During the pandemic, many nurses left hospital staff jobs for more lucrative travel jobs. However, many of these nurses are returning to hospitals for full-time positions, especially as travel pay falls and organizations offer new staff benefits, Melanie Evans writes for the Wall Street Journal.

Hospitals see more nurses return to their positions

During the pandemic, many hospitals struggled with staffing shortages as many nurses left their positions as a result of burnout or for more high-paying travel opportunities. However, many nurses are now returning to staff positions, especially as travel pay declines.

According to Aya Healthcare CEO Alan Braynin, travel nurse pay is now down 28% compared to a year ago. Hospital openings for travel nurses were also down by 51% at the end of April compared to the same time last year.

At HCA Healthcare, the country’s largest publicly traded hospital chain, nurse hiring increased by 19% in the first three months of the year compared to the average across the last four quarters. In addition, turnover levels have almost declined to pre-pandemic levels, and HCA’s travel nurse costs have dropped by 21% in the first quarter of this year compared to 2022.

According to the organization, many nurses who initially left their hospitals during the pandemic are now coming back. Since 2022, around 20% of the 37,000 nurses hired at HCA hospitals previously worked for the company at some point between 2016 and 2022.

Similarly, Houston Methodist has rehired around 60 nurses who initially left during the pandemic. Roberta Schwartz, the chief innovation officer at the health system’s flagship hospital, said these returning nurses have helped the hospital make more beds available and keep up with an 8% increase in demand.

“The boomerang nurses have returned,” said Gail Vozzella, Houston Methodist’s chief nurse.

How hospitals are attracting boomerang nurses

To attract more nurses to staff positions, hospital officials said they are offering higher pay, as well as several new benefits, such as childcare, less demanding work positions, and more flexible schedules.

For example, Suzane Nguyen, who took a teaching job during the pandemic, rejoined Houston Methodist in June 2022 after she was offered a virtual job. In her new position, she collects patient information by video. “The stress doesn’t compare,” she said.

Similarly, Linda Allen, an ED nurse who left to work for a temporary agency during the pandemic, returned to Sentara Healthcare in 2022 after the hospital system increased its wages and offered new, more flexible schedules.

According to Terrie Edwards, Sentara’s regional VP, the organization has increased its nurse wages by around 21% in the last two years and now offers student debt relief up to $10,000, as well as adoption and infertility benefits.

Overall, these changes have helped Sentara hire around 400 boomerang nurses, which has reduced staff overtime and cut its travel nurse expenses in half.

“They really did step up,” said Allen, who became a full-time employee in September 2022 after initially working temporary 13-week contracts.

Outside of these benefits, some nurses are also just ready for more permanent positions after spending the pandemic working in several different hospitals. “There is something to be said for working in the same place every day, consistently,” said Alexis Brockting, an advanced practice nurse at Mercy Hospital South.

A number of hospitals and health systems are trimming their workforces or jobs due to financial and operational challenges.

Below are workforce reduction efforts or job eliminations that were announced within the past nine months and/or take effect later this year.

1. Wenatchee, Wash.-based Confluence Health has eliminated its chief operating officer amid restructuring efforts and financial pressures, the health system confirmed to Becker’s May 16.

2. Conemaugh Memorial Medical Center, a Duke LifePoint hospital in Johnstown, Pa., has laid off less than 1 percent of its workforce, the hospital confirmed to Becker’s May 15.

3. Community Health Network, a nonprofit health system based in Indianapolis, plans to cut an unspecified number of jobs as it restructures its workforce and makes organizational changes. The health system confirmed the job cuts in a statement shared with Becker’s on May 11. It did not say how many jobs would be cut or which positions would be affected.

4. New Orleans-based Ochsner Healtheliminated 770 positions, or about 2 percent of its workforce, on May 11. This is the largest layoff to date for the health system.

5. Cedars-Sinai Medical Centereliminated the positions of 131 employees and cut about two dozen other jobs at related Cedars-Sinai facilities, a spokesperson confirmed via a statement shared with Becker’s May 7. The Los Angeles-based organization said reductions represent less than 1 percent of the workforce and apply to management and non-management roles primarily in non-patient care jobs.

6. Rochester (N.Y.) Regional Health is eliminating about 60 positions. A statement from RRH said the changes affect less than one-half percent of the system population, mostly in nonclinical and management positions.

7. Memorial Health Systemlaid off fewer than 90 people, or less than 2 percent of its workforce.The Gulfport, Miss.-based health system said May 2 that most of the affected positions are nonclinical or management roles, and the majority do not involve direct patient care.

8. Monument Healthlaid off at least 80 employees, or about 2 percent of its workforce. The Rapid City, S.D.-based system said positions are primarily corporate service roles and will not affect patient services. Unfilled corporate service positions were also eliminated.

9. Habersham Medical Center in Demorest, Ga., laid off four executives. The layoffs are part of cost-cutting measures before the hospital joins Gainesville-based Northeast Georgia Health System in July, nowhaberbasham.com reported April 27.

10. Scripps Health is eliminating 70 administrative roles, according to WARN documents filed by the San Diego-based health system in March. The layoffs take effect May 8 and affect corporate positions in San Diego and La Jolla, Calif.

11. Trinity Health Mid-Atlantic, part of Livonia, Mich.-based Trinity Health, eliminated fewer than 40 positions, a spokesperson confirmed to Becker’s April 24. The layoffs represent 0.5 percent of the health system’s approximately 7,000-person workforce.

12. PeaceHealtheliminated 251 caregiver roles across multiple locations. The Vancouver, Wash.-based health system said affected roles include 121 from Shared Services, which supports its 16,000 caregivers in Washington, Oregon and Alaska.

13. Toledo, Ohio-based ProMedicaplans to lay off 26 skilled nursing support staff. The layoffs, effective in June, affect 20 employees who work remotely across the U.S, and six who work at the ProMedica Summit Center in Toledo, according to a Worker Adjustment and Retraining Notification filed April 18. Most affected positions support sales, marketing and administrative functions for the skilled nursing facilities, Promecia told Becker’s.

14. Northern Inyo Healthcare District, which operates a 25-bed critical access hospital in Bishop, Calif., anticipates eliminating about 15 positions, or less than 4 percent of its 460-member workforce, by April 21, a spokesperson confirmed to Becker’s. The layoffs include nonclinical roles within support and administration, according to a news release. No further details were provided about specific positions affected.

15. West Reading, Pa.-based Tower Health is eliminating 100 full-time equivalent positions. The move will affect 45 individuals, according to an April 13 news release the health system shared with Becker’s. The other 55 positions are either recently vacated or involve individuals who plan to retire in the coming weeks and months.

16. Grand Forks, N.D.-based Altru Health is trimming its executive team as its new hospital project moves forward. The health system is trimming its executive team from nine to six and incentivizing 34 other employees to take early retirement.

17. Tacoma, Wash.-based Virginia Mason Franciscan Healthlaid off nearly 400 employees, most of whom are in non-patient-facing roles. The job cuts affected less than 2 percent of the health system’s 19,000-plus workforce.

18. Katherine Shaw Bethea Hospital in Dixon, Ill., will lay off 20 employees, citing financial headwinds affecting health organizations across the U.S. It will also leave other positions unfilled to reduce expenses amid rising labor and supply costs and reductions in payments by insurance plans. Affected employees largely work in administrative support areas and not direct patient care.

19. Danbury, Conn.-based Nuvance Health will close a 100-bed rehabilitation facility in Rhinebeck, N.Y., resulting in 102 layoffs. The layoffs are effective April 12, according to the Daily Freeman.

20. Charleston, S.C.-based MUSC Health University Medical Center laid off an unspecified number of employees from its Midlands hospitals in the Columbia, S.C. area. Division President Terry Gunn also resigned after the facilities missed budget expectations by $40 million in the first six months of the fiscal year, The Post and Courier reported March 30.

21. Winston-Salem, N.C.-based Novant Healthlaid off about 50 workers, including C-level executives, the health system confirmed to Becker’s March 29. The layoffs affected Jesse Cureton, the health system’s executive vice president and chief consumer officer since 2013; Angela Yochem, its executive vice president and chief transformation and digital officer since 2020; and Paula Dean Kranz, vice president of innovation enablement and executive director of the Novant Health Innovation Labs.

22. Penn Medicine Lancaster (Pa.) General Healtheliminated fewer than 65 jobs, or less than 1 percent of its workforce of about 9,700, the health system confirmed to Becker’s March 30. The layoffs include support, administrative and executive roles, and COVID-19-related support staff, spokesperson John Lines said, according to lancasteronline.com. Mr. Lines did not provide a specific number of affected workers.

23. McLaren St. Luke’s Hospital in Maumee, Ohio, will lay off 743 workers, including 239 registered nurses, when it permanently closes this spring. Other affected roles include physical therapists, radiology technicians, respiratory therapists, pharmacists and pharmacy support staff, and nursing assistants. The hospital’s COO is also affected, and a spokesperson for McLaren Health Care told Becker’s other senior leadership roles are also affected.

24. Bellevue, Wash.-based Overlake Medical Center and Clinics laid off administrative staff, the health system confirmed to the Puget Sound Business Journal. The layoffs, which occurred earlier this year, included 30 workers across Overlake’s human resources, information technology and finance departments, a spokesperson said, according to the publication. This represents about 6 percent of the organization’s administrative workforce. Overlake’s website says it employs more than 3,000 people total.

25. Columbia-based University of Missouri Health Care is eliminating five hospital leadership positions across the organization, spokesperson Eric Maze confirmed to Becker’s March 20. Mr. Maze did not specify which roles are being eliminated saying that the organization won’t address individual personnel actions. According to MU Health Care, the move is a result of restructuring “to better support patients and the future healthcare needs of Missourians.”

26. Greensboro, N.C.-based Cone Healtheliminated 68 senior-level jobs. The job eliminations occurred Feb. 21, Cone Health COO Mandy Eaton told The Alamance News. Of the 68 positions eliminated, 21 were filled. Affected employees were offered severance packages.

27. The newly merged Greensburg, Pa.-based organization made up of Excela Health and Butler Health Systemeliminated 13 filled managerial jobs. The affected employees and positions are from across both sides of the new organization, Tom Chakurda, spokesperson for the Excela-Butler enterprise, confirmed to Becker’s. The positions were in various support functions unrelated to direct patient care.

28. Crozer Health, a four-hospital system based in Upland, Pa., is laying off roughly 215 employees amid financial challenges. The system announced the layoffs March 15 as part of its “operational restructuring plan” that “focuses on removing duplication in administrative oversight and discontinuing underutilized services.” Affected employees represent about 4 percent of the organization’s workforce.

29. Philadelphia-based Penn Medicine is eliminating administrative positions. The change is part of a reorganization plan to save the health system $40 million annually, the Philadelphia Business Journal reported March 13. Kevin Mahoney, CEO of the University of Pennsylvania Health System, told Penn Medicine’s 49,000 employees last week that changes include the elimination of a “small number of administrative positions which no longer align with our key objectives,” according to the publication. The memo did not indicate the exact number of positions that were eliminated.

30. Sovah Health, part of Brentwood, Tenn.-based Lifepoint Health, eliminated the COO positions at its Danville and Martinsville, Va., campuses. The responsibilities of both COO roles will now be spread across members of the existing administrative team.

31. Valley Health, a six-hospital health system based in Winchester, Va., eliminated 31 administrative positions. The job cuts are part of the consolidation of the organization’s leadership team and administrative roles.

32. Marshfield (Wis.) Clinic Health System said it would lay off 346 employees, representing less than 3 percent of its employee base.

34. Roseville, Calif.-based Adventist Health plans to go from seven networks of care to five systemwide to reduce costs and strengthen operations. The reorganization will result in job cuts, including reducing administration by more than $100 million.

35. Arcata, Calif.-based Mad River Community Hospital is cutting 27 jobs as it suspends home health services.

36. Hutchinson (Kan.) Regional Medical Center laid off 85 employees, a move tied to challenges in today’s healthcare environment.

37. Oklahoma City-based OU Healtheliminated about 100 positions as part of an organizational redesign to complete the integration from its 2021 merger.

38. Memorial Sloan Kettering Cancer Center announced it would lay off to reduce costs amid widespread hospital financial challenges. The layoffs are spread across 14 sites in New York City, and equate to about 1.8 percent of Memorial Sloan’s 22,500 workforce.

39. St. Louis-based Ascensioncompleted layoffs in Texas, the health system confirmed in January. A statement shared with Becker’s says the layoffs primarily affected nonclinical support roles. The health system declined to specify to Becker’s the number of employees or positions affected.

41. Chillicothe, Ohio-based Adena Health System announced it would eliminate 69 positions — 1.6 percent of its workforce — and send 340 revenue cycle department employees to Ensemble Health Partners’ payroll in a move aimed to help the health system’s financial stability.

42. Ascension St. Vincent’s Riverside in Jacksonville, Fla., will end maternity care at the hospital, affecting 68 jobs, according to a Workforce Adjustment and Retraining Notification filed with the state Jan. 17. The move will affect 62 registered nurses as well as six other positions.

43. Visalia, Calif.-based Kaweah Health said it aimed to eliminate 94 positions as part of a new strategy to reduce labor costs. The job cuts come in addition to previously announced workforce reductions; the health system already eliminated 90 unfilled positions and lowered its workforce by 106 employees.

44. Oklahoma City-based Integris Health said it would eliminate 200 jobs to curb expenses. The eliminations include 140 caregiver roles and 60 vacant jobs.

45. Toledo, Ohio-based ProMedica announced plans to lay off 262 employees, a move tied to its exit from a skilled-nursing facility joint venture late last year. The layoffs will take effect between March 10 and April 1.

46. Employees at Las Vegas-based Desert Springs Hospital Medical Center were notified of layoffs coming to the facility, which will transition to a freestanding emergency department. There are 970 employees affected. Desert Springs is part of the Valley Health System, a system owned and operated by King of Prussia, Pa.-based Universal Health Services.

47. Philadelphia-based Jefferson Health plans to go from five divisions to three in an effort to flatten management and become more efficient. The reorganization will result in an unspecified number of job cuts, primarily among executives.

48. Pikeville (Ky.) Medical Center said it would lay off 112 employees as it outsources its environmental services department. The 112 layoffs were effective Jan. 1, 2023.

49. Southern Illinois Healthcare, a four-hospital system based in Carbondale, announced it would eliminate or restructure 76 jobs in management and leadership. The 76 positions fall under senior leadership, management and corporate services. Included in that figure are 33 vacant positions, which will not be filled. No positions in patient care are affected.

50. Citing a need to further reduce overhead expenses and support additional investments in patient care and wages, Traverse City, Mich.-based Munson Health said it would eliminate 31 positions and leave another 20 jobs unfilled. All affected positions are in corporate services or management. The layoffs represent less than 1 percent of the health system’s workforce of nearly 8,000.

51. West Reading, Pa.-based Tower Health on Nov. 16 laid off 52 corporate employees as the health system shrinks from six hospitals to four. The layoffs, which are expected to save $15 million a year, account for 13 percent of Tower Health’s corporate management staff.

52. Sioux Falls, S.D.-based Sanford Healthannounced layoffs affecting an undisclosed number of staff in October, a decision its CEO said was made “to streamline leadership structure and simplify operations” in certain areas. The layoffs primarily affect nonclinical areas.

53. St. Vincent Charity Medical Center in Cleveland closed its inpatient and emergency room care Nov. 11, four days before originally planned — and laid off 978 workers in doing so. After the transition, the Sisters of Charity Health System will offer outpatient behavioral health, urgent care and primary care.

Below is a summary of hospitals and health systems that have recently received affirmations of existing credit ratings. Some of these have not been reported on previously.

New York City-based cancer specialist Memorial Sloan Kettering Cancer Center was affirmed by Fitch Ratings May 22 at “AA” with a stable outlook both for its default rating and on a series of bonds totaling approximately $2.6 billion.

Baltimore-based University of Maryland Medical System had an “A” rating affirmed on a series of bonds May 19 amid its robust operating profile and status as a premier healthcare provider in Maryland, S&P Global said. The 12-hospital system reported an operating loss of $8.9 million for the nine months ending March 31.

Oakland, Calif.-based Kaiser Permanente had its “AA” default rating and that on a series of bonds affirmed May 15 by Fitch as the system was able to maintain a strong financial profile even in the face of a challenging operating environment.

Providence, R.I.-based Care New England has had its default rating and that on $135.8 million of bonds affirmed at “BB-,” Fitch Ratings said May 12. The system’s outlook remains negative.The ratings reflect Care New England’s “ongoing operational challenges and thin liquidity,” Fitch said. While operating performance is expected to improve, there remains a low cash position of concern, the note said.

New Hyde Park, N.Y.-based Northwell Health had an “A-” rating affirmed on a series of bonds amid strong market share and robust financial performance, Fitch said April 28. The 21-hospital system had $15.6 billion revenues in 2022.

While its relatively weaker operating performance may continue in the shorter term, Rochester, Minn.-based Mayo Clinic has had its long-term ratings affirmed because of its excellent reputation in overall health services, both S&P Global and Moody’s said.Mayo Clinic’s revenue bonds remain at “AA” with a stable outlook, S&P said. Mayo Clinic’s “Aa2” stable credit profile is characterized by its excellent reputations for clinical services, research and education, Moody’s said.

Moody’s affirmed New York City-based Montefiore Health System‘s “Baa3” rating because of the 10-hospital system’s leading market share in the Bronx, its clinical expertise, and its flagship status as the primary teaching hospital for Albert Einstein College of Medicine.

Renton, Wash.-based Providence has reported a $345 million operating loss in the first quarter on revenue of $6.8 billion.

While revenues were up on the same period in 2022, expenses also rose 5.1 percent to total $7.1 billion. The operating loss compares with a $510 million loss in the first quarter of 2022.

Improving non-operating income, mainly from investment returns, helped mitigate the net loss to $117 million compared with an $840 million net loss in the same period last year, excluding the disaffiliation of Newport Beach, Calif.-based Hoag.

The 51-hospital system reiterated it is taking a number of initiatives to reduce some of its costs under its Destination Health 2025 Recover and Renew plan. One of those prime areas of focus is reducing staffing costs, particularly in regard to contract labor, which continues to be a challenge for Providence.

“With current labor shortages, the use of premium labor, including the number and wage rate of agency nurses, continues to be significantly higher than in previous years,” management said in its filing. “Several initiatives are underway to reduce those expenses in combination with increasing core productivity.”

Providence is also undergoing portfolio management reassessment to try and improve efficiencies and save costs, according to the filing.

The system, which had $7.8 billion long-term debt as of March 31, provided $563 million in community benefit in the first quarter, up from $412 million in the same period of 2022.

“Together, we will continue meeting the health care needs of our communities, no matter how challenging the environment gets, and will ensure the mission of Providence thrives for years to come,” Rod Hochman, MD, Providence president and CEO said in the filing.

In the mid-1980’s, managed care advocate Dr. Paul Ellwood predicted that eventually, US healthcare would be dominated by perhaps a dozen vast national firms he called SuperMeds that would combine managed care based health insurance with care delivery systems. Ellwood was a leader of the “managed competition” movement which advocated for a private sector alternative to a federal government-run National Health Insurance system. Ellwood and colleagues believed that Kaiser Foundation Health Plans and other HMOs would be able to stabilize health costs and thus affordably extend care to the uninsured.

The US political system and market dynamics would not co-operate with Ellwood and his Jackson Hole Group’s vision. In the ensuing thirty-five years, healthcare has remained both highly fragmented and regional in focus. However, unbeknownst to most, during the past decade, as a result of a major merger and relentless smaller acquisitions, two SuperMeds were born- CVS/Aetna and UnitedHealth Group, that whose combined revenues comprise 14% of total US health spending.

CVS/Aetna is slightly larger than United, by dint of grocery sales in its drugstores and its vast Caremark pharmacy benefits management business. However, CVS’s Aetna health insurance arm is one third the size of United’s, and though CVS is rapidly scaling up its care delivery apparatus through its in-store Health Hubs, it remains is a tiny fraction of United’s care footprint. Despite being slightly smaller at the top line, United’s market capitalization is more than 3.5 times that of CVS.

United’s vast scope is difficult to comprehend because much of it is not visible to the naked eye, and the most rapidly growing businesses are partly nested inside United’s health insurance business.

United employs over 300 thousand people. At $287.6 billion total revenues in 2021, United exceeded 7% of total US health spending (though $8.3 billion are from overseas operations).

In 2021, United was $100 billion larger than the British National Health Service. It is more than three times the size of Kaiser Permanente, and five times the size of HCA, the nation’s largest hospital chain. United is both larger and richer than energy giant Exxon Mobil. United has over $70 billion in cash and investments, and is generating about $2 billion a month in operating cash flow.

Its highly regulated health insurance business is the visible tip of a rapidly growing iceberg. Revenue from United’s core health insurance business grew at 11% in 2021, compared to 14% growth in United’s diversified Optum subsidiary. Optum generated $155.6 billion in 2021 (of which 60% were from INSIDE United’s health insurance business). You can see the relationship of Optum’s three major businesses to United’s health insurance operations in Exhibit I.

Optum is the Key to United’s Growth

Understanding the role of Optum is key to understanding United’s business. It is remarkable how few of my veteran health care colleagues have any idea what Optum is or what it does. Optum was once a sort of dumping ground for assorted United acquisitions without a seeming core purpose. A private equity colleague once derided Optum as “The Island of Lost Toys”. Now, however, Optum is driving United’s growth, and generates billions of dollars in unregulated profits both from inside the highly regulated core health insurance business and from external customers.

Optum consists of three parts:Optum Health, its care delivery enterprise ($54 billion revenues in 2021), Optum Rx, its pharmacy benefits management enterprise ($91 billion revenues in 2021) and Optum Insight, a diversified business services enterprise ($12.2 billion in 2021). Virtually all of United’s acquisitions join one of these three businesses.

Optum Health: The Third Largest Care Delivery Enterprise in the US

By itself, Optum Health is almost the size of HCA ($54 billion in 2021 vs HCA’s $58.7 billion) and consists of a vast national portfolio of care delivery entities: large physician groups, urgent care centers, surgicenters, imaging centers, and now by dint of the recently announced $5.7 billion acquisition of LHC, home health agencies. Optum Health has studiously avoided acquiring beds of any kind: hospitals, nursing homes, etc. and likely will continue to do so. Optum Health’s physician groups not only generate profits on their own, but also provide powerful leverage for United to control health costs for its own subscribers, pushing down United’s highly visible and regulated Medical Loss Ratio (MLR), and increasing health plan profits.

Optum Health began in 2007 when United acquired Nevada-based Sierra Health, and thus became the new owner of a small multispecialty physician group which Sierra owned. The group did not belong in United’s health insurance business and came to rest over in Optum. Over the past twelve years, Optum Health has acquired an impressive percentage of the major capitated medical groups in the US- Texas’ WellMed, California’s HealthCare Partners (from DaVita), as well as Monarch, AppleCare and North American Medical Management, Massachusetts’ Reliant (formerly Fallon Clinic) and Atrius in Massachusetts (pending) , Kelsey Seybold Clinic (also pending) in Houston, TX and Everett Clinic and PolyClinic in Seattle.

Optum Health claims over 60 thousand physicians, though many of these are actually independent physicians participating in “wrap around” risk contracting networks. By comparison, Kaiser Permanente’s Medical Groups employ about 23 thousand physicians. United’s management claims that Optum Health provides continuing care to about 20 million patients, of whom 3 million are covered by some form of so-called “value based” contracts. Perhaps half of this smaller number are covered by capitated (percentage of premium-PMPM) contracts.

Optum Health straddles fierce competitive relationships between United’s health insurance business and competing health plans in well more than a dozen metropolitan areas. Almost half (44%) of Optum Health’s revenues come from providing care for health plans other than United.

When Optum acquires a large physician group, it acquires those groups’ contracts with United’s health insurance competitors, some of which contracts have been in place for decades. Premium revenues from other health plans, presumably capitation or per member per month (PMPM) revenues, are one-quarter of Optum Health’s $54 billion total revenues. These “external” premium revenues have quadrupled since 2018, largely for Medicare Advantage subscribers. Optum Health contributes about $4.5 billion in operating profit to United. It is impossible to determine from United’s disclosures how much of this profit comes from Optum Health’s services provided to United’s insured lives and how much from its medical groups’ extensive contracts with competing health plans.

Optum Health’s surgicenters and urgent care centers provide affordable alternatives to using expensive hospital outpatient services and emergency departments, potentially further reducing United medical expense. This creates obvious tensions with United’s hospital networks, since Optum Health can use its large medical practices and virtual care offerings to divert patients from hospitals to its own services, or else render those services unnecessary.

Though some observers have termed Optum/United’s business model “vertical integration”-ownership of the suppliers to and distributors of a firm’s product– Optum Health has actually grown less vertical since 2018, with revenues from competing health plans growing from 36% of total revenues in 2018 to 44% in 2021. A 2018 analysis by ReCon Strategy found at best a sketchy matchup between United’s health plan enrollment by market and its Optum Health assets (https://reconstrategy.com/2018/04/uniteds-medicare-advantage-footprint-and-optumcare-network-do-not-overlap-much-so-far/.

Optum Rx: The Nation’s Third Largest Pharmacy Benefits Management Business

Optum’s largest business in revenues is its Optum Rx pharmaceutical benefits management (PBM) business, which generates $91 billion in revenues, and processes over a billion pharmacy claims not only for United but also many competing insurers and employer groups. Pharmaceutical costs are a rapidly growing piece of total medical expenses, and controlling them is yet another source of largely unregulated profits for United; Optum Rx generated over $4.1 billion of operating profit in 2021.

Optum Rx is the nation’s third largest PBM business after Caremark, owned by CVS/Aetna and Express Scripts, owned by CIGNA, and processes about 21% of all scripts written in the US. Pharmacy benefits management firms developed more than two decades ago to speed the conversion of patients from expensive branded drugs to generics on behalf of insurers and self-funded employers. They were given a big boost by George Bush’s 2004 Medicare Part D Prescription Drug benefit, as a “pro-competitive” private sector alternative to Medicare directly negotiating prices with pharmaceutical firms.

Reducing drug spending is one key to United’s profitability. Since generics represent almost 90% of all prescriptions written, Optum Rx now relies on fees generated by processing prescriptions and on rebates from pharmaceutical firms to promote their costly branded drugs as preferred drugs on Optum Rx’s formularies. These rebates are determined based on “list” prices for those drugs vs. the contracted price for the PBMs, and are actual cash payments from manufacturers to PBMs.

Drug rebates represent a significant fraction of operating profits for health insurers that own PBMs, particularly for their older Medicare Advantage patients that use a lot of expensive drugs. Unfortunately, PBMs have incentives to inflate the list price, because rebates are caculated based on the spread between list prices and the contract pricel Unfortunately, this increases subscribers’ cash outlays, because patient cost shares are based on list prices.

Optum Rx generates about 39% of its revenues (and an undeterminable percentage of its profits) serving other health insurers and self-funded employers. Many of those self-funded employers demand that Optum pass through the rebates directly to them (even if it means being charged higher administrative fees!).

Unlike the situation with Optum Health, the “verticality” of Optum’s PBM business-the percentage of Optum revenues derived from serving United subscribers- has increased in the last seven years, to more than 60% of Optum Rx’s total business. What happens to the billions of dollars in rebates generated by Optum Rx is impossible to determine from United’s disclosures. However, our best guess is that pharmaceutical rebates represent as much as a quarter of United’s total corporate profits.

Optum Insight: “Intelligent” Business Solutions

The fastest growing and by far the most profitable Optum business is its business intelligence/business services/consulting subsidiary. Optum Insight was generated $12.2 billion in revenues in 2021, but a 27.9% operating margin, five times that of United’s health insurance business. Optum Insight is strategically vital to enhancing the profitability of United’s health insurance activities, but also generates outside revenues selling services to United’s health insurance competitors and hospital networks.

The core of Optum Insight is a business intelligence enterprise formerly known as Ingenix, which provided “big data” to United and other insurers about hospital and pricing behavior and utilization-crucial both for benefits design and administration. In 2009, Ingenix was accused by New York State of under reporting prices for out of network health services for itself and its clients, which had the effect of reducing its own medical reimbursements, and increasing patient cost shares. United signed a consent decree to alter Ingenix business practices and settled a raft of lawsuits filed on behalf of patients, physicians and employers. Its name was subsequently changed to Optum Insight.

By dint of aggressive acquisitions, Optum Insight has dramatically increased its medical claims management business, consulting services and business process outsourcing activities. . Most of United’s investment in artificial intelligence can be found inside Optum Insight. Big data plays a crucial role in United’s overall strategy. Optum Insight’s claims management software uses vast medical claims data bases and artificial intelligence/machine learning software to spot and deny medical claims for which documentation is inadequate or where services are either “inappropriate” or else not covered by an individual’s health plan. Providers also claim that the same software rejects as many as 20% of their claims, often for problems as tiny as a mis-spelled word or a missing data field.

Optum Insight software plays a crucial role in helping United’s health insurance plans manage their medical expense. Traditional health plan profitability is generated by reducing medical expense relative to collected premiums to increase underwriting profit. These profits are regulated, with highly variable degrees of rigor by state health insurance commissioners, and also by provisions of ObamaCare enacted in 2010.

Though its acquisition of Equian in 2019 and the proposed $13 billion acquisition of health information technology conglomerate Change Healthcare in 2021, United came within an eyelash of a near monopoly on “intelligent” medical claims processing software. The Justice Department challenged this latter acquisition and United may agree to divest Change’s claims processing software business as a condition of closing the deal. Even without the Change acquisition, Optum Insight processes hundreds of millions of medical claims annually not only for United’s health insurance business but for many of United’s competitors.

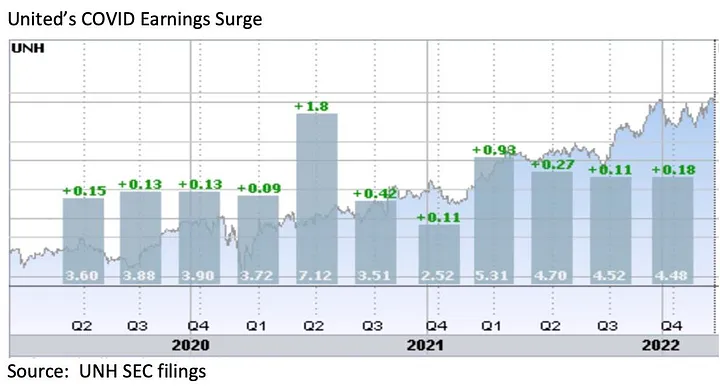

However, Optum Insight’s claims management system can also be used to increase MLR if medical expense unexpectedly declines, exposing the firm to federal requirement that it rebate excessive ‘savings’ to subscribers. This happened in 2020, when the COVID pandemic dramatically and unexpectedly added billions to United’s earnings due to hospitals suspending elective care. The chart below shows United’s 2Q2020 earnings per share almost doubling due to the precipitous drop in its medical claims expenses!

Hospital finance colleagues reported an immediate and substantial drop in medical claims denials from United and other carriers in the summer and fall of 2020. United’s quarterly profits dutifully and steeply declined in the subsequent two quarters, because its medical expenses sharply rebounded. The rise in

United’s medical expenses helped the firm avoid premium rebates to patients required by provisions of the ObamaCare legislation passed in 2010. The firm did voluntarily rebate about $1.5 billion to many of its customers in June, 2020.

However the most rapidly growing part of Optum Insight is its Optum 360 business process outsourcing business, which helps hospitals manage their billing and collections revenue cycle, as well as information technology operations, supply chain (purchasing and materials management) and other services. Through Optum 360, Optum Insight has signed five long term master contracts in the past two years’ worth many billions of dollars with care providers in California, Missouri and other states to provide a broad range of business services.

With all these different businesses, it is theoretically possible for one piece of Optum to be reducing a hospital’s cash flow by denying medical claims for United subscribers, while United’s health insurance network managers bargain aggressively to reduce the hospital’s reimbursement rates while yet another piece of Optum runs the billing and collection services for the same hospital and its employed physicians, while yet another piece of Optum competes with the hospital’s physicians and ambulatory services, diverting patients from its ERs and clinics, reducing the hospital’s revenues.

It is not difficult to imagine a future in which Optum/United offers hospital systems an Optum 360 outsourcing contract that run most of the business operations of a hospital system in exchange for preferred United health plan rates, an AI-enabled EZ pass on its medical claims denials and inpatient referrals from Optum physician groups and urgent care centers, at the expense of competing hospitals.

Managing these potential conflicts will be an increasing challenge as these various businesses grow, placing intense pressure on United’s leadership to get the various pieces of United to work together. To many anxious hospital executives, United resembles nothing so much as the Kraken, rising up out of the sea, surrounding and engulfing them- a powerful friend perhaps or a fearsome foe. As you might expect, United’s growing market power and growth has generated a fierce backlash in the hospital management community.

What Business is United Healthcare In?

United Healthcare is the most successful business in the history of American healthcare. The rapid growth of Optum and continued health insurance enrollment growth from government programs like Medicaid and Medicare has created a cash engine which generates nearly $2 billion a month in free cash flow. Optum’s portfolio has given United an impressive array of tools, unequalled in the industry, to improve its profitability and to reach into every corner of the US health system. United Healthcare is managed care on steroids.

United’s diversified portfolio of businesses gives the firm what a finance-savvy colleague termed “optionality”- the ability to redirect capital and management attention to areas of growth and away from areas that have ceased to grow, in the US or overseas. With its substantial investable capital, it will have the pick of the litter of the 11 thousand digital health companies as the overextended digital health market consolidates. United will be able to use its vast resources to build state-of-the-art digital infrastructure to reach and retain patients and manage their care.

United’s main short term business risks seem to be running out of accretive transactions effectively to deploy its growing horde of capital and managing the firm’s rising political exposure. United has had tremendous business discipline and has shied away from speculative acquisitions that are not immediately accretive to earnings. If its earnings growth falters, however, it will also encounter pressure from the investment community to increase dividends (presently about 1.2%) or share buybacks to bolster its share price, or else divest some or all of Optum in order to “maximize shareholder value”.

Answering the question, “What Business is United In” is simple: just about everything in health but hospitals and nursing homes.

Answering the questions- who are its customers and what do they want? — is a great deal harder. The customers United serves are in a sort of cold war with one another. United’s original business was protecting employers from health cost growth , and tempering the influence of hospitals and doctors by reducing their rates and utilization. By fostering so-called Consumer Directed Health Plans that expose many of their subscribers to very high front-end copayments, United and its health insurance brethren, have also increased their out-of-pocket costs, whether they have the savings to pay them or not.

There are also some ironies in United’s development. Optum Insight’s suite of hospital business services are designed to reduce administrative costs created in major part by United and other insurers’ medical claims data requirements. Its PBM business, originally intended to reduce drug spending by bargaining aggressively with pharmaceutical manufacturers has ended up pushing up drug list prices and consumer cost shares.

While presumably everybody benefits if United can somehow help patients become and remain healthy, it is still far from obvious how to do this. Managing all these markedly divergent customer needs will be a tremendous management challenge for whoever succeeds United’s reclusive (and very effective) 70 year old Chairman Stephen Hemsley.

What Does Society Get from this Vast Enterprise?

However, as Peter Drucker told a different generation of business giants, businesses are not entities unto themselves, accountable only to shareholders and customers. They are organs of society, and are expected to create social value. Americans are suspicious of vast enterprises, as businesses from Standard Oil, US Steel and ATT to Microsoft and Facebook have learned. As businesses grow and become more successful, public suspicion grows.

Private health insurers already face strident opposition from progressive Democrats, who believe that health coverage ought to be a public good, a right of citizenship provided publicly; in other words, that private health insurers have no business being in business. And large insurers like United also face intense opposition from hospitals and many physicians because they reduce their incomes and impose major administrative burdens upon them.

In the age of Twitter and TikTok, United is highly vulnerable to “event risks” that confirm the hostile narratives of the firm’s detractors that United is mainly about maximizing its own profits, not about improving the health of its subscribers or the communities it serves. It is not clear how many the tens of millions of United subscribers have warm and fuzzy feelings about their giant health insurer. Memories of the HMO backlash of the 1990’s reside in the firm’s corporate memory.

United has grown to its present immense scale largely without public knowledge. United has within its reach the capability of constraining overall health cost growth across dozens of metropolitan areas and regions, not merely cost growth for its own beneficiaries (roughly one in seven US citizens already get their health insurance through United). With its expanding digital health operations, it can deploy state of the art tools for helping United’s 50 million subscribers avoid illness and live healthier lives.

United also has the ability to damage the financial operations of beloved local hospitals and deny coverage to families, raising their out of pocket expenses. How United frames and defends its social mission and how it manages all the delicate and increasingly fraught customer relationships will determine its future, and in important ways, ours as well.

Kaiser Permanente on Wednesday announced it is acquiring Geisinger Health, and Geisinger will operate independently under a new subsidiary of Kaiser called Risant Health.

Deal details

The combination of the two companies will need to be reviewed by federal and state agencies, but if approved, the two companies will have more than $100 billion in combined annual revenue.

Geisinger will operate independently as part of Risant Health, which will be headquartered in Washington, D.C. and will be led by Geisinger president and CEO Jaewon Ryu. The health systems said they intend to acquire four or five more hospital systems to fold into Risant in an effort to reach $30 billion to $35 billion in total revenue over the next five years.

In an interview, Ryu and Kaiser chair and CEO Greg Adams said Risant will specifically target hospital systems already working to move into value-based care.

According to Adams, Risant Health “is a way to really ensure that not-for-profit, value-based community health is not only alive but is thriving in this country.”

“If we can take much of what is in our value-based care platform and extend that to these leading community health systems, then we extend our mission,” Adams said. “We reach more people, we drive greater affordability for health care in this country.”

Why we’re ‘cautiously optimistic’ about this acquisition

Just when you thought healthcare couldn’t get more interesting, Kaiser and Geisinger announce their union through newly established Risant Health. At first pass, it is hard to see a downside with this deal — and that’s something that raises my “spidey-senses.”

Kaiser and Geisinger are coming together through a vehicle that could allow them to clear an increasingly skeptical Federal Trade Commission. It affords two health systems — both in comparatively weaker financial positions than before the pandemic — the ability to get bigger through the merger. Its pitch is decidedly hospital- (and in the future provider) led, with Geisinger retaining its brand and elevating its CEO to the head of Risant. It also gives Geisinger and future partners the latitude to pursue their own payer relationships.

In addition, it is ostensibly a play to increase providers’ control over the nature and pace of value-based care (VBC) adoption. In its press release, Kaiser acknowledges that its closed network model of care management hasn’t scaled well to other markets. And Geisinger, with its own health plan and a track-record of developing its own VBC incentives, is no neophyte and brings a clear wealth of expertise.

Without a doubt, the offer to future partners is compelling: “Come for the size and stay for the value-based care.” But like all things in life, it’s all in the details. And that’s where my “spidey-sense” kicks in.

Partnership and affiliation models alone do not make the hard work of VBC easier. While this emerging group could become a valuable, provider-led clearing house for VBC concepts, applying them in communities remains a stubborn challenge that requires individual work and leadership.

The true test of the concept will come when the first new partner joins. How they decide to participate and whether the model has the right mix of scale and flexibility is what I’ll be watching closely. The overall objective and success measure of this endeavor remains somewhat opaque, but I would say that the concept has real legs here. Right now, I’m leaning toward “cautiously optimistic.”