U.S. hospital finances experienced a comparatively strong 2019, according to Kaufman Hall’s 2019 Year In Review Flash Hospital Report, which labeled the performance as “cautiously optimistic.”

While revenue and margins increased for the hospitals surveyed, inpatient volumes were weaker and more uneven.

The report from the management consultancy and data provider did unearth some potential warning signs for 2020, including a trend in rising expenses. The report also warned of a slowing economy and the potential economic impact from the coronavirus.

Dive Insight:

Hospitals are complex, high-volume and low-margin enterprises that often experience operational volatility. The latest report by Kaufman Hall confirmed the uneasy environment in which they operate.

Operating earnings were up 2% in 2019 compared to the prior year, and overall operating margin was up 7.4%. That was driven primarily by small bumps in revenue and patient volume. Net patient revenue per adjusted discharge rose 3.7%, and was up 1.5% per adjusted patient day.

Yet both pre-tax and overall operating margin were down 1.7% and 0.3%, respectively, when hospital budget forecasts were factored in. However, that drop was all attributable to hospitals in the Northeastern U.S.

Nevertheless, overall margins fell into the red in August and November, although they rebounded strongly in December, up 20% in that month compared to December 2018.

However, cost pressures were significant. Total expenses per adjusted discharge were up 3.4%, while labor expenses rose 2.6%. Non-labor expenses per adjusted discharge was up 4%. Adjusted discharges themselves were up only 0.7%, and showed year-over-year declines not only for the first quarter of 2019 but in June, August and November. And overall discharges declined among hospitals compared to budget forecasts in the Midwest and Northeast, down nearly 6% and 4%, respectively. Adjusted patient days were up 2.5%, although the average length of stay rose 1.9%.

While operating room minutes were up 2.2%, they were 0.3% below budget forecasts. Emergency department visits were down 0.4% compared to 2018, and were a full percentage point below forecasts.

“While it was good to see improvements in many financial areas, the long-term trendlines indicate that this is not a time for the C-suite to relax,” said Kaufman Hall Managing Director Jim Blake.

“These modest gains were made during a time when the economy was strong, unemployment was historically low, and government regulations favored business. There also were no existential health threats, such as the COVID-19 coronavirus outbreak nor the risks that come any time there is a national election,” Blake continued.

After the stock market closed yesterday, Community Health Systems disclosed it lost $675 million in 2019, still has $13.4 billion of long-term debt and will sell even more hospitals than it already has, Axios’ Bob Herman reports.

The intrigue: The company’s stock was up 12% in after-hours trading.

That’s because CHS expects 2020 to be better — but still lose upwards of $150 million.

The bottom line: CHS owns a lot of hospitals in rural and small communities. Putting aside CHS’ specific business flops, it’s become tougher to operate hospitals in areas where the population is stagnating or declining because hospitals still rely on filling their clinics and beds.

Here are seven health systems with strong operational metrics and solid financial positions, according to reports from Fitch Ratings, Moody’s Investors Service and S&P Global Ratings.

1. Durham, N.C.-based Duke University Health System has an “Aa2” rating and stable outlook with Moody’s. The three-hospital system benefits from its role as the academic medical center of Duke University’s School of Medicine and is a nationally recognized and leading provider of tertiary and quaternary services, according to Moody’s. The credit rating agency expects the health system to maintain operating cash flow margins in the double-digit range.

2. Edison, N.J.-based Hackensack Meridian Health has an “AA-” rating and stable outlook with S&P and Fitch. The health system has a solid financial profile and a strong presence in a large and demographically favorable market, according to Fitch. S&P expects the health system’s depth of clinical services and operations to contribute to its stable financial performance.

3. Fountain Valley, Calif.-based MemorialCare has an “AA-” rating and stable outlook with Fitch and S&P. The health system has a strong balance sheet and financial profile, according to Fitch. The credit rating agency expects MemorialCare’s cash flow to improve due to its market strategy, which focuses on revenue diversification.

4. Portland-based Oregon Health & Science University has an “Aa3” rating and stable outlook with Moody’s and an “AA-” rating and stable outlook with S&P. OHSU, which is the only academic medical center in Oregon, has favorable operating performance, strong philanthropy and its clinical offerings draw patients from across Oregon and neighboring states, according to Moody’s. The credit rating agency expects OHSU’s revenue to continue to grow.

5. Boston-based Partners HealthCare, which is changing its name to Mass General Brigham, has an “Aa3” rating and stable outlook with Moody’s. The health system has an excellent reputation in clinical care and research, a seasoned management team, large size and diversity of revenue sources across several locations and lines of business, according to Moody’s. The credit rating agency expects Partners to achieve an operating surplus in fiscal 2020.

6. Norfolk, Va.-based Sentara Healthcare has an “Aa2” rating and stable outlook with Moody’s. The health system has a leading market position in its core service area, strong patient demand, and solid margins, according to Moody’s. The credit rating agency expects Sentara’s liquidity and debt metrics to remain at recent levels.

7. Livonia, Mich.-based Trinity Health has an “AA-” rating and stable outlook with Fitch and S&P. The health system has a significant market presence in several states and a strong financial profile, according to Fitch. The credit rating agency expects the health system’s operating margins to continue to improve.

The Tewksbury, Massachusetts–based health system strives to post its first positive balance sheet in more than five years.

Stephen Forney, MBA, CPA, FACHE, excels in fixing “broken” organizations and he has built a track record of achieving financial turnarounds at seven healthcare facilities, he tells HealthLeaders in a recent interview.

Forney has over three decades of experience as a healthcare executive, with a primary focus on problem-solving. He began his career fixing problems in areas such as information technology and supply chain, an approach and skill he has carried over into financial operations in the C-suite.

“In finance, it wound up being the same thing. Pretty much every organization I’ve gone to has been broken in some way, shape, or form,” Forney says. “I’ve developed a specialty doing turnarounds and this will be my eighth.”

Forney speaks about his new CFO role at the Tewksbury, Massachusetts–based Catholic nonprofit health system Covenant Health, which he joined in mid-September, and how driving revenue and reducing expenses must go hand-in-hand to achieve financial balance.

This transcript has been lightly edited for brevity and clarity.

HealthLeaders: Covenant is coming off its fifth straight year of operating losses. What is contributing to those losses and how do you plan to address those financial challenges?

Forney: The thing is, most turnarounds—to a greater or lesser extent—look a lot alike. With organizations that have [financial] issues, there are obviously always unique aspects to every situation, but virtually every healthcare organization that’s not doing well is because of the same relatively small handful of issues.

[For example,] revenue cycle is probably No. 1. Productivity has not been well attended to; expenses haven’t had a lot of discipline around them in a broad sense. That’s not to say that all decisions are bad, but in a systematic fashion, things haven’t been looked at. Frequently, driving volume and growing the business needs a better focus.

In the case of Covenant … there has been a plan developed to address all those areas and we are addressing them already, even though we will be posting another operating loss in fiscal [year] 2019. But the trajectory is good and some of the things that we’re now looking at are what I would consider to be phase two–type initiatives. How do we accelerate and move them to the next level?

On October 1, we outsourced our revenue cycle. I’m pleased that we were able to get that accomplished. Obviously, it’s early but, at least anecdotally, initial trends look good.

HL: Where do you fall on the dynamic between focusing on expense control measures or revenue generation?

Forney: I always feel like you need to do both. Expense management and working towards expense strategies is easier, quicker, and more straightforward.

[Revenue growth strategies] take time, take effort, and tend to [have] a much higher degree of uncertainty around the volume projection. Those are necessary and they’re things that we need to invest in because, at some point, you can’t cut any more from your organization, you’ve got to grow the top line. To me, it’s sort of like step one is stabilize your revenue cycle and stabilize your expenses. Then while you’re doing that, work on growth that’s going to take place 12 to 18 months down the road.

HL: Are you optimistic about the federal government’s efforts to move the industry toward value-based care?

Forney: Going back about a decade, I thought the ACE program, which was [the federal government’s] bundled payment program, was a solid step in the right direction. It gave organizations a chance to collaborate in compliant fashion with physicians to bend the cost curve and have beneficiaries participate in the bending of the cost curve as well. I was with one of the pilot health systems that [participated], and it was a remarkable success.

Everybody got to win; CMS, patients, physicians, and systems won by creating value. Yes, I think that the government has a good role to play in [value-based care] because they have such a large group of patients that they’re willing to experiment like that. [The federal government] can come up with potentially novel ways to get people to buy into this.

HL: What is it like to be at the helm of a Catholic nonprofit system and how does it affect your leadership style?

Forney: From a philosophical standpoint, the principle of creating shareholder wealth and good stewardship are not significantly different. You’ve got an end goal in mind, which is, you’re taking care of the patients and a community. In one case, whatever excess is left goes to a private equity fund or shareholders. In the other case, [the excess] stays in your balance sheet and gets reinvested in the community.

HL: Given your three decades of healthcare experience, do you have advice for your fellow provider CFOs, especially some of the younger ones?

Forney:Focus on being that strategic right-hand person to the CEO. In my experience, that has been one of the things that marks a successful CFO from one that isn’t as successful.

CEOs are going to get ideas from everywhere. They’re outward and inward facing. They deal with the doctors and the community, and they’re going to get all sorts of great ideas.

The CFO needs to be that person [who is] grounded and says, ‘Well, what about this?’ That doesn’t mean saying no. The whole idea is how do you make it [sound] like a yes. To me, the CFO role just grounds all the discussions, from working with physicians to working with the community.

CFOs over the last couple of decades have been operationally oriented. Now they need to start becoming clinically oriented.

There’s a real benefit in being able to sit down and talk with a physician and understand [what] they’re doing. … It winds up becoming a way to help ground the clinicians in the hospital operations because now you’re having a dialogue with them instead of them just saying, ‘You don’t understand. You’re not a clinician.’ That would be something that I would have a young CFO try to stay focused on, even though it’s dramatically outside the comfort zone for people that typically go into accounting.

Allentown, Pa.-based Lehigh Valley Health Network saw its net income more than triple from $35.1 million in fiscal year 2018 to $115.3 million in fiscal year 2019, according to financial documents released Dec. 4.

The health system saw its revenue increase year over year to $2.96 billion in the 12 months ended June 30. In the same period in 2018, the system reported revenue of $2.73 billion.

In fiscal year 2019, Lehigh Valley Health reported expenses of $2.86 billion, up from $2.68 billion in 2018.

Expense growth resulted from several factors, including an increase in salaries and wages and supply costs.

Lehigh Valley Health System attributed the net income increase to cutting back on contract workers and overtime and reducing costs on readmissions and contracts, according to The Morning Call.

Trinity Health recorded higher revenue and operating income in the first quarter of fiscal year 2020 than in the same period a year earlier, but the Livonia, Mich.-based system ended the quarter with lower net income, according to unaudited financial documents.

During the first quarter of fiscal 2020, which ended Sept. 30, Trinity reported operating revenue of $4.8 billion, a 1.8 percent increase over the same period of the year prior. Operating expenses climbed 1.7 percent year over year to $4.7 billion.

Trinity ended the first quarter of fiscal 2020 with operating income of $94 million, up from $87 million in the first quarter of last year.

The system reported an operating margin of 2 percent in the first quarter of fiscal 2020, compared to an operating margin of 1.8 percent in the same period of the year prior. Margin growth was partially attributable to Trinity’s divestiture of Camden, N.J.-based Lourdes Health System in June. Growth in patient volumes and payment rates also supported margin growth.

After factoring in nonoperating items, including a decline in investment returns, Trinity reported net income of $166.4 million in the first quarter of fiscal 2020. That’s compared to the first quarter of fiscal 2019, when the system posted net income of $419.9 million.

Both expense and volume performance were mixed for the month, according to Kaufman Hall.

For only the second time this year, hospitals of all sizes experienced monthly profitability declines, primarily due to “softening volumes,” according to a Kaufman Hall report released Tuesday.

In the month of August, both overall hospital operating EBITDA margins and operating margins fell by 9.4% and 11.4% year-over-year, respectively.

Kaufman Hall compared the August stagnation to the challenges hospitals faced in June, specifically referencing the ineffective approaches to adjust expenses when patient volumes sputter.

Delving into geographic differences, Midwest hospitals continue to show more resiliency than other areas, according to the report.

Hospitals in the northeast and Mid-Atlantic regions witnessed the largest declines in August, a 15.8% year-over-year drop in operating EBITDA margin, while the Great Plains posted profitability of 16.7% above budget.

Despite a relatively promising year thus far where hospitals rebounded from market volatility in 2018, provider organizations hit the financial skids in August due to inconsistent volume metrics.

Most volume metrics took a hit, with discharges, adjusted discharges, emergency department visits, and operating room minutes falling by more than 1.2% each.

Meanwhile, adjusted patient days and average length of stay increased by more than 1.6% as well.

Additionally, expense metrics were mixed for most hospitals, as total expenses per adjusted discharge rose 4% year-over-year, while labor expenses for the same metric increased 2.4%.

Purchased service expenses per adjusted discharge rose 6.1% while non-labor expenses and supply expenses for the same metric rose more than 3.5%.

On the non-operating side, the U.S. labor market continued its strong performance in the face of global headwinds and fears about a potential recession in the coming months.

Kaufman Hall described August as “weak month” for investment assets, noting that investment portfolio returns for hospitals declined 0.46%, the first monthly decline since May.

Here are seven health systems with strong operational metrics and solid financial positions, according to recent reports from Moody’s Investors Service, Fitch Ratings and S&P Global Ratings.

Note: This is not an exhaustive list. Hospital and health system names were compiled from recent credit rating reports and are listed in alphabetical order.

1. St. Louis-based BJC Health System has an “Aa2” rating and stable outlook with Moody’s. The health system has good margins and a favorable market position, according to Moody’s.

2. Hollywood, Fla.-based Memorial Healthcare System has an “Aa3” rating and stable outlook with Moody’s. The health system has a dominant market position in the southern portion of South Broward County and above average balance sheet liquidity, according to Moody’s.

3. Broomfield, Colo.-based SCL Health has an “Aa3” rating and stable outlook with Moody’s and an “AA-” rating and stable outlook with S&P. The health system has strong operating performance and solid balance sheet measures, according to Moody’s. The credit rating agency expects the health system’s cash flow to continue to grow.

4. Seattle Children’s Healthcare System has an “Aa2” rating and stable outlook with Moody’s. The health system has consistently strong operating performance, solid liquidity measures, and a favorable reputation within a broad service area, according to Moody’s.

5 Norfolk, Va.-based Sentara Healthcare has an “Aa2” rating and stable outlook with Moody’s. The health system has a leading market position in its service area, robust balance sheet metrics and solid margins, according to Moody’s.

6. St. Louis-based SSM Health has an “AA-” rating and stable outlook with Fitch. The health system has a strong financial profile and a growing health plan, according to Fitch. The credit rating agency expects SSM to continue to grow unrestricted liquidity and sustain improved operating performance.

7. Arlington-based Texas Health Resources has an “Aa2” rating and stable outlook with Moody’s. The health system has solid financial performance, a leading market position, good coverage of moderate debt levels, and a strong cash position, according to Moody’s.

It’s been reported that up to 15% of Goldman Sachs partners are preparing to leave by year’s end. Truth is, firms across Wall Street are having a crummy year and lots of personnel are going to be purged soon.

Investment-banking revenues had their worst first half since 2006, according to a report last week by Coalition, a London-based research firm. The weakest performance is in bond, currency and commodity trading, which accounts for 42% of revenue, down from almost two-thirds before the financial crisis. When bankers complain about regulation tying them down, this is what they mean. Shed a tear?

Because revenues have fallen faster than expenses, the industry’s return on capital has dropped to 6.7%. Its cost of capital, however, is in the 10% to 12% neighborhood.

For Goldman, Morgan Stanley and the like, the encouraging news is they remain highly profitable and have fewer problems than Deutsche Bank or UBS and their never-ending restructuring. The grimmer news is shares of Goldman and Morgan Stanleyare 21% and 27% lower, respectively, than 18 month ago. President Donald Trump’s trade wars and sluggish economic conditions overseas are taking a toll.

What could turn things around? If recession fears abated there could be a jump in corporate mergers, which produce a ton of fees. It would also help if WeWork went public at a hefty price, but right now WeWork isn’t working well as a possible initial public offering. Help could come from a Trump administration eager to ease the banks’ regulatory burden by reducing the amount of capital they must hold.

Still, making money in the markets figures to get harder in the years ahead. Late last month the $210 billion New York state pension fund dropped the long-term assumed rate of return on its investments to 6.8% from 7%. It was the third time the pension fund has cut its expected return since 2010, when it was 8%.

“The long-term outlook for investors is changing and requires a more conservative approach,” state Comptroller Thomas DiNapoli said in a statement.

If big buyers of investments are dialing down expectations, their dealers will have little choice but to follow.

A business I know well—journalism—has been permanently altered by the same technological upheaval attacking the livelihoods of traders, dealmakers and number-crunchers. Staffers at BuzzFeed and other news organizations have responded by unionizing so their owners will collectively bargain with them. It would be odd indeed for the Wall Street crowd to spend some of their bonus money casting their lot with organized labor. But given how precarious their jobs look, maybe they should.

The number of rural hospital closures in the United States has increased over the past decade.1 Since 2010, 113 rural hospitals,2 predominantly in Southern states, have closed. This is a concerning trend, since hospital closures reduce rural communities’ access to inpatient services and emergency care.3 In addition, hospitals that are at risk financially are more likely to serve rural communities with higher proportions of vulnerable populations.4

Understanding the financial pressures facing rural hospitals is imperative to ensuring that America’s 60 million rural residents have access to emergency care.5 Rural hospitals are generally less profitable than urban ones, and those with the lowest operating margins maintain fewer beds and have lower occupancy rates. Low-margin rural hospitals are also more likely to be in states that have not expanded Medicaid under the Affordable Care Act (ACA). According to new analysis by the Center for American Progress, future hospital closures would reduce rural Americans’ proximity to emergency treatment. Among low-margin, rural hospitals—those most likely to close—the majority of those with emergency departments are at least 20 miles away from the next-closest emergency department.

This report first discusses the role that hospitals and emergency care play in rural health care as well as trends in hospital closures. It then uses federal data to examine differences in the financial viability of rural and urban hospitals and the availability of hospital-based emergency care in rural areas. The final section of this report offers policy recommendations to improve health care access and emergency care for rural residents.

Rural hospitals have been closing at an unprecedented rate

From 2013 to 2017, rural hospitals closed at a rate nearly double that of the previous five years.6 (See Figure 1) According to the Government Accountability Office (GAO), recent rural hospital closures have disproportionately occurred among for-profit and Southern hospitals. Southern states accounted for 77 percent of rural hospital closures over that time period but only 38 percent of all rural hospitals in 20137

Hospital closures may deepen existing disparities in access to emergency care. Closures are more likely to affect communities that are rural, low income, and home to more racial/ethnic minority residents.8 Although about half of acute care hospitals are located in rural communities and the other half are located in urban areas,9 rural residents live 10.5 miles from the nearest acute care hospital on average, compared with 4.4 miles for those in urban areas.10 According to a poll by the Pew Research Center, about one-quarter (23 percent) of rural residents said that “access to good doctors and hospitals” is a problem in their community, while only 18 percent of urban residents and 9 percent of suburban residents said it was a problem.11

A variety of factors influence hospitals’ sustainability. Thanks to medical and technological advances, conditions that once required hospitalization can now be treated in an ambulatory care center or a physician’s office. University of Pennsylvania professor and CAP nonresident senior fellow Ezekiel Emanuel has argued that one reason hospitals are closing is that “more complex care can safely and effectively be provided elsewhere, and that’s good news.”12 As a whole, the hospital industry remains highly profitable, and hospital margins are at their highest in decades.13

Evidence on the relationship between hospital closures and health outcomes is mixed. A 2015 study of nearly 200 hospital closures in Health Affairs found no significant changes in hospitalization rates or mortality in the affected communities, whether rural or urban.14 More recent studies have found an association between rural hospital closures and increased mortality. Harvard researcher Caitlin Carroll showed that rural hospital closures led to an overall increase in mortality rates for time-sensitive health conditions,15 and Kritee Gujral and Anirban Basu of the University of Washington found that rural hospital closures in California were followed by increases in mortality for inpatient stays.16

In rural areas, hospitals face additional challenges to their viability, including lower patient volumes; higher rates of uncompensated care; and physician shortages.17 In addition, rural patients tend to be older and lower income.18 Rural hospitals tend to be smaller, serve a higher share of Medicare patients, and have lower occupancy rates than urban hospitals.19 Rural hospitals commonly offer obstetrics, imaging and diagnostic services, emergency departments, as well as hospice and home care,20 but patients needing more complicated treatment are often referred to tertiary or specialized hospitals. In fact, rural patients are more likely to be transferred to another hospital than patients at urban hospitals.21

Most urban hospitals are reimbursed under the prospective payment systems (PPS) for Parts A and B of Medicare. Through both the inpatient and outpatient PPS, the Centers for Medicare and Medicaid Services (CMS) reimburse hospitals at a predetermined amount based on diagnoses, with adjustments—including those for local input costs and patient characteristics.22However, rural hospitals often face higher costs due to lower occupancy rates and provide care to a higher percentage of patients covered by Medicare, Medicaid, and the Children’s Health Insurance Program (CHIP). Such hospitals may be eligible to receive higher payments from Medicare if they qualify as a Sole Community Hospital (SCH) or Medicare-Dependent Hospital (MDH).23

Another form of financial relief for rural hospitals is obtaining designation as a Critical Access Hospital (CAH), which Medicare reimburses based on cost rather than on the PPS.24 To qualify as a CAH, a hospital must provide 24/7 emergency services; maintain no more than 25 beds; and serve a rural area that is 35 miles from another hospital.25 Medicare reimburses CAHs at 101 percent of reasonable costs, rather than through the inpatient and outpatient PPS structures.26 As of 2018, there were 1,380 CAHs nationwide,27 accounting for about two-thirds of all rural hospitals.28

Even with cost-based reimbursement, however, some CAHs are unable to sustain the costs required to maintain inpatient beds.29 The 25-bed limit for CAHs prevent participating hospitals from eliminating inpatient services and restrict their ability to expand in response to fluctuations in community populations or care volumes. Other challenges facing rural hospitals include lacking sufficient patient volume to maintain high-quality performance for certain procedures and pressure to drop high-value but poorly reimbursed services such as obstetrics while maintaining low-volume, high profit services such as joint replacement procedures. 30

A key way that states can support struggling rural hospitals is by expanding Medicaid under the ACA. Expanding Medicaid increases coverage among low-income adults, 31 which in turn reduces uncompensated care costs for hospitals32 and allows financially vulnerable hospitals to improve their viability.33 Consistent with other recent studies,34 the GAO concluded in a 2018 report on rural hospitals that those “located in states that increased Medicaid eligibility and enrollment experienced fewer closures.”35

Rural hospitals are cutting back on services

Rural hospitals in different states have responded to financial pressures in a variety of ways, trying to balance community needs with financial viability. For many hospitals this has meant cutting inpatient obstetric services, leaving more than half of rural counties without hospital obstetric services.36 For instance, in Wisconsin, falling birth rates led to 12 hospitals in the state closing their obstetric services in the past decade.37 In Grantsburg, Wisconsin, lower birth rates and an older community population led Burnett Medical Center to shut down its obstetrics services.38 In order to offer these services, Burnett Medical Center would have needed to keep a general surgeon on call to perform caesarean sections, and with just 40 deliveries in 2017, the hospital could not justify the expense.39 While the hospital will continue providing prenatal and postnatal care, it will refer patients to a facility in Minnesota for deliveries—a facility is almost 40 minutes away.40

In other communities, hospitals have been replaced by other types of health care facilities. For example, Appalachian Regional Healthcare System closed Blowing Rock Hospital in North Carolina in 2013. Three years later, it opened a 112-bed post-acute care center in Blowing Rock in response to demand for rehabilitation services and the aging population in the surrounding area.41

Financial data shows that rural hospitals are more likely to struggle

To compare the financial situations of rural and urban hospitals and examine how future rural hospital closures could affect the availability of emergency care, CAP analyzed data from the CMS Healthcare Cost Report Information System (HCRIS). The CMS requires all Medicare-certified hospitals to report their financial information annually. CAP used the HCRIS to examine the financial margins and other characteristics of 4,147 acute care hospitals for fiscal year 2017. Of these, 1,954 hospitals (47 percent) were in rural areas, while the remaining were in urban areas. Hospitals self-report their status in the HCRIS as either urban or rural, which the CMS defines as either inside or outside of a metropolitan statistical area, respectively.42 Further information about CAP’s hospital sample can be found in the Methodological appendix.

Hospital operating margins, which measure excess patient-related revenues relative to patient-related expenses, are often used as an indicator of financial health.43 A 2011 study by Harvard researchers Dan Ly, Ashish Jha, and Arnold Epstein found that the lowest 10 percent of hospitals by operating margin were 9.5 times more likely to close within two years compared to all others. 44 The same study concluded that hospitals with low operating margins were also more likely to be acquired or merge.45

In CAP’s hospital sample, the median operating margin was negative 2.6 percent among all hospitals, negative 0.1 percent for urban hospitals, and negative 4.9 percent for rural hospitals.46 Public hospitals and MDHs in the sample were more likely to have negative operating margins, consistent with what other studies have found.47 To analyze hospitals’ relative financial health across geographic areas, CAP ranked hospitals in the HCRIS sample based on operating margin, splitting them into three groups: the lowest 10 percent, the middle 80 percent, and the highest 10 percent. The range of operating margins for each group is shown in Table 1.

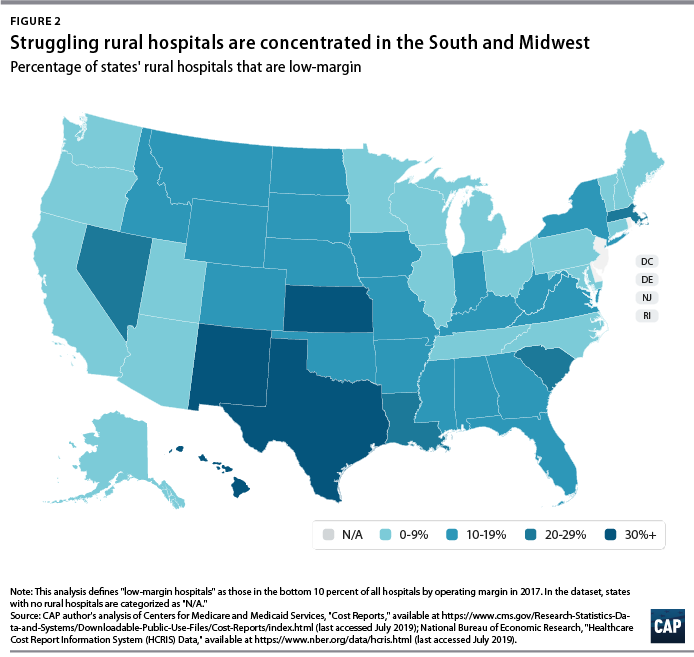

Rural hospitals are less likely to be financially healthy than urban hospitals. In 2017, rural hospitals comprised only 27.9 percent of the hospitals with operating margins in the highest decile but comprised 59.7 percent of the hospitals in the lowest decile. Southern and Midwestern states had the greatest proportion of rural hospitals with low operating margins, mimicking the geographic patterns in hospital closures that the GAO report identified. CAP finds that from 2015 through 2017, rural hospitals were consistently more likely than urban hospitals to fall in the bottom 10 percent of operating margins. CAP’s analysis also confirms that rural hospitals in states that expanded Medicaid had a higher median operating margin (negative 3.4 percent) than those in states that have not expanded Medicaid (negative 5.7 percent).

To examine commonalities among the hospitals most vulnerable to closure, CAP analyzed characteristics of the hospitals with low margins, defined as having an operating margin in the lowest 10 percent among all hospitals. Smaller, low-occupancy rural hospitals were most likely to struggle financially: nearly 1 in 6 (15 percent) of hospitals with 25 or fewer beds had low margins, and nearly one-fifth (17 percent) of hospitals with low-occupancy rates had low margins. (See Figure 3)

Emergency departments are on the front lines for rural health

In some emergency situations, hospital closures can be life-threatening, increasing the time and distance patients travel to receive care. Studies show that the probability of dying from a heart attack increases with distance from emergency care,48 and traumatic injuries are more likely to be fatal for rural residents than for urban ones.49

Rural residents are more likely than urban residents to visit the emergency department.50 A shortage of primary care providers; lack of public transportation infrastructure; shortages in preventive care; higher rates of smoking and obesity; and greater prevalence of chronic disease in rural areas all contribute to the greater utilization of emergency room care.51 As a result, emergency departments often stand in as the main source of care for vulnerable and low-income populations, especially for communities that face a shortage of primary care. 52 Among the dozens of rural hospitals that have closed in recent years, some served as the only emergency department in a community, according to MedPAC53

While freestanding emergency departments have proliferated,54 they are not filling the gap for rural emergency care. MedPAC found that, as of 2016, nearly all the country’s 566 stand-alone emergency departments were in urban areas and tended to be located in more affluent communities.55 Researchers at the North Carolina Rural Health Research Program found that the freestanding emergency department model was generally not viable in rural areas of the state due to low patient volumes, high rates of uninsured patients, and provider shortages.56 One limit on the growth of independent freestanding emergency centers is that they are not recognized in Medicare law and are therefore unable to bill the program, unlike hospital-affiliated off-campus emergency departments. 57

Future rural hospital closures would increase the distances that patients travel for emergencies

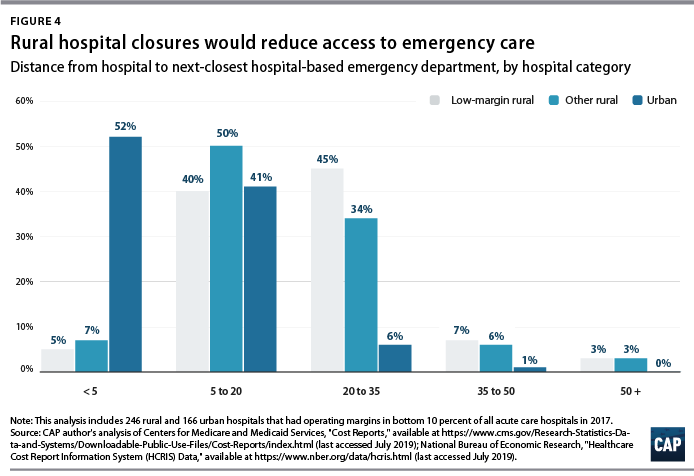

To better understand how future rural hospital closures could affect access to emergency care, CAP calculated hospitals’ distance to the next-closest hospital-based emergency department. CAP restricted its 2017 HCRIS data sample to the 3,616 acute care hospitals that provide 24-hour emergency services.58 Using addresses or coordinates provided in the HCRIS, CAP mapped each low-margin rural hospital to the next-closest hospital emergency department. Mapping strategies are detailed in the Methodological appendix.

Among the 222 low-margin rural hospitals, more than half (55 percent) were more than 20 miles away from the next-closest hospital-based emergency department, and one-tenth were more than 35 miles away. (See Figure 4). The average distance to the next-closest emergency department was 22 miles.

The disappearance of rural, low-margin hospitals would greatly increase patients’ travel distances for emergency care. Without other resources to fill the gap, some patients might forgo care they need and others would be forced to undertake an even longer journey to receive medical attention.

Policies to improve rural emergency and nonemergency care

As rural hospitals continue to close, it is crucial to preserve access to emergency care for rural Americans. The following section details a series of policy recommendations to support adequate emergency care and address care shortages in rural communities.

Expand Medicaid

Experience to date suggests that rural hospitals in those states that have not yet expanded their Medicaid programs under the ACA would benefit from Medicaid expansion through lower levels of uncompensated care and increased financial sustainability. Medicaid expansion is associated with improvements in health and a wide variety of other outcomes, including lower mortality, less uncompensated care, and lower rates of medical debt.59 According to the Kaiser Family Foundation, about 4.4 million adults would gain Medicaid eligibility if the remaining 14 nonexpansion states expanded their programs.60

Policymakers can also support rural communities and their hospitals by opposing efforts to repeal the ACA. If the Trump administration-backed lawsuit against the ACA were to succeed, 20 million Americans would lose health insurance coverage, and uncompensated care would rise by $50 billion, according to the Urban Institute.61

Create a greater number of rural emergency centers

To preserve access to emergency care, Congress could allow rural hospitals like CAHs to downsize to an emergency department and eliminate inpatient beds without giving up special Medicare reimbursement arrangements. Qualifying hospitals could transfer patients requiring inpatient admission to other hospitals, while continuing to offer some diagnostic imaging and other outpatient services.

One such proposal is the Rural Emergency Acute Care Hospital Act (REACH Act), bipartisan legislation proposed by Sen. Amy Klobuchar (D-MN) and Sen. Chuck Grassley (R-IA) that would create rural emergency centers.62 This designation would allow hospitals to provide only emergency care in rural communities and receive Medicare reimbursement at 110 percent of operating costs. Separately, MedPAC has recommended that rural hospitals located more than 35 miles from the nearest emergency department be allowed to convert to freestanding emergency departments while still being reimbursed at hospital rates.63

Institute global budgeting for rural hospitals

Under global budgeting, hospitals are paid a fixed amount rather than having their reimbursements based on the volume and types of services they provide.64 Global budgeting can reduce small, rural hospitals’ financial risk by providing them with a more predictable stream of revenue. In addition, payment reforms that include both hospital and nonhospital care can encourage communities to invest in services that are typically less generously reimbursed, such as preventive care.65

For example, in 2014, Maryland transitioned its acute hospitals from fee-for-service payments to a global budget.66 An evaluation of the global budget program showed that it reduced hospital expenditures relative to trend without transferring costs to other parts of the health care system.67 Future global budgets should emphasize improvements in population health and primary care,68 including ensuring that patients receive care in appropriate settings and reducing the number of avoidable hospital visits.

The Pennsylvania Rural Health Model is the first Medicare demonstration project to test the financial viability and community effects of a global budget for strictly rural hospitals.69 This six-year program aims to smooth out cash flow for 30 rural Pennsylvania hospitals on a monthly basis with the goal of enabling hospitals to meet community needs, especially for substance-use disorder and mental health services.70 With global budgets based on the previous year’s revenues, participating hospitals will have a more predicable stream of revenue. Importantly, the program allows hospitals to share in the savings that result from avoidable utilization.71

Improve transportation for rural residents

The lack of transportation infrastructure can lead rural residents to rely on ambulances and emergency rooms for nonemergency care. In nonemergency situations, patients often cite the lack of affordable transportation as a major barrier to care access.72 In order to fill the gap, payers and policymakers should consider efforts to utilize existing community transit resources for medical transportation or reimburse patients who use ride-sharing services in areas that lack public transit or taxi services. 73 Another option would be to formalize volunteer services for medical transit. Oregon offers a tax credit for volunteer rural emergency medical services (EMS) providers, who provide medical and transportation services analogous to those of volunteer firefighter programs.74 The CMS should also consider policies to better reimburse and expand the use of telehealth in remote areas to reduce patients’ burden of transportation.75Finally, the CMS should stop approving states’ requests to waive coverage of nonemergency medical transportation (NEMT) requirements under Medicaid.76 NEMT is vital to eligible beneficiaries’ access to care, including appointments for preventive care, chronic disease management, and substance-use disorder treatment.

Strengthen the rural health care workforce

Rural health care provider shortages contribute to poorer access to care and poorer quality of care in rural communities. While 20 percent of the U.S. population lives in rural areas, only 9 percent of primary care physicians practice in rural areas.77 Greater access to primary care providers in rural areas would improve quality of care and health outcomes while also reducing unnecessary emergency department visits.78

One way to assist rural areas would be to encourage health professionals to train and work in underserved communities. Federal funding for physician training should include reimbursements for community-based sites so that medical residents can rotate through nonhospital settings.79 Expanding the National Health Service Corps—which provides scholarships and student loan repayment for professionals who work in federally designated health professional shortage areas—could also help bolster the rural workforce. In addition, changes to immigration policy—such as expanding the Conrad 30 program that funnels immigrant doctors into rural and underserved communities, reforming H-1B visas to benefit high-need communities—could help alleviate rural areas’ shortage of medical professionals.80

Conclusion

Mounting closures of rural hospitals across the country are exacerbating the disparity in health care access between rural and urban areas. The financial vulnerability of the remaining rural hospitals suggests that the trend may continue, leaving shortages in emergency care and other hospital services.

Policymakers should support initiatives that allow remaining rural hospitals the flexibility to tailor their services to meet community needs and improve access to care for rural Americans.