As Donald Trump begins his second term, America’s healthcare system is in crisis: medical costs are skyrocketing, life expectancy has stagnated, and burnout runs rampant among healthcare workers.

These problems are likely to become worse now that Trump has handed the federal budget over to Elon Musk. The world’s richest man now co-heads the Department of Government Efficiency (DOGE), a non-government entity tasked with slashing $500 billion in “wasteful” spending.

The harsh reality is that Musk’s mission can’t succeed without gutting healthcare access and coverage for millions of Americans.

Deleting dollars from American healthcare

Since Trump’s first term, the country’s economic outlook has worsened significantly. In 2016, the national debt was $19 trillion, with $430 billion allocated to annual interest payments. By 2024, the debt had nearly doubled to $36 trillion, requiring $882 billion in debt service—12% of federal spending that is legally untouchable.

Add to that another 50% of government expenditures that Trump has deemed politically off-limits: Social Security ($1.35 trillion), Medicare ($848 billion) and Defense ($1.13 trillion). That leaves just $2.6 trillion—less than 40% of the $6.75 trillion federal budget—available for cuts.

In a recent op-ed, Musk and DOGE co-chair Vivek Ramaswamy proposed eliminating expired or misused funds for programs like Public Broadcasting and Planned Parenthood, but these examples account for less than $3 billion total—not even 1% of their target.

This shortfall will require Musk to cut billions in government healthcare spending. But where will he find it?

With Medicare off limits to DOGE, the options for major reductions are extremely limited. Big-ticket healthcare items like the $300 billion in tax-deductibility for employer-sponsored health insurance and $120 billion in expired health programs for veterans will prove politically untouchable. One will raise taxes for 160 million working families and the latter will leave veterans without essential medical care.

This means DOGE will have to attack Medicaid and the ACA health exchanges. Here’s how 20 million people will likely lose coverage as a result.

1. Reduced ACA exchange funding

Since its enactment in 2010, the Affordable Care Act (ACA) has provided premium subsidies to Americans earning 100% to 400% of the federal poverty level. For lower-income families, the ACA also offers Cost Sharing Reductions, which help offset deductibles and co-payments that fund 30% of total medical costs per enrollee. Without CSRs, a family of four earning $40,000 could face deductibles as high as $5,000 before their insurance benefits apply.

If Congress allows CSR payments to expire in 2026, federal spending would decrease by approximately $35 billion annually. If that happens, the Congressional Budget Office expects 7 million individuals to drop out of the exchanges. Worse, without affordable coverage alternatives, 4 million families would lose their health insurance altogether.

2. Slashing Medicaid coverage and tightening eligibility

Medicaid currently provides healthcare for over 90 million low-income Americans, including children, seniors and individuals with disabilities. To meet DOGE’s $500 billion goal, several cost-cutting strategies appear likely:

Reversing Medicaid expansion: The ACA expanded Medicaid eligibility to those earning up to 138% of the federal poverty level, reducing the uninsured rate from 16% to 8%. Undoing this expansion would strip coverage from millions in the 40 states that adopted the program.

Imposing work requirements: Proponents argue this could encourage employment, but most Medicaid recipients already work for employers that don’t provide insurance. In reality, work requirements primarily create bureaucratic barriers that disqualify millions of eligible individuals, reducing program costs at the expense of coverage.

Switching to block grants: Unlike the current Medicaid system, which adjusts funding based on need, less-expensive block grants would provide states with fixed allocations. This will, however, force them to cut services and reduce enrollment.

Medicaid currently costs $800 billion annually, with the federal government covering 70%. Reducing enrollment by 10% (9 million people) could save over $50 billion annually, while a 20% reduction (18 million people) could save $100 billion.

Either outcome would devastate families by eliminating access to vital services including prenatal care, vaccinations, chronic disease management and nursing home care. As states are forced to absorb the financial burden, they’ll likely cut education budgets and reduce infrastructure investments.

The first 100 days

The numbers don’t lie: Musk and DOGE could slash Medicaid funding and ACA subsidies to achieve much of their $500 billion target. But the human cost of this approach would be staggering.

Fortunately, there are alternative solutions that would reduce spending without sacrificing quality. Shifting provider payments in ways that reward better outcomes rather than higher volumes, capping drug prices at levels comparable to peer nations, and leveraging generative AI to improve chronic disease management could all drive down costs while preserving access to care.

These strategies address the root causes of high medical spending, including chronic diseases that, if better managed, could prevent 30-50% of heart attacks, strokes, cancers, and kidney failures according to CDC estimates.

Yet, in their pursuit of immediate budgetary cuts, Musk and DOGE have omitted these kinds of reform options. As a result, the health of millions of Americans is at major risk.

In late 2025, two events reset the U.S. health system’s future at least through 2026 and possibly beyond:

November 5, 2024: The Election: Its post-mortem by pollsters and pundits reflects a country divided and unsettled: 22 Red States, 7 Swing States and 21 Blue States. But a solid majority who thought the country was heading in the wrong direction and their financial insecurity driving voters to return the 45th President to the White House. With slim majorities in the House and Senate, and a short-leash before mid-term elections November 3, 2026, the Trump team has thrown out ‘convention’ in their setting policies and priorities for their second term. That includes healthcare.

December 4, 2024: The Murder of a Health Executive : The murder of Brian Thompson, United Healthcare CEO, sparked hostility toward health insurers and a widespread backlash against the corporatization of the U.S. health system. While UHG took the most direct hit for its aggressiveness in managing access and coverage disputes, social media and mainstream journalists exposed what pollsters affirmed—the majority of American’s distrust the health system, believing it puts its profits above their needs. And their polls indicate animosity is highest among young adults, in lower income households and among members of its own workforce.

These events provide the backdrop for what to expect this year and next. Four directional shifts seem to underly actions to date and announced plans:

From elitism to populism: Key personnel and policy changes will draw less from Ivy League credentials, DC connections and recycled federal health agency notables and more from private sector experience, known disruptors and unconventional thought leaders. Notably, the new Chairs of the 7 Congressional Committees that control healthcare regulation, funding and policy changes in the 119th Congress represent LA, AL, WV, ID, VA, MO & KY constituents—hardly Ivy League territory.

From workforce disparities to workforce modernization: The Departments of Health & Human Services, Labor, Commerce and Treasury will attempt to suspend/modify regulatory mandates and entities they deem derived from woke ideology. The Trump team will replace them with policies that enable workforce de-regulation and modernization in the private sector. Hiring quotas, non-compete contracts, DEI et al will get a fresh look in the context of technology-enabled workplaces and supply-demand constraints. The HR function in every organization will become ground zero for Trump Healthcare 2.0 system transformation.

From western medicine to whole person wellbeing: HHS Secretary Nominee Robert F. Kennedy Jr. (RFK) Jr.’s “Make America Healthy Again” pledges war on ultra-processed foods. CMS’ designee Mehmet Oz advocates for vitamins, supplements and managed care. FDA nominee Marty Makary, a Hopkins surgeon, is a RFKJ ally in the “Health Freedom” movement promoting suspicion about ‘mainstream medicine’ and raising doubts about vaccination efficacy for children and low-risk adults. NIH nominee Jay Bhattacharya, director of Stanford’s Center for Demography and Economics of Health and Aging, opposed Covid-19 lockdowns and is critical of vaccine policies. Collectively, this four-some will challenge conventional western (allopathic) medicine and add wide-range of non-traditional interventions that are a safe and cost-effective to the treatment arsenal for providers and consumers. The food supply will be a major focus: HHS will work closely with the USDA (nominee Brooke Rollins, currently CEO of the America First Policy Institute, to reduce the food chain’s dependence on ultra-processed foods in public health.

From DC dominated health policies to states: The 2022 Supreme Court’ Dobbs decision opened the door for states to play the lead role in setting policies for access to abortion for their female citizens. It follows federalism’s Constitutional preference that Washington DC’s powers over states be enumerated and limited. Thus, state provisions about healthcare services for its citizens will expand beyond their already formidable scope. Likely actions in some states will include revised terms and conditions that facilitate consolidation, allowance for physician owned hospitals and site-neutral payments, approval of “skinny” individual insurance policies that do not conform to the Affordable Care Act’s qualified health plan spec’s, expanded scope of practice for nurse practitioners, drug price controls and many others. At least for the immediate future, state legislatures will be the epicenters for major policy changes impacting healthcare organizations; federal changes outside appropriations activity are unlikely.

Transforming the U.S. health system is a bodacious ambition for the incoming Trump team. Early wins will be key—like expanding price transparency in every healthcare sector, softening restrictions on private equity investments, targeted cuts in Medicaid and Medicare funding and annulment of the Inflation Reduction Act. In tandem, it has promised to cut Federal government spending by $2 trillion and lower prices on everything including housing and healthcare—the two spending categories of highest concern to the working class. Healthcare will figure prominently in Team Trump’s agenda for 2025 and posturing for its 2026 mid-term campaign. And equally important, healthcare costs also figure prominently in quarterly earnings reports for companies that provide employee health benefits forecast to be 8% higher this year following a 7% spike the year prior. Last year’s 23% S&P growth is not expected to repeat this year raising shareholder anxiety and the economy’s long-term resilience and the large roles housing and healthcare play in its performance.

My take:

The 2024 election has been called a change election. That’s unwelcome news to most organizations in healthcare, especially the hospitals, physicians, post-acute providers and others who provide care to patients and operate at the bottom of the healthcare pyramid.

Equipping a healthcare organization to thoughtfully prepare for changes amidst growing uncertainty requires extraordinary time and attention by management teams and their Boards. There are no shortcuts. Before handicapping future state scenario possibilities, contingencies and resource requirements, a helpful starting point is this: On the four most pressing issues facing every U.S. healthcare company/organization today, Boards and Management should discuss…

Trust: On what basis can statements about our performance be verified? Is the data upon which our trust is based readily accessible? Does the organization’s workforce have more or less trust than outside stakeholders? What actions are necessary to strengthen/restore trust?

Purpose: Which stakeholder group is our organization’s highest priority? What values & behaviors define exceptional leadership in our organization? How are they reflected in their compensation?

Affordability: How do we measure and monitor the affordability of our services to the consumers and households we ultimately depend? How directly is our organization’s alignment of reducing cost reduction and pass-through savings to consumers? Is affordability a serious concern in our organization (or just a slogan)?

Scale: How large must we be to operate at the highest efficiency? How big must we become to achieve our long-term business goals?

This week, thousands of healthcare’s operators will be in San Francisco (JPM Healthcare Conference), Naples (TGI Leadership Conference) and in Las Vegas (Consumer Electronics Show) as healthcare begins a new year. No one knows for sure what’s ahead or who the winners and losers will be. What’s for sure is that healthcare will be in the spotlight and its future will not be a cut and paste of its past.

PS: The parallels between radical changes facing the health system and other industries is uncanny. College athletics is no exception. As you enjoy the College Football Final Four this weekend, consider its immediate past—since 2021, the impact of Name, Image and Likeness (NIL) monies on college athletics, and its immediate future–pending regulation that will codify permanent revenue sharing arrangements (to be implemented 2026-2030) between college athletes, their institutions and sponsors. What happened to the notion of student athlete and value of higher education? Has the notion of “not-for-profit” healthcare met a similar fate? Or is it all just business?

In late 2025, two events reset the U.S. health system’s future at least through 2026 and possibly beyond:

November 5, 2024: The Election: Its post-mortem by pollsters and pundits reflects a country divided and unsettled: 22 Red States, 7 Swing States and 21 Blue States. But a solid majority who thought the country was heading in the wrong direction and their financial insecurity driving voters to return the 45th President to the White House. With slim majorities in the House and Senate, and a short-leash before mid-term elections November 3, 2026, the Trump team has thrown out ‘convention’ in their setting policies and priorities for their second term. That includes healthcare.

December 4, 2024: The Murder of a Health Executive : The murder of Brian Thompson, United Healthcare CEO, sparked hostility toward health insurers and a widespread backlash against the corporatization of the U.S. health system. While UHG took the most direct hit for its aggressiveness in managing access and coverage disputes, social media and mainstream journalists exposed what pollsters affirmed—the majority of American’s distrust the health system, believing it puts its profits above their needs. And their polls indicate animosity is highest among young adults, in lower income households and among members of its own workforce.

These events provide the backdrop for what to expect this year and next. Four directional shifts seem to underly actions to date and announced plans:

From elitism to populism: Key personnel and policy changes will draw less from Ivy League credentials, DC connections and recycled federal health agency notables and more from private sector experience, known disruptors and unconventional thought leaders. Notably, the new Chairs of the 7 Congressional Committees that control healthcare regulation, funding and policy changes in the 119th Congress represent LA, AL, WV, ID, VA, MO & KY constituents—hardly Ivy League territory.

From workforce disparities to workforce modernization: The Departments of Health & Human Services, Labor, Commerce and Treasury will attempt to suspend/modify regulatory mandates and entities they deem derived from woke ideology. The Trump team will replace them with policies that enable workforce de-regulation and modernization in the private sector. Hiring quotas, non-compete contracts, DEI et al will get a fresh look in the context of technology-enabled workplaces and supply-demand constraints. The HR function in every organization will become ground zero for Trump Healthcare 2.0 system transformation.

From western medicine to whole person wellbeing: HHS Secretary Nominee Robert F. Kennedy Jr. (RFK) Jr.’s “Make America Healthy Again” pledges war on ultra-processed foods. CMS’ designee Mehmet Oz advocates for vitamins, supplements and managed care. FDA nominee Marty Makary, a Hopkins surgeon, is a RFKJ ally in the “Health Freedom” movement promoting suspicion about ‘mainstream medicine’ and raising doubts about vaccination efficacy for children and low-risk adults. NIH nominee Jay Bhattacharya, director of Stanford’s Center for Demography and Economics of Health and Aging, opposed Covid-19 lockdowns and is critical of vaccine policies. Collectively, this four-some will challenge conventional western (allopathic) medicine and add wide-range of non-traditional interventions that are a safe and cost-effective to the treatment arsenal for providers and consumers. The food supply will be a major focus: HHS will work closely with the USDA (nominee Brooke Rollins, currently CEO of the America First Policy Institute, to reduce the food chain’s dependence on ultra-processed foods in public health.

From DC dominated health policies to states: The 2022 Supreme Court’ Dobbs decision opened the door for states to play the lead role in setting policies for access to abortion for their female citizens. It follows federalism’s Constitutional preference that Washington DC’s powers over states be enumerated and limited. Thus, state provisions about healthcare services for its citizens will expand beyond their already formidable scope. Likely actions in some states will include revised terms and conditions that facilitate consolidation, allowance for physician owned hospitals and site-neutral payments, approval of “skinny” individual insurance policies that do not conform to the Affordable Care Act’s qualified health plan spec’s, expanded scope of practice for nurse practitioners, drug price controls and many others. At least for the immediate future, state legislatures will be the epicenters for major policy changes impacting healthcare organizations; federal changes outside appropriations activity are unlikely.

Transforming the U.S. health system is a bodacious ambition for the incoming Trump team. Early wins will be key—like expanding price transparency in every healthcare sector, softening restrictions on private equity investments, targeted cuts in Medicaid and Medicare funding and annulment of the Inflation Reduction Act. In tandem, it has promised to cut Federal government spending by $2 trillion and lower prices on everything including housing and healthcare—the two spending categories of highest concern to the working class. Healthcare will figure prominently in Team Trump’s agenda for 2025 and posturing for its 2026 mid-term campaign. And equally important, healthcare costs also figure prominently in quarterly earnings reports for companies that provide employee health benefits forecast to be 8% higher this year following a 7% spike the year prior. Last year’s 23% S&P growth is not expected to repeat this year raising shareholder anxiety and the economy’s long-term resilience and the large roles housing and healthcare play in its performance.

My take:

The 2024 election has been called a change election. That’s unwelcome news to most organizations in healthcare, especially the hospitals, physicians, post-acute providers and others who provide care to patients and operate at the bottom of the healthcare pyramid.

Equipping a healthcare organization to thoughtfully prepare for changes amidst growing uncertainty requires extraordinary time and attention by management teams and their Boards. There are no shortcuts. Before handicapping future state scenario possibilities, contingencies and resource requirements, a helpful starting point is this: On the four most pressing issues facing every U.S. healthcare company/organization today, Boards and Management should discuss…

Trust: On what basis can statements about our performance be verified? Is the data upon which our trust is based readily accessible? Does the organization’s workforce have more or less trust than outside stakeholders? What actions are necessary to strengthen/restore trust?

Purpose: Which stakeholder group is our organization’s highest priority? What values & behaviors define exceptional leadership in our organization? How are they reflected in their compensation?

Affordability: How do we measure and monitor the affordability of our services to the consumers and households we ultimately depend? How directly is our organization’s alignment of reducing cost reduction and pass-through savings to consumers? Is affordability a serious concern in our organization (or just a slogan)?

Scale: How large must we be to operate at the highest efficiency? How big must we become to achieve our long-term business goals?

This week, thousands of healthcare’s operators will be in San Francisco (JPM Healthcare Conference), Naples (TGI Leadership Conference) and in Las Vegas (Consumer Electronics Show) as healthcare begins a new year. No one knows for sure what’s ahead or who the winners and losers will be. What’s for sure is that healthcare will be in the spotlight and its future will not be a cut and paste of its past.

PS: The parallels between radical changes facing the health system and other industries is uncanny. College athletics is no exception. As you enjoy the College Football Final Four this weekend, consider its immediate past—since 2021, the impact of Name, Image and Likeness (NIL) monies on college athletics, and its immediate future–pending regulation that will codify permanent revenue sharing arrangements (to be implemented 2026-2030) between college athletes, their institutions and sponsors. What happened to the notion of student athlete and value of higher education? Has the notion of “not-for-profit” healthcare met a similar fate? Or is it all just business?

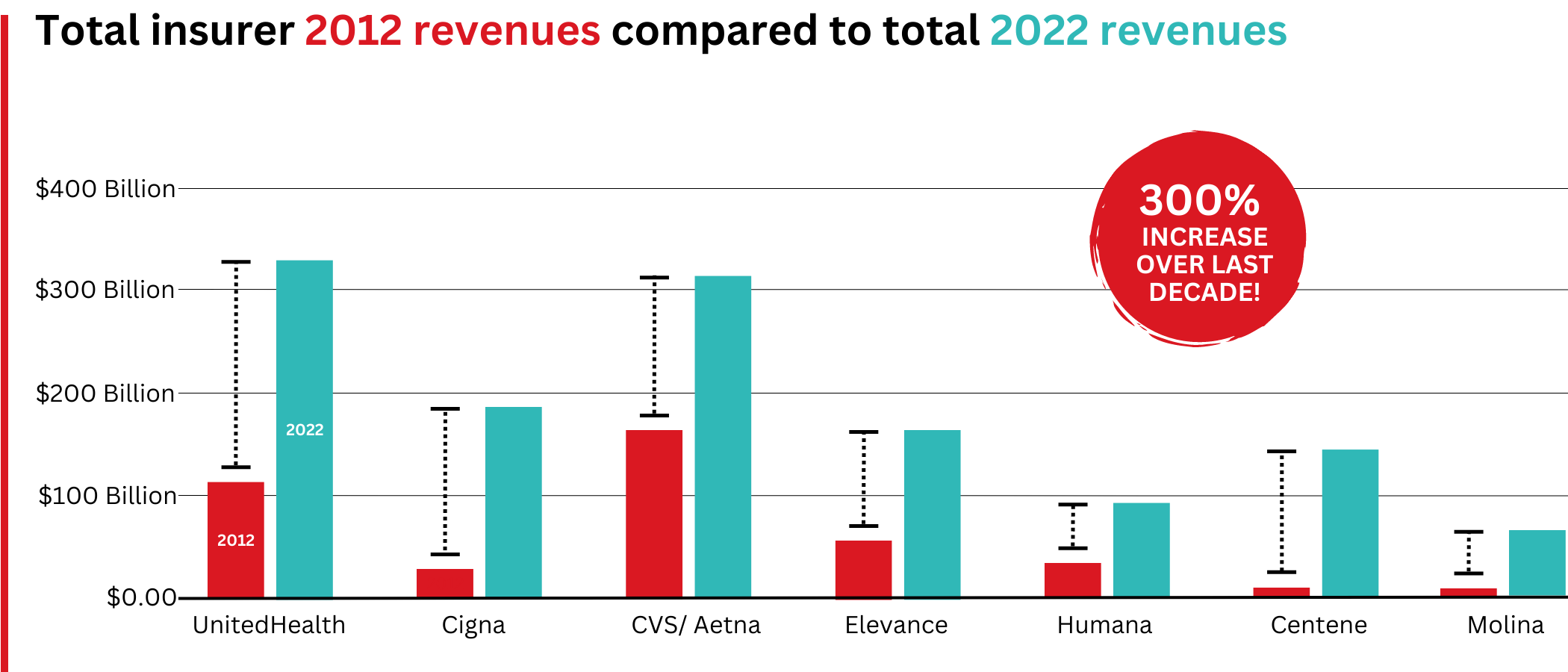

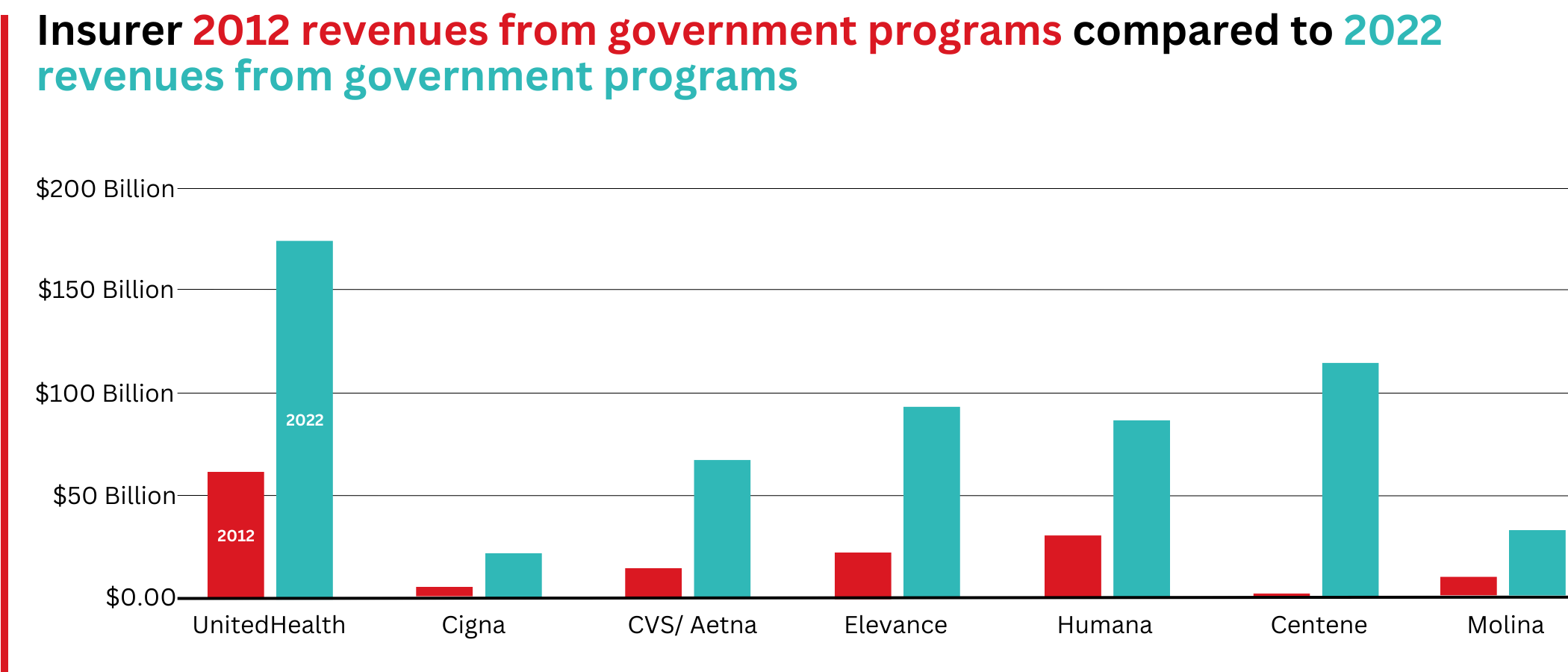

Big Insurance revenues and profits have increased by 300% and 287% respectively since 2012 due to explosive growth in the companies’ pharmacy benefit management (PBM) businesses and the Medicare replacement plans they call Medicare Advantage.

The for-profits now control more than 80% of the national PBM market and more than 70% of the Medicare Advantage market.

In 2022, Big Insurance revenues reached $1.25 trillion and profits soared to $69.3 billion.

That’s a 300% increase in revenue and a 287% increase in profits from 2012, when revenue was $412.9 billion and profits were $24 billion.

Big insurers’ revenues have grown dramatically over the past decade, the result of consolidation in the PBM business and taxpayer-supported Medicare and Medicaid programs.

Sucking billions out of the pharmacy supply chain – and taxpayers’ pockets

What has changed dramatically over the decade is that the big insurers are now getting far more of their revenues from the pharmaceutical supply chain and from taxpayers as they have moved aggressively into government programs. This is especially true of Humana, Centene, and Molina, which now get, respectively, 85%, 88%, and 94% of their health-plan revenues from government programs.

The two biggest drivers are their fast-growing pharmacy benefit managers (PBMs), the relatively new and little-known middleman between patients and pharmaceutical drug manufacturers, and the privately owned and operated Medicare replacement plans they market as Medicare Advantage.

With the exception of Humana, Centene, and Molina, most of the companies that constitute Big Insurance continue to make substantial amounts of money selling policies and services in what they refer to as their commercial businesses – to individuals, families, and employers – but the seven companies’ commercial revenue grew just 260%, or $176 billion, over 10 years (from $110.4 billion to $287.1 billion). While that’s significant, profitable growth in the commercial sector has become a major challenge for big insurers – so much so that Humana just last week announced it is exiting the employer-sponsored health-insurance marketplace entirely.

The percentage of U.S. employers providing some level of health benefits to their workers dropped from 69% to 51% between 1999 and 2022 – including a dramatic 8% decrease last year alone. Growth in this category is largely the result of insurers “stealing market share” from each other or from smaller competitors.

As a consequence of this segment’s relative stagnation, PBMs and government programs have become the new cash cows for Big Insurance.

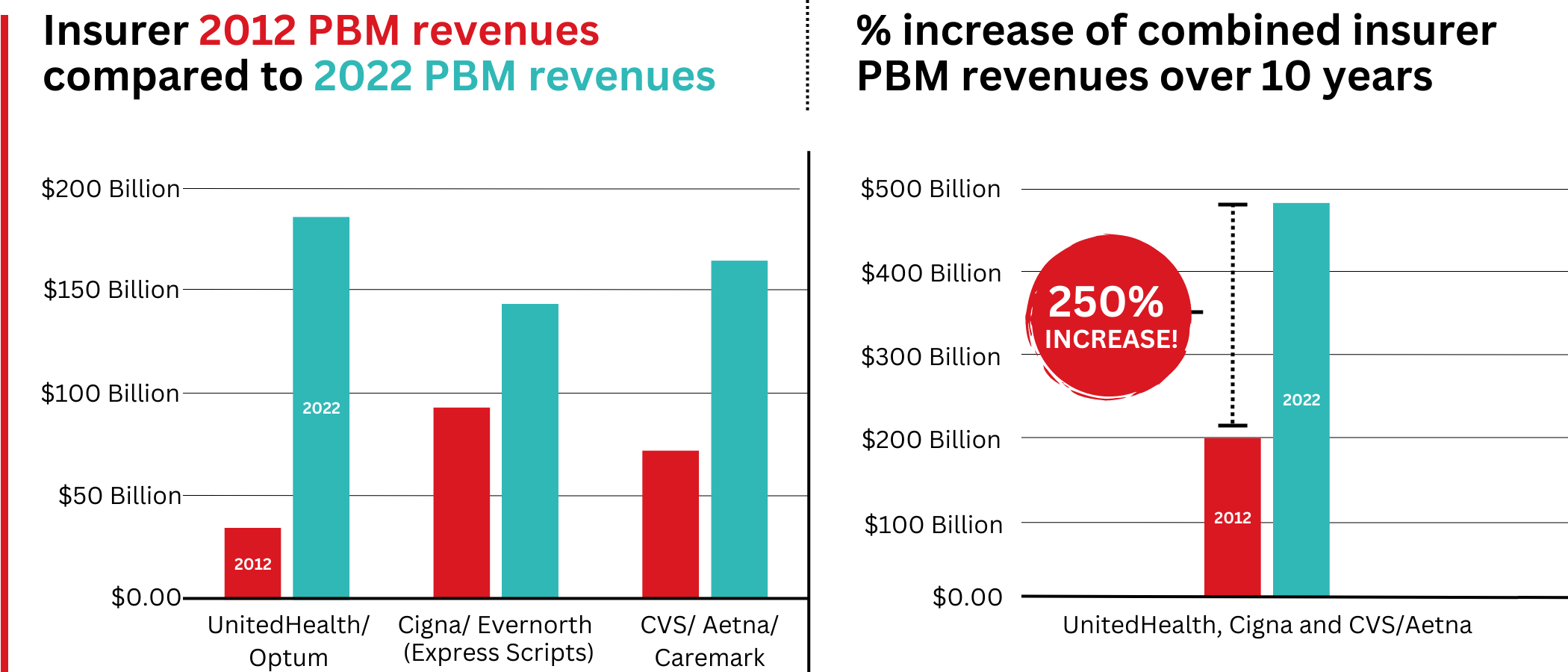

Spectacular PBM Growth

PBM HIGHLIGHTS

Cigna now gets far more revenue from its PBM than from its health plans. CVS gets more revenue from its PBM than from either Aetna’s health plans or its nearly 10,000 retail stores.

UnitedHealth has the biggest share of both the PBM and Medicare markets and, through numerous acquisitions of physician practices, is now the largest U.S. employer of doctors.

PBMs are middlemen companies that manage prescription drug benefits for health insurers, Medicare Part D drug plans, employers, and, in some cases, unions. As the Commonwealth Fund has noted:

PBMs have a significant behind-the-scenes impact in determining total drug costs for insurers, shaping patients’ access to medications, and determining how much pharmacies are paid.

The Commonwealth Fund went on to say that PBMs have faced growing scrutiny about their role in rising prescription drug costs and spending. A big reason for the scrutiny – by Congress, state lawmakers and now also by the FTC – is that the biggest PBMs are now owned by Big Insurance.

Through mergers and acquisitions in recent years, three of the seven for-profit insurers – Cigna, CVS/Aetna, and UnitedHealth – now control 80% of the U.S. pharmacy benefits market.

They determine which drugs will be listed in each of their formularies (lists of drugs they will “cover” based on secret deals they negotiate with pharmaceutical companies) and how much patients will have to pay out of their own pockets at the pharmacy counter – in many cases hundreds or thousands of dollars – before their coverage kicks in. The PBMs also “steer” health-plan enrollees to their preferred or owned pharmacies (and, increasingly, away from independent pharmacists), thereby capturing even more of what we spend on our prescription medications.

Cigna, CVS/Aetna, and UnitedHealth now control 80% of the U.S. PBM market. Correction: this graph was initially published with inaccurate numbers. The source for this information can be found here.

Ten years ago, PBMs contributed relatively little to the three companies’ revenues and profits. But since then, the rapid growth of PBMs has transformed all of the companies. The combined revenues from their PBM business units increased 250% between 2012 and 2022, from $196.7 billion to $492.4 billion.

Changes in PBM revenues between 2012 and 2022 for UnitedHealth Group, Cigna, and CVS/Aetna (Editor’s note: Cigna acquired PBM Express Scripts in 2018. To reflect revenue growth, Express Scripts’ pre-acquisition 2012 revenues are included in the Cigna total for that year.)

PBM Profit Generation

The PBM profit growth at the three companies over the past decade was even more dramatic than revenue growth. Collectively, their PBM profits increased 438%, from $6.3 billion in 2012 to $27.6 billion in 2022.

As a result of this fast growth, more than half (52%) of three companies’ profits in 2022 came from their PBM business units: Cigna’s Evernorth, CVS/Aetna’s Caremark, and UnitedHealth’s Optum. Cigna now gets far more revenue and profits from its PBM than from its health plans. And CVS gets more revenue from its PBM than from either Aetna’s health plans or its nearly 10,000 retail stores. (The companies’ business units that include their PBMs have also moved aggressively in recent years into health-care delivery through acquisitions of physician practices, clinics, dialysis centers, and other facilities. Notably, UnitedHealth Group is now the largest U.S. employer of physicians.)

Huge strides in privatizing both Medicare and Medicaid

GOVERNMENT PROGRAMS HIGHLIGHTS

More than 90% of health-plan revenues at three of the companies come from government programs as they continue to privatize both Medicare and Medicaid, through Medicare Advantage in particular.

Enrollment in government-funded programs increased by 261% in 10 years; by contrast commercial enrollment increased by just 10% over the past decade.

Commercial enrollment actually declinedat both UnitedHealth and Humana.

85% of Humana’s health-plan members are in government-funded programs; at Centene, it is 88%, and at Molina, it is 94%.

The big insurers now manage most states’ Medicaid programs – and make billions of dollars for shareholders doing so – but most of the insurers have found that selling their privately operated Medicare replacement plans is even more financially rewarding for their shareholders.

Revenue growth from government programs has been dramatic over the past 10 years. (Note the numbers do not include revenue from the Medicare Part D program, federal subsidy payments for many ACA marketplace plan enrollees, or Medicare supplement policies.)

This is especially apparent when you see that the Big Seven’s combined revenues from taxpayer-supported programs grew 500%, from $116.3 billion in 2012 to $577 billion in 2022.

These numbers should be of interest to the Biden administration and members of Congress, many of whom are calling for much greater scrutiny of the Medicare Advantage program. Numerous media and government reports have shown that the federal government is overpaying private insurers billions of dollars a year, largely because of loopholes in laws and regulations that enable them to get more taxpayer dollars by claiming their enrollees are sicker than they really are. The companies also make aggressive use of prior authorization, largely unknown in traditional Medicare, to avoid paying for doctor-ordered care and medications.

In addition to their focus on Medicare and Medicaid, the companies also profit from the generous subsidies the government pays insurers to reduce the premiums they charge individuals and families who do not qualify for either Medicare or Medicaid or who work for an employer that does not offer subsidized coverage. But many people enrolled in those types of plans – primarily through the health insurance “marketplaces” established by the Affordable Care Act – cannot afford the deductibles and other out-of-pocket requirements they must pay before their insurers will begin paying their medical claims.

Dramatic Enrollment Shifts

Changes in health-plan enrollment over the past decade show how dramatic this shift has been. Between 2012 and 2022, enrollment in the companies’ private commercial plans increased by 10%, from 85.1 million in 2012 to 93.8 million in 2022.

By comparison, growth in enrollment in taxpayer-supported government programs increased 261%, from 27 million in 2012 to 70.4 million in 2022.

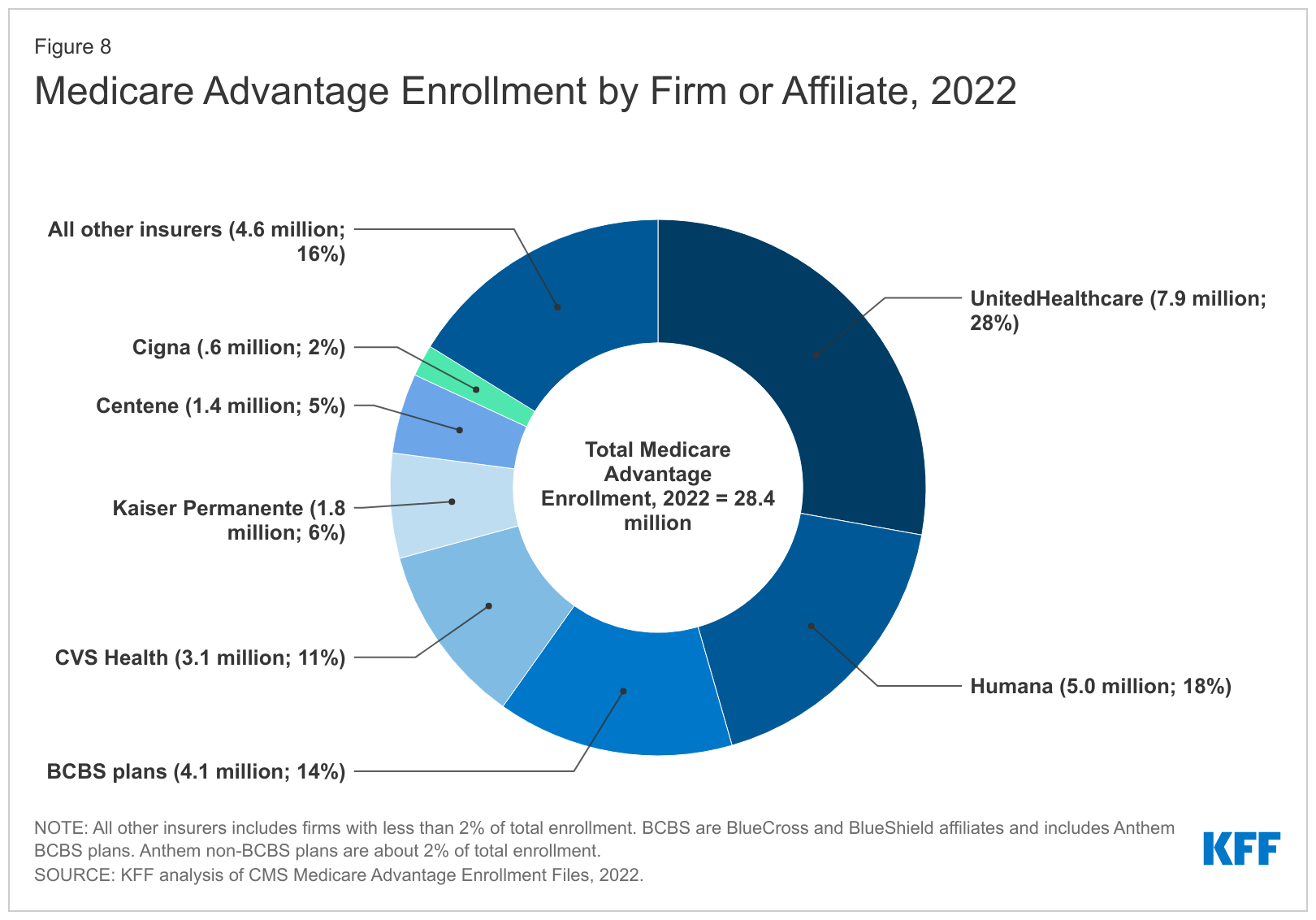

For-profit insurers dominate the Medicare Advantage market. Note that Anthem mentioned above is now known as Elevance. It owns 14 of the country’s Blue Cross Blue Shield plans.

Within that category, Medicare Advantage enrollment among the Big Seven increased 252%, from 7.8 million in 2012 to 19.7 million in 2022.

Nationwide, enrollment in Medicare Advantage plans increased to 28.4 million in 2022 (and to 30 million this year). That means that the Big Seven for-profit companies control more than 70% of the Medicare Advantage market.

UnitedHealth, Humana, Elevance, and CVS/Aetna have captured most of the Medicare Advantage market since the Affordable Care Act was passed in 2010.

The remaining growth in the government segment occurred in the Medicaid programs that a subset of the Big Seven (UnitedHealth, Elevance, Centene, and Molina in particular) manages for several states.

A few other facts and figures to keep in mind as Big Insurance thrives:

100 million of us – almost one of every three people in this country – now have medical debt.

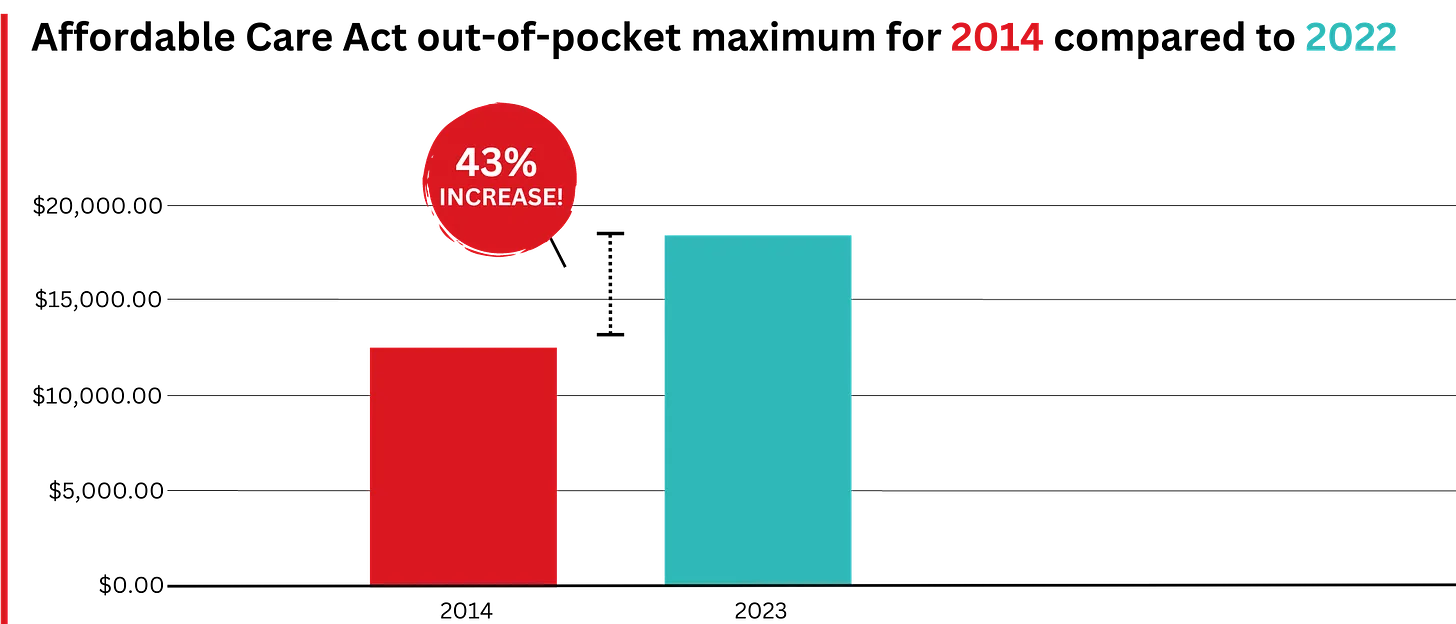

In 2023, U.S. families can be on the hook for up to $18,200 in out-of-pocket requirements before their coverage kicks in, up 43% since 2014 when it was $12,700.The Affordable Care Act allows the out-of-pocket maximum to increase annually – 43% since the maximum limit went into effect in 2014.

44% of people in the United States who purchased coverage through the individual market and (ACA) marketplaces were underinsured or functionally uninsured.

42% said they hadproblems paying medical bills or were paying off medical debt.

Half (49%) said they would be unable to pay an unexpected medical bill within 30 days, including 68% of adults with low income, 69% of Black adults, and 63% of Latino/Hispanic adults.

In 2021, about $650 million, or about one-third of all funds raised by GoFundMe, went to medical campaigns. That’s not surprising when you realize that in the United States, even people with insurance all too often feel they have no choice but to beg for money from strangers to get the care they or a loved one needs.

Even as we spend about $4.5 trillion on health care a year, Americans are now dying younger than people in other wealthy countries. Life expectancy in the United States actually decreased by 2.8 years between 2014 and 2021, erasing all gains since 1996, according to the Centers for Disease Control and Prevention.

BOTTOM LINE:

The companies that comprise Big Insurance are vastly different from what they were just 10 years ago, but policymakers, regulators, employers, and the media have so far shown scant interest in putting their business practices under the microscope.

Changes in federal law, including the Medicare Modernization Act of 2003, which created the lucrative Medicare Advantage market, and the Affordable Care Act of 2010, which gave insurers the green light to increase out-of-pocket requirements annually and restrict access to care in other ways, opened the Treasury and Medicare Trust Fund to Big Insurance. In addition, regulators have allowed almost all of their proposed acquisitions to go forward, which has created the behemoths they are today.

CVS/Health is now the 4th largest company on the Fortune 500 list of American companies. UnitedHealth Group is now No. 5 – and all the others are climbing toward the top 10.

While speculation swirls around key cabinet appointments in the incoming Trump administration, much is being written about how things might change for industries and the companies that compose them. Healthcare is no exception.

Speculation about possible changes originates from media coverage, healthcare trade associations, law firms, consultancies, think tanks and academics. Their views are primarily based on Trump Healthcare 1.0 initiatives (2017-2021), presumed Trump 2.0 leverage in the U.S. Senate, House and conservative Supreme Court and a belief by the Trump-team leaders that their mandate is to lower costs for “everyday Americans” and tighten border security.

Thus, Trump Healthcare 2.0 policy changes will be extensive, leveraging legislation, executive orders, agency administrative actions, court decisions and appropriations processes to reset the U.S. health system.

Context:

The red shift that enabled the 45th President to regain the White House was fueled by discontent and fear: discontent with prices paid by ordinary consumers and fear that illegal immigration was an existential threat. Abortion was an important concern to women but inflation and prices for gas, groceries, housing and healthcare mattered more. Exit polls indicate voter concern about how Trump 2.0 economic policies (tariffs et al) might inflate consumer prices or add up to $7 trillion to the national debt was low. And the fate of the Affordable Care Act was a non-issue: assurance about protection for pre-existing condition coverage neutered attention to other elements of the ACA that will get attention in Trump Healthcare 2.0 (i.e. subsidies, short-term plans, et al).

The Four Pillars of Trump Healthcare 2.0 Policy Changes

The new administration is inclined toward a transactional view of the U.S. health system. It does not envision transformational change; instead, it sees opportunity for the system to perform significantly better. Its policies, leadership appointments and actions will be predicated on these four pillars:

Access to the U.S. healthcare system is a right to be earned. Fundamentally, Trump Healthcare 2.0 builds on its moral conviction that there should be NO FREE LUNCHES whether it’s illegal immigrants or patients who use the health system without doing their part. Trump Healthcare 2.0 will advance mechanisms to enable self-care, increase personal responsibility, promote cheaper/better alternatives to traditional insurance and health delivery and challenge lawmakers to limit financial support to free-loaders. The fundamental notions of public health and community benefit will be revisited and restrictions enacted.

The status quo is not working. Change is needed. Polls show the majority of Americans are dissatisfied with the health system. Affordability is their major concern: escalating, inexplicable costs are forcing their employers to share more responsibility. Trump Healthcare 2.0 will implement changes that lower spending and costs for consumers and employers. They’ll leverage coalitions of working-class voters and businesses to enact policies that expose waste, fraud and abuse in the system and direct the U.S. Department of Health & Human Services to streamline its structure and prioritize cost-effectiveness (the HHS Strategic Plan for 2022-2026 is up for review).

Private solutions solve public problems better than government. Trump Healthcare 2.0 posits that government is broken including the federal and state agencies that control healthcare oversight and funding. Reducing regulatory barriers to consolidation and innovation and lessening risks for private investors whose ventures align with Trump Healthcare 2.0 priorities will be foci. Fundamentally, Trump Healthcare 2.0 believes the private sector is better able to address problems than government bureaucrats: key Trump Healthcare 2.0 leadership positions will be filled by successful private sector operators instead of re-cycled DC luminaries desiring attention.

Price transparency fuels competition and value. Trump Healthcare 1.0 mandated hospital price transparency via its 2019 Executive Order: Trump Healthcare 2.0 will expand the scope and usefulness of price transparency mandates in hospital, ancillary and outpatient services, physician services, insurance and others. It will facilitate accelerated use of Artificial Intelligence in decision-making by consumers, providers and payers. It will expand timely access to data on prices, direct costs, overhead, executive compensation, outcomes, user experiences and other elements of care management provided by hospitals, physicians and other providers. And it will move quickly to implement site neutral payments in the 119th Trump Healthcare 2.0 holds that providers, insurers and drug companies are not inclined to transparency despite strong support from elected officials and voters. They’ll advance these policy changes anticipating pushback from industry insiders. Trump Healthcare 2.0 believes price transparency in healthcare will produce transformational changes that enable more competition and lower costs.

Looking ahead:

The Trump 2.0 team’s immediate task is to assemble its Cabinet: that’s taken prior administrations 38 days on average to complete. In tandem, temporary fixes for CMS’ pending Physician Pay Cut and telehealth expansion will pass as Congress’ lame duck session begins this week.

Looking to 2025, the Trump Healthcare 2.0 team will focus initially on issues in Congress where Bipartisan support appears strong i.e. regulation of PBMs, implementation of site neutral payment policies, expansion of drugs subject to Inflation Reduction Act’s pricing limits and perhaps others. It will plan its legislative agenda coordinating with key committees (i.e. Senate HELP, House Ways and Means et al) and outside groups that share its predisposition. And it will use its political clout to build popular support for healthcare reforms that respond directly to consumer (voter) concern about affordability.

Trump Healthcare 2.0 will bring heightened transparency to the health system and be premised on pillars that are popular with working class voters. It will not be a duplicate of Trump Healthcare 1.0: it will be much more.

Health policy and politics are inextricably linked. Policy is about what the government can do to shift the financing, delivery, and quality of health care, so who controls the government has the power to shape those policies.

Elections, therefore, always have consequences for the direction of health policy – who is the president and in control of the executive branch, which party has the majority in the House and the Senate with the ability to steer legislation, and who has control in state houses. When political power in Washington is divided, legislating on health care often comes to a standstill, though the president still has significant discretion over health policy through administrative actions. And, stalemates at the federal level often spur greater action by states.

Health care issues often, but not always, play a dominant role in political campaigns. Health care is a personal issue, so it often resonates with voters. The affordability of health care, in particular, is typically a top concern for voters, along with other pocketbook issues, And, at 17% of the economy, health care has many industry stakeholders who seek influence through lobbying and campaign contributions. At the same time, individual policy issues are rarely decisive in elections.

Health “reform” – a somewhat squishy term generally understood to mean proposals that significantly transform the financing, coverage, and delivery of health care – has a long history of playing a major role in elections.

Harry Truman campaigned on universal health insurance in 1948, but his plan went nowhere in the face of opposition from the American Medical Association and other groups. While falling short of universal coverage, the creation of Medicare and Medicaid in 1965 under Lyndon Johnson dramatically reduced the number of uninsured people. President Johnson signed the Medicare and Medicaid legislation at the Truman Library in Missouri, with Truman himself looking on.

Later, Bill Clinton campaigned on health reform in 1992, and proposed the sweeping Health Security Act in the first year of his presidency. That plan went down to defeat in Congress amidst opposition from nearly all segments of the health care industry, and the controversy over it has been cited by many as a factor in Democrats losing control of both the House and the Senate in the 1994 midterm elections.

For many years after the defeat of the Clinton health plan, Democrats were hesitant to push major health reforms. Then, in the 2008 campaign, Barack Obama campaigned once again on health reform, and proposed a plan that eventually became the Affordable Care Act (ACA). The ACA ultimately passed Congress in 2010 with only Democratic votes, after many twists and turns in the legislative process. The major provisions of the ACA were not slated to take effect until 2014, and opposition quickly galvanized against the requirement to have insurance or pay a tax penalty (the “individual mandate”) and in response to criticism that the legislation contained so-called “death panels” (which it did not). Republicans took control of the House and gained a substantial number of seats in the Senate during the 2010 midterm elections, fueled partly by opposition to the ACA.

The ACA took full effect in 2014, with millions gaining coverage, but more people viewed the law unfavorably than favorably, and repeal became a rallying cry for Republicans in the 2016 campaign. Following the election of Donald Trump, there was a high profile effort to repeal the law, which was ultimately defeated following a public backlash. The ACA repeal debate was a good example of the trade-offs inherent in all health policies. Republicans sought to reduce federal spending and regulation, but the result would have been fewer people covered and weakened protections for people with pre-existing conditions. KFF polling showed that the ACA repeal effort led to increased public support for the law, which persists today.

The 2024 election presents the unusual occurrence of two candidates – current vice president Kamala Harris and former president Donald Trump – who have already served in the White House and have detailed records for comparison, as explained in this JAMA column. With President Joe Biden dropping out of the campaign, Harris inherits the record of the current administration, but has also begun to lay out an agenda of her own.

While Trump failed as president to repeal the ACA, his administration did make significant changes to it, including repealing the individual mandate penalty, reducing federal funding for consumer assistance (navigators) by 84% and outreach by 90%, and expanding short-term insurance plans that can exclude coverage of preexisting conditions.

In a strange policy twist, the Trump administration ended payments to ACA insurers to compensate them for a requirement to provide reduced cost sharing for low-income patients, with Trump saying it would cause Obamacare to be “dead” and “gone.” But, insurers responded by increasing premiums, which in turn increased federal premium subsidies and federal spending, likely strengthening the ACA.

In the 2024 campaign, Trump has vowed several times to try again to repeal and replace the ACA, though not necessarily using those words, saying instead he would create a plan with “much better health care.”

Although the Trump administration never issued a detailed plan to replace the ACA, Trump’s budget proposals as president included plans to convert the ACA into a block grant to states, cap federal funding for Medicaid, and allow states to relax the ACA’s rules protecting people with preexisting conditions. Those plans, if enacted, would have reduced federal funding for health care by about $1 trillion over a decade.

In contrast, the Biden-Harris administration has reinvigorated the ACA by restoring funding for consumer assistance and outreach and by increasing premium subsidies to make coverage more affordable, resulting in record enrollment in ACA Marketplace plans and historically low uninsured rates. The increased premium subsidies are currently slated to expire at the end of 2025, so the next president will be instrumental in determining whether they get extended. Harris has vowed to extend the subsidies, while Trump has been silent on the issue.

The health care issue most likely to figure prominently in the general election is abortion rights, with sharp contrasts between the presidential candidates and the potential to affect voter turnout. In all the states where voters have been asked to weigh in directly on abortion so far (California, Kansas, Kentucky, Michigan, Montana, Ohio, and Vermont), abortion rights have been upheld.

Trump paved the way for the US Supreme Court to overturn Roe v Wade by appointing judges and justices opposed to abortion rights. Trump recently said, “for 54 years they were trying to get Roe v Wade terminated, and I did it and I’m proud to have done it.” During the current campaign, Trump has said that abortion policy should now be left to the states.

As president, Trump had also cut off family planning funding to Planned Parenthood and other clinics that provide or refer for abortion services, but this policy was reversed by the Biden-Harris administration.

Harris supports codifying into federal the abortion access protections in Roe v Wade.

Addressing the High Price of Prescription Drugs and Health Care Services

Trump has often spotlighted the high price of prescription drugs, criticizing both the pharmaceutical industry and pharmacy benefit managers. Although he kept the issue of drug prices on the political agenda as president, in the end, his administration accomplished little to contain them.

The Trump administration created a demonstration program, capping monthly co-pays for insulin for some Medicare beneficiaries at $35. Late in his presidency, his administration issued a rule to tie Medicare reimbursement of certain physician-administered drugs to the prices paid in other countries, but it was blocked by the courts and never implemented. The Trump administration also issued regulations paving the way for states to import lower-priced drugs from Canada. The Biden-Harris administration has followed through on that idea and recently approved Florida’s plan to buy drugs from Canada, though barriers still remain to making it work in practice.

With Harris casting the tie-breaking vote in the Senate, President Biden signed the Inflation Reduction Act, far-reaching legislation that requires the federal government to negotiate the prices of certain drugs in Medicare, which was previously banned. The law also guarantees a $35 co-pay cap for insulin for all Medicare beneficiaries, and caps out-of-pocket retail drug costs for the first time in Medicare. Harris supports accelerating drug price negotiation to apply to more drugs, as well as extending the $35 cap on insulin copays and the cap on out-of-pocket drug costs to everyone outside of Medicare.

How Trump would approach drug price negotiations if elected is unclear. Trump supported federal negotiation of drug prices during his 2016 campaign, but he did not pursue the idea as president and opposed a Democratic price negotiation plan. During the current campaign, Trump said he “will tell big pharma that we will only pay the best price they offer to foreign nations,” claiming that he was the “only president in modern times who ever took on big pharma.”

Beyond drug prices, the Trump administration issued regulations requiring hospitals and health insurers to be transparent about prices, a policy that is still in place and attracts bipartisan support.

Ultimately, irrespective of the issues that get debated during the campaign, the outcome of the 2024 election – who controls the White House and Congress – will have significant implications for the future direction of health care, as is almost always the case.

However, even with changes in party control of the federal government, only incremental movement to the left or the right is the norm. Sweeping changes in health policy, such as the creation of Medicare and Medicaid or passage of the ACA, are rare in the U.S. political system. Similarly, Medicare for All, which would even more fundamentally transform the financing and coverage of health care, faces long odds, particularly in the current political environment. This is the case even though most of the public favors Medicare for All, though attitudes shift significantly after hearing messages about its potential impacts.

Importantly, it’s politically difficult to take benefits away from people once they have them. That, and the fact that seniors are a strong voting bloc, has been why Social Security and Medicare have been considered political “third rails.” The ACA and Medicaid do not have quite the same sacrosanct status, but they may be close.

Tomorrow night, the Presidential candidates square off in Philadelphia. Per polling from last week by the New York Times-Siena, NBC News-Wall Street Journal, Ipsos-ABC News and CBS News, the two head into the debate neck and neck in what is being called the “chaos election.”

Polls also show the economy, abortion and immigration are the issues of most concern to voters. And large majorities express dissatisfaction with the direction the country is heading and concern about their household finances.

The healthcare system per se is not a major concern to voters this year, but its affordability is. Out-of-pocket costs for prescription drugs, insurance premiums and co-pays and deductibles for hospitals and physician services are considered unreasonable and inexplicably high. They contribute to public anxiety about their financial security alongside housing and food costs. And majorities think the government should do more by imposing price controls and limiting corporate consolidation.

That’s where we are heading into this debate. And here’s what we know for sure about the 90-minute production as it relates to health issues and policies:

Each candidate will rail against healthcare prices, costs, and consolidation taking special aim at price gouging by drug companies and corporate monopolies that limit competition for consumers.

Each will promise protections for abortion services: Trump will defer to states to arbitrate those rights while Harris will assert federal protection is necessary.

Each will opine to the Affordable Care Act’s future: Trump will promise its repeal replacing it “with something better” and Harris will promise its protection and expansion.

Each will promise increased access to behavioral health services as memories of last week’s 26-minute shooting tirade at Apalachee High School fade and the circumstances of Colt Gray’s mental collapse are studied.

And each will promise adequate funding for their health priorities based on the effectiveness of their proposed economic plans for which specifics are unavailable.

That’s it in all likelihood. They’re unlikely to wade into root causes of declining life expectancy in the U.S. or the complicated supply-chain and workforce dynamics of the industry. And the moderators are unlikely to ask probative questions like these to discover the candidate’s forethought on matters of significant long-term gravity…

What are the most important features of health systems in the world that deliver better results at lower costs to their citizens that could be effectively implemented in the U.S. system?

How should the U.S. allocate its spending to improve the overall health and well-being of the entire population?

How should the system be funded?

My take:

I will be watching along with an audience likely to exceed 60 million. Invariably, I will be frustrated by well-rehearsed “gotcha” lines used by each candidate to spark reaction from the other. And I will hope for more attention to healthcare and likely be disappointed.

Misinformation, disinformation and AI derived social media messaging are standard fare in winner-take-all politics.

When used in addressing health issues and policies, they’re effective because the public’s basic level of understanding of the health system is embarrassingly low: studies show 4 in 5 American’s confess to confusion citing the system’s complexity and, regrettably, the inadequacy of efforts to mitigate their ignorance is widely acknowledged.

Thus, terms like affordability, value, quality, not-for-profit healthcare and many others can be used liberally by politicians, trade groups and journalists without fear of challenge since they’re defined differently by every user.

Given the significance of healthcare to the economy (17.6% of the GDP),

the total workforce (18.6 million of the 164 million) and individual consumers and households (41% have outstanding medical debt and all fear financial ruin from surprise medical bills or an expensive health issue), it’s incumbent that health policy for the long-term sustainability of the health system be developed before the system collapses. The impetus for that effort must come from trade groups and policymakers willing to invest in meaningful deliberation.

The dust from this election cycle will settle for healthcare later this year and in early 2025. States are certain to play a bigger role in policymaking: the likely partisan impasse in Congress coupled with uncertainty about federal agency authority due to SCOTUS; Chevron ruling will disable major policy changes and leave much in limbo for the near-term.

Long-term, the system will proceed incrementally. Bigger players will fare OK and others will fail. I remain hopeful thoughtful leaders will address the near and long-term future with equal energy and attention.

Regrettably, the tyranny of the urgent owns the U.S. health system’s attention these days: its long-term destination is out-of-sight, out-of-mind to most. And the complexity of its short-term issues lend to magnification of misinformation, disinformation and public ignorance.

That’s why this debate will frustrate healthcare voters.

PS: Congress returns this week to tackle the October 1 deadline for passing 12 FY2025 appropriations bills thus avoiding a shutdown. It’s election season, so a continuing resolution to fund the government into 2025 will pass at the last minute so politicians can play partisan brinksmanship and enjoy media coverage through September. In the same period, the Fed will announce its much anticipated interest rate cut decision on the heals of growing fear of an economic slowdown. It’s a serious time for healthcare!

The fate of billions of dollars of Affordable Care Act subsidies is riding on the election, which will also determine how much the next Congress will be consumed with relitigating the law.

Why it matters:

Enhanced ACA subsidies expire at the end of 2025 without congressional action. They’ve substantially lowered consumers’ premiums and driven more enrollment in marketplace plans, though at a hefty cost to the government.

Driving the news:

Although the fight over repealing the ACA itself has faded, the partisan battle is shifting to the fate of the enhanced subsidies, passed as part of the American Rescue Plan Act and then extended via the Inflation Reduction Act.

If Republicans win both chambers of Congress and the presidency, they’re strongly expected to let the subsidies expire.

But if Democrats win the presidency or even partial control of Congress, there’s a good chance for a prolonged debate and, possibly, a grand bargain to extend them.

Sen. Bill Cassidy, the top Republican on the HELP Committee, tied the fate of the subsidies to the election results when asked what’s ahead.

“Tell me, do Republicans have everything, do Democrats have everything, or is it divided government?” he told Axios.

By the numbers:

The enhanced subsidies have cut premium costs an average of 44%, or $705 per year, for qualified ACA enrollees, according to a KFF analysis.

“If they expire, the uninsured rate would jump and people would see huge premium increases,” said Larry Levitt, KFF’s executive vice president for health policy.

The CBO finds that extending them would raise the deficit by $335 billion over 10 years and increase the number of people with health coverage by 3.4 million.

Some Republicans are portraying the continuation of subsidies as a sop to health insurers.

“At a time when we are experiencing a record $35 trillion national debt … it is unconscionable that Democrats would continue to push for massive taxpayer-funded handouts to the wealthy and large health insurance companies,” House Budget Chair Jodey Arrington and Ways and Means Chair Jason Smith said in a joint statement responding to the CBO estimate.

What they’re saying:

“I think just not doing the enhanced subsidies, I would take that as a win for 2025,” said Brian Blase, a former Trump administration health adviser now president of Paragon Health Institute.

He pointed to the cost, also arguing that enhanced subsidies incentivize fraud, with ineligible people enrolling in zero-premium plans. “They’re associated with an unprecedented level of fraud,” he said.

“It’s entirely possible that some people are fraudulently misestimating their income,” Levitt said. But, he noted, many low-income people simply lead “volatile lives” and don’t always know what their income will be in a coming year.

What’s next:

Senate Finance Chair Ron Wyden told Axios he wants to combine an extension of the enhanced subsidies with a bill he’s sponsored that would crack down on unscrupulous insurance brokers, to help counter GOP arguments about fraud.

“I think it would be a real good package to crack down on these insurance scams and these brokers ripping off the ACA and focus on something that actually helps people, which is the premium [tax credits],” Wyden said.

The expiration of some of the 2017 Trump tax cuts next year also could provide an opening for a deal with Republicans to extend the ACA subsidies in divided government.

The bottom line:

Levitt said that although some of the repeal fervor has faded, “the future of the program, the future success of the program, very much depends on these enhanced subsidies.”

Cigna, my former employer, disclosed this morning that during the first seven months of this year, it spent $5 billion of the money it took from its health plan and pharmacy benefit customers to buy back shares of its own stock, a gimmick that rewards shareholders at the expense of those customers.

Cigna also disclosed that its revenues increased a stunning 25% – to $60.5 billion – during the second quarter of this year compared to the same period in 2023. Profits also grew, from $1.8 billion to $1.9 billion.

One of the ways Cigna made so much money was by purging health plan enrollees it decided were not profitable enough to meet Wall Street’s profit expectations.

Enrollment in its U.S. health plans fell by nearly half a million people – from 17.9 million to 17.4 million – over the past year. The company signaled to investors that it was more than OK with that decline, noting that it ran off those customers through “targeted pricing actions in certain geographies.” What that means is that Cigna increased premiums so much for those folks that they either found other insurers or joined the ranks of the uninsured.

It was an entirely different story in Cigna’s pharmacy benefit (PBM) business, which saw a 24% increase in total pharmacy customers. The vast majority of Cigna’s revenues now come from its role as one of the country’s largest middlemen in the pharmacy supply chain. Revenue from Cigna’s pharmacy operations totaled nearly $50 billion in the second quarter of this year, up from $38.2 billion last year. By contrast, revenue from its health plan business increased modestly, from $12.7 billion to $13.1 billion.

But by purging 478,000 men, women and children from its rolls, Cigna reported a profit margin of 9.2% for its health plan operations. That, folks, is exceedingly high in the health insurance business.

One way Cigna and the other industry giants can reward their shareholders so handsomely is by making their health plan and pharmacy customers pay more and more out of their own pockets before the insurers pay a dime.

The Affordable Care Act made it illegal for insurers to refuse to sell coverage to people with preexisting conditions or to set premiums based on someone’s health status.

But that law kept open a big back door that enables insurers like Cigna to make people with health problems pay huge sums of money for their care through deductibles and copayments. As a consequence, millions of Americans are walking away from the pharmacy counter without their medications, and many others who simply cannot live without their meds often wind up buried under a mountain of medical debt.

A growing number of bills have been or soon will be introduced by members of Congress to fulfill Biden’s pledge, but you can expect Cigna and other big insurers to insist that doing so will mean premiums will have to go up.

That’s bullshit.

It might mean that Cigna and the other giants might have to curtail their stock buyback programs and accept slimmer profit margins, but it does not mean premiums will have to go up.

Wall Street will howl if one of the tools insurers use to gouge their customers is taken away – just as investors are punishing Cigna today for the sin of not predicting even higher profits for the rest of the year –

but reducing out-of-pocket requirements would put a significant dent in the enormous and ongoing transfer of wealth by middlemen like Cigna from middle-class Americans, especially those struggling with health issues, to fat cat investors and corporate executives.

Growing demand for GLP-1 drugs like Ozempic and Wegovy and hospital consolidation could help drive up the cost of Affordable Care Act coverage next year by 9% or more, according to a preliminary review by the Peterson Center on Healthcare and KFF.

Why it matters:

While most enrollees in the market get subsidies and won’t have to foot the added bill, premium increases generally result in higher federal spending on subsidies, the analysis notes.

So, too, is the explosion in demand for drugsused for diabetes treatment and weight loss.

Though few ACA plans cover drugs that are approved only for weight loss, several insurers singled out GLP-1s as a driving force behind premium increases for 2025.

The analysis notes insurers are using strategies like prior authorization, step therapy and limiting quantities to control demand of Ozempic and other GLP-1s that are approved for diabetes but have potential for off-label use to lose weight.

Specialty drugs and biologics, including pricey gene therapies, are also becoming more prevalent and driving premiums upward.

Most insurers say ongoing state Medicaid redeterminations, COVID-19 treatment and tests and the federal surprise billing ban are not having a major effect on 2025 premiums.

Context:

Last year, insurers proposed rate increases for 2024 coverage that were between 2% and 10%, with a median increase of 6%, Peterson-KFF notes.

This year’s detailed review of factors driving premium changes for 2025 found insurers have somewhat higher proposed rate increases, with a median of 9%.

The basis for the federal subsidies is the percent change in the benchmark ACA silver plan.

The bottom line:

Medical inflation has picked up and now exceeds the growth of non-medical prices — a big change from 2021 to 2023. ACA plans are adjusting to keep pace and reflect their higher costs and overhead.