Cartoon – What about the Short-term?

Robert Wood Johnson University Hospital in New Brunswick, N.J., said it plans to temporarily cut off healthcare benefits for striking union workers, effective Sept. 1.

Hospital spokesperson Wendy Gottsegen described the move as unfortunate.

“We have said all along that no one benefits from a strike — least of all our nurses. We hope the union considers the impact a prolonged strike is having on our nurses and their families,” Ms. Gottsegen said in an Aug. 28 news release shared with Becker’s. “As of Sept. 1, RWJUH nurses must pay for their health benefits through COBRA. This hardship, in addition to the loss of wages throughout the strike, is very unfortunate and has been openly communicated to the union and the striking nurses since prior to the walkout on Aug. 4.”

The ongoing strike involves the United Steelworkers Local 4-200, which represents about 1,700 nurses at the facility.

Union members voted to authorize a strike in July. The union and hospital have been negotiating a new agreement for months, with the last bargaining session occurring Aug. 16.

During negotiations, the union has said it seeks a contract that provides safe staffing standards, living wages and quality, affordable healthcare.

Local 4-200 President Judy Danella, RN, said in a previous union release, “Our members remain deeply committed to our patients. However, we must address urgent concerns, like staffing. We need enough nurses on each shift, on each floor, so we can devote more time to each patient and keep ourselves safe on the job.”

Several nurses told TAPinto New Brunswick last week that they began preparing for the current situation ahead of the strike, taking overtime shifts and saving as much money as possible. Others told the publication they are taking part-time jobs or temporary employment elsewhere in the nursing field or adjacent roles.

“I think it’s important that you [remember] you might not get the job you want to do at that moment, but people have to do what they have to do to get it done,” Jessica Newcomb, RN, told TAPinto New Brunswick.

Meanwhile, the hospital has contracted with an agency to hire replacement nurses during the strike.

“As always, our top priority is to our patients. RWJUH is open, fully operational and completely staffed, and we remain steadfast in our commitment to deliver the highest quality and always-safe patient care,” Ms. Gottsegen said.

As of Aug. 28, no further dates for negotiations were scheduled by mediators.

Faced with tighter margins and continued rising costs, many health system C-suites are restructuring. At least 17 health systems have reorganized executive teams and some eliminated C-suite roles.

The chief operating officer role in particular has been on the chopping block for health systems but not everyone is slimming down.

Some are bulking up amid organizational transformation with an eye on the future.

In June, Sutter Health in Sacramento, Calif., named Todd Smith, MD, its inaugural senior vice president and chief physician executive, responsible for supporting the health system through clinical transformation. Dr. Smith will focus on service line standards, reducing variation and strengthening the system’s relationship with medical group and community physicians.

Sutter isn’t the only system adding clinical leaders to the C-suite. Mass General Brigham in Somerville, Mass., named Erica Shenoy, MD, PhD, its first chief of infection control in June. Her expanded role is accountable for leading the integration of infection control at the system and developing and implementing infection control standards, policies and measurements. She was also appointed to the National Infection Control Advisory Committee to guide HHS earlier this year.

Meritus Health in Hagerstown, Md., added physician leadership to its executive team. Adrian Park, MD, became the system’s first chief surgical officer with responsibility for building a surgical program with advanced technology and minimally invasive procedures to the system. He is known for surgical innovation in laparoscopic techniques, and holds more than 20 patents.

MaineHealth in Portland recently added Chris Thompson, MD, to the C-suite as the system’s first chief medical transformation officer. He is responsible for chief medical officer duties as well as innovating in care delivery.

Richmond, Va.-based VCU Health and OU Health in Oklahoma City named their first chief nursing executives as well earlier this year.

Health systems are also adding strategic experts with expertise in patient experience, transformation and data analytics.

Atlanta-based Emory Healthcare created a new role for Amaka Eneanya, MD, to serve as chief transformation officer, accountable for enhancing patient and clinician experiences. She took on the role in July and is tasked with developing systemwide strategies to boost patient experience, improve access to care, increase community engagement and enrich clinician experience. Dr. Eneanya works with the system’s diversity, equity and inclusion office to prioritize strategies for health equity, diversity and inclusion in care delivery as well.

“Amaka is a forward-thinking leader who is well versed in transformational strategy and operational structure and will help us move Emory Healthcare to the next level,” said Joon S. Lee, MD, CEO of Emory Healthcare. “We look forward to working with her in our continued pursuit to transform and strengthen patient access and the patient experience.”

Last year, Centura Health in Centennial, Colo., also added a chief transformation officer, Scott Lichtenberger, MD, as a new position to balance short-term improvements and long-term value. He is responsible for ensuring the system delivers results quickly.

Finally, Cleveland Clinic has elevated another IT leader into the C-suite in recent weeks. Albert Marinez was named the system’s first chief analytics officer, set to begin his new role Aug. 28. He previously served as chief analytics officer of Intermountain Health in Salt Lake City, and will be responsible for overseeing data strategies for better patient care and lower costs at Cleveland Clinic. He will also have accountability for boosting the system’s growth alongside chief digital officer Rohit Chandra, PhD.

https://mailchi.mp/27e58978fc54/the-weekly-gist-august-11-2023?e=d1e747d2d8

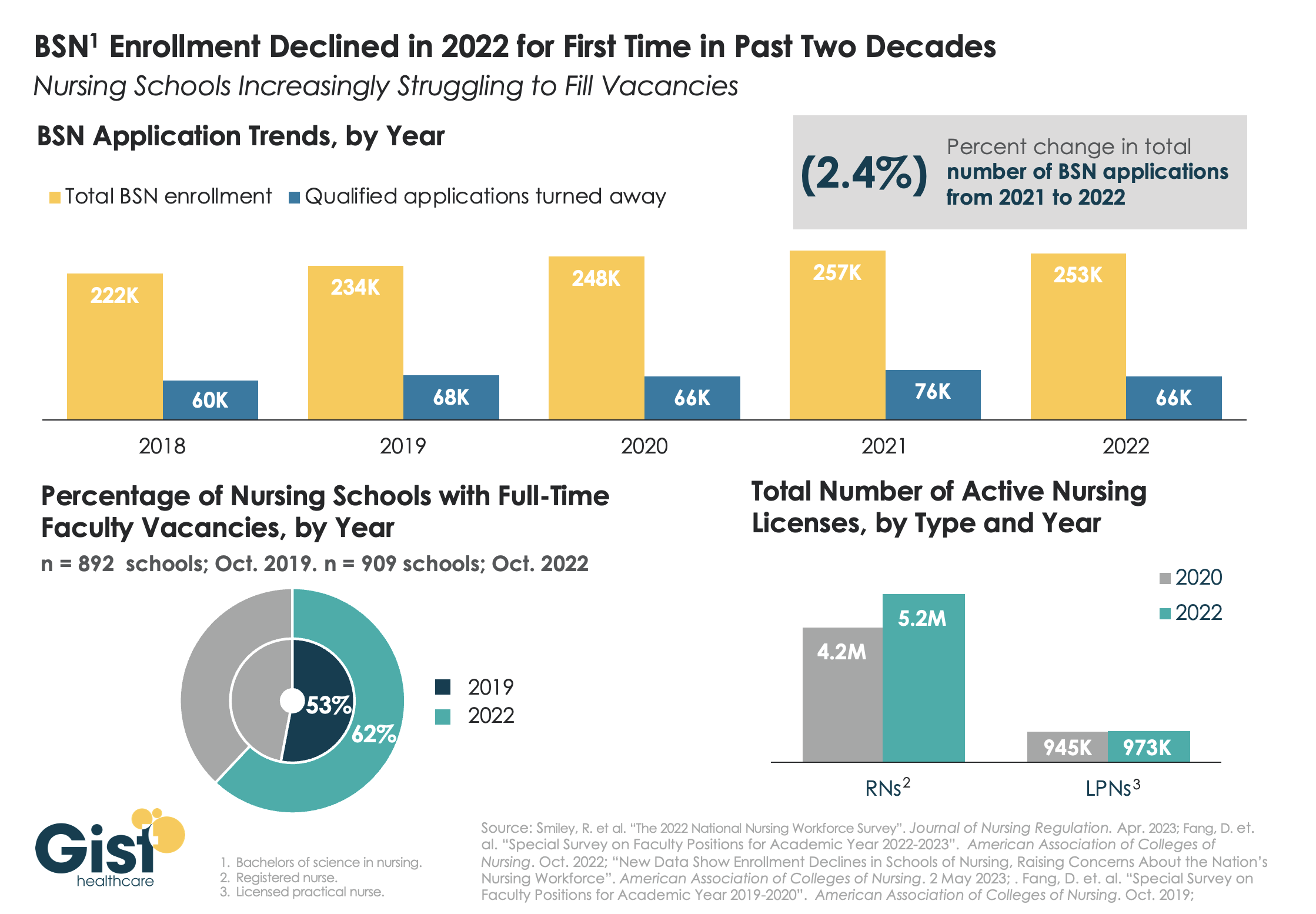

While last week’s graphic looked at how a wave of retirements has hit the nursing workforce, this week we take a look at the pipeline of nurses in training to fill that gap. In recent years, there has been a consistent stream of qualified applicants who want to become BSN nurses, but schools don’t have the capacity to admit them.

One reason: an ongoing shortage of nursing faculty, which recent retirements have exacerbated. The percentage of nursing schools with at least one full-time faculty vacancy grew from 53 percent in 2019 to 62 percent in 2022.

Looking at registered nurses (RNs), the number with active licenses has continued to grow at a much higher rate than the supply of licensed practice nurses (LPNs) with active licenses.

The relatively small LPN workforce is especially significant, given rising interest in team-based nursing care, which aims to utilize a higher number of LPNs, supervised by RNs and BSNs.

Expanding training programs with an eye toward the skills and mix needed to deliver team-based care will be critical to ensuring a stable, efficient nursing workforce for future decades.

https://mailchi.mp/377fb3b9ea0c/the-weekly-gist-august-4-2023?e=d1e747d2d8

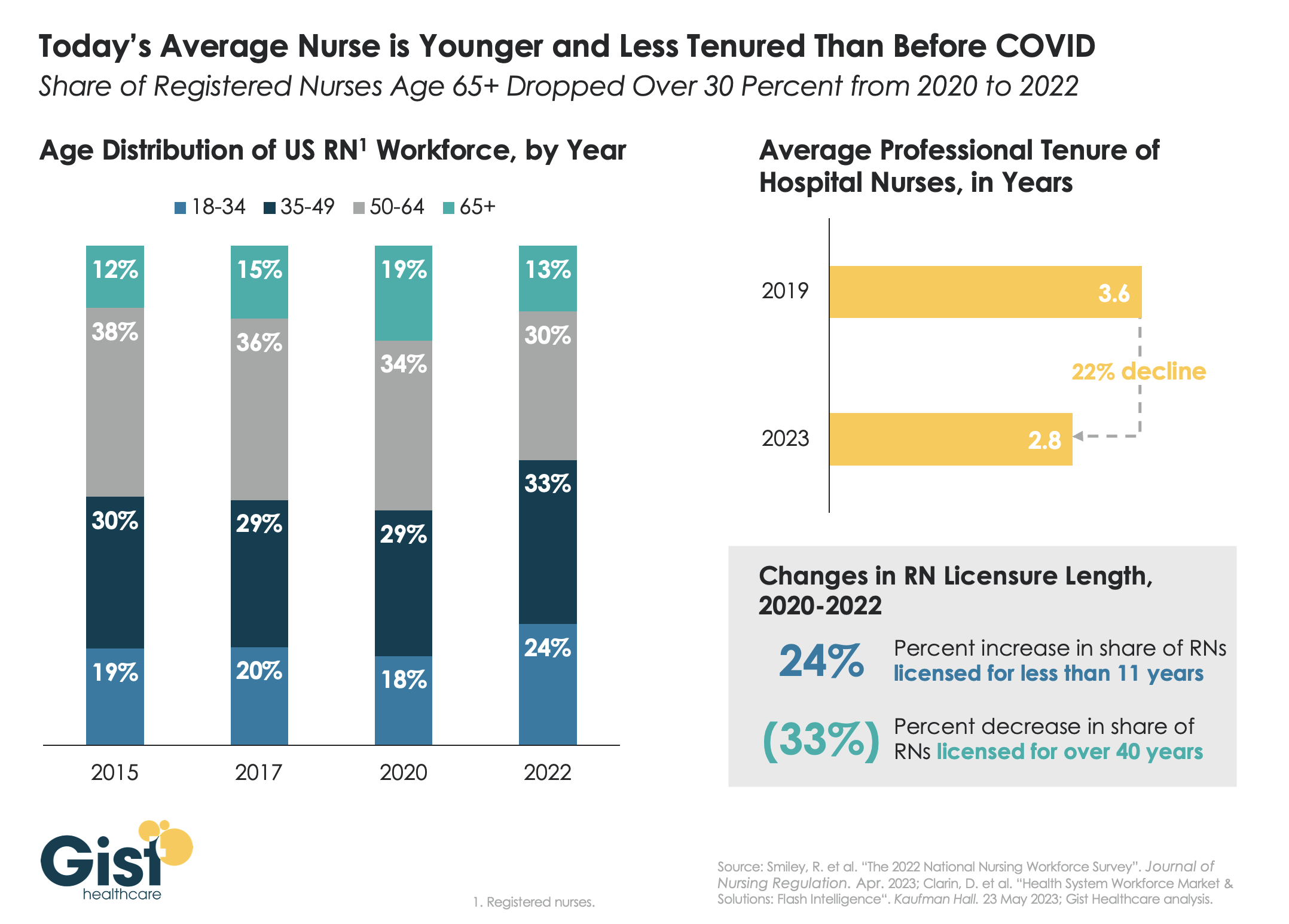

Last week we discussed how hospitals are still struggling to retain talent. This week’s graphic offers one explanation for this trend:

a significant share of older nurses, who continued to work during the height of the pandemic, have now exited the workforce, and health systems are even more reliant on younger nurses.

Between 2020 and 2022, the number of nurses ages 65 and older decreased by 200K, resulting in a reduction of that age cohort from 19 percent to 13 percent of the total nursing workforce. While the total number of nurses in the workforce still increased, the younger nurses filling these roles are both earlier in their nursing careers (thus less experienced), and more likely to change jobs.

Case in point:

From 2019 to 2023, the average tenure of a hospital nurse dropped by 22 percent. The wave of Baby Boomer nurse retirements has also resulted in a 33 percent decrease from 2020 to 2022 in the number of registered nurses who have been licensed for over 40 years.

Given these shifts, hospitals must adjust their current recruitment, retention, training, and mentorship initiatives to match the needs of younger, early-career nurses.

https://www.commercehealthcare.com/trends-insights/2023/healthcare-finance-trends-for-2023

This annual look at high-impact trends affecting healthcare in the coming year is based on evaluation of current industry research data. Healthcare Finance Trends for 2023 (Trends) explores eight themes identified by CommerceHealthcare® ranging across four areas:

This report’s consistent message is that these trends intersect in ways that compound both the challenges and the upside potential of strategies that address them.

Healthcare’s financial predicament for the next 12–18 months is being described in strong terms. Citing $450 billion of EBITDA that could be in jeopardy, more than half of the industry’s project profit pool by 2027, one analyst suggests “a gathering storm.” Another perceives “broad and serious threats” as “elevated expenses” erode margins and exact “a profound financial toll.” Fitch Ratings issued a “deteriorating” outlook for nonprofit health systems.

These financial headwinds are upending healthcare’s traditional status as “recession-proof.” It is helpful to probe the multiple forces in play, the urgent workforce management challenge, and the varied solution set.

Observing that margins will be down 37% in 2022 relative to pre-pandemic, a recent stark assessment concluded, “U.S. hospitals are likely to face billions of dollars in losses — which would result in the most difficult year for hospitals and health systems since the beginning of the pandemic.”

A confluence of factors is exacerbating the stress for 2023:

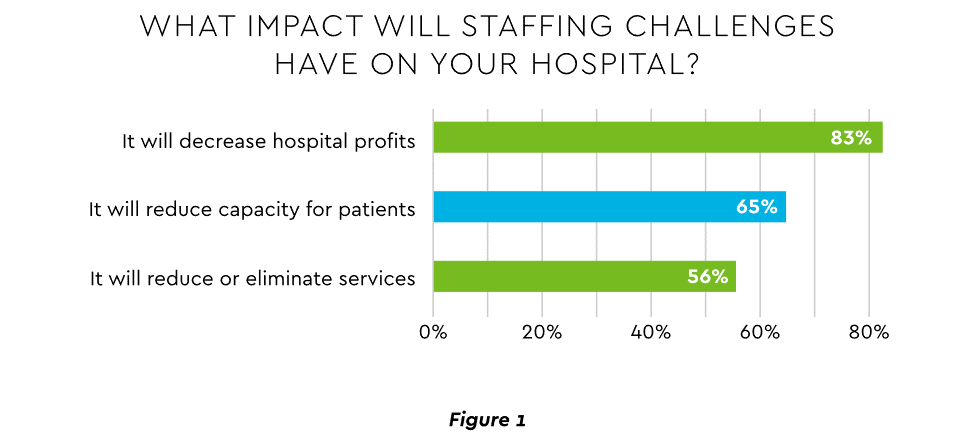

Burnout and shortages have disrupted the clinical workforce. Nearly 60% of physician, advanced practice provider and nurse survey respondents said their teams are not adequately staffed, and 40% lack resources to operate at full potential. Many providers face extreme to moderate shortages of allied health professionals.

The problem extends beyond the clinical. A survey saw 48% of respondents experiencing severe labor deficiencies in revenue cycle management (RCM) and billing, and one in four finance leaders must fill over 20 positions to be fully staffed.

An executive outlook highlighted demonstrable impact on financial performance and growth from these workforce problems, citing reductions in profitability, capacity and service (Figure 1).1

View PDF of Figure 1 chart[PDF]

Several studies detail negative outcomes:

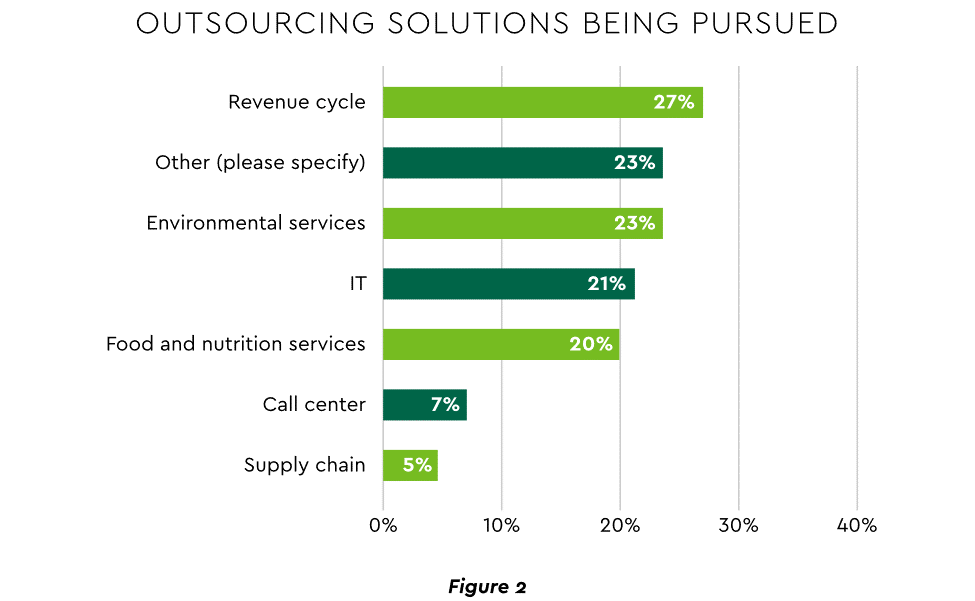

Health systems, hospitals and practices will vigorously pursue at least four direct actions to overcome the financial and staffing hurdles:

View PDF of Figure 2 chart[PDF]

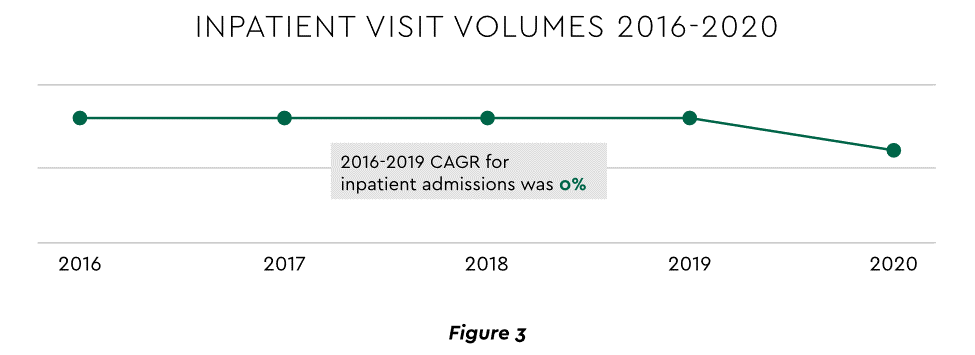

Pursuing top line growth in tandem with reining in expenses is essential. Inpatient volume growth has been tepid for several years ─ essentially flat in the 2016–20 period (Figure 3).

View PDF of Figure 3 chart[PDF]

Leaders have been pivoting to outpatient and virtual care to diversify revenue streams. Two high-potential 2023 growth tracks in this sector merit deeper assessment.

Considerable evidence attests to strong commitment to telehealth and remote care. Sixty-three percent of physicians worldwide expect most consultations to be performed remotely within 10 years. Approximately 40% of health centers are using remote patient monitoring today. Consumers are also positive: 94% definitely or probably will use telehealth again, 57% prefer it for regular mental health visits and 61% use it for convenient care.

Telehealth is still in early stages of maturity. Only 4% of surveyed top executives consider their organization proficient at implementing remote care. Healthcare is also recognizing that a full telehealth ecosystem must be constructed. A physician leader explained that the industry’s early telehealth incarnations failed to build “virtual-only environments or really drive e-consults as a way of doing things.” A vital ecosystem demands alterations to current contracts, coding, collections, patient financing, staff training and other business practices.

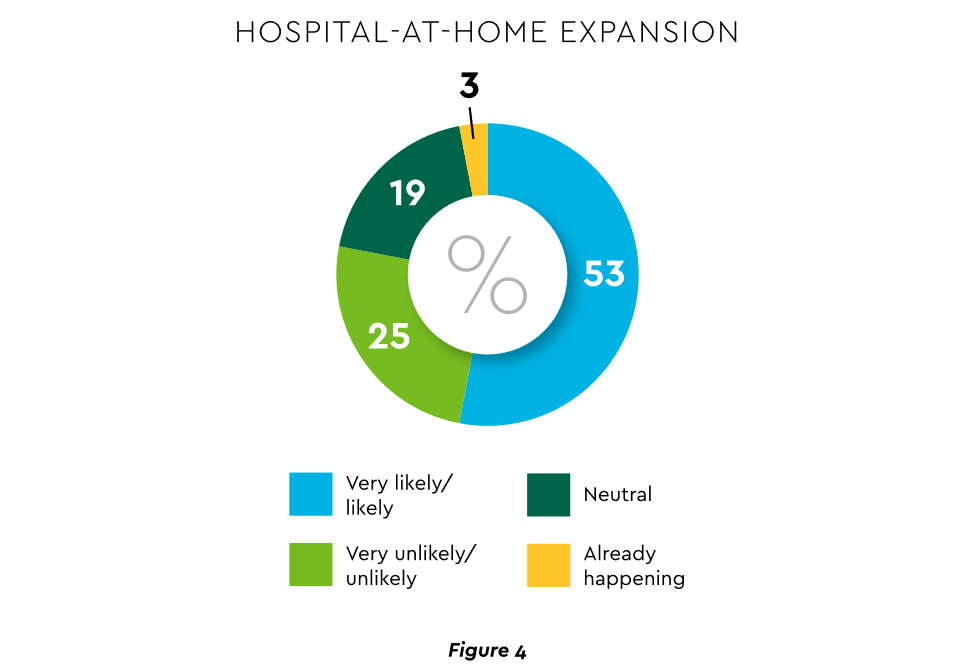

Health systems see particularly promising growth in the provision of acute care in patients’ home settings, including post-surgical and cancer treatment. The federal government has already allowed waivers to 114 systems and 256 hospitals to obtain inpatient-level reimbursement for acute care at home. However, these waivers were prompted by the pandemic and are slated to end in early 2023. The renewal uncertainty has stymied some activity and represents an overhang on the opportunity. However, enthusiasm appears strong, and 33% of hospitals in a recent poll said they would be prone to continue HaH even without renewal.

The forecasts are encouraging. Over half of hospitals believe it likely they will utilize HaH for at least half of their chronically ill patients over the next several years (Figure 4).

View PDF of Figure 4 chart[PDF]

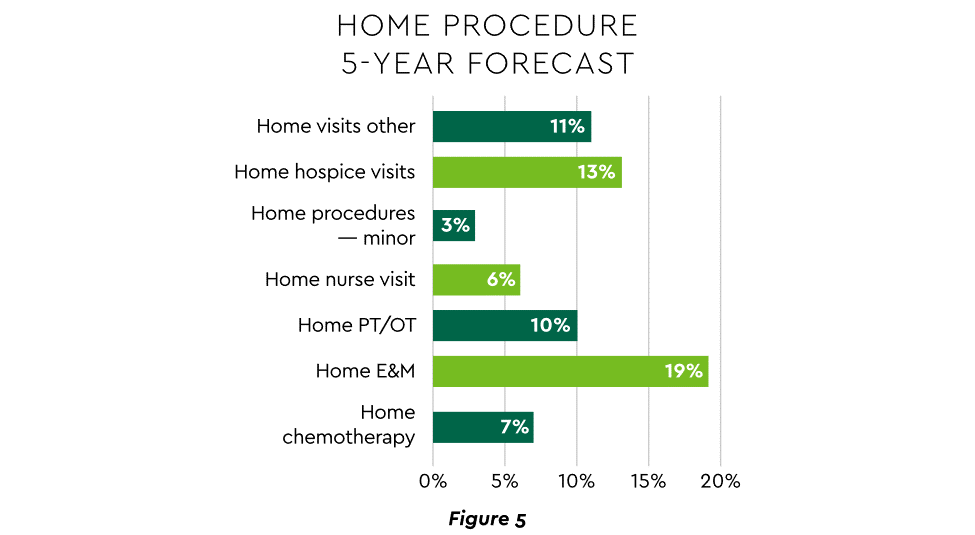

HaH exists within a broader matrix of home care, and solid growth is anticipated across the range of home procedures (Figure 5).

View PDF of Figure 5 chart[PDF]

Harvesting the HaH potential will require implementation of current and emerging enabling technologies in remote monitoring, high-speed networks and artificial intelligence that generates algorithmic guidance for caregivers and patients alike.

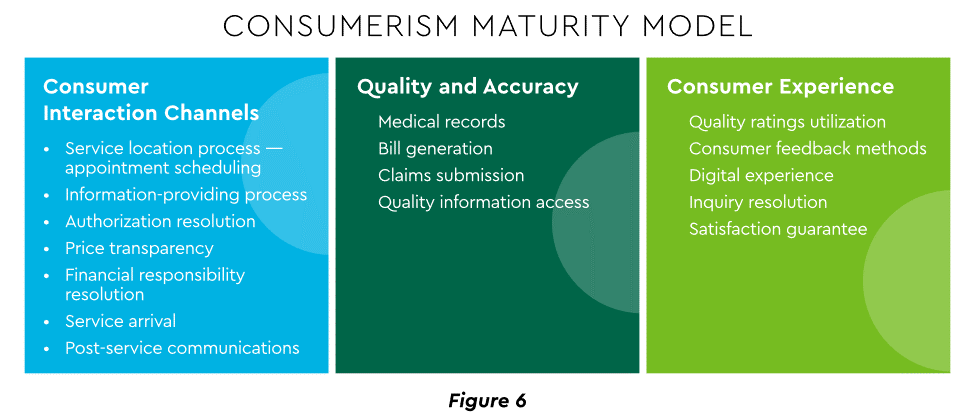

Today’s healthcare market dynamics place a premium on positive patient experiences. The goal is to deliver “an empathetic relationship between customers and brands built on what the customer wants and how they want to be treated.” It is a complex undertaking, with numerous touchpoints as captured in HFMA’s Consumerism Maturity Model (Figure 6).

View PDF of Figure 6 chart[PDF]

An array of studies underscores the value proposition for intense provider focus on patient financial experience:

Significantly improving the financial experience requires a unified strategy, not just a collection of individual initiatives. Three threads to such a strategy will be prominent in 2023.

Organizations have been moving swiftly to channel many patient financial transactions through an integrated Digital Front Door (DFD). This approach offers patients a singular online point of access and intelligent navigation to needed services.

Growth is accelerating. A DFD is their patients’ first contact point for 55% of responding organizations, according to one technology survey. A leading forecaster sees 65% of patients engaging services via digital front doors by 2023.

Mandates for full price transparency and “no surprises” billing are in effect, but estimates of compliance are mixed. An analysis of 2,000 hospitals determined that only 16% met the requirement to post an online “machine readable” file displaying clear charges for 300 “shoppable services.” Another assessment showed a more substantial 76% of hospitals had posted files, and 55% were deemed “complete.” One provision of interest to practices is the “good faith estimate” of expected charges required to be given to uninsured and self-pay individuals when they schedule visits.

CommerceHealthcare® has worked with clients to enhance the patient financial experience by complementing their website pricing data with clear information on patient financing options and enrollment access. Bill pay information can also be added for one-stop guidance.

Beyond choice and convenience, the deeper objective is truly personalized experiences throughout the care journey. The words of leading analysts best define the drive to personalize:

Opportunities abound to personalize the patient financial experience. Automating manual processes establishes a foundation. Patient financing with no- or low-interest credit lines and flexible terms can produce monthly payment schedules tailored to each patient’s needs. Refunds can be made through multiple payment modes to meet varying patient preferences.

Emphasizing patient financing as part of the overall experience is powerful. Patients continue to struggle paying for care. Recent granular data details three related forces at work.

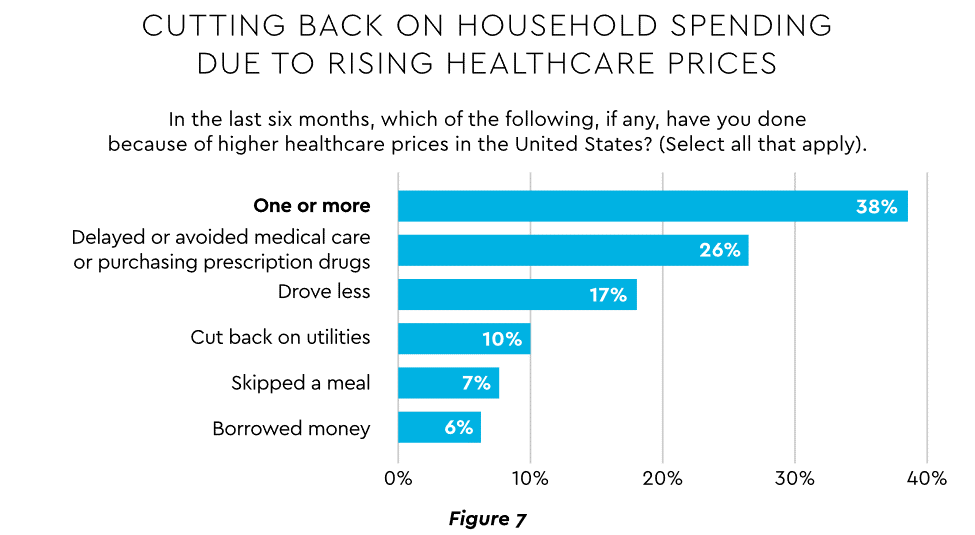

Commonwealth Fund found that 42% of individuals had problems paying medical bills or were paying off medical debt during the past year, while 49% were unable to pay an unexpected

$1,000 medical bill.42 Health costs trigger reduction in a range of personal expenditures, led by deferring or avoiding care and drugs (Figure 7).

View PDF of Figure 7 chart[PDF]

Twenty-eight percent of Americans now describe themselves as less prepared than last year to pay for routine or unanticipated care.

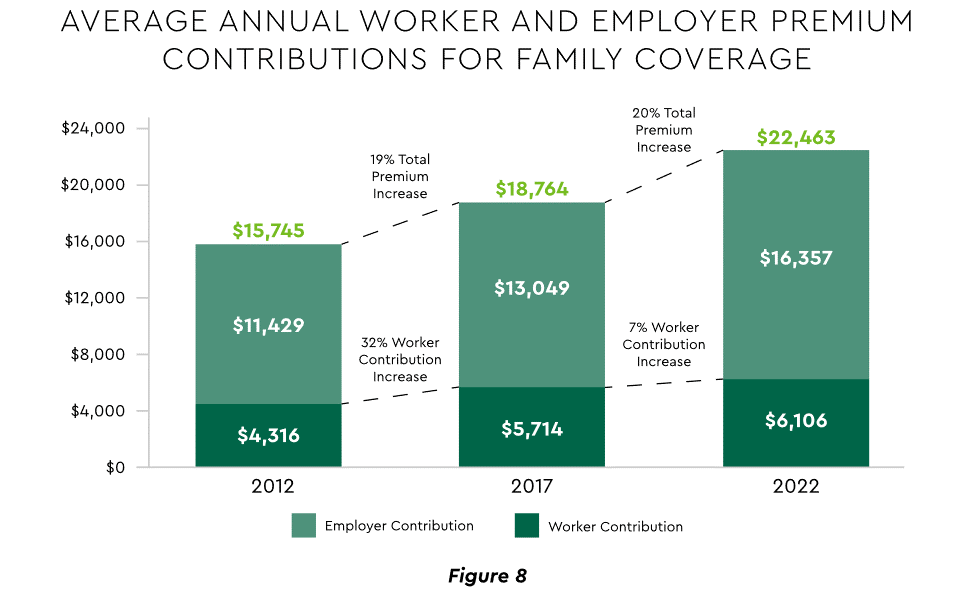

Patient obligation continues its upward march. Insurance premiums have climbed steadily for both the insured and their employers, and employees now pay over $6,000 annually on average for family coverage (Figure 8).45

View PDF of Figure 8 chart[PDF]

High deductible health plans (HDHP) also place substantial burden on the patient. Through 2021, 28% of workers were enrolled in an HDHP with an average family deductible of $4,705. Employer satisfaction with these plans is high, auguring further expansion.

Patient payment difficulties are clearly impacting provider financials. A recent in-depth analysis uncovered substantial self-pay issues:

Multiple chronic conditions add to the problem. A recent extensive analysis concluded: “Among individuals with medical debt in collections, the estimated amount increased with the number of chronic conditions ($784 for individuals with no conditions to $1,252 for individuals with 7–13).”

For their part, providers will be encouraged to broaden patient financing programs. Patients are certainly interested. When asked, 62% of consumers indicated they would use financing options or creative payment plans if available for large bill amounts. Many health systems, hospitals and practices will turn to outside help to satisfy the demand. A recent analysis recommended that health systems “consider keeping shorter-term payment plans in-house and extended term plans through external partnerships.”

Organizations will also need to step up their communications. A survey revealed that 64% of patients were unaware that their doctors and hospitals offered payment plans or financial help.

Trust has emerged as a paramount issue today for most organizations as they encounter an “imperative to build trust and transparency among different stakeholder groups — employees, customers, suppliers, regulators and the communities in which they operate.” Healthcare is no exception, and the trust issue is growing in both complexity and urgency.

Trust in healthcare took a hit from the COVID-19 experience. A spring 2022 HFMA survey recorded 44% of finance leaders saying they perceived decreased patient trust. Between April 2020 and December 2021, the percentage of Americans who trusted information from doctors “a great deal” declined by 23%, from hospitals 21%, and from nurses 16%. The patient financial experience also faces “drivers of mistrust,” according to surveyed leaders who cited general payment confusion (58%), surprise billing (39%), high prices of commodity items (28%) and lack of price transparency (26%). Building trust reaps dividends. People who trust their providers are five times more likely to stay with them than those who are neutral or distrustful.

Industry experts promote several approaches to galvanize trust among all constituencies:

A provider’s banking relationship can yield valuable collaboration in the trust-building endeavor. Banks enjoy solid trust among consumers. As an example, 53.4% of consumers rated banks as most trusted to provide payment “super apps” and financial digital front doors ─ exceeding the next closest source by 10 points.

Cybersecurity is part of the trust calculus and has become an evergreen topic in healthcare. Compromised data and ransomware attacks are ongoing and leaders must continually refine their understanding in at least three areas: the overall security landscape, particular financially related considerations and contemporary security defenses.

The latest statistics quantify the cyber assault on healthcare:

Finance leaders will also need awareness of the following:

Beyond a host of management and monitoring tools being deployed, a strategic philosophy is rapidly gaining ground. The “zero trust” model sounds counter to the trust-building mindset described earlier, but it has become essential. It “denies access to applications and data by default,” and 58% of hospitals and health systems have a zero trust initiative in place. Another 37% intend to implement one within 12–18 months.

Cybersecurity investment will challenge CFOs in 2023, especially in areas such as talent. Cybersecurity worker availability is estimated to satisfy only 68% of open positions. Banking partners will also be expected to play an important role. Over the years, major banks have become “leaders in enhancing cyber strategy and investing in cyber defenses, processes and talent.”

Digital transformation is fundamental to healthcare’s business and care delivery model changes. IBM’s website succinctly captures the goal, “Digital transformation means adopting digital-first customer, business partner, and employee experiences.” A leading forecaster believes 70% of healthcare organizations will rely on digital-first strategies by 2027.

Transformation efforts need to accelerate. One study showed that “digital, technology and analytics strategies exist for nearly all organizations, yet only 30% have begun to execute on those plans.”

One functional segment ramping up digital transformation is finance. According to a recent survey, 94% of CFOs and senior leaders stated that such efforts will be at the forefront of financial operations and strategy for 2023–2024, and 79% described it as an “absolute need” for “commercial stabilization and long-term survival of their healthcare organization.”

Advanced technology is gaining traction. Many see optimization in combining robotic process automation (RPA), artificial intelligence and machine learning to create “intelligent automation.” Together, these technologies create algorithms to automate decisions that guide “robotic” software to perform financial actions and thereby reduce manual labor.

Getting to digital-first in finance and across the enterprise has several critical success factors. These include sustained commitment, a platform-centric mindset and effective governance.

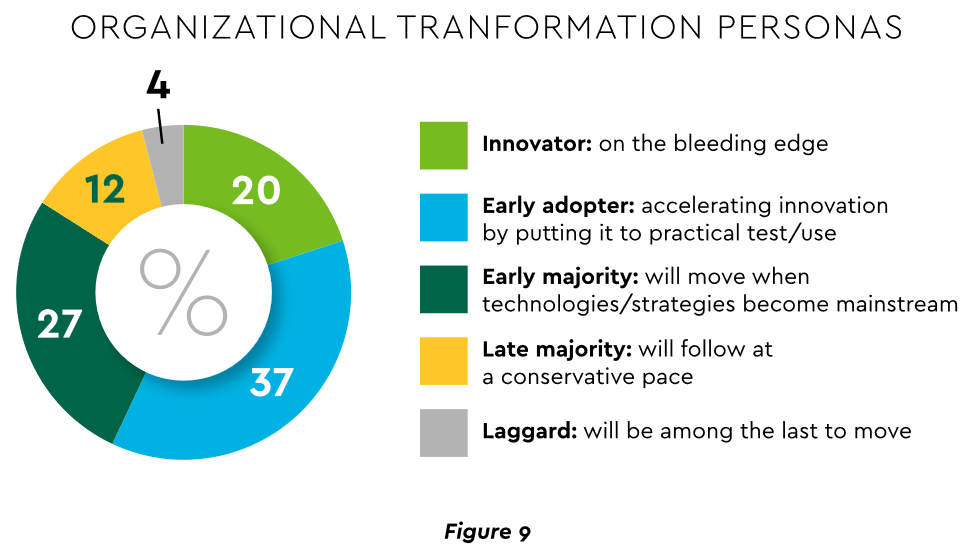

Some assert that few healthcare executives have “created digital strategies that look far enough into the future.” Speed of change is also important. Health systems, hospitals and practices exhibit varying risk appetites and change rates. When asked to self-identify “transformation personas,” a little over half regarded themselves as being on the innovative “early mover” end of the spectrum, while the remainder will adapt as technologies prove themselves (Figure 9). Slower organizations will likely need to increase the pace.

View PDF of Figure 9 chart[PDF]

Implementing enterprise platforms rather than proliferating “point solutions” is obligatory. Organizations must be “prepared to compete in the platform economy as platform-based business models have changed the way we live, work and receive care.”

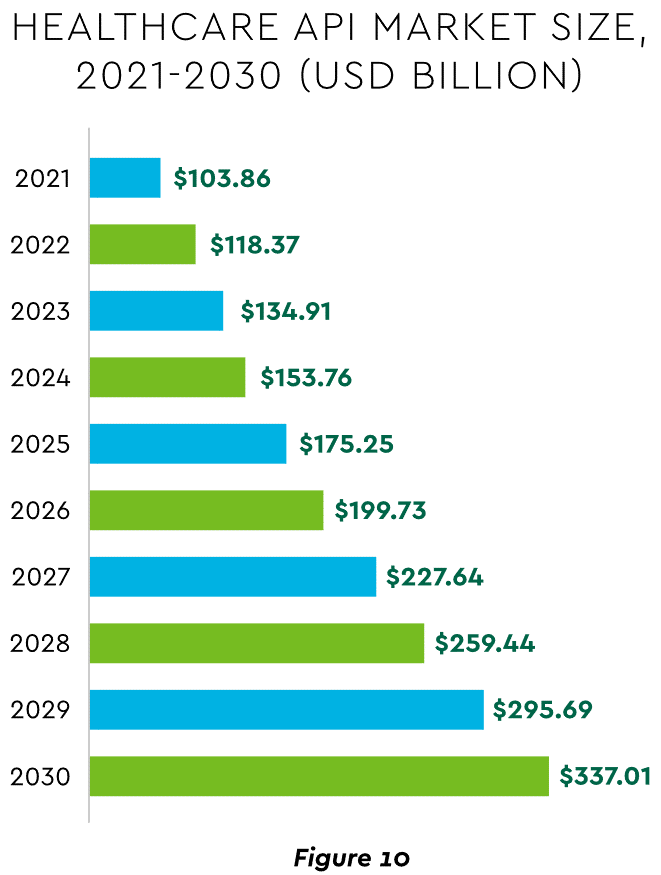

There are still too many tools and applications. A survey of top decision-makers at health systems found that 60% use over 50 software solutions just in operations (24% have over 150). System integration is one answer. Use of application programming interfaces (API) helps this effort substantially. API-first is fast becoming the norm among solution providers, with global API investment expected to nearly triple by 2030 (Figure 10)

View PDF of Figure 10 chart[PDF]

Effective governance is vital to constructing a platform-based transformative model and to ensuring wide user adoption. Healthcare has seen the rise of new senior roles such as Chief Digital Officer and Chief Transformation Officer, positions focusing on initiatives like ownership of technology success at the department level and devising user incentives.

A variety of emerging digital payment modes will further the transformation of finance. These payments are expected to grow almost 23% annually in healthcare. ACH payments have been on a strong upward trajectory in healthcare for several years, especially for business transactions. In 2021, ACH tallied a yearly increase of 18% in volume and 5% in dollars.

Notable technologies and payment rails to watch for expected crossover from consumer markets to healthcare include:

Seeking the right use cases for these payment technologies offers many potential provider benefits.

The connected forces discussed and quantified here create major challenges to address in 2023. The strategic agenda calls for balancing tight cost control with investment in growth opportunities, significantly enhancing patient financial experience by meeting growing patient financial need, shoring up trusted relationships and cybersecurity, and accelerating the digital transformation of finance.

https://mailchi.mp/c02a553c7cf6/the-weekly-gist-july-28-2023?e=d1e747d2d8

Of all the pandemic’s impacts still felt today, disruptions to the healthcare workforce and rising labor costs may be most impactful to current health system operations.

Over the next three editions of the Weekly Gist, we’ll be exploring the lingering effects of this workforce crisis, with a focus on nurse staffing and recruitment.

In this week’s graphic, we use data from the 2023 NSI National Health Care Retention Report to show how hospital turnover and vacancy rates have changed over the past several years.

While wage increases helped reduce hospital registered nurse (RN) turnover rates from 27 percent in 2021 to 23 percent in 2022, nurses—along with hospital employees in general—are still changing jobs at higher rates than before the pandemic.

Over half of all hospitals still face nurse vacancy rates above 15 percent, a slight improvement from 2022 but still far more than before the pandemic.

While the worst of nursing turnover appears to have passed, the “rebasing” of wages (for nursing, 27 percent higher compared to 2019) will provide ongoing pressure to strained hospital margins.

https://mailchi.mp/7f59f737680b/the-weekly-gist-june-30-2023?e=d1e747d2d8

At a recent board meeting, the discussion turned to what Millennial consumers want from healthcare. The system COO put the administrative coordinator, the sole Millennial in the room, on the spot to speak for the preferences of an entire generation.

Nearly every health system we work with is debating how to engage Millennial consumers or understand Millennial (and now Gen Z) employees—perhaps an even more pressing need, given that Millennials now outnumber Baby Boomers in the healthcare workforce. But having a real, live Millennial participating in a health system board meeting is a rarity.

Most often we rely on secondhand information, either from studies analyzing their behavior, or Boomer board members’ personal experiences as the parents of Millennials. When we suggested that systems are at a disadvantage in not having Millennial board members, the system CEO agreed, and said they had tried—and failed—to recruit younger members.

It was largely a question of availability. Family commitments were one challenge, but the greatest obstacle was committing to days away from work. Younger executives and community leaders are in the “high-growth” stage of their careers, and rarely in control of their own schedules, making the commitment to a (typically unpaid) board seat difficult.

As boards push for more diversity among members, recruiting younger directors is a critical component. Even if systems aren’t ready to reshape the director role for Millennials, they must find a way to directly engage younger leaders and integrate them into decision-making at all levels of the organization.

https://www.axios.com/2023/05/31/great-resignation-quitting-boom

A phenomenon that defined the pandemic-era labor market is over: the Great Resignation — workers furiously quitting for new, likely higher paying jobs — is a thing of the past.

Why it matters:

The historic surge of quitters was a symptom of an on-fire labor market, where demand for workers far outstripped supply of them.

By the numbers:

The quits rate fell to 2.4% in April, according to the Job Openings and Labor Turnover Survey, released this morning.

What they’re saying:

“We are pretty much back to a strong, robust labor market, but one that is no longer overheating,” says Julia Pollak, an economist at ZipRecruiter.

Flashback:

At the height of the Great Resignation, the overall quits rate most recently peaked at 3% in April 2022, when there were roughly 4.5 million quits in a single month.

The bottom line:

Americans who did job hop over the past few years have seen heftier pay gains. But that phenomenon, too, is fading — another sign of some heat coming off the labor market.

During the pandemic, many nurses left hospital staff jobs for more lucrative travel jobs. However, many of these nurses are returning to hospitals for full-time positions, especially as travel pay falls and organizations offer new staff benefits, Melanie Evans writes for the Wall Street Journal.

How Allegheny Health Network re-recruits experienced RNs

During the pandemic, many hospitals struggled with staffing shortages as many nurses left their positions as a result of burnout or for more high-paying travel opportunities. However, many nurses are now returning to staff positions, especially as travel pay declines.

According to Aya Healthcare CEO Alan Braynin, travel nurse pay is now down 28% compared to a year ago. Hospital openings for travel nurses were also down by 51% at the end of April compared to the same time last year.

At HCA Healthcare, the country’s largest publicly traded hospital chain, nurse hiring increased by 19% in the first three months of the year compared to the average across the last four quarters. In addition, turnover levels have almost declined to pre-pandemic levels, and HCA’s travel nurse costs have dropped by 21% in the first quarter of this year compared to 2022.

According to the organization, many nurses who initially left their hospitals during the pandemic are now coming back. Since 2022, around 20% of the 37,000 nurses hired at HCA hospitals previously worked for the company at some point between 2016 and 2022.

Similarly, Houston Methodist has rehired around 60 nurses who initially left during the pandemic. Roberta Schwartz, the chief innovation officer at the health system’s flagship hospital, said these returning nurses have helped the hospital make more beds available and keep up with an 8% increase in demand.

“The boomerang nurses have returned,” said Gail Vozzella, Houston Methodist’s chief nurse.

To attract more nurses to staff positions, hospital officials said they are offering higher pay, as well as several new benefits, such as childcare, less demanding work positions, and more flexible schedules.

For example, Suzane Nguyen, who took a teaching job during the pandemic, rejoined Houston Methodist in June 2022 after she was offered a virtual job. In her new position, she collects patient information by video. “The stress doesn’t compare,” she said.

Similarly, Linda Allen, an ED nurse who left to work for a temporary agency during the pandemic, returned to Sentara Healthcare in 2022 after the hospital system increased its wages and offered new, more flexible schedules.

According to Terrie Edwards, Sentara’s regional VP, the organization has increased its nurse wages by around 21% in the last two years and now offers student debt relief up to $10,000, as well as adoption and infertility benefits.

Overall, these changes have helped Sentara hire around 400 boomerang nurses, which has reduced staff overtime and cut its travel nurse expenses in half.

“They really did step up,” said Allen, who became a full-time employee in September 2022 after initially working temporary 13-week contracts.

Outside of these benefits, some nurses are also just ready for more permanent positions after spending the pandemic working in several different hospitals. “There is something to be said for working in the same place every day, consistently,” said Alexis Brockting, an advanced practice nurse at Mercy Hospital South.