Minneapolis-based Allina Health System’s move to turn away patients with outstanding debt is a cost-saving measure is not uncommon, according to the Lown Institute.

Allina provides emergency care to indebted patients, but they can be cut off for other services if they have a certain amount of unpaid debt,The New York Times found. A spokesperson for Allina confirmed to the Times that it cut off patients only if they have at least $1,500 of unpaid debt three separate times.

A 2022 investigation from KFF Health News found 55 hospitals allow denials of nonemergency care for patients with medical debt, and 22 said the practice is allowed but not current practice.

Allina’s refusal of care for indebted patients could contribute to medical debt, the Lown Institute said in a June 2 report. Allina is a nonprofit hospital and is required to offer financial assistance to patients who cannot afford services. However, there are no federal regulations regarding how much hospitals have to spend on financial assistance or who can be eligible. When groups refuse care, it can make it harder for patients to get help.

According to the Lown Institute, Allina skirted $266 million in taxes in 2020 from its nonprofit status and spent $57 million on financial assistance and community investment. It could have spent $209 million more to reach its tax exemption value.

The news of Optum’s bid to acquire Amedisys came as a surprise — but it fits a larger theme of payers, particularly Medicare Advantage plans, looking to acquire assets to build out a home ecosystem.

In recent years, we’ve seen this play out in a number of ways, with some buyers finding success in their endeavors and others selling off the asset shortly after acquisition. While some buyers, including payers and other providers, have been able to capitalize on owning home health assets, others have struggled to benefit financially.

The drivers

When acquiring a home health agency, payers’ objectives are largely centered around operating costs and the ability to refer as many of their patients to these organizations as possible. If the agency is not delivering a return on investment or is unable to refer enough patients, payers are not afraid to divest and reevaluate structure.

Despite these varying outcomes, the race is on to acquire home-based care assets. We suspect there are two main reasons:

1. Home-based care is a cost-effective alternative

Payers want to direct their members from acute care back to the home without a skilled nursing stay. Especially for Medicare Advantage patients, there is a financial incentive to avoid sending patients to a skilled nursing facility (SNF).

Amid the push to improve patient quality, SNFs are often seen as a cost center that payers are eager to cut out — leading many to invest in home health agencies and services.

2. Home-based care operators need to grow their workforce

All home-based care operators, whether part of a payer organization or not, need to grow their workforce. According to our research, this was the number one factor hindering the expansion of home-based care.

By adding Amedisys’s workforce to their own existing home-based care workforce, Optum could help overcome this challenge.

Optum’s interest in Amedisys is also notable because of the diversity of services that Amedisys offers. Not only do they support home health, but they also offer hospital at home services through Contessa as well as home-based palliative and hospice care. That’s an attractive suite of services for a Medicare Advantage payer interested in offering more care in the home.

What we’ll be watching

It’s still unclear what will happen with Optum’s offer for Amedisys. Even if Amedisys agrees to the acquisition, the deal is likely to face FTC scrutiny. If that does happen, we’ll be watching to see whether Optum has to divest from any of Amedisys’ assets as part of an eventual deal.

With the continued rise in seniors who require skilled care — most of whom would prefer to age in the home — investments and divestments in the home health space will continue to make headlines.

Moving forward, we’ll be paying close attention to the outcomes of larger home health acquisitions by payer organizations.

Specifically, we’ll be watching to see if they’re able to successfully move their members away from facility-based care and into the home, both in terms of quality and the bottom line.

Academic medicine combines healthcare with higher education, the two sectors of the American economy that have exhibited outsized cost growth during the past 50 years. The result is a stunning disconnection between the business practices of academic medical centers (AMCs) and the supply-demand dynamics reshaping healthcare delivery.

Market, technological and regulatory forces are pushing the healthcare industry to deliver higher-value care that generates better outcomes at lower costs. A parallel movement is shifting resources out of specialty and acute care services into primary, preventive, behavioral health and chronic disease care services. In the process, care delivery is decentralizing and becoming more consumer-centric.

AMCs Double Down

Counter to these trends, academic medicine is doubling down on high-cost, centralized, specialty-focused care delivery. Privilege has its price. Several AMCs — including Mass General Brigham, IU Health, UCSF, Ohio State and UPMC — are undertaking multibillion-dollar expansions of their existing campuses. Collectively, AMCs expect American society to fund their continued growth and profitability irrespective of cost, effectiveness and contribution to health status.

Despite being tax-exempt and having access to a large pool of free labor (residents), AMCs charge the highest treatment prices in most markets. [1] Archaic formulas allocate residency “slots” and lucrative Graduate Medical Education payments (over $20 billion annually) disproportionately into specialty care and more-established AMCs. Given their cushy funding arrangements, it’s no wonder AMCs fight vigorously to maintain an out-of-date status quo.

Legacy practices from the early 1900s still dominate medical education, medical research and clinical care. Like tenured faculty, academic physicians manage their practices with little interference. Clinical deans rule their departments with a free hand. With few exceptions, interdisciplinary coordination is an oxymoron. The result is fragmented care delivery that tolerates duplication, medical error and poor patient service.

Irresistible consumerism confronts immovable institutional inertia. As exhibited by substantial operating losses at many AMCs, their foundations are beginning to crack. [2]

Medicine’s Rise from Poverty to Prosperity

In his 1984 Pulitzer Prize-winning work, Paul Starr chronicles the social transformation of American medicine during the 19th and 20th centuries. Prior to the 1900s, doctors had low social status. Most care took place in the home. Pay was low. The profession lacked professional standards. There were too many quacks. Most doctors lived hand-to-mouth.

As the century turned, several cultural, economic, scientific and legal developments converged to elevate the profession’s status in American society. Stricter licensing reduced the supply of physicians and closed most existing medical schools. Legislation and legal rulings restricted corporate ownership of medical practices and enshrined physicians’ operating autonomy. Scientific breakthroughs gave medicine more healing power.

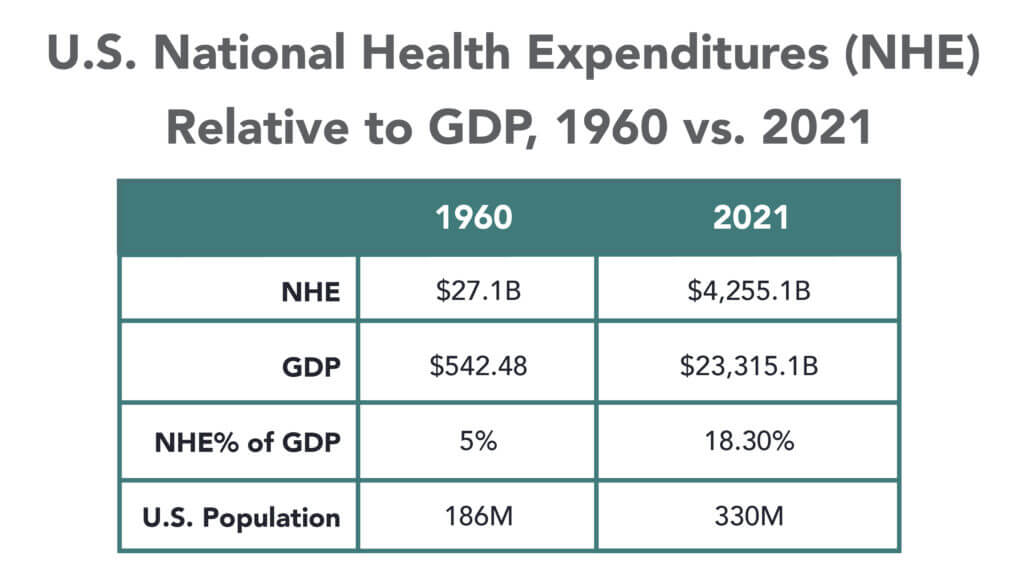

Through the decades that followed, the American Medical Association and state medical societies frustrated external attempts to control medical delivery externally and institute national health insurance. They insisted on fee-for-service payment and the absolute right of patients to choose their doctors. These are causal factors underlying healthcare’s skyrocketing cost increases, growing from 5% of the U.S. gross domestic product (GDP) in 1960 to over 18% in 2021.

Academic and community-based physicians have always had a tenuous relationship. Status and prestige accompany academic affiliations. Academic practices require referrals from community physicians but rarely consult with them on treatment protocols. For their part, community physicians marvel at the lack of market awareness exhibited by academic practices. They have tolerated one another to perpetuate collective physician control over healthcare operations.

Incomes and prestige for both community and academic physicians rose as the medical profession limited practitioner supply, established payment guidelines, encouraged specialization, controlled service delivery and socialized capital investment. One hundred years later, the business of healthcare still exhibits these characteristics. Gleaming new medical centers testify to the profession’s success in socializing capital investment and maintaining autonomy over hospital operations.

Entrenched beliefs and behaviors explain why most hospitals, despite their high construction costs, are largely deserted after 4 p.m. and on weekends. They explain the maldistribution of facilities and practitioners. They explain the overdevelopment of specialty care. They explain the underinvestment in preventive care, mental health services and public health.

Value-Focused Backlash Portends Reckoning

These beliefs and behaviors are contributing to AMC’s current economic dislocation. Dependent upon public subsidies and premium treatment payments to maintain financial sustainability, high-cost AMCs are particularly vulnerable to value-based competitors.

The marketplace is attacking inefficient clinical care with tech-savvy, consumer-friendly business models. Care delivery is decentralizing even as many AMCs invest more heavily in campus-based medicine. A market-based reckoning confronts academic medicine.

A visit up north illustrates the general unwillingness of academic physicians to accept market realities and their continued insistence on maintaining full control over the academic medical enterprise. It’s like watching a train wreck occur in slow motion.

Minnesota Madness

After experiencing severe economic distress, the University of Minnesota sold its University of Minnesota Medical Center (UMMC) to Fairview Health in 1997. Fairview currently operates UMMC in partnership with the University of Minnesota Physicians (UMP) under the banner of M Health Fairview.

In September 2022, Sanford Health and Fairview Health signed a letter of intent to merge. The new combined company would bear the Sanford name with its headquarters in Sioux Falls, South Dakota. Despite the opportunity to double its catchment area for specialty referrals, the University and UMP oppose the merger with Sanford. They fear out-of-state ownership could compromise the integrity of UMMC’s operations.

Fairview wants the Sanford merger to help it address massive operating losses resulting, in part, from its contractual arrangements with UMP. Negotiations between the parties have become acrimonious. Amid the turmoil, the University and UMP announced in January 2023 their intention to acquire UMMC from Fairview and build a new state-of-the-art medical center on the University’s Minneapolis campus.

The University has named this proposal “MPact Health Care Innovation.” It calls for the Minnesota state legislature to fund the multibillion-dollar cost of acquiring, building and operating the new medical enterprise. Typical of academic medical practices, UMP expects external sources to pony up the funding to support their high-cost centralized business model while they continue to call the shots.

The arrogance and obliviousness of the University’s proposal is staggering. Minnesota struggles with rising rates of chronic disease and inequitable healthcare access for low-income urban and rural communities. The idea that a massive governmental investment in academic medicine will “bridge the past and future for a healthier Minnesota” as the MPact tagline proclaims is ludicrous.

Out of Touch

Like the rest of the country, Minnesota is experiencing declining life expectancy. Despite spending more than double the average per-capita healthcare cost of other wealthy countries, the United States scores among the worst in health status measures. Spending more on high-end academic medicine won’t change these dismal health outcomes. Spending more on preventive care, health promotion and social determinants of health could.

The real gem in the University of Minnesota’s medical enterprise is its medical school. It has trained 70% of the state’s physicians. It ranks third and fourth nationally in primary care and family medicine. It is advancing a progressive approach to interdisciplinary and multi-professional care.

If the Minnesota state legislature really wants to advance health in Minnesota, it should expand funding for the University’s aligned health schools and community-based programs without funding the acquisition and expansion of the University’s clinical facilities.

No Privilege Without Performance

Our nation must stop enabling academic medicine’s excesses. Funding AMCs’ insatiable appetite for facilities and specialized care delivery is counterproductive. It is time for academic medicine to embrace preventive health, holistic care delivery and affordable care access.

Privilege comes with responsibility. AMCs that resist the pivot to value-based care and healthier communities deserve to lose market relevance.

America has the means to create a healthier society. It requires shifting resources out of healthcare into public health. We must have the will to make community-based health networks a reality. It starts by saying no to needless expansion of acute care facilities.

The median year-to-date operating margin index for hospitals improved slightly in April to 0 percent. While recent reports show signs of improving margins, they remain far below historical norms, and inflation and workforce expenses continue to challenge hospitals’ bottom lines.

“Hospital and health system leaders must figure out how to navigate the new financial reality and begin to take action,” Erik Swanson, senior vice president of data and analytics with Kaufman Hall, said in a May 31 report. “In the face of operating margins that may never fully recover and inflated expenses, developing and executing a strategic path forward to a future that is financially sustainable is crucial.”

Here are 29 health systems ranked by their operating margins in the first quarter:

Correction: An earlier version incorrectly referenced a Texas deal between Houston Methodist and Baylor Scott and White. News about deals is sensitive and unnecessarily disruptive to reputable organizations like these. I sourced this news from a reputable deal advisor: it was inaccurate. My apology!

Congressional Republicans and the White House spared Main Street USA the pain of defaulting on the national debt last week. No surprise.

Also not surprising: another not-for-profit-mega deal was announced:

St. Louis, MO-based BJC HealthCare and Kansas City, MO-based Saint Luke’s Health System announced their plan to form a $9.5B revenue, 28-hospital system with facilities in Missouri, Kansas, and Illinois.

This follows recent announcements by four other NFP systems seeking the benefits of larger scale:

Gundersen Health System & Bellin Health (Nov 2022): 11 hospitals, combined ’22 revenue of $2.425B

Froedtert Health & ThedaCare (Apr 2023 LOI): 18 hospitals, combined ’22 revenues of $4.6B

And all these moves are happening in an increasingly dicey environment for large, not-for-profit hospital system operators:

Increased negative media attention to not-for-profit business practices that, to critics, appear inconsistent with a “NFP” organization’s mission and an inadequate trade for tax exemptions each receives.

Decreased demand for inpatient services—the core business for most NFP hospital operations. Though respected sources (Strata, Kaufman Hall, Deloitte, IBIS et al) disagree somewhat on the magnitude and pace of the decline, all forecast decreased demand for traditional hospital inpatient services even after accounting for an increasingly aging population, a declining birthrate, higher acuity in certain inpatient populations (i.e. behavioral health, ortho-neuro et al) and hospital-at-home services.

Increased hostility between national insurers and hospitals over price transparency and operating costs.

Increased employer, regulator and consumer concern about the inadequacy of hospital responsiveness to affordability in healthcare.

And heightened antitrust scrutiny by the FTC which has targeted hospital consolidation as a root cause of higher health costs and fewer choices for consumers. This view is shared by the majorities of both parties in the House of Representatives.

In response, Boards and management in these organizations assert…

Health Insurers—especially investor-owned national plans—enjoy unfettered access to capital to fund opportunistic encroachment into the delivery of care vis a vis employment of physicians, expansion of outpatient services and more.

Private equity funds enjoy unfettered opportunities to invest for short-term profits for their limited partners while planning exits from local communities in 6 years or less.

The payment system for hospitals is fundamentally flawed: it allows for underpayments by Medicaid and Medicare to be offset by secret deals between health insurers and hospitals. It perpetuates firewalls between social services and care delivery systems, physical and behavioral health and others despite evidence of value otherwise. It requires hospitals to be the social safety net in every community regardless of local, state or federal funding to offset these costs.

These reactions are understandable. But self-reflection is also necessary. To those outside the hospital world, lack of hospital price transparency is an excuse. Every hospital bill is a surprise medical bill. Supporting the community safety net is an insignificant but manageable obligation for those with tax exemption status. Advocacy efforts to protect against 340B cuts and site-neutral payment policies are about grabbing/keeping extra revenue for the hospital. What is means to be a “not-for-profit” anything in healthcare is misleading since moneyball is what all seem to play. And short of government-run hospitals, many think price controls might be the answer.

My take:

The headwinds facing large not-for-profit hospitals systems are strong. They cannot be countered by contrarian messaging alone.

What’s next for most is a new wave of operating cost reductions even as pre-pandemic volumes are restored because the future is not a repeat of the past. Being bigger without operating smarter and differently is a recipe for failure.

What’s necessary is a reset for the entire US health system in which not-for-profit systems play a vital role. That discussion should be led by leaders of the largest NFP systems with the full endorsements of their boards and support of large employers, physicians and public health leaders in their communities.

Everything must be on the table: funding, community benefits, tax exemption, executive compensation, governance, administrative costs, affordability, social services, coverage et al. And mechanisms for inaction and delays disallowed.

It’s a unique opportunity for not-for-profit hospitals. It can’t wait.

More than a year after launching an in-house travel staffing agency, UPMC is adding a new regional approach to the effort.

Maribeth McLaughlin, MPM, BSN, RN, chief nursing executive for the Pittsburgh-based health system, told Becker’s the approach provides a new option for nurses and surgical technologists who desire to travel.

“Our overall travel program, when you travel for us, you travel across our hospitals in New York, Maryland and Pennsylvania,” she said. “And now we are launching a regional travel strategy where some staff can choose to travel only within certain regions.”

UPMC initially announced in December 2021 that it had created UPMC Travel Staffing, a new in-house travel staffing agency to address a nursing shortage and to attract and retain workers.

Through the agency, nurses and surgical technologists earn $85 an hour and $63 an hour, respectively, in addition to a $2,880 stipend at the beginning of each six-week assignment.

Ms. McLaughlin said the rate is lower — about $60 an hour — for those who opt for the regional approach.

As of June 1, UPMC has hired more than 700 staff into the in-house travel staffing agency, with 60 percent of those workers being external hires, according to Ms. McLaughlin. And there have been fewer workers leaving UPMC to go to other travel agencies.

“One of my goals since I’ve taken this role is to really look at building in as many flexible programs as I could for staff,” said Ms. McLaughlin, who has served in her current role since August 2022. “I think as we came out of the pandemic, it’s clear to me that work-life harmony means something different to staff today than it maybe meant when I was a young staff nurse years ago, and that we need to have as much flexibility and as many different programs as we can.”

She said UPMC Travel Staffing has delivered this flexibility and allowed the health system to cancel about 90 contracts with external travel agencies. Additionally, some external travelers have now moved into UPMC’s in-house agency. Ms. McLaughlin expects more to join the in-house agency now that UPMC has launched the regional approach.

“We’re launching a win-back program where we’re going out and trying to see some of the people who we know we lost and see if they’re interested in coming back closer to home and traveling closer to home,” she explained.

Still, she acknowledged some of the challenges along the way.

“Our IT department built us an app to be able to manage all of this because, as you can imagine, we have external travel, internal travelers, core staff and at times it could get a little confusing,” said Ms. McLaughlin. “So we’ve been able to build that to be able to figure out the best ways to assign the staff where the greatest needs are.”

Another challenge she noted is that shifts for workers from external travel agencies are often 12 weeks, while shifts with UPMC Travel Staffing are six weeks. She said this is a purposeful move because those in UPMC Travel Staffing receive benefits and are considered UPMC employees, rather than receiving an hourly rate.

“Overall, it’s been a really successful program for us because it’s allowed us to look at things in a different way,” said Ms. McLaughlin. “It’s a central function. It’s not something we did and farmed out to every hospital to administer themselves. We did it as a system and as a core, which I also think is important.”

Now, she said she’s excited about the new regional approach and the opportunities it presents for recruiting and retention.

“We’re growing our own students, we’re bringing in all these students, and we’re not saying, ‘You have to just work here.’ We’re saying, ‘You can work for us at UPMC, and here are all the options. You can even be a traveler with us,'” she said.