Cartoon – Importance of Employee Retention

https://mailchi.mp/c6914989575d/the-weekly-gist-march-31-2023?e=d1e747d2d8

It feels like governance questions are coming to the fore in a lot of places these days, at least judging by several recent conversations we’ve had with health system CEOs. Probably not surprising, given the number of potential mergers and other partnerships under consideration.

As one CEO told us, growth by M&A raises particularly thorny issues for a not-for-profit system board. “Our governance structure grew out of a single hospital board, which was made up of community members and local physician leaders,” he told us. As the system acquired hospitals in adjacent markets, the combined board took on a representational character—each hospital had local stakeholders involved in governance. “Now we’re talking about merging with an out-of-state system, and our board suddenly seems way too parochial and unsophisticated. Everyone’s still asking what’s in it for their community.” That’s a frustration we hear frequently.

There are legitimate reasons why a tax-exempt community institution should have local representation on the board, advocating for local priorities and resources. But a larger, multi-state board must also oversee the entire portfolio of assets, and make trade-offs across markets, sometimes making decisions that favor one hospital over another.

The larger system board also has a greater need for sophistication, both on business and healthcare issues, as its members are often responsible for billions of dollars of assets. What frequently results from this tension is a nesting series of system and community boards, with varying degrees of accountability—a recipe for tangled, lengthy decision processes, and an enormous time-sink for senior system executives. We’re keeping our eye out for next-generation solutions to the governance question in healthcare—let us know what you’re seeing.

https://mailchi.mp/c6914989575d/the-weekly-gist-march-31-2023?e=d1e747d2d8

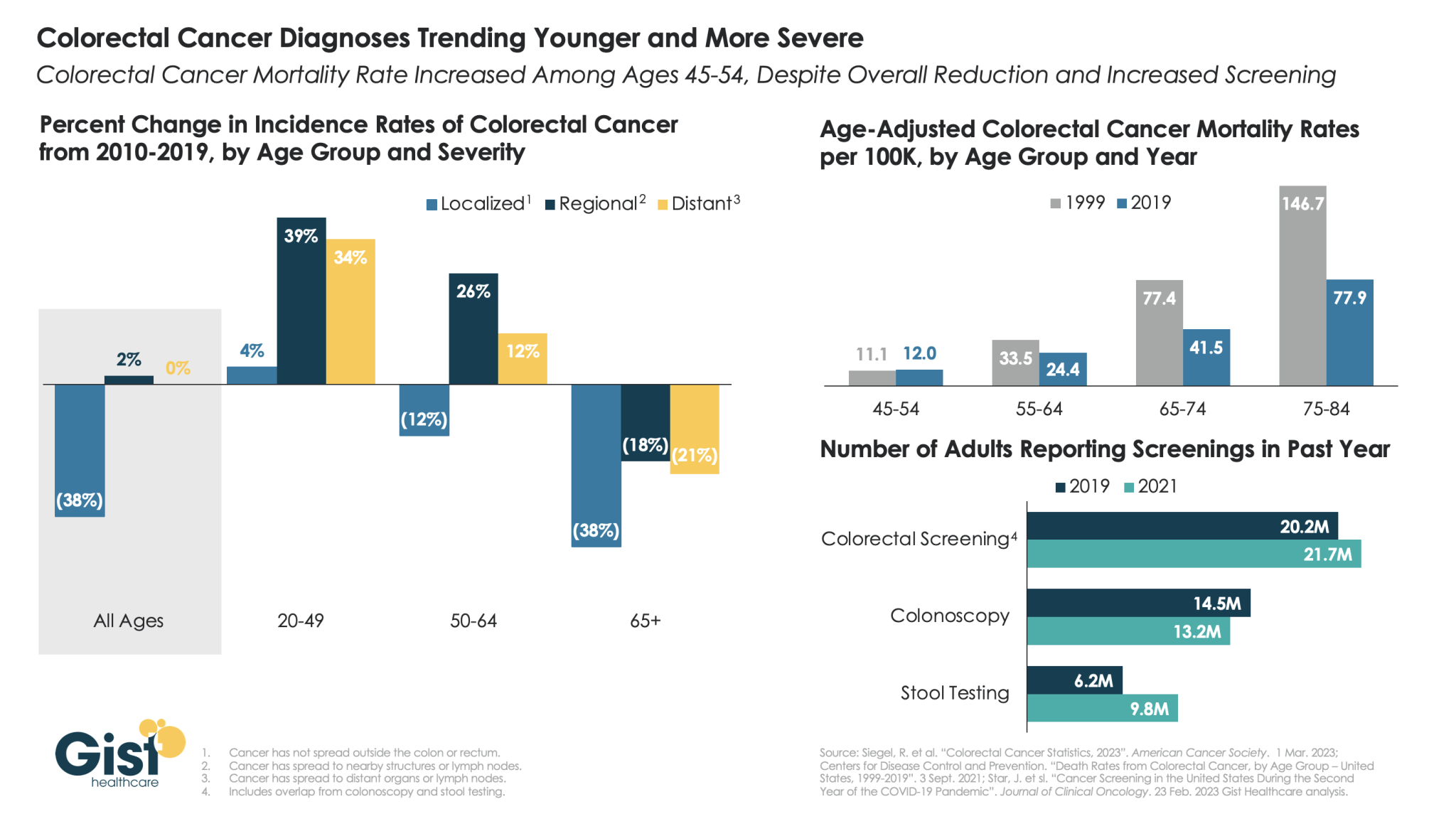

A new study from the American Cancer Society revealed a startling phenomenon in colorectal cancer: cases are trending younger while the severity of diagnoses is increasing. As shown in the graphic above, despite an overall reduction in the incidence of colorectal cancer—thanks to an emphasis on earlier detection and treatment—more severe diagnoses of colorectal cancer (termed “regional” and “distant”) each grew by over 30 percent in adults under age 50 from 2010 to 2019.

While researchers are still exploring the causes for the increase in younger people, it underscores the importance of new guidance from May 2021 which lowered the recommended colorectal cancer screening age from 50 to 45. One bright spot: unlike most other cancer screenings, screenings for colorectal cancer actually increased during the pandemic, thanks to the rise of at-home stool testing. Stool testing was especially common among lower income and minority populations who often struggle to access colonoscopies.

However, there is evidence that flagged patients are not scheduling critical follow-up colonoscopies. Better connection between at-home assessments and more thorough diagnostic services is a critical next step in the broader home-based care movement.

https://mailchi.mp/c6914989575d/the-weekly-gist-march-31-2023?e=d1e747d2d8

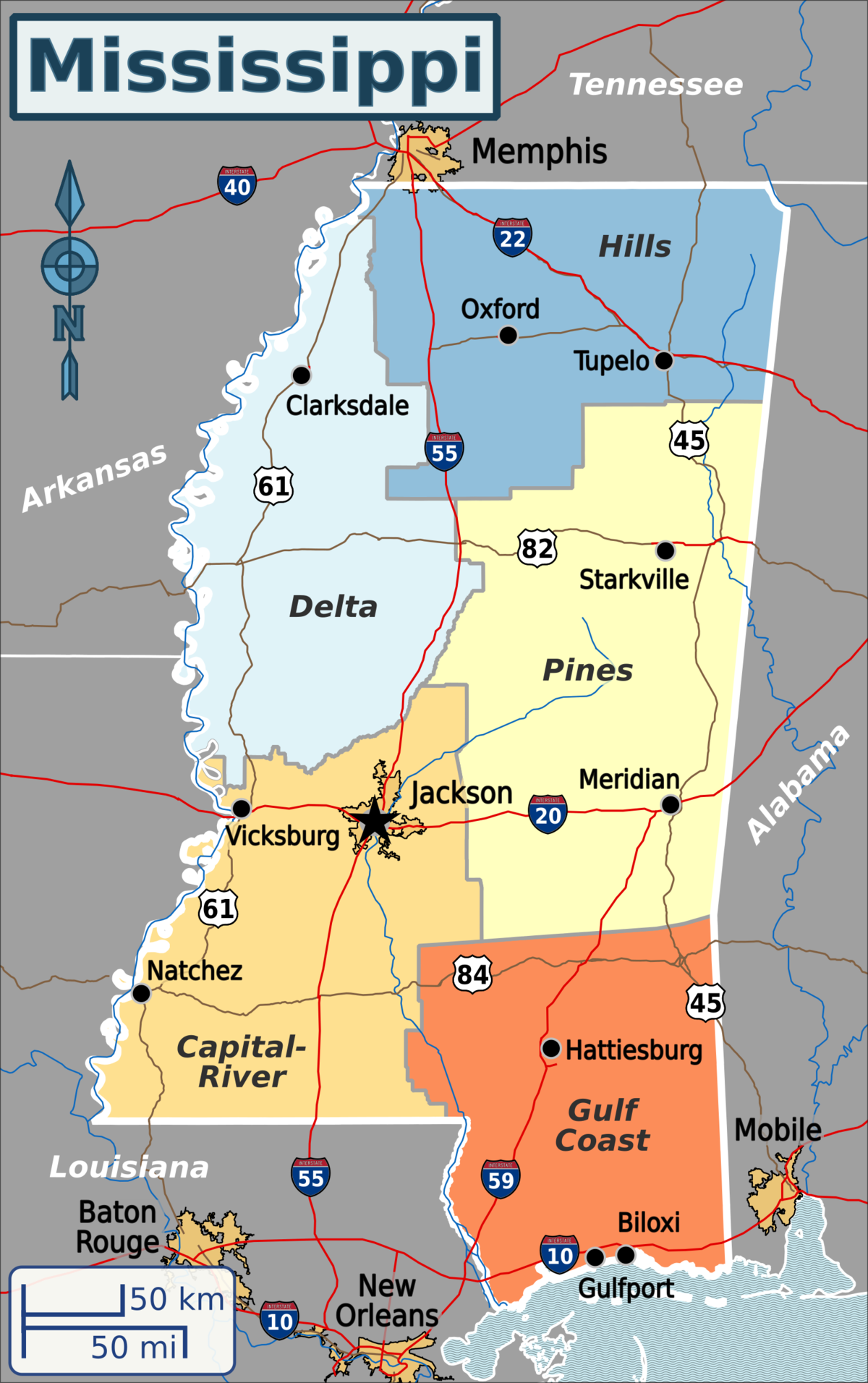

Published this week in the New York Times, this article describes the decaying state of Greenwood Leflore Hospital, a 117 year-old facility in the Mississippi Delta that may be within months of closure. While rural hospitals across the country are struggling, Mississippi’s firm opposition to Medicaid expansion has exacerbated the problem in that state, by depriving providers of an additional $1.4B per year in federal funds. Instead, only a few of the state’s 100-plus hospitals actually turn an annual profit, and uncompensated care costs are almost 10 percent of the average hospital’s operating costs.

Despite a dozen or more hospitals at imminent risk of closure, Mississippi officials would rather use the state’s $3.9B budget surplus to lower or eliminate the state income tax.

The Gist: Expanding Medicaid doesn’t just reduce rates of uncompensated care provided by hospitals, it changes the volume and type of care they provide.

Further, Medicaid expansion has been found to result in significant reductions in all-cause mortality.

Ensuring that low-income residents in Mississippi and other non-expansion states have access to Medicaid would allow providers to administer more preventive care and manage chronic diseases more effectively, before costly exacerbations require hospitalization.

https://mailchi.mp/c6914989575d/the-weekly-gist-march-31-2023?e=d1e747d2d8

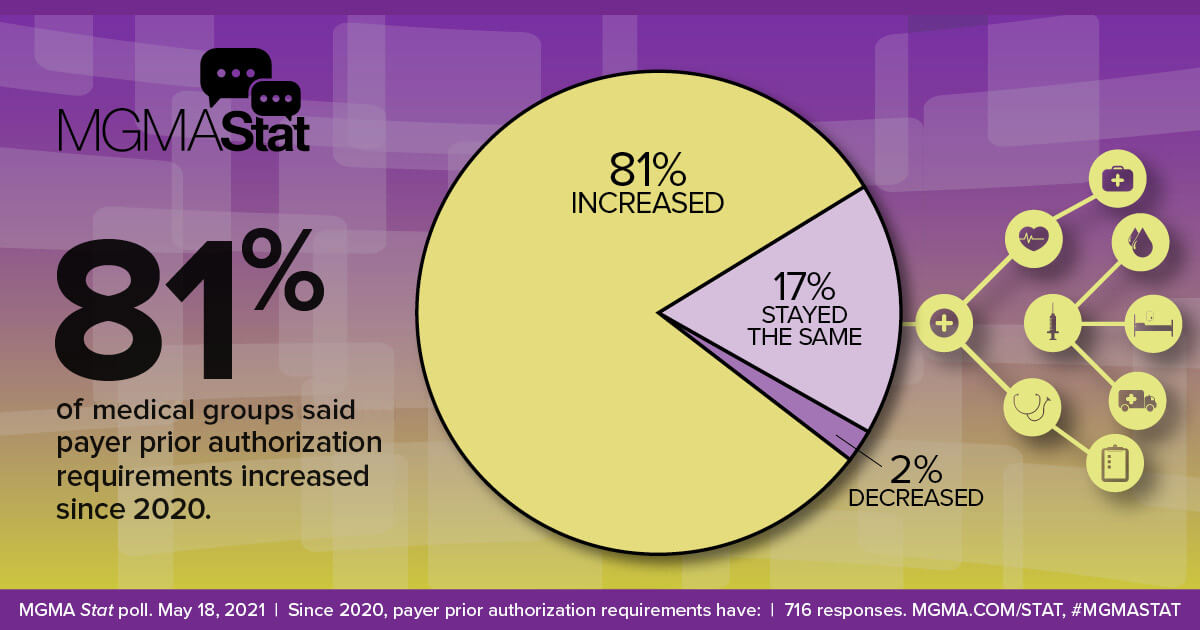

On Wednesday, UnitedHealth Group (UHG) announced that it will reduce its prior authorization claims volume by 20 percent for its commercial, Medicare Advantage, and Medicaid businesses later this year. Next year, it will launch a “gold card” program for qualifying providers that will further streamline care approvals. Cigna also shared that it has removed nearly 500 services from prior authorization review since 2020, relying on an electronic process for faster response times. These changes come in the wake of a Centers for Medicare and Medicaid Services (CMS) proposed rule, set to be finalized in April, that aims to streamline prior authorization by requiring certain payers to establish a method for electronic transmission, shorten response time for physician requests, and provide a reason for denials.

The Gist: These changes address two of providers’ primary complaints around prior authorizations: there are too many of them, and payers take too long to process them. However, technology options aiming to solve this problem through automation are by no means a foolproof solution.

As ProPublica recently reported, algorithm-based electronic claims processing solutions that improve response times can create other challenges, including improper automatic denials, and can expand prior authorization to lower-cost services, for which it was previously determined to be inefficient to rely on human review. Quicker responses must still be accurate and fair, necessitating that insurance companies closely monitor, audit, and hone technology solutions.

https://mailchi.mp/c6914989575d/the-weekly-gist-march-31-2023?e=d1e747d2d8

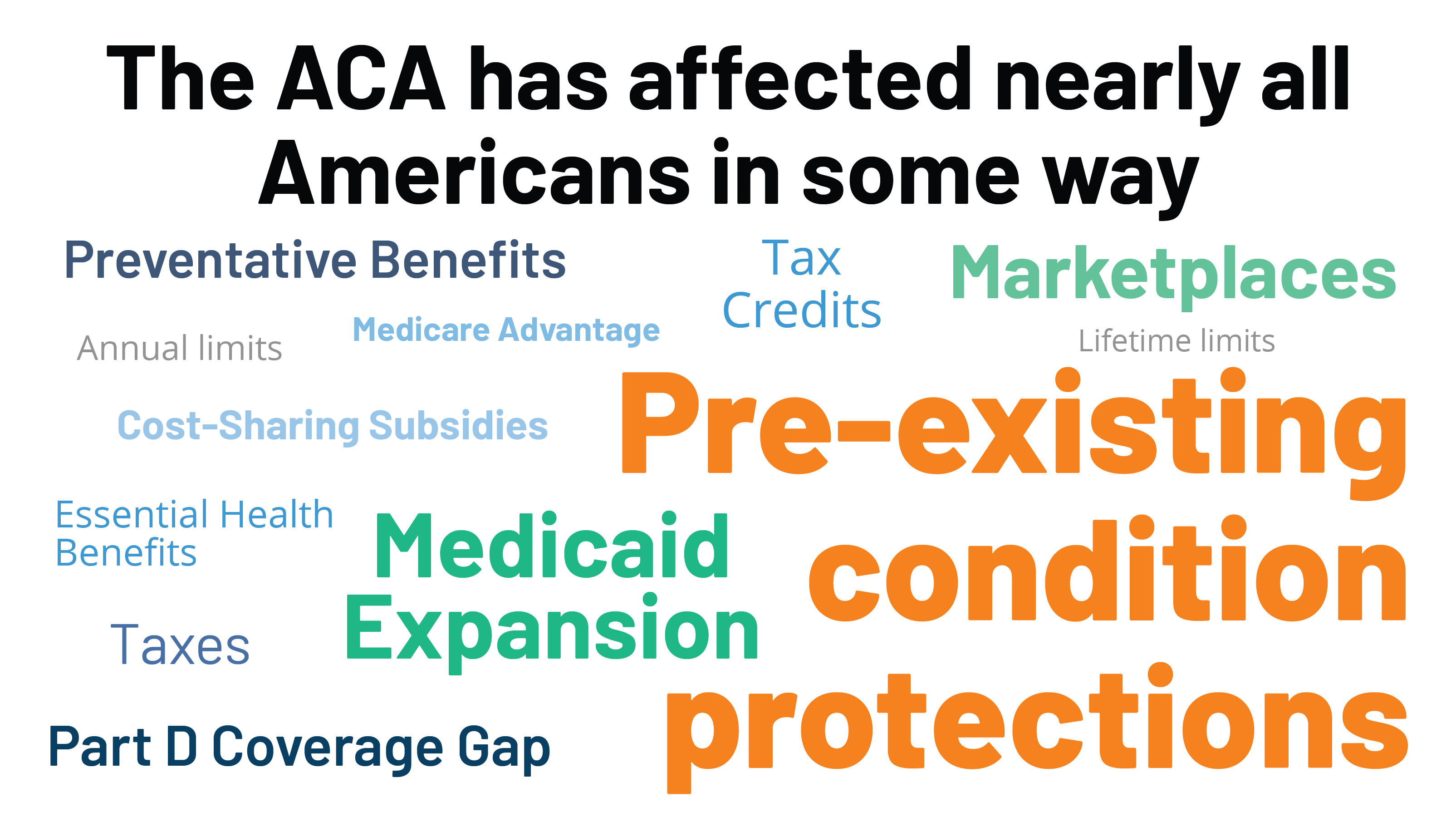

US District Judge Reed O’Connor ruled on Thursday that the Affordable Care Act’s (ACA’s) requirement for most insurers to cover certain preventative care services without cost-sharing is unlawful. Judge O’Connor—who invalidated the entire ACA in 2018, before the Supreme Court reversed that ruling—had already sided with the plaintiffs in Braidwood vs. Becerra last September, on the grounds that mandatory coverage of HIV prevention treatment, also known as PrEP therapy, violated their religious beliefs. His latest ruling applies to the ACA-mandated preventive services that are compelled by the US Preventative Services Task Force (USPSTF), on the grounds of the task force’s makeup and the fact that some of its recommendations predate the ACA. Services covered for no cost today include screening tests for a variety of cancers, sexually transmitted infections, and diabetes. The ruling does not impact other ACA preventative care services, like contraceptive services and children’s immunizations, as they are based on the recommendations of other government advisory groups. The immediate impact of this week’s ruling is unclear, as the Biden administration has already filed an appeal and may seek to stay the ruling, while most insurance contracts are set on an annual basis.

The Gist: Given the reasoning laid out in Judge O’Connor’s Braidwood v. Becerra ruling last fall, this decision was expected. As with previous attempts to repeal the ACA that have come through his district, the ultimate fate of the ACA’s cost-free preventative care services will likely be decided by the US Supreme Court. It’s possible that the Court may find the narrow targeting of this case more reasonable, making no-cost preventive care coverage optional for employers.

If that happens, millions of Americans could again have to pay for some of the most common and highest-value healthcare services. That additional financial burden, along with tightening of health plan benefit designs, could create barriers to access and exacerbate health disparities.

Republicans divided over tackling Medicare Advantage overpayments

Hard-pressed to come up with significant savings to reduce the deficit, some Senate Republicans are taking a closer look at reforms to Medicare Advantage in light of reports that insurance companies are collecting billions of dollars in extra profits by over-diagnosing older patients.

But the idea of cracking down on Medicare Advantage overpayments to insurance companies divides Republicans, who have traditionally championed the program.

Proponents of Medicare Advantage reform anticipated it will face strong opposition from the insurance industry, one of the most powerful special interest groups in Washington.

Sen. Bill Cassidy (La.), the top-ranking Republican on the Senate Health, Education, Labor and Pensions Committee, is leading the push to reduce Medicare overpayments.

“Medicare is going insolvent. If we don’t do anything, it’s going to go insolvent. We have a whole package of things, all of them bipartisan, and we’re doing it essentially to have something out there so that if somebody decides to do something, there will be things that are examined, considered and bipartisan” to vote on, he said.

“I come up with lots of stuff. We thought it through policy and think it’s policy that can make it all the way through,” he said.

Cassidy’s office says his bill could extend the solvency of Medicare by saving as much as $80 billion in federal funds over the next decade without cutting benefits.

He emphasizes that it would not cut Medicare Advantage benefits, but critics of the legislation are sure to challenge that claim.

“We’re not undermining Medicare Advantage,” he said.

“In fact, I would say this is a better alternative than what CMS is doing by rule,” he added, referring to a new rule-making action by the Biden administration to recover overpayments in Medicare Advantage through the Centers for Medicare & Medicaid Services.

The Medicare Payment Advisory Panel estimates that Medicare Advantage plans collected $124 billion in overpayments from 2008 to 2023. They collected an estimated $44 billion overpayments in 2022 and 2023 alone, according to MedPAC.

Unlike traditional fee-for-service Medicare, Medicare Advantage plans are offered by private companies. Both are funded by taxpayers through general revenues, payroll taxes and beneficiaries’ premiums.

Cassidy is also leading a bipartisan working group to reform Social Security to extend its solvency. Members include Sens. Angus King (I-Maine) and Mitt Romney (R-Utah).

“To have a significant impact on fiscal policy, you’d have to look at entitlements,” said Romney, who called Medicare Advantage “an area we’re going to be looking at very shortly — the committee will be looking at Medicare Advantage,

the cost of Medicare Advantage …. It’s become more expensive than the old fee-for-service Medicare.”

In a follow-up interview Thursday, Romney said senators are also looking at reforms to Pharmacy Benefit Managers, the companies that serve as middle-men between drug manufacturers, insurance companies and pharmacies.

Romney said, “in the past, Medicare Advantage has been a lower-cost way of providing Medicare than fee-for-service Medicare.”

“If that’s changing, I’d like to understand why and make sure we don’t create impediments to the lower-cost Medicare Advantage,” he said.

Sen. Mike Braun (R-Ind.) said Medicare Advantage overpayment “definitely” is a “reform issue.”

“I’ve been the loudest voice on reforming health care and that’s a commonsense idea,” he said. “Whatever it takes to bring down health care costs.

“I’m one of the most free-market people here, but the health care industry is not a free market. It’s like an unregulated utility,” he said. “There’s so much opaqueness.”

But some Republicans are already trying to paint efforts to reduce overpayments as cuts to Medicare Advantage.

“The problem with Medicare Advantage is President Biden is cutting $540 per member per year. That’s the problem. Medicare Advantage has been very successful,” said Sen. Roger Marshall (R-Kan.), an OB/GYN who practiced medicine for more than 25 years.

National Republican Senatorial Committee Chairman Steve Daines (R-Mont.) accused Biden of “proposing Medicare Advantage cuts” when the president accused some Republicans of wanting to sunset Medicare at his Feb. 7 State of the Union address.

Medicare Advantage is getting more popular among Democrats as well as the number of blue state enrollees in the program soars. The number of Americans enrolled in Medicare Advantage has nearly doubled over the last 12 years, according to the Kaiser Family Foundation.

Cassidy’s proposal, which he introduced with progressive Sen. Jeff Merkley (D-Ore.) on Monday, could draw broader interest from Republicans.

Sen. John Cornyn (R-Texas), an adviser to the Senate GOP leadership, called Medicare Advantage a “success.”

“That doesn’t mean that it should be immune from oversight, so I’ll be interested to see what they have to say,” he said.

Cassidy and Merkley say that Medicare Advantage plans have a financial incentive to make beneficiaries appear sicker than they are because they are paid a standard rate based on the health of individual patients. Their bill, the No Unreasonable Payment, Coding or Diagnoses for Elderly (No Upcode Act) would require risk models based on more extensive diagnostic data over a period of two years.

It would also limit the ability of insurance companies to use old or unrelated medical conditions to inflate the cost of care and ensure that Medicare is only charged for treatment related to relevant medical conditions, according to a summary provided by the senators’ offices.Biden administration approves California’s electric truck mandateFlorida transgender bathroom bill passes committee

The goal is to narrow the disparity in how patients are assessed by traditional Medicare and Medicare Advantage.

Studies and audits conducted by CMS and the Department of Health and Human Services’ inspector general found that insurance companies collected billion of dollars in overpayments because of diagnoses that were not later supported by enrollees’ medical records.

The Kaiser Family Foundation reported in August that more than 28 million people — or about 48 percent of the eligible Medicare population — were enrolled in Medicare Advantage plans in 2022. They accounted for $427 billion or 55 percent of total federal Medicare spending.

We dig into three research papers to make sense of what will happen to 15 million people set to lose their Medicaid over the next year.

Listen to the full episode below, read the transcript or scroll down for more information.

If you want more deep dives into health policy research, check out our Research Corner and subscribe to our weekly newsletters.

https://embed.acast.com/tradeoffs/?brandColor=e65a4b

Researchers estimate 15 million people will lose their Medicaid starting April 1 when states begin removing people from the low-income health insurance program for the first time in three years.

In March 2020, Congress banned states from removing people from Medicaid during the pandemic in exchange for more federal funding for state Medicaid programs. Medicaid enrollment is usually tied to people’s incomes, and individuals normally have to regularly prove they still qualify in what’s known as a redetermination. (In the 39 states and Washington, D.C., that have expanded Medicaid, a family of four has to make less than $40,000 to qualify. In non-expansion states, the cutoff is even lower.)

With redeterminations paused, Medicaid enrollment nationwide has grown from 71 million in February 2020 to an estimated 95 million in March 2023. Research shows Medicaid coverage is associated with better access to care, more financial security, better health and lower mortality. During the pandemic, beneficiaries have been able to enjoy these benefits without worrying about confirming their eligibility.

In December, Congress voted to let states restart the process of clearing their rolls on April 1, what’s sometimes referred to as “unwinding.” Lawmakers are giving states 14 months to redetermine millions of people’s eligibility — an unprecedented task made even more difficult by serious staffing and experience shortages in many Medicaid offices.

“It’s going to be a big lift,” said Sayeh Nikpay, a health policy researcher at the University of Minnesota and Tradeoffs Senior Research Advisor. “States have never had to do this many redeterminations this quickly before, and there’s a lot of uncertainty about what will happen.”

We asked Nikpay to pick out a few relevant studies to help us understand what is happening and how states and employers could keep more people insured. Here are three she identified as particularly helpful.

The Office of the Assistant Secretary for Planning and Evaluation, which provides research for the U.S. Department of Health and Human Services, released a report in August 2022 that estimated 15 million people will lose Medicaid coverage as a result of the unwinding. (The estimate is similar to another analysis by the independent Urban Institute.)

ASPE breaks those 15 million people into two groups. In the first group are people who make too much money to qualify for Medicaid. ASPE estimates there are about 8 million people in that category, and they should be able to get insurance through work or the Obamacare exchanges.

In the second group are roughly 7 million people ASPE estimates are still eligible but will lose coverage because of what’s called “administrative churn.” This can happen if the Medicaid office can’t get in touch with someone to confirm their eligibility because they’ve moved or changed their phone number or if they’re unable to make an in-person appointment because of work or child care responsibilities. (The Urban Institute projects about 4 million people will be in this group.)

These two groups represent a key tension to the unwinding process: States want to shed people who make too much money, but officials also know eligible people often lose coverage during redeterminations, and that danger is heightened given the scale and speed of this process.

This next paper looks at the first group: the roughly 8 million people expected to move from Medicaid to private coverage, and specifically the roughly 4 million who are expected to get coverage through the Obamacare exchanges. Adrianna McIntyre, an assistant professor of health policy at Harvard, wrote in JAMA Health Forum in October 2022 about the most effective ways to move people from Medicaid onto private Obamacare plans.

There’s limited data on this, but based on the few studies available, McIntyre found that only 3 to 5 percent of people who leave Medicaid end up getting an Obamacare plan. Many policymakers are relying on the Obamacare exchanges to provide a life preserver to millions of people losing Medicaid coverage, but the research cited by McIntyre shows getting people into these plans is not guaranteed and will take focused effort by states.

McIntyre’s review cites several randomized controlled trials where states tested different ways of increasing enrollment in Obamacare plans. These studies found simple reminders from the state – like physical letters, emails and phone calls help – boost sign-ups anywhere from 7 to 16 percent.

But what really seems to make a difference is reminders plus connecting people to someone who can get them signed up while they are on the phone. In one of those trials published in 2022, people in California who got a reminder email and a call connecting them to enrollment assistance were almost 50% more likely to sign up for a plan. Such extra effort is obviously costly, and it may not be a priority or financially feasible for some states.

McIntyre’s review did not include any research on what employers can do to help their workers transition from Medicaid to work-based coverage, but based on the studies McIntyre cited, Nikpay said she thinks it’s a good idea for employers to make sure people know Medicaid could be going away and provide as much help as possible in getting new coverage.

The final study looks at the second group of people expected to lose Medicaid coverage: the 7 million people who may lose coverage due to administrative churn even though they are still eligible.

Some states have tried to limit that churn, and researchers at the RAND Corporation evaluated New York’s effort. Starting in 2014, New York allowed people to stay on Medicaid without any redeterminations for 12 months once enrolled.

In addition to keeping more people on Medicaid for longer, researchers found that after this policy was in place, hospital admissions and monthly costs per beneficiary went down. The researchers can’t say whether the continuous enrollment policy directly caused these improved outcomes, but the findings suggest that avoiding administrative churn can help people stay covered without ballooning costs.

“It seems reasonable to me,” Nikpay said of the findings, “that making it easier to stay on Medicaid, even outside of a global pandemic, could benefit people’s health given what we know about how Medicaid affects people.”