Cartoon – Resuscitation is Available

Drug companies raised prices on seven popular drugs during 2017 and 2018 without clinical evidence that the drugs had been improved in any way, according to a new report.

The increases cost patients and insurers more than $5 billion, the Institute for Clinical and Economic Review (ICER) found in its report. None of the drugs examined showed evidence of improved safety or effectiveness, the analysis found.

The report looked at the seven top-selling drugs by sales revenue that had price increases of more than two times inflation, as measured by the medical consumer price index.

The culprits, and how much they added to drug spending over two years:

California Attorney General Xavier Becerra alleges that Sutter Health used its pre-eminent market power to artificially inflate prices. Photo: Rich Pedroncelli/Associated Press

As a jury trial draws near in a major class-action lawsuit alleging anticompetitive practices by Northern California’s largest health system (PDF), a new CHCF study shows the correlation between the prices consumers pay and the extensive consolidation in the state’s health care markets. Importantly, the researchers estimated the independent effect of several types of industry consolidation in California — such as health insurers buying other insurers and hospitals buying physician practices. The report, prepared by UC Berkeley researchers, also examines potential policy responses.

While other states have initiated antitrust complaints against large hospital systems and medical groups in the past, the case against Sutter Health is unique in both the expansive nature of the alleged conduct and in the scale of the potential monetary damages. The complaint goes beyond claims of explicit anticompetitive contract terms and argues that by virtue of its very size and structure, the Northern California system imposed implicit or “de facto” terms that led to artificially inflated prices. Sutter Health vigorously denies the allegations.

The formation of large health systems like Sutter is neither new (PDF) nor unique to California (PDF). Several factors seem to be encouraging their growth, including payment models that place health care providers at financial risk for the cost of care, increased expectations from policymakers and payers around the continuum of patient needs that must be managed, and economies of scale for investments in information technology and administrative services. Some market participants also point to consolidation in other parts of the health care system, such as health plans and physician groups, as encouragement for their own mergers.

In general, economists study two major categories of market consolidation:

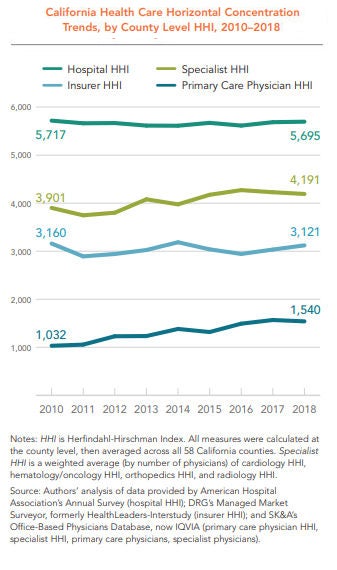

To measure market consolidation, the CHCF study relied on the Herfindahl-Hirschman Index (HHI), a metric used by the US Department of Justice and the Federal Trade Commission. An HHI of between 1,500 and 2,500 is considered moderately concentrated, and 2,500 or above is considered highly concentrated. According to this measure, horizontal concentration is high in California among hospitals, insurance companies, and specialist providers (and moderately high among primary care physicians), even though the level of concentration in all but primary care has remained relatively flat from 2010 to 2018.

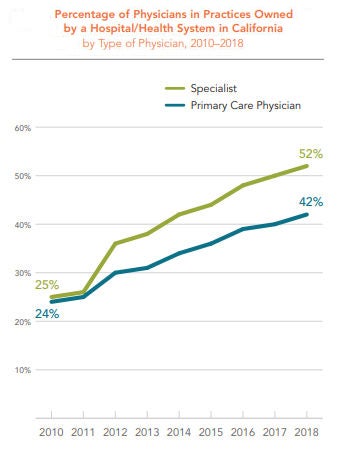

The percentage of physicians in practices owned by a hospital or health system increased dramatically in California between 2010 and 2018 — from 24% in 2010 to 42% in 2018. The percentage of specialists in practices owned by a hospital or health system rose even faster, from 25% in 2010 to 52% in 2018.

The percentage of physicians in practices owned by a hospital or health system increased dramatically in California between 2010 and 2018 — from 24% in 2010 to 42% in 2018. The percentage of specialists in practices owned by a hospital or health system rose even faster, from 25% in 2010 to 52% in 2018.

While this study defined and quantified the extent of consolidation across several industry segments in California, it is important to note that it did not define, quantify, or evaluate clinical integration within the state. Clinical integration has been defined by others in many ways, but generally involves arrangements for coordinating and delivering a wide range of medical services across multiple settings.

As the CHCF study authors point out, other analysis has shown that various types of clinical integration can lead to broader adoption of health information technology and evidence-based care management processes. Data from the Integrated Healthcare Association suggests that certain patient benefit designs and provider risk-sharing arrangements associated with clinical integration can lead to higher quality and lower costs.

Crucially, an emerging body of law (PDF) suggests that clinical integration does not require formal ownership and joint bargaining with payers.

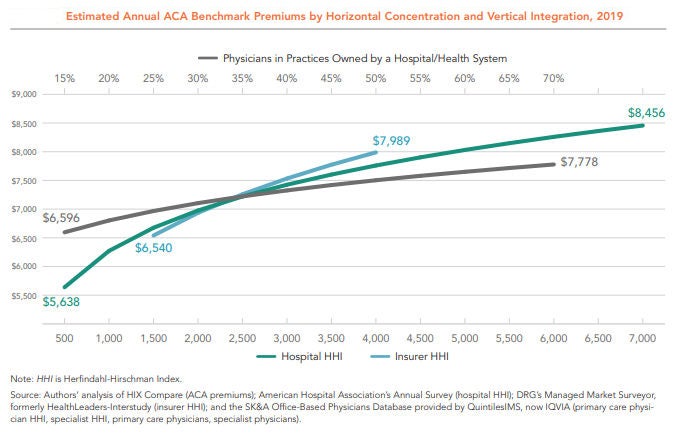

Among the six variables analyzed in the CHCF study, three showed a positive and statistically significant association with higher premiums: insurance company mergers, hospital mergers, and the percentage of primary care physicians in practices owned by hospitals and health systems. The remaining three variables studied — specialist provider mergers, primary care provider mergers, and the percentage of specialists in practices owned by a hospital and health system — were statistically insignificant.

The figure below shows the independent relationship between market concentration and premiums for these three variables. As the lines move left to right, concentration increases — that is, fewer individual insurers, hospitals, or providers occupy the market. The vertical axis shows the average premiums associated with each level of market concentration. In short, regardless of the industry structure represented by the other variables, insurer consolidation, hospital consolidation, and hospital-physician mergers each lead to higher premiums.

Unexplained Price Variation and Growth

Health insurance premiums rise when the underlying cost of medical care increases. California ranks as the 16th most expensive state on average in terms of the seven common services the researchers studied, after adjusting for wage differences across states. Among all states, California has the eighth-highest prices for normal childbirth, defined as vaginal delivery without complications. Childbirth is the most common type of hospital admission, and the relatively standardized procedure is comparable across states.

Even within California, prices vary widely and are growing rapidly. For example, the 2016 average wage-adjusted price for a vaginal delivery was twice as high in Rating Area 9 (which has Monterey as its largest county) as it was in Rating Area 19 (San Diego) — $22,751 versus $11,387. (See next figure.) Prices for the service are increasing rapidly across counties — rising anywhere from 29% in San Francisco from 2012 to 2016 to 40% in Orange County over the same period.

The authors of the CHCF report investigated the impact of various types of consolidation on the prices of individual medical services in California. For cesarean births without complications, a 10% rise in hospital HHI is associated with a 1.3% increase in price.

While the study shows significant associations between various types of market concentration and the prices consumers pay, policymakers should carefully consider implementing steps that restrain the inflationary impact of consolidation while allowing the benefits of clinical integration to proliferate. To that end, the authors of the CHCF report offered a series of recommendations, which include:

Enforce antitrust laws. Federal and state governments should scrutinize proposed mergers and acquisitions to evaluate whether the net result is procompetitive or anticompetitive.

Restrict anticompetitive behaviors. Anticompetitive behaviors, such as all-or-nothing and anti-incentive contract terms, should be addressed through legislation or the courts in markets where providers are highly concentrated.

Revise anticompetitive reimbursement incentives. Reimbursement policies that reduce competition, such as Medicare rules that implicitly reward hospital-owned physician groups, should be adjusted.

Reduce barriers to market entry. Policies that restrict who can participate in the health care market, such as laws prohibiting nurse practitioners from practicing independently from a physician, should be changed when markets are concentrated.

Regulate provider and insurer rates. If antitrust enforcement is not successful and significant barriers to market entry exist — including those in small markets unable to support a competitive number of hospitals and specialists — regulating provider and insurer rates should be considered.

Encouraging meaningful competition in health care markets is an exceedingly difficult task for policymakers. It is no easier to promote the benefits of clinical integration while restraining the inflationary aspects of economic consolidation through public policy. Despite these challenges, the rapid rise in health care premiums and prices in the state require a fresh look at the consequences of widespread horizontal and vertical consolidation in California.

:format(webp)/cdn.vox-cdn.com/uploads/chorus_image/image/65358995/843175548.jpg.0.jpg)

Is the rapidly rising cost of employer-sponsored health insurance sustainable?

Half of all Americans get their health insurance through work. Trouble is, doing so is becoming less and less affordable — especially for already low-wage workers.

In 2019, the Kaiser Family Foundation Employer Health Benefits Survey — an annual account of roughly 2,000 small and large businesses’ employer-sponsored insurance — found the average annual premium to cover a family through work was a whopping $20,576, and $7,188 for an individual. Employers cover most of that, but families still contributed an average of $6,015 in premiums, and single Americans covered about $1,242 of the annual cost.

The kicker? Over the past 10 years, the cost of the portion of employer-sponsored health insurance premiums that falls on American families has increased by 71 percent. Overall, premiums have gone up 54 percent since 2009. That’s faster than the rate of inflation and faster than the average wage growth.

Nearly half of all Americans get their health insurance through work, a system that covers roughly 153 million people. And for lower-wage workers it’s a system that is increasingly unaffordable.

Workers at companies with a significant number of low-wage employees (which the Kaiser Family survey quantifies as a company in which at least 35 percent of employees are making an annual salary of $25,000 or less) have lower premiums than those who work at companies with fewer low-wage workers, probably because their plans cover less. But at the same time, workers at firms with a significant number of low-wage employees are faced with high-deductible plans, and also pay a larger share of the premium cost than workers at companies with fewer lower-wage employees.

According to the survey, workers at lower-wage companies pay an average of $7,000 a year family plan — $1,000 more than employees at companies with higher salaried workers.

“When workers making $25,000 a year have to shell out $7,000 a year just for their share of family premiums,” Drew Altman, the president of Kaiser Family Foundation, said in a statement, that’s where cost becomes prohibitive. Such employees are putting almost 30 percent of their salaries toward premiums.

The takeaway is clear. Health care is getting more and more expensive, and families and employers are having to bear more of the cost, which research has shown not only has an effect on how much workers are actually getting paid, but how many workers are hired.

As Sarah Kliff reported for Vox, there are a lot of studies spanning decades that show how a rapid rise in health insurance premiums has unfavorable outcomes for workers. This is in large part because employers think of compensation in totality; they lump together an employee’s salary, as well as their benefits as one total cost. So if covering a worker’s health insurance gets more and more expensive, employers see less room to give the worker a raise.

For example, a 2006 study from Katherine Baicker and Amitabh Chandra, both with the National Bureau of Economic Research, found that an overall 10 percent increase in health insurance premiums reduced wages by 2.3 percent and actually reduced the probability of becoming employed by 1.2 percent.

Results such as these, and the high premiums low-wage workers must pay, led the Kaiser survey’s authors to explicitly question the tenability of employer-sponsored insurance: “the national debate about expanding Medicare or creating public program options provides an opportunity to step back and evaluate how well employer-based coverage is doing in achieving national goals relating to costs and affordability,” the report reads.

The United States is unique in its reliance on employers to provide health insurance. And, as Democratic candidates for president continue to go in circles debating health care, employer-sponsored insurance is often the biggest sticking point.

Several candidates, like Sen. Bernie Sanders, who popularized a plan for Medicare-for-all, a single government-run program, and Sen. Elizabeth Warren, who supports Sanders’s plan, have called for getting rid of the employer-based system, and private insurance, all together.

But their critics always bring up the same talking point: that the people who like their health insurance plans through work, should be able to keep it. The Kaiser survey raises questions as to how affordable those plans really are, and, as Democrats debate ideas like Medicare-for-all, how sustainable the current trajectory is.

The debate over healthcare and how it should proceed has apparently come down to either keeping what we’ve got, going back to what we had, or Medicare for All. At least, that’s how things are being framed for a coming presidential election. At stake is the cost and delivery of 17.9% of the country’s entire gross domestic product—$3.5 trillion in 2017 and heading north from there.

There have been previous attempts, of course, to change healthcare, whether the addition of Medicare and Medicaid under Lyndon Johnson, Bill and Hillary Clinton’s unsuccessful attempt to reshape the healthcare system, the addition of prescription drug coverage to Medicare signed by George W. Bush, or the Affordable Care Act under Barack Obama.

As a country, we periodically seek a better approach to healthcare—this way, that way, but not straying far from where we were. Understandable, to a (small, these days) degree. There is no guarantee that a quick change won’t cause more problems than it solves. Some people like their coverage, it’s true. But a great many do not.

Importantly, the day is coming (if it’s not right here) that most people can’t afford reasonable care. Average annual premiums for employer-sponsored healthcare for a family have reached $20,576, according to a survey by the Kaiser Family Foundation. Of that, $6,015 are paid by the employee and $14,561 by the employer.

The problem of cost is immense, especially when overall healthcare in the U.S. ranks as mediocre at best (which doesn’t mean good care isn’t available, but more likely is an indication of how relatively few people obtain it).

But many who have a vested interest in the system as it exists, whether for political or financial gain, loudly exclaim that any sort of solution that involves government as an insurer—like Medicare, which many participants prize given much lower rates than typical market-based programs—becomes untenable. “Can you afford how much taxes will go up?” they say.

Some voices have pushed back and we need more, because the question is a loaded one. Government-sponsored insurance would reduce the need for and expense of private insurance.

At issue is an analytic approach often used in business: the total cost of ownership. When taking up a new technology or operational strategy, a smart company analyzes the full costs. Not just the obvious price tag, but all that accompanying costs. It’s the corporate equivalent of an informed car buyer, who, beyond sticker price, is interested in the likely costs of fuel and maintenance, how well the vehicle maintains price in the used or trade-in markets, reliability, and other factors that represent accompanying expenses.

Taxes under a Medicare for All approach would go up. But, at the same time, commercial premiums come down (even if, as with Medicare, many people buy supplemental insurance to expand coverage). There may lower out-of-pocket costs, as is true in many countries with some sort of national coverage.

There is also an argument for resulting higher worker pay. Companies no longer be paying that $14,561 could shift that savings, or at least some, into additional wages or salary. Not increasing pay would effectively be a tax cut, as benefits are part of compensation.

The thought behind healthcare reform like Medicare for All is that it should be possible for the U.S. to do better. To gain improved coverage across the board at lower per-capita prices, as the rest of the developed world has managed to do for decades. People with better care can live better lives, which—and I take this as an article of faith—eventually comes back to communities and the country.

Consideration of changes requires a full understanding of the costs and financial gains throughout the system. Taxes go up, premiums go down, maybe pay increases (should increase), and a sudden illness doesn’t cause automatic financial stress for an individual or a family. Whenever someone makes sweeping claims like “taxes will go up” without context, others should step up and note that it’s like complaining about investing in mass transit without acknowledging that using an automobile to make the same commute will be much more expensive and that one may mean you don’t need the other.

https://apnews.com/1c5c5dc43950421a9ab4ff7edb9fe678?omnicid=CFC1688174&mid=henrykotula@yahoo.com

Major legislation to reduce prescription drug costs for millions of people may get sidelined now that House Democrats have begun an impeachment inquiry of President Donald Trump. Proposals had been moving in Congress, but there are more ways for the process to break down than to succeed. Still, nobody says they’re giving up.

Some questions and answers about the legislation and its uncertain prospects:

Q: Why, now, is there a big push to lower drug prices?

A: Some would say it’s overdue. Drug prices emerged as the public’s top health care concern near the end of the Obama administration as people with health insurance got increasingly worried about their costs.

In the 2016 campaign, Trump and Democrat Hillary Clinton called for authorizing Medicare to negotiate prices. But after Trump won the White House, his focus shifted to the failed Republican drive to repeal the Affordable Care Act. A year went by before the administration reengaged on prescription drugs .

Now, facing the 2020 election, Trump and lawmakers of both parties in Congress have little to show for all their rhetoric about high drug prices. For there to be a deal , enough Democrats and Republicans have to decide they’re better off delivering results instead of election-year talking points.

Q: What are the major plans on the table?

A: On the political left is House Speaker Nancy Pelosi’s plan authorizing Medicare to negotiate prices for the costliest drugs. In the middle is bipartisan legislation from Sens. Chuck Grassley, R-Iowa, and Ron Wyden, D-Ore., to restrain drug price increases. The wild card is Trump. He doesn’t share the traditional Republican aversion to government as price negotiator and keeps complaining that it’s unfair for Americans to pay more than patients in other countries.

There’s significant overlap among the major approaches.

Trump, the Senate bill, and Pelosi would all limit what Medicare enrollees pay annually in prescription copays. That would be a major change benefiting more than 1 million seniors with high costs.

Pelosi and the Senate bill would require drugmakers to pay rebates if they raise their prices to Medicare beyond the inflation rate. Long-available medicines like insulin have seen steep price hikes.

Pelosi and the administration would use lower international prices to determine what Medicare pays for at least some drugs. Pelosi is echoing Trump’s complaint that prices are unfair for Americans.

“If they wanted to do a deal, it’s sitting right there in front of them,” said John Rother, president of the National Coalition on Health Care, an umbrella group representing a cross-section of organizations.

Q: How would any of these plans reduce what I pay for prescription drugs?

A: Under Pelosi’s bill, private purchasers such as health insurers and employer-sponsored plans would be able to get the same price that Medicare negotiates. Medicare would focus on the costliest medications for individual patients and the health care system as whole.

People on Medicare could be the biggest winners. There’s consensus that seniors should get an annual limit on out-of-pocket costs for medications — $2,000 in the Pelosi bill or $3,100 in the Senate bill. Older people are the main consumers of prescription medicines.

Q: What would “Medicare for All” do about drug prices?

A: Under Medicare for All, the government would negotiate prices for prescription drugs.

Whether or not they support Medicare for All, Democratic presidential candidates are calling for Medicare to negotiate prices.

Q: Why are drug prices so much higher in the U.S. than in other countries?

A: It’s not the case for all drugs. U.S. generics are affordable for the most part.

The biggest concern is over cutting-edge brand-name drugs that can effectively manage life-changing diseases, or even cure them. Drugs with a $100,000 cost are not unusual any more. In other countries, governments take a leading role in setting prices.

In the U.S., some government programs such as Medicaid and the veterans’ health system get special discounts. But insurers and pharmacy benefit managers negotiate on behalf of Medicare and private health plans. Federal law protects the makers of a new drug from generic competition, which gives the manufacturer a lot of leverage.

Pharmaceutical companies say high initial prices are justified to recoup the costs of research and development.

However, a major case study — the 2015 Senate investigation of costly breakthrough drugs for hepatitis C infection — found that drugmaker Gilead Sciences priced the medication to maximize profits, not to foster access.

Q: What’s the outlook for drug pricing legislation?

A: Impeachment could suck the air out of the room.

“It is extremely difficult to get things done in that type of environment, and certainly for a president who is largely incapable of compartmentalizing,” said longtime Democratic health care adviser Chris Jennings. “Having said that, the work of policymakers in power must include being responsive to here-and-now domestic problems.”

Trump has pointedly refrained from criticizing Pelosi’s bill even as other Republicans called it “socialist.”

Pelosi’s legislation had its first committee consideration last week, and the leading Democrat on that committee promoted it using Trump-like rhetoric that it’s unfair for Americans to pay more. The bill will get a floor vote, and it could gain political momentum if a pending budget analysis finds big savings.

Democrats would be hard-pressed to drop their demand for Medicare negotiations. But could Trump agree to a more limited form of negotiations than what’s now in Pelosi’s bill? Could he sell that to Senate Republicans?

“It boils down to the crude political calculus of whether in the end this will help my side,” said health economist Joe Antos of the business-oriented American Enterprise Institute. “Will Democrats be able to stomach Donald Trump taking credit for all of this? On the Trump side, it is going to be more of a legacy issue for him.”

Americans need to know more before they can make up their minds about proposed overhauls to the nation’s health care system, according to a survey released Thursday.

When asked if they wanted to wipe out private health insurance for a so-called Medicare for All public insurance program, 40 percent of U.S. adults between the ages of 19 to 64 said they did not know enough to offer an opinion.

A few Democratic presidential candidates have put forward their proposed health care plans, including Medicare for All. Sen. Bernie Sanders, I-Vt. and Sen. Elizabeth Warren, D-Mass. have advocated for Medicare for All models that replace private insurance with a national health insurance plan. And Sen. Kamala Harris, D-Calif., released a health care proposal that covered 330 million Americans under one government health care plan. According to the candidates, these plans would make health care affordable for more Americans. It could help reduce the number of uninsured Americans, which currently amounted to 27.5 million people nationwide in 2018, according to the Census Bureau, marking a rise of 1.9 million people over the previous year.

According to a July 22 poll from the PBS NewsHour, NPR and Marist, 70 percent of U.S. adults said they supported Medicare for All proposals as long as they maintain an option to keep private health insurance. A system like this has been proposed by Pete Buttigieg. By comparison, when asked in a separate question, only 41 percent of survey respondents said they wanted to scrap private health insurance for a government-run plan.

In this latest poll from the Commonwealth Fund, another 32 percent of Americans said they opposed the idea, while 27 percent of Americans favored such a plan, according to the survey results published by the Commonwealth Fund, which researches health policy. The survey polled 4,914 U.S. adults ages 19 to 64 from March 19 to June 9.

“People are confused about what this might mean for them, and what it might mean for the health system and what it might mean in terms of trade-offs,” said Sara Collins, vice president of Health Care Coverage and Access at the Commonwealth Fund, during a call with reporters Wednesday.

Americans are largely satisfied with their health insurance, but lacked confidence that their health care coverage could protect them financially if they fell seriously ill and required medical care.

“These satisfaction rates reflect the fact that most people don’t use their insurance a ton,” said Sabrina Corlette, a research professor and co-founder of the Center on Health Insurance Reforms at Georgetown University. “It’s sporadic interactions.”

Eighty-five percent of working-age Americans said they were satisfied with their health insurance. That included private health insurance, Medicaid, and coverage purchased on the individual marketplace established under the Affordable Care Act. Another 14 percent said they were dissatisfied with their current health insurance.

In contrast, 61 percent of U.S. adults age 16 to 64 said they were confident that they would be able to afford the cost of care if they became seriously ill, while 38 percent of Americans said they were not confident.

These survey results come as Democratic presidential candidates promote their health care plans going into the 2020 election. Meanwhile, Republicans in Congress and the Trump administration have promised to replace the Affordable Care Act, known as Obamacare, with “something better,” although it is unclear what that would be. To date, they have eliminated some policies put into place under Obamacare, including dismantling the individual mandate.

Health care will be one of the most important issues among voters going into the next presidential election. Health care costs for Americans are the highest among industrialized nations. Meanwhile, life expectancy has dropped nationwide in recent years, in part due to the rise in drug overdose deaths, many of which are tied to the opioid crisis. Among developed nations the OECD ranked for infant mortality, the U.S. was among the bottom 11, after Russia.

This survey suggests that all the campaigns have their work cut out for them if they want to ramp up public awareness of proposals on the table to fix health care, Corlette said. She said the public needs more education and discussion about possible solutions aimed at problems in the U.S. health care system.

“It strikes me as a really good opportunity for people on both sides of the debate,” Corlette said. “There’s clearly a lot of people who have just not made up their mind.”

But she said the lack of confidence in how much protection health coverage affords people tugs at the reality that “the system doesn’t work really well for people who are very sick.”

New analysis from the Kaiser Family Foundation supports that notion. Annual family premiums for employer-based health insurance rose 5 percent to $20,576 on average, faster than wage growth, which increased by 3.4 percent, according to the study, published in Health Affairs. And since 2009, those premiums jumped 54 percent.

Health insurance costs and coverage only provide part of the picture of what troubles Americans, said Thomas Miller, a resident fellow with the conservative American Enterprise Institute.

Policymakers need to think about more than tinkering with “incremental expansions of coverage on the margins beyond where we already are,” Miller said. “It’s important to remember that people need most of all economic growth, job security and reasons to be optimistic about managing their lives.”

CMS is proposing that hospitals make public their payer-specific negotiated charges for a limited set of “shoppable” services.

Hospitals and insurers have made clear their opposition to the Centers for Medicare and Medicaid Services proposed rule requiring the disclosure of their privately negotiated contract rates.

CMS is proposing that hospitals make public their payer-specific negotiated charges for a limited set of “shoppable” services or face civil monetary penalties, in a rule to go into effect on January 1, 2020. Comments were due by September 27.

Under the rule, hospitals would display payer-specific negotiated charges for at least 300 shoppable services, including 70 selected by CMS and 230 by the provider.

The American Hospital Association called it the wrong approach, even though it said it supported ensuring patients have the information they need, including knowing what their expected out-of-pocket costs would be. However, the AHA said, “Instead of helping patients estimate their out-of-pocket obligations, it would introduce confusion and fuel anticompetitive behavior among commercial health insurers in an already highly-concentrated insurance industry, seriously limiting the choices available to patients.”

America’s Essential Hospitals said, “We are particularly concerned that the agency’s proposals regarding the public posting of charges, in particular the posting of negotiated rates, offer little benefit to the consumer, add substantial burden to hospitals, and pose harm to competition, potentially driving up prices.”

America’s Health Insurance plans said that forcing disclosure of privately and competitively negotiated rates will not provide consumers with information that is actionable or helpful. I

“Instead,”AHIP said, “it will hamper competitive negotiations and push healthcare prices and premiums higher for patients, consumers, businesses and taxpayers. This proposed rule also has significant implications for, and is interconnected with, other proposed rules regarding interoperability of health care data. We are concerned that unknown entities will have open access to the data, with few restrictions on how they may use it.”

WHY THIS MATTERS

CMS released the proposals on July 29 in the 2020 hospital outpatient prospective payment and ambulatory surgical center payment rule.

The rule also has three additional proposed policies that run afoul of the law, the AHA said.

Specifically, the AHA opposes completion of the phase-in of payment reductions for the hospital outpatient clinic visit in excepted off-campus provider-based departments to the “physician fee schedule equivalent” rate of 40% of the outpatient prospective payment system rate.

The AHA said the proposal “exceeds the Administration’s legal authority and should be abandoned.”

The AHA has already won a case in court on the government’s site neutral payment policy.

“On the clinic visit policy, we remind CMS that the agency was recently found by the courts to have exceeded its statutory authority when it cut the payment rate for clinic services at excepted off-campus provider-based departments,” the AHA said.

Hospitals also object to continuing the current policy that pays for separately payable drugs acquired through the 340B drug savings program at the rate of average sales price minus 22.5%.

And the AHA objects to the implementation of a prior authorization process for five categories of outpatient department services.

THE LARGER TREND

On September 17, a federal judge ruled in favor of the AHA and hospital organizations, saying CMS exceeded its statutory authority when it reduced payments for hospital outpatient services provided in off-campus provider-based departments that were grandfathered under the Bipartisan Budget Act of 2015.

The AHA, joined by the Association of American Medical Colleges and several member hospitals, had filed the lawsuit in December.

ON THE RECORD

America’s Essential Hospitals said, “These cuts deter hospitals from expanding access in communities with the most need for healthcare services and run counter to CMS’ goal of integrated, coordinated healthcare.

“Taken together, these proposals would have a chilling effect on beneficiary access to care while also increasing regulatory burden,” the AHA said.

https://apnews.com/1c5c5dc43950421a9ab4ff7edb9fe678?omnicid=CFC1688174&mid=henrykotula@yahoo.com

Major legislation to reduce prescription drug costs for millions of people may get sidelined now that House Democrats have begun an impeachment inquiry of President Donald Trump. Proposals had been moving in Congress, but there are more ways for the process to break down than to succeed. Still, nobody says they’re giving up.

Some questions and answers about the legislation and its uncertain prospects:

Q: Why, now, is there a big push to lower drug prices?

A: Some would say it’s overdue. Drug prices emerged as the public’s top health care concern near the end of the Obama administration as people with health insurance got increasingly worried about their costs.

In the 2016 campaign, Trump and Democrat Hillary Clinton called for authorizing Medicare to negotiate prices. But after Trump won the White House, his focus shifted to the failed Republican drive to repeal the Affordable Care Act. A year went by before the administration reengaged on prescription drugs .

Now, facing the 2020 election, Trump and lawmakers of both parties in Congress have little to show for all their rhetoric about high drug prices. For there to be a deal , enough Democrats and Republicans have to decide they’re better off delivering results instead of election-year talking points.

Q: What are the major plans on the table?

A: On the political left is House Speaker Nancy Pelosi’s plan authorizing Medicare to negotiate prices for the costliest drugs. In the middle is bipartisan legislation from Sens. Chuck Grassley, R-Iowa, and Ron Wyden, D-Ore., to restrain drug price increases. The wild card is Trump. He doesn’t share the traditional Republican aversion to government as price negotiator and keeps complaining that it’s unfair for Americans to pay more than patients in other countries.

There’s significant overlap among the major approaches.

Trump, the Senate bill, and Pelosi would all limit what Medicare enrollees pay annually in prescription copays. That would be a major change benefiting more than 1 million seniors with high costs.

Pelosi and the Senate bill would require drugmakers to pay rebates if they raise their prices to Medicare beyond the inflation rate. Long-available medicines like insulin have seen steep price hikes.

Pelosi and the administration would use lower international prices to determine what Medicare pays for at least some drugs. Pelosi is echoing Trump’s complaint that prices are unfair for Americans.

“If they wanted to do a deal, it’s sitting right there in front of them,” said John Rother, president of the National Coalition on Health Care, an umbrella group representing a cross-section of organizations.

Q: How would any of these plans reduce what I pay for prescription drugs?

A: Under Pelosi’s bill, private purchasers such as health insurers and employer-sponsored plans would be able to get the same price that Medicare negotiates. Medicare would focus on the costliest medications for individual patients and the health care system as whole.

People on Medicare could be the biggest winners. There’s consensus that seniors should get an annual limit on out-of-pocket costs for medications — $2,000 in the Pelosi bill or $3,100 in the Senate bill. Older people are the main consumers of prescription medicines.

Q: What would “Medicare for All” do about drug prices?

A: Under Medicare for All, the government would negotiate prices for prescription drugs.

Whether or not they support Medicare for All, Democratic presidential candidates are calling for Medicare to negotiate prices.

Q: Why are drug prices so much higher in the U.S. than in other countries?

A: It’s not the case for all drugs. U.S. generics are affordable for the most part.

The biggest concern is over cutting-edge brand-name drugs that can effectively manage life-changing diseases, or even cure them. Drugs with a $100,000 cost are not unusual any more. In other countries, governments take a leading role in setting prices.

In the U.S., some government programs such as Medicaid and the veterans’ health system get special discounts. But insurers and pharmacy benefit managers negotiate on behalf of Medicare and private health plans. Federal law protects the makers of a new drug from generic competition, which gives the manufacturer a lot of leverage.

Pharmaceutical companies say high initial prices are justified to recoup the costs of research and development.

However, a major case study — the 2015 Senate investigation of costly breakthrough drugs for hepatitis C infection — found that drugmaker Gilead Sciences priced the medication to maximize profits, not to foster access.

Q: What’s the outlook for drug pricing legislation?

A: Impeachment could suck the air out of the room.

“It is extremely difficult to get things done in that type of environment, and certainly for a president who is largely incapable of compartmentalizing,” said longtime Democratic health care adviser Chris Jennings. “Having said that, the work of policymakers in power must include being responsive to here-and-now domestic problems.”

Trump has pointedly refrained from criticizing Pelosi’s bill even as other Republicans called it “socialist.”

Pelosi’s legislation had its first committee consideration last week, and the leading Democrat on that committee promoted it using Trump-like rhetoric that it’s unfair for Americans to pay more. The bill will get a floor vote, and it could gain political momentum if a pending budget analysis finds big savings.

Democrats would be hard-pressed to drop their demand for Medicare negotiations. But could Trump agree to a more limited form of negotiations than what’s now in Pelosi’s bill? Could he sell that to Senate Republicans?

“It boils down to the crude political calculus of whether in the end this will help my side,” said health economist Joe Antos of the business-oriented American Enterprise Institute. “Will Democrats be able to stomach Donald Trump taking credit for all of this? On the Trump side, it is going to be more of a legacy issue for him.”