2023 with a $31 million net loss, compared to a $1 billion net loss the previous year.

As of Dec. 31, UPMC had more than $9.5 billion in cash and investments, $3.2 billion of which was held by its regulated health and captive insurance companies.