Published in the April edition of Health Affairs Forefront, this piece unpacks why payers and other corporations have replaced health systems as the top bidders for primary care practices, driving up practice purchase prices from hundreds of dollars to tens of thousands of dollars per patient. While corporate players like UnitedHealth Group, Amazon, and Walgreens have spent an estimated $50B on primary care, it pales in comparison to the potential “$1T opportunity” in value-based care projected by McKinsey and Company.

The authors argue that this tantalizing opportunity exists because the Centers for Medicare and Medicaid Services (CMS) invited corporations to “re-insure” Medicare through capitated arrangements in Medicare Advantage (MA) and its Direct Contracting program.

While CMS intended to promote risk and value-based incentives to improve care quality and costs, the incentive structures baked into these programs have afforded payers record profits, despite neither improving patient outcomes nor reducing government healthcare spending.

The Gist: While the critiques of MA reimbursement structures in this piece are familiar, they are woven together into a convincing rebuke of the “unintended consequences” of CMS’s value-based care policy.

Through poorly designing incentives, CMS paved a runway for corporate America to capture the lion’s share of the financial returns of value-based care, paying prices for primary care that health systems can’t match.

Meanwhile, despite skyrocketing valuations for primary care practices, primary care services remain underfunded and inadequately reimbursed, pushing primary care groups closer to payers with excess profits to invest.

Walgreens’ growing U.S. healthcare segment is continuing to bolster the retail health chain’s financial performance. The business, which includes value-based provider VillageMD, recorded $1.6 billion in sales in the second quarter, an increase of $1.1 billion from last year.

VillageMD sales were up 30%, including a boost from its recent acquisition of medical group Summit Health. Specialty pharmacy Shields Health Solutions grew sales 41%, while at-home care provider CareCentrix’s sales were up 25%.

Thanks in part to a jump in revenue in its healthcare segment, Walgreens’ results beat Wall Street expectations even as profit declined more than 20% amid lower COVID-19 vaccine volumes and test sales, higher salary costs, opioid litigation charges and costs associated with its $3.5 billion investment in its Summit acquisition.

Dive Insight:

Walgreens has been working to expand its business scope beyond pharmacies to more consumer-centric healthcare, and has acquired a number of companies to build out its growing U.S. healthcare division.

In its earnings results for the second quarter ended Feb. 28, the business reported gross profit of $32 million, as income from Shields and CareCentrix was offset by VillageMD expansion costs. VillageMD added 133 clinics compared to the second quarter last year.

“With the closing of VillageMD’s acquisition of Summit Health, [Walgreens] is now one of the largest players in primary care,” CEO Roz Brewer said in the company’s earnings release on Tuesday.

VillageMD also acquired a Connecticut-based medical group in March for an undisclosed amount. That group, called Starling Physicians, operates more than 30 primary care and multi-specialty practices across the state.

Starling “will contribute heavily to revenue and EBITDA growth in the second half of 2023,” said Walgreens CFO James Kehoe on a Tuesday morning call with investors. “Overall, the primary care business and the specialty care business is doing really, really well.”

Despite the recent deals, Walgreens is moving beyond its peak investment period in healthcare, management said on the call. VillageMD, for example, plans to concentrate growth and investments in specific markets where it can be “hyper-relevant” moving forward, according to Walgreens President John Standley.

After rumors of a possible deal first surfaced in early January, CVS Health announced on Wednesday that it has entered into a definitive agreement to acquire value-based primary care provider Oak Street Health for $10.6B. The Chicago-based company will join CVS’s recently formed Health Care Delivery organization, bringing with it roughly 600 physicians and nurse practitioners working at 169 senior-focused clinics in 21 states. This move is the latest by CVS to expand its care offerings, following its $100M investment last month in primary and urgent care provider Carbon Health, and its $8B acquisition of in-home evaluation company Signify in September.

The Gist: If this deal goes through, CVS will have the key pieces of the national primary care physician network it needs for a value-based care platform focused on Medicare Advantage—although how they will combine Oak Street’s clinics with retail-based HealthHUBs and other primary care assets remains unclear.

The fact that CVS is paying about a 50 percent share price premium shows how competitive the market for large physician organizations has become, driving up bidding prices such that only cash-rich payers, pharmacies, and retailers can afford them as they seek to emulate UnitedHealth Group’s Optum strategy.

Of note, the same day CVS announced the deal, Aetna competitor and erstwhile investor in Oak Street, Humana announced a five-year network partnership with Oak Street competitor ChenMed.

We’ll be watching for whose strategy proves most effective as we enter the next phase of the physician arms race between vertically-integrated payers, and the emphasis shifts from how many providers are employed to how they’re integrated and deployed.

CVS Health is close to a deal to acquire primary care provider Oak Street Health for around $10.5 billion, including debt, marking the latest move among major healthcare stakeholders in acquiring primary care companies, the Wall Street Journal reports.

According to people with knowledge of the matter who spoke to the Journal, the two companies are discussing a deal in which CVS would acquire Oak Street for a price of around $39 a share. If the deal goes through, it could be announced as soon as this week.

According to the Journal, “the Oak Street acquisition would further the company’s long-term shift to broaden into businesses beyond retail pharmacy by adding doctors who can more fully manage patients’ care.”

Oak Street has more than 160 centers across 21 states and focuses mainly on caring for patients enrolled in Medicare. The company, which is based in Chicago, was founded in 2012 and specializes in caring for patients under value-based care arrangements.

Aetna, which is owned by CVS, has a growing Medicare Advantage business that would likely tie in with Oak Street’s clinics, which care for about 159,000 patients under value-based arrangements, the Journal reports.

The move is the latest among major healthcare stakeholders acquiring primary care companies. In September 2022, CVS announced an $8 billion deal to acquire home healthcare company Signify Health.

Meanwhile, Amazon in July 2022 announced a $3.9 billion deal to acquire primary care company One Medical, Humana in September 2022 announced its intention to spend up to $550 million to purchase 20 CenterWell Senior Primary Care clinics, and Walgreens Boots Alliance in November 2022 announced a roughly $9 billion deal to acquire Summit Health.

Urgent care centers have become increasingly popular among patients in recent years. And while the facilities may be a more convenient care option than others, experts have voiced concerns about potential downsides, Nathaniel Meyersohn writes for CNN.

What is driving the urgent care ‘boom’?

Urgent care centers have been in the United States since the 1970s, but they were widely regarded as “docs in a box,” with slow growth in their early years. Then, during the COVID-19 pandemic, demand for tests and treatments drove an increase in patients at urgent care sites around the country. According to the Urgent Care Association (UCA), patient volume at urgent care centers has increased by 60% since 2019.

As patient volumes and demand increased, growth for new urgent care centers surged. Currently, there are a record 11,150 urgent care centers in the United States, with around 7% growth annually, UCA said. Notably, this figure excludes clinics inside retail stores and freestanding EDs.

According to estimates from IBISWorld, the urgent care market will reach roughly $48 billion in revenue in 2023, a 21% increase from 2019.

“Urgent care has grown rapidly because of convenience, gaps in primary care, high costs of emergency room visits, and increased investment by health systems and private-equity groups,” Meyersohn writes.

Urgent care center growth also “highlights the crisis in the US primary care system,” Meyersohn writes, noting that the Association of American Medical Colleges said it expects a shortage of up to 55,000 primary care physicians in the next decade.

In addition, it can be difficult to book an immediate visit with a primary care provider. Urgent care sites have longer hours during the week and are open on weekends, making it easier to get an appointment. According to UCA, roughly 80% of the U.S. population is within a 10-minute drive of an urgent care center.

“There’s a need to keep up with society’s demand for quick turnaround, on-demand services that can’t be supported by underfunded primary care,” said Susan Kressly, a retired pediatrician and fellow at the American Academy of Pediatrics.

Meanwhile, health insurers and hospitals have also prioritized keeping people out of the ED. In the early 2000s, they started opening their own urgent care sites and implementing strategies to deter ED visits.

The passage of the Affordable Care Act also triggered an increase in urgent care providers, with millions of newly insured Americans accessing healthcare.

In addition, data from PitchBook suggests that private-equity and venture capital funds invested billions into deals for urgent care centers.

“If they can make it a more convenient option, there’s a lot of revenue here,” said Ateev Mehrotra, a professor of healthcare policy and medicine at Harvard Medical School who has researched urgent care clinics. “It’s not where the big bucks are in health care, but there’s a substantial number of patients.”

The increase in urgent care sites may present challenges

Many doctors, healthcare advocates, and researchers have voiced concerns at the increase in urgent care sites, noting that there are potential downsides.

“Frequent visits to urgent care sites may weaken established relationships with primary care doctors,” Meyersohn writes. “They can also lead to more fragmented care and increase overall health care spending, research shows.”

In addition, some experts have questioned the quality of care at urgent care centers, particularly how well they serve low-income communities.

In a 2018 study by Pew Charitable Trusts and CDC, researchers found that urgent care centers overprescribe antibiotics, especially those used to treat common colds, the flu, and bronchitis.

“It’s a reasonable solution for people with minor conditions that can’t wait for primary care providers,” said Vivian Ho, a health economist at Rice University. “When you need constant management of a chronic illness, you should not go there.”

Some doctors and researchers also expressed concern that patients are visiting urgent care centers instead of a primary care provider altogether.

“What you don’t want to see is people seeking a lot [of] care outside their pediatrician and decreasing their visits to their primary care provider,” said Rebecca Burns, the urgent care medical director at the Lurie Children’s Hospital of Chicago.

“There are also concerns about the oversaturation of urgent care centers in higher-income areas that have more consumers with private health care and limited access in medically underserved areas,” Meyersohn writes.

A 2016 study from the University of California at San Francisco found thaturgent care centers typically do not serve rural areas, areas that have a high concentration of low-income patients, or areas that have a low concentration of privately-insured patients.

According to the researchers, this “uneven distribution may potentially exacerbate health disparities.”

Budget retailer Dollar General announced this week that it’s partnering with mobile medical service provider DocGo to deliver routine primary care in mobile clinics outside three stores near its Goodlettsville, TN headquarters.

The mobile clinics will accept public and select commercial insurance plans, as well as offer services for a flat fee. It’s the latest step in Dollar General’s tentative exploration of healthcare, which includes a partnership with Babylon Health to offer telehealth visits in several Missouri stores, and the DG Wellbeing initiative, which has placed basic health and wellness products in roughly 3,200 of its 19,000 stores nationwide.

The Gist: With an unmatched footprint in rural areas (an estimated 75 percent of the US population lives within five miles of one of its stores) Dollar General has the capacity to transform rural healthcare access.

Rather going head-to-head with other national retailers who are quickly expanding into healthcare delivery, Dollar General has so far taken a measured approach, aiming to develop workable services that improve rural healthcare access at the margins.

Since it hired a chief medical officer in 2021, it has dabbled in small care delivery pilots like this one, but one of these pilots will need to succeed at scale for Dollar General to enter the ranks of serious retail disruptors.

On Monday, San Francisco-based Carbon Health—a virtual-first primary and urgent care company with 125 clinics across 13 states—announced a partnership with CVS Health, which includes a $100M investment, as well as plans to pilot its operating model in select CVS stores. The announcement came just days after Carbon reported its second round of layoffs in the past year, as it scales back on less profitable business segments to focus on expanding its primary care model.

The Gist: It’s been over a year since CVS CEO Karen Lynch said the company was moving with “speed and urgency” to construct a physician-staffed primary care model. Last fall it purchased in-home health evaluation company Signify Health for $8B, after rumors that it had been close to acquiring One Medical.

Between its convenient retail footprint, insurance arm, and Signify’s risk-assessment tools, a nationwide primary care physician network is the last puzzle piece CVS needs to field a comprehensive and formidable primary care strategy.

While it’s currently rumored to be evaluating a $10B acquisition of Oak Street Health, this partnership with Carbon Health is a better bet to deliver value quickly, as CVS should be able to more easily integrate and leverage Carbon’s retail health expertise across its growing care delivery platform.

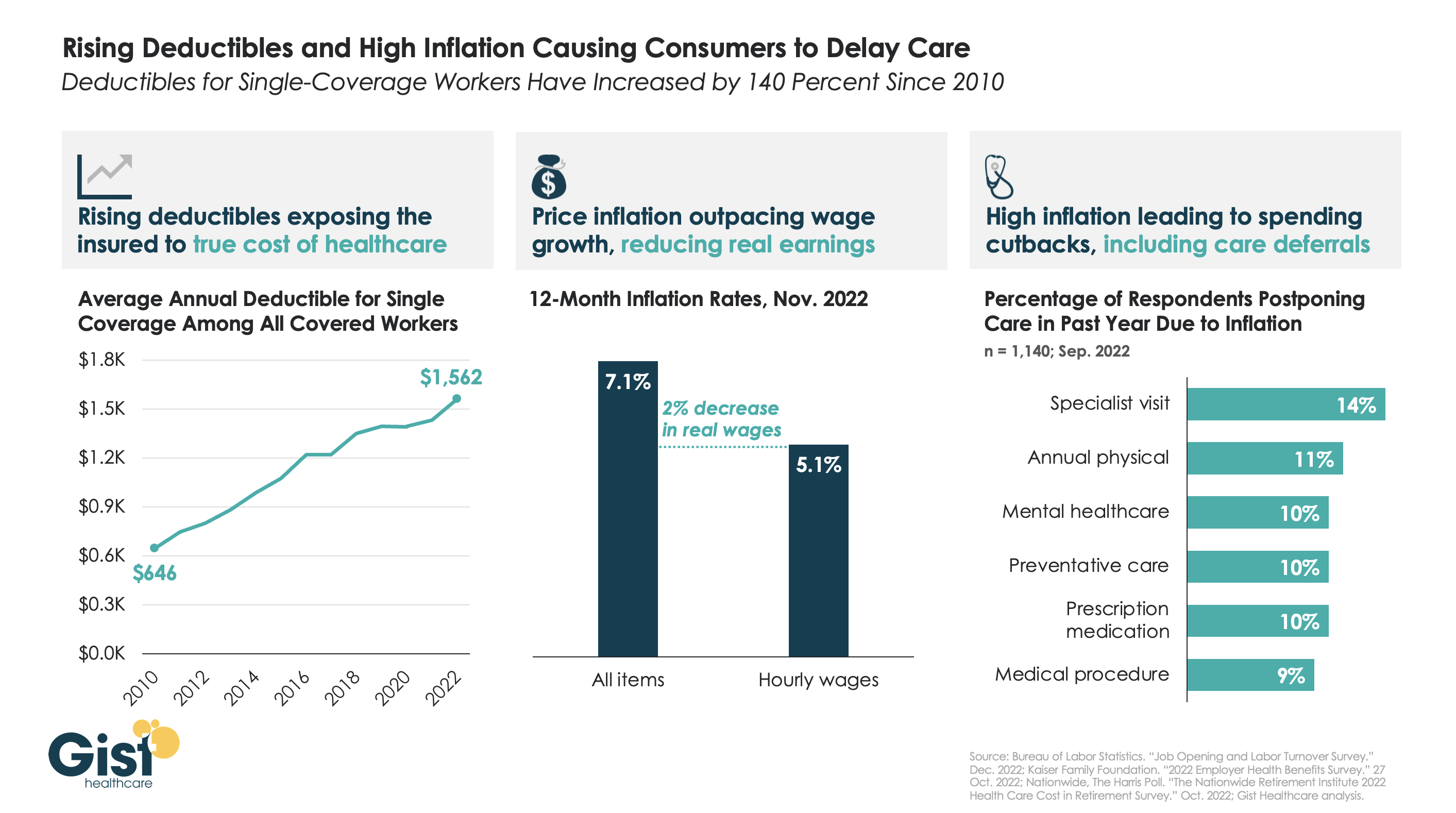

After COVID fears and shutdowns led consumers to delay care early in the pandemic, persistently high inflation over the past year has further suppressed volumes.

As the graphic above illustrates, the average deductible for individual coverage has grown by over 140 percent since 2010, exposing consumers to an increasing portion of healthcare costs, and prompting economists to reevaluate the adage that healthcare is “recession-proof”.

This year, that trend collided with an inflation spike that outpaced wage gains by two percent. Faced with diminished purchasing power, households are making budget tradeoffs which explicitly pit healthcare against other essential household needs.

For some, this cost-cutting impulse even extends to preventative screenings—required to be covered without cost-sharing—when consumers’ financial concerns drive them to avoid healthcare altogether.

While the latest inflation report suggests price increases are moderating, fears of a broader recession persist, making it critical for health systems and physicians to communicate with patients, encouraging them to continue to access preventive care, educating them about lower cost care options, and helping them prioritize treatment that should not be put off.

The demise of Haven — a coalition of three big employers aiming to lower the cost of healthcare for their workers — was met with a surprising reaction from Jamie Dimon, CEO of JPMorgan Chase: “We want to do this again.”

A Dec. 6 report from Bloomberg details some of the aftermath of Haven’s end and also the origins of Morgan Health, the bank’s second go at lowering healthcare costs that was rolled out in spring 2021. While still in its early stages, one tenet of its strategy is a return to basics, including appointments between clinicians and patients that take at least 30 minutes if not an hour.

Haven was the healthcare partnership formed in 2018 by Amazon, JPMorgan Chase and Berkshire Hathaway with an aim to lower healthcare costs for their 1.2 million workers. It disbanded in 2021. As its end neared, Mr. Dimon set out to learn what had gone wrong.

When he asked the question of Bill Wulf, MD, CEO of Central Ohio Primary Care, the internist told the businessman the initiative had moved too slowly. A virtual care program drew in only 150 people in Ohio, for example, before it was scrapped.

Shortly after the debrief with Dr. Wulf, Mr. Dimon assigned a lieutenant to restart the work on lowering employer healthcare costs, this time focusing on JPMorgan Chase alone. That leader was Peter Scher, vice chairman with the bank, who had his doubts at first. “There are a lot of things we could be spending our time on,” he told Bloomberg. “I was perfectly prepared to go back to Jamie and the operating committee and say, ‘Listen, it was a good try.'”

Mr. Scher stuck with it and brought on Dan Mendelson, founder and former CEO of healthcare advisory group Avalere Health, to lay the groundwork for JPMorgan’s second healthcare attempt. Mr. Mendelson, who had been a skeptic of Haven, spent three months crafting a strategy and playbook that recognized where Haven had fallen short and avoided repeated mistakes. He signed on to lead the group, dubbed Morgan Health.

The group has made more headlines since its launch than its predecessor Haven, which premiered with much bravado but went nearly a year without releasing any news except for its name and a new website. In fall 2022, Morgan Health openedthree advanced primary care centers in Ohio for a total of five and formed a healthcare venture capital team targeting early- to later-stage healthcare companies with innovations in areas like genetic medicine, autoimmune diseases, cardiometabolic diseases and rare disorders. It also hired Cheryl Pegus, MD, Walmart’s executive vice president of health and wellness, as a managing director.

Morgan Health’s strategy is marked by what appears to be common sense and a return to basics, including the placement of clinics in office building atriums — “a full-service practice where employees can develop long-term relationships with primary-care providers, wellness coaches, mental health providers and care coordinators.”

All appointments are booked for at least 30 minutes with many going an hour, according to Bloomberg. Patients generally see the same practitioner for each visit to build long-term relationships. Clinicians’ payments are tied to goals like avoiding emergency room visits, providing cancer screenings and keeping high blood pressure in check. If it plays out as designed, JPMorgan says the investment in prevention and primary care will curb high-cost services and hospital stays, ultimately leading to meaningful savings.

The goal is to “identify high-risk patients and then bubble-wrap them,” Dr. Wulf told Ohio business leaders in an October meeting, Bloomberg reports. “How do we keep you out of the hospital?”

JPMorgan has opened five clinics in the area of Columbus, Ohio, which will also be open to other employers who want to sign on. The clinics and primary care centers are managed and staffed by Vera Whole Health and Central Ohio Primary Care. JPMorgan is seeking “like-minded” medical groups in markets like New York, Chicago and Dallas where it has hubs of workers, Bloomberg reports.

VillageMD, which is majority owned by Walgreens Boots Alliance, plans to shell out nearly $9 billion to pick up medical practice Summit Health, the parent company of urgent care clinic chain CityMD.

The deal, announced Monday morning, is valued at $8.9 billion and includes investments from Walgreens Boots Alliance and Cigna Corp’s healthcare unit Evernorth, which will also become a minority owner in VillageMD. Bloomberg first reported on a potential deal back in late October.

The deal will expand Walgreen’s reach into primary, specialty and urgent care. The transaction creates one of the largest independent provider groups in the U.S., the organizations said. Combined, VillageMD and Summit Health will operate more than 680 provider locations in 26 markets. The two companies will have 20,000 employees.

Walgreens said Monday it will invest $3.5 billion through an even mix of debt and equity to support the acquisition, which is expected to close in the first quarter of 2023. The company will remain the largest and consolidating shareholder of VillageMD with about 53% stake.

Walgreens also raised its fiscal year 2025 sales goal for its U.S. healthcare business to between $14.5 billion and $16 billion from $11 billion to $12 billion previously. That business segment is now expected to achieve positive adjusted EBITDA by the end of fiscal year 2023.

Last year, Walgreens invested $5.2 billion in VillageMD and said it planned to open at least 600 Village Medical at Walgreens primary-care practices across the country by 2025 and 1,000 by 2027.

The deal comes amid a frenzy of M&A activity in the past two years. Major retailers like CVS, Walgreens and Amazon are ramping up their focus on providing medical services to gain bigger footholds in the healthcare market.

Drugstore rival CVS Health won the bidding war for home health and technology services company Signify Health and plans to shell out $8 billion to acquire the company. Amazon also plans to buy primary care provider One Medical for $3.9 billion.

The M&A move signals that Walgreens wants to become a “dominant entity in the overall healthcare services ecosystem,” according to David Larsen, healthcare IT and digital health analyst at financial services firm BTIG.

“Walgreens Boots Alliance is graduating up from being a drug retail store to owning the life-cycle of members’ health,” he wrote in an analyst’s note. “We view this transaction as being a statement by the market that primary care continues to be one of the key drivers of healthcare long-term.”

The deal also will put additional pressure on CVS Health to break into the primary care business “sooner rather than later,” Larsen wrote.

“I think at the most strategic level, I think there continues to be recognition that an integrated, coordinated, connected model of care is one that will ultimately deliver the best results. You see this through Optum’s acquisition of Kelsey-Seybold Clinic and VillageMD’s acquisition of Summit Health,” Tim Barry, CEO and chair of VillageMD, said in an interview with Fierce Healthcare.

“If we’re going to ultimately stem the rising tide of this fee-for-service healthcare system, we need a better solution, and that solution needs to have doctors working with other doctors in a coordinated way and trying to solve the unique problems that these patients have and making sure that the right doctors are accessing the patient at the right time, and doing it all underneath the umbrella of a risk-based contract,” Barry said.

He added, “We think that this is going to continue to be where healthcare goes. And, we have to do it in a way that is integrated and value-oriented. Any organization focused on doing that, and doing that at size and scale, is going to continue, I think, to be the successful winners of our healthcare system.”

In 2019, Summit Medical Group, a physician-owned and governed multispecialty group, merged with CityMD, a leading urgent care company in New York City. The combined organization, Summit Health, has more than 370 locations in New Jersey, New York, Connecticut, Pennsylvania and Oregon.

VillageMD provides value-based primary care for patients at traditional free-standing practices, Village Medical at Walgreens practices, at home and via virtual visits. VillageMD and Village Medical have grown to 22 markets and are responsible for more than 1.6 million patients, according to the company.

Barry said the combination of VillageMD and Summit Health-CityMD will enable the organizations to scale up value-based care and build out integrated primary and specialty care services.

“If you look at the long history of Summit Health, it’s an organization that has done some very innovative things. The way that they deliver multispecialty care, it is truly integrated, it’s truly connected and they are known as the preeminent brand in their marketplace. They also have CityMD, which is one of the more unique and differentiated urgent care models out there in the market. They really are a best-of-breed organization,” he said.

“When I look at what we’ve been able to do at VillageMD, we built this incredible model of value-based primary care delivery. The idea of bringing these two organizations together to bring those best-of-breed capabilities under one umbrella was just so compelling. We will soon be able to offer a more comprehensive, integrated and connected model by also offering other specialty services to our patients, but all still done through a value or risk-based reimbursement structure.”

Barry is bullish on the combined capabilities of the two companies in the primary and specialty care markets.

“We’ll be delivering a consistent value-based model of integrated, multispecialty care in a way that delivers the best clinical results on the planet,” he said.

Jeff Alter, CEO of Summit Health-CityMD, said in a statement that the deal adds Summit Health’s expertise and geographic coverage to VillageMD’s proven value-based primary care approach.

The acquisition also expands Walgreens’ reach into providing medical care directly to patients. “This transaction accelerates growth opportunities through a strong market footprint and wide network of providers and patients across primary, specialty and urgent care,” Roz Brewer, CEO of Walgreens Boots Alliance, said in a statement.

With Cigna’s investment, the combined company will be able to tap into Evernorth’s health services capabilities to potentially lower healthcare costs, Barry said. Evernorth encompasses Cigna’s health services businesses including pharmacy benefit manager Express Scripts

“In order to be a risk-based provider or a value-based provider, you have to have contracts with a payer that allows you to work in this value or risk-based construct. We learned over the years that Cigna has been a really good partner to us on that journey,” Barry said.

“There are companies that [Cigna] has purchased over the years that have different specializations and capabilities that we believe ultimately will allow us to deliver better care to our patients,” he noted. “Evernorth has some capabilities tied to behavioral health, and they have some capabilities tied to the management of specialty pharmaceutical spend, which everyone knows those costs continue to be soaring. We both liked the idea of supporting an organization like ours that’s going to continue to grow and continues to be focused on risk and value.”

With the investment in VillageMD and Summit Health, Cigna gets a leg up in the primary care space as it looks to build out its Evernorth division.

“Our collaboration with VillageMD accelerates our efforts to improve the way care is accessed and delivered,” said Eric Palmer, CEO of Evernorth, in a statement. “Harnessing the breadth of Evernorth’s health services capabilities and connecting them with physicians who provide care in a value-based model like VillageMD, helps more people to get the right care at the right time—driving better health and value.”